A MODEL FOR IMPROVING ENTERPRISE’S PERFORMANCE

BASED ON COLLABORATIVE E-LEARNING

Camelia Delcea

Department of Cybernetics, University of Economics, Bucharest, Romania

Maria Dascălu, Cristian Ciurea

Department of Informatics,University of Economics, Bucharest, Romania

Keywords: Collaborative e-Learning, Enterprise’s Performance, Grey Systems Theory, Fuzzy Sets Theory.

Abstract: Collaborative learning and e-learning are believed to be very important to the success of enterprises. Some

qualitative and quantitative variables that characterises collaborative learning through e-learning are

depicted. The incidence degree between them and enterprise’s performance was determined through a

model. Also, the difference between enterprise’s financial and non-financial performance was underlined.

The proposed model is constructed using the facilities offered by grey systems and ϕ-fuzzy sub-set theory.

For better understand the model, we used it on two branches of the same bank. We conclude our paper by

presenting and comparing the obtained results and by giving some future work guidelines.

1 INTRODUCTION

The economic context in which firms carry out their

activities is dynamic and constantly changing.

(Delcea & Scarlat, 2009)

By identifying changes and anticipating them,

firms can take decisions to compensate or eliminate

any negative effects and leverage the positive

effects, thus facilitating the achievement of the

firm’s goals.

Also, as Nonaka pointed out, in an economy

where the only certainty is uncertainty, the one

source of lasting competitive advantage is

knowledge (Nonaka, 1991).

From this point of view, an organization that

fails to learn may be sub-optimal or even

dysfunctional (Law & Ngai, 2008).

As Slater and Narver (1995) argue, an enterprise

with a continuous tendency of learning has a better

chance to respond to customer needs, to sense the

market opportunities and to offer more appropriate

and more finely targeted products, all these leading

the enterprise to superior levels of profitability, sales

growth and customer retention.

Over the years, all the traditional learning

techniques were revised and new ones were

introduced. Internet-oriented applications and e-

learning were the revolutionary new ways through

which the workforce got the necessary needed skills

and knowledge (Tzouveli, Mylonas, & Kollias,

2008).

In an enterprise, partners may accumulate

substantial experience and lessons through learning

from each other. Some theoretical and practical

learning related to how to avoid repetitious mistakes,

how to reduce production and transaction costs, and

how to enhance the capacity of mutual

understanding, coordination, and problem solving

can be acquired by partners’ interaction (Jiang & Li,

2008) . Sometimes, when partners are faced with a

physical distance, this collaborative interaction can

be done only through computer, mainly by

discussion forums and teleconference.

Depending on enterprise’s strategy, some

components of collaborative learning through e-

learning can be identified.

Our purpose is to identify the qualitative

variables that characterise best the collaborative

learning from the point of view of e-learning and

how these components are influencing enterprise’s

performance.

We will also analyse the enterprise performance

from two directions. The first one is given by the

5

Delcea C., Dasc

ˇ

alu M. and Ciurea C. (2010).

A MODEL FOR IMPROVING ENTERPRISE’S PERFORMANCE BASED ON COLLABORATIVE E-LEARNING.

In Proceedings of the 12th International Conference on Enterprise Information Systems - Human-Computer Interaction, pages 5-12

DOI: 10.5220/0002864600050012

Copyright

c

SciTePress

accountants’ point of view, related to the financial

perspective, while the second one is coming from

the managerial point of view.

Based on the idea that each firm is different from

another, we proposed a single firm model that will

help the managers to decide which component of

collaborative learning they should improve on their

enterprises based on their purpose. For this reason

the qualitative variables taken into account will be

ordered using grey systems theory and ϕ-fuzzy sub-

set theory as we shall see in the following.

2 COLLABORATIVE LEARNING

THROUGH E-LEARNING IN

ENTERPRISES

Over the past years, work becomes more

interdisciplinary, complicated and nevertheless

knowledge-based. In this sophisticated environment,

in which enterprises carry out their activity, e-

learning succeeded through the different interaction

tools to offer ample opportunities for learners to

collaborate with peers, experts, professionals or with

other learners.

The evolution of knowledge-based society

involves the development of enterprises through a

collaborative learning environment. Collaboration is

an important dimension when it comes to sharing

and integrating the experiences and training courses

of different groups of learners. Supervisors,

instructors, and learners from enterprises play

different roles in the learning process. They need to

work in the same environment, collaboratively

instead of individually, to perform an adaptive

learning strategy. (Yi, Schwaninger, & Gall, 2008)

In an enterprise, the use of collaborative learning

can develop higher level thinking skills, social

interaction skills, responsibility for each other and

even promote higher achievement. (Chang & Lee,

2009)

Interaction between learners is indispensable to

collaborative learning, and learners need to do real

work together in which they promote each other's

success by sharing resources, discussing, helping,

and congratulating each other's efforts to achieve.

