ARTIFICIAL NEURAL NETWORKS APPLIED TO AN AGENT

ACTING IN CDA AUCTIONS IN TAC

Robson G. F. Feitosa

1

, Dalmo D. J. Andrade

2

, Enyo J. T. Gonçalves

3

, Yuri A. Lacerda

1

,

Gustavo A. L. de Campos

2

and Jerffeson T. de Souza

2

1

Instituto Federal de Educação Ciência e Tecnologia do Ceará, Campus Crato (IFCE) – Crato, CE, Brazil

2

Centro de Ciências e Tecnologia, Universidade Estadual do Ceara (UECE), Fortaleza, CE, Brazil

3

Universidade Federal do Ceará (UFC), Campus Quixadá, Quixadá, CE, Brazil

Keywords: Artificial Neural Networks, Continuos Double Auction, Intelligent Agents.

Abstract: This paper describes an approach based on Artificial Neural Networks to estimate the trading price of bids

in CDA auctions in the TAC Classic scenario. To validate the approach, we used some methods to validate

the performances of both the ANN and an agent which uses the approach. By analyzing the results of the

experiments we could prove that such estimation helps improving the agent's performance.

1 INTRODUCTION

E-commerce, or electronic commerce, is an object of

study in the most various communities around the

world. According to (Vytelingum, 2006), the

auctions of Continuous Double Auction (CDA) type

are, presently, the commonest trading mechanisms

adopted in e-commerce. They are widely used by

institutions specialized in buying and selling titles

and goods, e.g., international exchange market and

stock exchange, such as New York Stock Exchange

(NYSE).

Markets such as NYSE trade several goods in

parallel, through simultaneous and independent

auctions. This way, besides the classical problems

found in the CDA trading, such as determining the

amount and values of the goods, the participants of

this market must analyze simultaneously the

evolution of several prices, in detriment of their

preferences, to choose which auctions they must

participate in. However, solving these problems is

not a trivial task.

The forecast of stock prices, options, electric

energy selling price, and other goods negotiated in

CDA markets can be modeled with use of statistical

techniques, intelligent systems or hybrid ones,

involving both of the previous (Melo et al., 2009).

Fuzzy systems (Petridis and Kehagias, 1997) and

ANNs (Ko et al., 2008) (Soares, 2008) are some of

the techniques employed in intelligent and hybrid

systems to support the forecast process in CDA

markets.

The study carried out by (Das et al., 2001)

proved that intelligent agents can overcome the

performance of humans at trading. These agents can

be employed in the simultaneous monitoring of

several markets, in the processing of a large amount

of information and in the execution of complex

calculations almost instantly.

Aiming at the development of high-level

research in trading agents, researchers from

Michigan University developed the TAC (Trading

Agent Competition) environment (Wellman and

Wurman, 1999). TAC is composed by a forum about

the subject of trading agents and a series of annual

tournaments. In addition, it is offered a complete

software infrastructure to the development and

simulation of trading agents, which eases the

generation of knowledge in the area.

TAC Classic is one of the tournaments created

and made available by the TAC forum. On it, agents

play the role of travel agencies whose objective is to

form travel packages according to the costumers'

portfolio. For that, the agents must buy travel goods

(air tickets, hotel rates and entertainment tickets).

Each good is traded in auctions of a certain type,

which occur simultaneously and separately. For

example, entertainment tickets are traded in separate

and simultaneous auctions of the CDA type.

271

G. F. Feitosa R., D. J. Andrade D., J. T. Gonçalves E., A. Lacerda Y., A. L. de Campos G. and T. de Souza J..

ARTIFICIAL NEURAL NETWORKS APPLIED TO AN AGENT ACTING IN CDA AUCTIONS IN TAC.

DOI: 10.5220/0003726302710276

In Proceedings of the 4th International Conference on Agents and Artificial Intelligence (ICAART-2012), pages 271-276

ISBN: 978-989-8425-95-9

Copyright

c

2012 SCITEPRESS (Science and Technology Publications, Lda.)

This paper describes an approach based in

Artificial Neural Networks (ANN) to estimate the

transaction price of CDA auction bids in the TAC

Classic scenario. For that, the work is organized as

follows. Section 2 describes the proposed approach.

Section 3 discusses the analysis of results obtained

through the use of the approach. Finally, Section 4

presents some conclusions and future works.

