INTERNAL FRAUD RISK REDUCTION

Results of a Data Mining Case Study

Mieke Jans, Nadine Lybaert

KIZOK Research Institute, Hasselt University Campus Diepenbeek, Agoralaan Building D, 3590 Diepenbeek, Belgium

Koen Vanhoof

Research Group Data Analysis and Modeling, Hasselt University Campus Diepenbeek, Diepenbeek, Belgium

Keywords:

Internal Fraud, Data Mining, Risk Reduction.

Abstract:

Corporate fraud these days represents a huge cost to our economy. Academic literature already concentrated

on how data mining techniques can be of value in the fight against fraud. All this research focusses on fraud

detection, mostly in a context of external fraud. In this paper we discuss the use of a data mining technique

to reduce the risk of internal fraud. Reducing fraud risk comprehends both detection and prevention, and

therefore we apply a descriptive data mining technique as opposed to the widely used prediction data mining

techniques in the literature. The results of using a latent class clustering algorithm to a case company’s

procurement data suggest that applying this technique of descriptive data mining is useful in assessing the

current risk of internal fraud.

1 INTRODUCTION

Saying that fraud is an important (however not loved)

part of business, is nothing new. Fraud is a mil-

lion dollar business, as several research studies reveal.

Among them are an important survey of PriceWater-

house&Coopers (PwC, 2007) and of the Association

of Certified Fraud Examiners (ACFE, 2006). The

study conducted in the United States by the ACFE

in 2004-2005 and the worldwide study, held by PwC

in 2006-2007 yield the following insights. 43% of

companies worldwide have fallen victim to economic

crime in the years 2006 and 2007. The average fi-

nancial damage to companies subjected to the PwC

survey was US$ 2.42 million per company over two

years. Participants of the ACFE study estimate a loss

of 5% of a company’sannual revenues to fraud. These

numbers all address corporate fraud.

Academic literature is currently investigating the

use of data mining for the purpose of fraud detec-

tion. (Brockett et al., 2002), (Cortes et al., 2002),

(Est´evez et al., 2006), (Fanning and Cogger, 1998),

(Kim and Kwon, 2006) and (Kirkos et al., 2007) are

just a few examples of a more elaborated list of ar-

ticles concerning the hot topic of fighting fraud. Al-

though a lot of this research may be framed in differ-

ent settings -going from different techniques to differ-

ent fraud domains-, there are two characteristics that

stand for all executed research up till now: the fo-

cus is on external fraud and a predictive data mining

approach is applied for fraud detection. We however

are interested in internal fraud, since this represents

mainly these large costs in the PwC and ACFE sur-

veys. Further, we are convinced that not fraud detec-

tion alone, but detection in combination with preven-

tion, is of priceless value for organizations. We will

use the term fraud risk reduction for encompassing

both fraud detection and prevention.

We continue this study on the positive results of

academic literature concerning the use of a data min-

ing approach for the purpose of fraud detection. Since

our aim is fraud risk reduction, we apply however an-

other category of techniques than applied up till now.

We believe in the value of descriptive data mining for

the purpose of fraud risk reduction. In contrast to the

explored predictive data mining techniques in current

academic literature, descriptive data mining provides

us with insights of the complete data set and can be of

value for assessing the fraud risk in selected business

processes.

In the following sections we explain the followed

methodology of this study, the data set, the used latent

161

Jans M., Lybaert N. and Vanhoof K. (2008).

INTERNAL FRAUD RISK REDUCTION - Results of a Data Mining Case Study.

In Proceedings of the Tenth International Conference on Enterprise Information Systems - AIDSS, pages 161-166

DOI: 10.5220/0001679201610166

Copyright

c

SciTePress

class clustering algorithm, and the results of investi-

gating a business process of the case company. We

end with a conclusion.

