A Hybrid Solver for Maximizing the Profit of an Energy Company

Łukasz Domagała, Tomasz Wojdyła, Wojciech Legierski and Michał Swiderski

Faculty of Automatic Control, Electronics and Computer Science, Silesian University of Technology,

16 Akademicka Str., 44-100 Gliwice, Poland

Keywords:

Optimization, Profit, Energy, Industry.

Abstract:

An energy company manages power stations, handles sales and purchases of electrical energy, CO2 emission

permits and other goods. The goal of such a company is to ensure energy safety of its clients and maximize

the profit. The problem is complex because of its structure and size therefore efficient automated approaches

for solving it are in demand. We have generalized the problem definition to account for any structure of the

power stations, market data and time scope. The definition describes a non-linear combinatorial optimiza-

tion problem. We have tested a number of approaches including: constraint/ logic/ dynamic/ integer/ linear

programming, local search and their hybrids using prototypes with input data from a real life process. We

present a hybrid solver to produce an acceptable, near optimal solution which satisfies the requirements of an

industrial application. Our research is a road-sign for development of similar software for the energy industry.

1 INTRODUCTION

The aim of the solver is to return a schedule of pro-

duction, sales and purchases of all the goods for a

given time horizon that satisfies all the hard con-

straints and optimizes the objective function. Hard

constraints are these that cannot be violated in the so-

lution. Satisfying them guarantees that technological

and marketing requirements are met and ensures the

energy safety of the company’s clients. The objective

function is the company’s profit gained for a given

time horizon. Maximizing this profit is the main goal.

The optimization is performed for problem instances

which consist of: technological capabilities and pa-

rameters of the power stations, market plans and es-

timates supplied by marketing and financial experts,

trade contracts, initial states for those goods that can

be accumulated.

2 PROBLEM DEFINITION

We haveobtained instances of the profit maximization

problem during work on a commercial project. Bas-

ing on the problem instances, we have built a general-

ized problem definition that accounts for any structure

of the power stations, market data and time scope. To

the best knowledge of the authors a definition of such

a problem has never been published before.

2.1 Timing and Notation

The production, trade and constraint setup is per-

formed for discrete time periods. h ∈ [1,H] is the

shortest period called, for convenience, an hour.

Each value of h is categorized as peak or off-

peak. Furthermore, consecutive values of h are

grouped into periods (H

m−1

,H

m

] = M

m

indexed by

m ∈ [1,M] where H

0

= 0,H

m−1

< H

m

,H

M

= H ,

which are, for convenience, called months. The

period of [1,H] = y is, for convenience, called a

year. An energy company handles the following

goods: energy {en}, CO2 emission permits {ep

p

, p ∈

[1,P]}, financial benefits {be

b

,b ∈ [1,B]}. An en-

ergy company handles the following objects: power

stations, production units, sales, purchases. Some

object-period pairs have corresponding control vari-

ables v(object, period). Numerical (unless otherwise

stated) attributesα(type,object/good, period) are at-

tached to objects/goods, where period denotes the pe-

riod to which it applies. The term ”volume” is used to

describe the quantity of some good.

2.2 Energy Production and Trade

An energy company (ec) is divided into power sta-

tions {ps

s

: s ∈ [1,S]}. Each power station ps

s

is di-

vided into production units {pu

s

i

: i ∈ [1,U

s

]} which

produce (electrical) energy. ec manages the volumes

278

Domagała Ł., Wojdyła T., Legierski W. and

´

Swiderski M..

A Hybrid Solver for Maximizing the Profit of an Energy Company.

DOI: 10.5220/0004000602780283

In Proceedings of the 14th International Conference on Enterprise Information Systems (ICEIS-2012), pages 278-283

ISBN: 978-989-8565-10-5

Copyright

c

2012 SCITEPRESS (Science and Technology Publications, Lda.)

vps

s,h

of energy supplied by ps

s

in period h. vps

s,h

=

f pv

s,h

(

∑

U

s

i=1

v(pu

s

i

,h)) where f pv

s,h

is a piecewise lin-

ear function. f pv

s,h

includes a number of compo-

nents:

• The actions of a regulatory body, which may in-

tervene with the production plans and are meant

to regulate the energy market. These actions are

predicted by experts as a piecewise linear function

frp

s,h

(

∑

U

s

i=1

v(pu

s

i

,h)).