(Wu, Zhengbing, Yang, & Liu, 2009)

The collaborative learning process from an

enterprise may be achieved through a virtual campus

or an intranet e-learning platform. The intranet

collaborative learning system should focus on how

to instruct and stimulate learners to achieve

knowledge, and the system is to visualize traditional

classroom education and learning environment in

web. (Xiuhua & Wenfa, 2008)

The intranet collaborative learning system is a

virtual organizational structure of collaborative type

in which interact three target groups:

The target group of learners, composed by

participants in tele-activities of training, testing,

documentation, participation in online meetings,

forums communication;

The target group of teachers who complete

multimedia teaching materials for virtual

campus training, evaluates papers submitted

online, update databases proper evaluations;

The target group of people outside the system,

which informs about the performance on

collaborative learning system and which allows

the selection on learners by interact and

conveying the information. (Ciurea, 2009)

Related to the idea of collaboration through

virtual knowledge spaces some systems have been

developed that insure more flexible mechanisms to

foster communication and cooperation in learning

and work processes. (Eßmann, Gotz, & Hampel,

2006)

Based on recent researches, some quantitative

and qualitative characteristics regarding the

collaborative learning through e-learning can be

identified, with a peculiar impact on enterprise’s

performance.

Some of qualitative characteristics related to the

knowledge acquisition (at individual, group and

enterprise level) and learning flow (exploration and

exploitation) are listed in the following: (Kreijns,

Kirschner, & Jochems, 2003) (Baker & Sinkula,

1999), (Prieto & Revilla, 2006) (Bodea & Dascalu,

2009)

The degree of group cohesion gained through

collaborative learning;

The development of critical thinking, shared

understanding, and long term retention of the

learned material;

The capability of the collaborative learners to

resolve effectively the conflicts;

The capacity of sharing successes and failures

within the collaborative group;

The degree of confidence and responsibility felt

by individuals about doing their work;

The degree to which the quality of the

enterprise’s market-oriented behaviours are

improved by collaborative learning through e-

learning;

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

6

The quality of enterprise’s learning structure

that allows working effectively;

The quality of internal training and work

training through collaborative e-learning

provided within the organization;

The development of social and

communicational skills;

The degree to which the collaborative learning

through e-learning enables the development of

competencies and skills for working properly.

From the quantitative point of view, we can

identify the following variables:

The number of qualifications that the

employees are getting in an year period;

The number of employees that are using

collaborative learning through e-learning in

enterprise;

Collaborative learning group size;

The number of training sessions that the

enterprise is financing in a year period.

All these variables and other more that can be

identified at enterprise’s level can be analysed and

ranked based on their influence on enterprise’s

financial and non-financial performance, as we shall

see in the following sections.

3 FINANCIAL AND

NON-FINANCIAL

PERFORMANCE MEASURE

The importance and the impact of organizational

learning or learning orientation on financial and non-

financial performance have been recognized in the

research literature related to this field many years

ago. (Jiang & Li, 2008)

The financial performance of an enterprise can

be measured through several indicators: sales

growth, increase in overall profitability, increase in

sales resulting from new products, improvement in

work productivity, improvement in production cost,

enterprise’s market share, defect rates, earnings per

share (EPS), return on assets (ROA), return on

investment (ROI), net income after tax (NIAT) and

other more, depending on the enterprise’s goals.

As for the non-financial performance, even it has

no intrinsic value for companies’ directors, it can be

used as a leading indicator of financial performance,

especially for future financial performance that is

not yet contained in the accounting measures. (Prieto

& Revilla, 2006)

Through the indicators that are measuring the

non-financial performance we can firstly identify the

customers’ satisfaction, expressed qualitatively by

the degree of satisfaction felt by customers or

numerically by the average number of satisfied

customers or by the number of customers whose

level of satisfaction exceeds a certain level.

Knowing that satisfied customers are more likely to

buy a greater volume of enterprise’s products or

services, or even to recommend those

products/services to other potentially customers, the

cost of attracting new customers is lower, the failure

costs are reduced and the financial performance is

increased.

