TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

Alexander Borisov

1

, George Runger

2

and Eugene Tuv

1

1

Intel, Chandler, AZ, U.S.A.

2

Arizona State University, Tempe, AZ, U.S.A.

Keywords:

Outliers, Process control, Contribution plots, Partial least squares.

Abstract:

Anomaly detection in data streams requires a signal of an unusual event, and an actionable response requires

diagnostics. Furthermore, monitoring for process control is often concerned with one or more target (con-

trolled) attributes. Consequently, it is necessary to separate anomalies (and their contributing attributes) that

could influence the controlled target strongly, and this becomes more important with the increased number

of monitored attributes in modern processes. This task leads to a difficult problem not addressed directly by

the machine learning/process control community. We introduce the target-aware anomaly detection problem

and present a solution for process control in modern systems (with nonlinear dependencies, high dimensional

noisy data, missing data, and so on). The main objective is to identify and rank outliers and also diagnose

their contributing attributes with respect to the possible effect on the response. The method is different from

traditional linear and/or univariate approaches, as it can deal with local data structure in the neighborhood of

an outlier, and can handle complex interactions via the use of an appropriate learner. In addition, the method

can be computed quickly and does not require time consuming matrix operations. Comparisons are made to

traditional contribution plots computed from partial least squares.

1 INTRODUCTION

The importance of anomaly detection has grown from

manufacturing to include systems such as environ-

mental, security, health, supply chains, transportation,

etc. Data are characterized by a set of input attributes

(or variables), and one (or several) controlled (target)

attribute(s). A typical example of an input set con-

sists of measurements generated over different stages

of a production process from numerous sensors (from

hundreds to thousands). Along with the input mea-

surements target attributes may result from final prod-

uct tests or other system performance measures. The

usual goal of the process control is to keep the values

of the target attributes within a given range. Further-

more, if we observe or predict an excursion in a target,

it is important to determine what inputs contribute to

the excursion.

In applications (such as process control) where the

objective is to control a target attribute, and as the

number of input attributes increase, it becomes im-

portant to focus anomaly detection to the effect on the

target. Furthermore, although target-labeled training

data is used, we do not assume that the process data is

target-labeled when the outlier diagnostics are comp-

uted. For many common process control applications

the decision for action must be based on the input at-

tributes before the target is measured. Consequently,

we refer to our approach as target-aware, rather than

supervised.

This problem has not been addressed in the ma-

chine learning literature. Instead, commonly used

methods in advanced process control applications (for

both unsupervised and supervised anomaly detection)

rely on linear data models (i.e., principal component

analysis (PCA) and partial least squares (PLS) (Hastie

et al., 2001)) and multivariate normal distribution as-

sumptions in the input space. Such approaches (e.g.,

for example, (Ergon, 2004)) can be successful in find-

ing anomalies in low-dimensional, non-noisy numeric

data when the dependency between the inputs and

outputs are near-linear. PLS provides an approach for

target-labeled outlier detection and attempts to iden-

tify input attributes that most strongly contribute to

an outlier. However, the above strong assumptions

limit the applicability for data that can be very large

(millions of samples and/or several hundreds to thou-

sands of predictors), noisy, with heterogeneous type

(numerical and categorical). Other anomaly detection

approaches (e.g., see reviews by (Hodge and Austin,

14

Borisov A., Runger G. and Tuv E..

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS.

DOI: 10.5220/0003530100140023

In Proceedings of the 8th International Conference on Informatics in Control, Automation and Robotics (ICINCO-2011), pages 14-23

ISBN: 978-989-8425-74-4

Copyright

c

2011 SCITEPRESS (Science and Technology Publications, Lda.)

2004)) can not be easily extended to supervised set-

tings.

Solutions to the problem above can be approached

in several ways. One is to build a model on previously

seen data that is capable of predicting failures or large

changes in a target from recently arrived new data.

We refer to this as predictive modeling. Such an ap-

proach based on different types of regression models

was used in an off-line setting (Angelov et al., 2006).

However, an important concern is that such models

may generalize poorly on new data when the distri-

bution of inputs changes. To address this concern

previous work considered adaptive models were up-

dated based on new test data that were determined to

be fault-free (Lughofer and Guardioler, 2008; Filev

and Tseng, 2006). An advantage of our approach is

that the model need not be updated and we integrate

unsupervised information.

An alternative is unsupervised anomaly detection

where the objective is to find points in input space that

are distant from the ”general” input distribution, thus

effectively detecting anomalies in new (or existing)

data (Chiang et al., 2001). However, such an anomaly

in the input attributes might (but does not always) lead

to a large change in the target value too. Still there

is not a direct link between the two, as the unsuper-

vised nature of anomaly detection does not take into

account the predictive model that is used.

We propose a novel target-aware anomaly detec-

tion approach that combines both predictivemodeling

and unsupervised outlier detection. We use a predic-

tive model learned from target-labeled training data

to assign ”outlier scores” to new data points. These

scores consider both the effect on the target as well as

the remoteness of point in the space of inputs. (Note

that this is different from predicting target probabili-

ties from the model directly, as those probability es-

timates also do not generalize outside of the current

input distribution.) Furthermore, we propose a mea-

sure that separates the most influential outliers, and

ranks them according to influence on the target, along

with a threshold used to filter the non-influential out-

liers and normal samples. As an important by-product

for signal diagnosis, we compute the contribution of

input attributes to the anomaly score. This task is re-

lated to fault isolation and several methods have been

used (Efendic et al., 2003; Runger et al., 1996). We

propose a ranking measure, along with a threshold, to

identify the input attributes that contribute to a partic-

ular point being an outlier. Our analysis statistically

quantifies risks and we use quite different models and

metrics than previous work.

