Integration of the Finnish National Tax Administration Systems with

EU Recapitulative Statement Data

Raita Melasniemi

1

and Rauno Pirinen

2

1

Finnish Tax Administration, Haapaniemenkatu, Helsinki, Finland

2

LAUREA University of Applied Sciences, Vanha maantie, Espoo, Finland

Keywords: Information System Integration, Development Project, European Union Recapitulative Statement, Distributed

Systems, Design Science Research, Recapitulative Statement Data.

Abstract: This study examined the European Union recapitulative statement data integration with the Finnish national

tax domain. The main challenges identified in realizing international integration were communication,

cooperation and distribution of information. In particular, the development of integration faced ontological

challenges in terms of specifications and final definition. The results highlight the process model and

mechanism for design digital system integration in distributed environments across national borders. The

study also offers administrative implications.

1 INTRODUCTION

This study focuses on the integration of the European

Union (EU) recapitulative statement data with the

Finnish national tax applications and digital

information system.

Recapitulative statement data comprise value-

added tax (VAT) for businesses registered with the

EU member states that provide intra-EU supplies to

actors who are obligated to complete recapitulative

statements. The statements list the aggregate value of

goods and services supplied to VAT-registered

customer elsewhere in the EU.

Economic operators submit recapitulative

statement data to their member states authority, which

is in charge of the VAT control and management

system. Member states collect VAT information and

store it in the value-added tax information exchange

system (VIES) database [see: Appendix (DG

TAXUD IT AO-03, 2012)].

The rationale underpinning this study is to learn

the integration of such data and its challenges as well

as contribute to the effectiveness of similar system

integration and development.

Overall, the reasoning culminated from a new

framework for administrative cooperation in the EU,

which is related to proposals made by the European

Commission in the past few years, and the

implementation of the framework by the Council for

administrative cooperation [note: Appendix (COM

722 final, 2012)].

Setting of new legislative instruments addresses

the manner in which new tools and instruments are

developed by the Commission and member states

[see: June Communication in the Appendix (COM

351 final, 2012)], which highlights effective and

comprehensive use by member states yet to be

attained. The member states must ensure full and

effective implementation and application of these

instruments, particularly by engaging in an enhanced

exchange of information.

In the Finnish tax environment, the amount of data

collected from the taxpayers has increased in the past

years. These enterprises are part of a group who have

to provide a recapitulative statement and adhere to

VAT control procedures. This setting is based on the

Council Directive 2008/117/EC of 16 December

2008, amended from the Directive 2006/112/EC on

the VAT common system, aimed at combating tax

evasion related to intra-community transactions and

obligations to declare services along with goods

transposition in the member states beginning in 2010.

In addition, the time limit to declare intra

community supplies in the recapitulative statement

has been reduced from the calendar quarter to each

calendar month within a period, not exceeding one

month [Appendix (EUR Lex, 2008)].

Administrations are obligated to exchange

increasing amounts of information and data and

require companies to electronically submit the

Melasniemi, R. and Pirinen, R..

Integration of the Finnish National Tax Administration Systems with EU Recapitulative Statement Data.

In Proceedings of the 7th International Joint Conference on Knowledge Discovery, Knowledge Engineering and Knowledge Management (IC3K 2015) - Volume 3: KMIS, pages 365-370

ISBN: 978-989-758-158-8

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

365

recapitulative statement. Therefore, there is growing

need for increased information system integration

within Finnish tax administration at the national level.

While tax administration requires declarations from

enterprises, the tax administrations’ obligation is to

exploit the data received.

Similar expansions can be noticed in line with this

study. The same type of development and realisation

work is being observed across Europe in tandem with

such changes.

These changes strain and increase the

administrative burden for taxpayers. Therefore, it is

significant to use the collected data for tax control and

audit purposes. Such data use is important to benefit

compliant taxpayers. In terms of tax administration,

this means developing tools to identify fraudsters and

those who do not qualify for the settled rules. These

tasks should be performed using appropriate

technologies that equally cover the entire field of

targeted taxpayers.

This study is based on activities and actions

performed to fulfil requirements to operate in line

with governmental viewpoints. The Finnish Tax

Administration Information Systems are currently

capable of collecting and exchanging data in line with

concerned regulations.

There are additional obligations which can be

improved using existing digital information systems.

These aims warrant the national integration of

information systems and increased global sharing of

digital information.