Another performance indicator, non-financial by

its nature, can be enterprise’s reputation. Having a

high reputation, an enterprise can easily introduce

new products and services, by reducing the buyer’s

risk of trial. (Anderson, Fornell, & Lehman, 1994)

Also, a good reputation can lead to a good

maintenance of the relationships with key suppliers,

distributors and potential allies. (Anderson, Fornell,

& Lehman, 1994)

Without expanding, other variables that succeed

in measuring non-financial performance can be

taken into account: employee satisfaction or morale,

employee efficiency, quality of products and

services, growth of number of customers, on-time

delivery, long term relation with suppliers and

customers response time.

Even the enterprise’s management is giving a

higher importance to the financial performance, the

non-financial performance is also extremely

important by the fact that it leads to the achievement

of a better financial performance, through a higher

reduction of production costs, an increasing in

productivity, an improving the yield or reducing the

material consumption and nevertheless a higher

level of sales growth over time.

Because all the two components of enterprise’s

performance are important, in the proposed model

we will analyse the impact that collaborative

learning through e-learning has on both financial and

non-financial performance.

4 THE RESEARCH MODEL

The model proposed in this paper is a hybrid one,

obtained by fusion between grey systems theory and

fuzzy theory. While fuzzy theory has the methods

A MODEL FOR IMPROVING ENTERPRISE'S PERFORMANCE BASED ON COLLABORATIVE E-LEARNING

7

and techniques for treating the quantitative variables,

but especially the qualitative ones, grey systems

theory manages to achieve good performance in

analysis conducted on a small range of data and on a

large number of variables.

4.1 Preparation

In this section we will present some definitions and

formula related to grey arithmetic and grey

incidence which we will use in the proposed model.

4.1.1 Grey Systems Theory Arithmetic

Definition: A grey number is a number whose exact

value is unknown but a range within the value lies is

known. (Liu & Lin, 2005)

In applications, a grey number in general is an

interval or a general set of numbers.

Assume that

1

⊗

and

2

⊗

are two grey numbers,

defined as follows:

baba <∈⊗ ],,[

1

and dcdc <

∈

⊗ ],,[

2

The following operations between them can be

done (Liu & Lin, 2005):

Sum:

],[

21

dbca +

+

∈⊗+⊗

(1)

Difference:

],[)(

2121

cbda −−∈⊗−+⊗=⊗−⊗

(2)

Reciprocal: The reciprocal of

],[

1

ba∈⊗

with

ba <

and

0>ab

, noted

1

1

−

⊗

is defined as:

]

1

,

1

[

1

1

ab

∈⊗

−

(3)

Product:

}],,,max{

},,,,[min{

21

bdbcadac

bdbcadac∈⊗•⊗

(4)

Quotient:

1

21

2

1

−

⊗•⊗=

⊗

⊗

(5)

Scalar multiplication: Assume that k is a

positive real number, the scalar multiplication

of k and

1

⊗

is defined as follows:

],[

1

kbkak ∈⊗•

(6)

Theorem: Interval grey numbers cannot in

general be cancelled additively or multiplicatively.

More specifically, the difference of any two grey

numbers is generally not zero, except in the case that

they are identical. And the division of any two grey

numbers is generally not 1 except in the case when

they are identical. (Liu & Lin, 2005)

4.1.2 Relative Degree of Grey Incidence

From the grey systems theory (Liu & Lin, 2005) we

will use in this paper only de items related to the

construction of the relative degree of grey incidence

and its calculation.

Assume that X

0

and X

j

, j=1...n, are two

sequences of data with non-zero initial values and

with the same length, with t = time period and n =

variables:

),,,,,,(

0,0,40,30,20,10 t

xxxxxX …=

(7)

),,,,,,(

,

,4,3,2,1

jt

jjjj

j

xxxxxX …=

(8)

The initial values images of X

0

and X

j

are:

),,,(),,,(

0,1

0,

0,1

0,2

0,1

0,1

'

0,

'

0,2

'

0,1

'

0

x

x

x

x

x

x

xxxX

t

t

…… ==

(9)

),,,(),,,(

,1

,

,1

,2

,1

,1

'

,

'

,2

'

,1

'

j

jt

j

j

j

j

jtjjj

x

x

x

x

x

x

xxxX …… ==

(10)

The images of zero-start points calculated based

on (3) and (4) for X

0

and X

j

are:

),,,(

),,,(

0'

0,

0'

0,2

0'

0,1

0,1

'

0,

'

0,1

'

0,2

'

0,1

'

0,1

''0

0

t

t

xxx

xxxxxxX

…

…

=

−−−=

(11)

),,,(

),,,(

0'

,

0'

,2

0'

,1

,1

'

,

'

,1

'

,2

'

,1

'

,1

''0

jtjj

j

jt

jjjj

j

xxx

xxxxxxX

…

…

=

−−−=

(12)

The relative degree of grey incidence is given by:

jj

j

j

ssss

ss

r

'

0

'''

0

'

0

'

0

1

1

−+++

++

=

(13)

where

0

'

s and

j

s

'

are computed as follows:

∑

−

=

+=

1

2

0'

0,

0'

0,

0

'

2

1

t

k

tk

xxs

(14)

∑

−

=

+=

1

2

0'

,

0'

,

'

2

1

t

k

jtjk

j

xxs

(15)

The relative degree of grey incidence represents

a numeric characteristic for the relationship of

closeness between the two sequences.

