Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud

Detection in Financial Data Streams

Roberto Saia, Ludovico Boratto and Salvatore Carta

Dipartimento di Matematica e Informatica, Universit`a di Cagliari, Cagliari, Italy

Keywords:

Fraud Detection, Pattern Recognition, User Model.

Abstract:

The exponential and rapid growth of the E-commerce based both on the new opportunities offered by the In-

ternet, and on the spread of the use of debit or credit cards in the online purchases, has strongly increased the

number of frauds, causing large economic losses to the involved businesses. The design of effective strategies

able to face this problem is however particularly challenging, due to several factors, such as the heterogeneity

and the non-stationary distribution of the data stream, as well as the presence of an imbalanced class distribu-

tion. To complicate the problem, there is the scarcity of public datasets for confidentiality issues, which does

not allow researchers to verify the new strategies in many data contexts. Differently from the canonical state-

of-the-art strategies, instead of defining a unique model based on the past transactions of the users, we follow

a Divide and Conquer strategy, by defining multiple models (user behavioral patterns), which we exploit to

evaluate a new transaction, in order to detect potential attempts of fraud. We can act on some parameters of

this process, in order to adapt the models sensitivity to the operating environment. Considering that our mod-

els do not need to be trained with both the past legitimate and fraudulent transactions of a user, since they use

only the legitimate ones, we can operate in a proactive manner, by detecting fraudulent transactions that have

never occurred in the past. Such a way to proceed also overcomes the data imbalance problem that afflicts

the machine learning approaches. The evaluation of the proposed approach is performed by comparing it with

one of the most performant approaches at the state of the art as Random Forests, using a real-world credit card

dataset.

1 INTRODUCTION

Any business that carries out activities on the Internet

and accepts payments through debit or credit cards,

also implicitly accepts all the risks related to them,

like for some transaction to be fraudulent. Although

these risks can lead to significant economic losses,

nearly all the companies continue to use these pow-

erful instruments of payment, as the benefits derived

from them will outweigh the potential risks involved.

Fraud is one of the major issues related with the use

of debit and credit cards, considering that these in-

struments of payment are becoming the most popular

way to conclude every financial transaction, both on-

line and in a traditional way. According to a study

of some years ago conduct by the American Associ-

ation of Fraud Examiners

1

, fraud related with the fi-

nancial operations are the 10-15% of the whole fraud

cases. However, this type of fraud is related to the

75-80% of all involved finances with an estimated av-

1

http://www.acfe.com

erage loss per fraud case of 2 million of dollars, in

the USA alone. The research of efficient ways to face

this problem has become an increasingly crucial im-

perativein order to eliminate, or at least minimize, the

related economic losses.

Open Problems. Considering that the number of

fraudulent transactions is typically much smaller than

that of the legitimate ones, the distribution of data is

highly unbalanced (Batista et al., 2004), reducing the

effectiveness of many learning strategies used in this

field (Japkowicz and Stephen, 2002). The problem

of the unbalanced data distribution is further compli-

cated by the scarcity of information in a typical record

of a financial transaction, which generates an overlap-

ping of the classes of expense of a user (Holte et al.,

1989). A fraud detection system can basically operate

following two different learning strategies: static and

dynamic (Pozzolo et al., 2014). Through the static

strategies, the model used to detect the frauds is com-

pletely generated after a certain time period, while in

the dynamic strategies it is generated one time, then

496

Saia, R., Boratto, L. and Carta, S..

Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud Detection in Financial Data Streams.

In Proceedings of the 7th International Joint Conference on Knowledge Discovery, Knowledge Engineering and Knowledge Management (IC3K 2015) - Volume 1: KDIR, pages 496-503

ISBN: 978-989-758-158-8

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

updated after a new transaction. Most of the state-of-

the-art approaches used in this context are based on

the detection of the suspicious changes in the user be-

havior, a quite trivial approach that in several cases

leads toward false alarms. This because numerous of

these approaches do not include some non-numeric

data in the evaluation process, due to their incapac-

ity to manage them (e.g., the machine learning ap-

proaches, such as the Random Forests, are not able to

manage many categories, typically not more than 32).

Our Contribution. The vision behind this paper is

to extend the canonical criteria, integrating to them

the ability to operate with heterogeneous informa-

tion, and by adopting multiple behavioral patterns of

the users. This approach reduces the problems pre-

viously underlined, related with the scarcity, hetero-

geneity, non-stationary distribution, and presence of

an imbalanced class distribution, of the transactions

data. This is possible because we take into account all

parts of a transaction, considering more information

about it, contrasting the scarcity of information that

leads toward an overlapping of the classes of expense.

