Online Portfolio Selection of LQ45 Stocks Index with the Adaptive

Online Moving Average Method

Irkham Muhammad Fakhri

1

, Deni Saepudin

1

and Aniq Atiqi Rohmawati

1

1

Department of Informatics, Telkom University, Bandung, Indonesia

Keywords:

Portfolio, Aolma, Equal Weight, Sharpe Ratio

Abstract:

An online portfolio is a collection or composition of a fund in financial assets with specific returns held online.

Online portfolio selection can increase the chances of getting the right stocks. One way to choose an online

portfolio is using the Adaptive Online Moving Average (AOLMA) method. This method predicts stock returns

using adaptive decay variables from moving averages so that the predictive rate increases even more. In this

paper, portfolio selection using the Adaptive Online Moving Average (AOLMA) method is carried out on the

LQ45 stock index dataset from April 2012 to April 2022. The portfolio performance is then compared to the

Equal Weight Portfolio (EWP). This portfolio is superior to the equal-weight portfolio in terms of mean return.

1 INTRODUCTION

An online portfolio is a collection of funds distributed

as financial assets with a specific return. In this study,

the portfolio comprises companies from the LQ45 in-

dex. Portfolio selection was studied for the first time

in 1952 by Markowitz. He developed a fundamental

idea of mean-variance to calculate the percentage of

asset allocation (Markowitz, 1952). An online port-

folio is different from a traditional portfolio. The on-

line portfolio does not consider the return distribution

of historical data to manage the portfolio return and

risk. One method currently used in an online portfo-

lio is the Adaptive Online Moving Average algorithm

or AOLMA. AOLMA was developed based on tech-

nical analysis to predict future stock price movements

as seen from historical data, including opening, high-

est, lowest prices, and most importantly, the closing

price and the trading volume (Brown and Jennings,

1989). AOLMA focuses primarily on accurate fore-

casting of future prices to help investors create opti-

mal investment strategies. In this paper, a portfolio

from LQ45 index stocks is constructed by maximiz-

ing the portfolio’s return value. Online selection of

portfolios has been carried out using various meth-

ods. However, these various methods use quite a lot

of historical data and a reasonably long time to predict

a stock closing price or stock return in a period in an

online portfolio. AOLMA is here to overcome this by

only needing data on a stock’s latest period’s closing

price to get predictions of closing prices and returns

for future periods. AOLMA can periodically improve

the effectiveness of predictions by updating the de-

cay factor every period. Stocks are selected based

on stock return predictions from the Adaptive Online

Moving Average Algorithm. In addition, the portfo-

lio will be compared to the Equal Weight portfolio by

calculating the mean return, standard deviation, and

Sharpe ratio.

2 LITERATURE REVIEW

Many studies on online portfolio selection have been

conducted in line with the development of computa-

tional intelligence techniques that prioritize efficient

and practical processes for managing stock as online

assets. The selection of this online portfolio does

not pay attention to the distribution function to pre-

dict future returns. The selection of online portfolios

is made by considering the selection of artificial in-

telligence techniques as a predictor of asset returns

and optimal investment strategies. There are many

types of portfolio selection, such as benchmarks, fol-

lowing the winner strategy, following the loser strat-

egy, a combination of winner and loser strategies,

as well as meta-learning strategies. One version of

the benchmark-type portfolio is the market method,

which buys and holds or sells the same stocks as an

index (Li and Hoi, 2014). The market method is

implemented by distributing available capital evenly

Fakhri, I., Saepudin, D. and Rohmawati, A.

Online Portfolio Selection of LQ45 Stocks Index with the Adaptive Online Moving Average Method.

DOI: 10.5220/0012639200003848

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 3rd International Conference on Advanced Information Scientific Development (ICAISD 2023), pages 321-327

