RULE EVOLUTION APPROACH FOR MINING MULTIVARIATE

TIME SERIES DATA

Viet-An Nguyen and Vivekanand Gopalkrishnan

School of Computer Engineering, Nanyang Technological University, 50 Nanyang Avenue, 639798, Singapore

Keywords:

Time Series, Data Mining, Rule Evolution.

Abstract:

In the last few decades, due to the massive explosion of data over the world, time series data mining has

attracted numerous researches and applications. Most of these works only focus on time series of a single

attribute or univariate time series data. However, in many real world problems, data arrive as one or many series

of multiple attributes, i.e., they are multivariate time series data. Because they contain multiple attributes,

multivariate time series data promise to provide more intrinsic correlations among them, from which more

important information can be gathered and extracted. In this paper, we present a novel approach to model and

predict the behaviors of multivariate time series data based on a rule evolution methodology. Our approach is

divided into distinct steps, each of which can be accomplished by several machine learning techniques. This

makes our system highly flexible, configurable and extendable. Experiments are also conducted on real S&P

500 stock data to examine the effectiveness and reliability of our approach. Empirical results demonstrate that

our system has substantial estimation reliability and prediction accuracy.

1 INTRODUCTION

Due to the rapid advances in database system tech-

nologies as well as the World Wide Web, the growth

of data captured and stored all over the world has in-

creased massively in the last few decades. Along with

this explosion, data in various complex forms have

also been created and used, requiring more efficient

and sophisticated data mining techniques. Among

these, time series data mining has been an attractive

research topic recently (Last et al., 2001), (Keogh and

Kasetty, 2002), (Last et al., 2004).

Mining time series data is the process of discov-

ering and extracting knowledge from data, taken at

equally spaced time intervals in a variety of domains

including financial markets, gene expressions, nat-

ural phenomena, scientific and engineering experi-

ments and medical treatments. In (Keoghand Kasetty,

2002), the time series data mining tasks are mainly di-

vided into four categories: indexing (finding the best

matching time series in database), clustering (group-

ing time series in database), classification (predicting

the class of an unlabeled time series) and segmen-

tation (constructing a model to approximate a time

series). Most of these approaches focus only on the

time series of a single attribute or univariate time se-

ries data. However, in many practical applications,

the time series data captured have very high dimen-

sionality which are characterized by a large number

of attributes. Such data are called multivariate time

series data, and they occur in various fields including:

• Medical observations: electrocardiograms (ECG)

and electroencephalograms (EEG) of patients are

usually recorded and used for diagnosis. Each

ECG or EEG might be considered a time series

which contains important information about the

patient’s health (Wei et al., 2005).

• Economic and financial data: each company in the

financial market is represented by multiple time

series over time. Modeling and classifying these

time series can help investors gain more insight

knowledge about the intrinsic health of each stock

in the market (Wah and Qian, 2002).

• Action sequences or gestures: sequences of move-

ments and gestures of hand and body can be used

to denote a sign in Auslan (Australian Sign Lan-

guage)

1

. Each sequence in a time series can be

used to train a model to recognize every sign in

the language (Kadous, 1999).

Univariate time series data normally store the cap-

tured values of an attribute over some period of time.

1

http://archive.ics.uci.edu/ml/datasets/

19

Nguyen V. and Gopalkrishnan V. (2008).

RULE EVOLUTION APPROACH FOR MINING MULTIVARIATE TIME SERIES DATA.

In Proceedings of the Tenth International Conference on Enterprise Information Systems - AIDSS, pages 19-26

DOI: 10.5220/0001688500190026

Copyright

c

SciTePress

Modeling these data can help us understand the char-

acteristics of the particular attribute as well as forecast

the future attribute values. However, in many cases

such as those mentioned above, single attribute time

series might not contain enough information to de-

scribe complex systems. Contrarily, multivariate time

series data contain the values of multiple attributes

changing over time. Based on these kind of data, in-

sightful correlations among different attributes can be

identified and captured to build more robust and reli-

able models.

In spite of these advantages of multivariate over

univariate time series data, some problems make

modeling and forecasting multivariate time series data

challenging and difficult. Due to the intricate correla-

tions among multiple attributes changing over time,

these problems usually require complicated models

which might lead to low accuracy and efficiency. In

addition, the high dimensionality makes the intrinsic

characteristics of the data too complex for the built

models to capture.

In this paper, we present a novel approach to

model and predict the behaviors of multiple attributes

time series databases. In our approach, from each data

set at each time point, a set of classification rules is

generated by supervised machine learning techniques

and optimized by pruning using some Interestingness

Measure. The problem of predicting the target at-

tribute based on historical data is then transformed

to the problem of predicting the classification rules.

Top-k evolutionary trends containing k pairs of rules

which represent the k most important and significant

changes in the data over time are extracted from data

sets at consecutive time points. The series of top-

k evolutionary trends are then used to build mod-

els to predict those trends at the current time point.

Each step in our proposed approach can be accom-

plished by various learning techniques which makes

the framework highly flexible and configurable.

