Prediction of Earnings per Share for Industry

Swati Jadhav, Hongmei He and Karl Jenkins

School of Aerospace, Transport and Manufacturing, Cranfield University, Cranfield, U.K.

Keywords: EPS Prediction, Data Mining, Regression, RBF Network, Multilayer Perceptron (MLP).

Abstract: Prediction of Earnings Per Share (EPS) is the fundamental problem in finance industry. Various Data Mining

technologies have been widely used in computational finance. This research work aims to predict the future

EPS with previous values through the use of data mining technologies, thus to provide decision makers a

reference or evidence for their economic strategies and business activity. We created three models LR, RBF

and MLP for the regression problem. Our experiments with these models were carried out on the real datasets

provided by a software company. The performance assessment was based on Correlation Coefficient and Root

Mean Squared Error. These algorithms were validated with the data of six different companies. Some

differences between the models have been observed. In most cases, Linear Regression and Multilayer

Perceptron are effectively capable of predicting the future EPS. But for the high nonlinear data, MLP gives

better performance.

1 INTRODUCTION

Even though financial market analysis requires

knowledge, intuition and experience, the automation

process has been growing steadily because of the

availability of large Finance data. There is a growing

evidence to research in the fields of data mining and

machine learning and their applications to

Computational finance industry.

In a mature finance industry, a company that takes

the dominant position in the industry earns greater

profits because of better ways of handling its

economic scale and market power (San Ong et al.,

2010).

Evaluation of stocks of a company to buy or sell

is an important decision to be made by the investors

of a company. Nowadays, when huge amounts of data

are made available with the advent of technology, this

decision does not become any easier without the help

of some model. Thus determining the best model

directly affects the investment decisions for a

company.

EPS is considered as one of the most important of

the profitability metrics of a company. It represents

the returns delivered by the company for each

outstanding share of common stock. It is a major

indicator for investors to purchase stocks. Price

Earnings (PE) ratio is obtained by dividing the stock

price by EPS. The EPS used here can be current or

future earnings. EPS over past quarters as well as

“forward” forecasted quarters is most frequently used

in the calculation of PE ratio of a company.

Comparison of a stock’s current PE with those of its

competitors or with its own average multiple over

three to ten years gives useful information about

hopeful future profits, investment in the company and

also if a possible bargain has happened. Investment

into a stock depends on the current PE ratio: Is it too

high or low compared with the PE ratio of the stock’s

peers, industry or aggregate market?

This paper proposes three regression models to

predict EPS: (1) Statistical Regression Model using

Linear Regression (LR) (2) Neural network (NN)

regression using Multilayer Perceptron (MLP) and

(3) Neural network regression using Radial Basis

Function (RBF). For construction of these models,

56-quarter EPS data are employed. The experimental

results indicate that LR and MLP models outperform

the RBF models, except for the high nonlinear data,

where MLP gives better performance.

If one has huge and complex dataset, data mining

can be carried out on it keeping in mind a particular

problem and goal of discovering insights and predict

future accurately. Formally, Data Mining or

Knowledge Discovery in Databases (KDD), is the

process of intelligent analysis of large amounts of

data, also called as big data to explore consistent

patterns and relationships among variables. This can

Jadhav, S., He, H. and Jenkins, K..

Prediction of Earnings per Share for Industry.

In Proceedings of the 7th International Joint Conference on Knowledge Discovery, Knowledge Engineering and Knowledge Management (IC3K 2015) - Volume 1: KDIR, pages 425-432

ISBN: 978-989-758-158-8

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

425

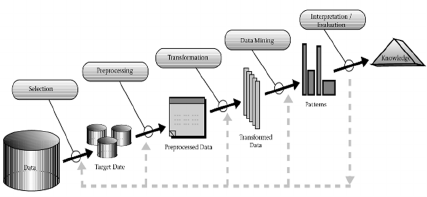

be seen in Figure 1. The patterns found are in the form

of models and are validated by subjecting them to

new datasets. This process is called as deployment of

the models. Data mining involves building models to

detect patterns which then are used to predict

situations. It is the amalgamation of different fields

like Statistics, Information systems, Applied Machine

learning, Data engineering, Database Systems,

Artificial intelligence and Genetic Algorithms.

Knowledge discovery process is being applied by

various industries for fraud detection, bankruptcy

prediction, marketing campaigns, forecasting high-

risk clients and improving production processes, to

name a few. Application of data mining in the area of

finance is becoming more amenable since large

financial datasets are becoming available.