ISBN: 978-989-758-678-1

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

321

across all assets in the index in each period. An-

other version of the benchmark-type portfolios is the

Constant Rebalanced Portfolio (CRP) which allocates

capital to the assets with the same risk level in all pe-

riods (Tan et al., 1991). Exponential Gradient (EG)

is a portfolio selection version of the winning strat-

egy type with an exponential gradient value adjust-

ment that is used to allocate investments using his-

torical return data and strategies from stocks in the

portfolio (Helmbold et al., 1998). The next version

for portfolio selection for the winning strategy type

is the Online Newton Step (ONS) through the appli-

cation of the cumulative log return calculation equa-

tion with the Hessian matrix variable and the gradient

matrix (Agarwal et al., 2006). The adaptive method

is another version of the portfolio selection of win-

ning strategy types. This version can determine mul-

tiple selections of stocks for portfolios such as op-

timal constant log portfolio and rebalancing, adap-

tive Markowitz portfolio selection method, and index-

based portfolio selection method (Gaivoronski and

Stella, 2003). Portfolio selection following the loser

strategy has several versions. The first version is the

Anticorrelation method, this method uses the mean

return and cross-correlation matrix of various risky

stocks in dividing the proportion of portfolio stocks

based on stocks that perform well and stocks that per-

form poorly (Thrun et al., 2004). The next version

is passive aggressive mean reversion (PAMR) from

the application of the loss equation depending on the

mean return portfolio (Li et al., 2012). The Confi-

dence Weighted Mean Reversion (CWMR) method is

another version for selecting portfolio types follow-

ing a loser strategy, this version is based on a vector

design on a portfolio with a Gaussian distribution pro-

cess and the process of adjusting the distribution con-

stantly depends on the nature of the average reversion

(Li et al., 2013). The latest version in the portfolio

of types following a losing strategy is Robust Median

Reversion (RMR), this version predicts the strength

of the median L1 value and can be used for symp-

tom revision in a simple linear time frame so that it

is easy to use (Huang et al., 2016). The selection of

stocks in a pattern-matching portfolio combines the

following winner and following loser strategies and

consists of two processes. The first process is to de-

termine a sample with the aim of selecting an existing

historical price model through a benchmark that is al-

most aligned with the current price pattern. The sec-

ond process is to build a better portfolio enhancement

model with reference to the selected pricing model.

The method used in selecting this type of portfolio is

selecting a sample based on a non-parametric kernel

to find a consistent price model by considering the dif-

ferent Euclidean model distances, then constructing

a log-optimal portfolio based on capital growth the-

ory (Gy

¨

orfi et al., 2006). This method has the latest

version by selecting samples based on nonparametric

nearest neighbors and proposes a method of embed-

ding the model from the log of the best nonparamet-

ric nearest neighbors (Gy

¨

orfi et al., 2008). These two

methods were further developed with the existence

of a nonparametric sample selection method based

on correlation using various model correlation coef-

ficients and proposed a Correlation-driven Nonpara-

metric (CORN) learning algorithm (Li et al., 2011).

The metalearning strategy is a type of portfolio selec-

tion using various strategies combined to get a suit-

able portfolio. One strategy is the strategy of using

the Aggregating algorithm which can solve the prob-

lem of selecting online portfolios, and generalizing

the worst case of the Universal Portfolio (UP) algo-

rithm [4]. There are also those who directly imple-

ment meta-learning algorithm methods such as On-

line Newton Update (ONU) and Online Gradient Up-

date (OGU) with satisfactory success rates in select-

ing stocks for online portfolios (Das and Banerjee,

2011). There is also another strategy implemented

in this portfolio using the Follow the Leading His-

tory (FLH) algorithm which is implemented in such

a way that the basic data set is adjusted periodically

and continuously with each base expert making calcu-

lations for future prices. with the start being the time

period varies in historical data (Hazan and Seshadhri,

2009).

2.1 Portfolio Selection with Online

Moving Average Revision

The Online Moving Average Revision or abbreviated

OLMAR is the first online portfolio selection algo-

rithm to use a moving average variable that assumes

that stocks performing poorly in the present will per-

form better in the future and vice versa. The OL-

MAR is exploited from the Moving Average Rever-

sion approach which considers the expected return

and stock risk. There are two moving averages used in

the OLMAR, namely Simple Moving Average or ab-

breviated SMA algorithm and the Exponential Mov-

ing Average or abbreviated EMA algorithm (Li et al.,

2015). The SMA algorithm uses the arithmetic av-

erage of truncated historical prices (Johnston et al.,

1999). Whereas, the EMA algorithm takes more his-

torical stock prices and then assigns an exponential

weight to each stock price.