In Section 2 we present some preliminary infor-

mation and method to transform our original prob-

lem to a new equivalent problem. Section 3 outlines

our approach in detail, including a preliminary step

(data preprocessing) and three main steps (rule prun-

ing, top-k evolutionary trends mining and top-k evolu-

tionary trends predicting). Experimental results with

analyses are shown in Section 4 to show the effec-

tiveness and reliability of our proposed framework.

Finally, Section 5 summarizes our contributions and

presents some directions for future work.

2 BACKGROUND

2.1 Time Series Database

In our problem, a time series database DB contains

an ordered sequence of data sets that arrives in timely

order.

DB = {D(t) | t ∈ [1, T]}

Each data set D(t) at time point t is a set of instances.

D(t) =

n

I

k

(t) | k ∈ κ(t)

o

,t ∈ [1, T]

where

• k is the id of the instance

• κ(t) is the set of instance’s ids at time point t

• I

k

(t) is the instance with id k at time point

t. I

k

(t) =

a

k

i

(t) | i ∈ [1, n]

,t ∈ [1, T], k ∈ κ(t);

where a

k

i

(t) is the value of the i

th

attribute. The

attributes can be either numeric or nominal.

Corresponding to each instance, c

k

(t) denotes the

class (or target attribute) of the instance I

k

(t) at time

point t. The target attribute c is nominal, and its do-

main is denoted by dom(c) = {c

m

| m ∈ [1, M]}.

2.2 Classification Rule

A classification rule is an implication of the form:

R

c

m

=

^

i∈[1,n]

(a

i

op A

i

) → (c = c

m

)

, c

m

∈ dom(c)

where:

• a

i

is the i

th

attribute which can be either nominal

or numeric.

• op is a relational operator. For numeric attribute,

op ∈ {<, =, >}, while for nominal attribute op ∈

{=, 6=}.

• A

i

is a value that belongs to the domain of a

i

.

• c is the class or target attribute.

• c

m

is a class value that belongs to dom(c). c

m

is

also considered the class of the rule R

c

m

.

In a rule, each term (a

i

op A

i

), ∀i ∈ [1, n] is called

an antecedent of the rule, whereas the rule consequent

refers to the part after the implication arrow (c = c

m

).

In this paper, when referring to a rule, the rule class

and rule consequent are used interchangeably.

A rule might not contain all the normal attributes

in its antecedents. In order to have a standard format

for all the rules, the classification rules would be re-

formatted. Let N denote the set of numeric normal

ICEIS 2008 - International Conference on Enterprise Information Systems

20

attributes and O denote the set of nominal normal at-

tributes in each data set D. Then, the new formatted

classification rules can be expressed as follows:

R

c

m

=

^

∀i∈N

(A

L

i

op

L

a

i

op

U

A

U

i

) ∧

^

∀ j∈O

(a

j

= A

j

)

→ (c = c

m

)

where:

• a

i

is a numeric attribute

• A

L

i

, A

U

i

are the lower and upper boundary numeric

values of attribute a

i

• op

L

, op

U

are the lower operator and upper opera-

tor respectively which can be either < or ≤

• a

j

is a nominal attribute

• A

j

is the nominal value of attribute a

j

In a re-formatted rule, a pair (A

L

i

, A

U

i

) and a value A

j

are used to determine the values of a numeric attribute

a

i

and a nominal attribute a

j

respectively.

2.3 Set of Rules

A set of classification rules RS(t) generated from the

data set D(t) can be defined as:

RS(t) =

n

R

c

m

j

(t) | c

m

∈ dom(c), j ∈ [1, l

c

m

]

o

,t ∈ [1, T]

where:

• c

m

is a class value in the domain of the target at-

tribute dom(c)

• l

c

m

is the number of rules which have class value

c

m

• R

c

m

j

(t) is the j

th

classification rule in the subset of

rules which have class value c

m

From the above definitions, we can also de-

fine RS

c

m

(t) as a subset of RS(t) which con-

tains all the rules having class c

m

in RS(t).

RS

c

m

(t) =

n

R

c

m

j

(t) ∈ RS(t) | j ∈ [1, l

c

m

]

o

, c

m

∈

dom(c),t ∈ [1, T].

2.4 Problem Transformation

As stated in Section 1, our goal is to model and pre-

dict the target attributebased on historical data of both

the normal and target attributes. By using this kind of

data, underlying characteristics of the data and corre-

lations between various attributes can be captured by

the learnt model. In our approach, in order to gen-

erate the model satisfying the above constraints, the

original problem is transformed to a new equivalent

problem.

From each data set D(t) at time point t, a set of

rules RS(t) will be generated, in which a rule R(t)

of RS(t) is an implication from the normal attributes

(a

1

(t), a

2

(t), ..., a

n

(t)) at time point t to the target at-

tribute c(t + 1) at the next time point (t + 1).