Data mining takes inspiration from Machine

learning which involves building and applying the

models or algorithms to predict the future without any

real explanation of any reasoning of the real causes of

relationships. Machine learning takes from statistics

but stresses more on accuracy of prediction. Various

unsupervised or supervised machine learning

techniques can be applied in the process of data

mining.

Predictive data mining identifies very complex

and generic model(s) which are then used to predict

the response of new data sets. Prediction is a form of

data analysis used to extract models to predict future

data trends and get better understanding of the data.

Prediction learns a mapping or function, y = f (X),

where X is the input and y is the continuous output to

model the relationship between X and y.

Figure 1: Data Mining as a step in the process of Knowledge

Discovery (Fayyad et al., 1996).

The paper is organized as follows. Next section

reviews the literature on usage of EPS for stock price

forecasting. Then, the methodology of the research

along with the applied methods is introduced. Next

section describes the dataset and experimental set up

of the work. The experimental results of forecasting

performance across the LR and NNs are compared in

next section followed by conclusions of the work.

2 RELATED WORK

Prediction of Earnings per share forms the basis for

stock price forecasting. Forecasting is s function

approximation problem involving choosing a model

and fitting its parameters to the data. This problem is

complex because of stock price changes in time being

highly nonlinear. Many artificial intelligence, soft

computing and machine learning methods have been

used wherein neural networks and regression show

good results since they are robust against noise, can

model nonlinear relationships and give good

generalization performance.

Data mining and regression have long been

researched upon to solve various problems. There are

three types of Regression models such as Linear,

Polynomial and Logistic Regression.

Regression modelling has many applications

wherein the output is continuous such as in trend

analysis, business planning, marketing, financial

forecasting, time series prediction, biomedical and

drug response modelling, and environmental

modelling (Sajja and Akerkar, 2012).

Artificial neural networks (ANNs) are one of the

most common supervised data mining techniques

used by the industry for forecasting.

MLPs have been employed for prediction of stock

prices and indexes on various stock markets, see:

(Mostafa, 2010; Ince and Trafalis, 2008; Guresen et

al., 2011). Similarly RBF neural networks were the

topic of choice for same purpose in: (Shen et al.,

2011; Chen et al., 2009; Yan et al., 2005). Use of

RBFs along with various other data mining

techniques can be found in (Guo et al., 2015;

Sermpinis et al., 2013; Kara et al., 2011).

Other research regarding forecasting and

prediction in the area of finance focuses on stock

market, bankruptcy, fraud, credit scoring and

business failures. Bankruptcy prediction attempts to

predict bankruptcy and financial distress of public

firms. It is one of the vast areas of finance research.

Creditors and investors have always given

importance to the evaluation of credit worthiness of

firms.

A lot of them consider ANNs as the main

technique of forecasting (Geng et al., 2015; Wong

and Versace, 2012; Ravisankar et al., 2011; Pacelli et

al., 2011; Du Jardin and Séverin, 2011; Ravisankar

and Ravi, 2010; Hsieh and Hung, 2010; Esichaikul

and Srithongnopawong, 2010; Wang et al., 2011; De

Oliveira et al., 2011; Vaisla and Bhatt, 2010).The

learning and predicting potential of the adaptive

neuro-fuzzy inference system (ANFIS) model, a

variant of ANN is used for stock market returns

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

426

prediction in (Bagheri et al., 2014; Chen, 2013;

Boyacioglu and Avci, 2010).

Classic economic model of regression is used to

predict stock trends in (Olaniyi et al., 2011). To

obtain n-day ahead volatility forecasts, the implied

volatility may be parameterized within an ARCH

model (Blair et al., 2010). Similarly Regression along

with neural network was applied in (Saigal and

Mehrotra, 2012) and along with support vector

machines was investigated in (Kazem et al., 2013).

Other research work using Regression can be found

in (Serrano-Cinca and GutiéRrez-Nieto, 2013; Pan,

2012; Öğüt et al., 2012).

The observation is that models based on neural

networks are suitable for stock market related

forecasting. They are efficient at producing better

results for trading systems with higher forecasting

accuracy. The literature demonstrates that soft

computing techniques have natural connection with

classical statistics methods and have been used

alongside conventional models. However, difficulties

arise when defining the structure of the model (the

hidden layers, number of neurons etc.). While

determining the structure of the model trial and error

procedures are still employed.

