Requirements Elicitation for a Holistic Mobile Wallet Ecosystem

João Casal, David Monteiro, Laís Sousa, Patrick Santos, João Santos and Jorge Ramos

TIMWE Lab, Covilhã, Portugal

Keywords: Requirements Elicitation, Mobile Wallet Architecture, Mobile Payments, Mobile Identification, Mobile

Ticketing, Mobile Marketing.

Abstract: The digitization of physical wallets into mobile applications is a promising trend, namely for payments,

personal identification, and for grouping marketing items or digital tickets. Mobile digital services emerge on

these areas promising to bring ease and convenience for wallet owners and, for place owners, lower costs on

payment processing fees, increased service efficiency and a closer relation with customers. However, there

are several challenges, like the users’ acceptance, security concerns and lack of interoperability between

wallet services, that delay a significant impact on persons’ lives. On this paper, we present the requirements

elicitation for a holistic mobile wallet ecosystem.

1 INTRODUCTION

Mobile devices are reaching a massive level of impact

on societies. Their growing capabilities of data

acquisition, communication and processing makes

them ideal instruments to foster paradigmatic changes

on people routines. This is the case of the digitization

of physical wallets into mobile applications, which is

a promising trend for payments, identification,

ticketing and marketing (Forrester Research, 2015).

Mobile digital services grow in these areas promising

improved usability, convenience, security, control

over items and novel disruptive experiences to wallet

owners. To place owners, these services have the

potential to offer lower costs on payments processing,

control over targeted marketing campaigns, improved

proximity to costumers and knowledge about their

interests and needs (Forrester Research, 2015,

TechNavio, 2015, M. Evans, 2015).

However, there are several challenges associated

with these systems. Research shows that “digital

mobile wallets do not fulfil consumer’s needs”

(Williams and Yu, 2015). Only 13% of the people

who own smartphones have mobile wallets installed,

and 76% of these rarely or never use it due to safety

concerns, unclear convenience and poor functional

characteristics (Williams and Yu, 2015). Other

studies identify issues on the: (i) User Experience

(lack of acceptability, usability, trust, privacy,

perceived value for wallet owners, place owners and

others); (ii) coexistence of mobile payments with

other services; (iii) coexistence of multiple mobile

wallets in one device; (iv) connection between wallets

of consumers and merchants; (v) interoperability

between mobile wallets; (vi) proximity payments;

information security; (vii) lack of collaboration

between the stakeholders (European Payments

Council, 2014, Shaw, 2014, Gannamaneni, Ondrus

and Lyytinen, 2015).

For this purpose, on weWallet project we aim to

face the mentioned challenges by researching and

developing a universal solution that dematerializes

the main items present on nowadays physical wallets,

namely the currency, personal identification, tickets

and marketing items (like coupons or discounts), all

integrated into one mobile solution available for the

main mobile operating systems (OS). Our approach is

based on three axels: (i) the fragmentation reduction

of mobile wallet services, currently separated in

several independent mobile applications. We propose

one single digital mobile wallet for converting every

physical wallet experience as a way of reducing

interoperability issues, improving the User Experience

for wallet owners and optimizing/increasing the

services provided to place owners; (ii) the abstraction

regarding mobile OS to optimize the number of

potential users and, therefore, increase the adoption

from place owners; (iii) the abstraction regarding

communication technologies between wallet owners

and place owners in order to reduce their investment

in hardware infrastructures and to increase its

acceptance across the smartphone owners, regardless

Casal, J., Monteiro, D., Sousa, L., Santos, P., Santos, J. and Ramos, J.

Requirements Elicitation for a Holistic Mobile Wallet Ecosystem.

DOI: 10.5220/0006390600630070

In Proceedings of the 14th International Joint Conference on e-Business and Telecommunications (ICETE 2017) - Volume 2: ICE-B, pages 63-70

ISBN: 978-989-758-257-8

Copyright © 2017 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

63

of their devices communication technologies (NFC,

QR Code, Wi-Fi, BLE).

On this paper, which is part an on-going industrial

R&D project, we present a study that combined

applied research with user-centered techniques for the

elicitation of the requirements for the envisioned

system. These are consolidated on a functional

architecture that illustrates an overview of the

solution.

2 RELATED WORK

This section surveys the most relevant related work

about mobile wallets and the solutions available on

the market, from their functionalities and

communication technologies used, to the identified

limitations.