R

c

m

(t) =

^

i∈[1,n]

(a

i

(t) op A

i

(t)) → (c(t + 1) = c

m

)

A set of classification rules can be generated from

each data set by various supervised machine learning

techniques. It is this characteristic that makes our ap-

proach highly flexible and configurable. Details on

choosing suitable techniques are discussed in Section

4.2.

Assume T is the current time point, then the trans-

formed problem can be stated as follows: Given the

sets of rules RS(1), RS(2), ..., RS(T − 1) generated

from data sets D(1), D(2), ..., D(T − 1) respectively,

predict the k most important rules at the current time

point T.

3 RULE EVOLUTION APPROACH

3.1 Preprocessing Data

In order to have a higher quality data to use in later

steps of the knowledge discovery process, data pre-

processing is required. In this step, we present two

basic components of data preprocessing:

• Data cleaning: to identify and replace inconsistent

and noisy values.

• Data normalization: to transform our raw data

into appropriate forms for using in later steps.

Data Cleaning. Due to the huge amount of data

processed, it is obvious that our time series database

tends to be incomplete, noisy and inconsistent. In or-

der to fill in missing values, smooth out noise while

identifying outliers and correct inconsistencies in the

data, data cleaning is performed.

Because of various reasons, the raw data have

missing values. In order to have a complete and con-

sistent database to process, those missing values need

to be filled. Here we replace the missing values by

the mean (for numerical attributes) or the median (for

nominal attributes.

In order to detect and replace outliers in nu-

merical data, we perform Boxplot Analysis (Tukey,

1977). Boxplot, invented in 1977 by John Tukey,

is a popular way of visualizing a distribution. The

RULE EVOLUTION APPROACH FOR MINING MULTIVARIATE TIME SERIES DATA

21

analysis is based on five-number summary including

five values: LowerWhisker, Q

1

(25

th

percentile),

Median, Q

3

(75

th

percentile) and UpperWhisker.

LowerWhisker and UpperWhisker are the most

extreme observations of a distribution. Any value

of the considered distribution falling outside this

range (from LowerWhisker to UpperWhisker) can be

considered an outlier and should be replaced by an

appropriate value (LowerWhisker if it is smaller than

LowerWhisker or UpperWhisker if it is greater than

UpperWhisker).

Data Normalization. Because different numerical at-

tributes have different ranges of values, data normal-

ization is needed in order to have all the attribute val-

ues in a standard predefined range. In this step, we

normalize all attribute data to the range [0,1]. Each

attribute value u is normalized to ¯u by the following

equation:

¯u =

u− u

min

u

max

− u

min

where u

min

and u

max

are the smallest and largest val-

ues of the attribute data respectively.

3.2 Pruning Rules

As discussed in the Section 2.4, from each data set

D(t), a set of classification rules RS(t) is generated.

Each rule R

c

m

(t) in the set shows that an instance will

be classified as class c

m

at timestamp t if all the an-

tecedents of the rule R

c

m

(t) are satisfied. In literature,

various rule induction techniques have been proposed.

Two of the most successful algorithms are ID3 (Quin-

lan, 1986) and its successor C4.5 (Quinlan, 1993), ba-

sically due to their simplicity and comprehensibility.

Both algorithms are used to generate decision trees,

from which classification rules can be created. (Su

and Zhang, 2006) proposed a fast decision-tree learn-

ing algorithm which is capable of reducing the time

complexity compared to C4.5 while still preserving

high accuracy. Other popular rule induction algo-

rithms include Decision Table (Kohavi, 1995), OneR

(Holte, 1993), PRISM (Cendrowska, 1987), CART

(Breiman et al., 1984), etc. Generally, sets of clas-

sification rules can be generated with high accuracy

and large data coverage by such rule induction algo-

rithms. However,if the data set is huge, the number of

rules generated in each RS(t) will be large, leading to

over-fitting the data, especially in noisy data sets, and

also causing difficulties for human experts to evalu-

ate the rules. In order to avoid these drawbacks, rule

pruning is performed based on some Interestingness

Measures.

Interestingness Measures are used to evaluate and

rank the discovered rules (or patterns) generated by

the data mining process. Various works have been

done on choosing the right interestingness measure

for specific kinds of discovered patterns (Tan et al.,

2002). In (Geng and Hamilton, 2006), these mea-

sures are generally divided into three categories: ob-

jective measures based on the statistical properties of

the rules, subjective measures based on the human

knowledge, and semantic measures based on the se-

mantics and explanations of the rules themselves. In

our approach, we use the following objective mea-

sures:

• Support S(R) of a rule R, which measures how

often the rule holds in the data set.

• ConfidenceC(R) of a rule R, which measures how

often the consequent is true given that the an-

tecedent is true.

• Data coverage DC(R) of a rule R, which measures

how comprehensive is the rule.

Based on these Interestingness Measures, we de-

fine a combined general measure IM(R) of rule R

which shows how interesting the rule is. IM(R) is

calculated as follows:

IM(R) =

w

S

× S(R) + w

C

×C(R)

w

S

+ w

C

where w

S

and w

c

are the weights of Support and Con-

fidence respectively.

