Tailoring the Business Modelling Method for R&D

L. O. Meertens, N. Sweet and M. E. Iacob

University of Twente, PO Box 217, Enschede, The Netherlands

{l.o.meertens, m.e.iacob}@utwente.nl

Keywords: Business modelling, modelling method, business models, research & development.

Abstract: While the benefits of innovation seem to be clear intuitively, Research and Development (R&D) organisations

are struggling to show the value they add. Especially in times of crisis, the result is that they get the first

budget cuts to reduce costs in the short term. This causes companies, industries, or even whole economies, to

lose competitive advantage in the long run. The field of business modelling deals with the creation and

capturing of value. However, it has not yet provided a method tailored to R&D previously. Building upon

earlier work on business modelling, we adapt the Business Modelling Method (BMM) to the field of R&D.

1 INTRODUCTION: CREATING

VALUE WITH R&D

For a company to grow, it must keep ahead of

competitors whenever possible. To do this,

companies must innovate, which often depends on

Research and Development (R&D). Following this

reasoning, investing in R&D would give competitive

advantage. However, it is not that simple. A higher

R&D spending does not automatically lead to more

or better innovation. R&D is difficult to manage,

while the success is not known in advance.

Because the direct effect is hard to measure, it is

interesting to see how R&D adds value. This question

remains unanswered since the beginning of research

on R&D.

The field of business modelling researches the

creation and capturing of value. A business model is

a simplified representation of reality which tries to

show how a company does business or creates value.

It is interesting to combine the fields of R&D and

business modelling to expose the business model

behind R&D. Translation of this interest to scientific

research leads to the main research question of this

paper:

How to build a business model for a research and

development organisation?

The research question combines two scientific areas,

the one of business model research and the one of

R&D research. R&D research is related closely to

innovation research and is intertwined with various

fields of expertise, such as knowledge management,

marketing, production, and so on.

Business modelling is a field with many changing

factors in the past two decades. The rise of

information technology, the introduction of a new

distribution channel ‘the internet’, and other new

forms of communication, together with the rise of

globalization, makes business model research an

interesting topic (Osterwalder, Pigneur, & Tucci,

2005).

Based on Vermolen (2010), Meertens, Iacob, &

Nieuwenhuis (2011) conclude that current literature

provides no methodological approach for the design

and specification of business models. In an attempt to

make business modelling a science instead of an art,

Meertens et al. (2011) propose a method that enables

the development of business models in a structured

and repeatable manner. They jump in one of the

research gaps defined by Vermolen (2010), as

‘Design’, and by Pateli and Giaglis (2004), as ‘Design

tools’. In this paper, we further advance this method

by demonstrating how it can be tailored. In this case,

we tailor it for the field of R&D.

The structure of the paper is as follows. Section 2

reviews current literature on business modelling and

identifies typical characteristics of research and

development. Section 3 provides a design science

method to tailor the BMM to R&D. By applying that

method, section 4 tailors BMM based on R&D

characteristics. In section 5, the first four steps of the

tailored BMM are demonstrated by means of a case

study. The last section consists of conclusions and

provides directions for further research.

96

Meertens L., Sweet N. and Iacob M.

Tailoring the Business Modelling Method for RD.

DOI: 10.5220/0005885900960106

In Proceedings of the Fifth International Symposium on Business Modeling and Software Design (BMSD 2015), pages 96-106

ISBN: 978-989-758-111-3

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

2 LITERATURE REVIEW:

BUSINESS MODELLING AND

R&D CHARACTERISTICS

This section is divided in two parts: business

modelling and R&D characteristics. First, in the

business model section (2.1), a business modelling

method is chosen and presented. Then, in the R&D

section (2.2), the characteristics of R&D are

discussed.

2.1 Business Modelling

The term ‘business model’ is often used, especially in

the entrepreneurial and management field, but also in

other areas. The combination of these two words is

used for multiple purposes with significant different

meanings. This is mostly due to the fact that the term

comes from different perspectives like e-business,

strategy, technology, and information systems (Zott

& Amit, 2010). In 2005, (Shafer, Smith, & Linder,

2005) found 12 definitions in literature with 42

different components. At the same time Osterwalder

et al. (2005) received 54 different definitions from

participants in the IS community. Nevertheless, no

consensus concerning the definition of a business

model (Pateli & Giaglis, 2004; Vermolen, 2010) from

an academic perspective has been reached. In this

research, the definition given by Meertens et al.

(2011) is followed: “A business model is a simplified

representation that accounts for the known and

inferred properties of the business or industry as a

whole, which may be used to study its characteristics

further...”.

We choose this definition, as it indicates the use

of a business model, not only as a design artefact, but

also from a business engineering perspective.

Besides the lack of a generally accepted

definition, no widely accepted methods for the design

of business models exists. To the best of our

knowledge, Meertens et al. (2011) propose the only

method to build a business model in a generic and

systematic way. Therefore, we focus on this Business

Modelling Method (BMM) in this paper. Application

of this method results in at least two business models.

One business model reflects the ‘as-is’ (current)

situation of the business, and the other reflects the ‘to-

be’ (target) business model(s). This represents the

potential impact on the business model after adoption

of innovative technologies or more efficient business

processes (Meertens et al., 2011).