On (Ma and Wei, 2014) is proposed a mobile

payments system using the NFC technology. Users

can charge the mobile service balance through their

their bank account, and then use it on a NFC-enabled

Point of Sale (POS). The transaction is forwarded to

a banking management system for validation and

money transfer. The planned system used identity

authentication, information encryption, data integrity

verification and digital signature as security

measures. Beside the conceptual prototype, the

solution was just developed for Android OS and

presented a limited number of functionalities.

Rehman and Coughlan presented another NFC-

enabled mobile payments system for Android

devices, where consumers and merchants need to be

registered on the same Financial Service (Rehman

and Coughlan, 2013). Using a different communica-

tion protocol, on (Ugwu and Mesigo, 2015) is

proposed an Android application that uses QR codes

as links to process transactions. This work identifies

the two main actors as receiver and the payer. The

receiver launches the mobile application, selects the

amount to receive, and a QR code for the transaction

is generated. The payer application scans the QR code

on the receiver’s smartphone, selects the payment

method, authenticates on the system and on the

financial institution, and the transaction is processed.

PayPal and credit card accounts can be used to make

the payments. This system is just for Android devices,

communicates just by QR codes and both the actors

have to be online for performing the transaction.

The dematerialization of identification cards into

mobile applications is also a current research trend. In

(Zhang et al., 2015) is proposed an identity

recognition framework based on NFC and fingerprint

technology for Android devices that can be used in

many different areas. In (Portnoi and Shen, 2015) is

presented an authentication system based on BLE

beacons. The system is conceptualized to work on

indoor locations, with beacons broadcasting

encrypted messages (Ciphertext-Policy Attribute-

Based Encryption) containing a session token. Users

with BLE devices are able to capture the encrypted

messages and, if their devices are capable to decrypt

these messages, then the users would be authenticated

in the system, at that exact location.

Other elements that are frequently present in

physical wallets are tickets and loyalty cards, and

there are also studies on mobile solutions for

digitizing them. In (Zupanovic, 2015) is described a

NFC ferry ticketing system implemented in Croatia

that enables users to acquire the tickets at home and

present them on a digital format through their

smartphones. This procedure aimed to speed up the

ferry boarding.

Besides the studies presented, there are

considerable solutions already on the market. The

Apple Pay (Apple Inc., 2014) allows consumers to

store credit/debit cards information, loyalty cards and

coupons on their smartphones, enabling online and

in-store purchases. The in-store purchase

communications are made through NFC, which is

only allowed on iPhone since the iPhone 6 model. It

supports payments using American Express,

MasterCard and Visa, and uses the Secure Element on

the smartphone to store personal encrypted

transactional data. The Android Pay (Google, 2015)

is a mobile wallet system for Android devices

developed by Google that dematerializes credit, debit

and loyalty cards. It allows payments by MasterCard,

Visa or American Express. The in-store payments can

be made using NFC technology. Differently from

Apple Pay, the Android Pay uses the Host-based Card

Emulation (HCE), which allows the emulation of

users’ cards on the smartphone, avoiding private

information from these cards to be directly stored on

the smartphone. By using this mechanism, a token,

that corresponds to the virtual information of the card,

is used to initiate the transaction, being this

information forwarded to the cloud, where the real

card information is retrieved to finish the purchase.

The Samsung Pay (Samsung, 2015) has been

developed for Samsung devices (Android) and allows

consumers to make payments through NFC or

Magnetic Secure Transmission (MST) technologies

(allows payments to be made using older POS). On

both cases, payments have to be authorized through

fingerprinting or PIN codes. The whole payment

system is based on a tokenization mechanism, which

allows private card information to be replaced by a

ICE-B 2017 - 14th International Conference on e-Business

64

token during the whole payment process between the

consumer and the merchant.

These wallets are mainly focused on mobile

payments and on the loyalty cards usage. However,

there are other applications in the market that can be

used for identification or ticketing purposes. The

MEO CardMobili (MEO, 2014) allows the

management of MEO services, and aggregates

identity, loyalty, and discount cards. To add those

cards, the user has to introduce the card number

manually and scan its bar code if it has one. To use

the cards, users have to show them on their

smartphones to the merchants, without any

automatized process. The m.Ticket application (NOS,

2015) is intended to allow people to buy cinema

movie tickets for the NOS theatres, with the tickets

being forwarded to the users through SMS. To

validate their entrance in the theatre, the users have to

pass their smartphones with the received SMS and

validity code on a terminal on the entrance of the

theatre room.

