Generalized Dirichlet Regression and other Compositional Models with

Application to Market-share Data Mining of Information Technology

Companies

Divya Ankam

a

and Nizar Bouguila

b

CIISE, Concordia University, Montreal, Canada

Keywords:

Compositional Data, Dirichlet Regression, Generalized Dirichlet, Market-shares, Financial Data Mining.

Abstract:

We explore the idea that market-shares of any given company have a linear relationship with the number of

times the company/product is searched for on the internet. This relationship is critical in deducing whether the

funds spent by a firm on advertisements have been fruitful in increasing the market-share of the company. To

deduce the expenditure on advertisement, we consider google-trends as a replacement resource. We propose a

novel regression algorithm, generalized Dirichlet regression, to solve the resulting problem with information

from three different information-technology fields: internet browsers, mobile phones and social networks.

Our algorithm is compared to Dirichlet regression and ordinary-least-squares regression with compositional

transformations. Our results show both the relationship between market-shares and google-trends, and the

efficiency of generalized Dirichlet regression model.

1 INTRODUCTION

Our aim is to predict the change in market-share

(Morais et al., 2018) (Tay and Mc Carthy, 1991) com-

position with respect to share-of-voice on social me-

dia. We assume it is directly proportional to the in-

vestment in marketing. We are making a strong as-

sumption that the google trends are a result of the

user’s search which were guided by advertisements

and people talking about the company/product. We

can thus deduce it to be directly proportional to the

money the company spends on advertising the prod-

uct (Cantner et al., 2012). The insider information

on the companies spendings on advertisements is not

readily available, though it would be a valuable piece

of information to have, it is confidential and the com-

panies are not obliged to disclose it. It could also give

the competitors an edge. Google-trends provides data

on ”interest over time” of the respective companies.

This could be a good measure of share-of-voice for

the company. This will be the independent predictor.

Market share (Moraisab et al., 2016) (Dussauge et al.,

2002) of company or similar data can be obtained as

a monthly statistic for few years. This will be propor-

tional data, assumed to follow a generalized Dirichlet

a

https://orcid.org/0000-0002-6898-4953

b

https://orcid.org/0000-0001-7224-7940

distribution (Fan and Bouguila, 2013b) (Bouguila and

Ziou, 2004b). This will be the prediction.

Mathematically compositional data (Aitchison,

1982) (Fan et al., 2013) are represented in a standard

simplex of the sample space given by,

S

D

= {x = [x

1

,x

2

,...,x

D

] ∈ R

D

} (1)

where x

i

> 0,i = 1, . . . , D and

∑

D

i=1

x

i

= k ; x is a D-

dimensional vector of features representing a given

object (e.g. document, image, video, etc.) and k is

a constant.

Regression problems based on compositional data

can be categorized into 2 groups. In the first group

the dependant variable is compositional (Ankam and

Bouguila, 2018), such problems have been solved

by using Aitchison’s geometric transformations. In

the second group the response variables are composi-

tional, with either same or different predictors. The

latter type of problems is more complex and this is

what we have tackled in this paper. So far, Dirichlet

regression (Maier, 2014) (Bouguila and Ziou, 2004a)

has been the best approach in the industry to define

compositional regression problems where the depen-

dent variables are compositional.

In this paper, we develop generalized Dirichlet

(GD) regression, where the dependent variables fol-

low a generalized Dirichlet distribution (Zhang et al.,

2017) (Bouguila and Ziou, 2006). With double the

158

Ankam, D. and Bouguila, N.

Generalized Dirichlet Regression and other Compositional Models with Application to Market-share Data Mining of Information Technology Companies.

DOI: 10.5220/0007708201580166

In Proceedings of the 21st International Conference on Enterprise Information Systems (ICEIS 2019), pages 158-166

ISBN: 978-989-758-372-8

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

number of parameters to estimate in comparison with

the Dirichlet, GD is more versatile and gives space to

model a flexible line of fit. We show how data fit-

ting can be done by using a geometric transformation

that reduces the generalized Dirichlet into a product

of Beta distributions.

The rest of the paper describes the main crux of

our research, it will answer the pinching question,

will the Google trends be able to predict the rise and

fall of shares in any given field? To demonstrate the

same, we have chosen the following three interesting

quintessential markets of the modern world, related

to technology and communication, mobile vendors in

Canada, social network sites in India and what is the

most used browser in the world! Let’s explore this

case and discuss how successful is Google-trends in

predicting the trends of the share markets. Section 2

describes the machine learning algorithms employed

for the research. Section 2.3.3 explains our contribu-

tion in devising the GD regression algorithm. Section

3 gives the background for experimental set-up. Sec-

tion 4 shows our results and analysis. We conclude

with Section 5.

