Cryptocurrency Position in Islamic Financial System: A Case Study

of Bitcoin

Nur Rizqi Febriandika, and Raditya Sukmana

Department of Islamic Economic Science, Postgraduate School Airlangga University, Surabaya, Indonesia

Keywords: Bitcoin, Islamic Finance, Cryptocurrency, Virtual Money, Commodity, Financial Asset

Abstract: The development of cryptocurrency is quite impressive. In 2017 at least there are 1148 types of

cryptocurency emerging spread in 5632 market sector. Bitcoin became the starting point for the

development of new applied cryptocurency science that is distributed ledger technology (DLT). It can be

said that the world of cryptocurrency entered a new era since the appearance of Bitcoin. This research is

purposed to find out how cryptocurrency position in islamic financial system, especially Bitcoin. This study

uses library research methods; its resources are taken from secondary sources in the form of books, journals

and fiqh rules related to cryptocurrency. This paper uses descriptive analysis and content analysis method.

The results of this study indicate that usefulness of Bitcoin is: 1) online shopping (for outlets, web, and

merchants that accept Bitcoin as a medium of exchange), 2) payments (for countries that legalize Bitcoin),

3) asset investment, and 4) trading. Bitcoin does not qualify either as money, commodity, or financial assets.

In Islam, it should not intentionally seek profit from the margin of buying and selling currency, because it is

included in the category of riba. One of the functions of Bitcoin is as a trading tool, it is clearly not allowed

in Islam because it contains the elements of maisir (gambling). If Bitcoin is regarded as commodity then it

causes a gharar because there is no intrinsic use / function contained in Bitcoin. Bitcoin also cannot be said

to be a financial asset because it has no underlying assets. Its value is based solely on market schemes

(supply-demand) and trust. Based on fiqh, Bitcoin contains a lot of syubhat and is not recommended for use.

1 INTRODUCTION

The development of cryptocurrency is quite

impressive, by the year 2017 there are at least 1148

cryptocurrency species sprung up in 5632 market

sectors (Marjan, 2017). The amount is expected to

continue to grow considering the public demand for

cryptocurrency continues to increase. It was a

historic day for the world of cryptocurrency in

January 2009 where on that date Genesis Block of

the new-born system, Bitcoin, was created by

Satoshi Nakamoto (Wijaya and Darmawan, 2017).

Bitcoin became the starting point for the

development of new applied cryptocurency science

that is distributed ledger technology (DLT).

Bitcoin's existing block-chain technology allows

many parties to exchange information without

having to rely on trusted central parties. Token

ownership verification can be performed using

cryptographic techniques with consensus method

mechanisms or collective agreements. Starting from

a simple transaction in Bitcoin, cryptocurrency

evolved with new concepts was put forwarded by

the community, which welcomed the emergence of

an open payment system that utilized the internet as

a transaction medium.

With the emergence of cryptocurrency itself

raises a lot of debate, many of which support or deny

its existence. Some countries have issued an official

circular banning cryptocurrency (Bitcoin) but not a

few also allow it. Many countries also have not

taken a stand regarding the existence of this

cryptocurrency itself.

Then how is this cyptocurrency viewed in an

Islamic perspective? What is the position of

cyptocurrency in the Islamic financial system? This

paper will discuss the characteristics of

cryptocurrency and how its position in the Islamic

economic system, especially Bitcoin. This study

uses library research methods; its resources are taken

from secondary sources in the form of books,

journals and fiqh rules related to cryptocurrency.

This paper uses descriptive analysis and content

analysis method.

Rizqi Febriandika, N. and Sukmana, R.

Cryptocurrency Position in Islamic Financial System: A Case Study of Bitcoin.

DOI: 10.5220/0007539401590163

In Proceedings of the 2nd International Conference Postgraduate School (ICPS 2018), pages 159-163

ISBN: 978-989-758-348-3

Copyright

c

2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

159

2 DISCUSSION

2.1 Cryptocurrency and Bitcoin

Cryptocurrency is a set of cryptographic and

logarithmic technologies, which will mathematically

compile codes and passwords to print virtual

currency (Nubika, 2018). Cryptography itself is a

programming language that serves to bind a virtual

program with certain security standards.

