Study of Green Information Disclosure on China’s Thermal

Power Plants

T Li, Y M Song

*

and Y Liu

Department of Economics and Management, North China Electric Power University,

No.2 Beinong Road, Changping District, Beijing

Corresponding author and e-mail: Y M Song, songyimiao@hotmail.com

Abstract. This paper studies the way of green accounting information disclosure by

introducing the basic idea of input-output analysis and combining it with the emergy analysis

in the field of ecological economics and aims to explore a framework to disclose green

accounting information. Firstly, through the research on the status quo of China's green

information disclosure, it is found that there are two main problems in the disclosure of green

information in China, that is, incompleteness in disclosure content and difficulty in

measurement. Then, by taking China’s coal-fired thermal power generation as an example,

the main input resources, flow of directions and the final transformation forms are

summarized from the perspective of material flow. By analy zing the generation process of

coal-fired generation plants, this paper attempts to apply the basic idea of input-output

analysis to construct the preliminary framework of green information disclosure. Furthermore,

emergy analysis is introduced to convert physical data to monetary information to provide a

unified enterprise disclosure framework of green accounting.

1. Introduction

With the development of the global economy, China has entered a new era. Before 1970s, China’s

environmental problems were neglected because of the priority of quick success and instant benefits

on economic progress and lack of environmental protection policies [1]. However, Chinese

environmental development is no longer a mere economic progress recently, ecological development

has also been elevated to a strategic level and has become one of the most important goals in which

China pursues. The 18

th

National Congress of the Communist Party of China proposed the five-in-

one strategic layout. Before that, four-in-one layout has played a dominant role for the past decade

which was made up by economic construction, political construction, cultural construction and social

construction. Compared to four-in-one layout, ecological civilization construction is brought into

five-in-one layout and become China’s strategy for the first time. The requirements of coordinating

ecological development and economic development make the enterprises pay increasing attention to

social responsibilities while pursuing the goal of maximizing profits. The point is that they should

shoulder social and environmental responsibilities [1]. The traditional accounting has been strongly

influenced by new ideas. A growing number of countries have added the content of environmental

information disclosure under the traditional accounting information disclosure framework [3]. Green

accounting is a tool of recognition, collection, and analysis of environmental information which is

Li, T., Song, Y. and Liu, Y.

Study of Green Information Disclosure on China’s Thermal Power Plants.

In Proceedings of the International Workshop on Environmental Management, Science and Engineering (IWEMSE 2018), pages 469-480

ISBN: 978-989-758-344-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

469

also known as environmental management accounting (EMA) by the international community [4].

The researches of F A Beams [5]and J T Marlin [6] on the social costs of pollution and the

accounting of pollution have created a new era of green accounting and researches on green

accounting have begun to grow.

The United Nations released the System of Integrated Environment and Economic Accounting

(SEEA) [7] in 1993. As a product of the sustainable development economy, it is mainly used for the

implementation of national accounts under the influence of environmental factors. Afterwards, the

UN Department of Public Information Strategic Communications Division (UNDSD) put forward

specific methods for implementing environmental management accounting [8]. The UNDSD EMA

method includes four types of environmental expenditures (costs) and one type of environmental

income measured by seven environmental media. By the implementation of this classification,

companies can find hidden costs and relevant cost savings. Since then, Gale[9]applied this method to

a Canadian manufacturing company and found that the natural and environmental costs under

traditional accounting were underestimated by approximately 50%.

As the topic of corporate social responsibility continues to intensify, more and more scholars

begin to pay attention to the relationship between organizational behavior and the environment [10].

One study found that environmentally sensitive organizations such as mining, chemical,

pharmaceutical and oil extraction are more likely to implement green accounting, while legal

requirements also force these industries to actively use environmental accounting as a method of

internal management[11]. Moreover, due to the limitation of organizational capital, the effective

utilization of environmental resource capital also urges managers to pay more attention to

environmental strategy [12]. In addition, the strategic direction of the enterprise, the industry in

which it operates and the size of the organization also have a great relationship with the use of

environmental accounting [13].However, although green accounting has received growing attention,

its application still faces many difficulties, lack of learning at the organizational level, excessive

attention to economic performance and lack of guidance on the application of environmental

accounting[14]have seriously hampered the development of green accounting.

China entered the ranks of the newly industrialized nations (NICs) in 2011, and the contradiction

between economic growth and environmental development has become increasingly prominent [15].

Recycling economy and green economy have become the theme of the development of new era. The

demand for green information is increasingly highlighted [16]. In the 1990s, Jiashu Ge

[17]introduced the concept of environmental accounting into China for the first time, marking the

beginning of China's systematic study of green accounting. So far, theorists have tentatively set up

the theoretical framework of green accounting [18] and pointed out that enterprises are facing serious

environmental risks and environmental liabilities [19]. However, there are only few studies on the

methods of green information disclosure in China. At present, the disclosure of green information

draws basically on traditional financial accounting and generates a series of forms such as

environmental balance sheet, environmental cash flow statement and environmental profit statement

[20]. However, there is no further study on how to quantify the green information which is of vital

importance in the information age.