The BMM describes six steps using specific

methods, techniques or tools. The first four steps

concern the creation of the ‘as-is’ business model:

1. Identify roles

2. Recognize relations

3. Specify activities

4. Quantify model

The remaining two steps concern developing the ‘to-

be’ model:

5. Design alternatives

6. Analyse alternatives

Meertens et al. (2011) provide the BMM only as a

baseline methodology, with a limited amount of

concepts. The methodology has to be extended and/or

tailored to specific situations. Each of the steps can de

detailed further by inserting applicable techniques.

The specific situation for this research is an R&D

organisation, which means that the known and

inferred properties of R&D are needed to tailor the

method.

2.2 R&D Characteristics

To discover the known and inferred properties of

R&D, we review the literature to investigate what the

Table 1: Concept matrix of selected R&D literature.

Projectmanagement

Managingactivities

Riskmanagement

Costmanagement

Value

Externallinkages

(Ali, 1994)

● ●

(Balachandra & Friar, 1997)

● ●

(Brockhoff, Koch, & Pearson,

1997)

● ● ●

(Chesbrough, 2003)

●

(Coombs, McMeekin, & Pybus,

1998)

●

(Sherman & Olsen, 1996)

●

(Healy, Myers, & Howe, 2002)

●

(Kleinschmidt & Cooper, 1991)

●

(Lev, Sarath, & Sougiannis, 2005)

●

(Liberatore & Titus, 1983)

● ●

(Morandi, 2011)

● ●

(Nobelius, 2004)

●

(Pinto & Covin, 1989)

●●

Tailoring the Business Modelling Method for R&D

97

specific characteristics of R&D are. We follow an

explicit and systematic methodology to conduct the

literature review. Based on the literature review, we

selected the relevant and useful papers for this

research (Sweet, 2012).

By analysing the selected literature, we derive the

main concepts used to describe R&D. Table 1 shows

a concept matrix with the selected literature. Each of

the concepts is characteristic of R&D. In the

following sub-sections, we discuss each of the

characteristics.

2.2.1 Project-oriented

Liberatore and Titus (1983) notice that R&D

management research has an emphasis on project

management, which is in line with the conclusions of

Coombs, McMeekin, & Pybus (1998), and others

(Balachandra & Friar, 1997; Brockhoff, Koch, &

Pearson, 1997), that project management has an

important role in R&D.

R&D consists of projects. Pinto and Covin (1989)

state that projects usually have the following

attributes:

1. a specified limited budget

2. a specified time frame or duration

3. a preordained performance goal or set of goals

4. a series of complex, interrelated activities

These attributes lead to a set of characteristics and

issues, which are specific for R&D.

2.2.2 Risk Management

Pinto and Covin (1989) notice the overt risks, which

are familiar to R&D projects. Ali (1994) mentions a

lack or loss of project support and uncertain resource

requirements. The duration of an R&D project can be

very long (Brockhoff et al., 1997), especially for

radical innovation (McDermott & O’Connor, 2002;

Veryzer, 1998), which makes it harder and more risky

to determine the allocation of resources and set

reasonable goals. The same goes for project support,

which is important for R&D, because R&D benefits

are often only seen on the long term and success rates

are often low (Pinto & Covin, 1989; Sherman &

Olsen, 1996). The outcomes of R&D projects are

difficult to predict (Balachandra & Friar, 1997;

Brockhoff et al., 1997; Pinto & Covin, 1989), which,

together with the managerial aversion of taking risk,

makes risk management an important R&D

characteristic.

2.2.3 Managing Activities

R&D activities are often considered as a black box,

which is hard to systematically manage and control.

According to Brockhoff et al. (1997), R&D activities

are more often non-repetitive. Which is in line with

Pinto and Covin (1989), who state that activities

involved in R&D project execution are less amenable

to scheduling. A project is a series of complex

interrelated activities and the task uncertainty

(Morandi, 2013) involving R&D processes makes it

even more complex. However, because it is difficult

to manage and control R&D activities, this does not

mean it should be neglected. It is a common

understanding that the distinguished types of

innovation need to be managed differently.

Incremental innovation is more structured than

radical innovation, therefore the same management

and control techniques cannot always be used

interchangeable.

2.2.4 Value

Value is hard to determine because the success of the

outcome is not known. Even if the outcome definitely

leads to a patent, then the lifetime of that outcome or

product is not predictable. The expected returns from

incremental innovations are lower than from radical

innovations (Kleinschmidt & Cooper, 1991).

However, the risk associated with their development

and commercialisation is lower than from radical

innovations. Incremental innovations are important

for the firm’s overall profitability (Kleinschmidt &

Cooper, 1991).

2.2.5 Cost Management

Liberatore and Titus (1983) address the existence of

cost-effective techniques that can improve project

management for R&D. However, costing techniques

may not directly apply because of (lack of)

availability of information, which is in line with

earlier mentioned uncertainties. Uncertainty is why

financial accounting rules treat R&D as an expense

instead of the capitalisation of costs (Healy, Myers, &

Howe, 2002; Lev, Sarath, & Sougiannis, 2005).

Because the success of a R&D project is not known,

and neither is the eventual life time of the R&D

outcome, it is impossible to capitalise the R&D costs

without the big risk of manipulation of earnings

(Healy et al., 2002; Lev et al., 2005). The downside is

that intangible assets are often undervalued.

Fifth International Symposium on Business Modeling and Software Design

98

2.2.6 External Linkages

Rothwell (1994) mentions five generations of R&D.