Cryptography technology is a major component in

cryptocurrency technology. In the early days,

cryptography was used to conceal information

during World War II, where German Nazi forces

developed one of the hardware devices called

Enigma used to randomize (encrypt) command

messages from control centers to all German troops

scattered throughout the world (Wijaya and

Darmawan, 2017).

Since then cryptography technology continues to

be developed in many ways, one of which is in the

making of a virtual currency that is currently on the

market. One of the first products that emerged and

had the largest market share was Bitcoin. Bitcoin has

a cryptocurrency market of 49% of the total and the

current market value is recorded at USD 4,348.99

(Marjan, 2017)

Actually, before the existence of Bitcoin, there

was an E-Gold, a digital currency established in

1996, by Gold & Silver Reserve Inc. which is based

in Nevis, the Lesser Antilles archipelago (Sondakh:

2016). E-Gold still purely uses the internet network

and does not use cryptographic and block-chain

technologies like Bitcoin today. Currently there are

still cryptocurrency types that offer gold as the

underlying gold-based cryptocurrency, such as:

Golden Currency, GoldVein, GoldMineCoin, AgAu,

and many more (http://www.goldscape.net). Based

on that cryptocurrency can be categorized into two

types; 1) that has underlying assets (gold), 2) has no

underlying.

Bitcoin is a pioneer in cryptocurrency as well as

implementation of the first block-chain technology.

This system was created by an anonymous who

claimed to be named Satoshi Nakamoto, although

until now no one knows the identity of the figure.

Satoshi laid down the basic principles of

cryptocurrency through a whitepaper titled bitcoin: a

peer-to-peer Electronic Cash System (Wijaya and

Damarwan, 2017). In 2009 was the first year of

Bitcoin's emergence in the global business world.

Peer to peer mechanism is a network between

computers that connect each other with the

mechanism of a single umbrella network, allowing

between computers can share. The technology that

governs the use of Bitcoin is called cryptocurrency

(Nubika: 2018).

Some things that can be used using Bitcoin: 1)

Shop online (for outlets, web and merchants that

accept Bitcoin as a medium of exchange), 2)

payments (for countries that legalize Bitcoin), 3)

asset investment, 4) trading (Nubika: 2018).