• The error factor α(zo, ps

s

,h) associated with the

imperfections of the energy distribution network

• The sales of energy {v(se

s

i

,h) : i ∈ [1, Se

s

]} man-

aged privately by the ps

s

The energy trade consists of purchases {ze

i

: i ∈

[1,Ze]} and sales {se

i

: i ∈ [1,Se]} managed by the ec.

The trade is further divided into contracts and plans.

The contract is a signed trade agreement, whereas the

trade plan is based on the expert predictions. This dis-

tinction, however, is reflected in the variable domains

and is transparent for the solver.

2.3 CO2 Emission Permits

The CO2 emissions of the ps

s

have to be covered

by permits of {ep

p

, p ∈ [1,P]} types. Permits may

be traded, may be granted by the government, may

be consumed, are limited by constraints depend-

ing on the ep

p

. The permit trade is managed for

each ps

s

separately. ∀p ∈ [1, P],s ∈ [1,S] the de-

fined sales and purchases are respectively {sp

p,s

i

: i ∈

[1,Sp

p,s

]}, {zp

p,s

i

: i ∈ [1,Zp

p,s

]}. The permits are

consumed to coveremissions which are relative to en-

ergy production. Consumption volume is v(pu

s

i

,h) ·

α(co2, pu

s

i

,h), where α(co2, pu

s

i

,h), is the emission

ratio.

2.4 Financial Benefits

Financial benefits of type be

b

,b ∈ [1,B] can be pro-

duced, purchased, sold or consumed. They are pro-

duced relatively to energy production, be

b

produc-

tion volume is v(pu

s

i

,h) · α(be

b

, pu

s

i

,h) . The ra-

tios of production are dependent on the efficiency

of, and resources used by pu

s

i

. Examples of fi-

nancial benefit types are type for energy produced

from renewable resources, type for high efficiency

coal powered production, type for natural gas pow-

ered production, etc. Sales and purchases respec-

tively, are denoted by {sb

b

i

: i ∈ [1,Sb

b

],b ∈ [1,B]},

{zb

b

i

: i ∈ [1,Zb

b

],b ∈ [1, B]}. The be

b

is consumed,

relatively to the volume of sold energy, to gain access

to certain energy markets, be

b

consumption volume is

v(se

i

,h) · α(be

b

,se

i

,h).

2.5 Control Variables

The solution to the optimization problem is defined

by values assigned to the control variables. The com-

plete set CV of control variables (see APPENDIX A)

is (A.1)-(A.7)where (A.1) are energyproduction vari-

ables, (A.2)-(A.3) are energy trade variables, (A.4)-

(A.5) are financial benefits trade variables, (A.6)-

(A.7) are CO2 emission permit trade variables.

2.6 Constraints

The formulas representing linear constraints are: vari-

able unary (variable domains) (A.8), production gra-

dient (A.9), a technological constraint of each pu

s

i

,

energy balance (A.10), financial benefit monthly bal-

ance (A.12), financial benefits yearly balance (A.11),

CO2 permits nonnegativity (A.13), CO2 permits

yearly balance (A.14). (A.12)-(A.14) are called long

period constraints. The attribute name ist explicitly

denotes the initial state, whenever indexation refers to

element 0 e.g. v(pu

s

i

,0) it signifies an implicit initial

state.

The formulas representing nonlinear constraints

are: minimal duration for which a pu

s

i

has to work

after startup (A.15), technological constraint for the

level of production (A.16), minimal number of pu

s

i

turned on in ps

s

(A.17), startup schedule of a pu

s

i

(A.18), relation between the production levels of pu

s

i

and energy provided to the ec by ps

s

(A.19). Attribute

α(startup, pu

s

i

,y) is an ordered set of values, # is a set

cardinal number.

2.7 Elements of the Objective Function

The objective function ω(CV) represents the total ec

profit. Each control variable has a corresponding

profit ratio represented by the profit attribute. For

production and purchases the profit ratio is negative

and for sales the profit ratio is positive. The profit of

control variables is linear and represented by (A.20).

(A.21) and (A.22) are nonlinear elements of the cost

function. The first represents the startup cost of pu

s

i

i.e. the cost of turning on a disabled production unit.

The latter corresponds to costs related to components

of the f pv

s,h

(Section 2.2).

