AN INNOVATIVE GA OPTIMIZED INVESTMENT STRATEGY

BASED ON A NEW TECHNICAL INDICATOR USING

MULTIPLE MAS

Adriano Simões, Rui Neves and Nuno Horta

Instituto das Telecomunicações, Instituto Superior Técnico, Av. Rovisco Pais 1, 1040-001 Lisboa, Portugal

Keywords: Optimization, Technical Analysis, Evolutionary Algorithms, Financial Analysis, Moving Average, Stocks.

Abstract: This paper proposes a new medium/long term investment strategy for stock markets based on a combination

of Simple Moving Averages Crossover (SMAC) and Moving Average Derivate (MAD). This strategy is

compared with the Buy and Hold, with the Moving Averages Crossover, and with the Moving Average

Derivate strategy. The experiments show that the combination of SMAC and MAD outperforms the results

of each strategy individually. The presented approach has an average return of investment of 9.0%,

compared with the 2.6% return of the Buy and Hold, for the S&P500, FTSE100, DAX30 and NIKKEI225,

between 2004 and 2009.

1 INTRODUCTION

The study of profitable trading rules in the stock

market constitutes a widely known problematic in

financial markets, although the existence of those

rules still generate great controversy for many

economists and academics (Fama, 1998). On the

other hand, investor, traders, and other stakeholders

of financial and investment firms, with large

experience in the stock market, claim that it is

possible to have excessive returns (compared with

the Buy and Hold) using algorithmic trading

(Bodas-Sagi, 2009) (Chan, 2009).

One investment technique commonly used is

Technical Analysis, which forecasts the price of

stocks based only on the price of the stock and the

volume traded in the past. Momentum strategies

based on the continuation in the evolution of a stock

price on their recent history (Jegadeesh & Titman,

1993), have proved to be consistently more

profitable than the indexes where those stocks were

included. The foundation of Technical Analysis is

the Dow Theory, written by Charles Dow, founder

of Wall Street Journal where the main ideas of the

Dow Theory where published (Kaufman, 2005)

(Kirkpatrick, 2009).

Genetic Algorithms are optimization techniques

based on the principles of natural evolution. This

paper presents a genetic algorithm for optimizing

Technical Indicators parameters in order to

maximize returns. Other GAs have been previously

used to optimize technical indicators parameters, in

particular (Fernández-Blanco, 2008) and to develop

investment strategies based on technical indicators

(Bodas-Sagi, 2009) (Gorgulho & Neves & Horta,

2009) (Yan & Clack, 2007).

The next section will discuss the related work on the

Genetic Algorithms and various trading strategies

currently used in Technical Analyses. Section 3

explains the system architecture and the investment

strategies used in this paper, the markets and years

used to test those strategies. Also in this section the

overall description of the GA is shown, and the

fitness, selection, crossover and mutation functions

used. In section 4 the results are presented and a

highlight of the most relevant results is made. In

section 5 the conclusions of this study are shown.

2 RELATED WORK

One of the most used and oldest strategies to

identify trends is the crossing of Moving Averages.

This strategy has been studied by Brock (1992) and

by Kaufman (2005). This studies concluded that

from 1910 to 2000 the Crossing of the Moving

Average perform better than the Buy and Hold

strategy, except for the period from 1980 to 2000

306

Simoes A., Neves R. and Horta N..

AN INNOVATIVE GA OPTIMIZED INVESTMENT STRATEGY BASED ON A NEW TECHNICAL INDICATOR USING MULTIPLE MAS.

DOI: 10.5220/0003058103060310

In Proceedings of the International Conference on Evolutionary Computation (ICEC-2010), pages 306-310

ISBN: 978-989-8425-31-7

Copyright

c

2010 SCITEPRESS (Science and Technology Publications, Lda.)

where the market exhibited a regular uptrend, and no

excess profits where possible as reported by Ellis &

Parbery (2005). More complete studies of other

Technical Indicators has been made, like the one by

Canegrati (2008) who studies the profitability of 76

Technical Indicators with robust results for some

indicators.

