The Efficiency of Distribution of Zakat Fund at LAZNAS in

Indonesia

Novi Nurul Aini

1

, Ari Prasetyo

2

, and Tika Widiastuti

2

1

Postgraduate School Universitas Airlangga, Surabaya, Indonesia

2

Departement of Sharia Economic, Economic and Business Faculty, Universitas Airlangga, Surabaya, Indonesia

Keywords: Efficiency, Zakat fund, Laznas, Data Envelopment Analysis

Abstract : This study aims to analyze the relative efficiency of Lembaga Amil Zakat Nasional in 2013 to 2016 and to

see the source of inefficiency. Respondents consist of four LAZNAS that have been confirmed by the

government since the year and have official financial statements published on their respective websites,

Rumah Zakat (RZ), Pos Peduli Peduli Umat (PKPU), Dompet Dhuafa (DD) and Yatim Mandiri. This study

uses a method that can measure the performance of companies that can handle many inputs and outputs at

once, the method of Data Envelopment Analysis (DEA). This method is chosen by the intermediation

approach and using the appropriate variables with the intermediation approach is the distribution of zakat

funds as output variables and the three components as input variables are zakat funds receipts, employee

salaries and operational costs. The results show that these four LAZNAS simultaneously achieve maximum

efficiency in 2016.

1 INTRODUCTION

The fact that the condition of Indonesian people is

still in low level of welfare cannot be denied,

according to the Central Bureau of Statistics (BPS)

recorded the number of poor people in September

2017 reached 26.58 million people. When the

discourse of poverty erupted, many people connect it

with the issue of zakat as an alternative solution. Ibn

Taimiyah in a history once offered a prescription to

eliminate poverty that is with the development of

zakat and grants from the government.

According to Wibisono (2010) zakat will

significantly influence if balanced with good

governance by establishing a strong and credible

zakat authority, with the role of National Zakat

Agency (Baznas) which will have regulatory and

supervisory authority in three main aspects, namely

compliance of sharia, transparency and financial

accountability, and economic effectiveness of the

utilization of zakat funds.

Discussion about the zakat cannot be separated

from the management, in this case is the

management of zakat. In Indonesia the management

of zakat has been regulated in Law no. 38 of 1999.

Under this Act the management of zakat is done by

the state (BAZ) and the community (LAZ). BAZ and

LAZ can manage zakat according to their level.

LAZ's hopes and aspirations are to tackle or reduce

poverty. Zakat management institutions are

considered as public sector institutions. Managing

zakat means managing public funds, which means

managing public sector funds, for fund management

the public can run well then it needs the involvement

of the community in its supervision

Related to the performance of zakat management

institution, in the official website of Ministry of

Religious Affairs, M. Fuad Nasar as Director of

Zakat Empowerment and Waqf of the Ministry of

Religious Affairs said that the growth of national

zakat has a positive trend from the accumulated

average of zakat, infaq and alms (ZIS) others. The

growth of zakat during 2017 increased about 20%

from the previous year to Rp 6 trillion, compiled by

the National Amil Zakat Agency (Baznas) and the

Amil Zakat Institute (LAZ). According to him, if

offset by the increase of service on zakat payments

that are creative and innovative one of them through

digital service then the realization can reach 30% of

the total revenue of zakat. Citing data from the

survey results Baznas also stated that the potential of

zakat wealth and income of individuals in Indonesia

can actually reach Rp 138 trillion per year.

Nurul Aini, N., Prasetyo, A. and Widiastuti, T.

The Efficiency of Distribution of Zakat Fund at LAZNAS in Indonesia.

DOI: 10.5220/0007539601710175

In Proceedings of the 2nd International Conference Postgraduate School (ICPS 2018), pages 171-175

ISBN: 978-989-758-348-3

Copyright

c

2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

171

On the other hand, according to Karim and

Sharif (2009) the proliferation of LAZ can lead to

inefficiency in the management and distribution of

zakat, infaq and alms funds. Therefore, the

importance of coordinative, consultative and

informative functions in the collection and

channeling of funds should be made by a body

recognized by all LAZ and state authorities.