What kind of green information should organizations disclose to the general public? How to

quantify the green information to make it more comparable? By analyzing the current situation of

China's green accounting information disclosure, this paper attempts to use the basic idea of input-

output analysis to build the preliminary framework of green information disclosure, taking the coal-

fired thermal power plant as an example. Also, by introducing the theory of emergy analysis into the

framework of green information disclosure, this research may help to solve the problem of the

current measurement dilemma of green information.

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

470

2. Green information disclosure in China

The demand for green information is the main motivation for enterprises’ disclose behaviors.

Although an increasing number of public listed companies in China have disclosed Corporate Social

Responsibility Report (CSR) in order to meet the economic decision-making needs of stakeholders

[21] in recent decades, the performance of environmental and social responsibility information in the

report is not enough to satisfy the needs of the public. Therefore, this paper studies the status quo of

Chinese corporate green information disclosure to find out the main problems existing in the green

information disclosure, and attempts to put forward effective solutions.

2.1. The institutional background of green information disclosure

The 1989 Environmental Protection Law stipulates that the government's environmental protection

authorities shall regularly public environmental accident reports (article 11). Projects that

endangering the environment must firstly submit environmental impact assessment reports to

environmental authorities(article 13). The 1989 Environmental Protection Law can be regarded as a

preliminary exploration of environmental information disclosure, but it is limited to a one-way

enterprise-government disclosure pattern. Although the 1989 Environmental Protection Law

regulates that enterprises should bear legal responsibility for environmental pollution, it lacks explicit

requirements on green information disclosure.

In the year 2015, Chinese government issued a new "Environmental Protection Law of the

People's Republic of China" in response to a series of problems facing China's environmental

protection in the new era. The environmental protection supervision and management work has

officially become the examination content of government staff and the result of the examination will

be disclosed to the social public (article 26).Also, the government shall promptly assess the

environmental impact and losses for potential environmental and release the result to the social

public (article 47). The law also adds a separate chapter on information disclosure and public

participation, emphasizing the importance of public disclosure of environmental information.

However, the new Environmental Protection Law only requires enterprises to disclose the discharge

and treatment of major pollutants, no specific guidelines on information disclosure have been issued,

resulting in the lack of comparability of environmental information disclosed by industries.

2.2. Practice of green information disclosure on enterprises

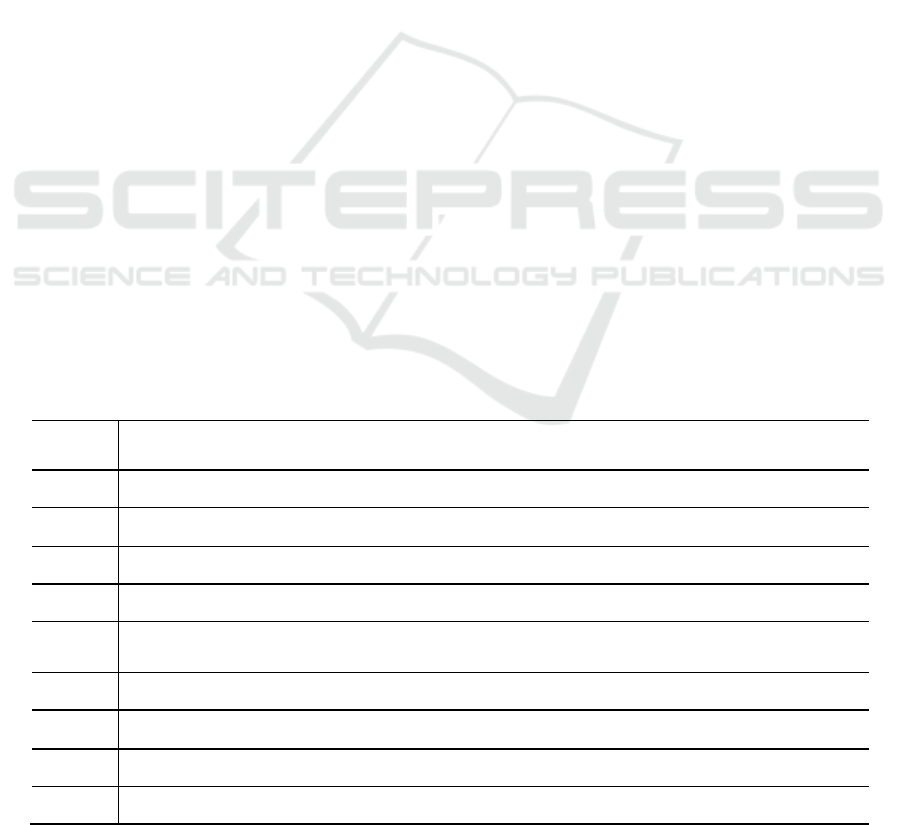

Table 1. The main content of green information disclosure.