2 THE APPROACH BASED ON

ARTIFICIAL NEURAL

The approach described herein was conceived

through the implementation of an agent called

LaconiBot, a software agent developed to act in the

TAC Classic environment. In this section we

present: the architecture of the agent; the logic

employed on its forecast component; details on the

implementation of the ANN, as well as its training

and testing methodologies.

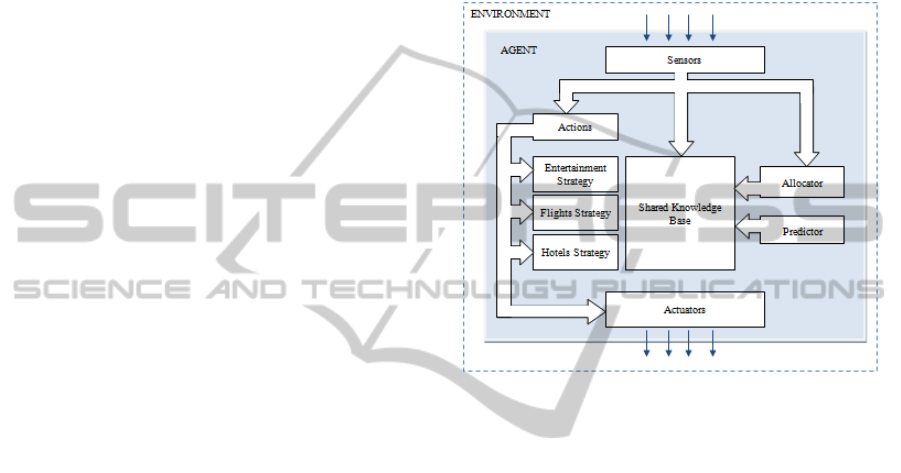

Figure 1 shows the main subsystems and

components of the LaconiBot agent (information

processing modules), as well as the information

processed by each subsystem. Among the modules

we have a Shared Knowledge Base, or SKB, which

works as a blackboard memory, where all the

modules can have access to it. So, it is possible to

share in the same data structure, both the

environment status and the agent's internal status, as,

for example: the updated values of the assessments

and other parameters used in the trade strategies, the

return of the solution presented by the Allocator

component and the price estimation calculated by

Predictor.

More specifically, this paper analyzes the

performance of the auction subsystem focused on

buying and selling tickets for entertainment, because

only in this auction type the CDA trading

mechanism is used. Leaving aside such information,

the agent can be described as follows.

By means of the Sensors the agent receives

information from the Environment - buy and sell

prices, besides the number of items which it traded.

The updates occur at each 30 seconds for all the 12

auctions. Right after that, the internal status of the

agent is updated, and the values received from the

Sensors are stored in the SKB. The actions of the

Predictor and the Allocator are executed. The

Predictor checks the pricing data and the elapsed

time of the SBK game. Next, it estimates the

transaction values for the information by means of

its ANN. The allocator, in turn, checks the SBK data

and updates the allocation of the items to be traded

by the Entertainment Strategy. The result of

allocations is stored in the SBK. (Feitosa et al.,

2010) describe the logic behind the Allocator

component in detail. According to the updated status

of the allocations in the SKB, the actions of the

Entertainment Strategy are executed. By means of

the Actuators the agent sends the actions selected by

the Entertainment Strategy for the environment.

Figure 1: LaconiBot architectural model.

The entertainment strategy uses a series of

parameters to determine a new bid. They are: the

buy price of an item in the auction, the sell price for

the same item and a reference price. The reference

prices is intended to give support to the trader's

decision making, supplying a reference to calculate

the deviation of the quoted price with respect to the

transaction value of the item. This way, the more

accurate the estimative of the value of the

transaction, the more accurate will be the decision

made by the controller, meaning a better

performance of the agent.

In this works we used an ANN to estimate the

transaction prices in CDA auctions, taking into

consideration the historical data of the auctions in

which the agent is participating or of auctions which

occurred in previous competitions. Among the

known ANN architectures, we opted for the

Multilayer Perceptron (MLP) Neural Network with

the Backpropagation learning algorithm. More

information about this in (Haykin, 2001).

In order to implement the ANN, we used the

Joone (Java Object Oriented Neural Engine)

framework (Marrone, 2007) (Heaton, 2005). It was

chosen by many reasons. Some of them are: it is

written in Java language and distributed over the

ICAART 2012 - International Conference on Agents and Artificial Intelligence

272

LGPL License, is well documented, has a well-

defined interface for the development of the ANN,

supplies several implemented classes which ease the

training and execution of the Neural Network and,

besides, is approved by the academic community

(Malcangi and Frontini, 2009) (Zhu et al., 2006).

