Attack Tree for Modelling Unauthorized EMV Card Transactions at

POS Terminals

Dilpreet Singh, Ron Ruhl and Hamman Samuel

Information System Security and Management Department,

Concordia University College of Alberta, 7128 Ada Blvd NW, Edmonton, AB, Canada

Keywords: EMV, EMV Transaction Process, Attack, Attack Tree Methodology, Point of Sale Terminal, PCIDSS.

Abstract: Europay, MasterCard and Visa (EMV) is a dominant protocol used for smart card payments worldwide,

with over 730 million cards in circulation. One goal of the EMV protocol is to secure debit and credit

transactions at a point-of-sale (POS) terminal, but still there are vulnerabilities, which can lead to

unauthorized disclosure of cardholder data. This research paper will provide the reader with a single

document listing the vulnerabilities leading to various possible attacks against EMV payment card

transaction process at a POS terminal. Attack tree methodology will be used to document these

vulnerabilities. This research will also provide the countermeasures against various possible attacks.

1 INTRODUCTION

For 25 years, EMV has implemented payment cards

which initially used a magnetic stripe only but now

contain a chip microprocessor which processes

payments at POS devices. This research examines

when the card is present at a POS terminal and will

use attack tree methodology to describe the security

of dynamic data authentication and combined data

authentication (DDA/CDA) EMV cards.

2 EMV TRANSACTION PROCESS

EMV developed common protocol standards

(Murdoch et al., 2010) which are published at

emvco.com. General core requirements are also

augmented by card specific standards of each party.

The EMV card issuing bank is responsible for sele-

cting specific subsets including authentication and

risk management. The EMV transaction process can

be categorized into three phases: card authentication,

card verification and transaction authorization.

2.1 Card Authentication

The card authentication assures the card and the card

issuer authenticity to the terminal. Card authentica-

tion involves a sequence of sub-steps.

2.1.1 Application Selection

EMV cards may contain multiple applications

(Debit/Credit/ATM) and files supporting the

applications. On inserting the EMV card into the

POS terminal, the terminal requests to read the EMV

file “1PAY.SYS.DDF01” listing the applications

that the chip card contains. After successful

application selection, the card sends the Processing

Options Data Object List (PDOL) to the terminal.

This lists the data elements that the card will require

from the terminal to execute the next commands in

the process. If high priority application selection

fails, the terminal switches to the next priority

application.

2.1.2 Read Application Data

After application selection, the terminal need to

know the functionalities supported by the EMV card

and the location of the information related to these

functionalities. The terminal then issues, the Get

Processing Options (GPO) command. In response,

the card issues the Application Interchange Profile

(AIP) and the Application File Locator (AFL). AIP

indicates the functions that the card supports while

AFL is a list of application data records for the

supported functions by the card. These records

contain cardholder information (e.g. primary account

number, start and expiry date) which can be read by

494

Singh, D., Ruhl, R. and Samuel, H.

Attack Tree for Modelling Unauthorized EMV Card Transactions at POS Terminals.

DOI: 10.5220/0006723304940502

In Proceedings of the 4th International Conference on Information Systems Security and Privacy (ICISSP 2018), pages 494-502

ISBN: 978-989-758-282-0

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

the terminal using the read record command

(Murdoch et al., 2010). These records have RSA digi-

tal signatures linked with a certificate authority (CA)

known to the terminal. Depending upon the variant of

the EMV, RSA crypto-graphic operations can be

performed. Both DDA and CDA cards contain RSA

private keys specific to the customer’s card intended

for use for asymmetric cryptographic operations such

as digital signatures and encryption. The certificate

for DDA and CDA public keys is created for the card

and this is chained to the issuing bank and a CA. The

CA public key is stored on all POS terminals.

2.1.3 Data Authentication

EMV specification for DDA and CDA is defined

below (EMV,2008):

• DDA uses asymmetric cryptography to

create a card-specific public-private key

pair assigned to the card. The private key is

securely stored and inaccessible to the

terminal. The DDA certificate with the card

public key is verified using challenge

response (Breekel et al.,2016).

• CDA authenticates the transaction and the

card by Message Authentication Code

(MAC) with a key that the bank knows.

The type of data authentication method depends

upon the terminal and the card capabilities.

2.1.4 Processing Restrictions

The terminal determines application compatibility

supported by the card and the terminal. It involves

matching the application version number, checking

the type of allowed transactions, card validity and

application validity and the current transactions

allowed by the Application Usage Control (AUC).

2.2 Cardholder Verification

Cardholder verification uses the CVM list which

specifies the card`s policy and when to use

encrypted PIN, plaintext PIN, signature or No-CVM.

It also specifies the steps to be taken if the

verification fails (Murdoch et al.,2010). Most

transactions today are PIN verified.