By analysing the state of the art, it is noticeable

that no mobile solution provides a holistic wallet

experience (with payments, identification, ticketing,

marketing items) for the main mobile OS, with more

than one communication protocol.

3 RESEARCH METHODOLOGY

For the purpose of this project we are using an action

research methodology, iterative and user-centered.

We are planning three iterations of the methodology,

related with three releases of prototypes iteratively

improved accordingly to research. The first iteration

starts with the combination of an applied research

with user-centered techniques, having as results the

requirements of the system (presented on this paper)

and a first functional prototype of weWallet. The

second iteration starts with a user-centered evaluation

of the former prototype, which will feed the applied

research to be done accordingly to its results. The aim

is to use users and stakeholders to confirm and adapt

the preliminary requirements gathered, now using a

hands-on prototype. The result of the applied research

of this iteration is a second prototype, more adapted

to the user’s perspective and to the project objectives.

The final iteration starts once more with the

evaluation of the preceding prototype, now in a real-

world setup. The goal is to use the results of this

evaluation to perform a final applied research, which

will end with a pilot of the system ready for running

on a real setting for a significant period of time.

Articulated with the user-centered approach, all the

iterations have the objective of measuring and

increasing the security, performance, scalability and

abstraction of the system (which is intended to be

applied in businesses of several types and

dimensions, and inherently with unique needs).

This paper shows the main results of the first

iteration of the research methodology, compiled on a

functional architecture that provides an overview of

the requirements and will guide the forthcoming

efforts. In this sense, for the applied research we have

performed a profound state of the art research on (i)

digitization flows of physical wallets for payments,

identification, ticketing and items of costumer

engagement/marketing; (ii) devices and technologies

for communication between mobile wallet owners

and place owners; (iii) current mobile wallets features

and interaction mechanisms; (iv) current solutions for

place owners’ in the management of mobile wallets;

(v) Cloud infrastructures and backend mechanisms

for supporting mobile wallet ecosystems (including

architecture, security, processing performance and

information systems’ needs). The applied research

included hands-on testing with current solutions and

technologies, as well as the testing of preliminary

technical possibilities.

In what concerns the techniques applied on the

user-centered research, is has been performed a

focusgroup and a questionnaire with potential mobile

wallet owners, and a set of 6 individual interviews

with potential place owners. The focusgroup and the

questionnaire were made in one session with 15

participants with distinct levels of experience

regarding mobile applications and mobile wallets

from different professional and demographic

characteristics, 10 males, and 5 females, aged from 25

to 50 years old guarantying a closer analysis to

different types of users that might interact with the

wallet in a real-world scenario. The session consisted

on three main phases: (i) the presentation of the

project and an introduction of the main mobile wallets

currently on the market, combined with an open

discussion regarding the good aspects of these

systems and of their limitations; (ii) a focusgroup

oriented for gathering scenarios of use of a holistic

mobile wallet in the context of payments,

identification, ticketing and marketing; and (iii) the

questionnaire, filled at the end of the session. The

questionnaire comprised 17 multiple-choice

questions with an open alternative, and had the goal

of gathering the individual perspective of the

potential mobile wallet owners. The focusgroup has

been recorded (video and audio) and its results

transcribed, categorized and measured for allowing

its analysis.

Requirements Elicitation for a Holistic Mobile Wallet Ecosystem

65

The interviews with place owners were held

individually, in order to consider their different

professional areas. Each session had the duration of

30 minutes, where issues related with payments,

ticketing and identification through mobile devices

were discussed. The first set of interviews was

performed with 4 place owners: (i) a responsible from

a tourism office that provides information about the

city and sells tickets for transports and public

attractions; (ii) a restaurant owner; (iii) a place owner

that manages multiple service provisioning; (iv) a bar

owner. After this first set, another stakeholder

approached our company, volunteering to provide

context and real world scenarios for the project. This

stakeholder owns a renown Portuguese winter sports

resort, and feels considerable efficiency problems on

payments, identification, ticketing and marketing that

fit the scope and goals of the weWallet project. In this

sense, were performed 2 more interviews: one with

the resort owner, focusing business goals and vision

regarding the use of mobile wallets at his place and

the second with the administrator of the resort, where

he showed operational needs, problems and

restrictions. The 6 interviews allowed to understand

the place owner’s perspective, assuring abstraction

regarding business areas and dimensions.