2 MACHINE LEARNING

TECHNIQUES

In this section we discuss the various ML algorithms

used in our research. They are explained in the in-

creasing order of computational complexity. Start-

ing from ordinary least squares with a combination of

transformations like clr and ilr. After which we de-

scribe Beta regression, Dirichlet regression and gen-

eralised Dirichlet regression.

2.1 OLS - Ordinary Least Squares

Regression

Ordinary least squares (OLS) regression is a case of

generalized linear modelling algorithm. It employs

linear least squares method for estimating a single re-

sponse variable. It could be multivariate of single in-

dependant variable x, to predict the response (Fox and

Monette, 2002). Principle of least squares minimizes

the sum of squares of the differences between the ac-

tual response y, in the given data and prediction of the

linear function (Hutcheson, 2011). If we consider a

linear system of variables, with n data points:

n

∑

j=1

X

i j

β

j

= y

i

,(i = 1,2,...,m) (2)

here β is the regression co-efficient

Xβ = y (3)

where

X =

X

11

X

12

··· X

1n

X

21

X

22

··· X

2n

.

.

.

.

.

.

.

.

.

.

.

.

X

m1

X

m2

··· X

mn

,

β =

β

1

β

2

.

.

.

β

n

,y =

y

1

y

2

.

.

.

y

m

(4)

Such a system usually has no arithmetic solution,

rather the aim is to find the best coefficients β which

better fit the equations, to solve the quadratic mini-

mization problem

ˆ

β = argmin

β

S(β) (5)

where the objective function S is given by

S(β) =

∑

m

i=1

y

i

−

∑

n

j=1

X

i j

β

j

2

= ky −Xβk

2

(6)

Finally,

ˆ

β is the coefficient vector of the least-squares

hyperplane, expressed as a product of Gramiam ma-

trix of X and moment matrix of regressors:

ˆ

β =

X

T

X

−1

X

T

y (7)

2.2 Aitchison Transformations

In the share market case, both dependent and in-

dependent variables are compositional. Hence both

are transformed to the Aitchison plane by applying

the transformations explained below. Then, they are

fed to ordinary least squares regression algorithm

(ols). The resultant matrix is transformed back to

Euclidean plane by applying an inverse transform.

Then, the actual and predicted values are compared

against the selection criteria explained in section 3.2.

We discuss two Aitchison transformations (Aitchison,

1982), CLR (centred log ratio transform) and ILR

(Isometric log ratio transform). These are widely used

in the case of compositional data.

2.2.1 Centered Log Ratio (CLR) + OLS

CLR is defined as:

y = (y

1

,...,y

D

)

0

=

ln

x

1

D

q

∏

D

i=1

x

i

,...,ln

x

D

D

q

∏

D

i=1

x

i

!

0

(8)

Generalized Dirichlet Regression and other Compositional Models with Application to Market-share Data Mining of Information

Technology Companies

159

CLR can also be represented as follows

y = {y

i

}

i=1,...,D

=

n

ln

x

i

g(x)

o

i=1,...,D

(9)

g(x) =

D

∏

j=1

x

j

1/D

(10)

Here g(x) is the geometric mean of the composition.

Resulting in D variables, each representing one com-

ponent of the original compositional part. Individual

contribution of each part is easily interpretable. Sub-

compositional incoherence and generation of singular

matrix are the drawbacks of CLR. Singular data is in-

compatible with most of the present statistical analy-

sis methods. This can be overcame by ILR transfor-

mation.

2.2.2 Isometric Log Ratio (ILR) + OLS

ILR is defined as:

z

i

=

r

D − i

D − i + 1

ln

x

i

D−i

q

∏

D

j=i+1

x

j

,i = 1,...,D − 1

(11)

This results in D − 1 coordinates in a chosen or-

thonormal basis. It represents only the ratios between

the components. ILR can also be represented in terms

of CLR as

z = Hy (12)

Where H is the Helmert sub- matrix, obtained by re-

moving the first row of Helmert matrix (Lancaster,

1965). H is a popular orthonormal basis. ILR is ap-

plied on data matrix X, subsequent ILR co-ordinates Z

are fed into the OLS algorithm in section 2.1. The re-

gression coefficient matrix thus obtained, using equa-

tion (3) is γ, has (D − 1) x n dimensions. When sub-

stituted in equation above, the predictor variables Y

are obtained.

