Framework to Efficiently Measure Firm Smart Business Performance

in a Global Management Environment

Chui Young Yoon

Department of IT Applied-Convergence, Korea National University of Transportation,

61 Deahak-ro, Jeungpyeong-gun, Chungbuk, South Korea

Keywords: Smart Business, Smart Business Performance, Measurement Factors and Items, Structural Framework.

Abstract: Many firms have implemented their smart business capabilities to efficiently perform management activities

and improve the performance of business tasks in a smart management environment. Firms have applied their

smart business capabilities to management activities in order to raise the performance of business execution

in a global management environment. That is, the measurement and management for the performance of a

firm’s smart business execution need to efficiently build and improve the smart business capability

appropriate for its management strategy and business departments. Hence, a measurement framework is

necessary for efficiently measuring a firm’s smart business performance in order to manage and improve its

smart management capability. The validity and reliability of the developed framework are verified by factor

analysis and reliability analysis based on previous studies. We find a 10-item framework that can reasonably

measure a firm smart business performance in a total performance perspective.

1 INTRODUCTION

Most enterprises perform their management activities

and business tasks with partially and fully utilizing

smart device, network, solutions and systems in a

smart business environment (Busquets, Rodon, and

Wareham, 2009; Chang, Chen, and Zhou, 2009; Heck

and Vervest, 2009; Hilty, Aebischer, and Rizzoli,

2014). Smart business technology is an important

means to improve and preserve a firm’s task

performance in the ever-changing business

environment. Firm smart business capability needs to

increase its business performance in a smart

management environment (Yoon, 2014). Firm smart

business capability needs to increase its business

performance in a smart management environment

(Yoon, 2014). Its smart business performance has to

be measured by a scientific and practical tool in order

to efficiently build and improve a smart business

capability appropriate for the management activities

and business tasks. Enterprise smart business

capability should be improved by objective criteria

based on the analysis results of its smart business

performance in a comprehensive performance

perspective. Enterprise smart business performance

means the business results that a firm performs its

management and business activities based on its

smart business capability in a smart business

perspective. But a comprehensive and practical tool

to measure a firm smart business performance has not

been studied in previous studies. Namely, we need a

measurement framework that can effectively gauge a

firm smart business performance in terms of its entire

smart business performance.

Therefore, this study provides a measurement

framework that can efficiently gauge a firm smart

business performance to effectively build its smart

business capability and improving its smart business

performance in terms of a total smart business

performance.

2 RELATED RESEARCH

Previous literature has considered smart business as

the critical factor to efficiently improve a firm’s

business performance and competitiveness, and to

effectively prepare for a future business environment

with progress of smart technology (Yoon, 2014).

Smart business can be defined as an approach to

increase the competitiveness of organizations by

improving management activities through using

smart technology such as smart devices, networks,

and solutions environment (Busquets, Rodon, and

Yoon, C.

Framework to Efficiently Measure Firm Smart Business Performance in a Global Management Environment.

In Proceedings of the 18th International Conference on Enterprise Information Systems (ICEIS 2016) - Volume 2, pages 625-629

ISBN: 978-989-758-187-8

Copyright

c

2016 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

625

Wareham, 2009; Chang, Chen, and Zhou, 2009; Heck

and Vervest, 2009; Hilty, Aebischer, and Rizzoli,

2014). Smart business can be described as a business

process that uses the smart technology medium as a

conduit to fulfil business transactions (Yoon, 2014).

Hence, smart business (SB) can be defined as an

approach to efficiently perform the firm’s

management activities by applying the smart

technology and solutions, and systems to its business

tasks and management activities in a global business

environment.

Literature on enterprise performance provides a

variety of perspectives (Bi and Zhang, 2008; Hu and

Xiang, 2008; Jiao, Chang, and Lu, 2008; Liao and

Chuang, 2006; Liu and Feng, 2008; Mei and Nie,

2007; Sun, Ding, and Gu, 2008; Tseng, Chiu, and

Chen, 2009). The firm performance includes three

factors such as improving client satisfaction,

enhancing organizational competitiveness, and

enhancing organizational image (Sun, Ding, and Gu,

2008). These studies focused on financial and non-

financial perspectives. In financial research, the

measurement of firm performance was studied in

terms of sale growth, earning growth, market share,

return on assets (ROA), return on sales (ROS), and

market value (Liu and Feng, 2008). In non-financial

research, a firm’s performance was measured by

efficiency, effectiveness, profitability, quality of

service, client satisfaction, and productivity (Bi and

Zhang, 2008; Hu and Xiang, 2008; Jiao, Chang, and

Lu, 2008; Liao and Chuang, 2006; Liu and Feng,

2008; Mei and Nie, 2007; Sun, Ding, and Gu, 2008).