Characteristic for the fifth generation is the emphasis

on external linkages, in other words R&D as a

network. The focus is on collaboration within a wider

system, involving competitors, suppliers, distributors,

etc.(Nobelius, 2004). This is in line with open

innovation that Chesborugh (2003) proposes. He

defines it as a paradigm that assumes that firms can

and should use external ideas as well as internal ideas,

and internal and external paths to market, as firms

look to advance their technology.

3 METHOD: DESIGN SCIENCE

APPROACH TO TAILOR THE

BMM TO R&D

Tailoring the BMM to R&D is a typical example of

design science. The result of this research consists of

artefacts at two levels according to the levels of

Gregor and Hevner (2013). We aim to contribute with

a second level (adapted method: the BMM4R&D)

and a first level (applied case: SBT) artefacts. We do

not have the intention to contribute to the third level

(grand design theory).

In the light of Gregor and Hevner (2013), we

position our research in the exaptation quadrant.

Exaptation in this context means that we attempt to

use the previously developed Business Modelling

Method (BMM) in another field: the field of Research

and Development (R&D). To achieve this, we tailor

the BMM for R&D by placing the right methods in

the slots/steps of the BMM, according to matching

with R&D characteristics.

In this paper, we attempt “to demonstrate that the

extension of known design knowledge into a new

field is nontrivial and interesting. The new field must

present some particular challenges that were not

present in the field in which the techniques have

already been applied" (Gregor & Hevner, 2013, p.

347).

The BMM contains prescriptive knowledge at the

second level (Nascent design theory—knowledge as

operational principles/architecture (Gregor &

Hevner, 2013, table 1)). Originally, it was developed

as a typical example of the improvement quadrant,

where a new solution was developed for a known

problem.

To adapt the existing BMM, we build on

methodology engineering as coined by Kumar and

Welke (1992) and further developed by Brinkkemper

(1996). More recently, Henderson-Sellers and Ralyté

(2010) captured the state-of-the-art on (situational)

methodology engineering. The methodology

engineering viewpoint has two aspects:

representational and procedural (Kumar & Welke,

1992). The representational aspect explains what

artefacts are looked at. The artefacts are the input and

deliverables of phases in the method. The procedural

aspect shows how these are created and used. This

includes the activities in each phase, tools or

techniques, and the sequence of phases.

In this research, we focus on the procedural

aspects, as the input and deliverables of each step are

quite well defined and suitable for almost any specific

situation where a business model has to be created.

Therefore, for each step (phase) in the BMM, we

reconsider the tools and techniques proposed in the

original method. For each step, we investigate the

literature for existing methods (tools/techniques)

possible in that step. Then, we compare those to the

R&D characteristics from the literature review in the

previous section. Based on this comparison, and

consideration of the originally proposed method, we

choose a method that best fits the particular

challenges of R&D. Thus, tailoring the BMM for

R&D. To demonstrate that the tailored method works,

we apply in two cases in an R&D organisation.

4 TAILORING THE BUSINESS

MODELLING METHOD FOR

R&D

In this section, the first four steps of the BMM are

assessed against the R&D characteristics from section

2.2. Step 5 and 6 are based on the first four steps or

use general techniques such as brainstorming. It is not

needed to assess them against the R&D

characteristics. Meertens et al. (2011) proposed

specific methods, techniques or tools that are suitable,

but they remark that other techniques may be useful

and applicable as well. Therefore, based on literature

reviews for every step, a possible set of suitable

techniques for BMM in an R&D setting is presented.

Before the tailored BMM is presented, it is

important to understand that this method is based on

the assumption that a R&D organisation is considered

as a portfolio of projects. This assumption is in line

with literature (Balachandra & Friar, 1997; Brockhoff

et al., 1997; Coombs et al., 1998; Liberatore & Titus,

1983; Pinto & Covin, 1989), but from the logic that

the projects create the value as well.

Tailoring the Business Modelling Method for R&D

99

4.1 Step 1: Identify Roles

One of the difficulties in ‘Risk management’ is the

often long time frame of R&D projects. While time

passes by, the interests of stakeholders change. The

stakeholder analysis (Elias, Cavana, & Jackson,

2002) focuses on the dynamics of stakeholders and

their changing interests. In this way, possible risks

can be foreseen and acted on.

Another focus of this stakeholder analysis is the

characteristic ‘External linkages’, which is implicitly

a part of every stakeholder analysis. This stakeholder

analysis distinguishes itself by conducting an analysis

on three levels, rational, process, and transactional.

This way, it gives a deeper insight in the management

of relations as well as the transactions that take place.

This information supports management of risks.

4.2 Step 2: Recognise Relations

The second step of the BMM aims to discover

relations among the roles. It may appear that relations

are already captured in the stakeholder analysis of the

first step and therefore this step is redundant.

However, several reasons exist why the recognition

of relations is a separate step in the BMM. First of all,

a stakeholder analysis often follows a hub-and-spoke

pattern, as the focus is on one of the roles (Meertens

et al., 2011). Meertens et al. (2011) suggest a role-

relation matrix as a deliverable, as this approach

forces to specify and rethink all possible relations

between the roles. Secondly, they note that relations

always involve some interaction between two roles.