There are several ANN architectures. However,

we opted for using a multilayer architecture. Some

works like (Melo et al., 2009) report the gain in the

performance of the ANN from a more refined choice

of its architecture. For the present work, we chose a

three-layer MLP. The first layer was composed by

three neurons, the internal layer by four neurons and

the output layer with just one neuron to represent the

output value of the network.

We opted for the supervised learning of the

ANN, which needed a training set capable of

representing both the information given as input to

the neural network and the information expected at

the output. Another necessary aspect was a dataset to

test and validate the trained ANN.

According to (Feitosa et al., 2010), TAC supplies

a complete software infrastructure for the

development, execution and analysis of the

performance of agents. This way, we used the TAC

server, some agents made available in the TAC

website, and the methodology, also described in the

same work, to generate the data that will form the

training dataset.

After analyzing the problem, it was possible to

distinguish the most important information to

compose the attributes of the training database of the

ANN. This way, we selected the buy price of the

good; the game time elapsed; the transaction value,

more formally described by the following tuple

=<

,

,,

>.

Where,

= sell price of an item at auction in the

time interval t;

= buy price of an item at auction

in the time interval t; t = elapsed game time;

=

transaction price at a given moment t.

After the execution of 70 games and the

preprocessing of data, it was generated a set with the

total of 1450 examples in the format of 4-tuples. No

separation concerning the types of ticket was made,

that is, new lines were added to a text file to form

the training set. After selecting the attributes and

generating data to form the training set, another

important step in the mining of this data is the

preprocessing. If significant amounts of data

containing noises, faulty, inconsistent or non-

normalized are presented, the ANN will possibly

have a unsatisfactory performance. So, the data

preprocessing occurs with the preparation of the

example values that will be presented to the network

in such a way that it can generalize the training set.

We carried out the following procedures.

As the number of bids that end up in a

transaction is quite smaller than the number of bids

that do not end up in a transaction, we selected only

examples where C

v

>0, C

c

>0 and P

t

>0; for values

concerning the buy and sell prices of some good, as

well as the transaction price, we noticed that: the

prices cannot be smaller than zero, because negative

prices do not exist; and the maximum prices offered

to the entertainment events do not go above 200

monetary units. So, all prices were divided by 200;

and, the calculation of the time unit was made with

basis on total time of the match. Since each match

takes 90 minutes or 540 seconds long, the time

values were divided by 540 to obtain the normalized

data.

For example, analyzing the auction for

amusement park tickets for the third day, if in the

time of 308 seconds of the auction the buy price is

$66 and the sell price is $98 and a transaction was

made by $79, the training set would generate the

following tuple T = <98.0, 66.0, 307, 79.0>. After

preprocessing, the values change to T = <0.49, 0.33,

0.57, 0.39>.

In the present work, the separation of the

examples set was made in 10 parts or instances.

After separation, 90% of data or 9/10 of the parts

were used for training and the remaining 10% for

tests. This set of techniques used for training and test

of the neural network is similar to the n-fold

stratified cross-validation technique, in this case, 10-

fold (Witten and Frank. 2005).

The training of the network by using the

described technique was performed according to the

following stages: with the training set (input and

desired response) already constructed, we separated

it in 10 parts, having in mind the equal

representation of the classes of data in each of the

parts; the parts were regrouped in 10 different

subsets, each one with 90% of the total number of

examples. Notice that for each subset created, one

part does not participate in the training set, making

sure that all the instances remain separated at least

once. The remaining part corresponds to the 10% not

used which were separated for tests; after the

separation, 10 batteries of trainings were performed.

At the end of each training session, the remaining set

will have been tested; the network training occurs

through the repetitive presentation of an example set

called epoch. The number of epochs must be chosen

so that the network result converges to a desired

minimal error. During the training of the ANN, at

each 1000 epochs the order of the values contained

ARTIFICIAL NEURAL NETWORKS APPLIED TO AN AGENT ACTING IN CDA AUCTIONS IN TAC

273

in the training set is randomly altered to minimize

any eventual tendency in the learning process;

finally, we evaluated the efficiency of the forecasts

obtained in the network using the metrics of Root

Average Squared Error (RMSE), Confusion Matrix

and Error Average, as will be described later.