DDA and CDA cards send a PIN from the

terminal to the chip encrypted with the public key of

the card. The PIN verification process could be

either ‘offline’ or ‘online’. In offline PIN

verification, the cardholder enters the PIN in the PIN

Entry Device (PED) which is sent to the card

(encrypted or unencrypted) (Murdoch et al.,2010). In

case of “Offline Encrypted PIN” the chip transforms

the PIN one-way according to the issuing banks

specifications and then compares the result with the

one which was previously stored on the card using

the same one-way process. Based on the terminal

capability it might send the “Offline Plain-text PIN”

to the card which is not a secure way of

communication thus making it susceptible to attacks.

If the PIN matches, the transaction is processed

further. If not correct, the PED asks for the PIN

again (unless the retry counter stored on the EMV

chip has reached its maximum). In “Online PIN” at

an ATM the PIN is sent directly to the issuer over

the payment network. Although most transactions

are PIN verified, there are still terminals that do not

have PIN entry devices and only accept magnetic

stripe. In United Kingdom (UK) there exists a type

of EMV card known as “Chip and Signature” card,

which does not support PIN verification (Murdoch et

al.,2010). These cards are issued to visually

impaired customers or who have memory loss.

Unsigned CVM lists allow someone to modify

the list and downgrade the card from one that

requires a PIN verification to `signature` or

`nothing` (i.e. no authentication at all).

2.3 Transaction Authorization

After successful cardholder verification, the terminal

requests the card to generate a MAC over the

transaction details which will be sent to the issuing

bank (Murdoch et al., 2010). The transaction

authorization can either be offline or online

depending upon the card and terminal compatibility.

2.3.1 Terminal Risk Management

Terminal risk management is to safeguard the

payment system against fraud. The risk of fraud can

be reduced by online authorizing the transaction.

Whether a transaction should be authorized online or

offline depends mainly on three factors: offline floor

limit; random selection of the transaction to be

processed online; and lastly, if the card has not

undergone an online transaction in a long time.

2.3.2 Terminal Action Analysis

In this step, the terminal makes the decision whether

to online or offline authorize or to decline the

transaction. For this, the terminal analyses the

previous verification and authentication results.

Irrespective of the terminal decision, it must request

confirmation from the card and uses a Generate

Application Cryptogram (generate AC) command.

Attack Tree for Modelling Unauthorized EMV Card Transactions at POS Terminals

495

2.3.3 Card Action Analysis

This step is the same as terminal action analysis. The

difference is that the card makes the decision to

authorize the transaction online or offline or to decline

the transaction. The card may perform its own risk

management (for example, in a Near Field

Communication or NFC “tapped” transaction the risk

limit for tapped transactions is held on the card). The

card decision of authorising the transaction may differ

from the terminal but is subjected to certain logic

rules (e.g. the card is not permitted to request offline

acceptance if the terminal proposed online autho-

rization). The card communicates its decision to the

terminal using a cryptogram. The card will then gene-

rate: transaction approved (Transaction Certificate -

TC); request online approval (Authorization Request

Cryptogram - ARQC); or, transaction declined

(Application Authentication Cryptogram - AAC).

2.3.4 Offline/Online Decision

If the terminal receives a TC or AAC that means the

transaction is completed with an offline authorized

or offline declined. But if the terminal received an

ARQC that means the transaction needs to be online

authorized and the transaction authorization request

is sent to the issuer. The cryptogram sent to the bank

includes a type code, a sequence counter identifying

the transaction (ATC – application transaction

counter), a variable length field containing data

generated by the issuer application, and a MAC,

which is calculated over the rest of the message

including a description of the transaction (Murdoch

et al.,2010). The MAC is computed, typically using

3DES, with a symmetric key shared between the

card and the issuing bank (Murdoch et al.,2010). The

issuing bank performs several checks and then

returns a ARC (authorization response code),

indicating how the transaction should proceed and

places this in an ARPC (authorization response

cryptogram) (Murdoch et al.,2010). The card

validates the computed MAC contained with ARPC

and if successful it means the issuer authorized the

transaction (Murdoch et al.,2010). Now the card

issues a TC that the terminal sends to the issuing

bank and stores a copy of it for record purposes.

2.4 Transaction Completion

In offline transaction approval, the card generated

TC is sent to the issuer right away or later as a part

of the transaction settlement process. If the

transaction is approved or declined online the

terminal will request a final transaction cryptogram

using the Generate AC command. After the final

card processing the card can be removed from the

terminal. An EMV card transaction can be made

contactless if the POS allows. For contactless

payments, the card needs to be in range of the

terminal so that information exchange takes place.

For contact type cards, the card needs to be inserted

in the terminal. Contactless EMV card transactions

have a similar transaction process with a few

exceptions in the protocol as follows:

• EMV contactless transaction have two

modes: EMV mode and Mag-Stripe mode.

• Contactless involves only one cryptogram

exchange and not two.