Regarding terminology, we note that supervised

and unsupervised anomaly detection can refer to

whether samples are labeled as normal or anomalous

and not the target attribute labels (Chandola et al.,

2009). Consequently, we refer to our method as

target-aware anomaly detection. We performed ex-

periments with simulated data sets that closely mimic

the behavior of real systems and show that our method

outperforms classical PLS contribution plot analysis,

both in terms of detecting outliers, calculating rel-

evant contributions, and in terms of improving pre-

dictive accuracy on new data when potential outliers

are detected automatically even before the target is

known. The algorithm was successfully applied on

real data too. Here we focus on the case of a nu-

merical target (regression case) with numerical inputs

because it is more relevant for statistical process con-

trol. We provide a short description of traditional PLS

based anomaly detection approach in Section 2. Sec-

tion 3 presents our new method. Section 4 offers il-

lustrative examples and compares to the traditional

PLS contribution plots, and Section 5 provides con-

clusions.

2 TRADITIONAL LINEAR

METHODS FOR SUPERVISED

ANOMALY DETECTION

The supervised outlier detection and contribution

problem has been addressed in the statistical litera-

ture through linear models with PLS regression (Wold

et al., 2001). The PLS approach is the only method

that has been been applied for outlier/contribution

analysis in the supervised case. PLS iteratively

computes components (directions) with maximum

correlation to the target, performing Gram-Schmidt

orthogonalization of the input space and the tar-

get with respect to the new identified component.

The process continues until a predefined number of

components is generated. In this way it yields a

number of mutually orthogonal directions that have

maximum correlation to the target. Projections of

the input space along these directions yield load-

ings/projection/scores (similar to PCA). PLS results

in the regression coefficients for target y with respect

to these directions.

More formally, a PLS model has the form X =

TP

t

, y = TQ

t

, where P, Q are X and y loadings, re-

spectively, and t denotes matrix transpose. Here T is

the score matrix with columns corresponding to di-

rections. So in addition to finding a new basis in X

space it provides a regression model for y. Similar to

PCA, a PLS model is sensitive to the scaling of at-

tributes, and therefore requires an appropriate scale

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

15

to be selected. In most applications the attributes are

standardized (zero mean and unit standard deviation)

and for simplicity we make this assumption in this

paper. The PLS algorithm description can be found,

for example, in (Hastie et al., 2001). The number of

directions is usually selected using an explained vari-

ance threshold or cross-validation.

Two common statistics are used to monitor for

anomalies (similar to the PCA case). First is squared

prediction error (SPE). That is, the distance from an

inspected sample to the model plane defined by se-

lected latent variables. Second is the distance from

zero (the center of the scaled distribution) in score

space. To account for different score scales, and their

different influence on the target, scores are multiplied

by the corresponding y-loadings and divided by the

standard deviation. More insight on these two mea-

sures follows next.

Suppose we computed and selected K directions

{T

1

, T

2

, .. . , T

K

} from a PLS model given by X =

TP

t

, y = TQ

t

, where T = T(N ×K), P = P(N ×

K), Q = Q(1×K) matrices. Let the kth column of

TandQ be denoted as T

k

and Q

k

, respectively. Here

Q denotes the coefficient estimates from the linear re-

gression of y on T and the (scalar) Q

k

is a measure

of the weight of T

k

in the regression. A modified

Hotelling’s T

2

statistic (Hotelling, 1947) with respect

to selected components is computed as follows:

T

2

=

K

∑

k=1

T

k

·Q

k

λ

k

2

, (1)

where λ

k

is the standard deviation of the elements of

T

k

. Here T

2

is similar to the (Mahalanobis) distance

of data sample x

x

x

0

from the centroid

¯

x

x

x after a projec-

tion to the subspace defined by the first K latent vari-

ables. An anomaly is signaled if this distance is too

large. However, multiplication by the y-loadings Q

allows one to take into account the influence of com-

ponents on the target.

Because T

2

statistic is not sensitive to anomalies

that are far from the subspace of the latent variables,

a second statistic is used that is sensitive to the dis-

tance from this subspace. Suppose R = R(N ×K) is

the projection matrix from the original input space to

scores, i.e T = XR, P

t

R = I. The squared prediction

error (SPE) is

SPE

0

= (x

x

x

0

−

ˆ

x

x

x

0

)

t

(x

x

x

0

−

ˆ

x

x

x

0

) (2)

where

ˆ

x

x

x

0

= x

x

x

0

RP

t

is the projection of x

x

x

0

to the sub-

space spanned by the first K PLS components in the

input space.

We define the (supervised) PLS contribution score

of attribute j to data sample x

x

x

0

to T

2

, in a manner

similar to (Ergon, 2004) and (Miller et al., 1998),

but scores are multiplied with their corresponding y-

loadings. That is,

C

j

(T

2

, x

0

) = x

0j

·

v

u

u

t

K

∑

k=1

T

k

Q

k

·R

jk

λ

k

2

(3)

and this can be interpreted as the multiplication of the

scores (normalized and weighted by y-loadings) by

the term x

0j

R

jk

that gives influence of attribute j on

the score T

k

= XR

k

.