ICAISD 2023 - International Conference on Advanced Information Scientific Development

322

2.2 Portfolio Selection with Adaptive

Online Net Profit Maximization

Portfolio selection using the Adaptive Online Net

Profit Maximization or abbreviated AOLNPM algo-

rithm is a development of the Online Moving Aver-

age Revision (OLMAR) method. This is because OL-

MAR has several drawbacks such as the house limit

for the rate of return that must be set, the selection

of strategies that are found only take the appropri-

ate strategy without looking at other strategies that

may have higher returns, and OLMAR returns also

do not impose special conditions and there are no

transaction costs calculated in making portfolio strat-

egy changes. The purpose of adding NPM is to add

value to the transaction cost variable and then trans-

form the non-linear model into a linear programming

problem that is commensurate with changes in the

variable in the portfolio. Even though AOL NPM is

an updated model, there are still limitations such as

the risky assets taken are determined only by histori-

cal asset data even though asset volume must also be

considered and assets with small risks are not consid-

ered in selecting online portfolios. This is evidenced

by the application of AOLNPM to the MSCI, NYSE-

O, NYSE-N, and TSE index stocks. The cumulative

return results are satisfactory (Guo et al., 2021).

2.3 Portfolio Selection with Adaptive

Online Moving Average

Adaptive Online Moving Average (AOLMA) is an al-

gorithm that focuses on predicting stock movements

to determine optimal investment strategies. AOLMA

uses historical data analysis that comes from financial

markets such as historical stock prices and stock trad-

ing volume. The AOLMA uses technical analysis to

determine whether or not the trend will continue in a

stock. Instruments that can be used to carry out trend

analysis are trend lines, candlestick formations, and

other systematic visualizations. The AOLMA relies

on design to factor decay over a given period. The

AOLMA method is based on regression techniques,

namely techniques obtained from analyzing two dif-

ferent and separate variables to obtain an equation to

estimate returns effectively and accurately. Adaptive

Online Moving Average (AOLMA) works by adjust-

ing the stock decay factor gradually from the mov-

ing average according to stock performance (Li and

Hoi, 2012). The advantages provided by the AOLMA

method include predictions that are made faster and

in real time, the data needed is only the latest stock

close price data, and the effectiveness of the predic-

tion is further improved by updating the decay factor

value by adding and subtracting Y values.

2.4 Equal Weight Portfolio

qual weight portfolio is the simplest and easiest to

implement portfolio selection approach. An equal-

weight portfolio is based on giving each company the

same weight. This portfolio can be relied upon to

maximize stock returns in the portfolio and is very

easy to allocate to many stocks. Equal weight portfo-

lio can be formulated as follows (Brandel, ).

w

i

=

1

N

′

i = 1, 2, ....N, (1)

where w

i

is the weight i

th

stock in the portfolio,

and N is the number of stocks contained in the port-

folio.

3 METHODOLOGY

The design of all processes of a system that is in this

article is built-in visualization with the format in the

form of a flow chart (flowchart) containing a work-

flow explanation of the system design built for the ba-

sic work of the system from the beginning to the end

of the process as shown in Figure 1.

Figure 1: Methodology.

The initial step in creating this system was to input

all weekly stock price index data with the LQ45 index

in the period April 2012 - April 2022 by taking the

dataset from the Yahoo Finance website. The sample

dataset used is shown in Table 1.

Table 1: Dataset Sample.

Date Close Close Close Close Close

BBCA TLKM ASII PTBA INTP

30/04/2012 1610 1670 7270 3650 18850

07/05/2012 1600 1640 6885 3250 18150

14/05/2012 1510 1580 6840 3290 17300

21/05/2012 1450 1450 6585 3240 17200

28/05/2012 1420 1520 6335 3000 17250

The next stage is the data preprocessing stage.

Data preprocessing is carried out to prepare raw data

on LQ45 stocks that have been previously obtained

to be processed into data that is ready to be used in

the system created. This data preprocessing step fo-

cuses on data cleaning, namely eliminating or mod-

ifying incorrect or empty data values (missing val-

ues), and correcting inconsistent data. Furthermore,

Online Portfolio Selection of LQ45 Stocks Index with the Adaptive Online Moving Average Method

323

the data normalization process is carried out, data nor-

malization is the process of comparing data so that it

can be described as data with normal distribution.