2.3 Distributions-based Regression

2.3.1 Beta Regression

Assuming the response data is Beta distributed (Bayes

et al., 2012), The authors in (Ferrari and Cribari-Neto,

2004) have proposed a regression model with mean

and dispersion parameters of the distribution. In con-

trary to the transformed response of a linear regres-

sion, Beta regression’s parameters are deduced using

maximum likelihood estimation. The Beta density

function is given as follows:

Y ∼ B(p,q), f (y; p, q) =

Γ(p + q)

Γ(p)Γ(q)

y

p−1

(1 − y)

q−1

(13)

Maximum likelihood estimation is performed to de-

duce the values of p and q. The closed form solution

to this equation is given in (Ferrari and Cribari-Neto,

2004). The partial derivatives of log of Beta distribu-

tion with respect to p and q are given by

∂log f (y; p,q)

∂p

= ψ(p + q) − ψ(p) + log y (14)

∂log f (y; p,q)

∂q

= ψ(p + q) −ψ(q) + log(1 − y) (15)

Where ψ(.) is the digamma function defined as

Γ(x) =

Z

∞

0

t

x−1

exp(−t)dt (16)

The expected score equals zero, it can be re-written

as:

E[logY ] = ψ(p) − ψ(p + q) (17)

E[log(1 −Y )] = ψ(q)− ψ(p + q) (18)

The distribution of response variable Y

i

is B (p

i

,q

i

)

where p

i

and q

i

are, for each i, described by sets of

explanatory variables (x

1

,...,x

m

) and (v

1

,...,v

M

) as

p

i

= g(β

1

x

1i

+ ··· + β

m

x

mi

) (19)

q

i

= h(γ

1

v

1i

+ ··· + γ

M

v

Mi

) (20)

Here g and h are link functions. The above equations

can be substituted in the log likelihood equation of

Beta distribution

`(θ) =

n

∑

i=1

logΓ(p

i

+ q

i

) −

n

∑

i=1

logΓ(p

i

) −

n

∑

i=1

logΓ(q

i

)

+

n

∑

i=1

p

i

logy

i

+

n

∑

i=1

q

i

log(1 − y

i

)

(21)

Whose first order derivatives are given by

∂`

∂β

r

=

n

∑

i=1

g

0

i

x

ri

[ψ(p

i

+ q

i

) − ψ (p

i

) + log y

i

]

∂`

∂γ

R

=

n

∑

i=1

h

0

i

v

Ri

[ψ(p

i

+ q

i

) − ψ (q

i

) + log (1 − y

i

)]

(22)

Maximum likelihood estimation of β and γ are ob-

tained by solving the above equations, equating to

zero. Thus, the regression parameters are obtained.

They can be multivariate or univariate, depending on

the application. It has to be noted that, in the case

of compositional data, where the predicted values are

more than one, the Beta regression needs to be ex-

tended to accommodate the prediction of multiple de-

pendant variables. This is explored in the further two

sections, Dirichlet regression and generalized Dirich-

let regression.

ICEIS 2019 - 21st International Conference on Enterprise Information Systems

160

2.3.2 Dirichlet Regression

Marco J Maier has proposed Dirichlet regression

(Maier, 2014) (Hijazi and Jernigan, 2009), which as-

sumes the dependent variables are compositional and

follow a Dirichlet distribution. He has deduced a

framework similar to general linear models for regres-

sion of Dirichlet distributed data. Dirichlet distribu-

tion is a generalized form of Beta distribution (Fan

and Bouguila, 2013a), defined in equation 23. Also

known as common parametrization.

D(y|α) =

1

B(α)

C

∏

c=1

y

(a

c

−1)

c

(23)

where B(α) =

C

∏

c−1

Γ(α

c

)/Γ

C

∑

c−1

α

c

!

(24)

and Γ(x) =

Z

∞

0

t

x−1

exp(−t)dt (25)

Alternately, Dirichlet distribution can also be repre-

sented as a function of mean µ and variance φ as in

equation 26, called alternate parametrization.

f (y|µ,φ) =

1

B(µφ)

C

∏

c=1

y

(µ

c

φ−1)

c

(26)

The full log-likelihood of the commonly parametrized

model is defined below

`

c

(y|α) = log Γ

C

∑

c=1

α

c

!

−

C

∑

c=1

logΓ (α

c

) +

C

∑

c=1

(α

c

− 1)log (y

c

)

(27)

The crucial part of converting a Dirichlet distribution

to a Dirichlet regression problem, lies in the link be-

tween the Dirichlet parameters (α) and the regression

parameters (β). The link function g(.) is selected as a

log(.) function, defined as

g(α

c

) = η

c

= X

[c]

β

[c]

(28)

The first order derivative of the log-likelihood:

∂`

c

∂β

[d]

m

= x

[c]

m

α

[d]

"

log

y

[d]

− ψ

α

[d]

+ ψ

C

∑

c=1

α

[c]

!#

(29)

The second order derivatives of the log-likelihood

with respect to βs on the same and different variables

are given below. The Hessian matrix of the same can

be obtained from (Maier, 2014).