3 ANALYSIS OF RESULTS

This section illustrates the process of analyzing the

results for the training, test and ANN validation

processes, as well as the results related to the gain

obtained by the agent after using the network.

With the objective of validating the training, two

forms of validation were applied. First, we evaluated

the Root Mean Square Error (RMSE) at the output

of the network. Next, we perform the analysis with

confusion matrix and, finally, we calculate the

average error obtained in the network training,

The network implemented in this project was

trained according to the 10-fold method. Hence, 10

error values were generated for each fold. So, for

each stage of network training it is generated an

error estimation, or global RMSE, and it is necessary

to calculate the average of the RMSE values. The

RMSE for each stage is calculated according to the

following equation:

=

∑

(

−

)

(1)

Where N is the number of patterns, a

k

represents

the real value and y

k

represents the expected value.

The generated values, as well as the global average

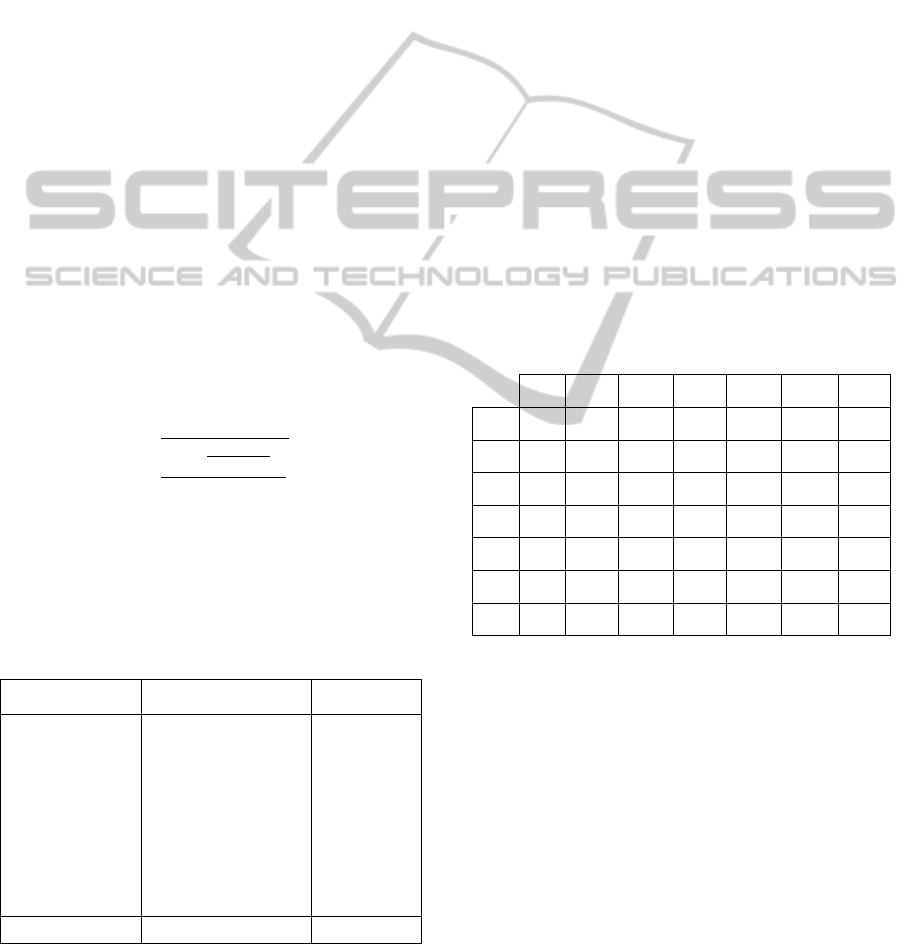

of the RMSE are shown in Table 1.

Table 1: Values of the RMSE obtained in the training of

the neural network.

Training/Test Stage RMSE RMSE * 100

1

0.03790378821188909 3.790

2

0.03792054262127483 3.792

3

0.03741238428226856 3.741

4

0.03837015819945445 3.837

5

0.0375940506948018 3.759

6

0.03772424081175014 3.772

7

0.037880241856337225 3.788

8

0.03692442292505494 3.692

9

0.037551458993737144 3.755

10

0.036275948189295366 3.627

Global Error 0.03755572367858635 3.755

As we can see in Table 1, the error generated by

the trained stayed around 4%. It is important to

highlight that just the obtainment of the RMSE is not

enough to correctly validate the training of an ANN.