This is their satisfaction level about their firm’s

performance in terms of growth in sale, growth in

profits, and growth in market share (Mei and Nie,

2007). By exploring these studies, this research

describes enterprise performance as the effectiveness

and efficiency of its management activities that are

improved by utilizing enterprise IT capability for its

management activities. Firm smart business

performance is able to transform enterprise

performance into a type of enterprise performance

based on a smart business performance perspective.

Hence, firm smart business performance (FSBP)

can be defined as the performance that a firm can

obtain with applying the smart business capability to

its management activities and business tasks in a

global management environment. Namely, FSBP

means a total smart business performance that a firm

can get from applying its smart business capability to

its management activities and business tasks in a

smart management environment.

Based on these previous literature, we extract the

analysis factors and items to measure firm

performance in a smart business perspective as

follows: operation performance (efficiency of

business process, inventory turnover and accounts,

quality of services, and client satisfaction), growth

performance (sale revenue growth, market growth,

market value, and return on sale), profitability

performance (sale gross and profit margin, net

income growth, growth in profits, and cash turnover

ratio), and competitiveness performance (sale growth

rate, capital structure, market share, number of

patents, customer share, and R&D expenditure ratio)

(Bi and Zhang, 2008; Hu and Xiang, 2008; Liao and

Chuang, 2006; Liu and Feng, 2008; Mei and Nie,

2007; Sun, Ding, and Gu, 2008; Tseng, Chiu, and

Chen, 2009). We use these items as measures with

which to gauge the FSBP through the verification

process of a validity and reliability analysis.

3 METHODS

This study initially generated 19 measurement items

for FSBP based on definitions and components of

enterprise performance (Bi and Zhang, 2008; Hu and

Xiang, 2008; Jiao, Chang, and Lu, 2008; Liao and

Chuang, 2006; Liu and Feng, 2008; Mei and Nie,

2007; Sun, Ding, and Gu, 2008; Tseng, Chiu, and

Chen, 2009). We analyzed the construct validity of

the refined items to ensure that FSBP is efficiently

measured by the items. The construct validity of the

model was researched by many researchers. These

studies presented two methods of model construct

validation: (1) correlations between total scores and

item scores, and (2) factor analysis (Etezadi-Amoli

and Farhoodmand, 1996; Mei and Nie, 2007;

Torkzadeh and Doll, 1999; Torkzadeh and Lee, 2003).

Etezadi-Amoli and Farhoodmand (1996) used factor

analysis to verify the validity of the measurement tool

construct. Torkzadeh and Doll (1999) and Torkzadeh

and Lee (2003) used correlation analysis to verify the

validity of the measurement tool construct. This study

is likely to verify the validity of the analysis tool

construct and the extraction of adequate analysis

items by factor analysis and reliability analysis. The

ratio of sample size to number of measurement items

(11:1) was above the minimum (10:1) ratio suggested

for factor analysis (Etezadi-Amoli and Farhoodmand,

1996; Torkzadeh and Doll, 1999; Torkzadeh and Lee,

2003). The analysis questionnaire used a five-point

Likert-type scale; where, 1: not at all; 2: a little; 3:

moderate; 4: good; 5: very good. The survey was

gathered data from a variety of industries, business

departments, experience, and education. We

performed two kinds of survey methods: direct

ICEIS 2016 - 18th International Conference on Enterprise Information Systems

626

collection and e-mail. The respondents either directly

mailed back the completed questionnaires or research

assistants collected them 2-3 weeks later. The

collected questionnaires represented 41 % of the

respondents.