Many papers have been recently published on the

use of GAs to optimize technical indicators like

Fernández-Blanco (2008), which use GAs to

optimize the parameter of a single Technical

Indicator, the MACD (Moving Average

Convergence-Divergence) with 3 parameters, and an

extra parameter for the history window size. Another

solution based also on optimizing Technical

Indicators parameters is the one used by Bodas-Sagi

(2009), where the chromosome is composed by the

MACD, RSI and history window size, also a

comparison between single and multi-objective is

made. Besides GAs others optimization techniques

have been applied to this area of study, like neural

networks by Kimoto & Asakawa (1990), where the

neural network uses for the inputs the price, volume,

interest rate and foreign exchange rate.

This study concentrates in the optimization of

technical trading rules which has not been yet tested

with GAs, like the SMAC and MAD strategies, and

also, combines these two strategies in one

chromosome trying to achieve better and solid

returns than with the solo strategies.

3 METHODOLOGY

The proposed system consists on a Genetic

Algorithm coupled with a market return evaluation

module based on the return of the strategies in

different markets in specific time-frames.

3.1 System Architecture

Figure 1: System Overall Architecture.

The complete process can be summarized as:

The user starts by specifying the markets to analyze

and next chooses the Technical Indicators used in

the strategy and the train and test period.

Afterwards, the Genetic Algorithm Kernel runs

several number of times, optimizing the parameters

of the strategy for the markets and training period

chosen. Finally for each run of the GA, its return on

the test period is calculated. Detail info is shown to

the user displaying the optimized strategy and the

return for each market in the test and in the training

period.

3.1.1 Modules Description

This section presents the overall description of each

module and their main responsibilities.

The “Technical Indicators” module is responsible

for the creation and management of the technical

indicators used by all the strategies. The “Train and

Testing Periods” module controls the time

components of the Stock Indexes. The “Stock

Market Indexes” is responsible for loading the stock

market indexes from the source (a .csv file).The

“Market Return Evaluation” module calculates the

return and other metrics for evaluating the

investment strategy (like the Sharpe Ratio). The

Genetic Algorithm Module is the most important

because it is the one who does the core functions of

the system. This module uses data from all the other

modules to calculate the perfect strategy with the

Technical Indicators. Finally the Optimized Strategy

module is responsible for showing the user the result

of the optimization.

3.2 Train and Test Data set

The time period chosen for training was from 1

January 1993 to 31 December 2003, eleven years of

daily data and the testing period was from 1 January

2004 to 31 December 2009. The markets tested

where the S&P500 (USA), FTSE100 (England),

DAX30 (Germany) and NIKKEI225 (Japan). They

represent the main indexes of the main developed

economies.

3.3 Technical Indicators

The first strategy to be tested was the Simple

Moving Average Crossover (SMAC) which is

composed by two Moving Averages (MA) with

different time periods. One of the MA is a long term

MA, and the other is a short term MA. A buying

signal is generated whenever the short term MA

crosses over the long term MA, and a sell signal is

AN INNOVATIVE GA OPTIMIZED INVESTMENT STRATEGY BASED ON A NEW TECHNICAL INDICATOR

USING MULTIPLE MAS

307

generated whenever the short term MA crosses

under the long term MA.

Another indicator that will be used in this paper is

the Moving Average Derivate (MAD). It is an

extended version of the “MA Change” described by

Kaufman (2005). In the original version it is

calculated by subtracting de value of the current MA

with the value of the MA in the previous day.

In mathematics this is simply the secant to the MA

curve in the last two days. In this way this generic

Derivate of the MA can be calculated based on the

definition of Secant of the MA, this way the MAD is

calculated by subtracting de value of the current MA

with the value of the MA at “n” days ago. Where

“n” is one of the variables that will be optimized.

The buying signal is given when the MAD is above

zero and a selling otherwise.