In practical numerical examples, the numerous

degree of grey incidence developed in the literature

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

8

were used to measure the incidence between two

quantitative variables. In our paper, we include some

qualitative variables related to collaborative learning

and we try to determine their influence on enterprise

performance. For a better work with qualitative

variables we will use some “expertons” built as it

can be seen from the following section.

4.1.3 Expertons

Fuzzy logic offers the suitable tools for the treatment

of uncertainty and subjectivity. Because in our

model, we will work with qualitative variables, we

will use the ϕ-fuzzy sub-set theory and some

exertons.

The main characteristic of fuzzy sub-sets is that

the function characteristic of membership is taking

its values from [0; 1] instead of {0; 1}. For a better

representation of reality, we will consider that those

values are intervals and not numbers, situated in [0;

1]. (Gil-Lafuente, 2005)

Once with the idea of ϕ-fuzzy sub-set comes

even the idea that the opinion of a single expert is

being insufficient. That is the reason why it is

preferred to gather several experts’ opinion and even

to construct an experton.

Expertons are in fact intervals built using the ϕ-

fuzzy sub-set and the opinion of several experts over

a certain problem. For a complete reading on how

these expertons are built, see (Gil-Lafuente, 2005).

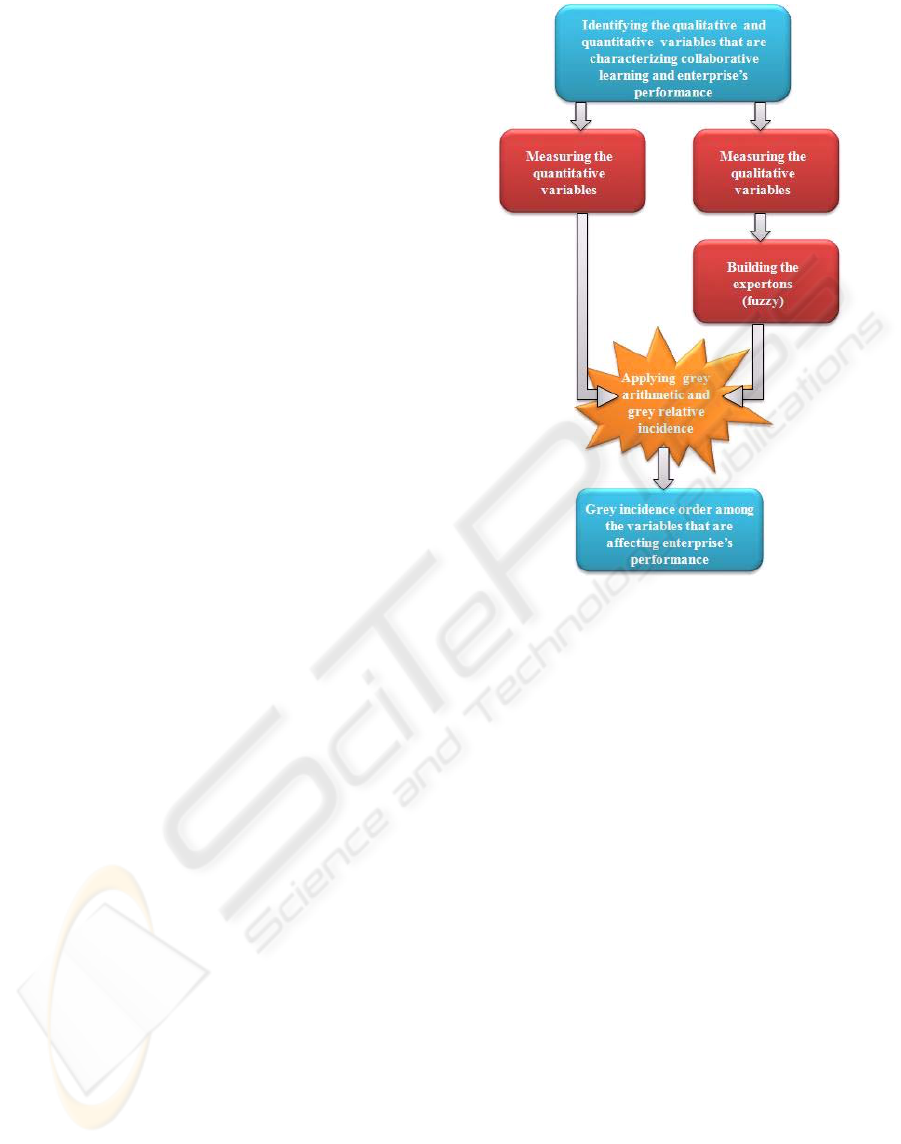

4.2 The Research Model

The proposed model combines the advantages

offered by grey systems theory and ϕ-fuzzy sub-set.

Figure 1 summarises the steps involved.

We shall mention that in first stage of the model

construction we will use some experts for the

selection of the collaborative e-learning variables

that are the most important at enterprise’s level.

Also, the team of experts will establish the

performance indicators that will be measured and