3.1 Sample Characteristics

This research collected a sample of 166 usable

responses obtained from a variety of industries and

business departments. We excluded nine incomplete

or ambiguous questionnaires, leaving 157 usable

questionnaires for statistical analysis. The

respondents in terms of business departments were

identified as strategy planning (16.6%), development

and maintenance (16.0%), business application

(36.9%), and administration support (30.5%). The

respondent had on average of 9.6 years of experience

(S.D. =1.018) in their field, their average age was

34.9 years old (S.D. =5.168), and their gender, male

(70.7%) and female (29.3%). This survey was

intentionally focused on various industries and

persons working above the 10 years within their firms.

Namely, the respondents could efficiently provide the

correct responses for our questionnaire survey.

3.2 Analysis and Discussion

After factor analysis and reliability analysis, the first

19 measurement items were reduced to 10 items, with

9 items were deleted, with applying the criterion of

previous studies (Etezadi-Amoli and Farhoodmand,

1996; Torkzadeh and Doll, 1999; Torkzadeh and Lee,

2003). The elimination was sufficiently considered to

ensure that the retained items were adequate analysis

items of FSBP. The validity and reliability of the

developed framework were also verified through

factor analysis and reliability analysis. They were

used to identify the underlying factors or components

that comprise the FSBP construct. Each of the 10

items had a factor loading > 0.634. The reliability

coefficients (Cronbach’s alpha) of four potential

factors had values > 0.801 as indicated in Table 1,

above the threshold recommended for exploratory

research (Etezadi-Amoli and Farhoodmand, 1996;

Torkzadeh and Doll, 1999; Torkzadeh and Lee,

2003). This research calculated the corrected item-

total correlations between each variable and its

corresponding factor in order to investigating the

reliability and validity of the measurement items.

These correlations along with alpha coefficients of

each factor are presented in Table 1.

Table 1: Reliability, validity, and factor loadings of FSBP

construct.

These coefficients indicate the relative contribution

of a measurement item to the construction of a scale

for gauging a particular factor. Most corrected item-

total correlations were greater than 0.602, showing

that the measurement items are good indicators of

their corresponding factors. The extracted items have

a validity and reliability in terms of an analysis

construct based on the analysis results as presented in

Table 1. These results may be successfully achieved

by accumulating many research findings and case

studies. Through reflecting the analysis results of case

studies, the developed analysis tool can be became

more objective and practical scale in the application

of industrial fields.

4 MEASUREMENT

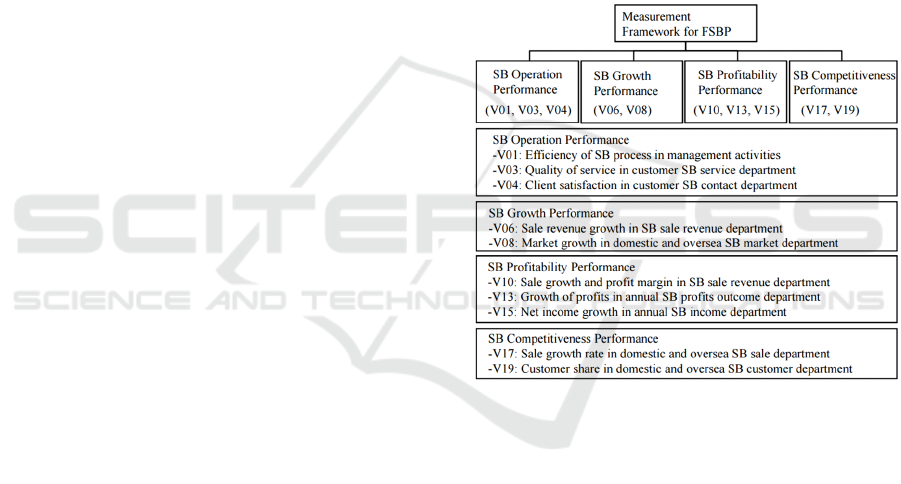

FRAMEWORK OF FSBP

We provided the 10 measurement items appropriate

for measuring FSBP. This research classified four

factor groups from the factor analysis. The factor

groups indicate the potential factors as major

measurement components to gauge FSBP. By

exploring the measurement items of each factor group,

we identified the following four potential factors:

factor 1: SB operation performance; factor 2: SB

growth performance; factor 3: SB profitability

performance; and factor 4: SB competitiveness

performance. These factors comprise the overall

measurement content for FSBP from SB operation

performance to SB competitiveness performance.