A company’s stock price is mainly affected by

Earnings Per Share (EPS) since the stocks vary

according to EPS ratio. Researchers have investigated

several methods to construct models taking help of

EPS: (Patell, 1976) suggested that firms disclose

more frequently when experiencing favourable

earnings results and that earnings forecasts are,

usually associated with positive returns. Financial

distress prediction was the topic of study in (Chen and

Du, 2009) wherein EPS was used as one of the inputs

to neural networks.

A study involving financial ratios included EPS

among others and showed that application of

ensemble methods with diverse models have good

predictive capacity and have good applications in the

area of forecasting. PE ratio has been used in many

research works: DJIA stock selection assisted by

neural network (Quah, 2008). Few researchers have

taken into consideration the EPS ratio as part of

dataset. (Khirbat et al., 2013; Lai et al., 2009) used it

for stock price forecasting and (Pan et al., 2011) used

it for financial crisis prediction.

In (Han and Chen, 2007), a method of SVM was

proposed with financial statement analysis for

prediction of stocks using EPS as one of the finance

parameters. EPS was used as a financial variable for

financial crisis prediction in (Song et al., 2010). SVM

and ANN models including PE ratio as one of the

basic financial indicator give meaningful

performance results for the stock selection (Timor et

al., 2012). Many stock prediction, stock selection,

financial crisis prediction and fraud detection studies

have used EPS as part of the study: (Qiu, 2007; Jiang

et al., 2009; Quah and Ng, 2007; Li and Wong, 2014;

Arefin and Rahman, 2011; Rezaie et al., 2013).

Actual EPS forecasting was the topic of research

in few studies. In an interesting study of Markov

process model to forecast subsequent quarterly EPS

values, the authors applied time independent

transition probability matrices to predict EPS of IT

companies (Rajakumar and Shanthi 2014).

It is seen that EPS forecasting using machine

learning techniques is still a new area. Neural

networks seem obvious choice to model nonlinear

data, but need the decision about parameters,

architecture and speed.

When a real problem needs to be solved, the goal

is to find an approach as easy as possible with the

performance as good as possible. Therefore, we select

three models of LR, MLP and RBF for the EPS

problem, and compare the suitability for the real data.

3 ALGORITHMS USED FOR THE

PREDICTIVE PROBLEM

In order to find the best model for the predictive

problem, we select Linear Regression (LR),

Multilayer Perceptron (MLP) and Radial Basis

Function (RBF) for the predictive problem.

3.1 Linear Regression

Regression is used to predict values in Data Mining.

The process starts with a dataset where the target

values are known and other attributes might be the

predictors in predicting value of the target. While

building the regression model, the algorithm which is

a relationship between predictors and target estimates

the target as a function of the predictors for each

observation in the dataset. This model then can be

applied to a dataset not seen by the model previously

to determine target values.

Least squares regression, a standard approach to

regression, finds a best-fitting line that minimizes the

mean squared difference between the observed values

and the fitted values.

The simplest regression model is the linear

regression model, which represents the linear

relations between independent (also called as x-

variables or predictors) and dependent variables (y-

Prediction of Earnings per Share for Industry

427

variables, response variables or goal variables), as

shown in formula (1).

f(X)= a0+a1x1+a2x2+a3x3+… (1)

3.2 MLP Architecture-Feedforward

Neural Networks

Artificial Neural Networks (ANN) are universal

approximators, and they are very popular with

regression applications where they obtain a close

relation to a continuous objective function. As they

are data-driven, if a good training dataset is available,

they provide good forecasting results.

It is comprised of a set of neural perceptrons. A

Perceptron is a simplest neural network. It is a linear

classifier, using sigmoid function as the activation

function. A perceptron can be described with the

following function:

=

(2)

)(

1

1

)(

θα

−−

+

==

u

e

ufv

(3)

where N is the total number of nodes in input layer,

W

i

is the weight vector connecting the neuron of the

output layer for the pattern p.

Multilayer Perceptron (MLP) extends the concept

of perceptron by adding one or more hidden layers of

neurons. Neural network is usually used to extract

patterns from complex data, as adaptive learning

makes it easy to model complex data, and they do not

assume about underlying probability density

functions or any information regarding the modelling

sample under consideration. Therefore, we

investigate the multiple layer perceptron regression

for the real predictive problem, and use classic

backpropagation algorithm to train the neural

network.