So, we used another metric, illustrated in the next

section.

A confusion matrix has the objective of showing

the number of correctly classified samples for each

class of data, thus it measures the efficiency of the

process under analysis. The confusion matrix used in

this work was adapted to compare values obtained in

test of network with the expected values.

At the construction of the confusion matrix, we

adopted the percentile intervals of 0.26 to 0.30, 0.31

to 0.35 and so on until 0.56 to 0.60. Such intervals

correspond to the normalized transaction values. The

choice of these values is due to the fact that these are

the intervals in which the transaction occurs more

frequently.

The matrix was calculated for the test sets. The

confusion matrix generated for these stages

correspond to the values obtained by the test

network compared with the expected values, shown

in Table 2. We can see the rate of success of the

network in the intervals close to what should be

estimated by the matrix in Table 3.

Table 2: Confusion matrix of the network test with the

percentile of success.

[0.26-

0.30]

[0.31-

0.35]

[0.36-

0.40]

[0.41-

0.45]

[0.46-

0.50]

[0.51-

0.55]

[0.56-

0.60]

[0.26-

0.30]

64.15%

5.71% 0.00% 0.26% 0.00% 2.33% 0.00%

[0.31-

0.35]

29.25%

43.33%

14.35% 2.07% 1.76% 2.33% 0.00%

[0.36-

0.40]

3.77% 43.81%

63.43%

19.69% 12.78% 18.60% 13.64%

[0.41-

0.45]

1.89% 7.14% 22.22%

77.72%

24.23% 25.58% 31.82%

[0.46-

0.50]

0.94% 0.00% 0.00% 0.26%

61.23%

13.95% 9.09%

[0.51-

0.55]

0.08% 0.00% 0.00% 0.00% 0.00%

34.88%

22.73%

[0.56-

0.60]

0.00% 0.00% 0.00% 0.00% 0.00% 2.33%

22.73%

In the presented matrix, the vertical values represent

the real expected data and the horizontal values

represent the data estimated by the network. For

example, analyzing Table 2 in the interval of 0.36 to

0.40, the network was successful in 1241 forecasts,

or 53.03 of the total of forecasts for that interval. To

obtain real price data, just multiply the value by 200

(the inverse path of normalization).