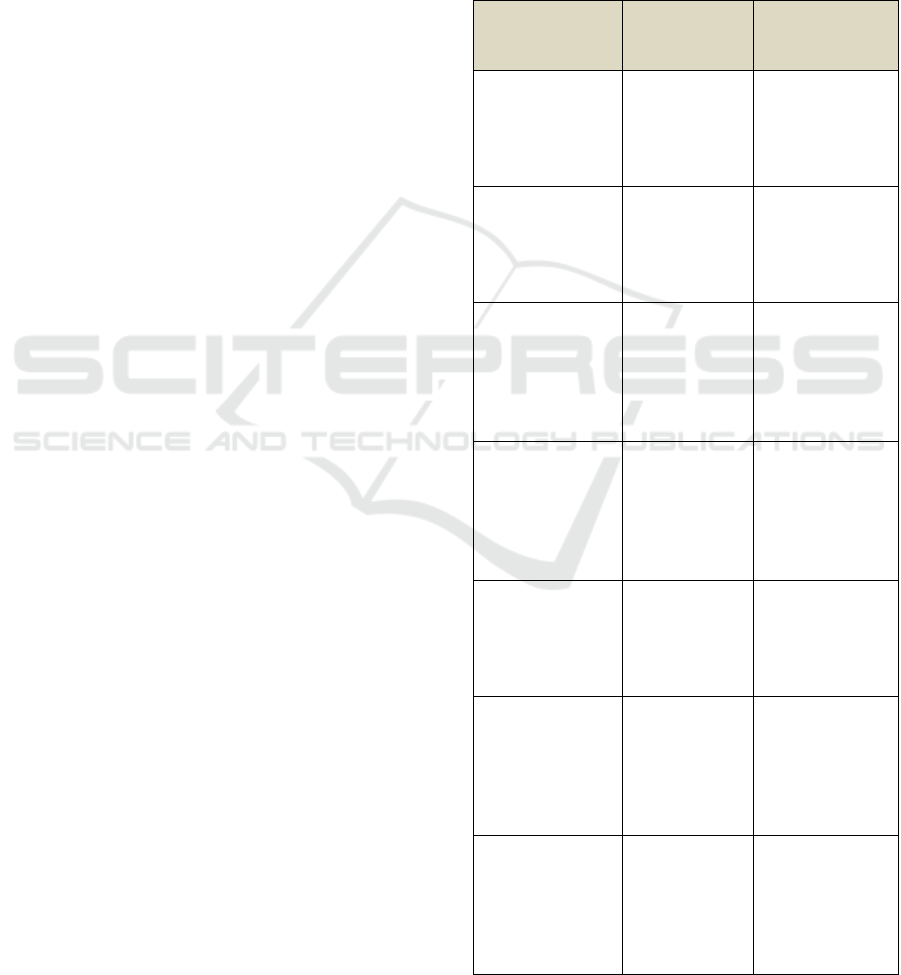

Table 1: Differences in Bitcoin, physical currency, and

e-money.

Bitcoin

Physical

Currency

(Fiat Mone

y

)

E-Money

Has no

physical form

Has physical

form

Derived from

physical

money

converted to

di

g

ital for

m

Using

cryptocurrency

technology and

produced by

"miner"

Issued by

Bank Central

Issued by a

Bank (or by a

licensed

private entity

Mining or

production is

limited to a

maximum of

21 million

Issues and

printers are

not limited as

long as there

is sufficient

warrant

y

Limited in

debit balances

and maximum

transactions

per day or

month

Requires a

computer desk

or smart phone

connected to

the Internet.

Does not

require any

device

Requires an

internet-based

device or it

may not be if

the device is

car

d

-

b

ase

d

There is no

official

regulation

There is

official

regulation

Regulated and

controlled by

each issuer,

with the

supervision

Can use

personal device

software,

mobile phone,

or on internet

network.

Physical

form, can be

placed

anywhere

that has an

empt

y

space

Stored on a

chip or server

connected to

an internet-

connected

device

The value of a

currency

depends on:

demand,

supply, and

trust level

Depending

on various

aspects of the

country's

economy

The value

follows the

physical

currency

ICPS 2018 - 2nd International Conference Postgraduate School

160

There is no

owner data

(anonymous),

No

ownership

data of any

currency in

circulation.

Ownership

data and each

transaction is

recorded by

each issue

r

Its current use

is still limited

to a particular

business.