Item

number

Content

1

Environmental protection guidelines, annual environmental protection objectives and achievements

2

Total annual resource consumption

3

Information on investment of environmental protection and environmental technology development

4

Type, volume and content of pollutants discharged and where the pollutants are discharged into

5

Information on the handling and disposal of waste generated from production Information on

recycling and comprehensive use of waste products

6

Information on the construction and operation of facilities

7

Voluntary agreement with environmental protection departments

8

Information on performance of social responsibilities

9

Environmental information voluntarily disclosed

Study of Green Information Disclosure on China’s Thermal Power Plants

471

The current green information disclosure forms of listed companies in China mainly include annual

report, CSR report and environment report. Environmental Protection Administration of China

promulgated the "Measures on Open Environmental Information" to encourage enterprises to

voluntarily disclose the environmental information and heavy polluting enterprises mandatorily

demanded to disclose environmental information. Enterprises should announce to public that the

company follows the relevant environmental protection guidelines, company’s annual environment

protection goals and achievements, annual resource consumption, etc., as shown in Table 1:

With the exception of heavily polluting enterprises, companies in other industries tend to use

environmental disclosure as a selective strategy because they have no mandatory requirements. As a

result, hey only disclose information that helps to enhance their corporate image and create a

reputation for their business [22]. In selecting the content for disclosure, they are preferable to give

priority to publicizing information on environmental benefits and social responsibility to the general

public, and to guide the information audience to focus on the positive output produced by enterprises.

This kind of merit-based selection behaviour of enterprises leads to the incompleteness of green

information disclosure content and the non-uniform form of disclosure. After a series of production

processes, a company's products are usually accompanied by negative environmental outputs, such as

sewage and exhaust emissions in addition to products flowing into the market that have a realizable

value. These negative outputs eventually flow to the natural environment and need to be governed

thereby with a large amount of expenditures which makes up the environmental cost of enterprises.

Environmental cost standing at the last link of the production chain is often ignored by enterprises

[23], and rarely reflected in the environmental report, resulting in an imbalance between input and

output.

Most enterprises disclose green information mainly in the form of narratives, lacking descriptions

in physical quantity and market value. So the information disclosed by different enterprises lacks

comparability. Some researches have studied the quality of corporate social responsibility reports

issued by China's transportation industry and found that over 80% of the reports failed to achieve

their aims. One of the reasons is that there is no comparability between reports[24]. Some scholars

use computers to extract and classify the diction of green information disclosed by the enterprises,

then measure the quality of green information disclosure from the perspective of semantic analysis

and find that the industry, property rights and geographical areas will reduce the comparability of

corporate green information disclosure[25]. The reason why the above problems arise is mainly due

to the difficulty of quantifying green information while it is easier for enterprises to describe what

laws and regulations they have followed in protecting the environment, what kinds of green

investment projects are carried out, but the extent and value of such items are difficult to measure.

In this paper, the basic idea of input-output analysis combined with the emergy analysis from eco-

economics is introduced to solve the problem of measurement and disclosure of green accounting

information theoretically. The input-output analysis is mainly used to define the content of green

information which is easily understood when illustrating the disclosure framework of green

information. Emergy is a type of certain energy stored in another kind of energy. Each substance is

formed by a specific kind of energy, and each kind of energy can be converted into the same unit of

measurement (solar emejoules) by emergy transformity. The introduction of emergy analysis aims to

solve the problem of measurement dilemma and incomparability of various sorts of information. This

paper attempts to put forward a full input-full output-full information coverage disclosure framework

to provide potential references for enterprises to disclose green information.

3. Green information disclosure framework based on China's coal-fired thermal power plants

As one of the main energy consuming country, China’s coal-fired thermal power occupies an

important position in the national economic field. Although the government vigorously advocates

clean energy generation in recent years, due to the limitation of capital and technical conditions, coal-

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

472

fired thermal power generation still plays a dominant role. Besides, coal-fired thermal power

generation has a huge impact on environment especially for its pollutant emission. Therefore, this

paper takes coal-fired thermal power generation as an example to discuss the application input-output

framework of green accounting information disclosure.

3.1. The basic idea of input-output analysis on green accounting

Input-output analysis [26] is a quantitative analysis of the interdependence of inputs and outputs

among various parts of an economy. It can be applied to the entire national economy as well as

corporations or specific corporate sector. Input refers to the consumption of raw materials, labor,

machinery and equipment consumed during the production and business activities. Output refers to

the distribution of products after the production process. Application of input-output analysis can

intuitively reflect the internal links of production and operation between various departments of

enterprises. The core idea of input-output analysis in this research can be summarized as substance

conservation, that is, all inputs are outputted in a certain form.

The input and output is imbalanced in modern financial accounting to the aspect of confirmation,

measurement and accounting [27]. Modern financial accounting only contains the cost of monetary

item for the measurement of input, but ignoring the cost of environmental resources. Meanwhile, in

the determination of output, financial accounting only confirm the economic value of the product, but

neglecting the harmful products, resulting in an imbalance between input and output. Green