∂

2

`

c

∂β

[d]

m

∂β

[d]

n

= x

[d]

m

x

[d]

n

α

[d]

(

log(y

d

) + ψ

C

∑

c=1

α

c

!

− K

)

(30)

K = ψ(α

d

) − α

d

"

ψ

1

C

∑

c=1

α

c

!

− ψ

1

(α

d

)

#

(31)

∂

2

`

c

∂β

[d]

m

∂β

[e]

n

= x

[d]

m

x

[e]

n

α

d

α

e

ψ

1

C

∑

c=1

α

c

!

(32)

Caution is to be taken to resist the urge to calculate α

of the Dirichlet distributed dependent variables. As

this is not the desired output, We are more interested

in calculating the regression parameters β, which

will be found only after relating it to α in the link

function. The maximum log-likelihood estimation

(MLE) of Dirichlet regression is different from that

of Dirichlet distribution MLE.

2.3.3 Generalized Dirichlet (GD) Regression

We now propose generalized Dirichlet regression to

solve the compositional regression problems of inter-

est. This distribution has double the number of pa-

rameters to estimate compared to Dirichlet distribu-

tion. This gives it more degrees of freedom to fit the

data in a better way. It’s probability density function

is as follows

c

n

∏

i=1

x

a

i

−1

i

1 −

i

∑

k=1

x

k

!

b

i

−1

(33)

To evaluate the normalizing constant c, we integrate

sequentially over x

n

,x

n−1

,...,x

2

,x

1

, where n is the

number of components of x.

c =

n

∏

i=1

Γ(1 +

∑

n

k=i

(a

k

+ b

k

− 1))

Γ(a

i

)Γ

b

i

+

∑

n

k=i+1

(a

k

+ b

k

− 1)

(34)

In an n dimensional GD distributed data, there are

2n variables to estimate. There would be 2n log-

likelihood equations to solve simultaneously. (Chang

et al., 2010) demonstrate that GD can be transformed

to n Beta distributions. Suppose (X

1

,...,X

n

) ∼

GD(a

1

,...,a

n

;b

1

,...,b

n

) Where Zi = Zi...Zn are n

mutually independent Beta distributed variables

Z

i

∼ B (a

i

,b

i

+(

n

∑

k=i+1

(b

k

+ a

k

− 1)),i = 1,...,n (35)

(X

1

,...,X

n

) ,

Z

1

,Z

2

(1 − Z

1

),...,Z

n

n−1

∏

i=1

(1 − Z

i

)

!

(36)

It follows that the problem can be reduced to n-

likelihood equations in pairs.

Z

i

= X

i

/

1 −

i−1

∑

j=1

X

j

!

∼ B(a

i

,c

i

) (37)

where i = 1,..., n for a random sample

(X

1 j

,...,X

n j

), j = 1, . . . , N, from X

1

,...,X

n

the

Generalized Dirichlet Regression and other Compositional Models with Application to Market-share Data Mining of Information

Technology Companies

161

corresponding log-likelihood function can be

expressed as follows:

N

∏

l=1

n

∏

i=1

Γ(a

i

+ c

i

)

Γ(a

i

)Γ (c

i

)

x

il

1 −

∑

i−1

j=1

x

jl

!

a

i

−1

∑

i

j=1

x

jl

1 −

∑

i−1

j=1

x

jl

!

c

i

−1

(38)

The first order derivatives of MLE are n pairs, where

i = 1,...,n is below:

0 =

∂logL

∂a

i

= ψ(a

i

)−ψ(a

i

+ c

i

)−

1

N

N

∑

l=1

logx

il

(39)

0 =

∂logL

∂c

i

= ψ(c

i

) − ψ (a

i

+ c

i

) −

1

N

N

∑

l=1

log(1 − x

il

)

(40)

Since a Dirichlet MLE has been transformed to n

Beta MLE, we will follow the steps in section 2.3.1 to

convert the Beta distribution to Beta regression esti-

mates using link function. Various link functions can

be used to relate the dependent variables to indepen-

dent variable, for example, log-link, logit-link, probit,

log-log link.

There is no closed form solutions for the above

equations. Newton-Raphson iteration is employed to

arrive at the solution in maximum likelihood estima-

tion. The initial values are obtained from method of

moments estimates. The estimated values of regres-

sion are normalised to equate to 1 as the expectation

is compositional data.