Furthermore, they assume that this interaction

involves some kind of value exchange as well. This is

in line with Gordijn and Akkermans (2001) who state

that all roles in a business model can capture value

from the business model. From this perspective, the

proposed technique for this step, e3-value modelling,

is a valid one. The e3-value model models the

economic-value exchanges between actors

(Andersson, Johannesson, & Bergholtz, 2009;

Kartseva, Gordijn, & Tan, 2006). This economic-

value exchange can be tangible as well as intangible

(Allee, 2008; Andersson et al., 2009). The initiators,

Gordijn and Akkermans (2003), present the e3-value

model as being:

1. lightweight

2. a graphical, conceptual modelling approach

3. based on multiple viewpoints

4. exploits scenarios, both operational and

evolutionary

5. recognising the importance of economic value

creation and distribution

Properties 3 and 5 are in line with the choice of this

model in this step. The multiple viewpoint approach

is the missing link between the stakeholder analysis

and the role-relation matrix. Furthermore, the focus

on value exchange fits the property of a relation being

an interaction between roles with some kind of value

exchange. The remaining properties 1, 2, and 4 are

useful in step 5 of the BMM. The lightweight and

visual-oriented approach facilitates brainstorming

and generating scenarios, which are important aspects

of step 5.

Two R&D characteristics, which are relevant for

this step, are ‘Value’ and ‘External linkages’. The

value exchange of intangible assets is an exchange

that occurs often, as knowledge transfer goes hand in

hand with R&D. By exposing the tangible value

exchanges, as well as the intangible ones, the e3-

value model is suitable for R&D from a ‘Value’

perspective. This automatically shows that this model

is suitable from the perspective of ‘External linkages’

as well. External linkages are the relations between

different roles, for example a supplier, and the

exchange of for example knowledge. The strength of

the e3-value model lies in business network

environments and an organisation together with their

external linkages can be typed as a business network.

4.3 Step 3: Specify Activities

Meertens et al. (2011) propose techniques from

business process management to create the intended

output. However, in contrast to the example, R&D

activities are considered as a black box, which makes

them hard to specify. It is possible to cluster activities

in groups, but the number of techniques offered by

business process management is considerable, it is

necessary to look deeper into the field of business

processes in R&D.

4.4 Step 4: Quantify Model

For an organisation to assign costs, several systems

are available, which can be distinguished in

traditional systems and more refined systems, such as

Activity-Based Costing (ABC) (Drury, 2008).

Process costing, job costing, and a hybrid form of

these two are considered as traditional systems.

Process costing allocates costs to masses of identical

or similar units of a product or service, and job

costing allocates costs to an individual unit, batch, or

lot of a distinct product or service (Horngren et al.,

Fifth International Symposium on Business Modeling and Software Design

100

2010). Not only products or services can be cost

objects, also a customer, product category, period,

project (R&D / reorganisation), activity or a

department may qualify as a cost object. ABC refines

a costing system by assigning cost to individual

activities.

ABC is not a suitable technique for R&D as

activities are clustered and complex. Process costing

is used to cost masses of identical or similar units.

One of the characteristics of R&D is its non-repetitive

nature (Brockhoff et al., 1997), therefore process

costing is not suitable for R&D. Job costing, on the

other hand, allocates cost to an individual unit, batch,

or lot of a distinct product or service. As mentioned,

this research considers an R&D organisation as an

organisation that is built on projects. Although project

management techniques are used to create uniform

structures, such as New Product Development (NPD)

processes, this does not mean that process costing can

be used. These kinds of structures do not cluster

uniform activities but try to support the process of

delivering certain outputs. Each output is unique or

has its unique features and therefore job costing is a

suitable technique for R&D.

5 DEMONSTRATING THE

BUSINESS MODELLING

METHOD: THE SE BLADES

TECHNOLOGY CASE

Suzlon Energy Blades Technology (SBT) is an R&D

division of Suzlon Energy Limited and is specialised

in the design and development of rotor blades for

wind turbines. The division is spread out over four

locations: Hengelo (Netherlands), Århus (Denmark),

Pune, and Baroda (India). SBT is a project-oriented

organisation as most R&D organisations. Earlier, it is

stated that an R&D business model is a portfolio of

innovation processes. At SBT these innovation

processes are reflected in new product development

(NPD), design change management, and technology

projects. The NPD projects ‘directly’ create value for

the organisation, where the technology projects are

feeders for NPD projects. Finally, the design change

management projects are the continued development

of NPD projects. The innovation process for NPD

projects is already imbedded in the organisation in the

form of a Stage Gate System (see section 5.3).

In this case study, we examine two NPD projects

after the implementation of the stage gate system.

Both projects together should give a good perspective

on the innovation process of NPD’s at SBT and gives

us the opportunity to demonstrate the BMM4R&D.

5.1 Identify Roles

Suzlon is a multinational company with complex

relations. First of all, the business unit SBT itself is

internationally situated. It has to deal with various

cultures and different interests within the R&D

departments, and with the manufacturing in India as

well.

Furthermore, the interests of the wind turbine

division, overall Suzlon interests, and of course

market needs and market opportunities always play a

role. This reflects on current NPDs, future NPDs,

current and future technology projects. In this study,

the NPD is the unit of analysis, because an NPD can

be seen as an example of the generic NPD process

within SBT. The project teams consist of the

recurring roles. Although the location of these roles

may differ per project, the built up of a project team

is generic. Furthermore, internal stakeholders are not

taken into account, because research on roles within

projects is largely available.

For the sake of clarity, stakeholders in this paper

are combined and renamed. The stakeholders are

addressed per stage of the NPD (see section 5.3).