3.3 RBF Network Architecture

RBF network is one of the most popular neural

networks and is a main competitor for MLP networks.

RBFs are faster to train than MLPs of a similar size,

as RBF is a feed forward neural network with a single

hidden layer. But the number of hidden layer neurons

required for RBF neural networks grows

exponentially with the number of inputs. A unique

feature of this network is the process that is performed

in the hidden layer. Input layer sends the input value

to each of the nodes in the hidden layer. Each node in

the hidden layer (neurons) are characterized by a

transfer function: G. Usually the transfer function

uses radial basis functions (e.g. Gaussian functions in

formula (4)) as activation functions. The output of the

network is a linear combination of radial basis

functions of the inputs and neuron parameters (See

formula (5)).

=−

(4)

GW = b (5)

where W is the weight vector, linking the hidden layer

to the output layer and b is the output.

To avoid overtraining of the network, 10-fold

cross validation method is used. This method splits

the data into 10 parts of equal size. In each of the 10

iterations, one part is used as testing set and

remaining as training sets. At the end of 10 runs,

overall performance is the average of all runs’ results.

4 EXPERIMENTS

4.1 Data for the Experiments

The nature of the data used in this work is Estimates

made by the market on Earnings per Share for a

company. The data is captured multiple times in a

quarter for 14 years. First, the records for EPS values

were extracted separately for each company, and data

for six companies were used in the experiments.

The problem domain is divided into two

problems: Problem 1 and Problem 2. The EPS

numeric data for six companies is chosen, which is

organized in matrix as follows:

Problem 1: The EPS data is columnised such that

previous four values are used to predict the fifth

value.

In Table 1, x1-x4 are inputs of the model and y is the

fifth value as the target.

Table 1: Format of the Data sample for Problem 1.

x

1

x

2

x

3

x

4

y

1 2 3 4 5

2 3 4 5 6

3 4 5 6 7

4 5 6 7 8

5 6 7 8 9

Table 2: Format of the Data sample for Problem 2.

x

1

x

2

x

3

x

4

y

1 2 3 4 6

2 3 4 5 7

3 4 5 6 8

4 5 6 7 9

5 6 7 8 10

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

428

Problem 2: The EPS data is columnised such that

previous four values are used to predict the sixth

value.

In Table 2, x1-x4 are the inputs of the model and y is

the sixth value as the target.

4.2 Experiment Set up

(1) The purpose of the work is to find the best model

for the EPS prediction problem. Therefore, we

perform the experiments for the data from six

companies, and compare the performance of the

three models LR, MLP and RBF.

(2) The parameter selection process for each

algorithm was carried out with the help of industry

experts.

(3) All the experiments are run for the datasets using

10-fold cross validation.

(4) Experiment platform: We use WEKA as the

experimental platform.

4.3 Performance Evaluation

In this study, Correlation Coefficient (r) and the root

mean square error (RMSE) are used for the evaluation

of performance of the models.

A correlation coefficient equal to zero indicates

that there is no relationship between the variables; i.e.

if one variable changes, the other may or may not

change. A correlation of +1.00 or -1.00 indicates that

the variables involved are perfectly associated

positively or negatively. A higher correlation

coefficient indicates better fitting to the data. It can be

calculated with formula (6).

=

∑

−

−

∑

−

−

(6)

RMSE gives the measure of the difference

between values predicted by the model and the real

values. The lower RMSE indicates the higher

accuracy. It can be calculated with formula (7).

=

∑

−

(7)

Where

n is the sample size

is the real observed value

is the predicted value

is the average of real observed value

is the average of predicted value from

the model

5 RESULTS AND EVALUATION

The performance of all the models built by the three

algorithms for Correlation Coefficient r and RMSE in

WEKA is shown in figures below.