Beside this two indicators a new indicator is created,

called SMAC & MAD that includes the two

indicators mentioned above (SMAC and MAD) that

signals a buy when both the indicators are buying,

does nothing when one of the indicators is out of the

market and issues a short-sell signal when both

indicators advise to short-sell.

3.3.1 Parameters of Technical Indicators

After defining the strategies it is necessary to define

the parameters to use both in the SMAC and in the

MAD strategies. Both strategies have two

parameters, with similar meanings. The first

parameter is similar to both strategies, the time

period of the long term MA. The second parameter

in one strategy is the time period of a short term MA

and in the other strategy is the distance between the

two points used to calculate the secant. In both

parameters they should indicate medium term

periods. The new Indicator (SMAC & MAD) has

four parameters, two for the SMAC and two for the

MAD. These parameters represent the parameter of

the underlying strategies.

3.4 Genetic Algorithm Kernel

3.4.1 Genetic Encoding

The chromosome created must represent the

Technical Indicators used, in this way the SMAC

chromosome is represented by two genes, one for

the shortest MA other for the longest MA in days

(natural numbers), the interval of this values is

between 1 and 250 (this value is above the largely

used MA for long term analysis: 200 days). The

same rule applies to the MAD chromosome, where

one of the parameters is the “gap” and the other the

number of days of the MA. In Table 1 it is shown a

representation of a possible chromosome for the

SMAC & MAD chromosome (which includes both

the SMAC and MAD genes):

Table 1: An example of a Chromosome.

SMAC MAD

Chromosome 25 160 40 100

3.4.2 Features of the GA

The Genetic Algorithm used for the optimization

uses a standard optimization procedure. The

selection of individuals for crossover is chosen

based on a roulette wheel selection (but only the best

half of the population enters the selection process),

and the probability of being chosen is equal to the

ratio: individual fitness function / Sum of fitness of

all individuals. Each individual can be chosen any

number of times for crossover (the only exception is

that an individual cannot be chosen to crossover

with himself).

The crossover is a one-point crossover, each

breading generates the two possible distinct children

and includes them in the population. In the

chromosome of only one indicator (SMAC or MAD)

the children are created by swapping the long and

shortest MA day. In the SMAC & MAD

chromosome the children are created by swapping

the 2 genes that represent each Indicator (the first

children takes the SMAC genes from parent A, and

MAD genes from parent B, and the second children

the other way around).

The fitness function used is the average return of the

individual for the 4 Stocks Indexes chosen, during

the 11 years of the train data (1993 to 2003).

4 RESULTS

The optimization procedure described above was run

fifty times for each approach namely, MAD, SMAC

and SMAC & MAD, additionally 50 random

strategies were evaluated. The random strategy

consists in each day deciding a random trade: long,

short-sell or do nothing, each with one third chance

of occur. In each run the best individual obtained

was evaluated for the test period (2004 to 2009) for

the yearly return of the average of the 4 Indexes.