3.1 Adaptive Online Moving Average

(AOLMA) Algorithm

The process of forming a portfolio by applying the

AOLMA algorithm is as follows:

1. Determine the first decay factor α

1

with 0 ≤ α

1

≤

1and the updating value of the next decay factor γ

with γ ≤ 0.001. The decay factor will be a vector

in the portfolio (α = (α

1

, α

2

, ..., α

m

)) in a period

(t) of an asset (i) ( i = 1, 2, . . . , m ).

2. Calculating stock predictions for period t with the

Simple Moving Average for the first 10 weeks.

3. Calculating stock predictions in period t + 1:

P

1

(t+1)

= a

(t+1)

.P

(t)

+ (1 − a

(t+1)

).P

′

(t)

(2)

Where P

t+1

is prediction close period t +1, a

t+1

is

period decay factor t+1, P

(t)

is close period t, and

P

′

(t)

is prediction close period t(from SMA predic-

tion calculations).

4. Calculating the expected stock return in the t+1

period:

r

′

(r+1)

= a

(t+1)

.1 + (1 − a

(t+1)

)P

(t)

.

r

′

t

r

t

(3)

Where r

′

(r+1)

is expected stock return period t+1,

a

(t+1)

is period decay factor t+1, r

′

t

is expected

stock return period t, and r

t

is period stock return

t.

5. Calculating the expected return of stock i in period

t:

r

′

(ti)

= a

(ti)

+ (1 − a

(ti)

).

r

′

(t−1)i

r

(t−1)i

(4)

the following formula is generated:

r

′

(ti)

−r

′

(ti)

= r

(ti)

−

r

′

(t−1)i

r

(t−1)i

−(1−

r

′

(t−1)i

r

(t−1)i

.a

(ti)

) (5)

Where r

′

(ti)

is expected stock return i period t, r

(ti)

is stock return i period t, a

(ti)

is stock decay factor

i period t, r

′

(t−1)i

is expected stock return i period

t-1, and r

(t−1)i

is stock return i period t-1.

6. Determine the conditions that occur in the portfo-

lio:

1st condition : r

(ti)

> r

′

(ti)

and r

(t−1)i

> r

′

(t−1)i

2nd condition : r

(ti)

> r

′

(ti)

and r

(t−1)i

≤ r

′

(t−1)i

3rd condition : r

(ti)

≤ r

′

(ti)

and r

(t−1)i

> r

′

(t−1)i

4rd condition : r

(ti)

≤ r

′

(ti)

and r

(t−1)i

≤ r

′

(t−1)i

If the first condition or 4th condition is found, the

decay factor coefficient is updated:

a

(ti)

= −(1−

r

′

(t−1)i

r

(t−1)i

< 0anda

(t+1)i

= a

(ti)

+γ (6)

If the 2nd condition or 3rd condition is found, the

decay factor coefficient is updated:

a

(ti)

= −(1−

r

′

(t−1)i

r

(t−1)i

≥ 0anda

(t+1)i

= a

(ti)

+γ (7)

Increasing and decreasing the value of the de-

cay factor can increase the accuracy as well as

adaptive updates in getting close stock price pre-

dictions and stock return predictions from the

AOLMA method.

7. Calculating the effectiveness of the Adaptive On-

line Moving Average (AOLMA) return predic-

tion. This is done by calculating the relative pre-

diction error of the stock at time j using the for-

mula.

Er

( j)

=

r

′

ji

− r

ji

r

ji

.100% (8)

and the average relative error of predictions:

Er =

1

n

n

∑

j=1

r

′

ji

− r

ji

r

ji

.100% (9)

Where Er(j) is a relative error of time stock pre-

diction j, Er is the average relative error, n is many

stocks in the portfolio, r

′

ji

is the expected Return

of stock i time j, and r

ji

is stock return i time j.

4 EVALUATION

4.1 Metric

In investigating the accuracy of the prediction results,

evaluation metrics are used, namely, the root means

square error is abbreviated as RMSE and the mean

absolute error is abbreviated as MAE (Chen et al.,

2021).

RMSE =

s

1

n

n

∑

i=1

(y

i

− y

′

i

)

2

(10)

ICAISD 2023 - International Conference on Advanced Information Scientific Development

324

MAE =

s

1

n

n

∑

i=1

|

y

i

− y

′

i

)

|

(11)

Where y

′

i

is the predicted stock return and y

i

is the ac-

tual stock return, and n is the total number of samples.