Suzlon Energy GmbH (SEG) and SBT manage

their organisations independently, which influences

an NPD on different levels. Not only do they interact

with each other, external factors as political change or

economic crises can have direct influence on each

project. The portfolio boards translate market needs

and opportunities into product strategies. NPD and

technology projects are derived from this strategy.

Table 2: Stakeholders per stage.

Stakeholder 1 2 3 4 5 6A 6B

SEG(SuzlonEnergyGmbH) ●● ●●●●

SBT(SuzlonBladeTechnology) ●●●●●●●

PBSEG(PortfolioBoardSEG) ●●●●●●●

PBSBT(PortfolioBoardSBT) ●●

NPDSEG(NPDonoveralllevel) ●●●●

Tailoring the Business Modelling Method for R&D

101

Most of the time the influence of the portfolio board

is long term, but some market changes need to be

reacted on quickly. Therefore, the potential influence

of such a stakeholder is always present. Finally, the

NPD SEG contains representatives from the whole

chain (R&D, moulding, purchasing, manufacturing,

services, finance, etc.). Every decision can influence

the financial cost of the other. Especially here, the

tension of the various forces can be intense.

These stakeholders are returning stakeholders

during every project and therefore people know by

experience how to act. The play of forces of the

different stakeholders’ interests, culture and politics

are managed by imbedded procedures and RASCIs.

The influence of the stakeholders at each stage differs

(see Table 2). Furthermore, an unexpected event can

lead to big power impact of a stakeholder which

would not have much influence during a certain stage

under other circumstances. Therefore, it is important

to give more insight in the relations between these

stakeholders in the next paragraph.

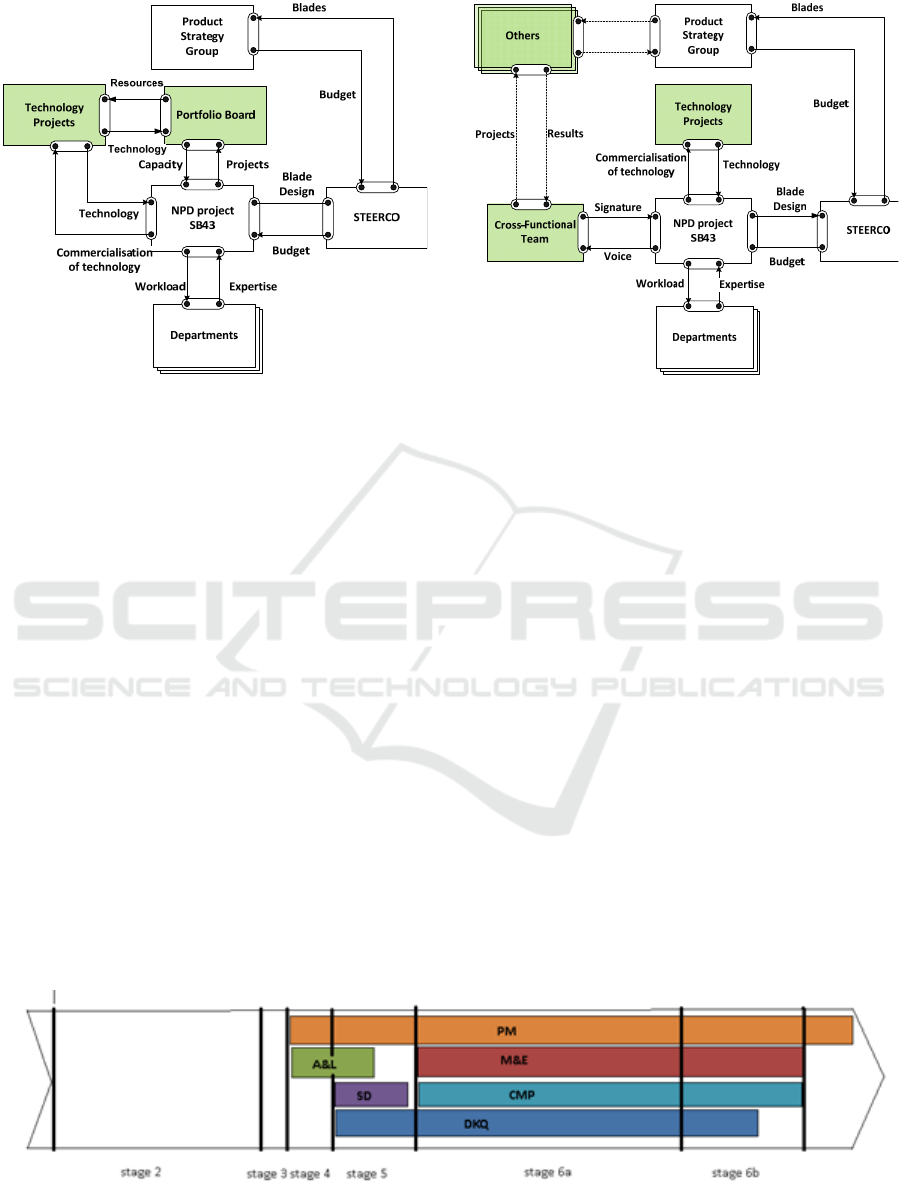

5.2 Recognize Relations

In the first step, we mapped the stakeholders per stage

and we do the same for this step, using the e3-value

model per stage. When done for every stage, we get

an extended view on the influence of stakeholders:

not only on the power aspect but on the value aspect

as well. Figure 1 shows the e3-value model of stage 3.