Similarly, the PLS contribution score of attribute

j for x

x

x

0

to SPE is calculated from the j-th term of (2)

in the same way as for PCA model. That is,

C

j

(SPE, x

0

) = (x

0j

− ˆx

0j

)

2

(4)

3 TARGET-AWARE ANOMALY

AND CONTRIBUTOR SCORING

ALGORITHM

As stated earlier, the notion of ”target-aware out-

lier/anomaly detection” is closely related to the effect

on a target. More precisely, call an outlier in X space

an influential outlier if it has a large influence on the

target. Call all other outliers (with minor or no influ-

ence on the target) non-influential outliers. For ex-

ample, an outlier in an irrelevant attribute will have

no influence. Our goal here is to detect influential

outliers and determine the attributes that contribute to

them. We assume training data with target-labels for

a predictive model, but to meet the conditions in pro-

cess control applications we assume that target values

are not available at the time anomaly detection is eval-

uated.

Due to the complexity and size of real data sets,

and to address nonlinear models, interactions, miss-

ing data, different units for attributes, and other prop-

erties of practical problems, we develop new scores

and diagnostics from tree based models. An ensem-

ble of gradient boosting trees models (GBT) (Fried-

man, 2001) is used to calculate a ”target-aware outlier

score”, that describes how well a new (or old) sample

fits into the input distribution partitioned by trees in

the model with adjustment for the target.

3.1 Decision Tree Formulas

We consider the practical case where both the input

attributes and the target are continuous. A decision

tree provides a supervised predictive model (Breiman

et al., 1984) that recursively partitions samples to

achieve smaller impurity of the target attribute. The

samples at a node are partitioned (split) into subsets at

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

16

the two child nodes (because we only consider binary

trees). Each split is defined by a binary rule on one

of the input attributes X

j

. For a continuous attribute

partitions of the form X

j

< v or X

j

> v are considered.

The attribute for which the binary rule minimizes the

impurity of the target is called the primary (best) split-

ter. The impurity is measure defined by entropy or the

Gini index for categorical targets and for a numerical

target we use squared error loss

I(T) =

∑

i∈T

(y

i

− ¯y(T))

2

where ¯y is the mean of the target values at the node.

After a split the impurity of the two child nodes is

computed as

I(T

L

) + I(T

R

) =

∑

i∈T

L

(y

i

− ¯y(T

L

))

2

+

∑

i∈T

R

(y

i

− ¯y(T

R

))

2

where ¯y(T

L

) and ¯y(T

R

) are the target means in the left

and right child nodes, respectively. The change in

impurity from the parent to the child nodes obtained

from the primary splitter is denoted as

W(T) = I(T) −I(T

L

) −I(T

R

) (5)

and referred to as the split weight. Larger values indi-

cate a more important split at node T.

The process continues until a stopping rule is true.

A single tree algorithm might further prune (remove)

nodes, but typically ensemble models do not. Given

a sample x

0

the attribute values in x

0

determine a

path through the nodes until a terminal (leaf) node is

reached. The majority class of the target at the leaf is

often used to predict a categorical target and the mean

of the target values at a leaf is often used to predict a

continuous target. A GBT model is a (serial) ensem-

ble of decision trees that is used to improve predictive

performance (Friedman, 2001).

3.2 Target-aware Algorithm

The algorithm starts with target-labeled training data

and a GBT ensemble generates a predictive model to

relate the process (input) attributes (X

1

, X

2

, . . . , X

M

) to

the target attribute Y. In the test phase the objective is

to determine if a new sample x

0

is an influential out-

lier, without the label Y. One may often have a col-

lection S

0

of samples in the test data so that ranking

and selection of the influential outliers, along with at-

tribute contributions, are important. In the following,

for simplicity, we describe the scoring for a single test

sample x

0

. We calculate the contribution of each at-

tribute X

j

to the outlier score for sample x

0

and this

simply leads to the final outlier score as the sum of

the contribution scores from all attributes. The contri-

bution of X

j

depends on the remoteness of the value

of X

j

in sample x

0

in X-space (the X-contribution),

as well as the importance of X

j

to predict the target

(the Y-contribution). Measures for both these terms

can be calculated quickly from the previously learned

GBT model.

For the X contribution, consider node T of a tree

in the ensemble. We define

d

j

(T, x

0

) =

|x

0j

− ¯x

j

(T)|

IQR(X

j

, T)

where ¯x

j

(T) is mean value of X

j

in the node T (com-

puted from the non-missing values), and IQR(X

j

, T)

is the difference between the 75% and 25% quantiles

of X

j

in the node T. The IQR is proportional to a ro-

bust estimate of the standard deviation. Here d

j

(T, x

0

)

measures the remoteness of the value of X

j

in sample

x

0

within the data at node T. The IQR is used in a

similar manner to a standard deviation, to (robustly)

adjust for different units among the X

j

’s. The algo-

rithm described below computes

max[0, d

j

(T, x

0

) −C

1

]

for a predefined (tuning) constant C

1

. If the contri-

bution is negative it is set to zero. The role of C

1

is

to truncate small absolute differences to zero. Small

differences indicate that x

0j

is not remote at node T.