By means of the generation of multiple behavioral

models of a user, made by dividing the sequence of

transactions in several event-blocks, we face instead

the problem of the non-stationarity of data, modeling

anyway the user behavior effectively.

Differently from the canonical machine learning

approaches at the state of the art (e.g., the Random

Forests approach to which we compared in this work),

our models do not need to be trained with the fraud-

ulent transactions, because their definition needs only

the legitimate ones. This overcomes the problem of

data imbalance that afflicts the machine learning ap-

proaches. The level of reliability of a new transac-

tion is evaluated by comparing its behavioral pattern

to each of the behavioral patterns of the user. This

work provides the following main contributions to the

current state of the art:

• introduction of a strategy able to manage hetero-

geneous parts of a financial transaction (i.e., nu-

meric and non-numeric), convertingthem in abso-

lute numeric variations between each pair of con-

tiguous events;

• definition of the Transaction Determinant Field

(TDF) set, a series of distinct values extracted

from a field of the transaction, and used to give

more importance to certain elements of a transac-

tion, during the fraud detection process;

• introduction of the Event-block Shift Vector

(EBSV) operations, made by sliding a vector of

size eb (event-block) over the sequence of abso-

lute variations previously calculated, in order to

store, in the behavioral patterns of a user, the av-

erage values of the variations measured in each

event-block;

• definition of a discretization process used to adjust

the sensitivity of the system in the fraud detec-

tion process, by converting the continuous values

in the behavioral patterns in output to the EBSV

process, in a number of d levels (discretization);

• formalization of the process of evaluation of a new

transaction, performed by comparing, through the

cosine similarity, its behavioral pattern with the

user behavioral patterns in P, in order to assign it

a certain level of reliability.

The paper is organized as follows: Section 2 provides

a background on the concepts handled by our pro-

posal; Section 3 provides a formal notation and def-

inition of the problem faced in this work; Section 4

provides all the details of the implementation of our

fraud detection system; Section 5 describes the ex-

perimental environment, the adopted metrics, and the

experimental results; the last Section 6 reports some

concluding remarks and future work.

2 RELATED WORK

The credit card fraud detection represents one of the

most important contexts, where the challenge is the

detection of a potential fraud in a transaction, through

the analysis of its features (i.e., description, date,

amount, an so on), exploiting a user model built on

the basis of the past transactions of the user. In (As-

sis et al., 2013), the authors show how in the field of

automatic fraud detection there is lack of real datasets

(publicly available) indispensable to conduct experi-

ments, as well as a lack of publications about the re-

lated methods and techniques.

Supervised and Unsupervised Approaches. In

(Phua et al., 2010) it is underlined how the unsuper-

vised fraud detection strategies are still a very big

challenge in the field of E-commerce. Bolton and

Hand (Bolton and Hand, 2002) show how it is pos-

sible to face the problem with strategies based both

on statistics and on Artificial Intelligence (AI), two

effective approaches in this field able to exploit pow-

erful instruments (such as the Artificial Neural Net-

works) in order to get their results. In spite the fact

that everysupervised strategy in fraud detection needs

a reliable training set, the work proposed in (Bolton

and Hand, 2002) takes in consideration the possi-

bility to adopt an unsupervised approach during the

fraud detection process, when no dataset of reference

containing an adequate number of transactions (legit-

imate and non-legitimate) is available. Another ap-

proach based on two data mining strategies (Random

Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud Detection in Financial Data Streams

497

Forests and Support Vector Machines) is introduced

in (Bhattacharyya et al., 2011), where the effective-

ness of these methods in this field is discussed.

Data Unbalance. As previously underlined, the un-

balance of the transaction data represents one of the

most relevant issues in this context, since almost all of

the learning approaches are not able to operate with

this kind of data structure (Batista et al., 2000), i.e.,

when an excessive difference between the instances

of each class of data exists. Several techniques of

pre-processing have been developed to face this prob-

lem (Japkowicz and Stephen, 2002; Drummond et al.,

2003).

Detection Models. The static approach (Pozzolo

et al., 2014) represents a canonical way to operate to

detect fraudulent events in a stream of transactions.

It is based on the initial building of a user model,

which is used for a long period of time, before its re-

building. In the so-called updating approach (Wang

et al., 2003), instead, when a new block appears, the

user model is trained by using a certain number of

latest and contiguous blocks of the sequence, then the

model can be used to infer the future blocks, or aggre-

gated into a big model composed by several models.