2 METHODOLOGY

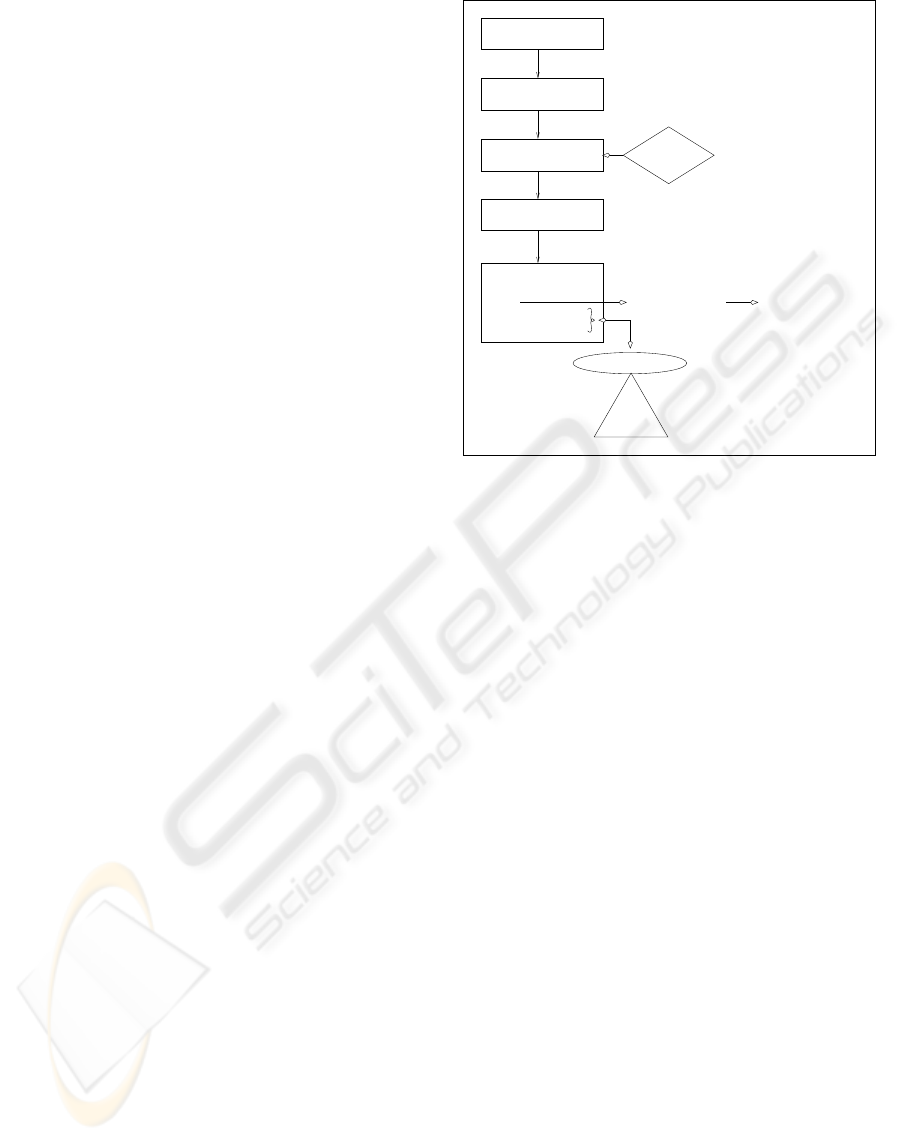

The applied methodology can be summarized by Fig-

ure 1. As a first step, an organization should select a

business process which it thinks is worthwhileinvesti-

gating. Further is the implementation of advanced IT

a breeding ground for employee fraud (Lynch and Go-

maa, 2003). For this reason and because data needs to

be electronically stored in order to mine it by means of

a data mining approach, the selected business process

needs to be one with an advanced IT integration. In a

second step the stored data will be collected, manipu-

lated and enriched. These are mainly technical trans-

actions. During the third step, the technical data will

be translated into behavioral data. This translation

builds upon domain knowledge and is not just a tech-

nical transformation. The core of the methodology

is then to apply descriptive data mining for getting

more insights in this behavioral data. The descrip-

tives should provide the researchers a recognizable

pattern of procedures of the selected business process.

In addition some other patterns of minor groups of ob-

servations in the data can arise, interesting to have a

closer look at. By auditing observations part of such a

subgroup, the domain expert can categorize the obser-

vations in four groups. The fraudulent observations

(a first category) are part of fraud detection, while

the observations that circumvent procedures or are

created by mistake (two other categories) are part of

fraud prevention. Fraud prevention is in this method-

ology primarily based on checking or taking away the

fraud opportunity. The importance of opportunity is

stressed by Cressey’s fraud triangle with opportunity

being the only element of fraud risk that an employer

can influence. The other two elements, rationaliza-

tion and incentive, are personal characteristics. The

fourth category of audited observations, the ones with

extreme values, can also occur, but are of no interest

for internal fraud risk reduction.