used, one for the financial performance and another

one for the non-financial performance. Depending

on the manager’s will, it can be taken into account

only the performance or only the non-performance

indicator.

In the next step, the quantitative variables,

including the quantitative performance indicators are

measured. In some cases, enterprise’s financial

statement or other enterprise’s documents can be

used.

The qualitative variables are also measured. For

this, each expert from the team will give his opinion

Figure 1: The proposed model.

on the values of qualitative variables through a

number or an interval between 0 and 1 in the

following manner: if an expert is absolutely sure

about the level of the considered variable, he will

note that value through a number; otherwise, he will

record an interval. Also, if the expert has no clue

about the values among which the variable can be

found, he will simply record the whole [0; 1]

interval.

After gathering all experts’ opinions, an experton

will be build for each variable.

Having all the variables measured, we will apply

the grey arithmetic on intervals presented at 4.1.1 to

the relative degree of grey incidence.

By computing, the collaborative e-learning

variables taken into account are ordered based on the

value of the relative degree of grey incidence.

Acting on them, the financial and the non-financial

situation of a company can be improved.

5 REAL NUMERICAL

APPLICATION

In period July 2008 – October 2009 we conducted a

study on two branches of Raiffeisen bank. Our

A MODEL FOR IMPROVING ENTERPRISE'S PERFORMANCE BASED ON COLLABORATIVE E-LEARNING

9

purpose was to detect which of the qualitative or

quantitative characteristics of collaborative

e-learning through learning identified in the two

branches are influencing the performance of each of

them. By comparing the findings we can establish

some similarities and some differences as we will

see further.