On the next section, we show the key findings,

which are summarized by the functional architecture

of the system.

4 RESULTS

As introduction to this section, which will have the

form of explanation of the requirements for a

holistic mobile wallet per area (payments,

identification, ticketing and marketing), our user-

centered studies confirmed that despite the

recognized advantages of mobile wallets, the current

solutions do not fulfil the users’ needs. All the

participants (Wallet Owners and Place Owners) see

advantages on these systems, but only one Wallet

Owner (6,7%) mentioned to have a mobile wallet

application installed on his smartphone, which just

works for one restaurant brand, for gathering points

to get discounts in future meals. The remaining

participants (93.3%) mentioned that they didn’t

have a mobile wallet installed because they never

needed it. Place Owners demonstrated that the

friction on the adoption of these kind of services

comes from the low adaptation on the current

solutions to their needs, the small number of users

of this kind of systems and the current safety

concerns users have. These findings confirmed the

challenges in hands. On the next subsections, we

will describe the requirements gathered, which are

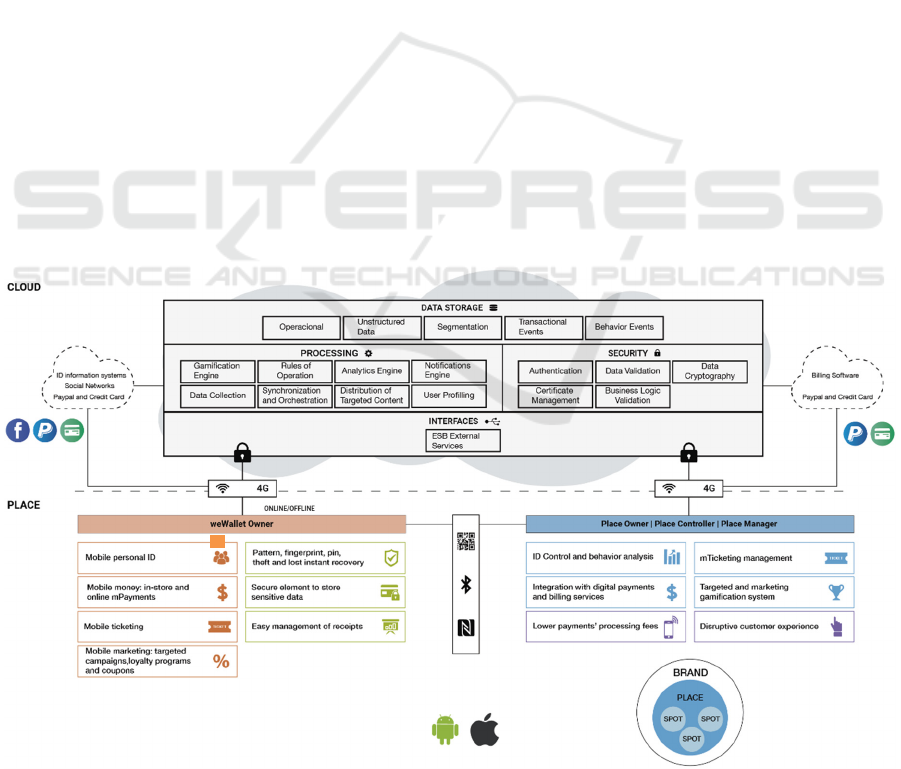

summarized and depicted on Figure 1.

4.1 Personas and Key System Concepts

Our studies revealed that to assure the abstraction

and the scalability of the mobile wallet ecosystem in

different areas of application (restaurants, resorts,

stores, public transports, corporate facilities,

summer festivals and others) and for different

business sizes, it has to consider the following

personas: (i) Wallet Owner: the persona that has the

mobile wallet application installed on the

smartphone, and is able to use it for payments and

management of receipts, personal identification,

buying and managing tickets of several types,

receiving and managing items of customer

engagement, such as loyalty programs or coupons.