4.2 Sharpe Ratio

The Sharpe Ratio is a way of measuring the perfor-

mance of a portfolio. The way to evaluate portfolio

performance with the Sharpe ratio is to look at the

value of the portfolio’s expected return and portfolio

risk. If the Sharpe values the smaller the ratio, the

less good portfolio performance will result and vice

versa. The portfolio Sharpe ratio can be formulated

as follows (Iorio et al., 2018).

MAE =

R

exp

σ

p

(12)

Where S

p

is the Sharpe ratio, R

exp

is the Expected

return portfolio, and σ

p

is portfolio risk.

4.3 Testing Scenario

The application of the AOLMA algorithm to the

LQ45 stock index is carried out in the following

stages:

1. Predict the return of stocks that are on the LQ45

index using AOLMA with an initialization of a de-

cay factor (α) value of 0.5 with γ (modifier of de-

cay factor value) of 0.001. In this paper, a first de-

cay factor (α) value of 0.5 was chosen because it

is the middle range in the choice of value and a de-

cay factor value modifier γ of 0.001. The modifier

for the decay factor value γ must be smaller than

the decay factor value because the decay factor

update is carried out every period and the change

must not be too significant but can be effective

in predicting stock close prices and stock returns

from the AOLMA method.

2. Form a portfolio with 2 stocks, 3 stocks, and 5

stocks. Stocks are selected based on the com-

pany’s industrial activity sector.

3. The selection or determination of stocks taken ev-

ery week for the portfolio is based on AOLMA’s

return predictions where the stocks taken must

have one of the largest return predictions in the

list of stocks in the portfolio every week.

4. Form a portfolio with the same list of stocks as

the portfolio obtained from point 3 but the weight

used must be the same for each stock in the port-

folio (portfolio with the same weight).

5. Comparing the results of portfolio performance in

points 3 and 4 with the performance of stocks in

the portfolio list using the calculation of the mean

return value, standard deviation value, and Sharpe

ratio value for each portfolio.

6. Determines the best portfolio to be taken based

on its performance from the highest mean return

value and the highest Sharpe ratio value of the

portfolio in this test.

4.4 Experiment Result

The return prediction results and model evaluation for

all stocks that will be formed into several portfolios

are shown in Table 2.

Table 2: Evaluation of Return Prediction Results.

Stock RMSE MAE

BBCA 0,033205 0,023546

TLKM 0,036214 0,026868

ASII 0,045645 0,032404

PTBA 0,064316 0,047836

INTP 0,051624 0,039506

PTPP 0,075572 0,05426

PGAS 0,065342 0,044468

INDF 0,039979 0,028801

The value of the portfolio using the AOLMA

method compared to the portfolio with the same

weight was carried out with 2 stocks, 3 stocks, and

5 stocks from different sectors. A comparison of

the portfolio with 2 stocks is shown in Figure 3.

The first 2 stock portfolios consist of BBCA.JK and

TLKM.JK. The second portfolio of 2 stocks with

ASII.JK and PTBA.JK. The third portfolio of 2 stocks

with INTP.JK and PTPP.JK. The fourth portfolio of 2

stocks with PGAS.JK and INDF.JK.

Based on Table 3, the average return of the portfo-

lio with the method used in this article is better than

the equal weight method. The equal weight portfolio

has a relatively smaller risk value in terms of the risk

obtained from the standard deviation (smaller) and

also has better performance than AOLMA in terms

of Sharpe ratio (larger). Thus, on testing a portofolio

of 2 stocks, the AOLMA portofolio only provides a

better mean return than the equal-weight portofolio.

The value of the portfolio using the AOLMA

method compared to the portfolio with the same

weight carried out with 3 stocks is shown in Fig-

ure 5. The first 3 stock portfolios consist of

BBCA.JK, TLKM.JK, and ASII.JK. The second port-

folio of 3 stocks consists of BBCA.JK, TLKM.JK and

PTBA.JK. The third portfolio of 3 stocks consists of

BBCA.JK, TLKM.JK and INTP.JK. The fourth port-

Online Portfolio Selection of LQ45 Stocks Index with the Adaptive Online Moving Average Method