3 TESTED APPROACHES

The approaches have been tested on problem in-

stances denoted by inst(ec,H) where ec is the def-

inition of objects and types, H is the time hori-

zon. In particular inst(ec

r

,H

r

) denotes the industrial

AHybridSolverforMaximizingtheProfitofanEnergyCompany

279

real life problem instance. inst(ec

r

,H

r

) consists of

289’200 control variables, 411’838 linear non-unary

constraints and 490’560 nonlinear constraints for the

H

r

= 8

′

760. Under the confidentiality agreement we

are not allowed to disclose the structure of ec

r

. For the

time cr(st) used to perform the optimization, the con-

dition cr(st) > 10min is called the timeout. ¬timeout

is a requirement for the solver.

We have used the following criteria to compare

models: cr(nlin) are nonlinearities included in the

model, cr(gopt) is guarantee of optimality provided,

cr(long) are long period constraints included in the

model, cr(tef f ) = cr(st)/H time efficiency. The ap-

proaches have been tested on personal computers with

2 x 2.2Ghz processors, 3GB of RAM and address

space.

3.1 Constraint (Logic) Programming

Constraint programming (CP) (Apt, 2009; Marriott

and Stuckey, 1998) is a programming paradigm with

the central notion of a constraint. A constraint states

relations between variable domains (allowed combi-

nations of domain values). CP is a form of declara-

tive programming where the program in the form of

constraint statements is a description of the problem,

rather than a path to the solution (unlike in the case

of procedural programming). CP makes a distinction

between 3 components required to obtain a solution:

the declarative constraint statement, constraint prop-

agation and search. Historically CP has grown out of,

and has been embedded in logic programming and of-

ten uses the LP based backtracking search, it is how-

ever possible to embed constraint programming in a

procedural language.

We have tested models written under two CP

systems (Schulte, 2010; Szymanek and Kuchci´nski,

2010) and a CLP system (Cisco Systems, 2010) with

the result of obtaining optimal solutions for problem

instances with H ∈ [1,⌊H

r

/2000⌋]. The cr(tef f) ∈

[5s,25s] depending on the CP system, constraint prop-

agation methods and search methods. However for

problem instances with H ≥ ⌊H

r

/100⌋ we have been

unable to produce a solution without a timeout.

The advantages of the CP approach are that the

complete problem model can be taken into account

cr(long) = cr(nlin) = true, solution with the guar-

antee of optimality can be obtained cr(gopt) = true.

The major disadvantage is that the models are imprac-

tical for problem instances near the real life problem

size

3.2 Dynamic Programming

Dynamic programming (DP) (Bellman, 1953; Cor-

men et al., 2001) is a mathematical and computer al-

gorithmic scheme for solving optimization problems.

The method builds the final solution by expanding ini-

tial conditions step by step into more complex cases

with cr(tef f) determined by the number of states and

the complexity of the step.

By means of DP it is possible to obtain a com-

plete solution with cr(gopt) = true in polynomial

time complexity by (i) calculating an initial solution

for h = 1 and pu

1

1

and (ii) expanding the solution upon

all of the pu and year. Unfortunately, the complexity

of our problem generates a state-space too large for

any direct approach. However, a combined approach

of DP and local search can be derived if only we are

able to separate a simple subproblems for DP.

We have used a DP approach to determine, for a

fixed hour h, the costs of volumes vol

s

h

∈

∑

i

v(pu

s

i

,h)

for all ps

s

∈ {ps

s

} and generate the maximized to-

tal profit pr

h

for hour h. In the basic version we

have determined pr

h

by managing costs of produc-

tion of each pu

s

i

. These costs included the joint

costs of maintaining the pu

s

i

on vol

s

i,h

along with a

few other parameters (e.g. profit and cost associated

with be

b

production). In the first step of the algo-

rithm we have generated a lookup table of production

volumes vol

s

h

and minimal costs of achieving them

for each ps

s

. Assume that, for a fixed h and ps

s

,

v(pu

s

i

,h) ∈ [mn

i

,mx

i

]. We denote the cost of pu

s

i

in

h with volume x ∈ [mn

i

,mx

i

] as ep(i,x). Let m[x][z],

where x ∈ [1,U

s

] and z ∈ [

∑

U

s

i=1

mn

i

,

∑

U

s

i=1

mx

i

] be an

optimal cost of the production units (pu

s

1

− pu

s

x

) gen-

erating a total production equal to z. The values of

m[x][z] are equal to: (i) cp(1,z) for z ∈ [mn

1

,mx

1

], (ii)

min(m[x−1][z− i] + cp(x,i)) for i ∈ [mn

i

,mx

i

] or (iii)

