Research on the Effectiveness of Financial Supervision of the

Supervisory Board

Wang Lu

Sichuan University, No.24 South Section 1, Yihuan Rode, Chengdu 610064, China

791305410@qq.com

Keywords: The Members of Supervisors Board, Financial Supervision, Corporate Governance.

Abstract: To strengthen system innovation and capacity building of the Supervisory Board, and to promote the

modernization of corporate governance, based on the samples of listed companies from 2007 to 2012 in china,

through the establishment of the modified Jones model to calculate discretionary accruals and adopted its

absolute value as a substitution variable for earnings management, this paper studied the problem of financial

supervision effectiveness of the Board of Supervisors. The results show that the age and degree of supervisors

are negative related to the company's earnings management while the banking background has a positive

correlation. The research did not find their sex or financial background has a significant influence on the

earnings management of listed companies. The conclusions show the professionalism of supervisors is limited

to exert, but the Supervisory Board still plays an irreplaceable role in corporate governance.

1 INTRODUCTION

In the modern corporate system, ownership and

management are separated. In order to solve the

interest conflict which might exists between the

owners and its managers, the new “Company Law”

article 54 provides that the Board of Supervisors the

right to inspect the company's financial situation. The

provision reflects that the financial supervision is an

important aspect of the Board of Supervisors to

represent the interests of shareholders to exercise

supervision functions. In reality, due to the Board of

Supervisors is not involved in day-to-day operation

and management, irregularities often be found after

the damages have happened to the company.

Therefore, in order to strengthen the function of the

Board of Supervisors, the new “Company Law”

article 55 stipulates that supervisors may attend board

meetings, and raise questions or suggestions on

resolutions or matters of the Board of Directors. As a

monitoring mechanism set up within company, the

responsibility fulfillment situation of the Board of

Supervisors is directly related to the stakeholders in

the protection of their interests, good condition of the

Board of Supervisors can help company to make the

right decisions, to maximize the shareholders' equity.

Then, how about the actual performance effect of

the legal power of the Board of Supervisors? This

article introduced the empirical data of listed

companies in our country, made an empirical study

between characteristics of the Supervisory Board

members and company's earnings management level

to provide some advices to the listed companies in

corporate governance.

2 RELATED LITERATURE

At present, a lot of studies suggest that the Board of

Supervisors has become a formality in China and its

supervision function is weakening. Jia et al., (2009)

studied the function of the Board of Supervisors when

listed companies were facing legal proceedings,

found it did not play a positive role which it should

play in corporate governance. Hu et al., (2010) argued

that, because of the influence of ownership

concentration, the Board of Supervisors had brought

negative impact to the operating performance of listed

companies. Sun Jingshui, Sun Jinxiu (2005) found

that the Board of Supervisors had no significant effect

on company’s performance through the empirical

analysis, and they had a conclusion that it did not

work as a role of supervision. Liu Shanmin (2008)

selected the negative independent opinion published

by the Board of Supervisors as a substitution

variables, found that the function of the Board of

Supervisors is very weak. Li Lijun, Jin Yuna (2010)

selected the size of the Board of Supervisors as the

422

422

Lu W.

Research on the Effectiveness of Financial Supervision of the Supervisory Board.

DOI: 10.5220/0006027704220426

In Proceedings of the Information Science and Management Engineering III (ISME 2015), pages 422-426

ISBN: 978-989-758-163-2

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

core, found that supervisory board’s constraints on

the manager's over-investment behavior is not fully

realized. Hu Haichuan, Zhang Xinling (2013) tested

the relationship between supervisory board

characteristics and the quality of information

disclosure of listed company, found that the Board of

Supervisors is negligible to improve the quality of

information disclosure.

However, there are also some studies suggest that

the Supervisory Board continues to play an

irreplaceable role in corporate governance. Firth et

al., (2007) found that the size of the Supervisory

Board, the Board of Supervisors meeting times is

positive related to earnings information content. Li

Weian, Hao Chen (2006) evaluated the situation of

Supervisory Board governance from the

characteristic of the Supervisory Board, the

evaluation results showed that supervisors lack

competence is the cause of the low level of

Supervisory Board Governance, but still come to the

Supervisory Board as the statutory corporate

oversight institutions play an irreplaceable role in

supervising. Wang Shuhui, Tong Ning (2009) [9]

study showed that in addition to the size of the Board

of Supervisors had no significant effect on

performance, the annual number of meetings of the

Board of Supervisors, the ratio of external

supervisors, Board of Supervisors shareholding

proportion and Supervisors shareholding proportion

was significantly positively correlated with company

performance, and indicated since the new “Company

Law” implemented, the Board of Supervisors play a

larger role in corporate governance.