3 EXPERIMENTAL SET-UP

3.1 k-fold Cross Validation

Our aim is to create a replica of the underlying model

generating the data. The approach we follow is to

work backwards from the collected data. In the pro-

cess, there is a danger of over-fitting/under-fitting the

data. Which means, the model is created specifically

around the given data. Any newly generated data,

even though coming from the same source, will not

be described with this model. To overcome this is-

sue, we have used the method of k-fold cross valida-

tion (Watt et al., 2016). It is a systematic hold out

method, where the data is splitted into k parts. over a

loop of k times, each part is held out for testing and

the model is trained over the remaining data (total-kth

part). This way k different models are created, and the

features are averaged over the k models. This gives

equal opportunity for the data being represented fully

compared to randomized hold-out cross validation.

The k-fold algorithm is used to compute the av-

erage of evaluation measures, and it is called 1000

times to average out the measures over the different

partitions. Thus, each dataset is modelled 1000*10

times, that is 10,000 times for a 10-fold cross vali-

dation. This is the most computationally expensive

component of the regression problem we are solving.

Algorithm 1: k-fold cross-validation pseudo-code.

Input Dataset, number of folds k,

Split the data into k equally sized (rounded to

integer) folds

1: procedure K-FOLD-REGRESSION

2: for <s = 1:k> do

3: Train a model on sth fold’s training set

4: Test the model on sth fold’s test set

5: Compute corresponding evaluation measures

6: Compute average of evaluation measures of

all k sets

3.2 Evaluation Measures

The goodness of fit of the regression models need to

be measurable. This helps us decide which model

is able to describe the data best. Since we are deal-

ing with compositional data, the regular measures of

regression need to be modified accordingly, There

are various measures explained in (Hijazi, 2006).

The efficacy of the learned models is compared with

these three parameters, sum of square of residuals, R-

squared measure based on total variability and KL di-

vergence.

3.2.1 R-squared Measure based on Total

Variability (R2T)

The term total variability based R square measure

was coined by Aitchison in the log ratio analy-

sis[Aitchison 1986]. It is defined as the ratio of total

variance in the predicted values to the total variance

in the actual values.

R

2

T

= totvar(

b

x)/totvar(x) (41)

T(x) = [τ

i j

] =

var

log(x

i

/x

j

)

(42)

totvar(x) =

1

2d

∑

T(x) (43)

3.2.2 Residual Sum of Squares (RSS)

Residual sum of squares (RSS) (Draper and Smith,

2014) is defined as the square of the difference be-

tween the predicted and actual values for each point

ICEIS 2019 - 21st International Conference on Enterprise Information Systems

162

in test set. In the compositional case, the sum of each

component’s RSS is summed up.

RSS =

n

∑

i=1

(y

i

−

b

y

i

)

2

(44)

3.2.3 Kullback-Leibler Divergence (KL)

KL divergence is the sum of ratio of the logarithm of

actual values o fitted values, weighed by the actual,

over each data point(Kullback and Leibler, 1951).

Minimum KL divergence is desired as it deduces

maximum likelihood (Haaf et al., 2014).

KL(S,

b

S) =

T

∑

t=1

D

∑

j=1

log

S

jt

b

S

jt

!

S

jt

(45)

KL divergence adapted to compositional data is de-

fined as follows (Martin-Fernandez et al., 1999):

KLC(S,

b

S) =

D

2

KL

0

D

,S

b

S

+ KL

0

D

,

b

S S

(46)

=

D

2

T

∑

t=1

log

S

t

/

b

S

t

·

b

S

t

/S

t

(47)

4 DATASETS AND RESULTS

In order to assess the usefulness of the regression

models,we have investigated 2 real-life data sets fol-

lowed by 3 different applications based on data col-

lected from real-life sources. The market shares data

are obtained from global-stats

1

website, the relation

we are trying to observe is the company’s market-

share to their trends in google-searches

2

, which is a

good measure of the company’s investment in adver-

tising.