Algorithm 1 shows a greedy method to prune un-

interesting rules from a given set. First, the Interest-

ingness Measure IM of each rule in the set is calcu-

lated. Rules are then sorted in an ascending order

based on their IM. After sorting, rules with small IM

value are pruned until the coverage of the remaining

set of rules is less than a predefined threshold.

Algorithm 1: PRUNE UNINTERESTING RULES

Input: uRS - An unpruned set of rules

Input: θ - The threshold for data coverage

Output: pRS - The pruned set of rules

foreach R ∈ uRS do1

calculate IM(R)2

calculate DC(R)3

sort RS in ascending order by IM4

pRS = uRS5

initialize coverage = 16

for i = 1 →| uRS | do7

if coverage− DC(R

i

) > θ then8

prune R

i

from pRS9

return pRS10

ICEIS 2008 - International Conference on Enterprise Information Systems

22

After pruning, the remaining set contains rules

which have high Interestingness Measures and guar-

antee that their data coverage is still greater than a

user-defined threshold θ, (0 < θ < 1). The pruned sets

of rules will be used in later steps to predict the set of

rules at the current time point.

3.3 Mining Top-k Evolutionary Trends

Given the sets of rules RS(1), RS(2),... , RS(T − 1)

in the previous time points, how can we predict the

set of rules RS(T) at the current time point T? In this

step, we introduce a novel approach to predict RS(T)

using rule evolution methodology.

The problem of mining interesting rules (or pat-

terns) from time series has been addressed by vari-

ous works (Weiss and Hirsh, 1998), (Povinelli, 2000)

and (Hetland and Saetrom, 2002) etc. (Keogh and

Kasetty, 2002) classifies these approaches into two

types: supervised and unsupervised. In supervised

methods, the rule target is known and used as an in-

put to the mining algorithm; while unsupervised ap-

proaches are trained with only the time series itself

without any known target. Almost all of these ap-

proaches use some form of evolutionary computation

such as genetic programming or genetic algorithms.

In our approach as shown in the previous sections,

from each data set D(t), a set of rules RS(t) is gen-

erated. Each set of rules R(t) can be considered a

model of the data at time point t which shows the cor-

relations between the normal attributes at time point

t and the target attribute at time point (t + 1). This

ensures that the most updated characteristics and pos-

sible changes of the data can be captured by our gen-

erated rules or models. However, having the model

of the latest data is not good enough. We also have

to make use of the historical models. Here, we con-

sider that, from the time point t to the next time point

(t + 1), rules in the set RS(t) evolve to rules int the set

RS(t + 1). Our goal is to capture these evolutionary

trends of rules over time.

As defined in section 2.2, our classification rule

contains two main components: antecedents and con-

sequent. The antecedents consist of ranges of n at-

tributes, satisfying which an instance will be classi-

fied as the corresponding rule’s consequent. Based on

that, a classification rule can be considered a hyper-

cube in an n-dimensional space, where each dimen-

sion corresponds to an attribute.

Minkowski-form distance measures the distance

between two points in high dimensional space, and

is defined as

d

L

r

(H, K) =

n

∑

i=1

|h

i

− k

i

|

r

!

1

r

(1)

where H and K are two points in n-dimensional space

with their coordinates h

i

and k

i

in the i

th

dimen-

sion respectively. The two most commonly used

Minkowski-forms are L

1

(Manhattan distance) and

L

2

(Euclidean distance). In our approach, the dis-

tance between two arbitrary rules is defined as the Eu-

clidean distance between the two hypercubes’ centers

corresponding to the two rules and is computed by the

following equation:

d

L

2

(R

1

, R

2

) =

n

∑

i=1

A

U

2i

− A

L

2i

2

−

A

U

2i

− A

L

2i

2

2

!

1

2

(2)

In equation (2), A

U

1i

and A

U

2i

are the upper boundary

values of antecedent a

i

of R

1

and R

2

respectively.

Similarly, A

L

1i

and A

L

2i

are the lower boundary values

of antecedent a

i

of R

1

and R

2

respectively. The Eu-

clidean distance d

L

r

(R

1

, R

2

) shows how far the two

rules R

1

and R

2

are from each other in n-dimensional

space. The smaller the distance is, the more similar

the two rules are. Applying this property in temporal

data, given two rules R(t) and R(t + 1) from two con-

secutive time points t and (t + 1) respectively, a small

d

L

r

(R(t), R(t + 1)) means there is a high probability

that the first rule R(t) will evolve to the second one

R(t + 1) over the period from t to (t + 1).

Let’s consider two sets of rules RS(t) and RS(t +

1) generated from data sets D(t) and D(t + 1) at two

consecutive time points t and (t + 1) respectively.