For the Y contribution, it is useful to compare the

split weight in equation 5 actually obtained at a node

T to a baseline. The baseline is the split weight ob-

tained after the target values at node T are randomly

permuted among the samples (denoted as W

0

(T)) and

minimum impurity is computed. That is, for the rows

at node T the y measurements are randomly permuted

among these rows, and then the minimum split weight

is determined as in 5. The intent is that is W

0

(T))

provides a baseline score for split weight when inputs

are not related to the target. Consequently, in our out-

lier algorithm we consider an adjustment to the split

weight as

max(0,

p

W(T) −C

2

p

W

0

(T))

whereC

2

is a (pre-specified)tuning constant. The role

of C

2

is to truncate Y-contributions that do not exceed

a baseline to zero. We apply a square root to put both

X- and Y-components on the same linear scale. The

importance of X

j

to predict the target is simply ob-

tained from a function of the split weight W(T) (and

the baseline W

0

(T)) at the nodes where X

j

is the pri-

mary splitter.

Then the contribution of the attribute in the

node is computed as the product of the X- and Y-

contributions. This allows us to take into account

the ”local” effect of attribute effects on the target in

a manner similar to the PLS T

2

score. But PLS uses

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

17

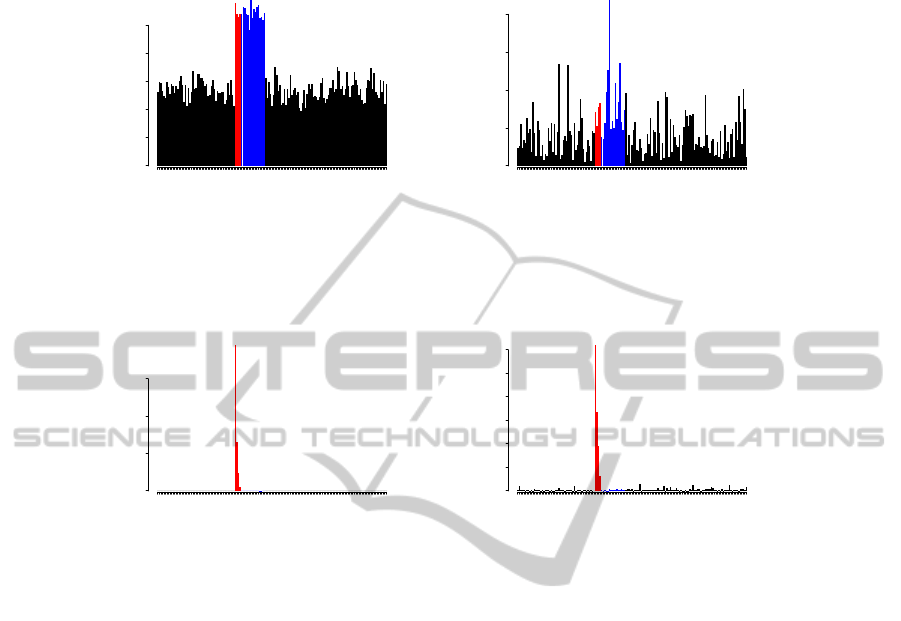

450 475 500 525 550 575 600

PLS SPE score

samples

score

0 2 4 6 8 10

450 475 500 525 550 575 600

PLS T^2 score

samples

score

0 1 2 3 4 5

(a) SPE, T

2

scores from PLS.

450 475 500 525 550 575 600

GBT outlier score

samples

score

0 20 40 60

450 475 500 525 550 575 600

GBT prediction errors

samples

score

0 1 2 3 4

(b) Outlier scores from GBT and prediction errors on the samples (for reference).