4.1 Real Data

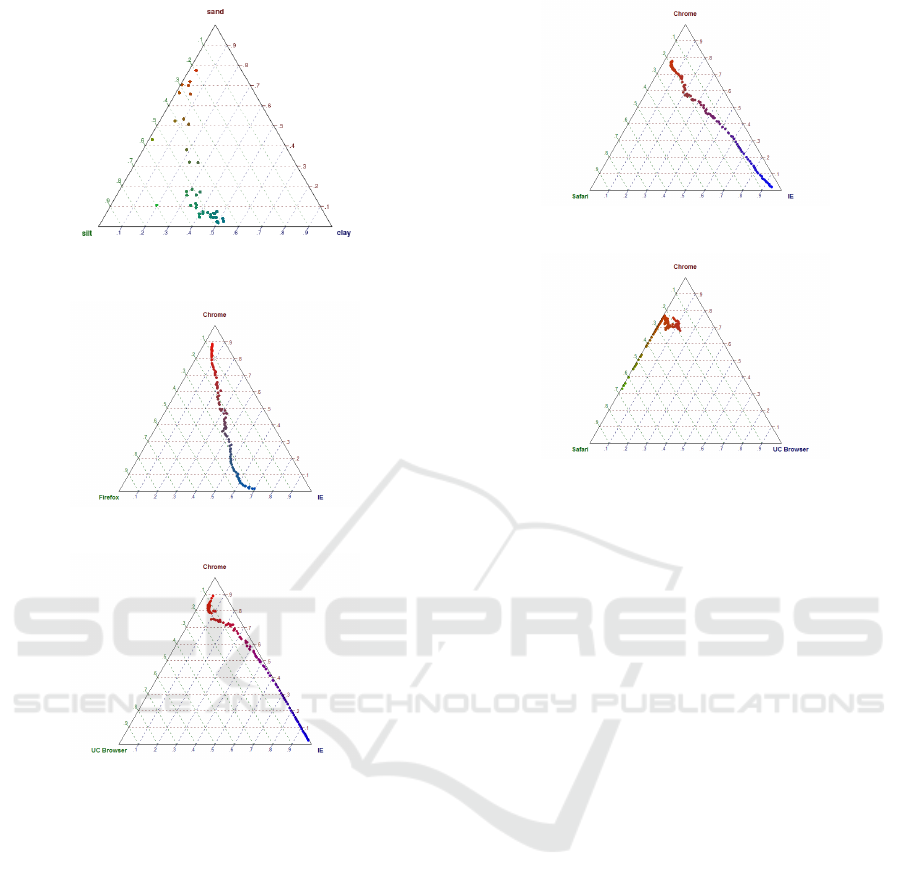

4.1.1 Arctic Lake Soil Compositions Dataset

We discuss Arctic lake data set, which shows how the

composition of ground soil comprising of silt, sand

and clay is altered as the depth of lake increases. This

is a famous dataset used by Aitchison to investigate

many transformations. It has been quoted in stud-

ies, like zero value substitution (Tsagris and Stewart,

2018) (Tsagris, 2015) and robustness checks (Tsagris,

2015). There are 39 data points with three compo-

nents. The distribution of the data points is shown in

1

http://gs.statcounter.com

2

https://trends.google.com/trends/

ternary diagram, Figure 1. Unlike most regression

problems, with a single response variable and multi-

ple independent variables, the Arctic lake data is dif-

ferent. It has a single independent variable (x) and

three different response variables, whose sum adds up

to unity. It is the compositions that we are predicting.

We could use a variety of arithmetic transformations

of x, like log(x), x

2

, x + x

2

. Table 1 shows the regres-

sion measures of the different regression algorithms

explained in the above sections. GD regression has

least residual sum of squares, which represents a good

fit. Dirichlet regression is the best in this case, given

R2T and KL divergence measures.

4.1.2 Glass Composition Dataset

Another dataset containing more number of composi-

tions is the forensic glass dataset (Tsagris and Stew-

art, 2018). It has 8 components and 214 observations.

They are are all dependant on a single parameter, the

refractive index (RI) of glass. The aim is to map how

the refractive index of glass can alter the composition

of glass, the minerals in it, like Aluminium, magne-

sium to name a few. The regression should ideally

appear the other way round, the RI is determined by

the composition. But, we are doing the reverse pro-

cess to see if we can find the required composition to

be able to manufacture/recreate the intended RI. As

per the results in Table 2, least SSR is by GD regres-

sion algorithm. Better KL divergence is shown by the

classical OLS methods, this could be due to the un-

equal distribution of metals in the glass. Some metals

like Silicon and Sodium have high compositions com-

pared to the rest.

4.2 Application - Market Shares for

Information Technology Companies

For future researchers to be able to reproduce our

work, we have chosen the public platform of google-

trends (Choi and Varian, 2012) (Vosen and Schmidt,

2011). It gives us a very good idea on how the data

search has spiked over the given time range, which is

of prime importance. Here have been a couple of ex-

periments done to see if any lag in trends and share is

observed. Trends seems to be more real time and the

data seemed to be more relevant to the current mar-

ket share. A lag of two months is observed between

the trends and market shares. The companies invest-

ment on advertisements seem to have been fruitful a

couple of months later in getting the google clicks

and thus for it to show effect on the market share.