In summary, research on effectiveness of the

Board of Supervisors has not yet formed a clear and

consistent conclusion, previous studies mainly

focused on the discussion of the relationship between

general characteristics of the Board of Supervisors

and its financial supervision effect. This paper

focused on the individual characteristics of

Supervisory Board members, tested its members’

impacts on the supervision function. Through manual

collection of personal traits of the members of

Supervisory Board, this paper tested the influence of

their age, gender, degree, financial and banking

background on the level of earnings management,

provided an important and useful perspective for the

existing controversy about the effects of the Board of

Supervisors.

3 RESEARCH DESIGN

3.1 Samples Selection

In this paper, we selected Shanghai and Shenzhen

stock exchange listed companies in China as samples,

the research time interval was 2007-2012. Data from

CSMAR database, background characteristics of

members of the Board of Supervisors mainly based

on the manual screening to resumes in CSMAR

database. In this paper, I excluded financial,

insurance companies; companies with negative net

assets; companies listed less than one year;

companies without complete financial data and

finally got 9732 observations.

3.2 Variables Settings

3.2.1 The Dependent Variable

The dependent variable was the level of earnings

management (EM).In this paper, used the modified

Jones model (1995) to calculate discretionary

accruals, and then adopted its absolute value to

measure the level of earnings management.

3.2.2 The Independent Variables

AGE, it obtained by the average age of all the

members of the Supervisory Board of the company.

GEND, it obtained by the average data of all the

members of the Supervisory Board of the company.

Male take 0, female take 1.

DEGRE, it obtained by the average degree level. Less

than or equal to high school take 1; college take 2;

master take 3; doctor take 4.

FAB, it equalled to the number of supervisors having

the financial or auditing background divided by the

total number of supervisors.

BSB, it equalled to the number of supervisors having

a banking or securities background divided by the

total number of supervisors.

3.2.3 Control Variables

Reference existing research, this paper selected the

company assets (SIZE), financial leverage (LEV),

return on assets (ROA), firm growth (GROWTH),

loss situation (LOSS), audit firm rankings (BIG4), the

size of board of directors (BOARDSIZE), listed year

of the company (LISTAGE), the proportion of the

largest shareholder (GENT), actual controller (SOE),

industry and year as control variables.

Research on the Effectiveness of Financial Supervision of the Supervisory Board

423

Research on the Effectiveness of Financial Supervision of the Supervisory Board

423

Table 1: Descriptive statistics.

Variable N mean min P25 median P75 max sd

AGE 9732 46.3043 24.3333 42.93 46.5 50 66 5.2715

GEND 9732 0.2457 0 0 0.2 0.3333 1 0.2385

DEGRE 9732 2.1887 1 2 2.1667 2.4 4 0.3980

FAB 9732 0.2460 0 0 0.25 0.3333 1 0.2297

BSB 9732 0.0558 0 0 0 0 1 0.1402

3.3 Research Model

To examine the relationship between characteristics

of the Supervisory Board and level of earnings

management, a multiple regression model was

constructed as follows:

EM=α_0+α_1 AGE+α_2 GEND+α_3 DEGRE+α_4

FAB+α_5 BSB+CONTROL VARIABLES+ε

(1)

4 RESULTS

4.1 Descriptive Statistics

As can be seen from table 1, in the five variables on

behalf of supervisor features, the average age of the

members of the Board of Supervisors is about 46

years old; the mean of proportion of female

members of the Board of Supervisors is about 25%,

there are even companies are about 0%, suggesting

that the proportion of male and female supervisors

is uncoordinated ;the mean degree of the

supervisors is about 2, indicating degree of the

supervisors focused on college; the mean and

median of proportion of supervisors have a financial

background in sample firms is 24.6% and 25%

respectively, showing that Chinese listed companies

have realized that supervisors have background in

financial play a special role in financial supervision,

and hired them serve as supervisors; the proportion

of supervisors With banking background is 5.58%,

showing that compared with financial background,

the listed companies in China don't tend to hire

people have banking background as supervisors.