With the above description the author is

interested to conduct research on Amil Zakat

Institute with topic Efficiency Amil Zakat Institute.

From this research is expected to be answered

whether LAZ has been efficient in terms of revenue

and distribution of funds.

2 LITERATURE REVIEW

2.1

Definition of Amil Zakat Institute

National Zakat Institution (LAZNAS) is a zakat

management institution that is formed by the

community and confirmed by the government to

carry out the activities of collecting, distributing, and

utilizing zakat to assist BAZNAS. (Law number 23

of 2011 concerning Management of Zakat Chapter II

Article 17)

Law number 23 of 2011 concerning Zakat

Management Chapter I Article 1 states that zakat

management institutions in Indonesia consist of two

groups of institutions, namely the National Zakat

Agency (BAZ) and the National Zakat Institution

(LAZNAS). BAZ is formed by the government,

while LAZ is formed by the community (Sudarsono,

2008: 262).

Currently amil framed in the form of Amil Zakat

and Amil Zakat Institute. According to Imam

Qurtubi in Hafidhuddin (2002: 125), amil is the

person assigned (by imam/government) to take,

write, calculate and record the zakat he took from

the muzakki to then be given to the right to receive

it.

According to the opinion of some scholars in

Qardhawi (1999: 532) that government (in this case

a manah, trustworthy and professional Zakah

Institution) is allowed to build companies, factories

and others from zakat money, to be given to

mustahik in a relatively large number, so that the

needs of the mustahik are met. But in the

implementation need seriousness, prudence and

precision, in order to avoid losses due to the

mistakes of the manager.

2.2 Fund Disbursement

According to Hafidhuddin (2008: 27-34) zakat

collected by zakat management institutions should

be immediately channeled to the mustahiq (recipient

of zakat) in accordance with the priority scale that

has been prepared in the work program. The zakat

should be distributed to the mustahiq as set forth in

the letter At-Taubah verse 60.

The productive distribution of zakat, as it had

been in the time of the Prophet, was mentioned in a

hadith of Imam Muslim's narration from Salim bin

Abdullah bin Umar from his father, that the

Messenger of Allah had given him zakat and told

him to be developed or rededicated. For now, in

Indonesia the role of government in the management

of zakat is replaced by the Agency Amil Zakat and

Institute of Amil Zakat.

2.3 Concept of Efficiency

Efficiency is a productivity component and refers to

the actual and optimal ratio of inputs and outputs

(Lovell, 1993). The concept of efficiency in

economics proposed by Worthington (2004) consists

of three types of efficiency as follows:

1. Technical efficiency, refers to possible

maximizing output with a number of inputs.

2. Allocative efficiency, concerning the choice

between a combination of the use of technically

efficient inputs to produce the maximum possible

output.

3. Cost Efficiency or economic efficiency, a

combination of technical and allocative

efficiency in a complete manner can be said to

have reached the total economic efficiency.

2.4 Previous Research

Wahab and Rahman (2012) analyzed the efficiency

of zakat institutions in Malaysia using Data

Envelopment Analysis (DEA). Empirical research

results show that zakat payments, computerized

zakat systems, board of directors, audit committee,

and decentralization significantly influence the

efficiency of zakat institutions in Malaysia.

Ahmad and Main (2014) use two stages of Data

Envelopment Analysis (DEA) to analyze the

efficiency of zakat institutions in Malaysia. The

analysis was carried out on the collection and

distribution of zakat funds at the Selangor Zakat

Institution.

Alfi Lestari (2015) in journal titled Efficiency of

Financial Performance of Regional Zakat Agency

ICPS 2018 - 2nd International Conference Postgraduate School

172

(BAZDA): Data Envelopment Analysis (DEA)

approach with the object of research of the BAZDA

financial report of East Lombok district 2012 to

2014.