In another strategy, based on the so-called forgeting

approach (Gao et al., 2007), a user model is defined

at each new block, by using a small number of non-

fraudulent transactions, extracted from the last two

blocks, but keeping all previous fraudulent ones. Also

in this case, the model can be used to infer the future

blocks, or aggregated into a big model composed by

several models. In any case, regardless of the adopted

approach, the problem of the non-stationary distri-

bution of the data, as well as that of the unbalanced

classes distribution, remain still unaltered.

Differences with Our Approach. The proposed ap-

proach introduces a novel strategy that, firstly, takes

into account all elements of a transaction (i.e., nu-

meric and non-numeric),reducing the problem related

with the lack of information, which leads toward an

overlapping of the classes of expense. The introduc-

tion of the Transaction Determinant Field (TDF) set,

also allows to give more importance to certain ele-

ments of the transaction, during the model building.

Secondly, differently from the canonical approaches

at the state of the art, our approach is not based on

an unique model, but instead on multiple user models

that involve the entire set of data. This allows us to

evaluate a new transaction by comparing it with a se-

ries of behavioral models related with many parts of

the user transaction history. The main advantage of

this strategy is the reduction, or removal, of the issues

related with the stationary distribution of the data,

and the unbalancing of the classes. This because the

operative domain is represented by the limited event

blocks, and not by the entire dataset. The discretiza-

tion of the models, according to a certain value of d,

permit us to adjust their sensitivity to the peculiarities

of the operating environment.

3 PROBLEM DEFINITION

This section defines the problem faced by our ap-

proach, preceded by a set of definitions aimed to in-

troduce its notation.

Definition 3.1 (Input Set). Given a set of users

U = {u

1

,u

2

,...,u

M

}, a set of transactions T =

{t

1

,t

2

,...,t

N

}, and a set of fields F = { f

1

, f

2

,..., f

X

}

that compose each transaction t (we denoted as V =

{v

1

,v

2

,...,v

W

}, the values that each field f can as-

sume), we denote as T

+

⊆ T the subset of legal trans-

actions, and as T

−

⊆ T the subset of fraudulent trans-

actions. We assume that the transactions in the set

T are chronologically ordered (i.e., t

n

occurs before

t

n+1

).

Definition 3.2 (Fraud Detection). The main objective

of a fraud detection system is the isolation and rank-

ing of the potentially fraudulent transactions (Fan and

Zhu, 2011) (i.e., by assigning a high rank to the poten-

tial fraudulent transactions), since in the real-world

applications this allows a service provider to focus

the investigative efforts toward a small set of suspect

transactions, maximizing the effectiveness of the ac-

tion, and minimizing the cost. For this reason, we

evaluate the ability of our fraud detection strategy in

terms of its capacity to assign a high rank to frauds,

using as measure the average precision (denoted as

α), since it is considered the correct metric in this

context (Fan and Zhu, 2011). Others metrics com-

monly used to evaluate the fraud detection strategies,

such as the AUC (a measure for unbalanced datasets),

and PrecisionRank (a measure of precision within

a certain number of observations with the highest

rank) (Pozzolo et al., 2014), then are not taken in con-

sideration in this work.

The formalization of the average precision is

shown in Equation 1, where N is the number of trans-

actions in the set of data, and ∆R(t

r

) = R(t

r

) − R(t

r

−

1). Denoting as π the number of fraudulent transac-

tions in the set of data, out of the percent t of top-

ranked candidates, denoting as h(t) ≤ t the hits (i.e.,

the truly relevant transactions), we can calculate the

recall(t) = h(t)/π, and precision(t) = h(t)/t values,

then the value of α.

α =

N

∑

r=1

P(t

r

)∆R(t

r

) (1)

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

498

Lemma 1. The values R(t

r

) and P(t

r

) represent, re-

spectively, the recall and precision of the r

th

transac-

tion, then we have ∆R(t

r

) = (1/π) when the r

th

trans-

action is fraudulent, and ∆R(t

r

) = 0 otherwise.

Corollary 1. When the set processed by the Equa-

tion 1 is a set composed by a certain number of legit-

imate transactions, but with only one potential fraud-

ulent transaction to evaluate

ˆ

t (i.e., T

+

∪

ˆ

t), accord-

ing to the Definition 3.2 we have π = 1 and t = 1.

Consequently, from the previous Lemma 1, we can de-

fine a binary classification of the transaction

ˆ

t, since

∆R(t

r

) = 1 when the r

th

transaction is fraudulent, and

∆R(t

r

) = 0 otherwise, which allow us to mark a new

transaction as reliable or unreliable.