3 DATA SET

The data set is established by performing the first

three steps of our methodology. For this study, the

corporation of a case company was acquired. This

company, which chooses to stay anonymous in this

study, is an international financial services provider,

ranked in the top 20 of Europeanfinancial institutions.

Knowledge

with advanced IT integration

1. Select business process

2. Data collection, manipulation

and enrichment

3. Transformation of data

5. Audit by domain experts:

4. Descriptive Data Mining

− extreme values

− fraud

− circumventing procedures

− errors/mistakes

FRAUD PREVENTION

FRAUD DETECTION Predictive Data Mining

Opportunity

Fraud

risk

Rationalisation Incentive/Pressure

Domain

Figure 1: Methodology for internal fraud risk reduction.

The business process selected for internal fraud risk

reduction is procurement, so data from the case com-

pany’s procurement cycle is the input of our study.

More specifically, the creation of purchasing orders

(PO’s) was adopted as process under investigation.

As a start, a txt-dumpis made out of SAP. All PO’s

that in 2006 resulted in an invoice are the subject of

our investigation. This raw data is then reorganized

into appropriate tables to support meaningful analy-

sis. After the creation of these new formats, additional

attributes were created as enrichment and resulted in

a data set of 36.595 observations. Based on domain

knowledge, supported by descriptive statistics, a pre-

clustering step is made. PO’s are split in two groups:

old PO’s and new PO’s. Old PO’s are the ones cre-

ated before July 2005. The fact that they are included

in our data is because an invoice of the year 2006 can

be linked to a PO created in 2005 or even before 2005.

However, if a PO is from before July 2005 (there are

PO’s even from 2000), this PO shows a different life

cycle than if it were younger (there are for example

much more changes on such PO’s). The subset of old

PO’s contains 2.781 observations while the subset of

new PO’s counts 33.814 observations. Both subsets

of PO’s were subjected to the proposed methodology.

Since the latter group is the most prominent in as-

sessing internal fraud risk (most recent) and given its

magnitude, this paper gives detailed test results of the

new PO’s. The other side of the picture is that this

large data set poses more problems in the fifth step of

our methodology, namely the auditing of interesting

observations. We restrict this study to provide recom-

ICEIS 2008 - International Conference on Enterprise Information Systems

162

mendations on this matter for the new PO’s. For the

subset of old PO’s however, the audit step is effec-

tively executed and these results will be reported after

the discussion of the new PO’s. In what follows, the

term data set refers to the subset of new PO’s (33.814

observations).

The most important attributes to describe a PO

and its life cycle are the following: the name of the

creator, the supplier, the purchasing group, the type

of purchasing document, the number of changes, the

number of changes after the last release and the num-

ber of price related changes after the last release. Con-

cerning the numerical attributes, there are 91 creators

recurring in the data set, 3.708 suppliers, 13 purchas-

ing groups and 6 document types. (see Table 1)

Table 1: Categorical attributes.

Categorical Recurrence in data set

Creator 91

Supplier 3.708

Purchasing Group 13

Document Type 6

Of the 91 creators, not all of them introduce

equally as much PO’s in the ERP system, because of

the individual characteristics of each purchase. Some

creators, responsible for a particular type of purchase,

need to enter lots of PO’s, while other creators, re-

sponsible for other types of purchase, only enter a

few PO’s. Also the turnover in terms of personnel has

its reflection on the number of PO’s per employee.

Like creators, the frequency of suppliers in the data

set is liable to the specific characteristics of the prod-

uct or service supplied. There will be for example

more PO’s concerning monthly leasing contracts for

cars than there will be for supplying desks. Hence the

former supplier will be more frequently present in the

data set than the latter. Concerning the 13 purchasing

groups, there is no difference in expected fraud risk

between the different groups. Some groups are more

present than others in the data set, but this can all be

explained by domain knowledge. The same goes for

the six differentpurchasing documenttypes. All types

have their specific characteristics, but there is no ex-

pected difference concerning fraud risk.

The numerical attributes are described in Table 2.

For each attribute, three intervals were created, based

on their mean and standard deviation. For the first

attribute, the intervals were [2-4], [5-8] and [9-...], for

the second attribute [0-0], [1-2] and [3-...] and for the

last attribute [0-0], [1-1] and [2-...]. In Table 2 we

see that there is a highly skewed distribution for the

three attributes, which is to be expected for variables

that count these types of changes. The changes are

supposed to be small in numbers.

