MAXIMUM LIKELIHOOD ESTIMATION OF MULTIVARIATE

SKEW T-DISTRIBUTION

Leonidas Sakalauskas and Ingrida Vaiciulyte

Institute of Mathematics and Informatics, Vilnius University, Akademijos 4, Vilnius, Lithuania

Keywords: Monte – Carlo Markov chain, Skew t distribution, Maximum likelihood, Gaussian approximation, EM –

algorithm, Testing hypothesis.

Abstract: The present paper describes the Monte – Carlo Markov Chain (MCMC) method for estimation of skew t –

distribution. The density of skew t – distribution is obtained through a multivariate integral, using

representation of skew t – distribution by a mixture of multivariate skew – normal distribution with the

covariance matrix, depending on the parameter, distributed according to the inverse – gamma distribution.

Next, the MCMC procedure is constructed for recurrent estimation of skew t – distribution, following the

maximum likelihood method, where the Monte – Carlo sample size is regulated to ensure the convergence

and to decrease the total amount of Monte – Carlo trials, required for estimation. The confidence intervals of

Monte – Carlo estimators are introduced because of their asymptotic normality. The termination rule is also

implemented by testing statistical hypotheses on an insignificant change of estimates in two steps of the

procedure.

1 INTRODUCTION

Stochastic optimization plays an increasing role in

modeling and statistical analysis of complex

systems. Conceptually, detection of structures in real

– life data is often formulated in the framework of

combinatorial or continuous optimization by using

the following stochastic techniques: Monte – Carlo

Markov chains, Metropolis – Hastings algorithm,

stochastic approximation, etc. (Rubinstein and

Kroese, 2007; Spall, 2003). In the present paper the

maximum likelihood approach for estimating the

parameters of the multivariate skew t – distribution

is developed, using the adaptive Monte – Carlo

Markov chain approach. Multivariate skew t –

distribution is often applied in the analysis of

parametric classes of distributions that exhibit

various shapes of skewness and kurtosis (Azzalini

and Genton, 2008; Cabral, Bolfarine and Pereira,

2008). In general, the skew t – distribution is

represented by a multivariate skew – normal

distribution with the covariance matrix, depending

on the parameter, distributed according to the

inverse – gamma distribution. According to this

representation, the density of skew t – distribution as

well as the likelihood function are expressed through

multivariate integrals that are convenient to be

estimated numerically by Monte – Carlo simulation.

Denote the skew t – variable by

),,,( bST ΘΣ

μ

. In

general, a multivariate skew t – distribution defines a

random vector

X

that is distributed as a multivariate

Gaussian vector:

)()(

2

1

2

1

)/(),,,(

axaxt

d

T

ettaxf

−⋅Σ⋅−⋅−

−

−

⋅Σ⋅=Σ

π

(1)

where the vector of mean

a

, in its turn, is

distributed as a multivariate Gaussian

()

tN 2/,Θ

μ

in

the half – plane

0)( ≥

−

⋅

μ

aq

, where

,

d

Rq ⊂

0,0 ≥

Θ

≥

Σ

are the full rank

dd ×

matrices,

d

is the

dimension, and the random variable

t

follows from

the Gamma distribution:

t

b

e

b

t

btf

−

−

⋅

Γ

=

)2/(

),(

1

2

1

(2)

By definition,

d

– dimensional skew t –

distributed variable

X

has the density:

∫∫

∞

≥−⋅

⋅Θ⋅Σ⋅=ΘΣ

00)(

1

),(),,,(),,,(2),,,,(

μ

μμ

aq

dadtbtftaftaxfbxp

(3)

This distribution is often considered in the

statistical literature, where it is applied in financial

forecasting (Azzalini and Capitanio, 2003; Azzalini

and Genton, 2008; Kim and Mallick, 2003;

Panagiotelis and Smith, 2008).

200

Sakalauskas L. and Vaiciulyte I..

MAXIMUM LIKELIHOOD ESTIMATION OF MULTIVARIATE SKEW T-DISTRIBUTION.