Salman Al Parisi (2016) conducted a study

entitled The Level of Efficiency and Productivity of

Zakat Institutions in Indonesia, in that the study

measured efficiency and productivity in five zakat

institutions in 2005 to 2014.

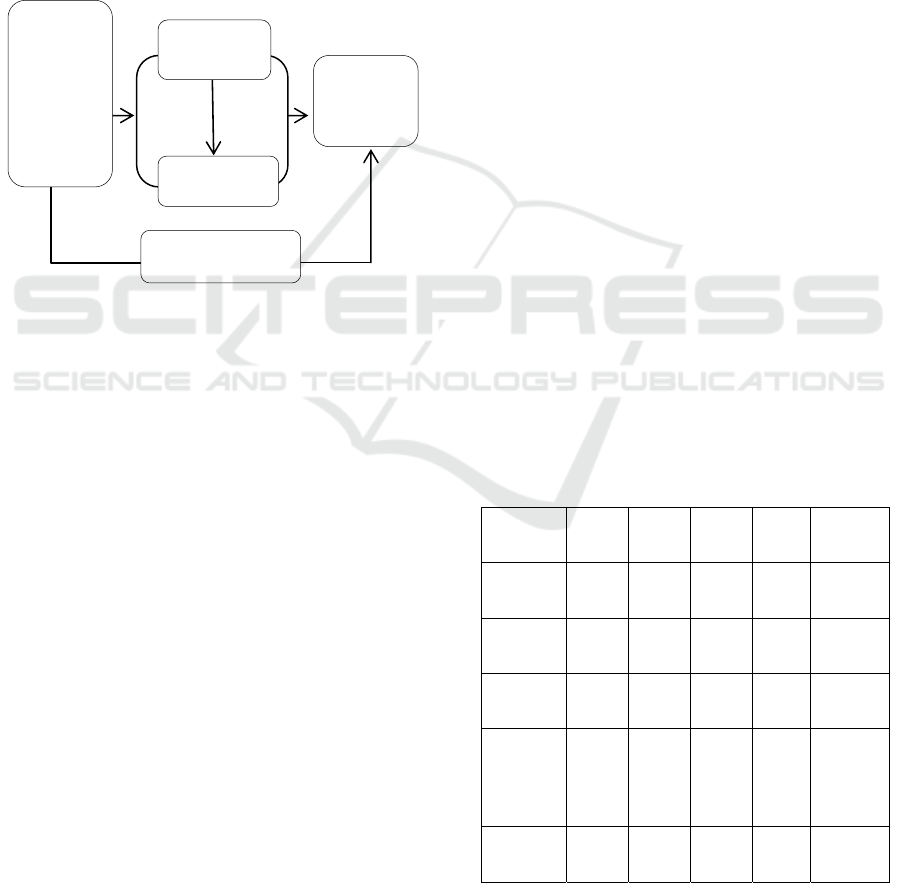

2.5 Conceptual Framework

Figure 1: Conceptual Framework.

The framework of thinking in this study is the

performance of LAZ seen from its operational

efficiency, in carrying out its function as an

intermediary institution. Variables used consist of

input variables, namely the receipt of zakat funds,

employee salaries and operational costs and the

distribution of funds as a variable output. This study

uses DEA as a measure of efficiency to see how

much efficiency LAZ generates, and to determine

which LAZ works most efficiently compared to

other LAZs.

3 METHOD AND RESERACH

This study uses a quantitative approach. The data

used in this study is secondary data that has been

published and audited obtained from the

publications published each zakat institution from

2013 to 2016.

Problems in this research will be analyzed by

Data Envelopment Analysis (DEA) method. DEA is

a mathematical programming model used to

calculate the relative efficiency of a unit compared

to other units using a variety of similar inputs and

outputs.