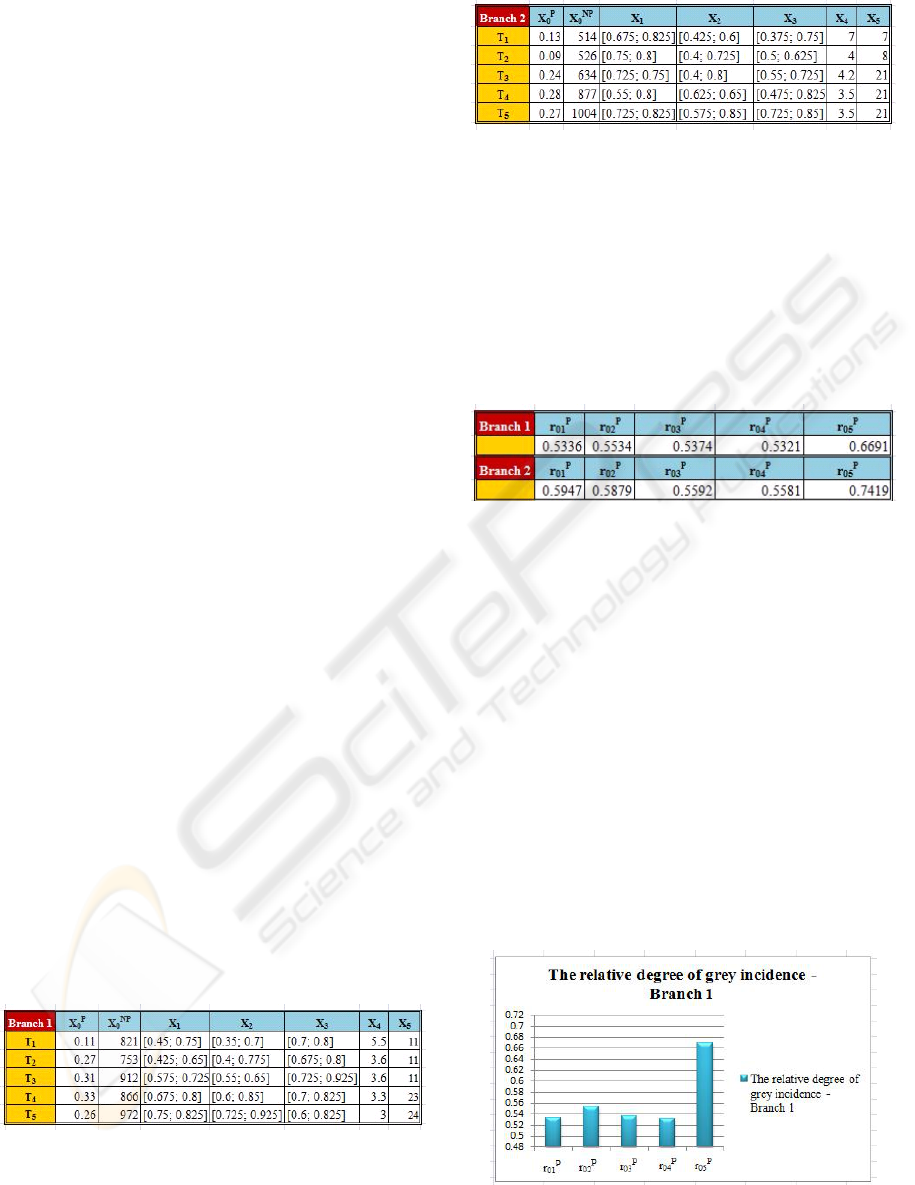

For this purpose, a number of four specialists in

the field helped us. Based on the interviews with the

managers of the two branches we established the

performance indicators. For the financial

performance we measured the sales growth (noted

X

0

P

), while for the non-financial performance: the

average number of satisfied customers (X

0

NP

). The

period of time of almost 15 month was divided into

five equal periods, each of them having three

months.

The qualitative and quantitative characteristics

identified related to the knowledge acquisition and

learning flow that are gained through the

collaborative learning held in the branches’ that are

more appropriate to influence their performance are

listed below: the development of social and

communicational skills (X

1

), the increase of

competences as a result of the collaborative learning

process made through e-learning (X

2

), the

development of critical thinking, shared

understanding and long term retention of the learned

material (X

3

), the average size of collaborative

learning group (X

4

) and the number of employees

that are using collaborative learning through e-

learning (X

5

).

For the qualitative variables (X

1

, X

2

and X

3

),

whose values were expressed by each one of the four

experts through intervals or numbers between 0 and

1, we have built three expertons for each branch.

The values of all the variables, including the

expertons, were gathered in two tables as they can

be seen in Figure 2 and Figure 3.

Next, we apply the relative degree of grey

incidence. In the qualitative variables case,

expressed through expertons, we will use some grey

arithmetic on intervals presented at 4.1.1.

Figure 2: The values of performance indicators and

qualitative and quantitative variables collected at Branch

1.

Figure 3: The values of performance indicators and

qualitative and quantitative variables collected at Branch

2.

After computing, the following results were

found. Figure 4 summarizes the values of the

relative degree of grey incidence for the case when

we are interested on financial performance, while

Figure 7 summarizes the values of the relative

degree of grey incidence for the case of non-

financial performance.

Figure 4: The values of the relative degree of grey

incidence on financial performance obtained in the two

branches.

For the first branch, from r

05

P

> r

02

P

> r

03

P

> r

01

P

>

r

04

P

it can be seen that

41325

XXXXX .

This is equivalent to say that the most influencing

factor in this case is the number of employees that

are using collaborative e-learning, while the factor

with the less influence is the average size of the

collaborative learning group. As for the second

branch, it can easily be seen that the factor with the

most and the less influence remains the same, with

the only difference that the order of the qualitative

factors is

321

XXX .

Graphically the values obtained in the two

branches cases are represented in Figure 5 and

Figure 6 below:

Figure 5: The values of the relative degree of grey

incidence for each variable on financial performance

indicator - Branch 1.

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

10

Figure 6: The values of the relative degree of grey

incidence for each variable on financial performance

indicator - Branch 2.