DOI: 10.5220/0003727002000203

In Proceedings of the 1st International Conference on Operations Research and Enterprise Systems (ICORES-2012), pages 200-203

ISBN: 978-989-8425-97-3

Copyright

c

2012 SCITEPRESS (Science and Technology Publications, Lda.)

2 THE MAXIMUM LIKELIHOOD

ESTIMATION OF

MULTIVARIATE SKEW

T – DISTRIBUTION

Let a matrix of observations be

given

⎟

⎠

⎞

⎜

⎝

⎛

=

K

XXXX ,...,

2

,

1

, where

i

X

independent

vectors, distributed as

),,,( bST ΘΣ

μ

. We will examine

the estimation of parameters

b,,, ΘΣ

μ

, following to

maximum likelihood approach. The log – likelihood

function can be expressed as:

b

K

i

i

bXpbL

,,,

1

max)),,,,(ln(),,,(

ΘΣ

=

→ΘΣ−=ΘΣ

∑

μ

μμ

(4)

The optimality conditions in this problem are

derived by taking and setting the first derivatives

with respect to parameters to be estimated equal to

zero. Then the maximum likelihood estimates

(MLE)

b

ˆ

,

ˆ

,

ˆ

,

ˆ

ΘΣ

μ

of parameters of multivariate skew t

– distribution (3) are found by solving the equations,

obtained in this way, subject to

0,0 ≥

Θ

≥Σ

.

Derivatives of the likelihood function are expressed

through derivatives of the density function. By

virtue of the Euler’s formula the skew t –

distribution density is as follows:

∫

∏

≥−⋅

+

−

=

⋅Θ⋅Σ⋅

⎟

⎠

⎞

⎜

⎝

⎛

+⋅

=ΘΣ

0)(

2

2

1

2

1

1

0

2

2

),,,,(

μ

π

μ

aq

d

b

d

d

i

da

A

i

b

bxp

(5)

where

.1)()()()(

11

+−⋅Θ⋅−+−⋅Σ⋅−=

−−

μμ

aaaxaxA

TT

After differentiation of this expression and using

the Euler’s formula again, we have:

dadtbtftaftaxfaxt

bxp

aq

),(),,,(),,,()(

),,,,(

1

00)(

1

⋅Θ⋅Σ⋅−⋅Σ⋅=

∂

ΘΣ∂

∫∫

∞

≥−⋅

−

μ

μ

μ

μ

(6)

()

dadtbtftaftaxf

axaxt

bxp

aq

T

),(),,,(),,,(

)()(

),,,,(

1

00)(

111

⋅Θ⋅Σ×

×Σ⋅−⋅−⋅Σ⋅+Σ−=

Σ∂

ΘΣ∂

∫∫

∞

≥−⋅

−−−

μ

μ

μ

(7)

()

dadtbtftaftaxf

aat

bxp

aq

T

),(),,,(),,,(

)()(

),,,,(

1

00)(

111

⋅Θ⋅Σ×

×Θ⋅−⋅−⋅Θ⋅+Θ−=

Θ∂

ΘΣ∂

∫∫

∞

≥−⋅

−−−

μ

μμ

μ

μ

(8)

dadtbtftaftaxf

i

b

A

b

bxp

aq

d

i

),(),,,(),,,(

2

1

)ln(

),,,,(

1

00)(

1

0

⋅Θ⋅Σ×

×

⎟

⎟

⎟

⎟

⎠

⎞

⎜

⎜

⎜

⎜

⎝

⎛

+

+−=

∂

ΘΣ∂

∫∫

∑

∞

≥−⋅

−

=

μ

μ

μ

(9)

Let us introduce the conditional density:

),,,,(

),(),,,(),,,(2

),,,,,(

1

bxp

btftaftaxf

xbtaf

ΘΣ

⋅Θ⋅

Σ

⋅

=ΘΣ

μ

μ

μ

(10)

It is easy to see that MLE satisfy the following

equations:

(

)

0)(

1

1

=−⋅

∑

=

K

i

ii

XaXtE

K

(11)

(

)

∑

=

−⋅−⋅=Σ

K

i

iTii

XaXaXtE

K

1

)()(

1

ˆ

(12)

(

)

∑

=

−⋅−⋅=Θ

K

i

iT

XaatE

K

1

)

ˆ

()

ˆ

(

1

ˆ

μμ

(13)

1

0

1

1

2

1

ˆ

ˆ

1

ˆ

ln( )

2

d

i

K

i

i

K

i

b

b

E

AX

−

=

=

⋅

⋅

+

=

⎛⎞

⋅

⎜⎟

⎝⎠

∑

∑

(14)

where

,1)

ˆ

(

ˆ

)

ˆ

()(

ˆ

)(

ˆ

11

+−⋅Θ⋅−+−⋅Σ⋅−=

−−

μμ

aaaXaXA

TiTi

and conditional expectation is taken for

b

ˆ

,

ˆ

,

ˆ

,

ˆ

ΘΣ

μ

.