• A new CVM method is added known as

consumer device CVM. It applies when the

contactless transaction uses a NFC phone

(Breekel et al.,2016).

Contactless transactions start with the terminal

choosing the high priority application from the list

specified in the Proximity Payment System included

in the 1PAY.SYS.DDF01 (Breekel et al.,2016).

Then the terminal specifies the mode of operation.

Mag-stripe mode is often in older infrastructure

where the terminal cannot process chip data nor

authenticate static data on the card (Breekel et

al.,2016). Instead of the normal GENERATE AC

command it uses the COMPUTE

CRYPTOGRAPHIC CHECKSUM command and an

Unpredictable Number is included as a parameter

(Breekel et al.,2016). For EMV mode a new CVM

called on-device cardholder verification is used. If

both terminal and card have high priority for this

CVM method, the transaction is performed with this

CVM (Breekel et al.,2016). The terminal then passes

the argument that offline plain text PIN is used and

how the device verifies the cardholder identity is not

specified. The rest of the transaction process flow is

like the contact transaction process flow. In

contactless transaction, there is only one cryptogram

involved so it has a different meaning from the

contact transaction described above:

• Contact EMV transactions generated TC

indicates the offline or online transaction

approval, whereas for contactless

transactions it indicates offline approval.

• A generated ARQC in a contactless

transaction is not followed by a TC or

AAC. This indicates that the card or

terminal requires issuer authorization for

the transaction (Breekel et al.,2016).

• If a transaction is declined, an AAC is

generated just like contact transactions.

ICISSP 2018 - 4th International Conference on Information Systems Security and Privacy

496

3 PCI DSS STANDARD

OVERVIEW

The Payment Card Industry Data Security Standard

(PCI DSS) sets the technical and operational

requirements for merchants to protect cardholder

data. This standard applies to any entity that stores,

transmits or processes cardholder data and the

standard is enforced by EMV. The important PCI

DSS goals related to this research are: Protect

cardholder data; and Implement strong access

control measures. The detailed document is available

online (PCI DSS quick reference guide, 2009).

4 THE ATTACKS

The various types of attacks possible on DDA/CDA

EMV cards, but not limited to, are given below:

4.1 Man-in-the-middle Attack (MITM)

The central fault in the EMV protocol is that the PIN

verification step is never clearly authenticated

(Murdoch et al.,2010). A man-in-the-middle device

can easily perform this attack if it can intercept and

modify the communication between card and

terminal. This attack makes the terminal believe that

PIN verification took place and was successful

whereas it makes the card believe PIN verification

was not attempted and another mechanism (e.g.

signature) was used. The entered dummy PIN never

gets to the card and therefore the PIN retry counter

on the card is not changed. If the transaction is

processed offline there is less ability to detect the

attack as the issuer will not be contacted during the

transaction process. If the transaction is processed

online, the man-in-the-middle can change the

cryptogram type thus turning an ARQC or AAC into

a TC (Murdoch et al.,2010). This may cause

cryptogram verification to fail and by the time it will

be detected the attacker would have left the POS.

This attack execution has been demonstrated on

live terminals (Murdoch et al.,2010). The illustration

shows that the man-in-middle circuit has a fake card

that will be inserted into the legitimate terminal. The

fake card is connected to an interface chip ($2

Maxim 1740 [8]) through thin wires used for voltage

shifting (Murdoch et al.,2010). This is connected to

a FPGA board ($189 Spartan-3E Starter Kit [9]) that

converts between the card and PC interface. FPGA

is then connected to a laptop through a serial link

which is then connected to smart card reader from

Alcor Micro (11) in which the stolen genuine card is

inserted (Murdoch et al.,2010). A python script

running on a laptop relays the transaction while

waiting for the verify command being sent by the

terminal (Murdoch et al.,2010). It then suppresses it

to the card and responds with a verify command

(Murdoch et al.,2010). The rest of the

communication is unchanged. The attack could be

easily miniaturised.

The cardholder could prevent this attack if the

cardholder were notified after every transaction the

card makes. The cardholder would deactivate the

stolen card if unauthorized transactions occurred.

Merchants could prevent this attack by giving proper

training to their employees. In addition, the bank

could prevent the attack by digitally signing the

CVM list so that the attacker cannot modify them.