Definition 3.3 (Performed Tasks). In order to operate

with only numeric elements, able to characterize the

sequence of transaction events, we transform the set

T in the set

ˆ

T = {

ˆ

t

1

= |t

2

− t

1

|,

ˆ

t

2

= |t

3

− t

2

|,...,

ˆ

t

N

=

|t

N

− t

N−1

|}, where |

ˆ

T| = (|T| − 1), and each sub-

traction operation is performed on all fields f ∈ F

of the considered transactions, by using a different

criterion for each type of data. We also denote as

I = {i

1

,i

2

,...,i

Z

} the set of behavioral patterns gen-

erated at the end of the shift process, performed on the

set

ˆ

T, where the shift operation aims to extract the av-

erage value of a certain number (defined by the event-

block parameter) of contiguous variations of the set

ˆ

T. The purpose of this process is the definition of a

set of behavioral patterns, which takes into account

a series of contiguous events (i.e., the average varia-

tion), instead of only one (or all). To uniform all the

variations in I in a certain range of values, we de-

fine a new set P = {p

1

, p

2

,..., p

Y

}, with contains the

same elements of I, but where the value of each field

f ∈ F is discretized, according to certain number of

levels (defined by the discretization parameter d, with

d ≥ 2)). It should be noted that |I| = |P|.

Problem 1. For the reasons explained in Defini-

tion 3.2, our objective is to maximize the α value, by

ordering the new transactions on the basis of their

similarity with the behavioral patterns in P, in order

to rank the fraudulent transactions ahead the legal

ones:

max

0≤α≤1

α =

N

∑

r=1

P(t

r

)∆R(t

r

) (2)

4 OUR APPROACH

The steps needed to implement our strategy can be

grouped into the following five steps:

• Absolute Variation Calculation: conversion of

the transactions set T of a user into a set of ab-

solute numeric variations between two contiguous

transactions t ∈ T, adopting a specific criterion for

each type of data in the set F;

• TDF Definition: creation of a Transaction Deter-

minant Field (TDF) set, a series of distinct terms,

extracted from the field place, used to define a bi-

nary element in each pattern of the set P, allow-

ing to give more relevance to this field during the

fraud detection process;

• EBSV Operation: application of a Event-block

Shift Vector (EBSV) over the set of absolute nu-

meric variations

ˆ

T, aimed to calculate the average

value of the elements in the event-block eb, stor-

ing the results as patterns in the set I;

• Discretization Process: discretization of the av-

erage values in the set I, in accord with a de-

fined number of levels d (discretization). It al-

lows to adjust the sensitivity of the system during

the fraud detection process. The result of this op-

eration, along with the result of the TDF query,

defines the set of behavioral patterns P;

• Transaction Evaluation: assignation of a level

of reliability to a new transaction, by comparing

all patterns in the set P with the pattern obtained

by inserting the transaction to evaluate as last ele-

ment of the set T, repeating the process previously

described only for the last eb transactions.

4.1 Absolute Variations Calculation

In order to convert the set of transactions T in the set

of absolute variations

ˆ

T, according with the criterion

exposed in Section 3, we need to define a different

kind of operation for each different type of data in the

set F (excluding the field place, used in the Transac-

tion Determinant Field). Differently from a canon-

ical preprocessing approach, which in such contexts

usually has the task to convert the non-numeric val-

ues into numeric ones, the output of this step are the

absolute numeric variations calculated between con-

tiguous transaction events.

Numeric Absolute Variation. Given a numeric field

f

x

∈ F of a transaction t

n

∈ T (i.e., in our case the field

amount), we calculate the Numeric Absolute Varia-

tion (NAV) between each pair of fields, that belong

to two contiguous transactions (denoted as f

(t

n

)

x

and

f

(t

n−1

)

x

), as shown in Equation (3). The result is the

absolute difference between the values taken into ac-

count.

NAV = | f

(t

n

)

x

− f

(t

n−1

)

x

| (3)

Temporal Absolute Variation. Given a temporal

field f

x

∈ F of a transaction t

n

∈ T (i.e., in our case

the field date), we calculate the Temporal Absolute

Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud Detection in Financial Data Streams

499

Variation (TAV) between each pair of fields, that be-

long to two contiguous transactions (denoted as f

(t

n

)

x

and f

(t

n−1

)

x

), as shown in Equation 4). The result is

the absolute difference in days, between the two dates

taken in account.