3 MONTE – CARLO MARKOV

CHAIN

Now it is convenient to calculate the estimates of

parameters by an iterative stochastic optimization

method, starting from some initial values.

Let us consider the application of the Monte –

Carlo Markov chain to implement the method

proposed. Say, random variables and vectors are

generated:

,

0if,

0if,

),,0(N~),

2

(Gamma~

⎪

⎩

⎪

⎨

⎧

<⋅−

≥⋅+

=Θ

jjk

jjk

jkj

k

j

q

q

G

b

B

ηημ

ηημ

η

where

k

Nj ,,2,1,0 K=

,

k

N

is the Monte – Carlo sample

size at the

th

k

step,

K,2,1,0

=

k

, and

0000

,,, bΘΣ

μ

are

some initial approximations. Then

∑

=

+

+=

K

i

ki

ki

kk

P

M

K

1

,

,

1

1

μμ

(15)

∑

=

+

=Σ

K

i

ki

ki

k

P

S

K

1

,

,

1

1

(16)

∑

=

+

=Θ

K

i

ki

ki

k

P

T

K

1

,

,

1

1

(17)

∑

−

=

+

+

+

⋅

⋅=

1

0

1

1

1

2

11

d

i

k

k

k

b

i

h

b

(18)

where the Monte – Carlo estimators are as follows:

∑

=

Σ=

k

N

j

kjj

i

k

ki

BGXf

N

P

1

,

),,,(

1

(19)

()

∑

=

Σ=

k

N

j

kjj

i

k

ki

BGXf

N

P

1

2

,

),,,(

1

1

(20)

()

∑

=

Σ⋅⋅−=

k

N

j

kjj

i

jj

i

k

ki

BGXfBGX

N

M

1

,

),,,(

1

(21)

()()

),,,(

1

1

, kjj

i

j

N

j

T

j

i

j

i

k

ki

BGXfBGXGX

N

S

k

Σ⋅⋅−⋅−=

∑

=

(22)

()()

,

1

1

(,,,)

k

N

T

i

ik jk jk j jjk

k

j

TGGBfXGB

N

μμ

=

=

−⋅− ⋅⋅ Σ

∑

(23)

MAXIMUM LIKELIHOOD ESTIMATION OF MULTIVARIATE SKEW T-DISTRIBUTION

201

∑

=

Σ⋅=

k

N

j

kjj

i

k

k

ki

BGXfA

N

B

1

,

),,,()ln(

1

(24)

()

∑

=

Σ⋅=

k

N

j

kjj

i

k

k

ki

BGXfA

N

B

1

2

,

),,,()ln(

1

1

(25)

() ()

∑∑∑

===

===

K

i

ki

ki

k

k

K

i

ki

ki

k

K

i

ki

ki

k

P

B

K

N

V

P

P

K

Q

P

B

K

h

1

2

,

,

1

2

,

,

1

,

,

1

,

1

1

,

1

(26)

Next, the estimate of the log – likelihood

function (4) is obtained using the Monte – Carlo

estimate (19):

()

∑

=

−=

K

i

kik

PL

1

,

ln

(27)

The 95% confidence interval of the estimate of

the log – likelihood function might also be estimated

by the Monte – Carlo method:

⎥

⎥

⎦

⎤

⎢

⎢

⎣

⎡

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

−

⋅

⋅+

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

−

⋅

⋅−

∑∑

==

K

i

ki

kki

k

k

K

i

ki

kki

k

k

P

NP

N

L

P

NP

N

L

1

2

,

,

1

2

,

,

1

2

2

,1

2

2

(28)

where

()