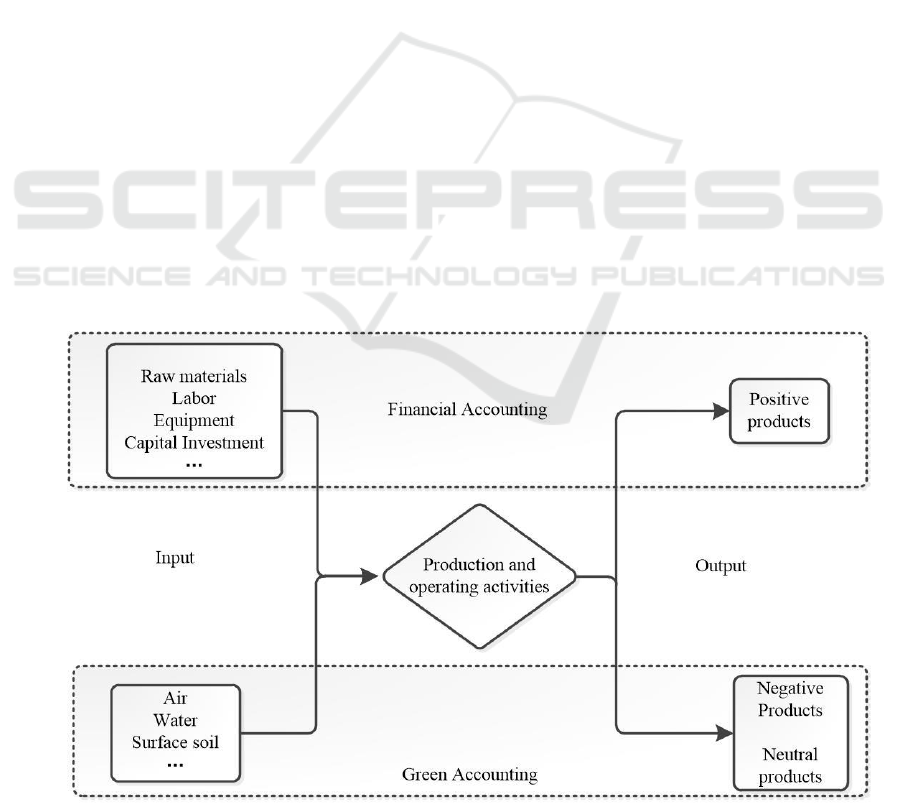

accounting aims to make up for the lack of two deficiencies mentioned above. As shown in Figure 1,

the main difference between green accounting and financial accounting lies in the scope of its

accounting object. Accounting objects for financial accounting include resources available for

production and operation such as raw materials, human resources, machinery and equipment, capital

investment and other quantifiable resources. Output of financial accounting mainly targets in positive

products that eventually enter to the market and help the organization to obtain profits. The object of

green accounting is more extensive, it reflects the use of environmental resources, such as sunlight,

air, surface soil loss, etc. At the same time, green accounting also deals with environmental pollution

of the negative products as well as some neutral products which ultimately discharge into the natural

environment but the degree of damage is not clear.

Figure1. The main difference between green accounting and financial accounting.

Study of Green Information Disclosure on China’s Thermal Power Plants

473

Input-output analysis under the green accounting is a full input-full output-full coverage of

information disclosure method. All resources invested by the enterprise should be outputted in a

certain form. For example, coal is the main raw material inputs of coal-fired power plant which

contains largely of carbon. The final product of coal-burning is disclosed in the form of electricity

energy under the traditional financial accounting framework. However, the carbon element should

also be discharged as CO

x

and eventually emitted to the environment. Although some enterprises

have already mentioned their contributions in regard to the energy conservation and emission

reduction in the annual report, the disclosure is confined to describing whether the emission of CO

x

is

excessive and no specific emission quantity is released. The green accounting approach studied in

this paper aims at using a full coverage information disclosure way to guide enterprises in disclosing

all inputs and outputs so as to achieve a substantial balance between investment and production.

3.2. The main input and output of coal-fired thermal power plants

For the application of input-output analysis on green information disclosure, it is necessary to

understand the production and operation process of all input resources and all output products. This

paper simplifies the generation process of coal-fired thermal power plant from the perspective of

material flow and summarizes the main input items, the flow of direction and the final transformation

forms, which lays the foundation for the green information disclosure.

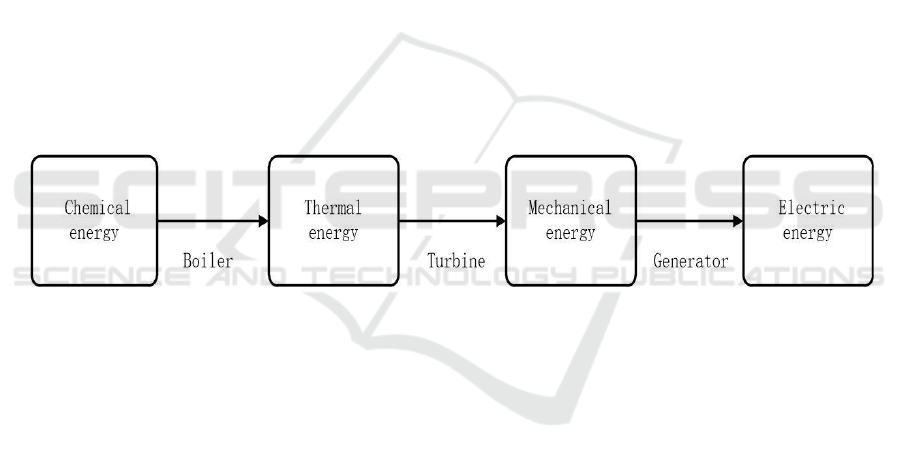

Coal-fired power plant involves four kinds of energy conversion. As shown in figure 2, the

chemical energy of the fuel is firstly transformed into heat energy after being burned in the boiler.