TAV = |days( f

(t

n

)

x

− f

(t

n−1

)

x

)| (4)

Descriptive Absolute Variation. Given a textual

field f

x

∈ F of a transactiont

n

∈ T (i.e., in our case the

description field), we calculate the Descriptive Ab-

solute Variation (DAV) between each pair of fields,

that belong to two contiguous transactions (denoted

as f

(t

n

)

x

and f

(t

n−1

)

x

), by using the Levenshtein Dis-

tance metric described in Section 5.4.2, as shown in

Equation 5). The result is a value in the range from 0

(complete dissimilarity) to 1 (complete similarity).

DAV = lev

f

(t

n

)

x

, f

(t

n−1

)

x

(5)

4.2 TDF Definition

In order to define the Transaction Determinant Field

(TDF) from a field that we decide to consider as cru-

cial in the fraud detection process (in our case, the

field place), we extract from the set of transactions all

distinct values v

1

,v

2

,...,v

W

of this field, storing them

in a new set

ˆ

V = { ˆv

1

, ˆv

2

,..., ˆv

W

}

6=

, according with the

formalization introduced in Section 3. The set

ˆ

V will

be queried in order to check if the place of the transac-

tion under analysis is a place already used by the user,

or not. When it is true, the binary value of the corre-

sponding element of the behavioral pattern (i.e., the

field place of the behavioral pattern of the transaction

to evaluate, defined as described in Section 4) is set to

1, otherwise to 0. It should be noted that this value is

always set to 1 in the behavioral patterns related with

the past transactions of the user. In other words, the

TDF process operates like a drift detector (Kuncheva,

2008), and allows us to give more importance to cer-

tain parts of the transaction, during the building of the

behavioral models.

4.3 EBSV Operation

After we have converted the set of transaction T into

a set of absolute variations

ˆ

T, adopting the criteria

exposed in Section 4.1, we operate the shift opera-

tion by sliding the Event-block Shift Vector over the

sequence of absolute variation values stored in

ˆ

T,

one step at a time, extracting the average value of

the variations present in the defined event-block eb.

Given a event-block eb = 3, a set of variations

ˆ

T =

{v

1

,v

2

,v

3

,v

4

,v

5

,v

6

}, we can execute a maximum of

|C| shift operations, with |C| = |I| = (|

ˆ

T| − |eb| − 1),

as shown in the Equation 6.

ˆ

T = [v

1

,v

2

,v

3

,v

4

,v

5

,v

6

]

⇓

c

1

=

v

1

+v

2

+v

3

|eb|

,c

2

=

v

2

+v

3

+v

4

|eb|

c

3

=

v

3

+v

4

+v

5

|eb|

,c

4

=

v

4

+v

5

+v

6

|eb|

⇓

I = [c

1

,c

2

,c

3

,c

4

]

(6)

The sequence of values calculated in each event-

block eb, for each considered field (i.e., description,

amount, and date), represents the set I of behavioral

patterns of the user. It should be observed that we

have to discretize the patterns obtained through the

shift process, adding to them the binary value deter-

mined by querying the Transaction Determinant Field

set (as described in Section 4.2), before using them in

the evaluation process of a newtransaction. It is a pro-

cess quite similar to that performed in the context of

the time series (Hamilton, 1994), but in this case the

data in input are the numeric absolute variations mea-

sured between the numeric and non-numeric fields of

all transactions, and the output is a set of user behav-

ioral models.

4.4 Discretization Process

The continuous values f ∈ F present in the pattern set

I, obtained through the shift operation described in

Section 4.3), must be transformed in discrete values,

in accord with a certain level of discretization d. It al-

low us to determine the level of sensitivity of the sys-

tem during the fraud detection process. The result is a

set P = {p

1

, p

2

,..., p

Y

} of patterns that represent the

behavior of a user in different parts of her/his trans-

action history. Given a discretization value d, and a

set of patterns I, each continuous value v

c

of a field

f (i.e., we process only the fields description, date,

and amount, because the field place assumes a binary

value determined by the TDF process) is transformed

in a discrete value v

d

, following the process shown in

the Equation 7.

v

d

=

v

c

max( f) −min( f)

d

(7)