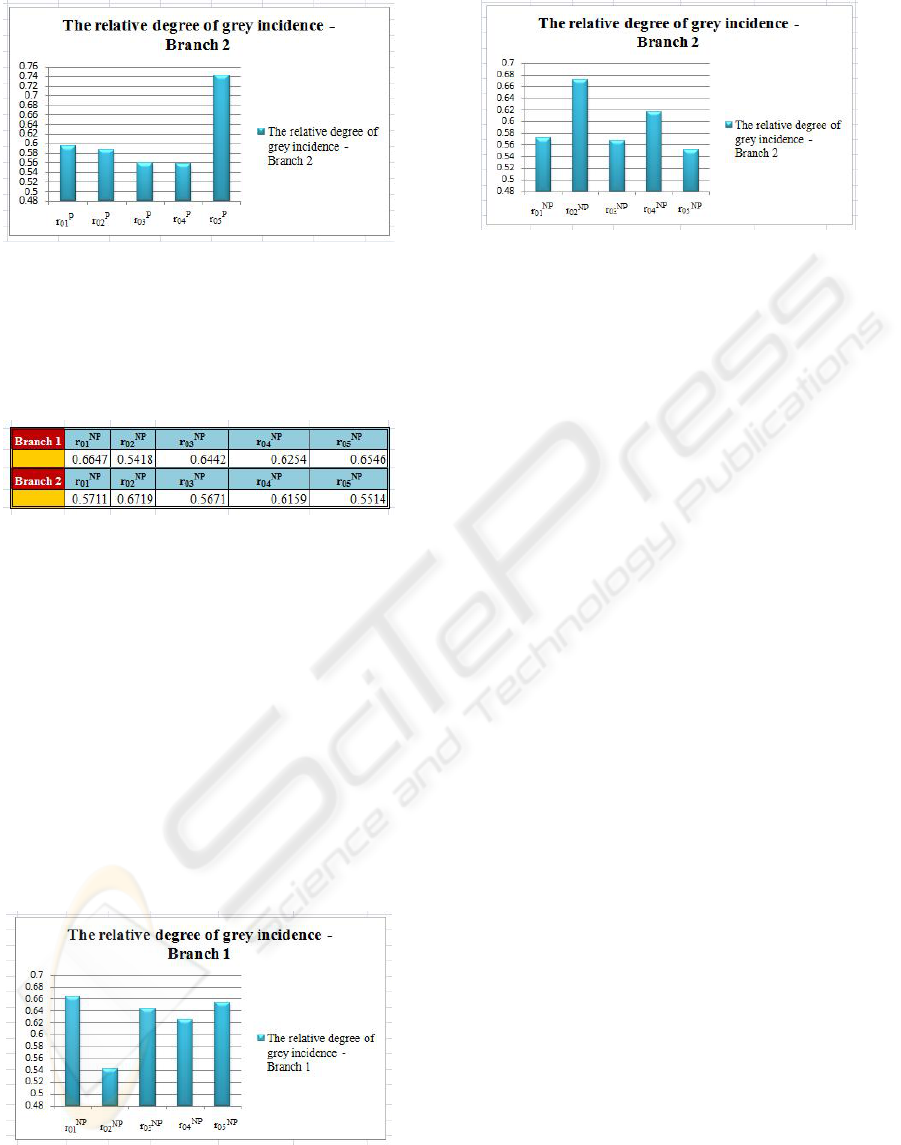

For the non-financial performance case, the

values of the relative degree of grey incidence are

presented in the following figure:

Figure 7: The values of the relative degree of grey

incidence on non-financial performance obtained in the

two branches.

In the case of non-financial performance, the

order of the variables identified at first branch’s

level according to their relative degree of grey

incidence is:

24351

XXXXX . That is

equivalent to say that the average number of

satisfied customers depends most on the

development of social and communicational skills of

the employees. For the second branch, the increase

of competences as a result of collaborative learning

process is the most influencing variable on non-

financial performance, followed by X

4

, X

1

, X

3

and

X

5

. This can also be seen from Figure 8 and 9.

Figure 8: The values of the relative degree of grey

incidence for each variable on non-financial performance

indicator - Branch 1.

Figure 9: The values of the relative degree of grey

incidence for each variable on non-financial performance

indicator - Branch 2.

6 CONCLUSIONS

In the analize of enterprise’s performance a peculiar

attention should be given to the variables that are

influencing it. From this cathegory, the variables that

undeline the level of collaborative e-learning

represent an important cathegory.

Starting from idea that each enterpise is unique,

we propose a single-enterprise model, built using

grey systems theory and ϕ-fuzzy sub-set theory.

By simulating the model on the data collected in

the two branches, it was easy to see that the results

obtained in the two cases were different. From this

point, based on each manager’s purpose, the

manager can decide whether to act on the variables

that are influencing financial or to the ones that are

influencing the non-financial performance. For our

numerical example, in the first branch case, if the

manager wants to improve the financial

performance, he/she should try to increase primary

the number of the employees which are using the

collaborative e-learning by offering the possibility of

studying through intra/internet and through

collaboration to a large number of employees. Or,

contrary, if the non-financial performance is aimed,

the manager should concentrate on the

communicational skills, which can be acquired

through some training sessions.