Can be used

freely while

still in the

territory

Its use is

limited to

business

owners who

have

cooperation

with publishers

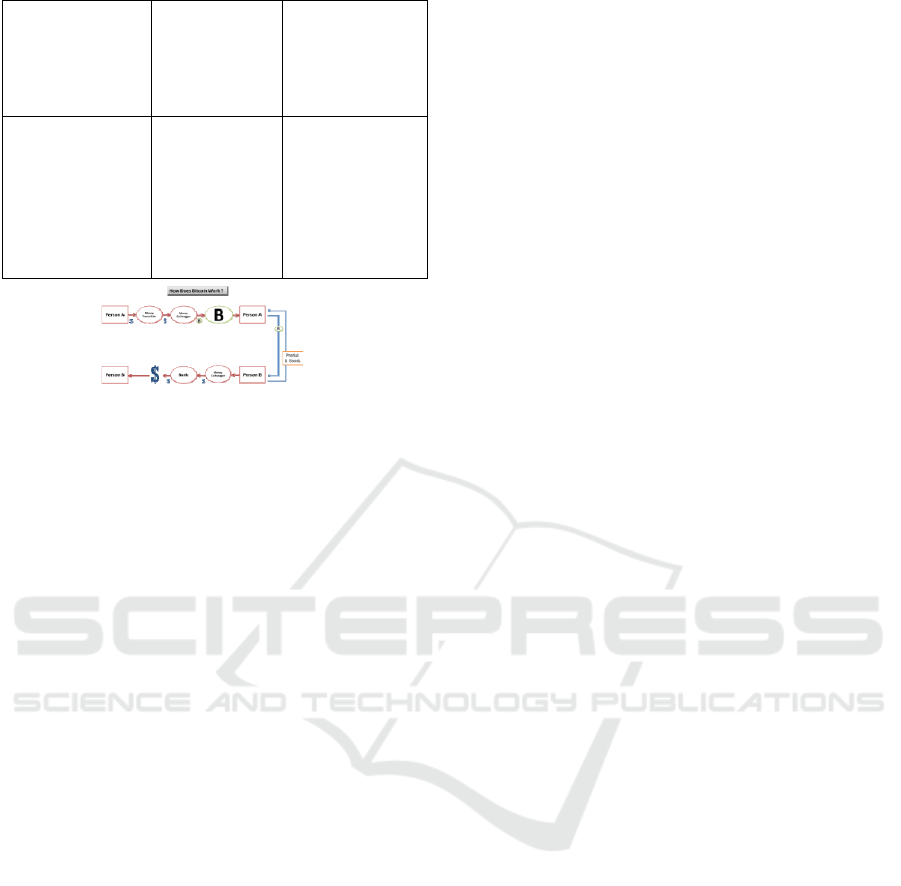

Figure 1: How Bitcoin works

2.2 Electronic Money and Virtual

Money

In Conventional economics, money functions as: 1)

medium of exchange; 2) standard of value or unit of

account; 3) store of value or store of wealth; 4)

standard of deferred payment. However, this is

different from the Islamic economic system that only

recognizes the function of money as a medium of

exchange and unit of account. As for the store of

value and standard of deferred payment is still a

debate among Islamic economists (Hasan, 2005).

Islam does not set in detail how the terms of a

currency because when Islam emerged already

contained the currency first. Based on the agreement

the terms of the currency are: 1) acceptability (the

money is widely accepted by the public and its

users), 5) divisibility (can be divided into smaller

fractions), 6) legal tender (no government

guarantee), 7) portability (easy to carry anywhere),

and 8) durability (last long and not easily damaged

when stored) (Nubika, 2018).

In 2012 the European Central Bank defines as a

form of non-regulated currency created and

supervised by the developer for use by its

specialized members of the virtual community

(Sondakh, 2016).

While the US Department of Treasury in 2013

states explicitly that virtual money as a medium of

exchange that operates like a currency in certain

environments, but does not have any attribute as a

real currency. So virtual money has no definition as

legal tender. In the case of regulation itself,

circulation cannot be controlled by the local Bank

Central. What distinguishes the virtual money with

electronic money (digital) is related to its existence

that still has the original money underlying. As often

used in debit card transactions, e-cash, e-tol, go-pay,

and the like, the numbers shown in the digital

nominal are representations of the ownership of a

certain amount of fiat nominal value. In this case the

ministry of finance and Bank Central have

regulation related to this matter and its circulation

can still be supervised.

2.3 Bitcoin Position In Fiqh Perspective

and Islamic Finance

In fiqh perspective, currency terms are known as

nuqud (Hasan: 2005). As a currency, money cannot

be a commodity at the same time, because fiqh law

has different rules between commodities and

currencies. Money will not be used as an investment

object because money is a medium of payment.

Currency exchange (sharf) may only be carried out

with special conditions formulated in Fatwa Dewan

Syariah Nasional-Majelis Ulama Indonesia (DSN-

MUI) or the Accounting and Audit Organization for

Islamic Financial Institutions (AAOIFI). The main

problem that arises in Bitcoin is not only a character

that is not stable and does not have legal tender, but

its own function which is used as an investment

medium (commodity/financial assets) makes its

form increasingly unclear (containing syubhat). The

terms of riba will apply to money that contains

profits from sales, in contrast to goods that are

indeed allowed to profit from buying and selling

activities. Based on fiqh, Bitcoin contains a lot of

syubhat and is not recommended for use.