At the macro level, this study was completed in

compliance with the international research and

development agenda. The study expanded and

produced additional viewpoints from the students’

workplace to the European Union’s Common

Information Sharing Environment’s (EU CISE, 2020)

research project and dissemination, the EU CISE

2020 research consortium and Finland’s research

agenda targets.

The study examines information sharing

applications to foster cross-sectorial and cross-border

collaboration between public authorities and the

dissemination of the EU CISE 2020 initiative as well

as the steps along the recapitulative statement data

roadmap in the EU.

The macro-level work of interest entails the

possible experimental environments encompassing

innovative and collaborative services and processes

between European authorities and actors and takes as

reference, an extensive spectrum of factors in the field

of European integrated services, arising from the

European legal framework, collaborative studies and

related pilot projects.

Expected advances of this study were addressed

in an investigation of tax administrative and

controlling processes and implications, such as

technical, practical and administrative viewpoints.

The main finding of this study is a mechanism and

realisation steps in information systems integration.

The model contributes an improved an effective way

to perform similar projects in distributed digital

architecture and a multi-unit environment where

several international parties and actors are involved.

2 METHODOLOGY

This study attempted to answer the following

question: how can information systems related to the

EU recapitulative statements data be designed,

realised and evaluated?

More specific to this research, how can

recapitulative statements data from EU member states

be integrated with the Finnish national tax

administrative systems?

The unit of analysis uses a realisation project that

has been well documented and launched as a case

study.

The rationale underlying this unit of analysis and

study is to learn how EU recapitulative statement data

can be nationally integrated and the entailed

challenges as well as ways to improve the

effectiveness of similar system integration

developments.

The purpose of this study is in the realisation,

design and evaluation of the Finnish national tax

information systems.

The selection of the questions ‘how’ and ‘why’

led to the choice and use of descriptive methods, as

described in (Robson, 2002). Therefore, and due to

the nature of the present research question, a

qualitative analysis, case study research approach

(Yin, 2009) and design science theory and process

(Gregor, 2002) were used as the research design.

This study includes a literature review and

empirical research data, including documentation

material (n = 188) and interviews (n = 6).

Investigated data collected were triangulated

(Campbell and Fiske, 1959) and analysed, as advised

in Miles and Huberman (1994).

From the methodological viewpoint, the present

analysis is a case study with a design science research

extension in the domain in which the EU

recapitulative statements data can be integrated with

national applications (Hevner and Chatterjee, 2010).

In this case, the rationale is the research and

development project launched in response to the need

ISE 2015 - Special Session on Information Sharing Environments to Foster Cross-Sectorial and Cross-Border Collaboration between Public

Authorities

366

to develop a more efficient way to use collected and

stored data for tax control and audit purposes [cf.

methodology in Nunamaker and Briggs (2011)].

The important motives are to improve the

efficiency of tax control, neutral treatment of

customers and progressive use of collected data.

Achieved impacts were estimated to harmonise

customer service, improve tax control and tax

auditing processes and reduce manual work and

redirect tasks to the appropriate answerable taxation

unit [cf. methodological in March and Smith (1995)

and Markus et al., (2002)].

The integration development adopted by the tax

auditing unit was based on the EU Regulation

904/2010 and its demands to improve administrative

cooperation and tackle tax frauds.

In addition, the main methodological references

reviewed were as follows: the case research strategy

in Benbasat et al., (1987) and rigor in information

systems positivist case research by Dubé and Paré

(2003).

3 RESULTS

The first administrative implication of this study is

that the participants of development work should be

committed to being careful and has strong will to

meet the objectives of parties involved in the

international integration project.

The study also reveals that resources should be

afforded and participants have professional skills and

adequate knowledge and capabilities in the applied

domain.

Further, the roles of the participants have to be

clarified for all parties.

The importance and need of cooperation and

information sharing have to be understood and

realised in the project and research environment.

However, the main challenges in the integration

project are communication, cooperation, trust sharing

and information distribution.

Development mostly faces challenges in the

specifications and final definition of integration.

Here, these two ontology-related parts are strongly

linked.

The study further revealed that pre-operational

validation and balancing work pressure and workload

in the project as well as steering cognitive settings

reduces difficulties.

3.1 Project Issues

Issues experienced in the project could not have been

solved solely with an understanding of the entire tax

system or deeper testing. There were numerous issues

which could not have been tested in advance, also

known as preoperational validation, and some

situations were only discovered after the

implemented artefact was in use. This point reiterates

the importance of technical specifications and control

process methods.