The potential 4 analysis factors are used as the 4 core

measurement factors of our framework construct. The

meanings and measurement items of each factor are

as follows. SB operation performance represents the

Va ri ab l e

Factor Loading

Corrected

Item-Total

Correlation

Coefficients

Alpha

Factor 1 Factor 2 Factor 3 Factor 4

V01 0.771 0.679

0.815V03 0.794 0.731

V04 0.665 0.637

V06 0.802 0.733

0.833

V08 0.826 0.636

V10 0.801 0.725

0.837V13 0.836 0.641

V15 0.711 0.612

V17 0.796 0.659

0.801

V19 0.634 0.602

Framework to Efficiently Measure Firm Smart Business Performance in a Global Management Environment

627

efficiency and effectiveness improved by applying

the firm smart business capability to its management

activities in a firm operation perspective. That is, the

operation performance indicates the result that a firm

obtains from its smart management activities in terms

of business execution. It includes efficiency of

business process, quality of service, and client

satisfaction in firm management activities. SB growth

performance presents the efficiency and effectiveness

raised by applying the firm smart business capability

to its management activities in a firm growth

perspective. It comprises sale revenue growth and

market growth. SB profitability performance means

the efficiency and effectiveness improved by

applying the firm smart business capability to its

management activities in an enterprise profit

perspective. It has sale gross and profit margin,

growth in profits, and net income growth. And, SB

competitiveness performance refers to the efficiency

and effectiveness increasing by utilizing the firm

smart business capability for its management

activities. Namely, SB competitiveness performance

means the total smart business performance of an

enterprise in a competitiveness perspective. It

contains sale growth rate and market share. Our

findings provide a structural framework that can

efficiently measure FSBP in terms of a total smart

business performance from SB operation

performance to SB competitiveness performance,

including 4 measurement factors and 10 items. This

framework includes four measurement factors such as

SB operation performance, SB growth performance,

SB profitability performance, and SB

competitiveness performance (Fig. 1). Each factor

has two or three measurement items. As indicated in

Table 1 and Fig.1, SB operation performance has the

analysis items, such as V01, V03, and V04. SB

growth performance includes V06 and V08. SB

profitability performance contains V10, V13, and

V15. SB competitiveness performance comprises

V17 and V19. These factors affect FSBP, that is, the

total FSBP of a firm. It is important to improve and

manage FSBP by measuring a firm’s SB performance

with a valid and reliable instrument. Using this

framework can facilitate efficiently raising a firm’s

SB performance. Measuring FSBP is a critical

method to investigate the total smart business

performance of an enterprise, based on its SB

operation performance, SB growth performance, SB

profitability performance, and SB competitiveness

performance. Hence, the developed framework for

FSBP consists of 4 measurement factors and 10 items

verified by the previous analysis results as shown in

Figure 1. The developed framework is an important

theoretical construct to efficiently measure the total

smart business performance that a firm can obtains by

utilizing its smart business capability for its

management activities in a smart management

environment.

Hence, understanding the FSBP construct is

essential to measure the success of FSBP that denotes

the total SB performance to efficiently support its

management activities. We can use the structural

framework to measure FSBP across different

industrial fields and business departments, and

perhaps even as a global measure. Therefore, the

developed framework is an important theoretical

construct to efficiently gauge the total SB

performance that a firm can obtains by utilizing its SB

capability for its management activities in a global

management environment.

Figure 1: The developed measurement framework

construct.

5 CONCLUSIONS

This study provides a structural framework that can

measure perceived FSBP from a total smart business

performance perspective. This 10-item scale

framework is implicative, concrete, easy to use, and

appropriate for practical and research purposes. We

also have some limitations in terms of a specific

FSBP perspective. This problem can be solved by

many comparative and cumulative research findings.

The developed framework with adequate validity and

reliability provides groundwork for the development

of a standard framework of FSBP.

Therefore, this study presents a structural

framework that can efficiently measure FSBP that a

ICEIS 2016 - 18th International Conference on Enterprise Information Systems

628

firm can obtain by applying a firm smart business

capability to its management activities and business

tasks in a global management environment. In future

research, we will find the practicality and availability

of the developed framework with providing the

measurement results by applying it to many case

studies.

ACKNOWLEDGEMENTS

This research was supported by Basic Science

Research Program through the National Research

Foundation of Korea (NRF) funded by the Ministry

of Education, Science and Technology (NO:

2013R1A1A2012350).