During the case study, an economic crisis

influenced the market dramatically. Governments

economised on subsidies for alternative resources

such as wind energy, which directly influenced

budgets. Other possible scenarios, such as radical

innovation because of a breakthrough in a technology

project, capacity problems in a department, or a

political change can be assessed per stage using the

e3-value model.

5.3 Specify Activities

An organisation needs to adapt the Stage-Gate system

according to its own needs (Cooper, 2009). This

Figure 1: e3-value model of SB43 Stage 3.

Figure 2: Departmental activity per stage.

Figure 3: e3-value model of SB43 Stage 4, 5, 6.

Fifth International Symposium on Business Modeling and Software Design

102

allows the method to be applicable to various kinds of

R&D organisation. At SBT, all the stages are present,

but stages are split up, and/or named differently, to fit

with the specific situation of SBT. Although stage 1

is part of the NPD process, it is not part of an NPD

project. In the best case, the activities of stage 1 are

assigned to a Technology project and, if possible, an

NPD project is set up at the start of stage 2.

The organisation has a structured innovation

process for NPD projects, which has all the elements

that the literature appoints. The projects at SBT are

managed on costs, which means in this case on hours

spent. At the end of each stage, there is a Go/No Go

decision and a new budget is assigned/approved. To

review the activities within the stages, the assigned

hours and the hours spent need to be compared.

Unfortunately, the setup of the budgets is not yet

aligned with the hour registration, which makes

comparison impossible.

An alternative comparison is possible because

SBT clusters departmental activities and embeds

them in their stage gate model as well. Clustering is

universal over all their NPD projects and shows

which departments are involved at what stage. Their

involvement is based on the needed output at the end

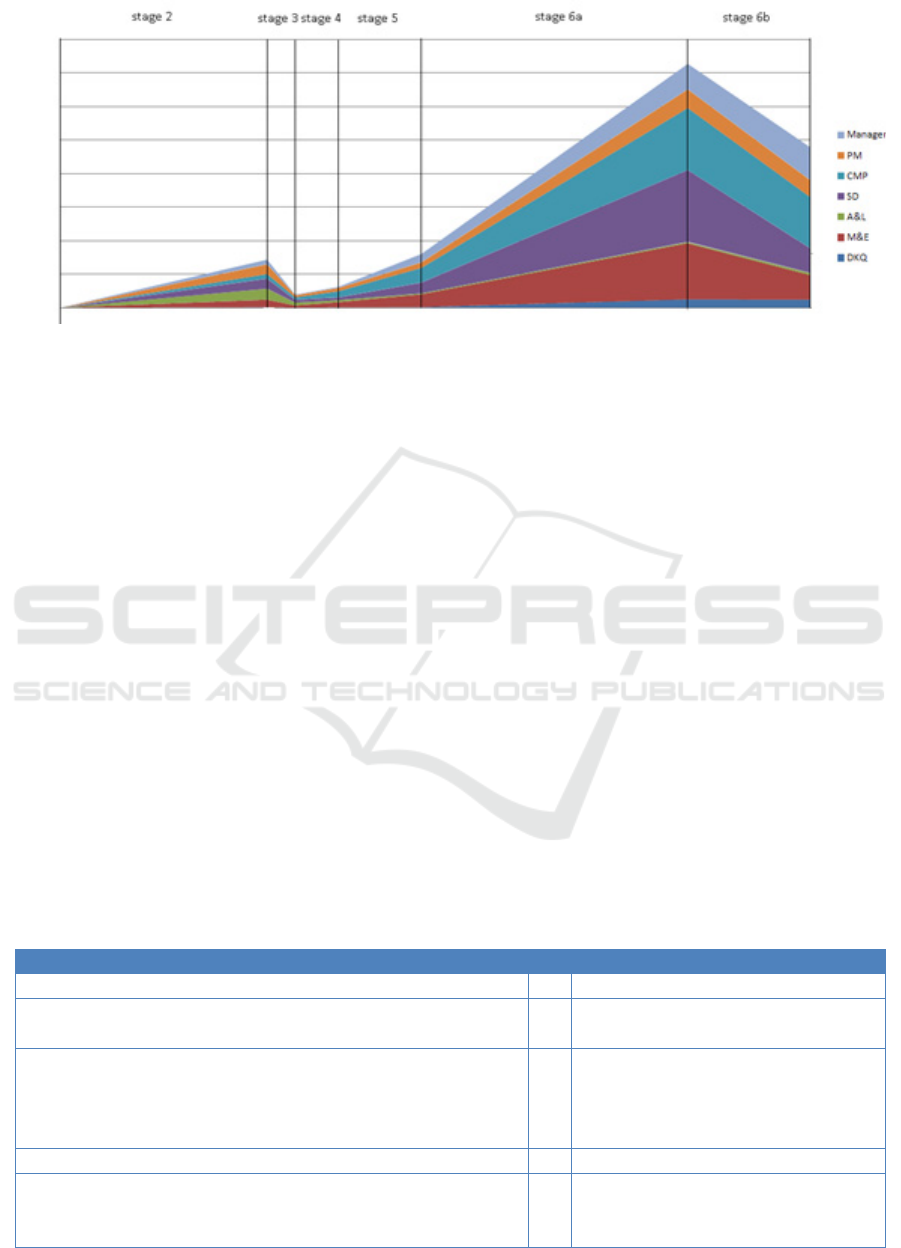

of each stage. Figure 2 gives an overview of the

departmental activity.