Based on (2), the distance between every two rules,

each from RS(t) and RS(t + 1) respectively can be

computed. Each such pair of rules is considered an

evolutionary trend, whose significant level can be

expressed by the Euclidean distance. The smaller

the distance is, the more similar the two rules are,

and thus, the more significant the pair of rules is in

the evolutionary process. Therefore, all the pairs of

rules are sorted according to their distance and the k

pairs with lowest distance form the top-k evolutionary

trends which contain and represent the most impor-

tant underlying changes of the data over two consecu-

tive time points. Thus, from each pair of consecutive

time points t and (t + 1), a set of k pairs of rules de-

noted by evoK(t,t+1) is extracted and used to predict

the top k evolutionary trends at the current time point

T in the next step of our approach.

3.4 Predicting Top-k Evolutionary

Trends

These k evolutionary trends are ranked in ascend-

ing order according to the Euclidean distance be-

tween each pair of rules in the trend. Using all

the data sets from time point 1 to time point (T −

RULE EVOLUTION APPROACH FOR MINING MULTIVARIATE TIME SERIES DATA

23

1), we can form a series of k evolutionary trends

{evoK(t, t + 1) | t ∈ [1, T − 2]}. Based on these k se-

ries of trends, in this step we predict the k evolution-

ary trends from time point (T − 1) to the current time

point T, with which the most important movements

of stock prices in the near future can be forecasted.

Recall that, each evolutionary trend evoK(t,t + 1)

over the period from time point t to (t +1) contains k

pairs of rules. Each pair contains R(t) and R(t + 1),

where R(t) is considered to evolve to R(t + 1) over

the period from t to (t + 1). In order to capture the

underlying changes of the data that each pair of rules

in evoK(t,t + 1) represents, we define the operators,

by which each antecedent of R(t) evolves to the cor-

responding antecedent of R(t + 1).

Let evoOp

a

i

(R(t),R(t+1))

denote the operator by

which the antecedent a

i

evolves from the value a

it

of the rule R(t) to the value a

i(t+1)

of the rule R(t +

1). The domain of evoOp

a

i

(R(t),R(t+1))

is denoted by

dom(evoOp) and contains three operators: increased

(I), unchanged (U) and decreased (D). Each opera-

tor is defined based on comparing the values of an-

tecedent a

i

from time point t to (t + 1) as follows:

evoOp

a

i

(R(t),R(t+1))

=

I ⇔ a

it

′

≥ a

it

+ ε

U ⇔ a

it

+ ε ≥ a

it

′

> a

it

− ε

D ⇔ a

it

− ε > a

it

′

By extracting all the evolutionary operators from

every pair of classification rules in our k series of evo-

lutionary trends, we can obtain k series of evolution-

ary operators. These series of operators describe how

the data change over time and capture the most im-

portant underlying characteristics of our multivariate

time series data. Using each generated series of evo-

lutionary operators, regression models can be built

by various machine learning techniques and used to

predict the future evolutionary trends. Details about

choosing the learning techniques are discussed in sec-

tion 4.3.

4 EXPERIMENTAL RESULTS

AND ANALYSES

4.1 Database

We conducted experiments on data from the S&P 500

database. The whole database consists of quarterly

data sets from 1975 to 2006. Each quarterly data set

contains 500 instances corresponding to 500 compa-

nies in the S&P 500 index, 13 normal attributes which

are financial ratios, and a target attribute which indi-

cates the status of the company.