In this case, the implications for development

works vary by purpose of data. Differences in

businesses lead to misunderstandings between

parties. Other parties tend to value technical matters

more than others. This causes weight differences

between parties and varying levels of understanding

regarding the entity of the project tasks.

One of the most challenging aspects seemed to be

cooperation between business units, that is, better

communication between business and information

system professionals.

A review of the extant literature reveals a

widespread agreement on the importance of user

involvement in system development and

maintenance; however, the level and quality of user

involvement often remains inadequate.

Even though the environment was a mature

collective, users found it difficult to express their

needs’. At a different organisational level, but in a

similar vein, misalignment between business and

information systems is an ongoing source of

frustration and inefficiency.

In this case, there are several participating parties

from different system organisations and businesses,

where communication becomes increasingly

important. The roles of the parties should be clarified

for all participants of the project. More specifically,

the role describes the responsibilities and authorities

of the actors.

In this case, it is recognised that, if the technical

solutions and business unit’s needs are in

contradiction, there should a person who understands

the technical and business side to guide both ends to

a final solution. The end-user view and user-centred

aspects should also be carefully considered.

Further evaluation shows that some parameters

have already been re-evaluated and corrected to meet

the requirements from the perspective of everyday

use. These changes can be seen as a normal cycle in

the development of the digital information system.

From the research data and the evaluation of the

project perspective, it is evident that all decisions

made regarding the implementations were not

optimal. Thus, it is essential to account for diverse

understandings when there are many operators and

needs.

Integration of the Finnish National Tax Administration Systems with EU Recapitulative Statement Data

367

Preliminary integration work and information

sharing should have been performed better

throughout the project. Certain misunderstandings

and lack of knowledge affected the final

specifications and implemented solution.

3.2 Communication

Communication channels should undergo project

organisation. The transparency of all prepared and

implemented plans, decisions and actions should be

available to all parties. The distribution of

information is important to maintain uniformity and

for further evaluation. From a communication

perspective, the work flow for a successful project

should be as follows:

Business representatives should communicate and

identify the aims and final objectives and at the same

time, the technical side should be aware of these aims

to develop a sufficient understanding of the business.

A mutual consensus and trust has to be achieved

before technical development. These aims should be

clear and accordingly, technical plans and decisions

should be made. The business and technical side have

to evaluate final decisions. All concerned parties have

to accept and subscribe to the plans.

Implementing the technical solution should be

trouble-free and when the implementation is

complete, the development lifecycle can proceed with

the evaluation and re-specification when needed.

3.3 Documentation

During the case project, there was also a need for

more accurate reasoning in the decision-making

process for development. Decisions have and will

always be questioned and therefore, there should

accurate documentation and reasoning in place.

Appropriate documentation can significantly help

further evaluating purposes.

The importance regarding documenting reasoning

and general reporting was highlighted by several

interviewees. There appeared to be a need to improve

project documentation for the entire project.

Furthermore, through the research, it was realised that

there was no exact consensus on the goals and aims

during the development work.

Few other problems identified were confusion in

the decision-making process and regarding roles as

well as the mandate to perform certain actions. The

evaluation showed that, in addition to

communication, reporting was inadequate and should

have been improved.

3.4 Proposed Model

The model and results answer the following question:

how can information systems related to EU data be

designed and evaluated?

An attempt to answer the question ‘How can EU

data be integrated and digital information systems

designed?’ facilitated the motivation underlying this

study: the description of a mechanism as well as

guidance and process steps for development.

List of process steps for development followed:

1. Participants of the developing work, that is,

project organisation should be carefully selected

and there should be a strong will to complete the

objective proposed by all concerned parties.

2. Sufficient resources should be available and

participants must have adequate knowledge and

the will to see the project through.

3. Role descriptions should be clear in the early

phase and revised later, if necessary.

4. Business representatives should communicate and

identify the aims and final goal. The technical side

should be presented; however, interviews should

first focus on listening or obtaining information to

sufficiently understand the business side.

5. A mutual consensus has to be reached before

technical development. This solution should be

clear and decisions should be made on the basis of

the setting.

6. Technical planning, including specifications,

process descriptions and final documentations,

should subscribe to the entire project organisation

and serve as a transparent information sharing

process.