The demography of this persona is very broad,

basically anyone with a smartphone; (ii) Place

Owner: the persona responsible for the business with

which the mobile wallet owner interacts, being

interested on the system business metrics (data

visualization, business performance notifications

and other management features), on managing the

system modules and on managing the employees’

performance and permissions on the system. This

persona has permissions to do everything that the

Place Manager and Place Controller do. The

businesses scope (places that a Place Owner may

own) is defined by any place that involves

payments/money transfer, user’s identification,

ticketing or marketing; (iii) Place Manager: the

operator responsible for interacting with the wallet

owner in payments, identification, ticketing and

marketing; (iv) Place Controller: the operator that

confirms/validates wallet owner’s ID or the

permission for those personas to be on a specific

spot.

As key concepts for ensuring the encompassing

of different types and dimensions of businesses, we

found that the system needs to be prepared to have

representation of: (i) Brands: group of places from

the same company (ex: set of restaurants or hotels

from a group; set of facilities from a company or

public corporation, or other); (ii) Places: a specific

place, like a store, office, restaurant, cinema, mall,

football stadium, or other; (iii) Spots: a specific spot

on a place, for example a specific corridor, the

entrance, the spot nearby a specific Nike shoes.

On the next subsections, we present the system’s

requirement findings organized per functional area.

ICE-B 2017 - 14th International Conference on e-Business

66

4.2 Mobile ID

On Figure 1 is possible to see that a Wallet Owner

will have the possibility of presenting a mobile ID,

feature valued by 93.3% users, to be used in

scenarios of corporate ID, insurance ID, or others

like gym ID, or library ID. The mobile wallet ID will

be composed by a fixed and a variable component.

The fixed part will be similar to the citizen card and

have personal info like the name, fiscal number,

email, photo, address, phone number and birth date.

This information will be extended with data related

with the users’ relation with each Brand, like the ID

of the person on that Brand.

The Wallet Owner will be able to present the

mobile ID in two forms: active or passive. For the

active presentation of ID, the Wallet Owner selects

that option, inserts the security PIN or fingerprint,

and the system generates and presents a QR Code

and activates the NFC for transmitting his ID from

his mobile wallet to the Place Manager application

(which may be just a reader that activates the

opening of a physical barrier on clearance, p.e. a

door). When no digital communication of

information is required, the Wallet Owner can

present his ID on the smartphone screen in a format

like regular cards (which we call weWallet ID card).

When the Wallet Owner leaves the ID screen or the

smartphone enters in standby mode, the ID stops

being transmitted. The personal mobile ID info is

securely stored on the persons’ devices to allow

offline presentation of ID, and at the Cloud, to allow

the recovery of a lost/stolen wallet (feature valued

by 73.3% of the potential Wallet Owners). The

passive presentation of ID is when the user

authorizes his mobile wallet to send automatically

his ID after receiving specific BLE signals. Using

BLE beacons broadcasting a signal on specific

spots, the mobile wallet will send the users’ ID to

the Cloud infrastructure. This data that may be used

for marketing matters, for corporate ID and others.

Place Managers and Place Controllers, will be

able to read wallet owners’ ID on their mobile

devices, using an NFC tap or reading the QR Code.

Both users will need to check-in on a specific spot

when logging in, in order to record the location of

the action performed. Place Managers will also be

able to do access management, namely granting

access to specific places to Wallet Owners.

Place Owners will be able to see, on a web

application, dashboards characterizing the Wallet

Owner’s patterns of behaviour, namely entrances,

exits, passing on a specific spot, and others, per

wallet owner or segment of wallet owners. This

actor will also be able to manage the places and

spots, meaning, creating and managing new

places/spots by identifying the related location and

sensors.

Figure 1: weWallet Functional Architecture.

Requirements Elicitation for a Holistic Mobile Wallet Ecosystem

67

4.3 Mobile Payments

Mobile payments are the most common features of

current mobile wallets. On our studies, 73.3% of the

potential Wallet Owners recognize advantages on

mobile payments of low value (<20€), and 60% on

higher values, mainly related to the convenience.

However, the majority still finds issues related to the

security and to the lack of vendors that allow

payments through mobile wallets, which harms the

added value of current solutions.

Our approach will differ from the current systems

by the possibility of payments using several channels

of communication between wallet owner and place

owner, by the seamless integration of all the elements

on the wallet, by the abstraction regarding the mobile

OS, and by the possibility for the Wallet Owner to

perform payments being offline.