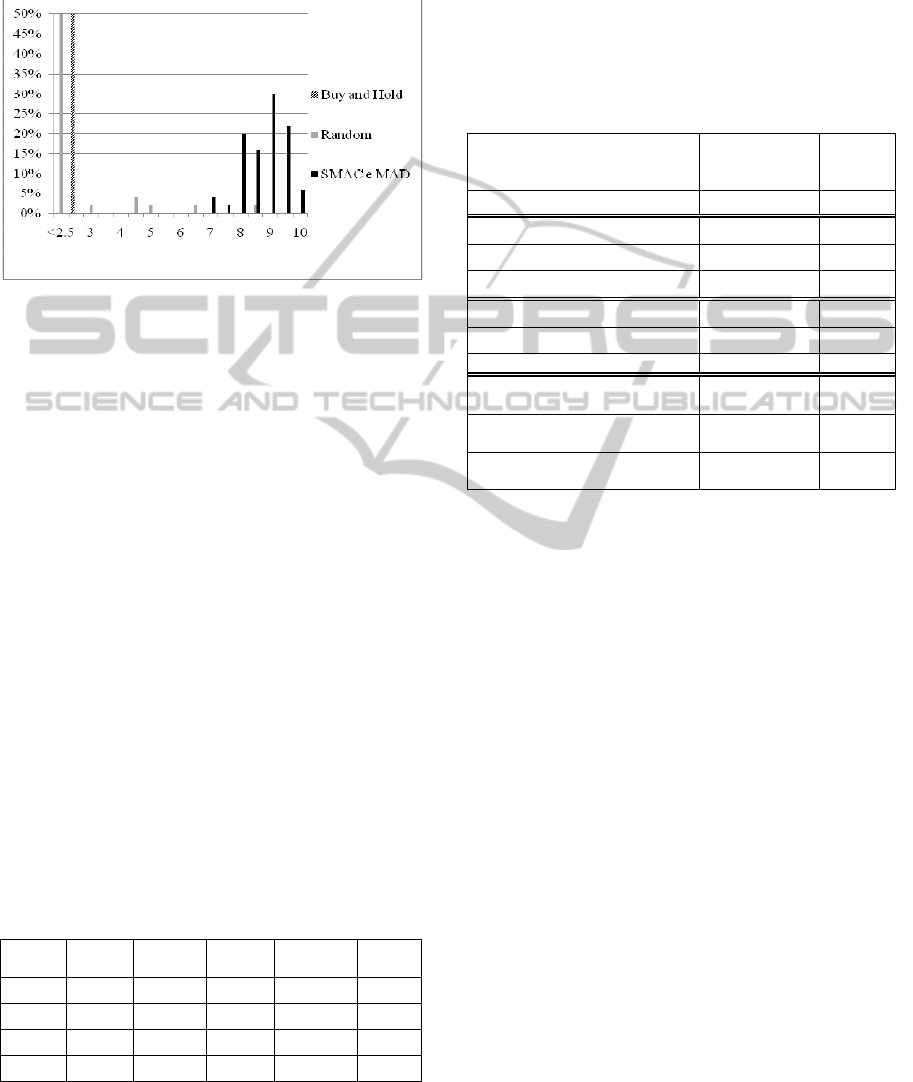

In Figure 2 it is shown the histogram for the returns

of the 50 runs although the percentage go only to

ICEC 2010 - International Conference on Evolutionary Computation

308

50% for better perception of the other values, the

Buy & Hold is 100% on the 2.5 column, and the

random strategy has 88% in the less than 2.5

column.

Figure 2: Histogram of returns of the Buy & Hold,

Random SMAC& MAD, and SMAC & MAD, from 2004

to 2009.

As we can see in this figure, all the chromosomes

beat the Buy and Hold and the random strategy, this

confirms the validity of the Technical Indicators

proposed.

The SMAC & MAD Compost Chromosome is very

similar with a Gaussian curve, which proves that this

strategy has the most solid results. The detailed

statistics can be seen in Table 2.

In this table it is possible to see that the Buy & Hold

and the Random Strategy have the lowest Worst,

Median, Average and Best Values. And that the

“SMAC & MAD” have Average, Median, and

Worst value beating all the other strategies (and the

Best value is not far away from the first). This

means that using the optimized “SMAC &

MAD”, not only the expected profit is better, but the

possibility of a “bad return” happen during the

test period has a low probability of occur, and even

if it occurs the return will not be too low (the worst

return of the SMAC & MAD in 50 runs in the test

period is 7.3%).

Table 2: Statistics of the returns in the test period for the

different strategies.

Buy &

Hold

SMAC MAD

Random

Strategy

SMAC &

MAD

Best:

2.6% 10.1% 10.5% 8.58% 10.2%

Average:

2.6% 8.5% 8.7% -1.01% 9.0%

Median:

2.6% 8.9% 8.0% -1.11% 9.2%

Worst:

2.6% 6.3% 6.8% -7.33% 7.3%

4.1 Return on Investment

In the next table we can see the yearly average return

in the test period of the three best chromosomes

found in the training period, with the respective

number of trades, contrary to the return (which is

annualized), during all the testing period (6 years).