4.5 Transaction Evaluation

To evaluate a new transaction, we need to compare

each behavioral pattern p ∈ P with the single behav-

ioral pattern ˆp obtained by inserting the transaction

to evaluate as last element of the set T, repeating the

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

500

entire process previously described (variation calcu-

lation, shift, and discretization) only for the transac-

tions present in the last event-block (i.e., the event-

block composed by the last |time-frame| transactions

of the set T, were the last one element is the trans-

action to evaluate). The comparison is performed by

using the cosine similarity metric (described in Sec-

tion 5.4.1), and the result is a series of values in the

range from 0 (transaction completely unreliable) to 1

(transaction completely reliable). It should be noted

that the value of the field place depends on the re-

sult of the query operated on the TDF set, as de-

scribed in the Section 4.2. The value of similarity

is the average of the sum of the minimum and maxi-

mum values of cosine similarity cos(θ), measured be-

tween the pattern ˆp and all patterns of the set P, i.e.,

sim( ˆp,P) = (min(cos(θ)) + max(cos(θ)))/2. The re-

sult is used to rank the new transactions, on the basis

of their potential reliability.

5 EXPERIMENTS

This section describes the experimental environment,

the adopted dataset and strategy, as well as the in-

volvedmetrics, the parameters tuning process, and the

results of the performed experiments.

5.1 Experimental Setup

In order to evaluate the proposed strategy, we per-

form a series of experiments using a real-world pri-

vate dataset related to one-year (i.e., 2014) of credit

card transactions, provided by a researcher. Due to

the scarcity of datasets publicly available, that are rel-

evant to our context and that are not synthetic (or too

old), in order to test our strategy we chosen to adopt

this real and updated dataset, even considering that

the detection of potential frauds, using for the training

a small set of data, is more hard than using a big set of

data. The proposed EBSV approach was developed in

Java, while the implementation of the state-of-the-art

approach, used to evaluate its performance, was made

in R

2

, using the randomForest package.

5.2 Dataset

The dataset used for the training, in order to generate

the set of behavioral patterns P, contains one year of

data related to the credit card transaction of a user. It

is composed by 204 transactions, operated from Jan-

uary 2014 to December 2014, with amounts in the

2

https://www.r-project.org/

range from 1.00 to 591.38 Euro, 55 different descrip-

tions of expense, and 7 places of operation (when the

transaction is operated online, the place reported is In-

ternet). Considering that all transactions in the dataset

are legal, we have T

+

= 204 and T

−

= 0. The fields of

the transaction taken in consideration are five: Type of

transaction, City of transaction, Date of transaction,

and Amount in Euro. It should be noted that we do not

consider any metadata (e.g., mean value of expendi-

ture per week or month).

5.3 Strategy

Considering that it has been proved (Pozzolo et al.,

2014) that the Random Forests (RF) approach outper-

forms the other approaches at the state of the art, in

this work we chose to compare our EBSV approach

only to this one. For the reason described in Section 3,

we perform this operation by comparing their perfor-

mance in terms of Average Precision (AP). Since we

do not have any real-world fraudulent transactions to

use, we first define a synthetic set of data T

−

, com-

posed by 10 transactions aimed to simulate several

kind of anomalies, as shown in Table 1 (they have

been marked as unreliable, as well as the other ones

have been marked as reliable). We perform the ex-

periments following the k-fold cross-validation crite-

rion. Regarding the EBSV approach, we first parti-

tioned the entire dataset T

+

into k equal sized sub-

sets (according with the dataset size, we set k = 3),

which denote as T

(k)

+

. Thus, each single subset T

(k)

+

is

retained as the validation data for testing the model,

after adding to it the set of fraudulent transactions

T

−

(i.e., T

(k)

+

∪ T

−

). The remaining k− 1 subsets are

merged and used as training data to define the user

models. We repeat the same previous steps for the RF

approach, with the difference that, in this case, we add

the set T

−

also to training data. In both cases, we con-

sider as final result the average precision (AP) related

to all k experiments.

Since the RF approach is not able to operate a tex-

tual analysis on the transaction description, and that is

well-known that the RF approaches are biased by the

categorical variables that generate many levels (such

as the Description field), we do not use this field in

the RF implementation. In addition, in order to work

with the same type of data, in the RF implementa-

tion we converted the information of the field Date,

in time intervals between transactions, expressed in

days. For reasons of reproducibility of the RF exper-

iments, we fix the seed value of the random number

generator by the method set.seed(123) (the value is

not relevant). The RF parameters (e.g., the number of

trees to grow) have been defined in experimental way,

Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud Detection in Financial Data Streams

501

Table 1: Fraudulent Transactions Set.