After creating these attributes and providing de-

scriptives, we turn to the third step of our method-

ology. For the specification of our model, we take

into account the particular type of fraud risk we wish

to reduce. The fraud risk linked with entering PO’s

into the ERP-system is connected with the number

of changes one makes to this PO, and more specifi-

cally, the changes made after the last release. There

is namely a built-in flexibility in the ERP system to

modify released PO’s without triggering a newrelease

procedure. For assessing the related risk, we selected

four attributes to mine the data. A first attribute is the

number of changes a PO is subjected to in total. A

second attribute presents the number of changes that

is executed on a PO after it was released for the last

time. The third attribute we created is the percent-

age of this last count that is price related. So what

percentage of changes made after the last release is

related to price issues? This is our third attribute. The

last attribute concerns the magnitude of these price

changes. Considering the price related changes, we

calculate the mean of all price changes per PO and its

standard deviation. On itself, no added value was be-

lieved to be in it. Every purchaser has its own field of

purchases, so cross sectional analysis is not really an

option. However, we combine the mean (µ) and stan-

dard deviation (σ) to create a theoretical upper limit

per PO of µ + 2σ. Next, we count for each PO how

often this theoretical limit was exceeded. This new

attribute is also taken into account in our model. In

this core model, no categorical attributes were added.

As a robustness check however, attributes like docu-

ment type and purchasing group were included in the

model. The results did not significantly change by

these inclusions.

4 LATENT CLASS CLUSTERING

ALGORITHM

For a descriptive data mining approach, we have cho-

sen for a clustering algorithm, more specifically a la-

tent class (LC) clustering algorithm. We prefer LC

clustering to the more traditional K-means clustering

for several reasons. The most important reason is that

this algorithm allows for overlapping clusters. An ob-

servation is provided a probability to belong to each

cluster, for example .80 for cluster 1, .20 for cluster 2

and .00 for cluster 3. This gives us the extra opportu-

nity to look at outliers in the sense that an observation

does not belong to any cluster at all. This is for exam-

ple the case with probabilities like .35, .35 and .30.

Other considerations to apply the LC clustering algo-

rithm are the ability to handle attributesof mixed scale

INTERNAL FRAUD RISK REDUCTION - Results of a Data Mining Case Study

163

Table 2: Descriptives of numerical attributes.

Attribute Minimum Maximum Mean Standard 1st interval 2nd interval 3rd interval

deviation frequency (%) frequency (%) frequency (%)

Number of changes 1 152 4.37 3.846 71.3 21.5 7.2

Number of changes 0 91 .37 1.343 80.9 11.9 7.2

after last release

Price related number of 0 46 .15 .882 91.1 6.7 2.2

changes after last release

types and the presence of information criteria statis-

tics to determine the number of clusters. For a more

detailed comparison of LC clustering with K-means

we refer to (Magidson and Vermunt, 2002). For more

and detailed information about LC analysis, we refer

to (Kaplan, 2004) and (Hagenaars and McCutcheon,

2002).