In Figure 4, the hours per department are put

against the SBT process model.

This figure shows that all the departments are

already involved at stage 2 and 3, which does not

match the distribution of the departmental activities

in Figure 2. However, the activities of department SD

should occur at stage 5, but most of them occur at

stage 6A and 6B. Furthermore, the activities of

department A&L are most spent at stages 2 and 3, but

should occur at stage 4 and 5.

Figure 4 shows a difference between the

clustering of activities at SBT and the actual

clustering. This can be related to step 1 and 2. For

example, the portfolio board allocates resources at

Table 3: Stage-Gate at SBT compared to Cooper (2008).

Stage SBTStageGateSystem StageGateSystem (Cooper,2008)

1 Marketneedsandbusinessperspectives 1 Scoping

2 FeasibilityStudy

2 Businesscase

3 ProjectPlanningandCommitment

4 SystemSpecification/Requirements

3 Development

5 PreliminaryDesign

6A StableDesign

6B StableDesign(incl.Prototyping)

7 SystemValidation 4 Testing&Verification

8 InitialLaunch

5 Launch

9 SeriesLaunch

10 ProjectClosure

Figure 4: Hours of departments involved at each stage.

Tailoring the Business Modelling Method for R&D

103

stage 3, but taking figure x into account, the allocation

already happened.

5.4 Quantify Model

A straightforward cost allocation method is used.

Typical for an R&D organisation, most costs occur

from labour hours. All indirect and direct costs can be

summed up and allocated to a single cost pool. In

Figure 5, the total cost of one of the projects is

calculated by adding all the direct and indirect costs.

The figure shows that the total costs are largely

build up out of indirect costs. For one of the projects

this percentage is as high as 96%. It can be expected

from a R&D organisation that most activities involve

labour hours. The amount of hours spent, which we

used in step 3 as a review of the clustering of

activities, is in line with the allocation in figure X.

Also, it indicates that the labour rate has a great

influence on the cost of a project. Using step 1, 2 and

3, potential threats for the labour rate can be assessed.

By demonstrating the BMM4R&D, we did a

quick scan of the current situation at SBT.

Furthermore, at every step we showed the possibility

to evaluate possible scenarios.

6 CONCLUSIONS: A BUSINESS

MODELLING METHOD FOR

RESEARCH AND

DEVELOPMENT

In this paper, we built a business model for a research

and development organisation. To achieve this, we

further specified the business modelling method

(BMM) (Meertens et al., 2011), to align it with

characteristics of research and development (R&D).

This led to the BMM4R&D: a Business Modelling

Method for Research and Development

organisations. The case studies for the field of R&D

illustrate that it is possible to tailor the BMM to

specific needs, as was originally proposed.

6.1 Academic and Business

Contributions

Our main contribution is the demonstration of how

the BMM can be tailored. Using the design science

approach, we deliver a level 2 artefact (Gregor &

Hevner, 2013), namely the BMM4R&D. It is a

tailored specialisation of the BMM The approach that

we used to tailor the BMM, improves the usability of

it for specific fields. The approach consists of

attaching applicable, field-specific methods to the

available hooks (steps) in the BMM. This opens the

way to tailoring the BMM to other fields as well, so

it can be used in practice.

The business contribution of this paper is

threefold. First, we define a set of characteristics for

R&D. Second, we provide a method to create

business models for R&D organisations: the

BMM4R&D. Third and final, we provide two cases

where a business model shows the value of R&D.

These all add to the relevance of this paper.

6.2 Limitations and Further Research

As part of this design science research, we built a

business model for an R&D organisation, using two

projects as cases. This demonstrates the use of the

BMM4R&D. To evaluate this new artefact further, it

should be applied to more cases. Additional case

studies could come from within the same

organisation, but also from other R&D organisations,

especially in other industries.

We tailored the BMM for R&D; however, we

advocate that the BMM can also be tailored to other

fields (Meertens et al., 2011). The originally proposed

BMM has several hooks where different methods

may be attached. Thus, tailoring to new fields is easy

to do. Yet, finding out which methods are most

suitable for a field is a harder challenge.

REFERENCES

Ali, A. (1994). Pioneering versus incremental innovation:

Review and research propositions. Journal of Product

Innovation Management, 11(1), 46–61.

Allee, V. (2008). Value network analysis and value

conversion of tangible and intangible assets. Journal of

Intellectual Capital, 9(1), 5–24.

Figure 5: Direct and indirect costs at each stage.

Fifth International Symposium on Business Modeling and Software Design

104

Andersson, B., Johannesson, P., & Bergholtz, M. (2009).

Purpose driven value model design. In Proc. CAiSE

workshop BUSITAL (Vol. 9). Citeseer.

Balachandra, R., & Friar, J. H. (1997). Factors for success

in R&D projects and new product innovation: a

contextual framework. Engineering Management,

IEEE Transactions On, 44(3), 276–287.

Brinkkemper, S. (1996). Method engineering: engineering

of information systems development methods and tools.

Information and Software Technology, 38(4), 275–280.

Brockhoff, K. K., Koch, G., & Pearson, A. W. (1997).

Business process re–engineering: experiences in R&D.