Then, the water absorbs heat energy and becomes steam to drive the steam turbine to generate

mechanical energy. Finally, the generator produces the final product, electric energy.

Figure 2.The energy conversion of coal-fired thermal power generation.

Figure 3 shows the main generation process of coal-fired power plants in China. The main input

resources, flow of directions and the final transformation forms are summarized from the perspective

of material flow. The dotted line in the figure divides it into two parts, with the left side

demonstrating the main input resources and the right side displays the output products. Due to the

diversity in the scale and equipment among different coal-fired thermal power plants in China, the

resource conversion efficiency is uneven. Therefore, this paper assumes that all the input resources

are 100% converted into output in order to theoretically explain the feasibility of the application of

input-output analysis in the green information disclosure.

During the preparation work, coal is pulverized and mixed with air in order to make it sufficient

burning. After that, pulverized coal is sent into the boiler as shown in path ① during combustion

process in which generating heat energy. Heat then converts water into water vapor to drive the

steam turbine. Finally the turbine drives the generator to generate electricity which is mandatorily

disclosed in the corporate annual report as the main source of revenue.

In addition to electrical energy, a large number of by-products are contained in the gas generated

by the boiler. Those by-products are mainly composed of dust, coal cinder and harmful gases (SO

x

,

NO

x

, CO

2

) which are permitted to discharge only after a series of environmental governance

equipment such as desulfurization device, denitration device and dedusting device. Currently, coal-

fired thermal power plants mainly use dust collector to control fly ash pollution, remove sulfur in flue

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

474

gas with desulfurization device, and reduce the formation of nitrogen oxides through the reasonable

design and operation of the boiler.

One of the results of coal burning is the generation of SO

x

, of which SO

2

will have a great harm to

the environment. SO

2

is the main cause of air pollution and acid rain and for now flue gas

desulfurization is considered as the most effective way to control the pollution of SO

2

. As shown in

path ②, the limestone powder is used to wash the flue gas so that the two substances can react to

remove SO

2

and ultimately produce gypsum which can be comprehensively utilized without

secondary pollution. Besides, a small part of incompletely reacted SO

2

will be emitted to the air. In

addition to SO

x

, there is a large amount of NO

x

contained in the boiler gas because of coal

combustion. The NO in the flue gas can be oxidized into NO

2

after being discharged into the

atmosphere, which is very harmful to the human body. As shown in path ③, at present, the catalyst

and certain reductant is mainly used in China to converse NO

x

in the flue gas to N

2

and H

2

O, thereby

reducing the pollution of the environment and releasing only a tiny amount of NO

2

into the

atmosphere. In addition, the slag and ash generated by coal-fired thermal power plants can be

transported to the ash field for secondary utilization after specific treatment, as shown in path ④.

Also, coal combustion produces large amounts of CO

2

and soot as shown in path ⑤. CO

2

emissions

from boilers account for about 30% of China's carbon dioxide emissions which becomes the main

reason for the global warming. At present, the relevant department is actively implementing energy

saving and emission reduction measures to control the emission of CO

2

.

Figure 3. Main generation process of coal-fired power plants.

3.3. Green information disclosure framework of coal-fired thermal power plants

After defining the production process and resource consumed of an enterprise, it is necessary to make

a comprehensive green information disclosure. Under the principle of input-output analysis, the total

Study of Green Information Disclosure on China’s Thermal Power Plants

475

input of an enterprise is equal to the total output. Although these outputs are not necessarily market-

product-specific, they should also be disclosed about their subsequent processing, especially those

that have a negative impact on the environment and require further tracking by enterprise until the

substance enters in nature with minimal impact. Only in this way can the company's green mission be

seen as terminated. Figure 4 shows a preliminary framework for green information based on the idea

of input-output analysis with the example of coal-fired thermal power enterprises.