The term "Decision Making Unit" (DMU) was

therefore introduced to cover, in a flexible manner,

similar to that of similar input outputs. (Cooper et

al., 2006)

This technique is used to find out how efficiently

DMUs are used with the utilization of existing

equipment to be able to produce optimum output.

4 RESULTS AND ANALYSIS

4.1

Nilai Efisiensi

The purpose of this study is to look at the efficiency

level of four LAZNAS during the period 2013 to

2016. The Zakat Institute is said to be efficient if it

has an efficiency value (ε) = 1 (one) or 100% which

means LAZ is no longer wasting the use of its inputs

and / or has been able to optimally utilize the inputs

to produce maximum output so that it can be a

reference for LAZ that has not been efficient. On the

contrary Zakat Institute is said to be inefficient if its

efficiency value is 0 ≤ ε < 1 or less than 100%. The

value of ε less than 1 (one) indicates that the LAZ is

still performing wasteful action in the use of its input

units.

Here are the results of data processing on

LAZNAS in the period 2013 to 2016 using the

method of data envelopment analysis (DEA). The

results of data processing show the value of

efficiency as follows:

Table 4.1: Table of efficiencies.

LAZ 2013 2014 2015 2016 Perform

RZ 10.70 24.01 90.28 100 Increase

DD 85.89 100 100 - Increase

PKPU 6.05 14.39 100 100 Increase

Yatim

Mandiri

- 94.11 100 100 Increase

Average 34.21 58.12 97.57 100 Increase

Input:

-zakat

fund

-employee

salary

-operating

cost

Operational

efficiency

LAZ

Performance

Output:

distributio

n of zakat

Data Envelopment

An

a

l

ys

i

s

(

DEA

)

The Efficiency of Distribution of Zakat Fund at LAZNAS in Indonesia

173

The table above shows that on average the LAZ

has increased the efficiency level from the year 2013

by 34.21% up to 58.12% in 2014, then in 2015 rose

to 97.57% and in 2016 rose to 100%. The table

shows changes in the efficiency values of the four

LAZs in the period 2013 to 2016 which are all

included in the upgraded performance group.

4.2 Maximum Efficiency

In table 4.1 in 2016 three LAZNAS namely RZ,

PKPU, and Yatim Mandiri simultaneously achieve

maximum efficiency, in connection with this matter

here will be described regarding the maximum

efficiency that can be achieved by the LAZNAS.

One example taken in the discussion of maximum

efficiency here is the result of data processing on the

efficiency of the receipt and distribution of zakat

funds in the RZ in 2016.

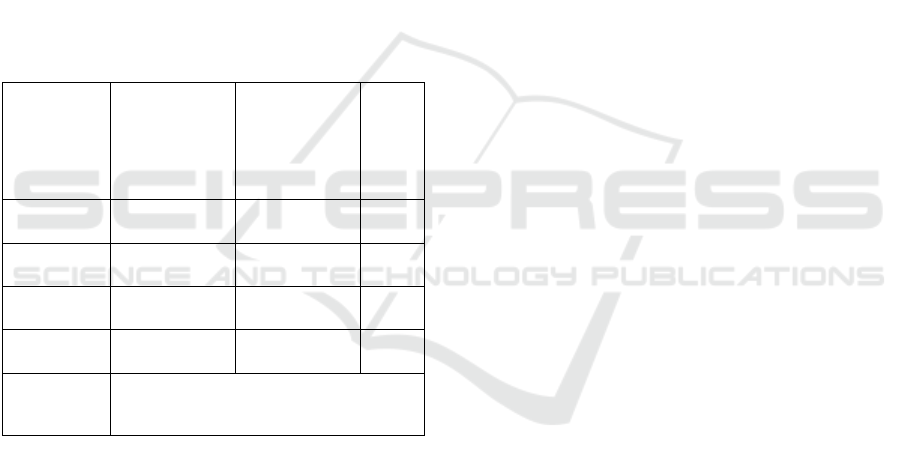

Table 4.2: Potential Improvement RZ 2016.