In general terms, we have found that the flow of

dematerialization of payments in mobile wallets has

3 main stages: (i) The charge of the wallet balance;

(ii) The payment/money transfer from the Wallet

Owner to a Brand; (iii) The transfer of the weWallet

balance of the Place Owner to his bank account.

For the first stage, on our study, 85,7% of the

potential mobile wallet owners assumed that the

integration of the mobile wallet with PayPal would be

the best solution for charging the balance (as well as

for redeem it). As reasons for this choice, the

participants mentioned that PayPal is a well-accepted

and secure system that users already know and trust.

An alternative suggested by 46,67% of the

participants is to aggregate a credit card to the mobile

wallet account, solution mentioned to be interesting,

especially after the weWallet system gains the trust of

the users. In this sense, as can be seen on Figure 1, the

system will integrate PayPal as a solution to the safety

concerns that exists on other wallets (as mentioned

above users already trust this platform) and credit

card services for the charging of the mobile wallet. It

is also shown that the wallet owner solution connects

directly with these systems, which happens to assure

the security of the solution (we will not store any

confidential bank information from the wallet owners

on our systems). The personal bank information will

be stored locally using the Secure Element of the

mobile device. At our Cloud infrastructure, we only

store information about the balance and money

transfers, for allowing offline payments and for the

locking of balance when needed.

The balance transfer (payment) between a Wallet

Owner and a Place Owner (or its Brand) can be done

using NFC or QR Code, or directly (online) when

purchasing a mobile ticket. On in-store payments,

articulated with the billing system (with which we

integrate case by case), the Place Owner application

generates a QR Code and an NFC signal for the wallet

owner to read accordingly to the communication

protocol available on his device, and transfer the

related balance. This operation has to be authorized

using the mobile device security pattern, fingerprint

or PIN. After the balance transfer, the place owner is

notified and launches the related receipt, which is

stored in the Wallet Owner account (at the Cloud) and

is possible to be retrieved by this persona anytime

anywhere.

The Place Owner has available one dashboard

showing the patterns of income using mobile wallets

per place or spots and per product or service

(including mobile tickets). This persona has also the

possibility of transferring the money from the system,

which can be made by the transfer of the balance to

his PayPal account (and then to his bank account).

4.4 Mobile Ticketing

On the questionnaire filled by potential wallet

owners, 93.3% mentioned the management of tickets

on mobile wallets to be a valuable feature.

From the analysis of the interviews with Place

Owners we identified three types of mobile tickets: (i)

Entrance (with time constrains and possible multiple

uses): tickets for entering on shows, summer festivals,

cinemas, football stadiums, thematic parks or others.

These tickets validity can be associated with a time

frame or with the first presentation of the ticket. (ii)

Exchange for product or service (without time

constrains but with a validity date): tickets that can be

exchanged by a meal or a drink (p.e. in events that do

not want to have money circulation), or by services,

like a car wash, a training class or a night at a hotel.

(iii) Renting equipment (with time constrains and

possible weWallet balance lock): this type of tickets

allows the Wallet Owner to rent an equipment made

available by a Place Owner. Examples of equipment

to be rented are bikes in city centers or ski material in

winter resorts. The rent of an equipment may obligate

to a value lock on weWallet balance to assure the

return in good conditions.

From the scenarios obtained on the studies, the

Place Owners should be able to manage the ticketing

system, creating and submitting tickets (including the

number available), see the list of tickets of type (iii)

pending (with equipment not returned in the due

period) and act regarding that (p.e. notify wallet

owner). This user is also able to see a dashboard that

shows the patterns of the selling and of the use of the

ICE-B 2017 - 14th International Conference on e-Business

68

tickets with historic data and forecasts based on prior

data.

The Wallet Owner is able to see the list of tickets

available, apply filters accordingly to preferences,

buy tickets with weWallet balance, and present the

tickets using QR Code or NFC to a Place Manager or

a Place Controller (online or offline). In the case of

the need of a balance lock (rental of equipment), the

Wallet Owner is notified at the moment of purchase

and of the use of the ticket, and the acceptance of that

lock is asked and confirmed by the submission of the

security PIN or fingerprint.