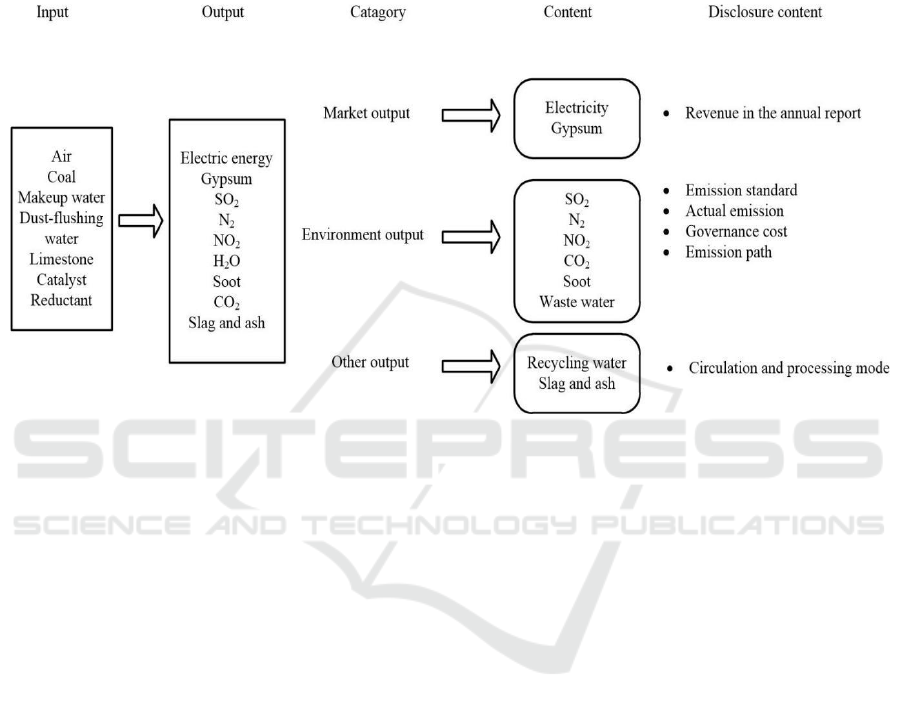

Figure 4. Green information disclosure framework of coal-fired thermal power plant.

On the disclosure of green information, enterprises firstly need to illustrate all the inputs and

outputs in order to facilitate information audiences to understand the whole production and operation

process of enterprises. This is also an initial step to achieve full input-full output- full information

coverage objective. Taking coal-fired thermal power plants as an example (assuming that the

resource conversion efficiency is 100%), as shown in Figure 4, inputs include air, coal, etc. while

outputs refers to electricity, gypsum, etc. All inputs are outputted in a corresponding form.

From the perspective of information disclosure, the total output of enterprises can be divided into

three categories: market output, environment output and other output. Market output means output

flowing to the market. Environment output means output flowing to natural environment and other

output means output flowing in other directions.

For market output such as electricity and gypsum, enterprises can make quantitative information

disclosure in the annual report. Such output secedes from the enterprise information disc losure

process since the sale to a third party, and the financial disclosure mission of the enterprise is

terminated.

For environment output such as N

2

, CO

2

, SO

2

, soot and a portion of waste water, companies need

to disclose the implementation situation of emission standards, actual emissions, governance costs

and emission paths to prove that this part of the environmental output being reasonable followed up.

This also reflects the corporate performance of environmental and social responsibility. When these

emissions are finally disposed into the environment and enter into the natural circulation, the green

mission of the enterprise is terminated.

For other output such as recyclable water, slag and ash temporarily stored, companies need to

explain the circulation and processing mode.

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

476

4. Application of emergy analysis on green information disclosure

The construction of green information disclosure framework aims to initially solve the problem of

incompleteness and inconsistency of green information disclosure. However, in the era of big data,

there is a strong demand on quantitative information. The traditional disclosure of green information

is based on the "discharge list" of emission standards set by the relevant departments, which only

lists the emission of harmful substances. However, because of the differences in units of

measurement between different emission sources, there exists a lack of comparability on various data.

In response to this problem, this paper introduces the method of emergy analysis in the field of

ecological economics in order to solve the problems encountered in the measurement of green

information.

4.1. Introduction of emergy analysis

Emergy analysis is a theory of ecological economics proposed by H.T. Odum [28]. Emergy refers to

a type of certain energy stored in another kind of energy. Emergy analysis assumes that any form of

energy originates from solar energy, so all kinds of energy in the natural environment can be

measured in a unified unit which is solar emejoules (sej). In the eco-economy, all sorts of energy and

materials with different units can be converted into the same unit of measure through emergy

transformity so that they can be quantitatively measured and compared to analyze the real benefits of

environmental resources.

Emergy theory regards the ecosystem as a self-organizing energy system which is similar to the

flow of the food chain. The energy is accompanied by a certain amount of loss at every stage of

economic production. Therefore, as the energy goes from a low level (solar energy) to a high level

(consumer energy at different stage of conversion), the amount of energy showed a declining trend,

while the energy level is increasing. In an eco-economic system, the energy flow always flows from a

low energy level (such as solar energy) to a high energy level (such as electricity) [29].