5 CASE STUDY RESULTS

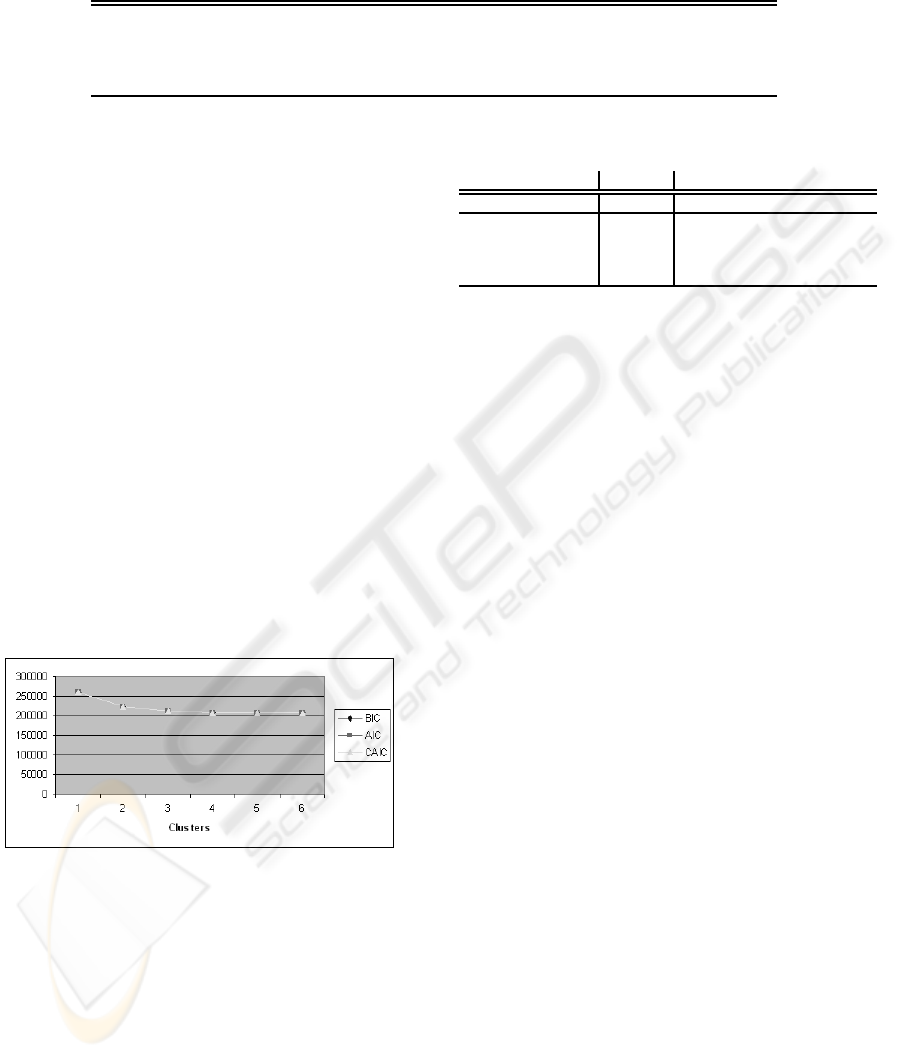

5.1 Model Specifications

Using the four attributes described in Section 3,

we executed the LC clustering algorithm with the

number of clusters (K) set equal to 1 till 6. This

yielded the information criteria (IC) values plotted

in Figure 2. As you can see, the IC values drop

heavily until the 3-cluster model. Beyond the 3-

cluster model, the decreases are more modest. Based

on these values, we decide to use this 3-cluster model.

Figure 2: Information criteria values.

5.2 Results

The profile of the 3-cluster model is presented in Ta-

ble 3. It gives the mean value of each attribute in each

cluster. To compare with the data set as a whole, the

mean values of the population are also provided.

Looking at the profile of the 3-cluster model, there

is an interesting cluster to notice, the third cluster, if

it was even only for its size. Cluster 1 comprehends

76.6% of the total data set, cluster 2 22.1% and cluster

3 only 1.3%. Why is there 1.3% of all PO’s behaving

Table 3: Profile of data set and 3-cluster model.

Population Cluster 1 Cluster 2 Cluster 3

Cluster size 100 0.7663 0.2212 0.0125

Number of changes 4.37 3.3378 6.7608 25.459

Changes after release 0.37 0.0193 1.2376 6.1257

Percentage price related 0.0756 0 0.3185 0.4094

Count over limit 0.01 0.0072 0.0194 0.2725

differently than the remaining PO’s? Regarding the

mean attribute values of this small cluster, this clus-

ter is, besides from its size, also interesting in terms

of fraud risk. The mean number of changes per PO

in this cluster, is 25, as opposed to a mean number

of changes of 4 in the data set. Why are these PO’s

modified so often? Not only are these PO’s changed

so much in their entire life cycle, they are also mod-

ified significantly more after they were last released

(6 times) in comparison with the mean PO in the data

set (0.37 times). These are odd characteristics. The

mean percentage in cluster 3 of changes after the last

release that is price related is also the highest per-

centage of the three clusters (40.9%). All together

this means that the average PO in cluster 3 is changed

25 times in total, of which 6 changes occur after the

last release and 2.4 of those 6 changes are price re-

lated. Concerning the magnitude of the price related

changes, we can conclude that these changes of PO’s

in cluster 3 are more often much larger than the aver-

age price change in that PO if we compare this with

price related changes of PO’s in the other clusters. In

cluster 3, there are on average 0.2725 price related

changes larger than µ + 2σ per PO, in comparison

with 0.0072 and 0.00194 per PO in cluster 1 and 2

and 0.01 changes in the entire data set.

Taking these numerical characteristics into ac-

count, one can conclude that cluster 3 has a profile

with a higher fraud risk than the other two clusters.