5.1 Problem 1

In Problem 1, we predict fifth value using previous

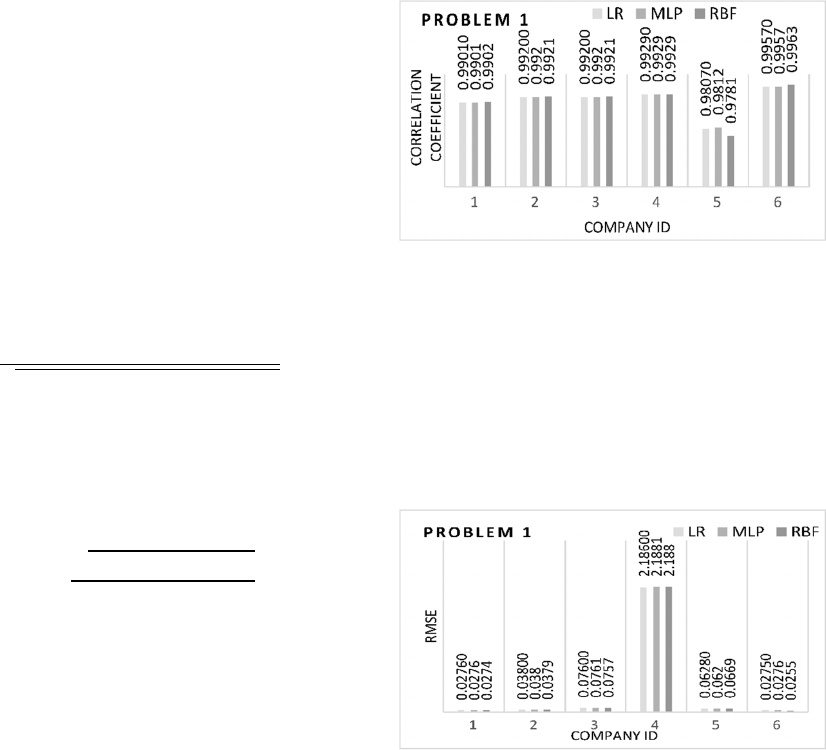

four values. Figure 2 illustrates the Correlation

coefficient obtained with the three models for

Problem 1. From Figure 2 we can see that the three

models obtained similar performance for all the

companies except for Company 5, for which MLP is

slightly better than LR and RBF. Also the

Correlation

Coefficient for Company 5 is lowest among all the six

companies. It means the data for Company 5 is

weakly linear. So MLP obtained better performance

for Problem 1.

Figure 2: Correlation Coefficient obtained with the three

models for Problem 1.

Figure 3 illustrates the RMSE obtained with the three

models for Problem 1. Obviously it can be seen that

RMSE for Company 4 is highest among all the

companies. Although for all companies the three

models obtained similar RMSE, for Company 5, MLP

obtained the lowest RMSE compared with other two

models for Problem 1. This is consistent with the

Correlation

Coefficient for Company 5 in Figure 2.

Figure 3: RMSE obtained with the three models for

Problem 1.

Prediction of Earnings per Share for Industry

429

5.2 Problem 2

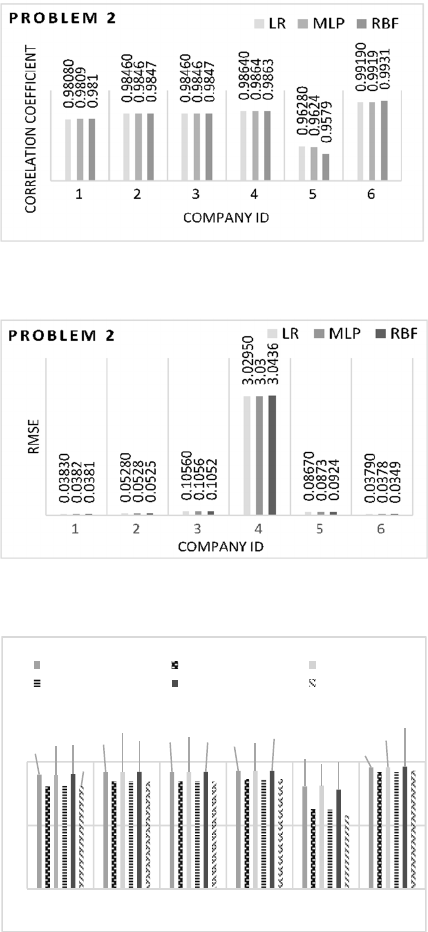

Figure 4 illustrates the Coefficient of Correlation of

six companies for Problem 2. From Figure 4, the

performance in Correlation Coefficient for all the six

companies for Problem 2 is similar to the

performance for Problem 1. But all values for

Problem 2 are lower than that of Problem 1. Company

5 still got the lowest Correlation Coefficient among

all the companies. LR and MLP obtained better

performance than RBF.

Figure 4: Correlation Coefficient obtained with the three

models for Problem 2.