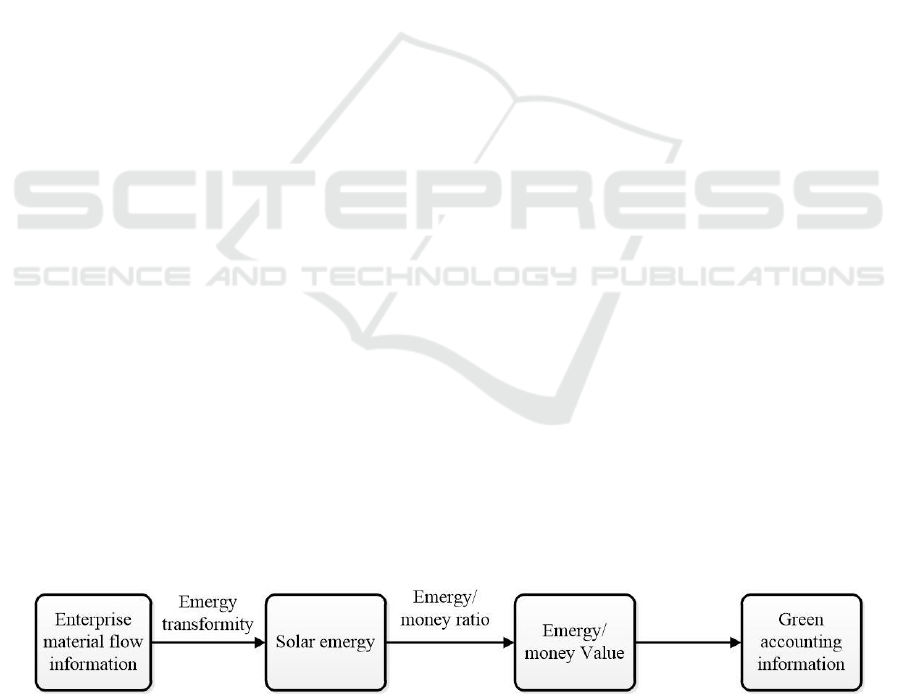

4.2. Application of emergy analysis on green information disclosure framework

One of the biggest problems in green accounting when disclosing information is the inability to

quantify the resources. The use of emergy theory may help to solve this problem. Although all the

inputs and outputs have been summarized in the green information disclosure framework shown in

Figure 4, the units for various kinds of substances are different (for example, coal is measured in tons

and wastewater is measured in cubic meters), resulting in the lack of comparability between them

which is not conducive to evaluate and compare enterprise's environmental protection performance.

Therefore, as shown in Figure 5, after obtaining all the input and output data information of an eco-

economic system, resources of different units can be first converted into solar emejoules. This step

needs to use the emergy transformity as a conversion intermediary. Emergy transformity is the

amount of another energy contained per unit of a material or energy. In emergy analysis, the

commonly used transformity is solar transformity which is the the amount of solar energy contained

per unit of a material or energy .The solar transformity increases as the energy level increases.

Figure 5. Application of emergy analysis on green information disclosure framework.

After converting the physical consumption into the same unit through the conversion of the

emergy transformity, the solar emejoules obtained is still a material unit and cannot become the

Study of Green Information Disclosure on China’s Thermal Power Plants

477

financial information commonly understood by the majority of investors. Therefore, further

conversion through the emergy / money ratio is required. The emergy / money ratio is the ratio of the

total annual energy value of a country or region divided by GDP of that country or region in a year.

The higher the ratio, the greater the emergy wealth can be exchanged by the individual units, the

greater the proportion of natural resources made up in the national economy. This often indicates that

the country or region has a strong dependence on environmental resources, and such features are

usually found in the extensive economies [30].

As shown in figure 5, it is known that the solar emejoules of a certain substance can be converted

into the corresponding monetary value, that is, quantified green accounting information through the

emergy /money ratio. Thereby, investors can be conducted to compare various resources consumed

by an enterprise through unified calculation of different kinds of results. It should be noted that the

monetary value is different from the currency used in traditional financial reports. The value of the

monetary value in emergy analysis refers to the equivalent market value of the currency rather than

the actual cost of purchasing such resources.

5. Conclusions

As an emerging branch of management accounting, the implementation of green accounting mainly

focuses on the disclosure of green information. However, although the concept of green accounting

has been proposed in China for a long time, there is a lack of a unified framework and method to

apply green information to the practice of enterprises.

This paper aims to combine the basic idea of input-output analysis, take the green information

disclosure of China's coal-fired thermal power plants as an example, apply the method of emergy

analysis from ecological economics to the disclosure of information in green accounting and try to

provide a unified enterprise disclosure framework of green accounting. First of all, through the

research on the status quo of China's green information disclosure, it is found that there are some

problems in the disclosure of green information in China, such as incompleteness in disclosure

content and difficulty in measurement. In view of the above dilemma, this paper puts forward a

tentative idea of setting up a green information disclosing framework by using the input-output

analysis. After making clear of the production process and material inputs and outputs of an

enterprises, this paper attempts to set up an information disclosure framework with full input-full

output-full information coverage assumption. In addition, for the measurement of green information

disclosure, this research introduces the theory of emergy analysis from eco-economics into the

framework of green information disclosure and attempts to convert all input and output substances

into a unified unit of measurement in order to evaluate the green information preferably.

However, this article also has some shortcomings in the method of the research. Taking the

Chinese coal-fired thermal power generation plants as an example, the green information disclosure

framework set up in this paper may have some omissions in the recognition of input and output

substances due to professional constraints when taking the Chinese coal-fired thermal power

generation plants as an example. Such defect may cause some scalability of the disclosure content of

green information. Secondly, this paper proposes that emergy analysis method can measure all the

input and output of enterprises theoretically. However, this method has not been widely used in

China at present, and the data collection needs a lot of costs. Therefore, its application effect needs to

be further studied.

Acknowledgment

My deepest gratitude goes first and foremost to Professor Li , my supervisor, for his constant

encouragement and guidance. He has walked me through all the stages of the writing of this paper.