Technology Analysis & Strategic Management, 9(2),

163–178.

Chesbrough, H. W. (2003). Open innovation: The new

imperative for creating and profiting from technology.

Harvard Business Press.

Coombs, R., McMeekin, A., & Pybus, R. (1998). Toward

the development of benchmarking tools for R&D

project management. R&D Management, 28(3), 175–

186.

Cooper, R. G. (2008). Perspective: The Stage-Gate® Idea-

to-Launch Process—Update, What’s New, and NexGen

Systems*. Journal of Product Innovation Management,

25(3), 213–232.

Cooper, R. G. (2009). How companies are reinventing their

idea–to–launch methodologies. Research-Technology

Management, 52(2), 47–57.

Drury, C. (2008). Management and cost accounting.

Cengage Learning, London.

Elias, A. A., Cavana, R. Y., & Jackson, L. S. (2002).

Stakeholder analysis for R&D project management.

R&D Management, 32(4), 301–310.

Gordijn, J., & Akkermans, H. (2001). Designing and

evaluating e-business models. IEEE Intelligent

Systems, 16(4), 11–17.

Gordijn, J., & Akkermans, J. M. (2003). Value-based

requirements engineering: exploring innovative e-

commerce ideas. Requirements Engineering, 8(2), 114–

134.

Gregor, S., & Hevner, A. R. (2013). Positioning and

presenting design science research for maximum

impact. MIS Quarterly, 37(2), 337–356.

Healy, P. M., Myers, S. C., & Howe, C. D. (2002). R&D

accounting and the tradeoff between relevance and

objectivity. Journal of Accounting Research, 40(3),

677–710.

Henderson-Sellers, B., & Ralyté, J. (2010). Situational

Method Engineering: State-of-the-Art Review. Journal

of Universal Computer Science, 16(3), 424–478.

Horngren, C. T., Foster, G., Datar, S. M., Rajan, M., Ittner,

C., & Baldwin, A. A. (2010). Cost accounting: A

managerial emphasis. Issues in Accounting Education,

25(4), 789–790.

Kartseva, V., Gordijn, J., & Tan, Y.-H. (2006). Toward a

modeling tool for designing control mechanisms for

network organizations. International Journal of

Electronic Commerce, 10(2), 58–84.

Kleinschmidt, E. J., & Cooper, R. G. (1991). The impact of

product innovativeness on performance. Journal of

Product Innovation Management, 8(4), 240–251.

Kumar, K., & Welke, R. J. (1992). Methodology

Engineering: a proposal for situation-specific

methodology construction. In Challenges and

Strategies for Research in Systems Development (pp.

257–269). Chichester: Wiley.

Lev, B., Sarath, B., & Sougiannis, T. (2005). R&D

Reporting Biases and Their Consequences*.

Contemporary Accounting Research, 22(4), 977–1026.

Liberatore, M. J., & Titus, G. J. (1983). The practice of

management science in R&D project management.

Management Science, 29(8), 962–974.

McDermott, C. M., & O’Connor, G. C. (2002). Managing

radical innovation: an overview of emergent strategy

issues. Journal of Product Innovation Management,

19(6), 424–438.

Meertens, L. O., Iacob, M. E., & Nieuwenhuis, L. J. M.

(2011). Developing the business modelling method. In

B. Shishkov (Ed.), BMSD 2011 : First International

Symposium on Business Modeling and Software Design

(pp. 88–95).

Morandi, V. (2013). The management of industry–

university joint research projects: how do partners

coordinate and control R&D activities? The Journal of

Technology Transfer, 38(2), 69–92.

Nobelius, D. (2004). Towards the sixth generation of R&D

management. International Journal of Project

Management, 22(5), 369–375.

Osterwalder, A., Pigneur, Y., & Tucci, C. L. (2005).

Clarifying Business Models: Origins, Present, and

Future of the Concept. Communications of the

Association for Information Systems, 16(1).

Pateli, A. G., & Giaglis, G. M. (2004). A research

framework for analysing eBusiness models. European

Journal of Information Systems,

13(4), 302–314.

Pinto, J. K., & Covin, J. G. (1989). Critical factors in project

implementation: a comparison of construction and

R&D projects. Technovation, 9(1), 49–62.

Rothwell, R. (1994). Industrial innovation: success,

strategy, trends. The Handbook of Industrial

Innovation, 33–53.

Shafer, S. M., Smith, H. J., & Linder, J. C. (2005). The

power of business models. Business Horizons, 48(3),

199–207.

Sherman, J. D., & Olsen, E. A. (1996). Stages in the project

life cycle in R&D organizations and the differing

relationships between organizational climate and

performance. The Journal of High Technology

Management Research, 7(1), 79–90.

Sweet, N. (2012, December 12). How research &

development adds value : a business modelling method

for R&D organisations. University of Twente,

Enschede.

Vermolen, R. (2010). Reflecting on IS Business Model

Research: Current Gaps and Future Directions. In

Proceedings of the 13th TSConIT, University of Twente,

Enschede, Netherlands.

Tailoring the Business Modelling Method for R&D

105

Veryzer, R. W. (1998). Discontinuous innovation and the

new product development process. Journal of Product

Innovation Management, 15(4), 304–321.

Zott, C., & Amit, R. H. (2010). Business model design: an

activity system perspective. Long Range Planning,

43(2-3), 216–226.

Fifth International Symposium on Business Modeling and Software Design

106