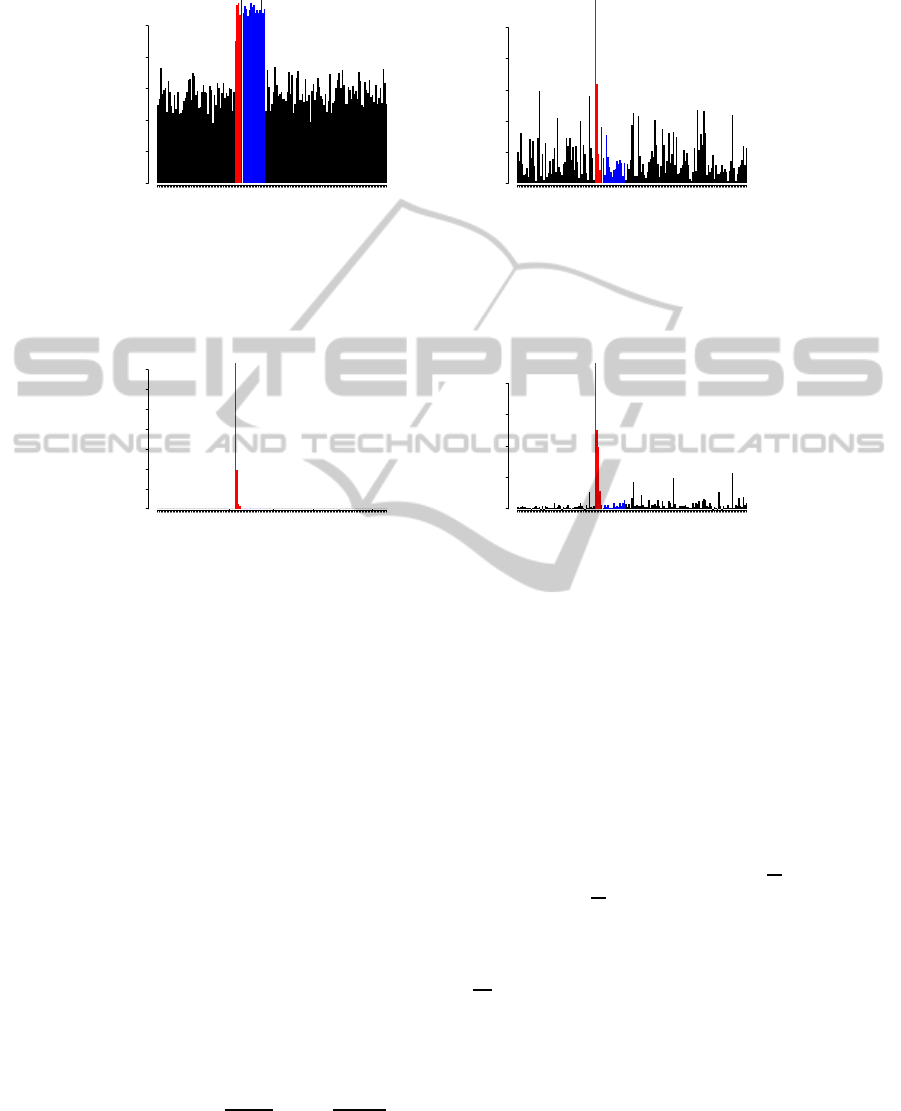

Figure 1: SPE and T

2

score plots from PLS vs. our target-aware method for experiments with a basic linear model. Influential

and non-influential outliers are shown with red and blue bars, respectively.

theY-loadings as multipliers, i.e., ”global” score mul-

tipliers. Both constants are usually fixed. We used

the same values C

1

= 3, C

2

= 2.5 for all experiments.

The algorithm is not too sensitive to C

1

, and C

2

acts

as false alarm/rejection rate threshold to detect influ-

ential outliers.

The details of the algorithm follow.

1. Build a GBT model for a given target. Initialize

the contribution score matrix C

j

= 0, j = 1. . . M.

2. Compute the contributions of an attribute to a se-

lected sample x

0

. The contribution calculation is

based on the GBT ensemble. Select an attribute

X

j

. For each node T in each tree, where the pri-

mary splitter is X

j

, the contributionC

j

(T) of vari-

able X

j

to sample x

0

is defined as

C

j

(T) = max(0, d

j

(T, x

0

) −C

1

)

·max(0,

p

W(T) −C

2

p

W

0

(T))

Then the contribution score C

j

of variable X

j

to

sample x

0

is increased by the term C

j

(T).

3. Compute the total outlier score for sample x

0

sums

over all attributes as

C

0

=

M

∑

j=1

C

j

The most time consuming operation of our

method is building a GBT model, but this is only per-

formed once (or when the model is refreshed). As

each tree has time complexity N ·

√

N · M we ob-

tain O(K ·N ·

√

N · M) complexity for GBT model

with K trees. For very wide data sets we can use

embedded feature selection for GBT (Borisov et al.,

2006), and the complexity is reduced by a factor of

√

M. Although it is still more expensive than the

PLS algorithm, we avoid a quadratic complexity in

both the number of samples and the number of at-

tributes. To score a sample x

0

as a potential outlier

the steps are comparable to a prediction from a GBT

model (traverse the trees in the model), along with

some simple intermediate calculations for the X- and

Y-contributions, and these computations are fast on

modern hardware for even large data sets.