7. Plans should be evaluated by both, the business

and technical side, including all participating

operators. If something remains to be addressed or

revisited, then step four should be reconsidered.

8. Implementation should be clear and trouble-free if

all previous steps have been completed.

9. Implemented functionalities should be evaluated.

10. Check if re-specification is needed.

There should be adequate knowledge and open

mindedness to identify as many scenarios as possible

and an eye for future development in the environment

and related changes. In addition, there should be

awareness regarding how integration can affect

confidence in the existing processes.

Another implication is that when outside

customers are involved, the customers’ perspective

should be accounted for in the scenarios.

ISE 2015 - Special Session on Information Sharing Environments to Foster Cross-Sectorial and Cross-Border Collaboration between Public

Authorities

368

There is always a gap between the technical and

business side. Research data have often highlighted

that information systems do not talk the same

language as businesses. Despite the lack of a mutual

language and ontological understanding, it remains

important to involve both sides from the beginning.

The roles and activities will undergo continuous

change during the project steps.

A similar discussion can be found in the literature

regarding business professionals facing difficulties in

discussing software-related details that are not

directly linked with everyday work. In addition,

discussions related to information systems could miss

several key terms and ‘displays’, which can engage

business professionals and should be discussed before

dealing with technical details.

4 CONCLUSION

The study marked at identifying more efficient ways

of tax control in the domain of recapitulative

statements data integration. Information systems and

tools were distributed and a lot of manual work was

conducted to control recapitulative statements data.

The results indicate that it is important to evaluate

the integration project. The need for integration was

obvious, but a deeper understanding was needed with

an in-depth analysis of the development project.

It also offered implications for tax administrators

regarding the effectiveness of similar projects and the

importance of cooperation communication. A more

effectively run project can reduce costs and help

devise better ways to define control procedures.

The created model for the above-mentioned

research and development steps and concluded

mechanisms are presented in Table 1 and can help

future works on a similar type of integration. Based

on the evidence, the most important issue is the

overall understanding of the operational field, that is,

domain ontology. A challenging point is the

difference between business units and related

approaches, in this case, toward data. This challenge

can be tackled with strong cooperation and

collaborative activities. This needs flexibility,

resilience, listening abilities and perception of wider

entities than one’s own business unit.

In conclusion, the need for integration was

obvious. Although the implementation method was

not entirely clear, it was concluded and successful.

The integration affected the existing ways of working

and suggested new ones for tax control across

national borders.

From a researcher’s viewpoint, some mistakes

made during the project have helped find direction in

modelling design work. When data were collected

and triangulated from various sources, such

causalities can be dealt with. A review of the entire

data revealed the exact points at which mistakes were

made. It is noteworthy that this study exposed certain

challenges in this type of work, which otherwise

would have remained unnoticed.

How can these problems be avoided? The easiest

way is to improve participants’ overall understanding

of the control area, or pre-operational validation.

However, this may be a rather simplified answer

given that the field comprises different businesses,

information systems, operative developers and actors

as well as varying levels of digitalisation. Thus,

cooperation seems to be the most vital aspect,

particularly when there are several parties, a point

highlighted by every interviewee.

The challenges are not restricted to activities in

the research and development project. In fact, the

organisational environment and existing

circumstances can also affect the background agency.

These larger observations are difficult to analyse

and there exist certain factor that could affect this

project and the integration, for example, lack of

resources. Limited resources can affect challenges to

organisational capability.

This study emphasises the significance of

cooperation and higher participant commitment to

understand the facts and learn from experiences of

other businesses, which is parallel to a deeper

understanding of one’s own business. The study

found that cooperation, commitment and trust can

affect every step in the project and the lifecycle of the

development work.

Different organisational units not only collaborate

with each other to share knowledge, but also compete

with each other to maximise their own benefits.

Internally, they vie for the organisation’s limited

resources. Consequently, they try to outperform other

units that offer similar products or services in the

market place. Thus, it is reasonable to expect that the

effectiveness of coordination mechanisms for

knowledge sharing depends on the conditions of

competition among organisational units.

As mentioned earlier, this study project is not only

about techniques and processes but also cooperation

and trust building as well as choices to be evaluated

and decisions to be made.

The study offers suggestions for future works. The

regulation includes many international and domestic

anti-tax fraud motives, such as the Organisation for

Economic Co-operation and Development (OECD)

Integration of the Finnish National Tax Administration Systems with EU Recapitulative Statement Data

369

tax compliance model. Research can be furthered in

anti-tax fraud work, given the exiting call for actions

regarding the shared tax administration.