TransactionID Fields Values (1=anomalous 0=regular)

From To

Description Place Date Amount Status

1 2 1 0 0 0 unreliable

3 4

0 1 0 0 unreliable

5 6

0 0 1 0 unreliable

7 8

0 0 0 1 unreliable

9 10

1 1 1 1 unreliable

by researching those that minimized the error rate

given as output during the RF process. The experi-

ments are articulated in two steps: in the first step, we

define the values to assign to the parameters that de-

termine the performance of the EBSV approach (i.e.,

event-block and discretization), as described in Sec-

tion 5.5; in the second step, we evaluate the EBSV

performance, comparing to the RF approach, by test-

ing the ability to detect a number of 2,4, . . . , 10 fraud-

ulent transactions (respectively, a frauds percentage

of 2.8%,5.5%, . . . , 12.8%).

5.4 Metrics

This section reports the metrics used during the ex-

periments, as well as those involved in our approach.

5.4.1 Cosine Similarity

In order to evaluate the similarity between the behav-

ioral pattern of a transaction under analysis, and each

of the behavioral patterns of the user, generated at the

end of the process exposed in Section 4, we use the

cosine similarity metric. The output of this measure

is bounded in [0, 1], with 0 that means complete di-

versity, and 1 complete similarity. Given two vectors

of attributes x and y (i.e., the behavioral patterns), the

cosine similarity, cos(θ), is represented using a dot

product and magnitude as shown in Equation 8.

similarity = cos(θ) =

x·y

kxkkyk

=

n

∑

i=1

x

i

×y

i

s

n

∑

i=1

(x

i

)

2

×

s

n

∑

i=1

(y

i

)

2

(8)

5.4.2 Levenshtein Distance

The Levenshtein Distance is a metric able to measure

the difference between two sequences of terms. Given

two strings a and b, it indicates the minimal number

of insertions, deletions, and replacements, needed to

transforming the string a into the string b. Denoting

as |a| and |b| the length of the strings a and b, the Lev-

enshtein Distance is given by lev

a,b

(|a|,|b|), as shown

in Equation 9.

lev

a,b

(i, j) =

max(i, j) ifmin(i, j) = 0

min

lev

a,b

(i− 1, j) + 1

lev

a,b

(i, j − 1) + 1 otherwise

lev

a,b

(i− 1, j − 1) + 1

(a

i

6=b

j

)

(9)

Where 1

(a

i

6=b

j

)

is the indicator function equal to

0 when a

i

= b

j

and equal to 1 otherwise. It should

be noted that the first element in the minimum corre-

sponds to deletion (from a to b), the second to inser-

tion and the third to match or mismatch, depending

on whether the respective symbols are the same.

5.4.3 Average Precision

The average precision (AP) is considered as the cor-

rect measure to use in the fraud detection context, as

described in Definition 3.2. Given N the number of

transactions in the dataset, ∆Recall(t

r

) = Recall(t

r

)−

Recall(t

r

− 1), π the number of fraudulent transac-

tions in the dataset (out of the percent t of top-ranked

candidates), h(t) ≤ t the truly relevant transactions,

Recall(t) = h(t)/π, and Precision(t) = h(t)/t, we can

obtain the AP value as shown in Equation 10.

AP =

N

∑

r=1

Precision(t

r

)∆Recall(t

r

) (10)

5.5 Parameter Tuning

Considering that the performance of our approach de-

pends on the parameters eb (event-block) and d (dis-

cretization), before evaluating its performance, we

need to detect their optimal values. To perform this

operation we test all pairs of possible values of eb and

d, in a range from 2 to 99 (to be meaningful, both

values must be greater than 1). The criterion applied

to choose the best values is the average precision AP,

as described in Section 3. The experiments detected

eb = 41 as best value of event-block, and d = 11 as

best value of discretization (i.e., the best performance

measured in all subsets involved in the k-fold cross-

validation process).

5.6 Experimental Results

The final result is given by the mean value of the

results of all experiments performed, in accord with

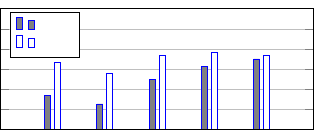

the k-fold cross-validation criterion. As we can ob-

serve in Figure 1, the performance of the EBSV ap-

proach reach those of the RF one, and this without

train its models with the past fraudulent transactions

(as occurs in RF). This result shows an important as-

pect, i.e., that EBSV is able to operate in a proactive

manner, by detecting fraudulent transactions that have

never occurred in the past.

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

502

2 4

6

8 10

0.2

0.4

0.6

0.8

1.0

Fraudulent Transactions

Average Precision

EBSV

RF

Figure 1: Experiment Results.