Cryptocurrency position with foreign currency is

not the same. In Indonesia for example, the money

that applies is money issued by a trusted government

agency (for example rupiah), but may exchange it

for foreign money (for example dollars) under

certain conditions such as foreign travel, investment

or trade in goods and services related to international

market (Bank Indonesia Regulation no. 18/20 pbi

2016. In Indonesia itself, Bank Indonesia bans

transactions using virtual currency (bitcoin) (Bank

Indonesia regulation chapter VII article 34 number

14/40 /pbi/ 2016. In AAOIFI and Fatwa standards

DSN-MUI states that foreign currency transactions

may only be done directly/spot and may not be

forwarded to avoid potential gharar and riba due to

changes in the value of a currency in the future.

Although some foreign currencies are often

unstable (sometimes weakening and rising), they are

still within reasonable limits. Changes in the value

Cryptocurrency Position in Islamic Financial System: A Case Study of Bitcoin

161

of a country's currency against another country's

currency have nothing to do with the validity of the

currency in the country itself. Although the money

compared to foreign currencies tends to weaken, it

still applies in its own country based on regulations

made by the local government. Unlike Bitcoin, it can

be worthless at any time if no country wants to

accept it. On the other hand, the main function of

Bitcoin is trading and investment tools. The function

of bitcoin as a payment medium is still very limited

to certain merchants and it only aims to promote the

cryptocurrency itself so that its value continues to

soar without having an intrinsically certain use.

Bitcoin is one of the most unique cases in

Islamic finance. Unlike the conventional financial

system, in the Islamic economic paradigm the status

or position of a business object implies the law of

halal and haram, whether Bitcoin is money,

commodities, or financial assets? The following

characteristics of Bitcoin are shown in Table 2.

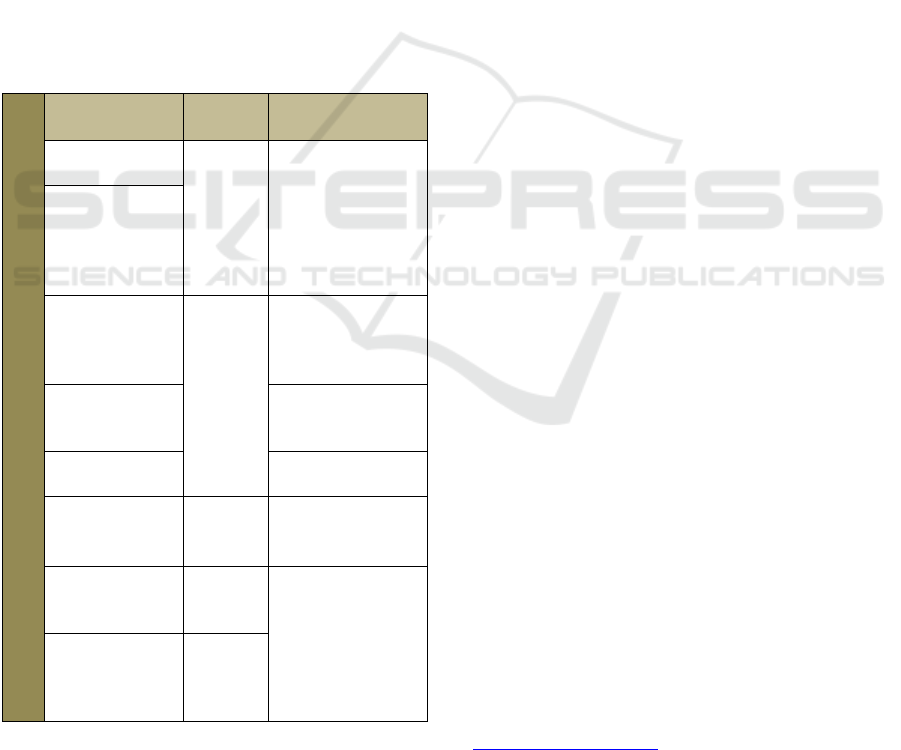

Table 2: Position Bitcoin (Marjan, 2017)