Another important viewpoint for future research

is reorganizing tax control duties by increasing the

automation level of control procedures and

digitalizing EU recapitulative statement data.

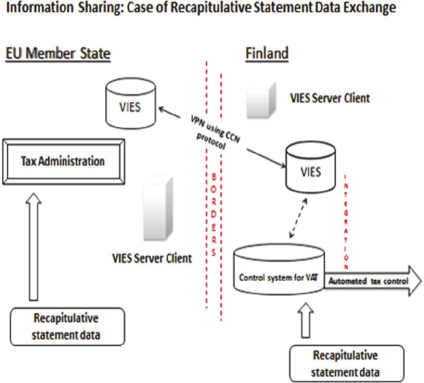

Figure 1: Mechanism of recapitulative statement data

exchange.

List of abbreviations used in Figure 1: VAT

(Value Added Tax), VIES (VAT Information

Exchange System), Recapitulative statement data

(Data of business registered for VAT), CCN

(Common Communication Network), VPN (Virtual

Personal Network).

The term “recapitulative statement data” (in the

title of Figure 1) consist of value-added tax (VAT) for

businesses registered with the EU member states that

provide intra-EU supplies to actors who are obligated

to complete recapitulative statements. The statements

grade the aggregate value of goods and services

supplied to VAT-registered customer elsewhere in

the EU.

This study was based on the European Union’s

Common Information Sharing research theme and

research agenda targets related to the public authority

in Finland. The target of study is addressed to the

information sharing utilisation that foster cross-

sectorial and cross-border collaboration among

public authorities, the dissemination of the related EU

initiative and steps along the EU information sharing

roadmap.

REFERENCES

Benbasat, I., Goldstein, D. K., Mead, M., 1987. The case

research strategy in studies of information systems. MIS

Quarterly, 11(3), 369-386.

Campbell, D. T., Fiske, D. W., 1959. Convergent and

discriminant validation by the multitrait-multimethod

matrix. Psychological Bulletin, 56, 81-105.

Dubé, L., Paré, G., 2003. Rigor in information systems

positivist case research: Current practices, trends, and

recommendations. MIS Quarterly, 27(4), 597-635.

Gregor, S., 2002. Design theory in information systems.

Australian Journal of Information Systems, Special

Issue, 14-22.

Hevner, A. R., Chatterjee, S., 2010. Design research in

information systems: Theory and practice. New York:

Springer.

March, S. T., Smith, G. F., 1995. Design and natural science

research on information technology. Decision Support

Systems, 15(4), 251-266.

Markus, M. L., Majchrzak, A., Gasser, L., 2002. A design

theory for systems that support emergent knowledge

processes. MIS Quarterly, 26(3), 179-212.

Miles, M. B., Huberman, A. M., 1994. Qualitative data

analysis: An expanded sourcebook. Thousand Oaks:

Sage Publications.

Nunamaker, J. F., Briggs, R. O., 2011. Toward a broader

vision for information systems. ACM Transactions on

Management Information Systems, 2(4), 1-12.

Robson, C., 2002. Real world research. Oxford: Blackwell

Publishing, 2

nd

edition.

Yin, R. K., 2009. Case study research design and methods.

Thousand Oaks: Sage Publications, 4

th

edition.

APPENDIX

COM (2012) 351 final. Communication from the

Commission to the European Parliament and the

Council. 2012. On concrete ways to reinforce the fight

against tax fraud and tax evasion including in relation

to third countries.

COM (2012) 722 final. Communication from the

Commission to the European Parliament and the

Council. 2012. An action plan to strengthen the fight

against tax fraud and tax evasion.

DG TAXUD IT AO-06. 2012. INVITATION TO TENDER

TAXUD/2012/AO-06. Annex II. A.

http://ec.europa.eu/taxation_customs/resources/docum

ents/common/tenders_grants/tenders/ao-2012-

06/annex_2a.pdf (Accessed: 7 August 2013).

EUR Lex. 2008 Access to European Union law and related

documents. http://eur-lex.europa.eu/homepage.html

(Accessed: 5 October 2015).

ISE 2015 - Special Session on Information Sharing Environments to Foster Cross-Sectorial and Cross-Border Collaboration between Public

Authorities

370