6 CONCLUSIONS AND FUTURE

WORK

In this paper we proposed a novel approach able to

reduce or eliminate the threats connected with the

frauds operated in the electronic financial transac-

tions. Differently from almost all strategies at the

state of the art, instead of exploiting a unique model

defined on the basis of the past transactions of the

users, we adopt multiple models (behavioral pat-

terns), in order to consider, during the evaluation of

a new transaction, the user behavioral in different

temporal frames of her/his history. The possibility

to adjust the levels of discretization and the size of

the temporal frames, give us the opportunity to adapt

the detection process to the operating environment

characteristics. Considering that our approach does

not need fraudulent transactions occurred in the past

to build the behavioral models, it allows us to op-

erate in a proactive manner, by detecting fraudulent

transactions that have never occurred in the past, al-

lowing also to overcome the problem of data imbal-

ance, which afflicts the canonical machine learning

approaches. The experimental results show that the

performance of the proposed EBSV approach reach

those of the state-of-the-art approach to which we

compared (i.e., Random Forests), and this without

training our models with the past fraudulent transac-

tions. A possible follow up of this work could be its

development and evaluation in scenarios with differ-

ent kind of financial transaction data, e.g., those gen-

erated in an E-commerce environment.

ACKNOWLEDGEMENTS

This work is partially funded by Regione Sardegna

under project SocialGlue, through PIA - Pacchetti

Integrati di Agevolazione “Industria Artigianato e

Servizi” (annualit`a 2010), and by MIUR PRIN 2010-

11 under project “Security Horizons”.

REFERENCES

Assis, C., Pereira, A., Pereira, M., and Carrano, E. (2013).

Using genetic programming to detect fraud in elec-

tronic transactions. In Proceedings of the 19th Brazil-

ian symposium on Multimedia and the web, pages

337–340. ACM.

Batista, G. E., Carvalho, A. C., and Monard, M. C. (2000).

Applying one-sided selection to unbalanced datasets.

In MICAI 2000: Advances in Artificial Intelligence,

pages 315–325. Springer.

Batista, G. E., Prati, R. C., and Monard, M. C. (2004). A

study of the behavior of several methods for balancing

machine learning training data. ACM Sigkdd Explo-

rations Newsletter, 6(1):20–29.

Bhattacharyya, S., Jha, S., Tharakunnel, K. K., and West-

land, J. C. (2011). Data mining for credit card fraud:

A comparative study. Decision Support Systems,

50(3):602–613.

Bolton, R. J. and Hand, D. J. (2002). Statistical fraud de-

tection: A review. Statistical Science, pages 235–249.

Drummond, C., Holte, R. C., et al. (2003). C4. 5, class

imbalance, and cost sensitivity: why under-sampling

beats over-sampling. In Workshop on learning from

imbalanced datasets II, volume 11. Citeseer.

Fan, G. and Zhu, M. (2011). Detection of rare items with

target. Statistics and Its Interface, 4:11–17.

Gao, J., Fan, W., Han, J., and Philip, S. Y. (2007). A

general framework for mining concept-drifting data

streams with skewed distributions. In SDM, pages 3–

14. SIAM.

Hamilton, J. D. (1994). Time series analysis, volume 2.

Princeton university press Princeton.

Holte, R. C., Acker, L., Porter, B. W., et al. (1989). Concept

learning and the problem of small disjuncts. In IJCAI,

volume 89, pages 813–818. Citeseer.

Japkowicz, N. and Stephen, S. (2002). The class imbal-

ance problem: A systematic study. Intell. Data Anal.,

6(5):429–449.

Kuncheva, L. I. (2008). Classifier ensembles for detecting

concept change in streaming data: Overview and per-

spectives. In 2nd Workshop SUEMA, pages 5–10.

Phua, C., Lee, V. C. S., Smith-Miles, K., and Gayler, R. W.

(2010). A comprehensive survey of data mining-based

fraud detection research. CoRR, abs/1009.6119.

Pozzolo, A. D., Caelen, O., Borgne, Y. L., Waterschoot, S.,

and Bontempi, G. (2014). Learned lessons in credit

card fraud detection from a practitioner perspective.

Expert Syst. Appl., 41(10):4915–4928.

Wang, H., Fan, W., Yu, P. S., and Han, J. (2003). Mining

concept-drifting data streams using ensemble classi-

fiers. In Proceedings of the ninth ACM SIGKDD in-

ternational conference on Knowledge discovery and

data mining, pages 226–235. ACM.

Multiple Behavioral Models: A Divide and Conquer Strategy to Fraud Detection in Financial Data Streams

503