Sources: RZ Financial statements 2016 are processed with

DEA

In the table above it can be seen that the actual

value (true value) and target value (the value that

must be achieved) are the same, it shows that in each

variable both input and output can be used

optimally. The potential improvement shown in

figure 0 shows that both the receipt and distribution

of zakat funds have been efficient so there is no

potential improvement value to increase efficiency

because the efficiency achieved has been

maximized.

5 CONCLUSION

Based on research on the efficiency of zakat fund

distribution at LAZNAS in Indonesia, it can be

concluded that four LAZNAS both achieve

maximum efficiency in 2016. In 2014 only DD

reaches 100% efficiency level and consistent until

the following years. LAZNAS with the lowest level

of efficiency is PKPU (2013) of 6.05% but in the

next year increased efficiency to 14.39% and in

2015-2016 reached 100% efficiency level. In 2015-

2016 Yatim Mandiri has achieved maximum

efficiency while the new RZ achieve maximum

efficiency in 2016.

With the above explanation, the consistency of

efficiency scores experienced by DD, PKPU, and

Yatim Mandiri for two consecutive years indicates

that LAZ operationally has savings from its inputs or

optimization in the deployment of inputs so that the

output is maximized.

The maximum efficiency can occur because the

actual value (true value) and target value (the value

to be achieved) are the same, it shows that in each

variable both input and output can be used

optimally.

REFERENCES

Ahmad and Main. 2014. The Efficiency of Zakat

Collection and Distribution: Evidence from Two

StageAnalysis. Journal of Economic Cooperation and

Development Vol 35 No 3 133-170.

Al Parisi, Salman. 2016. Tingkat Efisiensi dan

Produktivitas Lembaga Zakat di Indonesia. Jurnal

Bisnis dan Manajemen Vol 7 (1) 63-72.

Alfi Lestari. 2015. Efisiensi Kinerja Keuangan Badan

Amil Zakat Daerah (BAZDA): Pendekatan Data

Envelopment Analysis (DEA). Jurnal Ekonomi dan

Studi Pembangunan. Vol 16 No.2 hal 177-187

Cooper, William W., Lawrence M. Seiford, Kaoru Tone.

2007. Data Envelopment Analysis: A Comprehensive

Text with Models, Applications, References and DEA-

Solver Software. Edisi Kedua. Springer.

Hafidhuddin, Didin. 2002. Zakat dalam Perekonomian

Modern. Jakarta: Gema Insani.

Karim, Adiwarman A & A. Azhar Syarif. 2009. Fenomena

Unik Di Balik Menjamurnya Lembaga Amil Zakat

(LAZ) Di Indonesia. Zakat & Empowering Jurnal

Pemikiran dan Gagasan Vol I.

Norazlina Abd Wahab dan Abdul Rahim Abdul Rahman.

2012. Efficiency of Zakat Institution in Malaysia: An

Application of Data Envelopment Analysis. Journal of

Economics Cooperation and Development. Vol.33

No.1 hal 95-112

Qardhawi, Yusuf. Hukum Zakat. 1999. Bandung: Mizan.

Input/Output Actual Target

Potent

ial

Impro

ve-

ment

Salary 4820051132 4820051132 0

Operational 10920759037 10920759037 0

Income 109338881331 109338881331 0

Distribution 113599505962 113599505962 0

Efficiency

RZ 2016

100%

ICPS 2018 - 2nd International Conference Postgraduate School

174

Sudarsono, Heri. 2007. Bank dan Lembaga Keuangan

Syariah: Deskripsi dan Ilustrasi. Edisi Kedua.

Yogyakarta: EKONISIA.

Wibisono, Yusuf. 2010. Mengelola Zakat Indonesia.

Jakarta: Kencana Prenada Media Grup.

The Efficiency of Distribution of Zakat Fund at LAZNAS in Indonesia

175