We would further like to explain how the shares have

changed over the time, any interesting patterns are ex-

Generalized Dirichlet Regression and other Compositional Models with Application to Market-share Data Mining of Information

Technology Companies

163

plained. It is to be noted that google-trends (Carri

`

ere-

Swallow and Labb

´

e, 2013) only supports comparison

of 5 key-words at a time. To support more searches,

we will compare the term with a standard term such as

”photo” to get a relative measure of frequency. This

process is done with all the variables, then put to-

gether and normalized.

4.2.1 Browser Market Shares - Worldwide

It is interesting to note, in 2009, Internet-Explorer

(64.97%) and Firefox (26.85%) were leading the mar-

ket, and today they are mere 3-5% share holders in

the world-wide browser markets. This owes to the in-

troduction of new browser by Google, Chrome and

Apple’s Safari. The major market shares in internet

browsers is held by Chrome (51.5%) followed by Sa-

fari (15.13%) in 2018. We have collected monthly

from 2009 January to 2018 September, with n = 118

data points, with D = 6 components, including UC

browser and Opera. The ternary diagrams of 3 sets

of browsers are given in Figures 2, 3, 4 and 5. This

shows how the compositions have changed over the

course of 10 years. They clearly follow a linear pat-

tern. Table 3 has the results of the experiment. It

is observed that GD regression shows close to unity

R2T, and least KL divergence (0.23). Dirichlet re-

gression has slightly better RSS (0.03) than GD re-

gression (0.09). The arithmetic transforms combined

with OLS with less computational complexity, take

lesser time to execute, with acceptable results.

4.2.2 Mobile Seller Market Shares in Canada

The Canadian mobile market was ruled by Apple

(88.97%) in the year 2010. It is now sharing space

with Samsung (25.14%) in 2018. We have included

LG, Huawei, Google and Motorola in the study. With

D = 6 and n = 95, we have the independent variables

obtained from Google-trends, individually for each

company, the trends are in accordance with the share

market patterns. Table 4 describes the results. Look-

ing at the measures, we can say that google trends has

been a good measure of predicting the shares, with

the regression fits of RSS close to zero. The general-

ized Dirichlet regression performed well compared to

other methods.

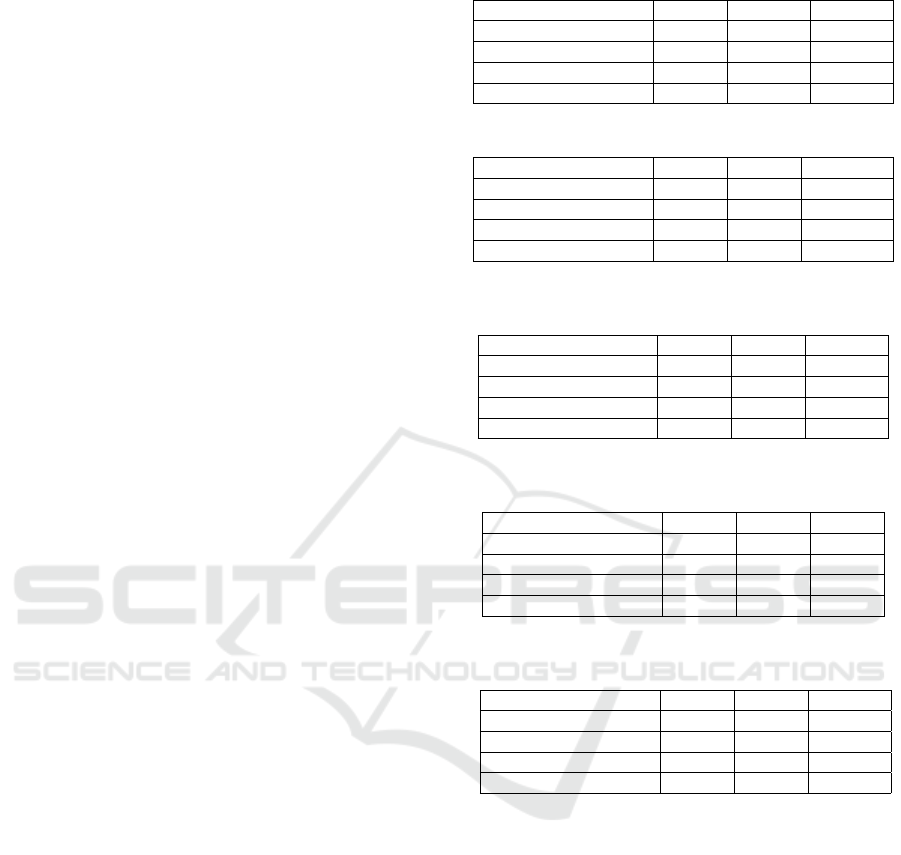

Table 1: Regression measures of Arctic lake sediments data.