∞ in all remaining cases. This relation gave us, for

each h and ps

s

, an optimal configuration of vol

s

i,h

nec-

essary to produce vol

s

h

. In the second step we merged

all obtained lookup tables (using DP) along with pur-

chases ze

i

modeled as an artificial pu with its own

lookup table. In the following step we generated (us-

ing DP once again) a lookup table for hour h and for

sales se

i

, containing the optimal methods of selling

of particular en volumes. In the last step of the al-

gorithm we have compared the two obtained lookup

tables and greedily chosen the best vol

h

as the pro-

duction volume of the ec.

The basic DP algorithm described above was fast

(cr(tef f ) = 5 − 8ms) comparing to CP but did not

include cr(long) leading to a very complicated local

search with poor final result for the year. Thus, we

have refined the solution by introducing partial op-

ICEIS2012-14thInternationalConferenceonEnterpriseInformationSystems

280

timization of goods to the DP algorithm. The best

configuration we have obtained by introducing only

one hard constraint - CO2 emission permit, leading to

cr(tef f) = 50ms.

The main advantages of this approach are: (i) fast

and always optimal solution for a fixed h and (ii) in-

clusion of cr(nlin) without any additional time ef-

forts. Unfortunately, the overall cr(long) manage-

ment is poor leading to very complex local search that

need to be applied as a superior algorithm.

3.3 Linear and Integer Programming

Linear programming (LP) (Dantzig, 1963) is a natu-

ral approach to solving linear problems but does not

apply directly to nonlinear problems. This drawback

can be partially overcome by including relaxations

of nonlinearities in the problem model, it however

comes at a cost of loosing accuracy and efficiency.

We have tested the LP model with a number of relax-

ations. First of all it has to be noted that the relaxation

of (A.19) is required for the model to be of any use be-

cause it relates the production to sales and is required

in the balance constraints (A.10). For any piece-

wise linear function f p, defined as (A.23) a convex

hull relaxation (Hooker, 2006) has been used (A.24).

In the initial solution of the LP model with (A.24),

(A.10) are not satisfied because they contain biases

caused by the relaxation. To eliminate the bias the

LP model is solved again with additional constraints

(A.25) that linearize the f pv

s,h

around the steady

states obtained from the first solution. To tighten the

relaxation, models of further nonlinearities can be in-

cluded: startup relaxation (A.26) of (A.16), startup

cost relaxation (A.27), (A.28) of (A.21) (where vstc

is the total cost of startups) , minimum pu

s

i

enabled

relaxation (A.29) of (A.17). Mixed integer/linear

programming (MILP) approach, can also be used to

tighten the relaxation by introducing integrality con-

straints integer(ar

i

), integer(on

s,i,h

).

We have tested the LP and MILP approaches, for

inst(ec

r

,H

r

) using the COIN-OR (IBM, 2010) CLP

and CBC solvers. The LP model with (A.24) and

(A.25) had produced the solution with cr(tef f) =

10ms, LP model with (A.24), (A.25) and (A.29) had

cr(tef f) = 40ms, the model with additional relax-

ations (A.27) and (A.28) produced a solution af-

ter cr(st) = 1853s with the timeout and cr(tef f) =

211ms. A model with integrality constraints did not

produce a solution within 1h.

To summarize, the LP relaxation approach has a

number of advantages: taking into account all the

long period constraints cr(long) = true, producing

an optimal solution for the defined model cr(gopt) =

true, a relatively short cr(tef f) = 10ms (LP model

with (A.24) even for inst(ec

r

,H

r

). The main dis-

advantage is that nonlinearities are accounted for in

a very limited scope. Therefore, an additional opti-

mization step has to be used to fully satisfy the non-

linearities.

3.4 Local Search

Local search (LS) (Aarts and Lenstra, 1997) is a

meta-heuristic for solving computationally hard op-

timization problems. For the case of ec optimiza-

tion the LS algorithm is organized as follows: it

assumes an initial solution (step 1), repairs the vi-

olated nonlinear constraints (step 2) by applying a

set of repair heuristics, looks for a better solution

(step 3) using a set of improvement heuristics (step

3a). All value assignmentsCV = vals(heur,CV) (step

2a,3a), are performed by choosing a neighborhood

pu

k

j

and applying new values to CV such that all lin-

ear constraints are satisfied and that only the vari-

ables {v(pu

k

j

,h) : h ∈ [1,H]} in neighborhood pu

k

j

are changed from all productionvariables {v(pu

s

i

,h)}.