4.2 Pre-play Attack (PPA)

Michael Roland and Josef Langer demonstrated an

attack scenario to forge the magnetic stripe

information for contactless payment cards using

skimming. This PPA is used to obtain dynamic card

verification codes (CVC) required for authorising

payments. They further described a weakness in

credit cards by downgrading its CVM list to

magnetic stripe mode. Mike Bond et al. (2014)

demonstrated a type of PPA where he predicted the

unpredictable number (UN) for the automated teller

machine (ATM) but for this attack the target is

limited to an EMV contactless protocol in mag-

stripe mode. The limit of the attack is the maximum

amount that can be authorized with a contactless

card transaction (Vila and Rodrıguez). There are

four kernel specification (1,2,3,4) variants for the

EMV contactless payment systems (Vila and

Rodrıguez). For this attack scenario, Kernel 2

specifications were used in that the protocol interacts

with payment cards supporting the MasterCard Pay

Pass or similar cards. In the mag-stripe

implementation, the UN used in the COMPUTE

CRYPTOGRAPHIC CHECKSUM command is

weakened by the protocol design itself. The UN is a

4-byte value limited by a BCD-encoding numeric

value in the kernel 2 specification in which UN

ranges from 0 to 99,999,999. In the magnetic stripe

protocol, the UN is reduced to 0 to 999. This set of

UN was predicted in a minute using the Android

App running on a Google Galaxy Nexus S (Vila and

Rodrıguez). An attacker communicating for one

minute with the EMV mag-stripe card can generate

enough information required for a successful

payment transaction. The CVC is obtained using the

Attack Tree for Modelling Unauthorized EMV Card Transactions at POS Terminals

497

UN, the card secret key and Application Transaction

Counter (ATC). The ATC increases for each EMV

transaction which prevents against replay attacks.

However, an attacker can use only one ATC+ CVC

set per transaction. The attacker overwrites AIP

clearing the flag containing EMV mode

downgrading it to mag-stripe. Mag-stripe mode data

returned in GET PROCESSING OPTIONS is not

authenticated. With this data, the attacker can create

a functional contactless clone with pre-played data.

To demonstrate a successful combined pre-play

attack and downgrade to mag-stripe attack scenario,

the system involves a Java card application and an

Android app. The Android app running on Galaxy

Nexus is used to collect mag-stripe data and pre-play

data from a genuine card through its contactless

interface which later can be transferred to a Java

card with the same application.

The simplest fix against this attack is a

cryptographically secure random number generator.

The cardholder could also prevent this attack by

placing the card in an aluminum box. Banks could

prevent this by digitally signing the CVM list so the

attacker cannot modify the list.

4.3 NFC Relay Attack

Jose Vila and Ricardo J. Rodrıguez showed

implementation alternatives to achieve relay attacks

in Android devices and to demonstrate practical

implementation of the attacks using NFC-enabled

phones (Kfir and Wool). This attack is a type of

passive relay attack. In this attack, the attacker can

trick the reader into communication with a victim

that is very far away. An attacker can use a pick-

pocket system to use the victim’s contactless card

data without the victim’s knowledge. In near-field

communication (NFC), there are three modes of

operation (i.e. peer-to-peer mode, read/write and

card-emulation mode). In peer-to-peer mode, NFC

devices communicate with each other directly. In

read/write mode, NFC devices communicate with

the NFC tag. In card-emulation mode, the NFC

device emulates as a contactless smartcard (Kfir and

Wool). The NFC relay attack is achieved by: a peer-

peer communication channel; a malicious verifier

(i.e. fake terminal) communicating with the

legitimate contactless payment card; and, a

malicious prover (i.e. fake card) communicating

with the legitimate POS terminal.

The communication is relayed from the

legitimate card to the legitimate terminal without the

cardholder knowing about a malicious verifier and

malicious prover. The limitations of this attack are

that the NFC-enabled device acting as a malicious

verifier must be in read/write mode (Kfir and Wool);

and, the card must be in host-card emulation (HCE)

mode, which is natively supported from Android

KitKat onward (Kfir and Wool).

To successfully perform this attack, two off-the-

shelf Android NFC-enabled mobile devices

executing an Android application were developed

for testing purposes (about 2000 Java Lines of Code

Counter (LOC) and able to act as dishonest

verifier/prover, depending on user’s choice), having

a single constraint: The dishonest prover must

execute, at least, an Android KitKat version (Kfir

and Wool). The POS device used is Ingenico

IWL280. The experiment has been successfully

tested (Kfir and Wool) on several mobile devices,

such as Nexus 4, Nexus 5 as dishonest provers, and

Samsung Galaxy Nexus, Sony Xperia S as dishonest

verifiers (Kfir and Wool).

This attack can be prevented by using a Faraday-

cage approach as well. Another countermeasure is to

control the activation of the card (i.e. the card gets

activated only with the PIN entry by the cardholder).

4.4 Shim-in-the-middle Attack

Shim-in-the-middle attacks involve inserting a thin,

flexible circuit board into the card slot between the

reader and the card chip. A circuit that transmits the

signal to a nearby receiver is hard to detect in the

PED. An attacker can also attach a shim to the card

and insert it into the PED. The shim stays in place in

the machine and the card is removed by the attacker.