Also categorical attributes behave in a different fash-

ion than they behave in the data set as a whole. So

there are the creators of the PO. One person for ex-

ample created 39 out of the 408 PO’s from cluster 3

(hereby representing 9.56% of cluster 3), while the

same person only created 131 out of the 33.814 PO’s,

which counts only for 0.39% of the entire data set.

For calculating the probability of taking this per-

ICEIS 2008 - International Conference on Enterprise Information Systems

164

son (called xxx) by chance 39 times of 408, given the

prior distribution, we use the hypergeometric distri-

bution. This looks as follows.

h

m

=

M

m

N−M

n−m

N

n

The hypergeometric distribution is a discrete

probability distribution that describes the number of

successes m in a sequence of n draws without replace-

ment, givena finite population N with M successes. In

our situation concerning person xxx this leads to:

h

39

=

131

39

33.814−131

408−39

33.814

408

< 1

−15

So if we select 408 cases at random out of the pop-

ulation of 33.814 observations, there is a probability

less than 1

−15

that we pick 39 cases with user-id xxx,

given the prior distribution of 131 successes in the

population. This event is very unlikely to happen by

coincidence.

Not only creators made such significant increases

in representation, but also some suppliers are signif-

icantly more represented in cluster 3 than they are in

the full data set. We screened all creators and suppli-

ers on significant increases in representation between

the data set and cluster 3 with a significance level of

h < 1

−5

. 14 suppliers and 12 creators met this cri-

terium. Not all of them are however equally important

since an increase of 0.03% representation to 0.98% is

not as impressive as an increase of 1.47% to 7.6%.

Table 4 gives us more insights into the importance of

the 14 suppliers and 12 creators.

Table 4: Descriptives of creators and suppliers with a sig-

nificant higher representation in cluster 3.

Representation (r) in cluster 3 Number of suppliers Number of creators

r < 1% 4

1% < r < 2% 4

2.2% < r < 4.5% 3

6% < r < 7.5% 3

Total 14

r < 2% 3

2.9% < r < 3.5% 3

5% < r < 10% 6

Total 12

Since it is more than likely that auditing all 408

PO’s of cluster 3 is too time consuming, it would be

interesting to take a sample of PO’s that are made by

one of the creators described above or involve one of

those suppliers (or both). The smallest sample to ex-

tract from this cluster is to take only those PO’s of the

six creators and three suppliers that are most repre-

sented in the cluster. This yields a sample of 38 PO’s.

Why is it that they merely induce PO’s in this small

cluster than in the other two clusters. What makes

these purchases this risky? Also the recurrence of a

particular purchasing group and purchasing document

type can shed an interesting light on deciding which

PO’s to audit. Auditing this kind of PO’s can learn

the company a lot about the opportunities that exist to

commit fraud, in view of the fraud risky profile that

the numerical attributes describe.

The possibility LC clustering provides to audit ob-

servations that do not belong to any cluster is also ex-

plored. 42 PO’s were identified and audited in-depth.

There was no uniform profile for these cases. The au-

dit resulted in a few questions with regard to the use

of the ERP-system. Nothing however showed misuse

of procedures or any other fraud risk.

5.3 Audit by Domain Experts of Old

PO’s

As already mentioned, the audit step is not (yet) exe-

cuted for the subset of new PO’s. The entire method-

ology, provided in Figure 1, is however also applied

on the subset of old PO’s, including the fifth step. The

results of the descriptive data mining step are similar

to the discussed results. The small interesting cluster

(in perspective of a fraud risky profile) of old PO’s

only contained 10 observations, with nine of them

stemming from the same purchasing group and six of

them created by the same employee. These 10 obser-

vations were audited by domain experts. The results

of their investigation are summarized in Table 5.

Table 5: Summary of investigation by domain experts.

Category Number of cases

Extreme values 0

Fraud 0

Circumventing procedures 9

Errors/Mistakes 1

These are very good results in the light of inter-

nal fraud risk reduction. Nine PO’s, the ones in the

particular purchasing group, are created and modified

all over and over again. This is against procedures

and makes investigating these PO’s very difficult. By

creating such complex histories of a PO, the opportu-

nity of committing fraud increases. Only insiders can

unravel what really happened with these PO’s, since

they are such a mess. This off course increases the

opportunity and risk of internal fraud. Also, the in-

vestigation of this practice has put things in another

perspective concerning the separation of functionali-

ties. A follow-up investigation by the audit and in-

vestigations department of the case company for this

matter is approved.