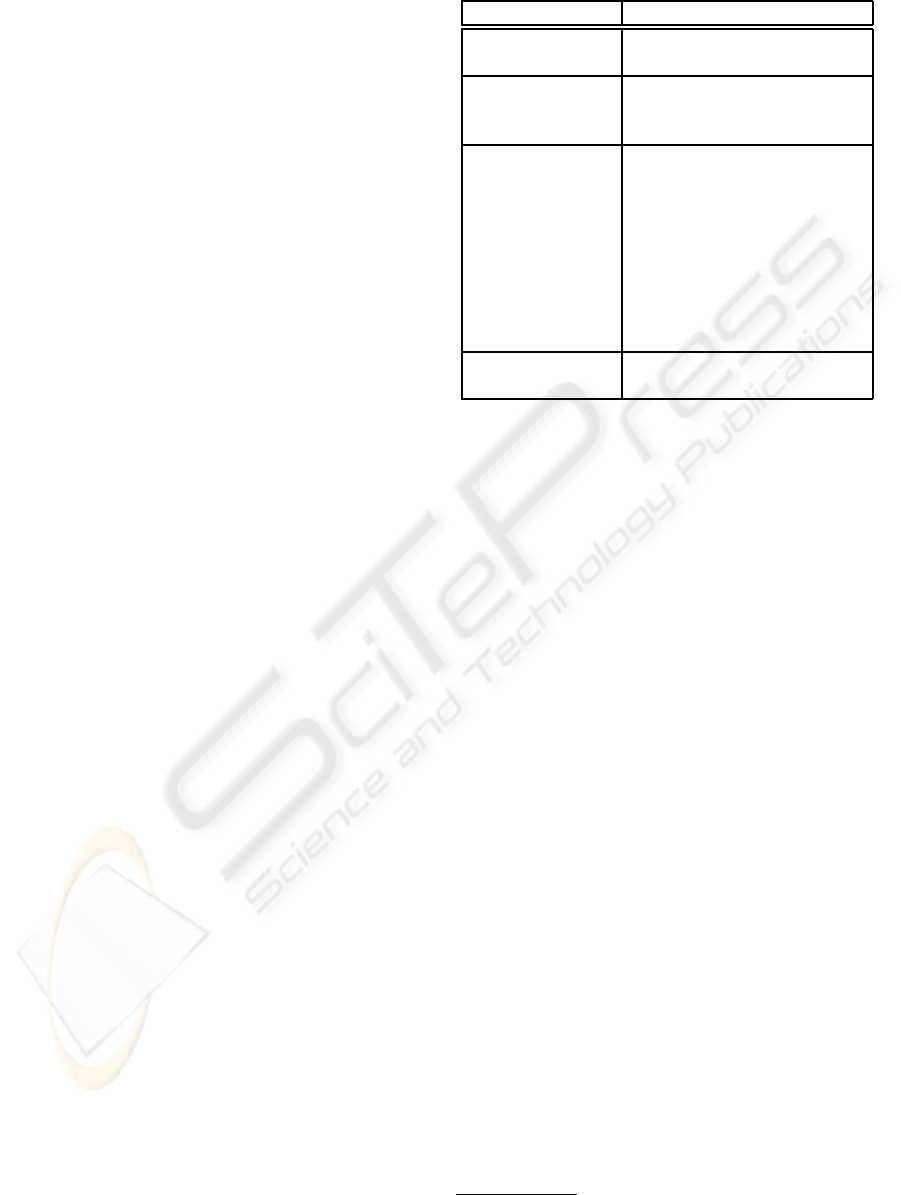

Table 1: Financial ratios used in our database.

Type Ratio

Liquidity ratio

Current ratio

Quick ratio

Debt ratio

Debt ratio

Long term debt common eq-

uity

Profitability ratio

Working capital per share

Operating margin before de-

preciation

Operating margin after de-

preciation

Pretax profit margin

Return on asset

Return on equity

Net profit margin

Market ratio

Price earning

Price to book

Table 1 shows all financial ratios used in our ex-

periments. They are divided into four categories and

are verified by financial experts as being able to de-

scribe the intrinsic status of a company at a given

time. The domain of the target attribute is {good(G),

average(A), bad(B)} showing the status of the com-

pany as based on its return.

4.2 Rule Generating

As discussed in Section 3, from each data set D(t) at

time point t, a set of classification rules RS(t) is gen-

erated, using the C4.5 decision tree learning method

(Quinlan, 1993). Each data set D(t) is trained using

J48 provided by WEKA

2

(Witten and Frank, 2005)

to generate a decision tree. From each decision tree,

a set of classification rules are obtained. The exper-

iments are conducted with the default configurations

in WEKA.

4.3 Top-k Evolutionary Trends

Prediction

As stated in Section 3.4, for each series of evolution-

ary operators generated from our top-k evolutionary

trends, a regression model is built. In our experi-

ments, we apply three popular supervised machine

learning methods

• Multi-nominal Logistic Regression (MNL)

• Multi-layered Perceptron Neural Network (MLP)

• Support Vector Machines (SVM)

2

http://www.cs.waikato.ac.nz/ml/weka/

ICEIS 2008 - International Conference on Enterprise Information Systems

24

We use the implementations of the above three algo-

rithms in WEKA with their default configurations.

Results of these experiments are shown in Table 2.