325

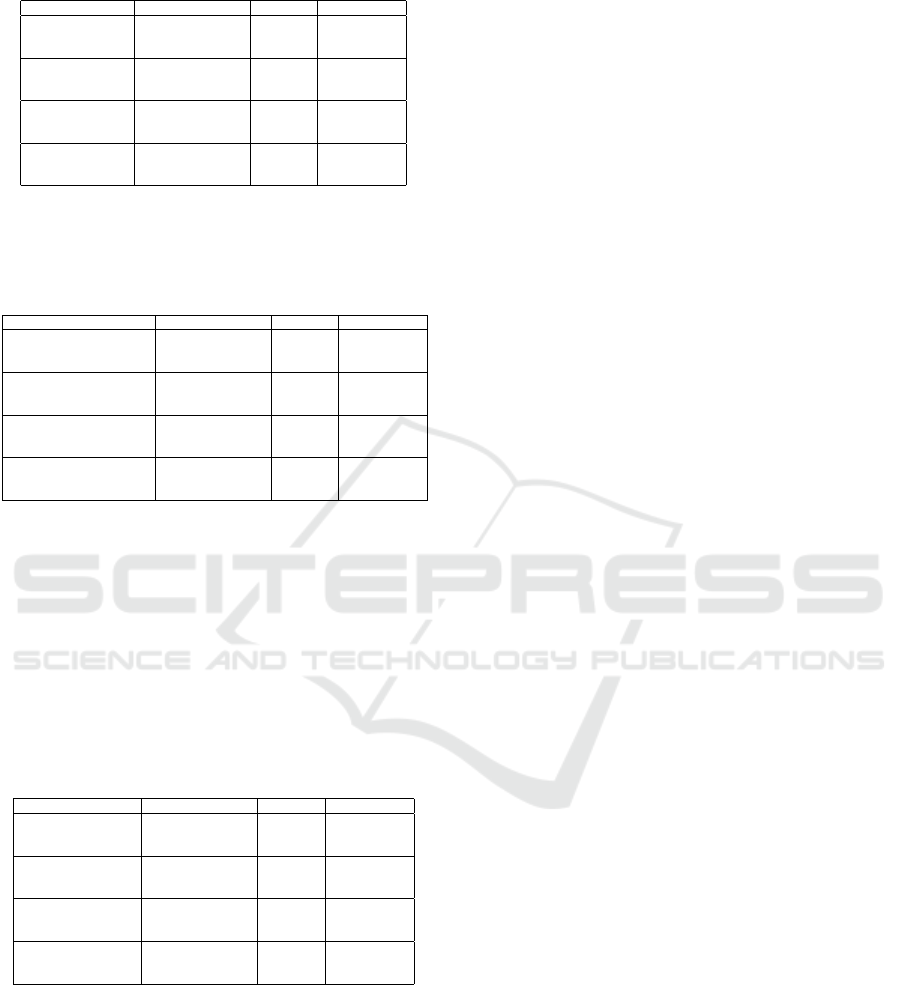

Table 3: Comparative Evaluation of Portfolio Value for 2

Stocks.

Portofolio Evaluation AOLMA Equal Weight

BBCA and TLKM Mean Return 1,00549 1,00323

Standard Deviation 0,03321 0,02836

Sharpe Ratio 30,2729 35,3713

ASII and PTBA Mean Return 1,00198 1,00156

Standard Deviation 0.05337 0,04074

Sharpe Ratio 18,7727 24,5833

INTP and PTPP Mean Return 1,00368 1,00161

Standard Deviation 0,05916 0,04826

Sharpe Ratio 16,9639 20,7519

PGAS and INDF Mean Return 1,00180 1,00055

Standard Deviation 0,05176 0,04052

Sharpe Ratio 19,3514 24,6889

folio of 3 stocks consists of BBCA.JK, TLKM.JK and

PTPP.JK stock.

Table 4: Comparative Evaluation of Portfolio Value for 3

Stocks.

Portofolio Evaluation AOLMA Equal Weight

BBCA, TLKM, and ASII Mean Return 1,00549 1,00253

Standard Deviation 0,03952 0.02957

Sharpe Ratio 25,4389 33,8964

BBCA, TLKM, and PTBA Mean Return 1,00348 1,00282

Standard Deviation 0,04689 0,03058

Sharpe Ratio 21,3965 32,7929

BBCA, TLKM, and INTP Mean Return 1,00452 1,00220

Standard Deviation 0,04286 0,03079

Sharpe Ratio 23,4342 32,5485

BBCA, TLKM, and PTPP Mean Return 1,00429 1,00318

Standard Deviation 0,05285 0,03451

Sharpe Ratio 18,9997 29,0654

Based on Table 4, the average return of the portfo-

lio with the method used in this article is better than

the equal weight method. The equal weight portfolio

has a relatively smaller risk value in terms of the risk

from standard deviation (smaller) and also has bet-

ter performance than AOLMA in terms of Sharpe ra-

tio (larger). In testing the portfolio of 3 stocks, the

AOLMA portfolio only provides a better mean return

than the equal-weight portfolio.