REFERENCES

Bi, X., Zhang, H., 2008. An Empirical Research on

Relationship between Information Technology

Capability and Firm Performance: the Evidence from

Listed Companies and Information Power 500 in China.

Proceedings of 2008 International Conference on

Computer Science and Software Engineering. 540-544.

Busquets, J., Rodon, J., Wareham, J., 2009. Adaptability in

smart business networks: An exploratory case in the

insurance industry. Decision Support Systems. 47, 287-

296.

Chang, Y. F., Chen, C. S., Zhou, H., 2009. Smart phone for

mobile commerce. Computer Standards & Interface. 31,

740-747.

Etezadi-Amoli, J., Farhoomand, A. F., 1996. A Structural

Model of End User Information Satisfaction and User

Performance. Information & Management. 30, 65-73.

Heck, E. V. and Vervest, P., 2009. Smart business networks:

Concepts and empirical evidence. Decision Support

Systems. 47, 275-276.

Hilty, L. M., Aebischer, B., Rizzoli, A., 2014. Modeling

and evaluating the sustainability of smart solutions.

Environmental Modeling & Software. 56, 1-5.

Hu, B., Xiang, Y., 2008. An Empirical Study of Effects of

Information Systems Resources. Proceedings of 2008

International Seminar on Future Information

Technology and Management Engineering. 335-338.

Jiao, H., Chang, C., Lu, Y., 2008. The Relationship on

Information Technology Capability and Performance:

An Empirical Research in the Context of China’s

Yangtze River Delta Region. Proceedings of the IEEE

International Conference on Industrial Engineering

and Engineering Management. 872-876.

Jiang, J., Zhang, J., 2008. Strategic Co-operative E & D and

Firm Performance in Emerging B2B E-Commerce.

Proceedings of the IEEE International Conference on

e-Business Engineering. 537-542.

Liao, C., Chuang, S. H., 2006. Exploring the Role of

Knowledge Management for Enhancing Firm’s

Innovation and Performance. Proceedings of the 39th

Hawaii International Conference on System Sciences.

7, 158a-167a.

Liu, Z. Q., Feng, Y. J., 2008. An Analysis of Diversification

and Firm Performance. Proceedings of the 15th

International Conference on Management Science &

Engineering. 456-461.

Mckeen, J. D., Zack, M. H., Singh, S., 2006. Knowledge

Management and Organizational Performance: An

Exploratory Survey. Proceedings of the 39th Annual

Hawaii International Conference on System Sciences.

1-9.

Mei, S., Nie, M., 2007. Technology Capability, Marketing

Capability and Network Capability: Keys to Enhancing

Competitiveness and Improving Performance.

Proceedings of the 14th International Conference on

Management Science & Engineering. 728-733.

Sherif, K., Hoffman, J., Thomas, B., 2006. Can technology

build organizational social capital? The case of a global

IT consulting firm. Information & Management. 43(7),

795-804.

Sun, J., Ding, L., Gu, X., 2008. Empirical Study on Impact

of Information Technology on Construction Firm

Performance. Proceedings of 2008 International

Conference on Information Management, Innovation

Management and Industrial Engineering. 54-57.

Tippins, M. J., Sohi, R. S., 2003. IT Competency and Firm

Performance: Is Organizational Learning a Missing

Link. Strategic Management Journal. 24, 745-761.

Torkzadeh, G., Doll, W. J., 1999. The Development of a

Tool for Measuring the Perceived Impact of

Information Technology on Work. Omega,

International Journal of Measurement Science. 27,

327-339.

Torkzadeh, G., Lee, J. W., 2003. Measures of Perceived

End-user’s Information Skills. Information &

Management. 40, 607-615.

Tseng, F. M., Chiu, Y. J., Chen, J. S., 2009. Measuring

business performance in the high-tech manufacturing

industry: A case study of Taiwan’s large-sized TFT-

LCD panel companies. The International Journal of

Management Science. 37, 686-697.

Yoon, C. Y., 2014. A Structural Tool to Efficiently Analyze

Enterprise Smart Business Capability in a total Smart

Business Capability Perspective. iNFORMATION An

International Interdisciplinary Journal. 17(11-A),

5607-5618.

Framework to Efficiently Measure Firm Smart Business Performance in a Global Management Environment

629