A nearby receiver records card details and PINs. The

cardholder PIN can be intercepted if the PIN was

sent in the plain-text (Bond,2006). The intercepted

information related to PINs or accounts enables

counterfeiting magnetic stripes which can be later

used for unauthorised transaction purposes at

terminals accepting magnetic stripe. This attack does

not need employee participation. Therefore, corrupt

merchants prefer it as they can easily deny any

knowledge of the shim existence in their PED.

This attack can be prevented by merchants

obeying to the PCI DSS goals stated earlier. The

cardholder could prevent this attack if they know

how to detect the presence of shimmer in the

terminal. Merchant could also train their employees

and use tamper-resistance terminal to prevent this

attack. POS clerks could also identify modification

to the terminal during daily inspection routine.

ICISSP 2018 - 4th International Conference on Information Systems Security and Privacy

498

4.5 Eavesdrop Attacks

During an EMV transaction process at a POS

terminal, account details or a PIN can be

eavesdropped to forge the magnetic stripe for

fraudulent activates.

4.5.1 Camera and Double-swipe Method

This approach involves a camera facing the PIN pad

and a fraudulent merchant who secretly swipes the

customer’s card through his own device to intercept

information needed to counterfeit the magnetic

stripe. The fraudulent merchant keeps two terminals:

one genuine terminal and one fraud merchant

terminal since modifying a working terminal

requires bypassing a tamper resistant device.

Tampering with the POS is complicated and requires

considerable manual effort (Bond, 2006).

4.5.2 Counterfeit Terminal

This approach constructs a counterfeit terminal

which captures data to forge the magnetic stripe. The

counterfeit terminal may require the cardholder to

enter the PIN which is intercepted using sensors or

software key loggers (Bond, 2006).

4.5.3 Signal Eavesdropping Attack

This attack is used to tap the data line in the PED to

get the unencrypted information required to create a

fake magnetic stripe card. This attack was

demonstrated on two widely deployed PEDs in the

UK (i.e. the Ingenico i3300 and the Dione Xtreme)

(Drimer, Murdoch and Anderson, 2008). Ingenico

PED was defeated easily with a simple ‘tapping

attack’ (due to design flaws in the Ingenico PED).

This PED has a user accessible compartment in its

rear which is not tamper-proof (Drimer, Murdoch

and Anderson, 2008). This compartment leads to

the circuit board and many signals routed at the

bottom layer. The PED’s designers opted to provide

1mm diameter holes and other holes through the

printed circuit board (PCB) (Drimer, Murdoch and

Anderson,2008). The holes are used for positioning

optional surface mount sockets. If the PED has one

of these holes, it can be easily used to tap a metal

hook to a data line. The tap can be placed between

the card chip and the microprocessor. However, in

the given case, this attack was easily achieved using

a bent paperclip placed through the hole (Drimer,

Murdoch and Anderson,2008).

In the Dione Extreme PED there is no concealed

compartment that helps to hide the wiretap but it is

still vulnerable. However, a 4cm needle can be

inserted into a flat ribbon connector socket through a

0.8 mm hole from rear (Drimer, Murdoch and

Anderson, 2008). A thin wire connected to a FPGA

board can translate the data and send it to a laptop

that will show an answer to reset (ATR) initial

exchange intercepted using the tap (Drimer,

Murdoch and Anderson, 2008). In Ingenico PED, a

small FPGA board can easily be inserted into the

compartment without anyone’s knowledge from

where the attacker can easily record transaction

details. In the case of Dione PED, a small FPGA

board can be hidden under the counter and cannot be

easily detected unless the cardholder knows what to

look for (Drimer, Murdoch and Anderson, 2008).

Eavesdropping attacks can be prevented by

merchants complying to the PCI DSS goals “Protect

Cardholder Data and Implement Strong Access

Control Measures” (PCI quick reference

guide,2009). In some of the eavesdrop attacks, the

merchants themselves can be an attacker. To protect

against this, the cardholder should be given tips on

how to detect the modifications in the terminal.

4.6 Fall-back to Magnetic Stripe and

Cross-border Fraud

The weakness that current EMV cards are facing is

fallback to the magnetic stripe whenever the Chip

and PIN is not used. This enables the attackers to

skim a customer`s credit card and record the PIN as

well. An attacker can then create a new card with the

skimmed data and the observed PIN (Anderson,

Bond and Murdoch). This is a widely faced problem

with countries accepting PIN’s along with magnetic

stripe technology for EMV transactions. Thus, an

attacker can use the card stolen from one country in

another country using the magnetic stripe

technology. This attack is an international version of

the fallback to magnetic stripe attack and therefore

known as cross-border fraud.

Encrypted PIN and use of ‘iCVV’ (card verifica-

tion value for integrated circuit cards) is a counter-

measure for fallback to magnetic stripe based attacks.

The previously stored CVV is replaced by iCVV in

the chip cards. When using iCVV during the chip

based transactions the CVV from the magnetic stripe

can be recovered by swiping the card into a separate

reader (Drimer, Murdoch and Anderson, 2008).