Table 5: Comparative Evaluation of Portfolio Value for 5

Stocks.

Portofolio Evaluation AOLMA Equal Weight

BBCA, TLKM, ASII, Mean Return 1,00468 1,00176

INTP, and INDF Standard Deviation 0,04361 0,02942

Sharpe Ratio 23,0342 34,0494

BBCA, TLKM, ASII, Mean Return 1,00347 1,00154

INTP, and PGAS Standard Deviation 0,05001 0,03227

Sharpe Ratio 20,0629 31,0356

BBCA, TLKM, ASII, Mean Return 1,00432 1,00216

INTP, and PTPP Standard Deviation 0,05483 0,03327

Sharpe Ratio 18,3153 30,1165

BBCA, TLKM, ASII, Mean Return 1,00484 1,00195

INTP, and PTBA Standard Deviation 0,04971 0,03043

Sharpe Ratio 20,2105 32,9218

The value of the portfolio using the AOLMA

method compared to the portfolio with the same

weight carried out with 5 stocks. The first 5

stock portfolios are BBCA.JK, TLKM.JK, ASII .JK,

INTP.JK , and INDF.JK. The second portfolio of 5

consists of BBCA.JK, TLKM.JK, ASII.JK, INTP.JK

and PGAS.JK. The third portfolio of 5 stock con-

sists of BBCA.JK, TLKM.JK, ASII.JK, INTP.JK,

and PTPP.JK. The fourth portfolio of 5 stock con-

sists of BBCA.JK, TLKM.JK, ASII.JK, INTP.JK and

PTBA.JK.

Based on Table 5, the average return of the portfo-

lio with the method used in this article is better than

the equal weight method. Portfolios of equal weight

have relatively smaller risk values in terms of standard

deviation risk (smaller) and also have better perfor-

mance than AOLMA in terms of Sharpe ratio (larger).

Thus, in testing a portfolio of 3 stocks, the AOLMA

portfolio only provides a better average return than a

portfolio with equal weight.

A portfolio comparison for 2 stocks, 3 stocks, and

5 stocks as a whole got the results that, the AOLMA

portfolio provides better performance in terms of

mean return alone. Whereas performance in terms

of standard deviation and Sharpe ratio of the equal

weight portfolio is better. That matter shows that the

AOLMA portfolio can get a bigger profit than the

equal portfolio weight, but the big profits are worth

the bigger risks too. Besides that, a portfolio con-

sisting of several stocks does not necessarily provide

better portfolio performance.

5 CONCLUSIONS

Experimental results for stock selection for a portfo-

lio of 2 stocks, 3 stocks, and 5 stocks with AOLMA

and EW show that the portfolio with AOLMA return

predictions has better performance than the mean re-

turn side compared to equal-weight portfolios, espe-

cially with stocks that have history of performance

good and uniform. If the stocks selected for selec-

tion with AOLMA have performance and movement

each week, the value and performance of the AOLMA

portfolio are lower than the equal-weight portfolio.

The portfolio with the best performance is the one

with the most stocks in the experiment is a portfo-

lio of 5 stocks whose performance is seen from the

Sharpe ratio. Although the portfolio with AOLMA’s

return prediction has a high return the risk that is ob-

tained is also higher, that is which makes the shape

ratio smaller. This indicates that the increased risk

is compensated by a higher increase in returns. In

further research, it is suggested to be able to expand

the method comparison for the selection of portfolios

used in addition to equal weight portfolio and perfect

the AOLMA method by changing the parameters used

or even combining them with another method.

ICAISD 2023 - International Conference on Advanced Information Scientific Development

326

REFERENCES

Agarwal, A., Hazan, E., Kale, S., and Schapire, R. (2006).

Algorithms for portfolio management based on the

newton method. In Proceedings of the 23rd interna-

tional conference on Machine learning, page 9–16.