Figure 5: RMSE obtained with the three models for

Problem 2.

Figure 6: Correlation Coefficient for all the three models for

six companies in both the problems.

From Figure 5, we can see that the RMSE of six

companies for Problem 2 are similar to that for

Problem 1. But the RMSE values of all companies for

Problem 2 are larger than for Problem 1. For each

company, the order of three models’ performance in

RMSE in Figure 5 is the same as the order of three

models’ performance in Correlation Coefficient in

Figure 4 for Problem 2. The Coefficient of

Correlation is consistent to the RMSE assessment.

In summary, Figure 6 illustrates all the

Correlation Coefficients of six companies for

Problems 1 and 2. It can be seen that the performance

of the three models for Problem 1 is better than that

for Problem 2. For company 5, which has high non-

linearity, the MLP obtained the best performance.

6 CONCLUSIONS

In this paper, we employ three models (LR, MLP and

RBF) to predict the change in the EPS of market firms

with historical data. The experiments were carried out

by running the three models on the data of six

companies. We use the Correlation Coefficient and

RMSE to assess the performance of the three models

on the data of the six companies.

The experimental results show that MLP obtained

best performance for high non-linear data. The

performance in Correlation Coefficient is consistent

to the performance in RMSE for the three models.

The performance of the three models for Problem 1 is

better than their performance for Problem 2. It means

that we need to use different models for different data.

REFERENCES

Arefin, J. & Rahman, R.M. 2011, "Testing different forms

of efficiency for Dhaka Stock Exchange", International

Journal of Financial Services Management, vol. 5, no.

1, pp. 1-20.

Bagheri, A., Peyhani, H.M. & Akbari, M. 2014, "Financial

forecasting using ANFIS networks with quantum-

behaved particle swarm optimization", Expert Systems

with Applications, vol. 41, no. 14, pp. 6235-6250.

Blair, B.J., Poon, S. & Taylor, S.J. 2010, "Forecasting S&P

100 volatility: the incremental information content of

implied volatilities and high-frequency index returns"

in Handbook of Quantitative Finance and Risk

Management Springer, , pp. 1333-1344.

Boyacioglu, M.A. & Avci, D. 2010, "An adaptive network-

based fuzzy inference system (ANFIS) for the

prediction of stock market return: the case of the

Istanbul stock exchange", Expert Systems with

Applications, vol. 37, no. 12, pp. 7908-7912.

Chen, K., Lin, H. & Huang, T. 2009, "The prediction of

0.9901

0.9920

0.9920

0.9929

0.9807

0.9957

0.9808

0.9846

0.9846

0.9864

0.9628

0.9919

0.9901

0.992

0.992

0.9929

0.9812

0.9957

0.9809

0.9846

0.9846

0.9864

0.9624

0.9919

0.9902

0.9921

0.9921

0.9929

0.9781

0.9963

0.981

0.9847

0.9847

0.9863

0.9579

0.9931

123456

CORRELATION COEFFICIENT

COMPANY ID

PROBLEM 1 VS PROBLEM 2

LR for Prob.1 LR for Prob.2 MLP for Prob.1

MLP for Prob.2 RBF for Prob.1 RBF for Prob.2

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

430

Taiwan 10-year government bond yield", WSEAS

Transactions on Systems, vol. 8, no. 9, pp. 1051-1060.

Chen, M. 2013, "A hybrid ANFIS model for business

failure prediction utilizing particle swarm optimization

and subtractive clustering", Information Sciences, vol.

220, pp. 180-195.

Chen, W. & Du, Y. 2009, "Using neural networks and data

mining techniques for the financial distress prediction

model", Expert Systems with Applications, vol. 36, no.

2, pp. 4075-4086.

De Oliveira, F.A., Zárate, L.E., de Azevedo Reis, M. &

Nobre, C.N. 2011, "The use of artificial neural

networks in the analysis and prediction of stock prices",

Systems, Man, and Cybernetics (SMC), 2011 IEEE

International Conference onIEEE, , pp. 2151.

Du Jardin, P. & Séverin, E. 2011, "Predicting corporate

bankruptcy using a self-organizing map: An empirical

study to improve the forecasting horizon of a financial

failure model", Decision Support Systems, vol. 51, no.

3, pp. 701-711.

Esichaikul, V. & Srithongnopawong, P. 2010, "Using

relative movement to support ANN-based stock

forecasting in Thai stock market", International

Journal of Electronic Finance, vol. 4, no. 1, pp. 84-98.