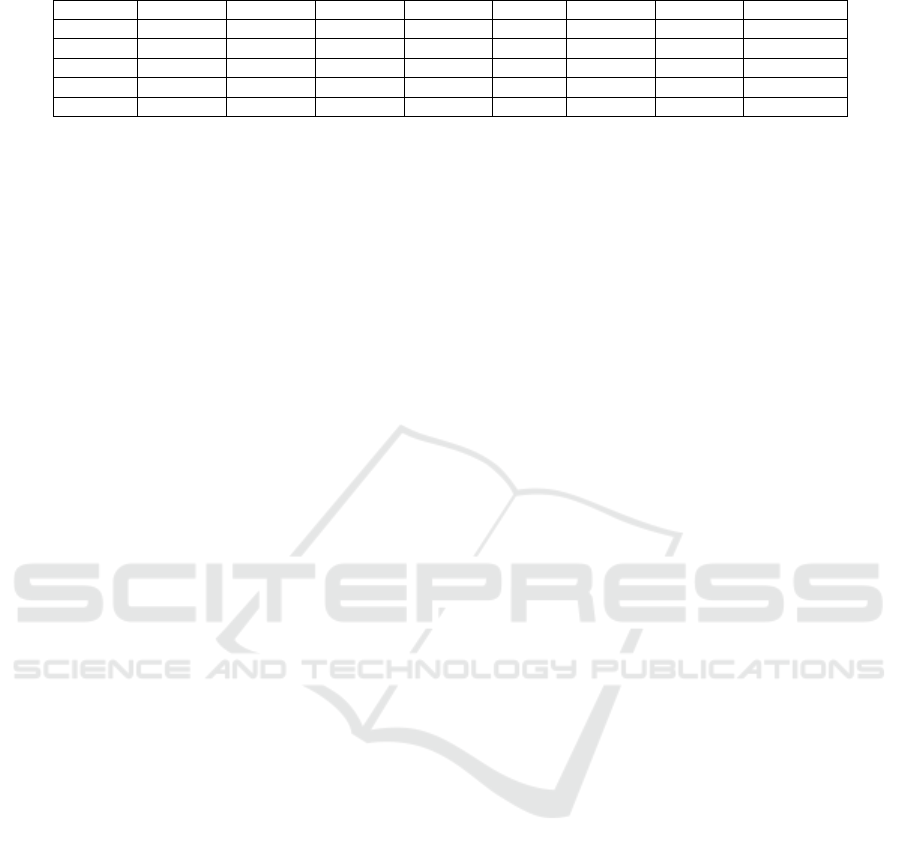

4.2 Regression Analysis

Table 2 reports the test result of the relationship

between characteristics of the Board of Supervisors

and the level earnings management( EM). (1)~ (5)

are regression equations in the presence of five

separate variables and control variables. (6) is the

regression equation including both all independent

variables and control variables. From table 2, there

are a significant negative correlation relationship

between the average age, average degree of

supervisors and level of earnings management,

indicating that the older and higher degree of

supervisors, the more constraints on the earnings

management behaviours of company. The

relationship between the proportion of banking

background of supervisors and earnings

management level is also significant, indicating that

the company is more likely to occur earnings

management behaviour with a larger proportion of

banking background of supervisors. The regression

coefficient of proportions of the members of

supervisors financial background and banking

background is negative, the reason may be that, our

Supervisory Board members are not entirely

composed by people independent and outside the

company, many supervisors of listed companies

include the head of company's accounting or

financial manager, etc..Because their independence

is difficult to guarantee as insiders, these internal

financial or banking experts may be constrained to

exert.

5 CONCLUSION

This paper studied the relationship between age,

gender, degree, financial and banking background

of the members of the Board of Supervisors and the

earnings management of listed companies in our

country. The research results show that the age of

the supervisory board members and the company's

earnings quality is significantly related. The older

the supervisors, the bigger likelihood to inhibit

earnings management behaviour of listed

companies. Degree and level of earnings

management are negatively correlated, suggesting

that supervisors with higher degree has higher

comprehensive qualities, have better ability to

perform financial supervision function. At the same

time, banking background of supervisors is

positively related to the company's earnings

management, showing the professionalism of

supervisors is limited in raising the quality of

earnings management. The sex and financial

background of supervisors has not a significant

influence on the earnings quality of listed compa-

ISME 2015 - Information Science and Management Engineering III

424

ISME 2015 - International Conference on Information System and Management Engineering

424

Table 2: Characteristics of Supervisory and Earnings Management.