The research can be extended to include facilities

offered by other theories, such as case based

reasoning, which is similar to the human way of

thinking. Also, a soft procedure can be created in

order to aggregate easier the identified variables and

the experts’ opinions. In order to bring future

improvement to the proposed model, the number of

variables can be extended by taking into account

other variables unrelated to the collaborative e-

learning.

A MODEL FOR IMPROVING ENTERPRISE'S PERFORMANCE BASED ON COLLABORATIVE E-LEARNING

11

ACKNOWLEDGEMENTS

This article is a result of the project „Doctoral

Program and PhD Students in the education research

and innovation triangle”. This project is co funded

by European Social Fund through The Sectorial

Operational Program for Human Resources

Development 2007-2013, coordinated by The

Bucharest University of Economics.

REFERENCES

Anderson, E., Fornell, C., & Lehman, D. (1994).

Customer Satisfaction, Market Share, and

Profitability: Findings from Sweden. Journl of

marketing .

Baker, W., & Sinkula, J. (1999). The Synergistic Effect of

Market Orientation and Learning Orientation on

Organizational Performance. Journal of the Academy

of Market Science , 411-427.

Bodea, C. N., & Dascalu, M. I. (2009). Designing Project

Management Tests on Semantic Nets and Concept

Space Graph. The 12th International Business

Information Managemnet Association Conference,

(pp. 1232-1236). Kuala Lumpur.

Chang, C.-K., & Lee, C.-S. (2009). Using Computer-

Assisted Test to Harmlessly Improve the Efficiency of

Heterogeneous Grouping in Collaborative Learning.

International Conference on Advanced Computer

Control, (pp. 129-133).

Ciurea, C. (2009). A Metrics Approach for Collaborative

Systems. Informatica Economica Journal , 41-49.

Delcea, C., & Scarlat, E. (2009). The Diagnosis of Firm's

"Disease" Using the Grey Systems Theory Methods.

IEEE Grey Systems and Intelligent Services, (pp. 755-

762). Nanjing, China.

Eßmann, B., Gotz, F., & Hampel, T. (2006). Collaborative

Visualisation in Rich Media Environments. Enterprise

Information Systems, 8

th

International Conference,

ICEIS, (pp. 375-387). Paphos, Cyprus

Gil-Lafuente, A. M. (2005). Fuzzy Logic in Financial

Analysis. Berlin Heidelberg New-York: Springer.

Jiang, X., & Li, Y. (2008). The relationship between

organiyational learning and firms' financial

performance in strategic alliance: A contingency

approach. Journal of World Business , 365-379.

Kreijns, K., Kirschner, P., & Jochems, W. (2003).

Indentifying the pitfalls for social interaction in

computer-supported collaborative learning

environments: a review of the research. Computers in

Human Behaviour , 335-353.

Law, C., & Ngai, E. (2008). An empirical study of the

effects of knowledge sharing and learning behaviours

on firm performance. Expert Systems with

Applications , 2342-2349.

Liu, S., & Lin, Y. (2005). Grey Information. Theory and

Practical Applications. London: Springer-Verlang.

Nonaka, I. (1991) The knowledge creating company,

Harward Business Review 69, 96-104.

Prieto, I., & Revilla, E. (2006). Learning Capability and

Business Performance: a Non-financial and Financial

Assessment. The Learning Organization.

Slater, S., & Narver, J. (1995). Market orientation and the

learning organization. Journal of Marketing, 63-74

Tzouveli, P., Mylonas, P., & Kollias, S. (2008). An

intelligent e-learning system based on learner profiling

and learning resources adaptation. Computers &

Education , 224-238.

Wu, J., Zhengbing, H., Yang, Z., & Liu, Y. (2009). Design

of Collaborative Learning in Cyber-Schools. First

international Workshop on DatabaseTechnology and

Applications, (pp. 703-706).

Xiuhua, H., & Wenfa, H. (2008). An Innovative Web-

Based Collaborative Learning Model and Application

Structure. International Conference on Computer

Science and SOftware Engeneering.

Yi, G., Schwaninger, A., & Gall, H. (2008). An

Architecture for an Adaptive Collaborative Learning

Management System in Aviation Security. 17th IEEE

Workshop on Enabling Technologies: Infrastructure

for Collaborative Enterpises, (pp. 165-170).

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

12