4.7 Active Relay Attack

In this attack, a victim initiates the EMV transaction

process with an attacker installed reader which the

Attack Tree for Modelling Unauthorized EMV Card Transactions at POS Terminals

499

victim is unaware of. A victim thinks he is paying a

small amount at the malicious reader but the reader

relays the card response to a remote legitimate

reader to pay for more expensive items

(Mehrnezhad, Hao and Shahandashti, 2017). The

relayed wirelessly communication allows a real POS

purchase. The victim thinks they paid a small

amount but instead they would eventually be billed

for a much larger amount. Since the malicious reader

is not connected to the bank, the victim will never be

charged for the small amount and will show only

one large transaction (Drimer and Murdoch, 2013).

This attack is possible for both contact and

contactless EMV transactions depending on the POS

and the card compatibility.

Attack requirements for this attack include a fake

terminal and a fake card. A FPGA board is used in the

fake terminal (Saar and Murdoch,2013). Two laptops

are needed to relay signals. The FPGA code and PC

software written in python and Verilog requires

programming skills (Drimer and Murdoch, 2013).

This attack can be prevented by either using a

distance-bounding protocol or using a user-interface.

For a user-interface, the customer inserts the card

into an interface and then the interface into the

terminal. If the amount shown on the interface is

satisfactory to the cardholder he/she can carry on

with the transaction. This interface will protect

against magnetic-stripe forging. For distance-

bounding protocol, the card and terminal must

support the protocol (Drimer, Murdoch and

Anderson, 2008).