Brandel, S. Markov regime switching model implementa-

tion to the stockholm stock market comparison with

equal weight portfolio,”(2017.

Brown, D. and Jennings, R. (1989). On technical analysis.

The Review of Financial Studies, 2:527–551.

Chen, W., Zhang, H., Mehlawat, M., and Jia, L. (2021).

Mean–variance portfolio optimization using machine

learning-based stock price prediction,”applied. Soft

Computing, 100:106943.

Das, P. and Banerjee, A. (2011). Meta optimization and

its application to portfolio selection. In Proceed-

ings of the 17th ACM SIGKDD international confer-

ence on Knowledge discovery and data mining, page

1163–1171.

Gaivoronski, A. and Stella, F. (2003). On-line portfolio se-

lection using stochastic programming. Journal of Eco-

nomic Dynamics and Control, 27:1013–1043.

Guo, S., Gu, J.-W., and Ching, W.-K. (2021). Adap-

tive online portfolio selection with transaction

costs. European Journal of Operational Research,

295:1074–1086.

Gy

¨

orfi, L., Lugosi, G., and Udina, F. (2006). Non-

parametric kernel-based sequential investment strate-

gies. Mathematical Finance: An International Jour-

nal of Mathematics, Statistics and Financial Eco-

nomics, 16:337–357.

Gy

¨

orfi, L., Udina, F., and Walk, H. (2008). Experiments

on universal portfolio selection using data from real

markets.

Hazan, E. and Seshadhri, C. (2009). Efficient learning algo-

rithms for changing environments. In Proceedings of

the 26th annual international conference on machine

learning, page 393–400.

Helmbold, D., Schapire, R., Singer, Y., and Warmuth, M.

(1998). On-line portfolio selection using multiplica-

tive upyears. Mathematical Finance, 8:325–347.

Huang, D., Zhou, J., Li, B., Hoi, S., and Zhou, S. (2016).

Robust median reversion strategy for online portfolio

selection. IEEE Transactions on Knowledge and Data

Engineering, 28:2480–2493.

Iorio, C., Frasso, G., D’Ambrosio, A., and Siciliano, R.

(2018). A p-spline based clustering approach for port-

folio selection. Expert Systems with Applications,

95:88–103.

Johnston, F., Boyland, J., Meadows, M., and Shale, E.

(1999). Some properties of a simple moving average

when applied to forecasting a time series,”journal. the

Operational Research Society, 50:1267–1271.

Li, B. and Hoi, S. (2012). On-line portfolio selec-

tion with moving average reversion. arXiv preprint

arXiv:1206.4626.

Li, B. and Hoi, S. (2014). Online portfolio selection: A

survey. ACM Computing Surveys (CSUR, 46:1–36.

Li, B., Hoi, S., and Gopalkrishnan, V. (2011). Corn:

Correlation-driven nonparametric learning approach

for portfolio selection. ACM Transactions on Intel-

ligent Systems and Technology (TIST, 2:1–29.

Li, B., Hoi, S., Sahoo, D., and Liu, Z.-Y. (2015). Moving

average reversion strategy for on-line portfolio selec-

tion. Artificial Intelligence, 222:104–123.

Li, B., Hoi, S., Zhao, P., and Gopalkrishnan, V. (2013).

Confidence weighted mean reversion strategy for on-

line portfolio selection. ACM Transactions on Knowl-

edge Discovery from Data (TKDD, 7:1–38.

Li, B., Zhao, P., Hoi, S., and Gopalkrishnan, V. (2012).

Pamr: Passive aggressive mean reversion strategy for

portfolio selection. Machine learning, 87:221–258.

Markowitz, H. (1952). Portfolio selection. journal of fi-

nance.

Tan, G., Kelly, P., Kim, J., and Wartell, R. (1991). Com-

parison of camp receptor protein (crp) and a camp-

independent form of crp by raman spectroscopy and

dna binding. Biochemistry, 30:5076–5080.

Thrun, S., Saul, L., and Sch

¨

olkopf, B. (2004). Advances

in neural information processing systems 16. In Pro-

ceedings of the 2003 Conference, page 47–110, Lon-

don, England. The MIT Press.

Online Portfolio Selection of LQ45 Stocks Index with the Adaptive Online Moving Average Method

327