INTERNAL FRAUD RISK REDUCTION - Results of a Data Mining Case Study

165

In the tenth PO a mistake is made. As explained

before, a mistake that stays unnoticed creates a win-

dow of opportunity for internal fraud. The employee

that first makes a mistake by accident, can afterwards

consider how to turn this opportunity to one’s advan-

tage.

By investigating the 10 selected observations, ad-

ditional odd practices came to light, which also in-

duced extra investigations. On top of this, the case

company gave priority on auditing the procurement

cycle in depth.

5.4 Comparing Results with Reporting

Results

The results of using a descriptive data mining tech-

nique, provides us with interesting results. In the

smaller subset we encounter PO’s that are changed

over and over again. Also in the larger subset, chang-

ing the PO a lot of times is a primal characteristic of

the selected observations. However, one could won-

der if this outcome was not much easier to obtain,

simply by applying some form of reporting. For ex-

ample, maybe we get the same results when we just

take the observations with lots of changes? We do not

go into the discussion about one method being gener-

ally better than another. What we can and want to say

however, is that in our case, we did not find the same

results by using basis reporting as we found by ap-

plying the LC clustering algorithm. The multivariate

analysis was indispensable to come to the presented

results. Another remark to consider about reporting,

is that you do not know in advance which attribute

to go on. Also analyzing the influence of categorical

variables is not easy with reporting tools.

6 CONCLUSIONS

In this paper, a methodology for reducing internal

fraud risk is presented. This is a contribution to the

literature in that it concerns internal fraud whereas

the literature focusses on external fraud. Further we

broaden our scope from fraud detection to fraud risk

reduction, which encompasses both fraud detection

as prevention. We were able to apply our suggested

methodology in a top 20 ranked European financial

institution. The results of the case study suggest that

the use of a descriptive data mining approach and the

latent class clustering technique, can be of additional

value to reduce the risk of internal fraud in a com-

pany. Using simple reporting tools did not yield the

same results, nor would be able to provide similar in-

sights in current use of procedures. The application of

the suggested methodology at the case company pro-

duced a tone of more concern about the topic of inter-

nal fraud along with concern about the opportunity of

committing this crime.

REFERENCES

ACFE (2006). 2006 ACFE Report to the nation on occupa-

tional fraud and abuse. Technical report, Association

of Certified Fraud Examiners.

Brockett, P. L., Derrig, R. A., Golden, L. L., Levine, A., and

Alpert, M. (2002). Fraud classification using principal

component analysis of RIDITs. The Journal of Risk

and Insurance, 69(3):341–371.

Cortes, C., Pregibon, D., and Volinsky, C. (2002). Com-

munities of interest. Intelligent Data Analysis, 6:211–

219.

Est´evez, P., Held, C., and Perez, C. (2006). Subscription

fraud prevention in telecommunications using fuzzy

rules and neural networks. Expert Systems with Appli-

cations, 31:337–344.

Fanning, K. and Cogger, K. (1998). Neural network detec-

tion of management fraud using published financial

data. International Journal of Intelligent Systems in

Accounting, Finance & Management, 7:21–41.

Hagenaars, J. A. and McCutcheon, A. L. (2002). Applied

Latent Class Analysis. Cambridge University Press.

Kaplan, D. (2004). The Sage Handbook of Quantitative

Methodology for the Social Sciences. Thousand Oaks:

Sage Publications.

Kim, H. and Kwon, W. J. (2006). A multi-line insurance

fraud recognition system: a government-led approach

in Korea. Risk Management and Insurance Review,

9(2):131–147.

Kirkos, E., Spathis, C., and Manolopoulos, Y. (2007). Data

mining techniques for the detection of fraudulent fi-

nancial statements. Expert Systems with Applications,

32:995–1003.

Lynch, A. and Gomaa, M. (2003). Understanding the po-

tential impact of information technology on the sus-

ceptibility of organizations to fraudulent employee be-

haviour. International Journal of Accounting Informa-

tion Systems, 4:295–308.

Magidson, J. and Vermunt, J. K. (2002). Latent class mod-

els for clustering: A comparison with k-means. Cana-

dian Journal of Marketing Research.

PwC (2007). Economic crime: people, culture and controls.

the 4th biennial global economic crime survey. Tech-

nical report, PriceWaterhouse&Coopers.

ICEIS 2008 - International Conference on Enterprise Information Systems

166