LS performs backtracking (backtrack) in the cases

when constraints cannot be repaired to undo wrong

heuristic choices. A solution is returned in the form of

variable values values(solution) and the correspond-

ing profit. The details of particular heuristics shall

not be discussed because they are dependent on a par-

ticular class of problem instances and are subject to

customization.

1. CV = values(init), profit = −∞

2. for all heur ∈ repair heuristics:

(a) for all cstr ∈ violated(heur,CV) : CV =

values(heur(cstr),CV)

(b) if ¬#violated(heur,CV) = 0 then backtrack

3. for all heur ∈ improvement heuristics:

(a) CV = values(heur,CV)

(b) if #violated(all,CV) = 0∧ ω(CV) > profit

then values(solution) = CV, profit = ω(CV)

else backtrack

The advantages of local search is that it can be

applied to large and nonlinear problems. The disad-

vantage is that any LS algorithm is custom tailored

for a specific problem definition and class of problem

instances. It is typical that LS is highly dependent on

the quality of the initial solution CV = values(init)

(how many constraints, and of which classes, are vi-

olated, are those difficult for LS to handle satisfied

etc.)

AHybridSolverforMaximizingtheProfitofanEnergyCompany

281

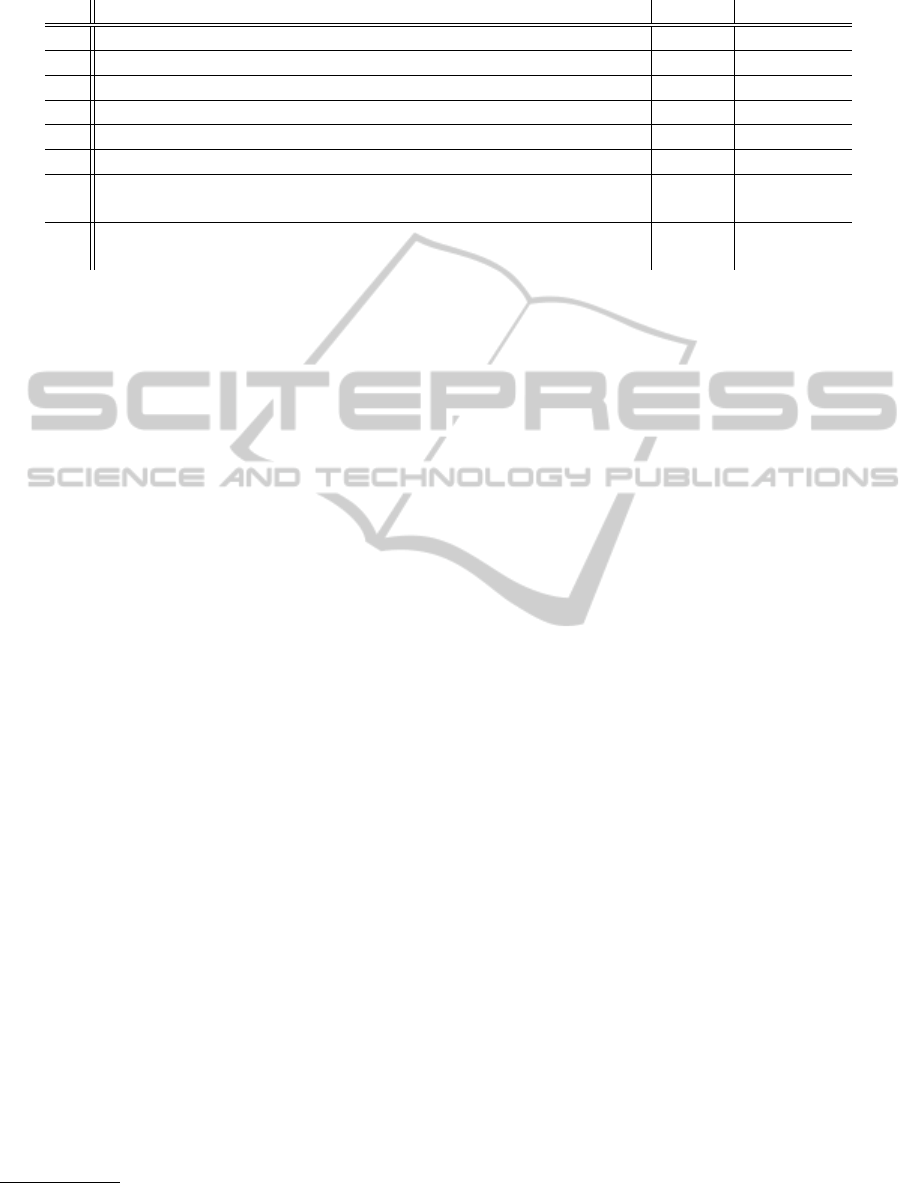

Table 1: Execution times of the hybrid solver (CP+LP+LS) for several problem instances derived from inst(ec

r

,H

r

).

Nr Problem instance (inst(ec,H)) CP+LP CP+LP+LS

1 Original problem instance for a year (inst(ec

r

,H

r

)) 46.8s 161.8s

2 3 quarters of the year (inst(ec

r1

,H

r

· 3/4)) 31.3s 111.1s

3 2 quarters of the year (inst(ec

r2

,H

r

· 2/4)) 19.8s 74.2s

4 1 quarters of the year (inst(ec

r3

,H

r

· 1/4)) 9.4s 41.3s

5 Higher costs of energy production (inst(ec

r4

,H

r

)) 12.7s 121.9s

6 Unconstrained sales and purchases (inst(ec

r5

,H

r

)) 183.9s 295.5s

7 Unconstrained sales and purchases, higher energy production cost 448.2s 614.2s

(inst(ec

r6

,H

r

))

8 Unconstrained sales and purchases, heavier constrained production 372.4s 490.7s

gradient (inst(ec

r7

,H

r

))

3.5 Hybrid Approach

Due to the fact that a single method approach is in-