.),,,(

1

2

1

2

,

∑

=

Σ=

k

N

j

kjj

i

k

ki

BGXf

N

P

As it follows from equations derived (15) – (18),

the Monte – Carlo chain can be terminated at the

th

k

step, if difference between estimates of two current

steps differs insignificantly:

kkkkkkkk

bb ≈Θ≈ΘΣ≈Σ≈

++++ 1111

,,,

μ

μ

(29)

and, besides, Monte – Carlo estimates are presented

with an admissible confidence interval. Note, since

estimators (19) – (26) are averages of a large number

of identically distributed random variables, their

distribution is approximated, using CLT. Hence, the

statistical criteria about the equality of sampling

mean and covariance matrices to the given vector or

matrices can be used for testing termination

condition (29). It is more convenient to test

hypothesis

kk

hh ≈

+1

instead of

kk

bb ≈

+1

, using the test

for comparison of means from two populations with

the same variance. Thus, the hypothesis on the

termination condition is rejected, if

()()()

()

()

()

()

]

()

p

kk

kk

kkkk

kkk

T

kk

k

k

k

k

k

k

Z

hV

hh

KNd

Q

K

H

,

2

1

2

1

1

1

1

1

1

1

1

11

2SPSP

lnln

α

μμμμ

>

−

−

⋅⋅+⋅−Θ⋅Θ+Σ⋅Σ+

+−⋅Σ⋅−

⎢

⎢

⎣

⎡

+

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

Θ

Θ

−

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

Σ

Σ

−⋅=

+

+

−

+

−

+

+

−

+

++

(30)

where

p

Z

,

α

is the quantile of

2

χ

distribution with

1)2( ++⋅= ddp

degrees of freedom,

α

is the

significance level.

Note that there is no great necessity to estimate

the likelihood function with a high accuracy on

starting the optimization, because then it is enough

to evaluate only an approximate direction, leading to

its maximum. The next rule of sample size

regulation is implemented; in order large samples

would be taken only at the moment of making the

decision on termination of the Monte – Carlo

Markov chain:

k

k

p

k

H

N

ZN ⋅≥

+

,

1

β

(31)

where

β

is the significance level (Sakalauskas,

2000).

4 NUMERICAL EXAMPLE

The random

),,,( bST

Θ

Σ

μ

sample with

100=K

has

been simulated to explore the approach developed.

The above computational scheme has been used

satisfactorily in numerical work with the following

model data:

()

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

=Θ

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

=Σ===

55.286.0

86.067.3

,

9.227.0

27.061.1

,21,5,2

μ

bd

(32)

The Monte – Carlo Markov chain of 100

estimators (15) – (29) has been computed with the

following initial data:

.5.1,5.1,5.1,5.1

0000

bb ⋅=Θ⋅=ΘΣ⋅=Σ⋅=

μμ

The changes of the log – likelihood function

estimate (27), termination statistics (30), sample size

(31) and the length of the confidence interval (28)