Without his consistent and illuminating instruction, this thesis could not have reached its present

form. Second, I would like to express my heartfelt gratitude to Yang Liu of Institute of finance and

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

478

economics, who has instructed and helped me a lot during the past few months. I also owe my sincere

gratitude to my friends and family who gave me their help and time in listening to me and helping me

to work out my problems during the difficult course of the thesis.

References

[1] Wu C W, Yang T and Leon O C 2017 Study on transformation of ideas of environmental

protection administration and construction of ecological civilization in China Int. J.

Bifurcation Chaos. 6 455

[2] Wei Z, Shen H, Zhou K Z and Li J J 2017 How Does Environmental Corporate Social

Responsibility Matter in a Dysfunctional Institutional Environment? Evidence from China J.

Bus. Ethics 140 209-223

[3] Ernst & Young and Boston College Centre 2013 Value of sustainability reporting EYGM

Limited pp 1-30

[4] Schaltegger S and Burritt R 2000 Contemporary Environmental Accounting: Issues, Concepts

and Practice Corp. Soc. Resp. Environ. Manage. 2 288

[5] Beams F A and Fertig P E 1971 Pollution Control Through Social Cost Conversion J. Account.

37-42

[6] Marlin J T 1973 Pollution of the accounting issues J. Account. 18-22

[7] UN Statistics Division Environment Statistics Section 1993 Integrated environment and

economic accounting an operational manual United Nations(New York)

[8] UNDFS Development 2001 Environmental management accounting procedures and

principles United Nations Publication(New York)

[9] Gale R 2006 Environmental costs at a Canadian paper mill: a case study in environmental

management accounting (EMA) J. Clean. Prod. 14 1237-51.

[10] Martina L, Jacqueline B and Andrew G 2015 The role of accounting in supporting adaptation

to climate change Account. Financ. 55 607-625

[11] Frost G R and Wilmshurst T D 2000 The Adoption of Environment‐related management

accounting: an analysis of corporate environmental sensitivity Account. Forum 24 344-365

[12] Frank Figge and Tobias Hahn 2013 Value drivers of corporate eco-efficiency:Management

accounting information for the efficient use of environmental resources Manage. Account.

Res. 24 387–400

[13] Christ K L and Burritt R L 2013 Environmental management accounting: the significance of

contingent variables for adoption J. Clean. Prod. 41 163-173

[14] Kapardis M K and Setthasakko W 2013 Barriers to the development of environmental

management accounting Euromed J. Bus. 5 15-331

[15] Mokhtar N, Jusoh R and Zulkifli N 2016 Corporate characteristics and environmental

management accounting (EMA) implementation: evidence from Malaysian public listed

companies (PLCs) J. Clean. Prod. 136 111-122

[16] Xie M and Tang W 2016 The research on environmental accounting information disclosure of

Chinese listed companies in the steel industry International Conference on Service Systems

& Service Management

[17] Ge J S and Li R S 1992 A New trend of thought in western accounting theory in the 1990s -

green accounting theory Account. Res. 1-6

[18] Xu J L and Cai C L 2004 Review and prospect of China’s environmental accounting research

Account. Res. 87-92

[19] Xiao X and Zhou Z F 2012 Research on enterprises’ environmental risk management and

environment debt evaluation framework Audit Econ. Res. 27 33-40

[20] Zhang H L, Zhu Y L and Jiang H Q 2016 Study on the preperation method of enterprises’

environmental balance sheet Friends Account. 23-29

Study of Green Information Disclosure on China’s Thermal Power Plants

479

[21] Fuente J A, García-Sanchez I M and Lozano M B 2017 The role of the board of directors in

the adoption of GRI guidelines for the disclosure of CSR information J. Clean. Prod. 141

737-705

[22] Huang R and Chen D 2015 Does Environmental Information Disclosure Benefit Waste

Discharge Reduction? Evidence from China J. Bus. Ethics 129 535-552

[23] Noodezh H R and Moghimi S 2015 Environmental Costs and Environmental Information

Disclosure in the Accounting Systems Int. J. Academic Res. Account. Finance Manage. Sci.

5 13-18

[24] Qi L Y, Zhang B B and Li T F 2016 Research on the quality evaluation of corporate social

responsibility report Sci. Res. Manage. 644-651

[25] Zhang X M, Wang J, Xue Y and Li X L 2016 Application of semantic analysis in the study of

enterprises’ environmental information disclosure Account. Res. 87-94

[26] Leontief W W 1936 Quantitative Input and Output Relations in the Economic Systems of the

United States Rev. Econ. Stat. 18 105-125

[27] Jasch C 2006 Environmental management accounting (EMA) as the next step in the evolution

of management accounting J. Clean. Prod. 14 1190-93

[28] Odum H T 1983 Energy Analysis Overview of Nations Working Paper(Laxenburg Austria)

International Institute for Applied System

[29] Odum H T 2000 Emergy evaluation of an OTEC electrical power system Energy 25 389-393

[30] Lan S F and Qin P 2001 Emergy analysis of ecological economy system Chin. J Appl. Eco. 12

129-131

IWEMSE 2018 - International Workshop on Environmental Management, Science and Engineering

480