Characteristic of Bitcoin

Money Comm

odities

Financial Assets

Acceptability

(

y

es)

Recogn

ized by

sharia

as

valuabl

e

(Yes)

Value is

dependent on the

time is priced

(Yes)

Difficult to

Imitate

(yes)

Storable

(yes)

Must

have an

intrinsi

c value

that can

be

benefit

ed from

(No)

Recognized by

sharia as

valuable

Yes)

S

t

ability of

value (No)

Identifiable/trans

ferable

(Yes)

Legal tende

r

(No)

Can be owne

d

(Yes)

Portability

(Yes)

Can be

owned

(Yes)

Store of value

(Yes)

Divisibility

(Yes)

Identifi

able

(Yes)

Must be backed

by underlying

aset/ sharia

compliant

investment

activities

(No)

Durability

(Yes)

Transfe

rable

(Yes)

Based on the analysis, Bitcoin does not qualify

either as money, commodity, or financial assets. In

Islam, it should not intentionally seek profit from the

margin of buying and selling currency because it is

included in the category of riba.

Moreover, one of the functions of Bitcoin is as a

trading tool, it is clearly not allowed in Islam

because it contains elements of maisir (gambling). It

is regarded as a commodity raises a hardship

because there is no use/intrinsic function contained

in Bitcoin. Its existence becomes worthless because

it serves as a means of exchange (money). While

Bitcoin also cannot be said to be a financial asset

because it has no underlying assets. Its value is

based solely on market schemes (supply-demand)

and trust, without the support of the

guarantor/regulator of the government to make the

future Bitcoin contains elements of Gharar.

3 CONCLUSIONS

The results of this study indicate that Bitcoin does

not qualify either as money, commodity, or financial

assets. In Islam, it should not intentionally seek

profit from the margin of buying and selling

currency, because it is included in the category of

riba. One of the functions of Bitcoin is as a trading

tool, it is clearly not allowed in Islam because it

contains elements maisir (gambling). If Bitcoin is

regarded as commodity then it causes a gharar

because there is no intrinsic use/function contained

in Bitcoin.

Bitcoin also cannot be said to be a financial asset

because it has no underlying assets. Its value is

based solely on market schemes (supply-demand)

and trust. However, as a currency, money cannot be

a commodity at the same time because fiqh law has

different rules between commodities and currencies.

Money will not be used as an investment object

because money is a medium of payment. Based on

fiqh, Bitcoin contains a lot of syubhat and is not

recommended for use.

REFERENCES

Marjan Muhammad (2017), Shari’ah Analysis of

Cryptocurrency: bitcoin. a presentation made at

Shariah Fintech Forum (SFF), 8 November 2017,

Hilton Hotel, Petaling Jaya.

Hasan. Ahmad.2005. Mata Uang Islami. Jakarta : PT Raja

Grafindo Persada

http://www.goldscape.net accessed 05-05-2018.

Nubika, Ibrahim. 2018. Bitcoin:mengenal cara baru

berinvestasi generasi milenial. Yogyakarta :Ganesa

Learning

ICPS 2018 - 2nd International Conference Postgraduate School

162

Sondakh,Alfred M. 2016. Berburu Bitcoin: Bagaimana

Meemanfaatkan Peluang Sukses Melalui Mata Uang

Global Ini. Jakarta : PT.Gramedia

Wijaya, Dimasz Anka, Darmawan, Oscar. 2017.

Blockchain : Dari Bitcoin untuk Dunia. Jakarta

:Jasakom.

Cryptocurrency Position in Islamic Financial System: A Case Study of Bitcoin

163