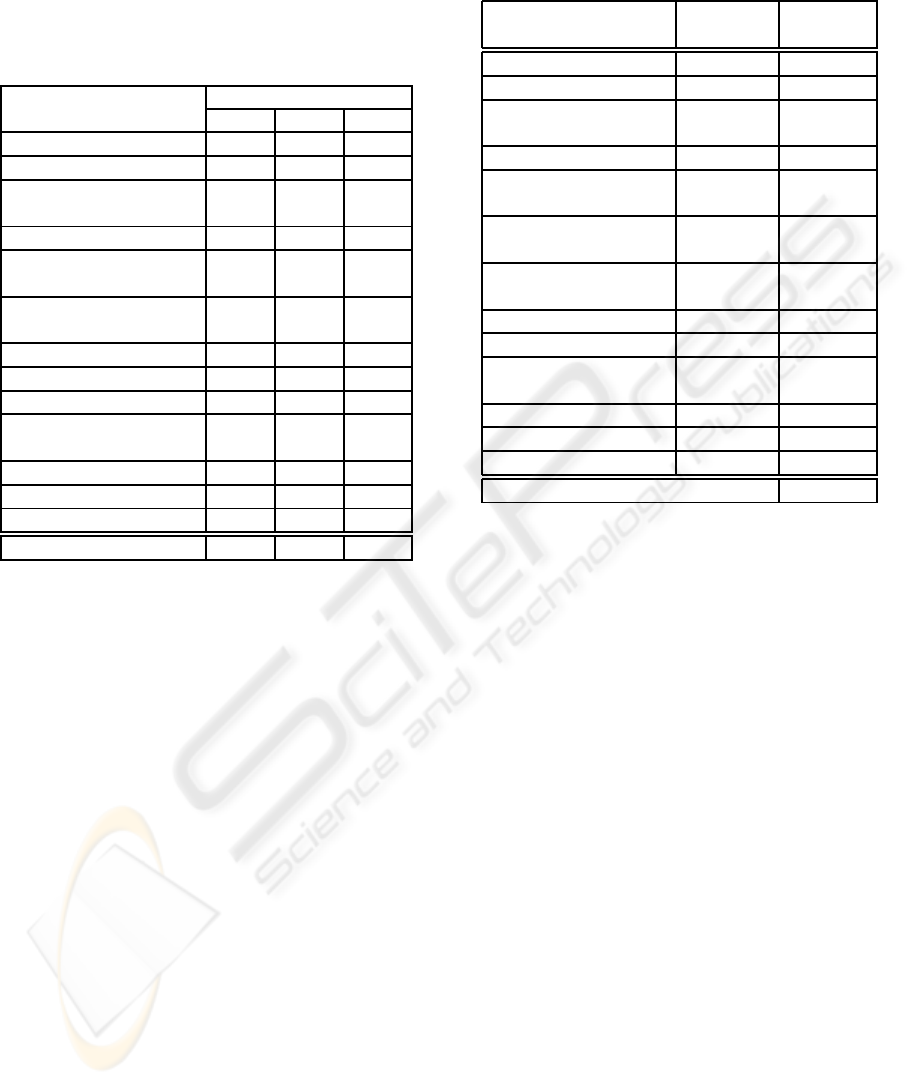

Table 2: Results of top-k evolutionary trends prediction

models using MNL, MLP and SVM.

Financial ratio Accuracy (%)

MNL MLP SVM

1. Current ratio 61.83 64.12 81.70

2. Quick ratio 73.58 84.38 76.62

3. Working capital per

share

83.51 76.26 67.91

4. Net profit margin 83.99 69.81 66.92

5. Operation margin

before depreciation

77.96 72.80 79.60

6. Operation margin

after depreciation

69.30 74.50 81.88

7. Pretax profit margin 76.37 79.54 76.39

8. Return on assets 74.87 65.92 78.96

9. Return on equity 76.46 64.35 66.40

10. Long term debt

common equity

73.94 81.87 81.76

11. Price earning 74.48 82.4 74.78

12. Price to book 73.27 75.36 77.29

13. Debt equity 78.49 70.00 72.83

Average 75.23 73.95 75.62

On each financial ratio, three models using three

above machine learning techniques are built. How-

ever, we observe that each technique achieves high

accuracy only on certain financial ratios but performs

badly on others. For example, SVM outperforms the

two other techniques on Current ratio (81.7%) and

Operation margin after depreciation (81.88%), but

suffers a poor accuracy of 66.4% on Return on eq-

uity. MLP has higher accuracy than the other two on

Quick ratio as well as Price earning. Although MNL

successfully models Net profit margin (83.99%) and

Working capital per share (83.51%), it has the low-

est accuracy on Current ratio (61.83%). That’s why

the overall accuracies of the three techniques MNL

(75.23%), MLP (73.95%) and SVM (75.62%) are rel-

atively low and approximately equal.

In order to have a more accurate and reliable

model, a combined model using three above tech-

niques is used. The combined model is built by choos-

ing the technique which has the highest accuracy for

each financial ratio. Table 3 shows the chosen learn-

ing techniques with their corresponding accuracy for

each financial ratio. As we can see, the overall ac-

curacy of the combined model increases to 80.77%,

which outperforms every individual model.

Table 3: Results of top-k evolutionary trends prediction

models using combined learning techniques.

Financial ratio Learning

technique

Accuracy

(%)

1. Current ratio SVM 81.70

2. Quick ratio MLP 84.38

3. Working capital

per share

MNL 83.51

4. Net profit margin MNL 83.99

5. Operation margin

before depreciation

SVM 79.60

6. Operation margin

after depreciation

SVM 81.88

7. Pretax profit mar-

gin

MLP 79.54

8. Return on assets SVM 78.96

9. Return on equity MNL 76.46

10. Long term debt

common equity

MLP 81.87

11. Price earning MLP 82.4

12. Price to book SVM 77.29

13. Debt equity MNL 78.49

Average 80.77

5 CONCLUSIONS

In this paper, we have proposed a new approach to

model and predict the behavior of target attributes in a

multi-attribute time series problem. In our approach,

the original problem of predicting future values of tar-

get attributes is transformed to a new equivalent prob-

lem of predicting the set of rules.

We have developed a framework to solve the

transformed problem based on the rule evolution

methodology. The framework consists of a prelimi-

nary step - data preprocessing and three main steps in-

cluding rule pruning - prune uninteresting rules, top-

k evolutionary trends mining - determine k most im-

portant evolutionary trends of every consecutive data

set, and top-k evolutionary trends prediction - pre-

dict the set of k most significant trends in the near

future. Each step of our framework can be accom-

plished by different individual as well as combined

learning techniques which makes it highly flexible

and configurable. The framework is validated on real

S&P 500 stock data to show its effectiveness and reli-

ability.