The Place Manager validates the tickets of types

(ii) and (iii) and registers its use. This user also

registers the return of the equipment (ticket of type

(iii)) and the system unlocks the Wallet Owner

balance regarding the delivery of the equipment.

Regarding the Mobile Ticketing group of features, the

Place Controller is responsible for the validation of

tickets of type (i), entrance in events or transports.

4.5 Mobile Marketing and

Gamification

The ubiquity of mobile technologies on people lives

gives place owners the opportunity to get closer to

their target customers.

Our findings show that place owners are aware

and value considerably mobile marketing and

gamification features to promote costumers’

engagement in a mobile wallet context. All referred

that they would use frequently the weWallet system

to perform targeted marketing (campaigns directed to

segments of consumers) and that they would try to

change their current costumer engagement system, of

loyalty cards or discount coupons to equivalent

mobile wallet items.

In this sense, for what concerns an integrated

Mobile Marketing and Gamification system, Place

Owners shall be able to: (i) Manage targeted mobile

marketing campaigns, for specific in-situ delivery of

content (using the spots’ sensors) or for delivery

anywhere accordingly to rules established; (ii) Define

the Gamification system: as type of gamification

system we make available loyalty cards, ranks and

coupons, for which the Place Owners can define the

rules of application. These rules consist on

mechanisms that will be automatically applied

integrated with the remaining system (identification,

payments or ticketing) accordingly to the Wallet

Owners’ actions on the interaction with the Brand,

Place or Spot. (iii) Analyse the efficacy of the

marketing campaigns through dashboards with the

following KPI’s: Number of deliveries; Number of

content visualizations; Number of conversions or

purchases. All the KPI’s may analysed per costumer

segment and per period with different granularities,

and may be analysed using a customer funnel of

engagement representation to understand where the

campaigns are less effective.

The Place Owner can grant permissions to

perform these actions to the Place Manager.

The participants on the Wallet Owner user-

centered studies referred to be very interested on the

digitization of the items of brand engagement. 93.3%

referred to prefer digital loyalty cards and coupons on

a mobile wallet to the physical current alternatives,

and some mentioned the ease of use and the possible

decision support for remembering when to use these

items as reasons. However, 73.3% of the participants

had privacy concerns regarding the user profiling

needed for the targeted marketing campaigns, namely

the use of their personal data on digital sources like

social networks. Specifically, the results of our

research regarding marketing and gamification issues

suggest that Wallet Owners shall have the following

features on weWallet: (i) Manage the relation with

different Brands or Places, for the purpose of

costumer engagement items (loyalty cards, ranks and

coupons), having the option of being open to

campaigns of Brands with which they are not related

but are related with their preferences; (ii) Manage the

preferences for targeted marketing campaigns; (iii)

Manage the decision support system regarding

marketing items, defining if and when they want to be

remembered of using them, or if they want to receive

recommendations of Brands / Places regarding their

preferences and location. (iv) Receive targeted

marketing campaigns.

5 CONCLUSION AND FUTURE

WORK

Our studies confirmed that despite the interest and the

recognition of advantages of digital mobile wallets

from the part of Wallet Owners and Place Owners, the

current solutions still do not fulfil their needs. On this

paper, we described the elicitation of requirements for

a holistic digital mobile wallet, based on the

combination of applied research with user-centered

techniques. Our approach to face the current

challenges is based on the reduction of fragmentation

of mobile wallet services and on the abstraction

regarding mobile OS and communication interfaces.

This approach aims to provide a closer digital

substitute to nowadays physical wallets, increasing

Requirements Elicitation for a Holistic Mobile Wallet Ecosystem

69

the perceived added value for Wallet Owners, and to

optimize the number of potential users of the system,

increasing the perceived added value for Place

Owners.

For future work, we will build the first prototype

based on the requirements defined, and will invite

end-users to evaluate it. We plan to do 3 iterations of

the action research methodology, with the phases of

research, development of prototype and evaluation

(which feeds the next iteration). On the last iteration,

the final prototype will be deployed in a resort of

winter sports for an operational pilot with the duration

of one month.

ACKNOWLEDGEMENTS

This work is part of the weWallet project, co-funded

by COMPETE/P2020/EU, in the context of the

Portuguese Sistema de Incentivos à I&DT

Empresarial (project 010463).

We would like to sincerely thank all the participants

of the sessions of user-centered design, namely from

Parkurbis and Turistrela.