sufficient to time-efficiently account for all the com-

ponents of the ec profit optimization problem a hy-

brid approach (solver) has been developed compris-

ing of CP+LP+LS. The hybrid solver takes advantage

of the interactions and key strengths of the methods

included.

The function of CP has been reduced to perform-

ing bound propagation (Dechter and van Beek, 1997)

on the constraints (A.8)-(A.14)(A.19) in order to de-

termine correction variables

1

for the equality con-

straints in the LP model and determine infeasible con-

straints at the outset without time consuming proof of

infeasibility by the LS.

The LP model with (A.24) and (A.25) has been

used as described in Section 3.3 to obtain an initial

solution for the LS. The LP model is preferred to

DP because it accounts for all long period constraints

(A.12)-(A.14), these constraints are ”difficult” to sat-

isfy by the LS (which leads to LS timeouts) if they are

not accounted for in the initial solution. Secondly the

LP model outperforms DP with respect to cr(tef f).

The final optimization stage is LS which uses the so-

lution provided by the the LP model as the initial vari-

able assignment. LS is meant to account for the non-

linearities, find a feasible solution (repair phase) and

optimize it (improvement phase).

The hybrid approach is supreme because it is

the only one that accounts for the complete prob-

lem model and produces an acceptable solution for

inst(ec

r

,H

r

) without a timeout. The hybrid solver

was tested for several problem instances, derived by

modification from the industrial real life problem in-

stance, and the results are presented in Table 1. The

results show that the solver execution time is linearly

1

correction variables are used to compensate rounding

errors performed by the LP solver

dependent on the size of the problem (time horizon

modifications in row 1 to 4) and is strongly depen-

dent on the problem structure i.e. the types of con-

straints (tightened or relaxed) and profit ratios for con-

trol variables. This vulnerability to modification of

problem structure is a feature of LP.