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

18

1 6 12 19 26 33

obs501

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs502

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs503

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs504

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs505

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs506

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs507

variables

PLS T^2 contr

0.00 0.06

1 6 12 19 26 33

obs508

variables

PLS T^2 contr

0.00 0.06

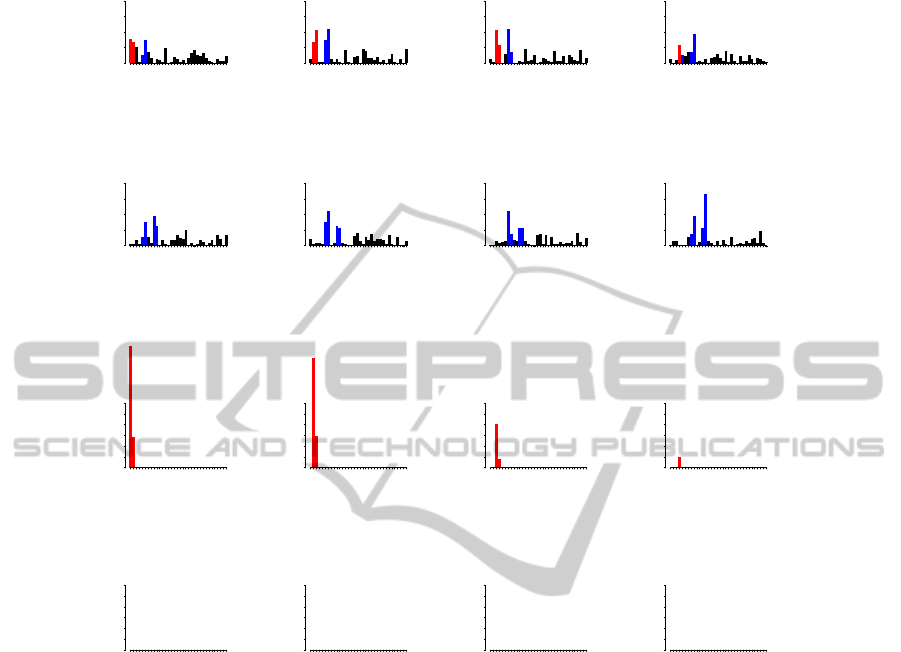

(a) Contributions from PLS T

2

scores.

1 6 12 19 26 33

obs501

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs502

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs503

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs504

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs505

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs506

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs507

variables

GBT contr

0 2 4 6

1 6 12 19 26 33

obs508

variables

GBT contr

0 2 4 6

(b) Contributions from the target-aware outlier scores.

Figure 2: T

2

score contribution plot from PLS vs. contribution plot from our target-aware method for experiments with a

basic linear model. Contributions for all variables are shown for the first 8 test samples. Correct relevant contributors are

shown with red bars. Other contributors are shown with blue bars. For the first three outliers there are 2 relevant contributors,

the fourth outlier has only 1 relevant contributor, and the other four groups have none.

4 EXPERIMENTS

The only existing competitive method for supervised

outlier ranking and contribution estimation is a PLS

contribution plot analysis which is widely used in sta-

tistical process control (along with more traditional

PCA). However, linear methods can be ineffective for

nonlinear high-dimensional data with many noisy or

irrelevant attributes. We illustrate the limitations of

PLS on several experimental scenarios that are very

similar to actual problems that are encountered in

manufacturing applications. Typical data have very

few relevant inputs and/or contributors for an outlier,

even when the total number of inputs can range from

several hundreds to tens of thousands. Therefore,

consider similar, representative scenarios in our ex-

periments, but with the pragmatic advantage that the

ground truth is known. From a linear model built with

PLS we can obtain two scores: SPE (distance from

the model that is computed in the same way as PCA)

and T

2

(modified with Y-loadings). It is worthy to

mention that the SPE score is useless for distinguish-

ing influential/non-influential outliers or contribution

analysis as it does not use Y-loadings.

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

19

396 431 466 501 536 571

PLS SPE score

samples

score

0 2 4 6 8 10

396 431 466 501 536 571

PLS T^2 score

samples

score

0 1 2 3 4

(a) SPE, T

2

scores from PLS.

396 431 466 501 536 571

GBT outlier score

samples

score

0 10 20 30 40

396 431 466 501 536 571

GBT prediction errors

samples

score

0.0 1.0 2.0 3.0

(b) Outlier scores from our target-aware method and prediction errors on the samples (for reference).

Figure 3: SPE and T

2

score plots from PLS vs. our target-aware method for a linear model with 100 noise variables. Samples

with relevant contributors (influential outliers) and non-influential outliers are shown with red and blue bars, respectively.

Each outlier has one contributor.

4.1 Linear Data with Noise

Reference data are simulated from 34 independent

attributes with 500 samples (rows). Each is nor-

mally distributed with mean zero and standard devi-

ation one. The four first attributes are relevant predic-

tors, with the target y = x

1

+ 0.5x

2

+ 0.3x

3

+ 0.15x

4

.

The other 30 attributes are irrelevant. We added 100

test samples generated from the same distribution, in

which we create 20 anomalies. Anomaly i has values

of attributes x

i

, x

i+1

, x

i+4

, x

i+5

equal to 5. Therefore,

the first three outliers have 2 relevant and 2 irrelevant

contributors, the fourth outlier has 1 relevant contribu-

tor, and the other outliers have 0 relevant contributors

(all 4 contributors irrelevant) to the target. The targets

for these additional samples are generated from the

same linear function of relevant variables. For PLS

we used two latent components as suggested by cross

validation based on the explained y-variance. (The

two components explained 98% of the y variance.) A

GBT model was built with 700 trees, shrinkage rate

= 0.01, tree depth = 4, and each tree used 60% sub-

sampling. The least squares loss function was em-

ployed.

Figure 1 shows the PLS SPE and T

2

plots for 50

(last) training samples and all testing samples for this

example, compared to the GBT outlier scores plot.

Figure 1 shows that PLS cannot distinguish the

influential and non-influential outliers. Actually it

does not even separate the two last influential out-

liers, while the target-aware outlier score plot gener-

ates the correct results. All four influential outliers are

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

20

450 475 500 525 550 575 600

PLS SPE score

samples

score

0 2 4 6 8 10

450 475 500 525 550 575 600

PLS T^2 score

samples

score

0 1 2 3 4

(a) SPE, T

2

scores from PLS.

450 475 500 525 550 575 600

GBT outlier score

samples

score

0 20 40 60

450 475 500 525 550 575 600

GBT prediction errors

samples

score

0 5 15 25

(b) Outlier scores from our target-aware method and prediction error on the samples (for reference).