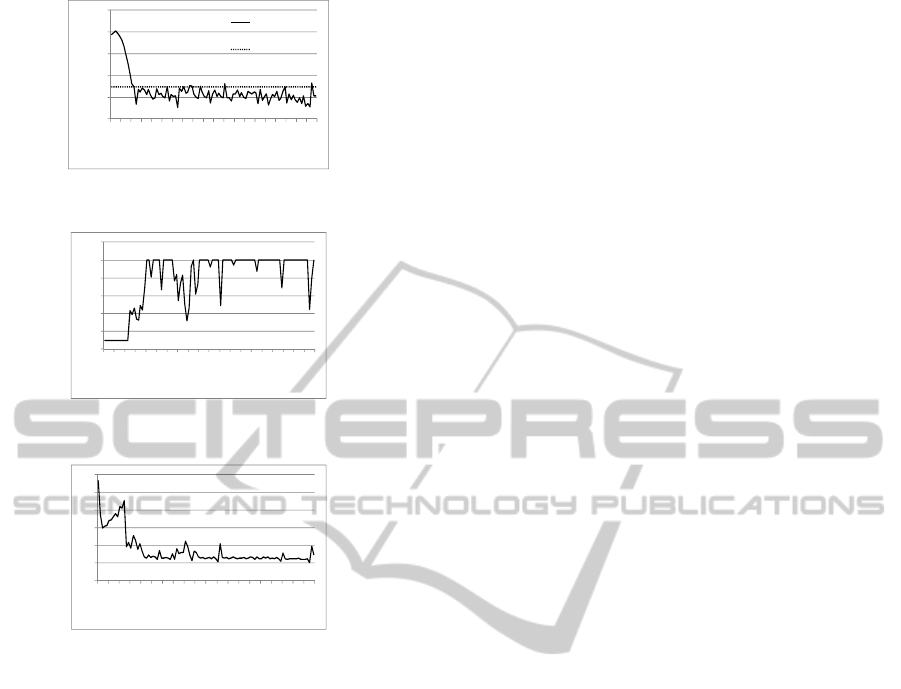

are depicted in Figures 1 – 4. As we see in Figure 1,

the log – likelihood function is decreasing until the

zone of possible solution is achieved.

Correspondingly, the termination criteria in Figure 2

are decreasing too, until the critical value of

termination is achieved. The sample size in Figure 3

is changed so that it was small starting the chain and

increased in the zone of possible solution. To avoid

very small or very large sample sizes, the following

limits were applied:

5000500 ≤≤

k

N

.The length of

the confidence interval in Figure 4 and the error of

estimates decreased as well. The termination

conditions started to be valid at

33=k

.

270

290

310

330

350

370

390

5 152535455565758595

k

Figure 1: Log – likelihood function.

ICORES 2012 - 1st International Conference on Operations Research and Enterprise Systems

202

1

10

100

1000

10000

100000

5 152535455565758595

k

test

critical value

Figure 2: Termination test.

0

1000

2000

3000

4000

5000

6000

5 152535455565758595

k

Figure 3: Sample size

k

N

.

0

0,4

0,8

1,2

1,6

2

2,4

5 152535455565758595

k

Figure 4: Confidence interval.

The maximum likelihood estimates (11) – (14),

obtained from this sample by means of the

subroutine Minimize () of MathCAD, are as

follows:

()

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

=Θ

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

=Σ==

52.1475.0

475.035.2

ˆ

,

86.2708.0

708.091.1

ˆ

,08.295.0

ˆ

,9.3

ˆ

μ

b

(33)

5 CONCLUSIONS

Stochastic optimization approach by the Monte –

Carlo Markov Chain (MCMC) method for

estimation of the skew t – distribution has been

developed in the paper. It distinguishes by adaptive

regulation of Monte – Carlo sample size and

treatment of the simulation error in the statistical

manner. Furthermore, the computer example with

test data have illustrated that numerical properties of

the method correspond to the theoretical model.

REFERENCES

Azzalini, A. and Capitanio, A. (2003). Distributions

Generated by Perturbation of Symmetry with

Emphasis on a Multivariate Skew t Distribution.

Journal of the Royal Statistical Society: Series B

(Statistical Methodology), 65, 367 – 389.

Azzalini, A. and Genton, M. G. (2008). Robust Likelihood

Methods Based on the Skew – t and Related

Distributions. International Statistical Review, 76 (1),

106 – 129.

Cabral, C. R. B., Bolfarine, H. and Pereira, J. R. G.

(2008). Bayesian Density Estimation using Skew

Student-t-normal Mixtures. Computational Statistics

and Data Analysis, 52 (12), 5075-5090.

Kim, H. M. and Mallick B. K. (2003). Moments of

Random Vectors with Skew t Distribution and their

Quadratic Forms. Statistics & Probability Letters, 63,

417–423.

Panagiotelis, A. and Smith, M. (2008). Bayesian Density

Forecasting of Intraday Electricity Prices using

Multivariate Skew t Distributions. International

Journal of Forecasting, 24, 710–727.

Rubinstein, R. Y. and Kroese, D. P. (2007). Simulation

and the Monte Carlo Method (2nd ed.). New York:

Wiley.

Sakalauskas, L. (2000). Nonlinear Stochastic Optimization

by Monte-Carlo Estimators. Informatica, 11 (4), 455-

468.

Spall, J. C. (2003). Introduction to Stochastic Search and

Optimization: Estimation, Simulation, and Control.

New York: Wiley.

MAXIMUM LIKELIHOOD ESTIMATION OF MULTIVARIATE SKEW T-DISTRIBUTION

203