Fayyad, U., Piatetsky-Shapiro, G. & Smyth, P. 1996, "From

data mining to knowledge discovery in databases", AI

magazine, vol. 17, no. 3, pp. 37.

Geng, R., Bose, I. & Chen, X. 2015, "Prediction of financial

distress: An empirical study of listed Chinese

companies using data mining", European Journal of

Operational Research, vol. 241, no. 1, pp. 236-247.

Guo, Z., Wang, H., Yang, J. & Miller, D.J. 2015, "A Stock

Market Forecasting Model Combining Two-

Directional Two-Dimensional Principal Component

Analysis and Radial Basis Function Neural Network", .

Guresen, E., Kayakutlu, G. & Daim, T.U. 2011, "Using

artificial neural network models in stock market index

prediction", Expert Systems with Applications, vol. 38,

no. 8, pp. 10389-10397.

Han, S. & Chen, R. 2007, "Using svm with financial

statement analysis for prediction of stocks",

Communications of the IIMA, vol. 7, no. 4, pp. 63.

Hsieh, N. & Hung, L. 2010, "A data driven ensemble

classifier for credit scoring analysis", Expert Systems

with Applications, vol. 37, no. 1, pp. 534-545.

Ince, H. & Trafalis, T.B. 2008, "Short term forecasting with

support vector machines and application to stock price

prediction", International Journal of General Systems,

vol. 37, no. 6, pp. 677-687.

Jiang, Y., Wang, H. & Xie, Q. 2009, "Classification model

of companies' financial performance based on

integrated support vector machine", Management

Science and Engineering, 2009. ICMSE 2009.

International Conference on IEEE, , pp. 1322.

Kara, Y., Boyacioglu, M.A. & Baykan, ÖK. 2011,

"Predicting direction of stock price index movement

using artificial neural networks and support vector

machines: The sample of the Istanbul Stock Exchange",

Expert Systems with Applications, vol. 38, no. 5, pp.

5311-5319.

Kazem, A., Sharifi, E., Hussain, F.K., Saberi, M. &

Hussain, O.K. 2013, "Support vector regression with

chaos-based firefly algorithm for stock market price

forecasting", Applied Soft Computing, vol. 13, no. 2, pp.

947-958.

Khirbat, G., Gupta, R. & Singh, S. 2013, "Optimal Neural

Network Architecture for Stock Market Forecasting",

Communication Systems and Network Technologies

(CSNT), 2013 International Conference onIEEE, , pp.

557.

Lai, R.K., Fan, C., Huang, W. & Chang, P. 2009, "Evolving

and clustering fuzzy decision tree for financial time

series data forecasting", Expert Systems with

Applications, vol. 36, no. 2, pp. 3761-3773.

Li, H. & Wong, M. 2014, "Knowledge discovering in

corporate securities fraud by using grammar based

genetic programming", Journal of Computer and

Communications, vol. 2, no. 04, pp. 148.

Mostafa, M.M. 2010, "Forecasting stock exchange

movements using neural networks: Empirical evidence

from Kuwait", Expert Systems with Applications, vol.

37, no. 9, pp. 6302-6309.

Öğüt, H., Doğanay, M.M., Ceylan, N.B. & Aktaş, R. 2012,

"Prediction of bank financial strength ratings: The case

of Turkey", Economic Modelling, vol. 29, no. 3, pp.

632-640.

Olaniyi, S.A.S., Adewole, K.S. & Jimoh, R. 2011, "Stock

trend prediction using regression analysis–a data

mining approach", ARPN Journal of Systems and

Software, vol. 1, no. 4, pp. 154-157.

Pacelli, V., Bevilacqua, V. & Azzollini, M. 2011, "An

artificial neural network model to forecast exchange

rates", Journal of Intelligent Learning Systems and

Applications, vol. 3, no. 02, pp. 57.

Pan, N.H., Lee, M.L. & Chang, C.W. 2011, "Construction

Financial Crisis Warning Model Using Data Mining",

Advanced Materials Research Trans Tech Publ, , pp.

684.

Pan, W. 2012, "A new fruit fly optimization algorithm:

taking the financial distress model as an example",

Knowledge-Based Systems, vol. 26, pp. 69-74.

Patell, J.M. 1976, "Corporate forecasts of earnings per

share and stock price behavior: Empirical test", Journal

of accounting research, , pp. 246-276.