Figure 4: SPE and T

2

score plots from PLS vs. our target-aware method for nonlinear data. Samples with relevant contributors

(influential outliers) and non-influential outliers shown with red and blue bars, respectively.

detected, without false alarms. Furthermore, the in-

fluential outliers are correctly ranked and their scores

are higher than the scores for the non-influential out-

liers and the normal samples (non-outliers). Also,

the figure shows that the target-aware outlier scores

are very well correlated to prediction errors for the

corresponding samples. Although, as mentioned pre-

viously, the prediction errors are assumed to not be

available at the time of these diagnostics. The PLS T

2

plot cannot even separate outliers from non-outliers.

While the SPE plot can separate in this case, below

we have the slightly modified version of this example

where it fails too.

Figure 2 shows plots of PLS T

2

contribution

scores and target-aware outlier score contributions for

the first 16 test samples.

Again PLS does not correctly rank and separate

the relevant and irrelevant contributors. The target-

aware outlier scores correctly detect and rank both the

outliers and the contributing attributes with respect to

their effect on the target.

However, when the number of noise attributes in-

crease and the outliers do not deviate much from zero,

the SPE and T

2

plots may not detect them at all. Con-

sider a simplified version of the above linear example

with 100 noise attributes, and each i-th outlier is cre-

ated by setting x

i

= 5. Figure 3) shows PLS SPE and

T

2

plots vs the target-aware scores plot for this exam-

ple.

It can be seen that now SPE cannot readily iden-

tify outliers, although their scores are slightly above

average, and T

2

shows only the single most influential

outlier.

4.2 Nonlinear Data

Next we consider a similar example with the target a

nonlinear function of inputs–a quadratic target func-

tion y = x

2

1

+0.5x

2

2

+0.3x

2

3

+0.15x

2

4

. All other settings

were similar to the previous experiment, except we

used four latent components for PLS (again as sug-

gested by a 10-fold cross-validation model error plot).

Figure 4 shows PLS SPE and T

2

plots for 35 (last)

training samples and all test samples for this example,

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

21

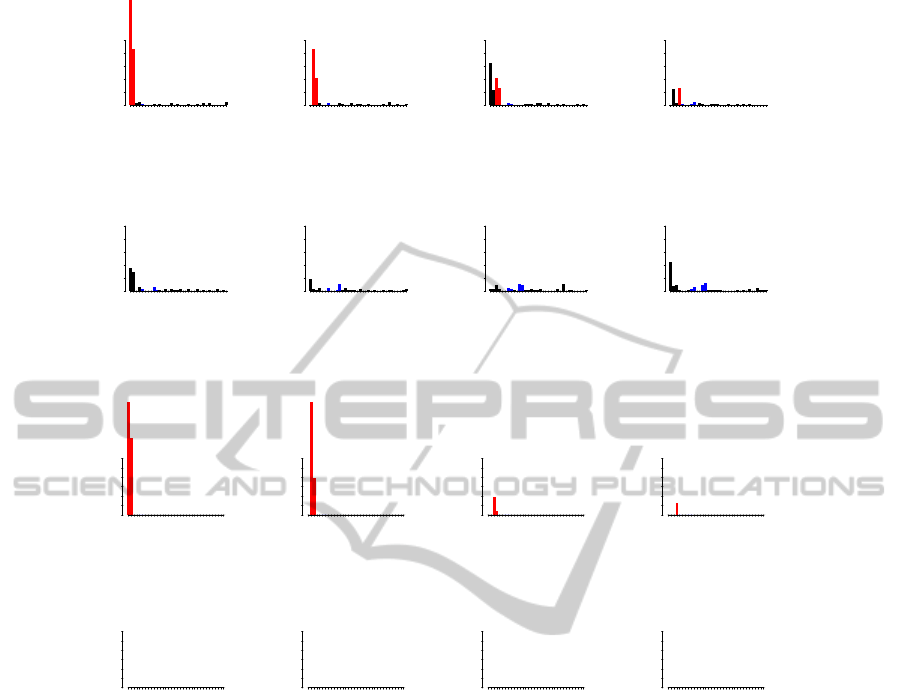

1 6 12 19 26 33

obs501

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs502

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs503

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs504

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs505

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs506

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs507

variables

PLS T^2 contr

0.00 0.10 0.20

1 6 12 19 26 33

obs508

variables

PLS T^2 contr

0.00 0.10 0.20

(a) Contribution from PLS T

2

scores.

1 6 12 19 26 33

obs501

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs502

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs503

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs504

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs505

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs506

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs507

variables

GBT contr

0 4 8 12

1 6 12 19 26 33

obs508

variables

GBT contr

0 4 8 12

(b) Contributions from target-aware outlier scores.

Figure 5: T

2

score contribution plot from PLS vs. contribution plot for our target-aware method for nonlinear data. Contri-

butions for all variables are shown for the first 8 test samples. Correct relevant contributors are shown with red bars. Other

contributors are shown with blue bars. For the first 3 outliers there are 2 relevant contributors, the fourth outlier has only 1

relevant contributor, and the other four groups have none.

along with our target-aware outlier scores plot.

Figure 4 indicates that PLS cannot distinguish

the influential and non-influential outliers (actually it

does not separate even the last two influential out-

liers), while the target-awareoutlier scores plot gener-

ates the correct results. It shows that all four influen-

tial outliers are correctly detected and ranked, without

false alarms. Also it can be seen that the target-aware

outlier scores are well correlated to prediction errors

for corresponding samples. The PLS T

2

plot fails to

separate even outliers from non-outliers.