For future work, although the experimental results

are promising, many parts of the system framework

can be re-configured and extended. Each step of our

approach is flexible in term of choosing the method

to solve. For example, generating classification rules

RULE EVOLUTION APPROACH FOR MINING MULTIVARIATE TIME SERIES DATA

25

from each data set at each time point can be done by

other supervised machine learning techniques. In the

rule pruning step, different dissimilarity measurement

can be used to achieve different sets of rules. Or in

the evolutionary trends predicting step, other regres-

sion techniques can be applied to compare with the

existing results. We are also interested in applying

our system to other databases which have the same

properties to test its correctness and effectiveness.

ACKNOWLEDGEMENTS

Viet An’s work has been supported by the Undergrad-

uate Research Experience on Campus (URECA) pro-

gramme from Nanyang Technological University.

REFERENCES

Breiman, L., Friedman, J., Olshen, R., and Stone, C. (1984).

Classification and regression trees. Chapman and

Hall, New York, 368 p.

Cendrowska, J. (1987). Prism: An algorithm for inducing

modular rules. International Journal of Man-Machine

Studies, 27(4):349–370.

Geng, L. and Hamilton, H. J. (2006). Interestingness mea-

sures for data mining: A survey. ACM Computing

Survey, 38(3):9.

Hetland, M. and Saetrom, P. (2002). Temporal rule discov-

ery using genetic programming and specialized hard-

ware. In 4th International Conference on Recent Ad-

vances in Soft Computing, RASC.

Holte, R. (1993). Very simple classification rules per-

form well on most commonly used datasets. Machine

Learning, 11:63–91.

Kadous, M. W. (1999). Learning comprehensible descrip-

tions of multivariate time series. In ICML, pages 454–

463.

Keogh, E. and Kasetty, S. (2002). On the need for time

series data mining benchmarks: a survey and em-

pirical demonstration. In KDD ’02: Proceedings of

the eighth ACM SIGKDD international conference on

Knowledge discovery and data mining, pages 102–

111, New York, NY, USA. ACM.

Kohavi, R. (1995). The power of decision tables. In 8th Eu-

ropean Conference on Machine Learning, pages 174–

189. Springer.

Last, M., Kandel, A., and Bunke, H. (2004). Data Mining in

Time series databases. Series in Machine Perception

and Artificial Intelligence. World Scientific.

Last, M., Klein, Y., and Kandel, A. (2001). Knowledge

discovery in time series databases. IEEE Transactions

on Systems, Man, and Cybernetics, Part B, 31(1):160–

169.

Povinelli, P. (2000). Using genetic algorithms to find tem-

poral patterns indicative of time series events. In

GECCO 2000 Workshop: Data Mining with Evolu-

tionary Algorithsm, pages 80–84.

Quinlan, J. R. (1986). Induction of decision trees. Machine

Learning, 1(1):81–106.

Quinlan, J. R. (1993). C4.5: Programs for machine learn-

ing. Morgan Kaufmann Publishers Inc.

Su, J. and Zhang, H. (2006). A fast decision tree learn-

ing algorithm. In Proceedings of The Twenty-First

National Conference on Artificial Intelligence and the

Eighteenth Innovative Applications of Artificial Intel-

ligence Conference (AAAI/IAAI), July 16-20, 2006,

Boston, Massachusetts, USA.

Tan, P.-N., Kumar, V., and Srivastava, J. (2002). Selecting

the right interestingness measure for association pat-

terns. In KDD ’02: Proceedings of the eighth ACM

SIGKDD international conference on Knowledge dis-

covery and data mining, pages 32–41, New York, NY,

USA. ACM.

Tukey, J. W. (1977). Exploratory Data Analysis. Addison-

Wesley, Reading, MA.

Wah, B. W. and Qian, M. (2002). Constrained formula-

tions and algorithms for stock-price predictions using

recurrent FIR neural networks. In Proceedings of The

Twenty-First National Conference on Artificial Intel-

ligence and the Eighteenth Innovative Applications of

Artificial Intelligence Conference (AAAI/IAAI), pages

211–216, Edmonton, Alberta, Canada.

Wei, L., Kumar, N., Lolla, V. N., Keogh, E. J., Lonardi, S.,

Ratanamahatana, C. A., and Herle, H. V. (2005). A

practical tool for visualizing and data mining medical

time series. In CBMS, pages 341–346.

Weiss, G. and Hirsh, H. (1998). Learning to predict rare

events in event sequences. In 4th Conference on

Knowledge Discovery and Data Mining KDD, pages

359–363, Menlo Park, CA, USA. AAAI Press.

Witten, I. H. and Frank, E. (2005). Data Mining: Practi-

cal Machine Learning Tools and Techniques. Morgan

Kaufmann Series in Data Management Systems. Mor-

gan Kaufmann, second edition.

ICEIS 2008 - International Conference on Enterprise Information Systems

26