Table 3: Yearly average return and Total Number of

Trades of the various strategies tested from 2004 to 2009.

Average

Return

Average

Sharpe

Ratio

Buy & Hold

2.55% 0.030

SMAC (227, 210)

8.34% 0.570

SMAC (225, 210)

8.27% 0.531

SMAC (222, 210)

7.73% 0.352

MAD (110, 11)

8.15% 0.365

MAD (112, 10)

8.01% 0.349

MAD (112, 11) 7.52% 0.314

MAD(186, 45) & SMAC(202,

193)

9.37% 0.522

MAD (108, 20) & SMAC(206,

195)

8.38% 0.466

MAD(112, 11) & SMAC(242,

128)

8.27% 0.458

In this table we can see that the “MAD & SMAC”

strategy have the best, the second and fourth best

results. This means that this is the most optimal and

robust strategy, because it’s the one who maintains

the best results from the training period to the testing

period.

4.2 Sharpe Ratio

The Sharpe Ratio is a measure that was created by

Nobel Prize William Sharpe, to measure the reward-

to-variability ratio of a trading strategy (Sharpe,

1994). This measure allow to compare two strategies

with different returns, and see if the additional return

of one strategy is due to applying a more risky

strategy, or to a smarter investment strategy.

In Table 3 we can see that the “MAD & SMAC”

strategy has worse Sharpe Ratio results that the

SMAC strategy (the SMAC has the best and second

best result, while the “MAD & SMAC” has the third

and fourth and fifth best Sharpe Ratio. The values of

the “MAD & SMAC” are more stable with small

differences between the best and the worst. This

means that the returns showed in Table 3 are due to

the “MAD & SMAC strategy” being a bit more

riskier (with more variance in the yearly returns)

than the SMAC strategy. This means that the

deciding factor on the choice of these two strategies

AN INNOVATIVE GA OPTIMIZED INVESTMENT STRATEGY BASED ON A NEW TECHNICAL INDICATOR

USING MULTIPLE MAS

309

is the investor profile risk. The investor can choose

between a strategy with better returns but more

volatility (the “SMAC & MAD”) and the SMAC

with more regular but less attractive results.

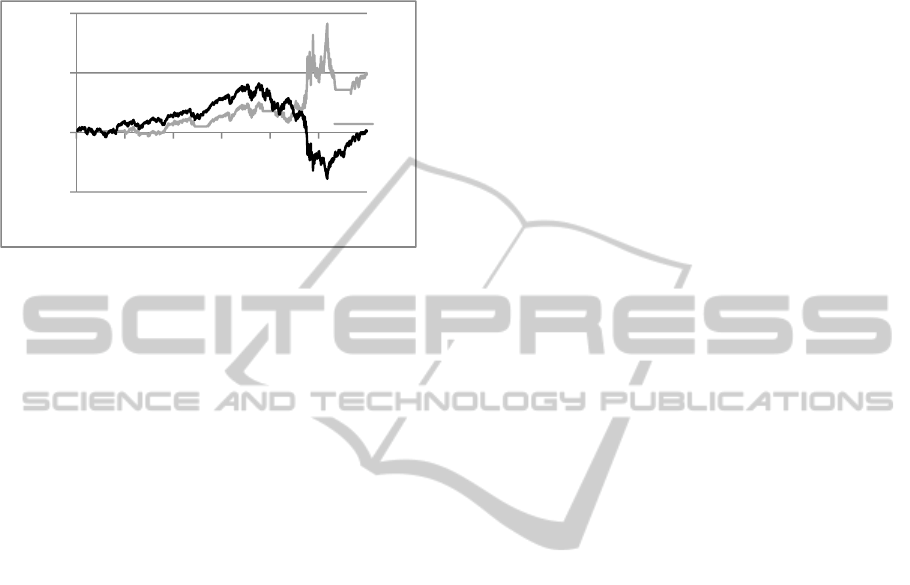

Figure 3: Evolution of the return of the Buy and Hold, and

the “MAD (108, 20) & SMAC(206, 195)” strategy, on

S&P500 from 2004 to 2009.