Figure 5 shows plots of PLS T

2

contribution

scores and target-aware outlier score contributions for

the first 16 test samples.

Again PLS fails to correctly rank and separate rel-

evant and irrelevant contributors. Still, target-aware

outlier scores correctly rank the outliers and the con-

tributing attributes with respect to their effect on the

target.

5 CONCLUSIONS

The target-aware anomaly detection and associated

contribution problem is introduced to the machine

learning community and a solution for complex data

from modern systems is described. Newoutlier scores

and contributions are developed, and thresholds (de-

ICINCO 2011 - 8th International Conference on Informatics in Control, Automation and Robotics

22

rived from baselines obtained from target permuta-

tions) are used to filter non-influential outliers and

normal samples. The target-aware paradigm uses

target-labeled data for training, but the diagnostics are

calculated before the corresponding target attribute

value is available (to meet the conditions for pro-

cess control applications). The ensemble model al-

lows us to deal with complex interactions in predic-

tor space and local data structures. Linear methods

based on principal components often fail to detect

outliers and/or contributors in anomaly detection, es-

pecially in the presence of noise. The linear meth-

ods are also sensitive to scaling. Furthermore, linear

methods rarely work when the target is a non-linear

function of the inputs. Furthermore, methods such as

partial least squares often fail to rank the contributors

correctly and fail to separate relevant from irrelevant

contributors. When the number of irrelevant variables

increases it even can fail to identify influential outliers

on relevant predictors. The proposed method works

equally well for linear and non-linear cases in terms

of diagnostics. Our method can correctly rank out-

liers with respect to their effect on the target, rank at-

tributes that contribute to an outlier score, and filter

non-influential and normal sample. It is insensitive

to noise and ranks outliers and contributors for a data

sample using a fast, robust, nonparametric technique.

ACKNOWLEDGEMENTS

This research was partially supported by ONR grant

N00014-09-1-0656. We wish to thank anonymous

referees for comments that improved this work.

REFERENCES

Angelov, P., Giglio, V., Guardiola, C., Lughofer, E., and

Luj´an, J. (2006). An approach to model-based fault

detection in industrial measurement systems with ap-

plication to engine test benches. Measurement Science

and Technology, 17:1809.

Borisov, A., Eruhimov, V., and Tuv, E. (2006). Tree-

based ensembles with dynamic soft feature selection.

In Guyon, I., Gunn, S., Nikravesh, M., and Zadeh,

L., editors, Feature Extraction Foundations and Ap-

plications: Studies in Fuzziness and Soft Computing.

Springer.

Breiman, L., Friedman, J., Olshen, R., and Stone, C. (1984).

Classification and Regression Trees. Wadsworth, Bel-

mont, MA.

Chandola, V., Banerjee, A., and Kumar, V. (2009).

Anomaly detection: A survey. ACM Computing Sur-

veys (CSUR), 41(3):15.

Chiang, L., Russell, E., and Braatz, R. (2001). Fault de-

tection and diagnosis in industrial systems. Springer

Verlag.

Efendic, H., Schrempf, A., and Del Re, L. (2003). Data

based fault isolation in complex measurement sys-

tems using models on demand. In Proceedings of the

5th IFAC-Safeprocess 2003, IFAC, pages 1149–1154.

ACM.

Ergon, R. (2004). Informative pls score-loading plots for

process understanding and monitoring. Journal of

Process Control, 14(6):889–897.

Filev, D. and Tseng, F. (2006). Novelty detection based

machine health prognostics. In Evolving Fuzzy Sys-

tems, 2006 International Symposium on, pages 193–

199. IEEE.

Friedman, J. H. (2001). Greedy function approximation: A

gradient boosting machine. The Annals of Statistics,

29(5):1189–1232.

Hastie, T., Tibshirani, R., and Friedman, J. (2001). The

Elements of Statistical Learning. Springer.

Hodge, V. J. and Austin, J. (2004). A survey of outlier de-

tection methodologies. Artificial Intelligence Review,

22:85–126.

Hotelling, H. (1947). Multivariate quality control-

illustrated by the air testing of sample bombsights.

In Eisenhart, C., Hastay, M., and Wallis, W., edi-

tors, Techniques of Statistical Analysis, pages 111–

184. McGraw-Hill, New York.

Lughofer, E. and Guardioler, C. (2008). On-line fault detec-

tion with data-driven evolving fuzzy models. Control

and Intelligent Systems, 36(4):307–317.

Miller, P., Swanson, R., and Heckler, C. (1998). Contri-

bution plots: A missing link in multivariate quality

control. Applied Mathematics and Computer Science,

8(4):775–792.

Runger, G., Alt, F., and Montgomery, D. (1996). Con-

tributors to a Multivariate Statistical Process Control

Chart Signal. Communications in Statistics–Theory

and Methods, 25(10):2203–2213.

Wold, S., Sjostrom, M., and Eriksson, L. (2001). PLS-

regression: a basic tool of chemometrics. Chemo-

metrics and intelligent laboratory systems, 58(2):109–

130.

TARGET-AWARE ANOMALY DETECTION AND DIAGNOSIS

23