4 CONCLUSIONS AND RELATED

WORK

Hybridization is an approach to optimization prob-

lems that often yields shorter computation times than

single method approaches. The relative advantage of

hybrid solvers can range up to a few orders of mag-

nitude. This means that for applications with time-

outs imposed on optimization it may be the only ap-

plicable solution. Furthermore, real life problems of-

ten contain heterogeneous constraints and hybridiza-

tion allows to choose techniques best suited for par-

ticular classes of constraints and let them exchange

information. A survey of computational results per-

formed by John N.Hooker in (Hooker, 2006) lists

some applications of hybrid solvers and their advan-

tages over single method approaches to problem such

as: ”Scheduling with earliness and tardiness cost”

(Beck and Refalo, 2003) solved 5 times more prob-

lem instances, ”Polyprophylene batch scheduling”

(Timpe, 2002) solved previously insoluble problem

in 10min, ”Lesson timetabling” (Focacci et al., 1999)

2 to 50 times faster, ”Min-cost multiple machine

scheduling” (Jain and Grossmann, 2001) 20 to 2000

times faster, ”Product configuration” (Thorsteinsson

and Ottosson, 2002) 30 to 40 times faster.

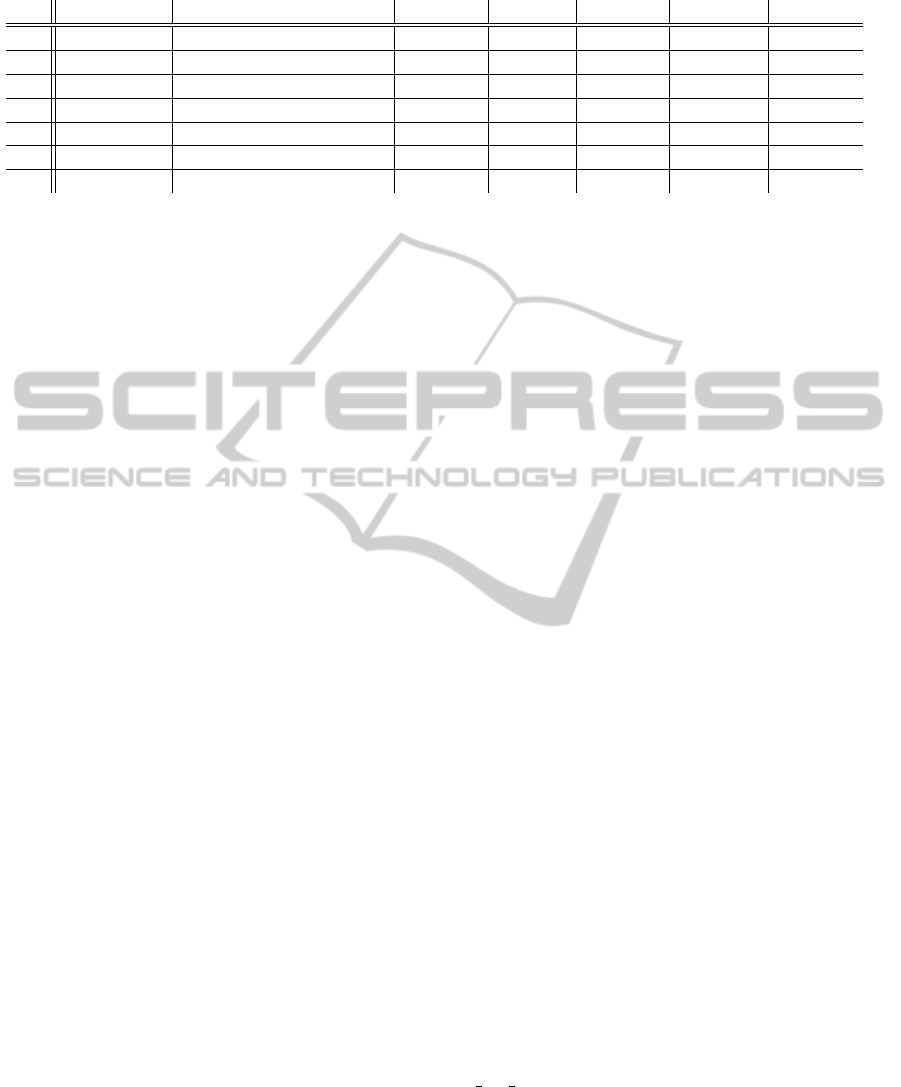

For the ec optimization problem, on the basis of

our experiments (Section 3 and Table 2), we believe

that a hybrid approach (Section 3.5 and Table 2 entry

7) is the only one that can achieve performance suffi-

cient to meet the requirements of an industrial appli-

ICEIS2012-14thInternationalConferenceonEnterpriseInformationSystems

282

Table 2: Comparison of experimental results for different approaches to inst(ec

r

,H

r

).