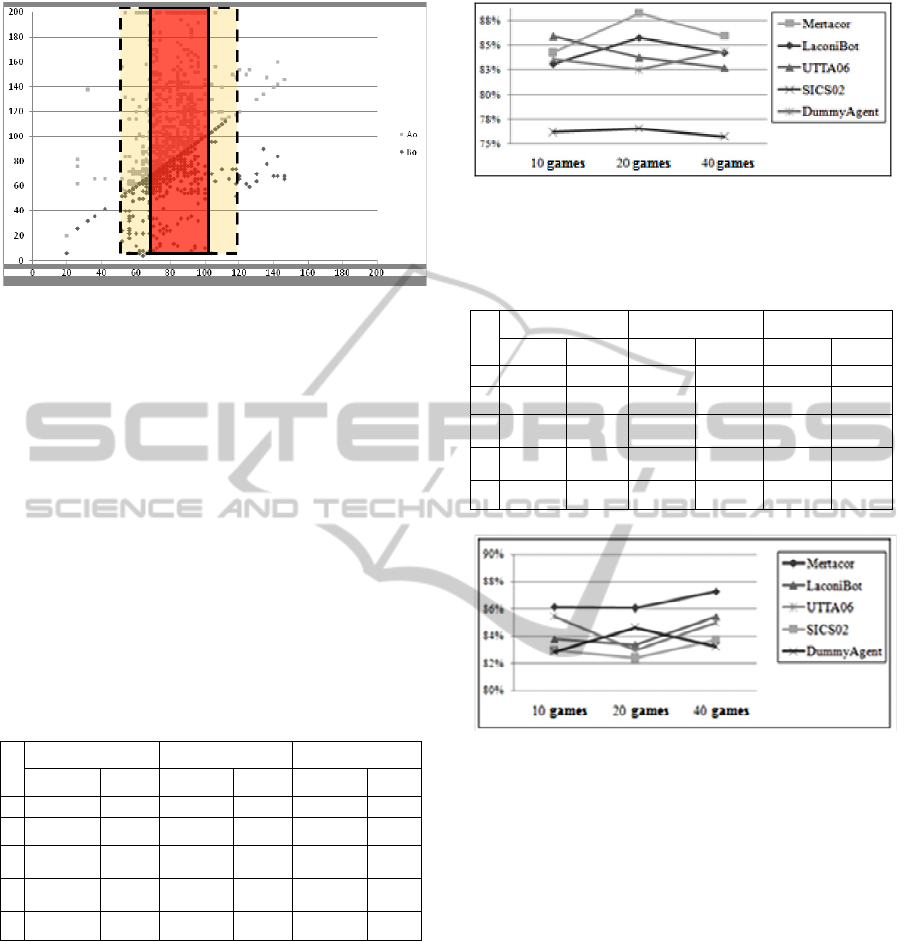

The graph of Figure 2 illustrates the distribution

of buy, sell and transaction prices data retrieved

from the training set. In this graph are represented

the buy prices (Bo) and sell prices (Ao) right before

the materialization of a transaction, whose value

corresponds to the abscissas axis (horizontal). The

rectangle with dashed edges illustrates the limits of

data analyzed in the confusion matrix (between $52

ICAART 2012 - International Conference on Agents and Artificial Intelligence

274

Figure 2: Graph of Buy Prices (Bo) and Sell Prices (Ao) X

Transaction price.

and $120) and the rectangle with flat edges

illustrates the limits of data with the highest number

of instances and, also, where occurred the best

performance of the ANN, presented in the confusion

matrix (between $72 and $100).

Table 3 and the graph of Figure 3 illustrate the

performance of the LaconiBot agent without the

Predictor component. Analyzing them, we notice

that the agent a average of 9316.22 and average of

84.37% of the optimal percentage. The average

points of the first placed was of 9497.47, that is, the

difference between the agent and the first placed was

of 181.25 points, or 1.90%.

Table 3: Points and classification of the LaconiBot agent

without the Predictor.

10 games 20 games 40 games

Agent Points Agent Points Agent Points

1º Mertacor

9460.43

Mertacor

9562.20

Mertacor

9469.79

2º LaconiBot

9372.86

LaconiBot

9321.54

LaconiBot

9254.27

3º UTTA06

9249.43

UTTA06

9298.85

Dummy

Agent

9222.63

4º

Dummy

Agent

9230.95

Dummy

Agent

9233.11

UTTA06

9180.90

5º SICS02

8234.58

SICS02

8337.40

SICS02

8356.34

The graph of Figure 3 shows that the presented

strategy (with the LaconiBot agent without the

Predictor component) achieved a curve which is

closer to that of Mertacor, for the optimal

percentage, when compared to other agents.

Table 4 and the graph of Figure 4 illustrate the

performance of the LaconiBot with the presence of

all components. Analyzing them, we notice that the

agent had a average of 9389.69 points and the

average of 84.19 for the optimal percentage. The

average points of the first placed was of 9489.56,

with difference of 99.87 points between the agent

and the first placed, or 1.05%.

Figure 3: Optimal percentage for the LaconiBot agent

without Predictor.

Table 4: Points and classification for the complete

LaconiBot agent.

10 games 20 games 40 games

Agent Points Agent Points Agent Points

1º

M

ertacor

9445.03

M

ertacor

9539.59

M

ertacor

9484.06

2º

L

aconiBot

9417.63

L

aconiBot

9371.73

L

aconiBot

9379.72

3º

U

TTA06

9324.26

U

TTA06

9235.29

D

ummy

A

gent

9274.00

4º

D

ummy

A

gent

9260.46

D

ummy

A

gent

9198.99

U

TTA06

9230.51

5º SICS02

9245.65

SICS02

9191.72

SICS02

9198.55

Figure 4: Optimal percentage for the complete LaconiBot

agent.

Analyzing the graph of Figure 4 again, we notice

the resemblance in the optimal percentage curve,

when comparing the agents LaconiBot and

Mertacor. The performance of points of LaconiBot

was superior to what was analyzed in the previous

battery. This situation can be explained, since the

bids sent caused a slightly more aggressive strategy,

because the return of the ANN is more precise than

the calculation done without using the ANN (median

of historical values).

Table 5 summarizes the main data needed to

evaluate the overall performance of the LaconiBot,

as well as its evolution during the incorporation of

its Predictor component, when compared to the

agent without ANN.

As observed in the summary of the table above,

the complete LaconiBot achieved a performance

superior in the average of points. Besides, it

managed to lower the difference between its points,

ARTIFICIAL NEURAL NETWORKS APPLIED TO AN AGENT ACTING IN CDA AUCTIONS IN TAC

275

Table 5: Summary of all results.