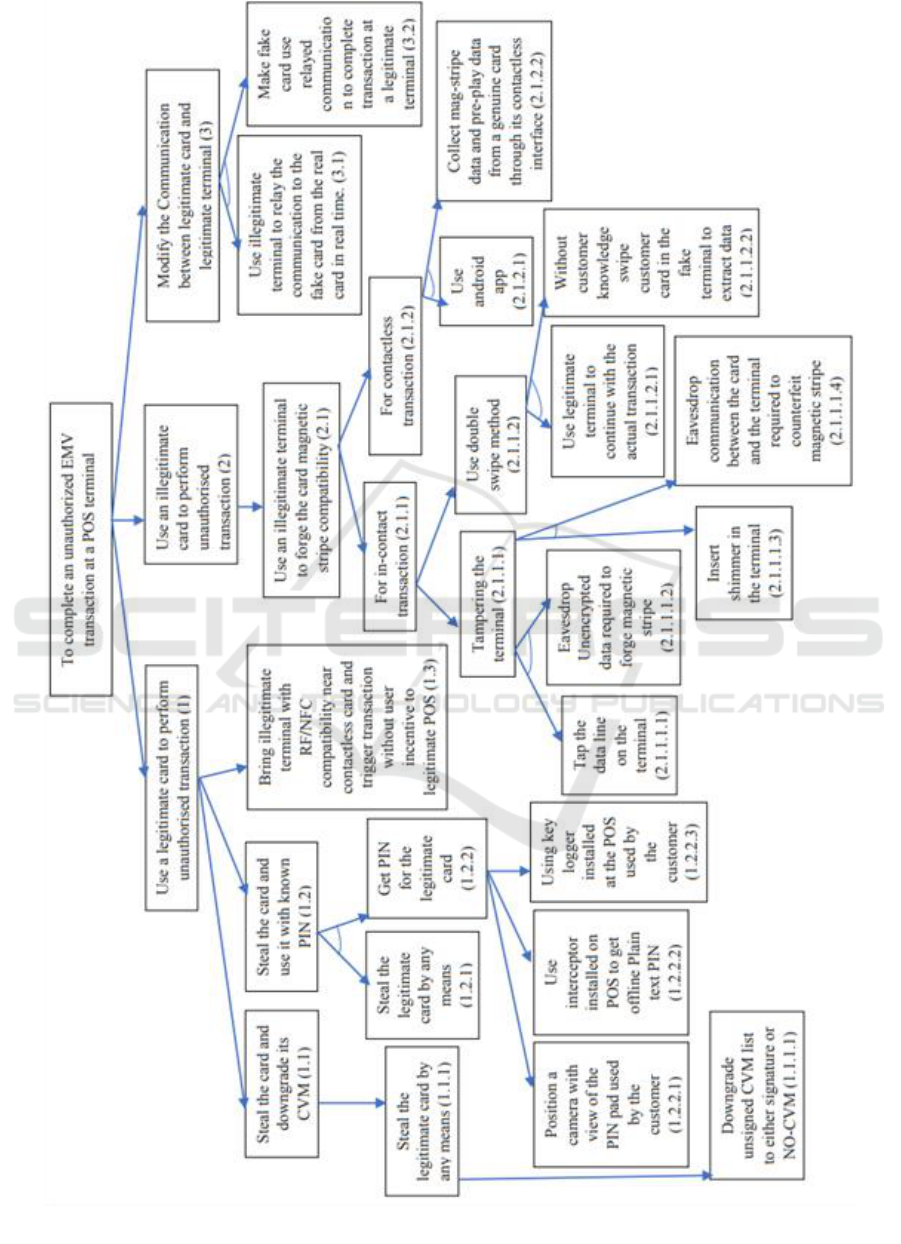

5 ATTACK TREE

METHODOLOGY

Attack tree methodology can be used to demonstrate

different ways in which a system can be attacked

and to design countermeasures thwarting the attacks

(Schneier,1999). Various attacks against a system

are represented with the goal as root node and how

to achieve it in different ways as leaf nodes.

Each leaf node becomes a sub-goal and children

of those leaf nodes are ways to achieve that sub-goal

(Schneier,1999). The attack tree structure is refined

using AND or OR logical connections. In AND

logical connections, all sister node conditions should

be met to achieve the sub-goal, whereas OR logical

connection acts as alternative methods. In the attack

tree, AND logical connection is represented as ‘ﮞ’ in

between the line connectors whereas OR logical

connections are simple line connectors.

The table below list EMV attacks. An arrow

vector is used to represent the down hierarchy of the

attack tree nodes (i.e. the sequence an attacker can

follow to achieve an attack). The AND logical

connection from the attack tree configuration is

represented as ‘&’ whereas OR logical connection is

represented as ‘-’. The attack tree follows Table 1.

Table 1: Attack tree nodes mapping various attacks and

countermeasures against those attacks.

ATTACKS

ATTACK

TREE

NODES

ATTACK MITIGATION

STRATEGY

Man-in-the-middle

attack

11.11.1.

1 1.1.1.1

Cardholder gets real time

notification of the transactions

made. Merchants inserting

cards into the terminal by

themselves. Card issuing bank

signing the CVM list.

Pre-play

attack

22.12.1.

22.1.2.1&2

.1.2.2

Cryptographically secure

random number generator.

Faraday-cage approach. Signed

CVM list.

NFC-Relay

Attack

11.3

Faraday-cage approach and

controlling the card activation.

Shim-in-the-

middle attack

22.12.1.

12.1.1.1

2.1.1.1.3&

2.1.1.1.4

Tamper-resistance terminal.

Daily routine inspections by

merchants. Cardholder

detection of changes to the

terminal.

Camera and

Double

-swipe

method

22.12.1.

12.1.1.2

2.1.1.2.1&

2.1.1.2.2

The cardholder having

adequate knowledge about how

to detect the modification in the

terminal and to determine

suspicious activities.

Counterfeit

Terminal

11.21.2.

1

&1.2.21.2.

2.1-1.2.2.2-

1.2.2.3

Encrypted PIN and use of

‘iCVV’ (i.e. ensure the

transaction if chip based)

Signal eavesdropping

attack

22.12.1.

12.1.1.1

2.1.1.1.1&

2.1.1.1.2

PCI DSS requirement: Encrypt

transmission of cardholder data

across open, public network

and restrict physical access to

cardholder data. The

cardholder able to detect the

modification in the terminal.

Active

relay

attack

33.1 & 3.2

Distance-bounding protocol of

card and terminal and/or user-

interface method.

ICISSP 2018 - 4th International Conference on Information Systems Security and Privacy

500

Figure 1: Attack tree modelling an unauthorised EMV transaction at a POS terminal.

Attack Tree for Modelling Unauthorized EMV Card Transactions at POS Terminals

501

6 CONCLUSIONS

This paper studied various attacks producing

unauthorized EMV card transaction at POS

terminals using an attack tree. Countermeasures

against those attacks are also provided. EMV card

industry participants can use this to understand the

risk to various parties during EMV transactions at a

POS terminal. This research adds to the existing

attack trees for ATM and browser EMV exploits.

REFRENCES

Bruce Schneier, "Attack Tree" [Online]. Available:

https://www.schneier.com/academic/archives/1999/12/

attack_trees.html [Accessed 11 May 2017].

EMV – Integrated Circuit Specifications for Payment

Systems, Book 2: Security and Key Management,

version 4.2 ed., LLC, June 2008.

Ezeude, Kingsley Anayo " The Modeling of An Identity

Catching Attack on The Universal Mobile

Telecommunication system (UMTS) Using Attack

Tree methodology" [Online]. Available: https://www.

scribd.com/document/243982400/The-Modeling-Of-

An-Identity-Catching-Attack-On-The-Universal-Mobi

le-Telecommunication-System-UMTS-Using-Attack-

Tree-Methodology [Accessed 14 May 2017].

How EMV (Chip and PIN) Works - Transaction Flow

Chart [Online]. Available: https://www.level2kernel.

com/flow-chart.html.