Nr Method Comment cr(gopt) cr(nlin) cr(long) ¬timeout cr(tef f)

1 C(L)P 3 approaches tested true true true false na

2 DP basic algorithm true true false true 8ms

3 DP with CO2 constraints true true false

∗

true 50ms

4 LP with (A.24)(A.25) true false

∗

true true 10ms

5 LP with (A.24)(A.25)(A.29) true false

∗

true true 40ms

6 DP + LS false true true false na

7 CP+LP+LS false true true true 58ms

∗ partially taken into account.

cation.

We have presented a generalized definition of the

ec optimization problem. We have also laid out the

overall structure and details of a hybrid solver de-

veloped for the generalized problem, indicating a

promising area of research and leaving room for cus-

tomization (especially in the LS area). We have also

discussed approaches which have been discarded at

an early stage of development because of their low

performance, indicating areas of development which

are unlikely to yield satisfactory results. To the best

knowledge of the authors no other solution to the ec

optimization problem has been reported.

The presented hybrid CP+LP+LS approach is

generalizable because many complex optimization

problems (other than ec optimization) can also be de-

composed into linear and nonlinear components and

then subjected to CP bound consistency, solved by LP

to produce an initial solution that is next extended to a

feasible solution with respect to nonlinearities by LS

and improved by LS, in the same manner as described

in this paper.

REFERENCES

Aarts, E. and Lenstra, J., editors (1997). Local Search in

Combinatorial Optimization. Discrete Mathematics

and Optimization. Wiley, Chichester, UK.

Apt, K. (2009). Principles of Constraint Programming.

Cambridge University Press, New York, NY, USA, 1st

edition.

Beck, J. C. and Refalo, P. (2003). A hybrid ap-

proach to scheduling with earliness and tardiness

costs. Annals of Operations Research, 118:49–71.

10.1023/A:1021849405707.

Bellman, R. (1953). An introduction to the theory of dy-

namin programming. The RAND Corporation, Report

R-245.

Cisco Systems (2010). ECLiPSe constraint logic program-

ming system. http://www.eclipse-clp.org/.

Cormen, T. H., Leiserson, C. E., Rivest, R. L., and Stein, C.

(2001). Introduction to algorithms (2nd edition). MIT

Press and McGraw-Hill.

Dantzig, G. B. (1963). Linear programming and extensions.

Princeton Univ. Press, Princeton, NJ.

Dechter, R. and van Beek, P. (1997). Local and global rela-

tional consistency. Theor. Comput. Sci., 173:283–308.

Focacci, F., Lodi, A., and Milano, M. (1999). Cost-based

domain filtering. In Proceedings of the 5th Interna-

tional Conference on Principles and Practice of Con-

straint Programming, CP ’99, pages 189–203, Lon-

don, UK. Springer-Verlag.

Hooker, J. N. (2006). Operations research methods in con-

straint programming, pages 525–568. Handbook of

Constraint Programming. Elsevier, Amsterdam.

IBM (2010). Coin-or computational infrastructure for oper-

ations research. http://www.coin-or.org/ .

Jain, V. and Grossmann, I. E. (2001). Algorithms for hybrid

milp/cp models for a class of optimization problems.

INFORMS J. on Computing, 13:258–276.

Marriott, K. and Stuckey, P. J. (1998). Introduction to Con-

straint Logic Programming. MIT Press, Cambridge,

MA, USA.

Schulte, C. (2010). Gecode constraint programming sys-

tem. http://www.gecode.org/.

Szymanek, R. and Kuchci´nski, K. (2010). Jacop constraint

programming system. http://jacop.osolpro.com/.

Thorsteinsson, E. S. and Ottosson, G. (2002). Linear re-

laxations and reduced-cost based propagation of con-

tinuous variable subscripts. Annals of Operations Re-

search, 115:15–29. 10.1023/A:1021136801775.

Timpe, C. (2002). Solving planning and scheduling prob-

lems with combined integer and constraint program-

ming. OR Spectrum, 24:431–448. 10.1007/s00291-

002-0107-1.

APPENDIX A

The appendix contains equations of the prob-

lem model and its relaxation. APPENDIX A

is available at http://sun.aei.polsl.pl/∼twojdyla/opt/

ec opt appA.pdf.

AHybridSolverforMaximizingtheProfitofanEnergyCompany

283