REFERENCES

Apple Inc. (2014) Apple Pay. Available at:

http://www.apple.com/apple-pay/ (Accessed: 21

February 2017).

European Payments Council (2014) EPC White Paper

Mobile Wallet Payments. Available at:

http://www.europeanpaymentscouncil.eu/index.cfm/kn

owledge-bank/epc-documents/epc-white-paper-

mobile-wallet-payments-and-feedback-questionnaire/

(Accessed: 23 February 2017).

Forrester Research (2015) The Future Of Mobile Wallets

Lies Beyond Payments. Available at:

http://blogs.forrester.com/thomas_husson/15-02-09-

the_future_of_mobile_wallets_lies_beyond_payments

(Accessed: 19 February 2017).

Gannamaneni, A., Ondrus, J. and Lyytinen, K. (2015) ‘A

Post-failure Analysis of Mobile Payment Platforms’, in

48th Hawaii International Conference on System

Sciences (HICSS). doi: 10.1109/HICSS.2015.141.

Google (2015) Android Pay. Available at:

https://www.android.com/intl/en_us/pay/ (Accessed:

21 February 2017).

M. Evans (2015) Why merchants should adopt a mobile

wallet strategy, Mobile Payments Today. Available at:

https://www.mobilepaymentstoday.com/blogs/why-

merchants-should-adopt-a-mobile-wallet-strategy/

(Accessed: 20 February 2017).

Ma, X. and Wei, W. (2014) ‘The architecture of mobile

wallet system based on NFC (near field

communication)’, Research Journal of Applied

Sciences, Engineering and Technology, 7(12), pp.

2589–2595.

MEO (2014) MEO CardMobili. Available at:

https://meo.cardmobili.com/welcome.xhtml;jsessionid

=cgkWPS+TtmQsu+n0nyz6FgpG.standalone-

ap2?cid=1534 (Accessed: 21 February 2017).

NOS (2015) NOS m.Ticket. Available at:

http://cinemas.nos.pt/Pages/m-ticket.aspx (Accessed:

21 February 2017).

Portnoi, M. and Shen, C.-C. (2015) ‘Loc-Auth : Location-

Enabled Authentication Through Attribute-Based

Encryption’, in International Conference on

Computing, Networking and Communications. doi:

10.1109/ICCNC.2015.7069321.

Rehman, S. and Coughlan, J. (2013) ‘An Efficient Mobile

Payment System Based On NFC Technology’, World

Academy of Science, Engineering and Technology,

7(78), pp. 1695–1698.

Samsung (2015) Samsung Pay. Available at:

http://www.samsung.com/us/samsung-pay/ (Accessed:

21 February 2017).

Shaw, N. (2014) ‘The mediating influence of trust in the

adoption of the mobile wallet’, Journal of Retailing and

Consumer Services, 21(4), pp. 449–459. doi: 10.1016/

j.jretconser.2014.03.008.

TechNavio (2015) Global Mobile Wallet Market 2019 -

Drivers, Challenges and Trends Analysis and

Forecasts. Available at: http://www.prnewswire.com/

news-releases/global-mobile-wallet-market-2019---

drivers-challenges-and-trends-analysis-and-forecasts-

296076821.html (Accessed: 23 February 2017).

Ugwu, C. and Mesigo, T. (2015) ‘A Novel Mobile Wallet

Based on Android OS and Quick Response Code

Technology’, International Journal of Advanced

Research in Computer Science & Technology, 3(1), pp.

85–89.

Williams, S. and Yu, D. (2015) Digital Wallets Don’t

Deliver What Consumers Need. Available at:

http://www.gallup.com/opinion/gallup/184094/digital-

wallets-don-deliver-consumers-need.aspx (Accessed:

19 February 2017).

Zhang, Y., Xin, C., Liu, W., Ding, J. and Zhu, Q. (2015)

‘Identification System Based on Near Field

Communication and Fingerprint Technology for

Android Mobile Devices’, in International Conference

on Automation, Mechanical Control and

Computational Engineering, pp. 2232–2235.

Zupanovic, D. (2015) ‘Implementation model for Near

Field Communication in Croatian ferry ticketing

system’, Energy Procedia. Elsevier B.V., 100, pp.

1396–1404.

ICE-B 2017 - 14th International Conference on e-Business

70