In Figure 3 we can see the evolution of the return of

the strategy with the best results in the training

period, during the test period, compared with the

evolution of the Buy and Hold.

The proposed strategy is best suited for medium and

long term investment since it only takes a decision

after the confirmation of a trend is clear, it has the

great advantage of avoiding long periods of

downtrends. The classical stategy of Buy and Hold

that is only good in markets that do not exibited bear

markets like the 80s and 90s in the S&P500 does not

perform well in markets characterized by long bear

markets.

5 CONCLUSIONS

This document presented the use of Genetic

Algorithms to optimize the parameters of various

Technical Indicators and with them create various

trading strategies. The results obtain showed that

this strategies beat significantly the Buy and Hold

(the “MAD & SMAC” strategy had an average of

9.0% against the 2.6% of the Buy and Hold), once

more proving the validity of Technical Analysis.

Finally the optimized “MAD & SMAC” strategy is

compared with the random strategy, with excellent

results: the optimized has an average of return of

9.0% against the -1.01% of the random strategy. The

use of the “MAD & SMAC” has also shown better

results than the use of any of the indicators

individually.

REFERENCES

Bodas-Sagi, et al. (2009). Multiobjective optimization of

technical market indicators. In Proceedings of the

GECCO '09, Montreal, Canada .

Brock, et al. (1992). Simple Technical Trading Rules and

the Stochastic Properties of Stock Returns. Journal of

Finance, American Finance Association, vol. 47(5) ,

1731-6.

Canegrati, E. (2008). A Non-Random Walk down Canary

Wharf. MPRA Paper, University Library of Munich .

Chan, E. P. (2009). Quantitative Trading. New Jersey:

John Wiley and Sons.

Ellis, Craig A. & Parbery, Simon, A. (2005). Is smarter

better? A comparison of adaptive, and simple moving

average trading strategies. Research in International

Business and Finance, Elsevier, vol. 19(3) , 399-411.

Fama, Eugene F. (1998). Market efficiency, long-

term returns, and behavioral finance. Journal of

Financial Economics, Elsevier, vol. 49(3) , 283-306.

Fernández-Blanco, P., et al. (2008). Technical market

indicators optimization using evolutionary algorithms.

Proceedings of the 2008 GECCO conference

companion on Genetic and evolutionary computation ,

1851-1857.

Gorgulho, A., Neves, R. and Horta N. (2009). Using GAs

to Balance Technical Indicators on StockPicking for

Financial Portfolio Composition. Proceedings of the

GECCO, 2009, Montreal, Canada. , 2041-2046.

Jegadeesh, N., and Titman, S. (1993). Returns to buying

winners and selling losers: Implica-tions for stock

market efficiency. Journal of Finance 48 , 65-91.

Kaufman, P. J. (2005). New Trading Systems And

Methods. San Francisco, CA: John Wiley & Sons Inc.

Kimoto, T. and Asakawa, K. (1990). Stock Market

Prediction System with Modular Neural Networks.

IJCNN International Joint Conference on Neural

Networks, vol. 1 , 1-6.

Kirkpatrick, C. D. and Dahlquist R. D. (2009). Technical

Analysis. FT press.

Sharpe, W. F,. (1994). The Sharpe Ratio. Journal of

Portfolio Management 21 (1) , 49–58.

Yan, W. and Clack, C. (2007). Evolving Robust GP

Solutions for Hedge Fund Stock Selection in

Emerging Markets. Proceedings of the GECCO 2007 ,

London, UK, 2234-224.

‐50%

0%

50%

100%

2004 2005 2006 2007 2008 2009

MA

…

ICEC 2010 - International Conference on Evolutionary Computation

310