Qiu, X.Y. 2007, "On building predictive models with

company annual reports", .

Quah, J.T. & Ng, W. 2007, "Utilizing computational

intelligence for DJIA stock selection", Neural

Networks, 2007. IJCNN 2007. International Joint

Conference onIEEE, , pp. 956.

Quah, T. 2008, "DJIA stock selection assisted by neural

network", Expert Systems with Applications, vol. 35,

no. 1, pp. 50-58.

Rajakumar, M.P. & Shanthi, V. 2014, "Forecasting

earnings per share for companies in it sector using

Markov process model", Journal of Theoretical and

Applied Information Technology, vol. 59, no. 2, pp.

332-341.

Ravisankar, P. & Ravi, V. 2010, "Financial distress

prediction in banks using Group Method of Data

Prediction of Earnings per Share for Industry

431

Handling neural network, counter propagation neural

network and fuzzy ARTMAP", Knowledge-Based

Systems, vol. 23, no. 8, pp. 823-831.

Ravisankar, P., Ravi, V., Rao, G.R. & Bose, I. 2011,

"Detection of financial statement fraud and feature

selection using data mining techniques", Decision

Support Systems, vol. 50, no. 2, pp. 491-500.

Rezaie, K., Dalfard, V.M., Hatami-Shirkouhi, L. & Nazari-

Shirkouhi, S. 2013, "Efficiency appraisal and ranking

of decision-making units using data envelopment

analysis in fuzzy environment: a case study of Tehran

stock exchange", Neural Computing and Applications,

vol. 23, no. 1, pp. 1-17.

Saigal, S. & Mehrotra, D. 2012, "Performance comparison

of time series data using predictive data mining

techniques", Advances in Information Mining, vol. 4,

no. 1, pp. 57-66.

Sajja, P.S. & Akerkar, R. 2012, Intelligent technologies for

Web applications, CRC Press.

San Ong, T., Yichen, Y.N. & Teh, B.H. 2010, "Can High

Price Earnings Ratio Act As An Indicator Of The

Coming Bear Market In The Malaysia?", International

Journal Of Business And Social Science, vol. 1, no. 1.

Sermpinis, G., Theofilatos, K., Karathanasopoulos, A.,

Georgopoulos, E.F. & Dunis, C. 2013, "Forecasting

foreign exchange rates with adaptive neural networks

using radial-basis functions and particle swarm

optimization", European Journal of Operational

Research, vol. 225, no. 3, pp. 528-540.

Serrano-Cinca, C. & GutiéRrez-Nieto, B. 2013, "Partial

least square discriminant analysis for bankruptcy

prediction", Decision Support Systems, vol. 54, no. 3,

pp. 1245-1255.

Shen, W., Guo, X., Wu, C. & Wu, D. 2011, "Forecasting

stock indices using radial basis function neural

networks optimized by artificial fish swarm algorithm",

Knowledge-Based Systems, vol. 24, no. 3, pp. 378-385.

Song, X., Ding, Y., Huang, J. & Ge, Y. 2010, "Feature

selection for support vector machine in financial crisis

prediction: a case study in China", Expert Systems, vol.

27, no. 4, pp. 299-310.

Timor, M., Dincer, H. & Emir, S. 2012, "Performance

comparison of artificial neural network (ANN) and

support vector machines (SVM) models for the stock

selection problem: An application on the Istanbul Stock

Exchange (ISE)-30 index in Turkey", .

Vaisla, K.S. & Bhatt, A.K. 2010, "An analysis of the

performance of artificial neural network technique for

stock market forecasting", International Journal on

Computer Science and Engineering, vol. 2, no. 6, pp.

2104-2109.

Wang, J., Wang, J., Zhang, Z. & Guo, S. 2011, "Forecasting

stock indices with back propagation neural network",

Expert Systems with Applications, vol. 38, no. 11, pp.

14346-14355.

Wong, C. & Versace, M. 2012, "CARTMAP: a neural

network method for automated feature selection in

financial time series forecasting", Neural Computing

and Applications, vol. 21, no. 5, pp. 969-977.

Yan, X., Wang, Z., Yu, S. & Li, Y. 2005, "Time series

forecasting with RBF neural network", Machine

Learning and Cybernetics, 2005. Proceedings of 2005

International Conference onIEEE, , pp. 4680.

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

432