Agent

Average

of places

Optimal

Average

%

Final

Points

Average

%

Difference

for 1

st

LaconiBot

sem RNA

2 84,37 9316,22 1,90

LaconiBot

Completo

2 84,19 9389,69 1,05

when compared to the winner agent (the Mertacor

agent). Despite the average of the optimal

percentage had no improvements, we notice an

improvement in the real performance of the agent

(average of points).

4 CONCLUSIONS AND FUTURE

WORKS

Research in electronic commerce, trading agents and

negotiation strategies in CDA environments have

been pushed by researchers all over the world by the

use of statistical and artificial intelligence

techniques. As a contribution, this work proved in an

empirical fashion that the approach herein described

to calculate the estimation of prices of goods

negotiated in CDA auctions, applied to the TAC

scenario, is viable, bringing real benefits to the

performance of a negotiation agent. In the future, we

intend to analyze the impact in the modification of

the topology of the ANN as illustrated in (Melo et

al., 2009), the implementation of other ANN models

besides the MLP model, and the use of an ANN

trained for each type of ticket.

Other future works include: compare the

performance of other ANN implementations, applied

to the same scenario; we also intend to generalize

the approach described to support the selection of

auctions in any CDA scenario and support the

selection of auctions in markets that use other

negotiation mechanisms; still, we intend to supply a

complete framework to support the development of

strategies for selection of auctions in the most

various electronic commerce scenarios.

REFERENCES

Das, R.; Hanson, J. E.; Kephart, J. O.; Tesauro, G., 2001.

Agent-Human Interactions in the Continuous Double

Auction. Proceedings of the Seventeenth International

Joint Conference on Artificial Intelligence.

Washington: B. Nebel, Vol.17, No.1, pp. 1169-1178.

Feitosa, Robson G. Fechine; Carmo, R.; Gonçalves, E. J.

T; Campos, G. A. L ; Souza, J. T.; Oliveira, P., 2010.

Algoritmo Genético Aplicado a um Agente para a

Seleção de Leilões do Tipo CDA do TAC. In:

AutoSoft, 2010, Salvador. CBSOFT 2010.

Haykin, S. Neural networks: a comprehensive foundation.

Prentice hall, 2001

Heaton, J., 2005. Introduction to Neural Networks with

Java. Heaton Research Inc.

Ko, Po-Chang and Lin, Ping-Chen, 2008. Resource

allocation neural network in portfolio selection.

Expert Systems with Applications, Vol.35, pp.330-

337.

Malcangi, M. and Frontini, D., 2009. Language-

independent, neural network-based, text-to-phones

conversion Neurocomputing, Elsevier, 73, 87-96.

Marrone, Paolo., 2007. Joone (Java Object Oriented

Neural Engine). Available at: www.jooneworld.com.

br.

Melo, G. S.; Campos, G. A. L.; Silva, J.; Sousa, J., 2009.

Projeto Automático De Redes Neurais Artificiais Para

O Problema De Previsão Em Séries Temporais. In:

Simpósio Brasileiro de Pesquisa Operacional, Porto

Seguro - BA. 41º Simpósio Brasileiro de Pesquisa

Operacional.

Petridis, V.; Kehagias, A., 1997. Predictive modular fuzzy

systems for time-series classification. IEEE

Transactions on Fuzzy Systems 5: 381-397.

Soares, A. S., 2008. Predição de séries temporais

econômicas por meio de redes neurais artificiais e

transformada wavelet: combinando modelo técnico e

fundamentalista. Universidade de São Paulo.

Vytelingum, P., 2006. The Structure and Behaviour of the

Continuous Double Auction. PhD, School of

Electronics and Computer Science, University of

Southampton.

Wellman, M. and Wurman, P., 1999. A trading agent

competition for the research community, IJCAI-99

Workshop on Agent-Mediated Electronic Commerce,

Stockholm.

Witten, I. H. and Frank, E, 2005. Data mining: practical

machine learning tools and techniques. Elsevier.

Zhu, J.; Liu, C.; Gong, J.; Wang, D.; Song, T., 2006. A

Distributed Computing Service for Neural Networks

and Its Application to Flood Peak Forecasting Neural

Information Processing, 890-896.

ICAART 2012 - International Conference on Agents and Artificial Intelligence

276