EM (1) (2) (3) (4) (5) (6)

AGE -0.000 -0.000

(-2.20)** (-1.90)*

GEBD 0.005 0.004

(1.63) (1.09)

DEGRE -0.004 -0.006

(-2.29)** (-2.95)***

FAB 0.005 0.003

(1.60) (1.05)

BSB 0.013 0.015

(2.23)** (2.39)**

SIZE -0.004 -0.004 -0.004 -0.005 -0.004 -0.004

(-5.09)*** (-5.20)*** (-5.13)*** (-5.35)*** (-5.28)*** (-4.72)***

LEV 0.032 0.032 0.033 0.032 0.033 0.033

(6.60)*** (6.71)*** (6.75)*** (6.62)*** (6.82)*** (6.74)***

ROA 0.167 0.168 0.170 0.168 0.170 0.171

(7.42)*** (7.47)*** (7.52)*** (7.44)*** (7.55)*** (7.58)***

LOSS 0.035 0.036 0.036 0.035 0.036 0.036

(10.78)*** (10.79)*** (10.79)*** (10.76)*** (10.81)*** (10.89)***

BIG4 -0.003 -0.003 -0.002 -0.003 -0.003 -0.003

(-1.49) (-1.60) (-1.43) (-1.55) (-1.69)* (-1.49)

GENT 0.016 0.015 0.015 0.015 0.015 0.016

(2.85)*** (2.75)*** (2.79)*** (2.74)*** (2.79)*** (2.86)***

LISTAGE 0.000 0.000 0.000 0.000 0.000 0.000

(0.72) (0.41) (0.67) (0.45) (0.26) (0.71)

BOARDSIZE -0.001 -0.001 -0.001 -0.001 -0.001 -0.001

(-2.33)** (-2.38)** (-2.45)** (-2.45)** (-2.55)** (-2.42)**

GROWTH 0.021 0.022 0.022 0.022 0.021 0.021

(11.15)*** (11.24)*** (11.27)*** (11.23)*** (11.16)*** (11.10)***

SOE -0.008 -0.009 -0.008 -0.009 -0.009 -0.007

(-4.41)*** (-4.73)*** (-4.58)*** (-5.00)*** (-4.71)*** (-3.84)***

YEAR yes yes yes yes yes yes

INDUSTRY yes yes yes yes yes yes

_CONS 0.162 0.149 0.157 0.152 0.151 0.164

(7.98)*** (7.48)*** (7.92)*** (7.70)*** (7.65)*** (7.92)***

N 9732 9732 9732 9732 9732 9732

adj. R

2

0.171 0.171 0.171 0.171 0.172 0.173

F 30.195 30.209 30.334 30.150 30.371 27.751

nies. Thus, the effectiveness of Board of

Supervisors in financial supervision is limited to a

certain extent, but the Board of Supervisors still

plays an indispensable role.

REFERENCE

Jia C, Ding S, Li Y, et al. 2009.Fraud, enforcement action,

and the role of corporate governance: Evidence from

China. Journal of Business Ethics, 90(4): 561-576.

Hu H W, Tam O K, Tan M G S.2010. Internal governance

mechanisms and firm performance in China. Asia

Pacific Journal of Management, 27(4): 727-749.

Sun Jingshui, Sun Jinxiu.2005. Empirical study of

supervisory board and corporate performance of listed

companies in china(in Chinese). Statistics and

Decision, (2): 64-65.

Liu Shanmin. 2008. Empirical research between

independence and oversight functions of supervisory

board (in Chinese). Macroeconomics, (8): 48-52.

Li Lijun,Jin Yuna. 2010. Quartet control checks and

balances, free cash flow and over-investment (in

Chinese).Management Review, 22(2): 103-108.

Hu Haichuan, Zhang Xinling. 2013. Relation of corporate

governance and information disclosure quality (in

Chinese).Statistics and Decision, (22): 182-185.

Firth M, Fung P M Y, Rui O M. 2007. Ownership, two-tier

board structure, and the informativeness of earnings–

Research on the Effectiveness of Financial Supervision of the Supervisory Board

425

Research on the Effectiveness of Financial Supervision of the Supervisory Board

425

Evidence from China[J]. Journal of accounting and

public policy, 26(4): 463-496.

Li Weian, Hao Chen. 2006. Empirical Study of Chinese

Listed Company Supervisory Board Governance(in

Chinese).journal of Shanghai University of Finance

and Economics, 8(3): 78-84.

Wang Shuhu,Tong Ning,Zhou Zhao.2009. Empirical

research of supervisory board governance of listed

companies(in Chinese). Journal of Hebei University,

(4): 61-65.

Dechow P M, Sloan R G, Sweeney A P.1996. Causes and

consequences of earnings manipulation: An analysis

of firms subject to enforcement actions by the sec.

Contemporary accounting research, 13(1): 1-36.

ISME 2015 - Information Science and Management Engineering III

426

ISME 2015 - International Conference on Information System and Management Engineering

426