Joeri de Riuter and Erik Poll, Formal Analysis of EMV

Protocol Suite, Digital Security Group, Radboud

University Nijimegen, Netherlands. 2011 [Online]

Available; http://www.cs.ru.nl/E.Poll/papers/emv.pdf

Jordi van den Breekel, Diego A. Ortiz-Yepes, Erik Poll,

and Joeri de Ruiter, "EMV in a nutshell" [Online].

Available:https://www.cs.ru.nl/E.Poll/papers/EMVtec

hreport.pdf [Accessed 18 May 2017].

Jose Vila and Ricardo J. Rodrıguez," Practical

Experiences on NFC Relay Attacks with Android:

Virtual Pickpocketing Revisited"[Online]. Available:

https://conference.hitb.org/hitbsecconf2015ams/materi

als/Whitepapers/Relay%20Attacks%20in%20EMV%2

0Contactless%20Cards%20with%20Android%20OTS

%20Devices.pdf [Accessed 28 May 2017].

M. Bond. Chip and PIN (EMV) interceptor, March

2006.http://www.cl.cam.ac.uk/research/security/banki

ng/interceptor/ [Accessed 28 May 2017].

Maryam Mehrnezhad, Feng Hao, and Siamak F.

Shahandashti, " Tap-Tap and Pay (TTP): Preventing

the Mafia Attack in NFC Payment "[Online]. Availa-

ble:https://www.researchgate.net/publication/3001329

31_TapTap_and_Pay_TTP_Preventing_the_Mafia_At

tack_in_NFC_Payment [Accessed 12 June 2017].

Maxim Integrated Products, Inc., MAX1740, MAX1741

SIM/smart-card level translators in μMAX, January

2001, [Online] Available http://datasheets.maxim-

ic.com/en/ds/MAX1740-MAX1741pdf

Michael Roland and Josef Langer," Cloning Credit Cards:

A combined pre-play and downgrade attack on EMV

Contactless "[Online]. Available: https://www.usenix.

org/system/files/conference/woot13/woot13-roland.

pdf [Accessed 04 June 2017].

Mike Bond, Omar Choudary, Steven J. Murdoch, Sergei

Skorobogatov, Ross Anderson" Chip and Skim:

cloning EMV cards with the pre-play attack," 2014

IEEE Symposium on Security and Privacy.

Ogundele Oludele, Zavarsky Pavol, Ruhl Ron and

Lindskog Dale, “Implementation of a Full EMV

Smartcard for a Point-of-Sale Transaction”, World

Congress on Internet Security (WorldCIS), 2011,

Publication Year: 2012, Pages(s): 28 – 35.

Oludele Ogundele, Pavol Zavarsky, Ron Ruhl, Dale

Lindskog" Fraud Reduction on EMV Payment Cards

by the Implementation of Stringent Security Features"

International Journal of Intelligent Computing

Research (IJICR), Volume 3, Issues 1/2, Mar/Jun 2012

PCI Quick Reference Guide Understanding the Payment

Card Industry Data Security Standard version 1.2

[Online] Available: https://www.pcisecuritystandards.

org/pdfs/pci_ssc_quick_guide.pdf [Accessed 02

October 2017]

Ross Anderson, Mike Bond, and Steven J. Murdoch" Chip

and Spin" [Online]. Available: http://www.chip

andspin.co.uk/spin.pdf [Accessed 15 March 2017].

Saar Drimer and Steven J. Murdoch," Chip and PIN

(EMV) relay attacks" [Online]. Available: https://

www.cl.cam.ac.uk/research/security/banking/relay/

[Accessed 08 June 2017].

Saar Drimer, Steven J. Murdoch, Ross Anderson"

Thinking Inside the Box: System-Level Failures of

Tamper Proofing" 2008 IEEE Symposium on Security

and Privacy

Step by step: How does a EMV contact card payment

work? [Online]. Available: https://www.quora.com/

Step-by-step-How-does-a-EMV-contact-card-payment

-work.

Steven J. Murdoch, Saar Drimer, Ross Anderson, Mike

Bond " Chip and PIN is Broken," 2010 IEEE

Symposium on Security and Privacy.

Visa Expands Technology Innovation Program for U.S.

Merchants to Adopt Dual Interface Terminals.

[Online]. Available: http://usa.visa.com/download/

merchants/bulletin-tip-us-merchants-080911.pdf

Xilinx Inc., “Spartan-3E starter kit,” November 2009.

[Online]. Available: http://www.xilinx.com/products/

devkits/HW-SPAR3E-SK-US-G.htm

Ziv Kfir and Avishai Wool," Picking Virtual Pockets

using Relay Attacks on Contactless Smartcard

Systems" [Online]. Available: http://ieeexplore.ieee.

org/document/1607558/ [Accessed 24 May 2017].

ICISSP 2018 - 4th International Conference on Information Systems Security and Privacy

502