Methods\Measures SSR R2T KL

CLR + OLS 3.3287 11.0777 25.4432

ILR + OLS 3.3183 11.8528 25.3671

Dirichlet regression 0.8193 6.2170 15.9382

Generalized Dirichlet 0.5415 8.9557 17.9848

Table 2: Regression measures of forensic glass data.

Methods\Measures SSR R2T KL

CLR + OLS 9.4718 0.0126 216.8152

ILR + OLS 9.4577 0.0129 217.3527

Dirichlet regression 0.0186 0.0023 333.3006

Generalized Dirichlet 0.0145 0.0015 336.3690

Table 3: Regression measures of world-wide browser

shares.

Methods\Measures SSR R2T KL

CLR + OLS 4.1566 0.9075 0.7468

ILR + OLS 6.2981 0.0386 11.4344

Dirichlet regression 0.0279 1.0533 0.2290

Generalized Dirichlet 0.0840 0.8230 0.8385

Table 4: Regression measures of mobile vendor shares in

Canada.

Methods\Measures SSR R2T KL

CLR + OLS 4.9768 5.6769 9.6099

ILR + OLS 4.9934 0.3337 9.1590

Dirichlet regression 0.0004 0.9443 0.0044

Generalized Dirichlet 0.0100 0.2747 0.1194

Table 5: Regression measures of Social Media Shares in

India.

Methods\Measures SSR R2T KL

CLR + OLS 5.0926 0.0419 11.3324

ILR + OLS 5.1004 0.0395 11.4662

Dirichlet regression 0.0720 0.0741 11.5216

Generalized Dirichlet 0.6679 0.1262 21.2748

4.2.3 Social Networks Market Shares in India

Facebook is the most followed social networking site

in India. It has been growing popularity from 52.3%

in 2010 to 86.56% in October 2018. Many companies

have mushroomed in this space but Youtube has sus-

tained it’s second place with 10% and it saw it’s peak

with 25% in 2012. Twitter had a good 7% share in

2013, but now it has a mere 1% share. Results have

been recorded in Table 5. Dirichlet regression seems

to fit the data better than GD regression, with slight

variation in the measures.

ICEIS 2019 - 21st International Conference on Enterprise Information Systems

164

Figure 1: Arctic Lake.

Figure 2: Browser shares: Chrome, IE, Firefox.

Figure 3: Browser shares: Chrome, IE, UC.

5 CONCLUSION

We have introduced an implementation of general-

ized Dirichlet regression that extends Beta regres-

sion for compositional, multiple response variables.

An application in share-market analysis demonstrates

the modelling capabilities of this solution. Vari-

ous compositional regression models have been dis-

cussed, and their results compared. The question, ”Is

google-trends a good predictor of the share market

dynamics?” is answered with three real-world exam-

ples. Google trends seem to capture the share-market

trends well. The distribution-based regression algo-

rithms fared better than transformations-based regres-

sion. Though the trade-off is the use of more compu-

tationally complex calculations.

Additionally, we suggest future work should ex-

plore new choices of starting values for the maxi-

Figure 4: Browser shares: Chrome, Safari, IE.

Figure 5: Browser shares: Chrome, UC, Safari.

mum likelihood estimation of generalized Dirichlet

regression and their corresponding sensitivity stud-

ies for these choices. A more robust system with

less sensitivity to the estimation of regression coef-

ficients could be developed, with the use of mixture

models (Bouguila and Ziou, 2012) in Dirichlet regres-

sion. This work could be applied in the fields of image

recognition (Boutemedjet et al., 2007) and intrusion

detection (Fan et al., 2011).

ACKNOWLEDGEMENTS

The completion of this work was made possible

thanks to NSERC and Concordia University research

chair.

REFERENCES

Aitchison, J. (1982). The statistical analysis of composi-

tional data. Journal of the Royal Statistical Society.

Series B (Methodological), pages 139–177.

Ankam, D. and Bouguila, N. (2018). Compositional data

analysis with pls-da and security applications. In 2018

IEEE International Conference on Information Reuse

and Integration (IRI), pages 338–345. IEEE.

Bayes, C. L., Baz

´

an, J. L., Garc

´

ıa, C., et al. (2012). A new

robust regression model for proportions. Bayesian

Analysis, 7(4):841–866.

Bouguila, N. and Ziou, D. (2004a). Dirichlet-based prob-

ability model applied to human skin detection [im-

age skin detection]. In 2004 IEEE International Con-

Generalized Dirichlet Regression and other Compositional Models with Application to Market-share Data Mining of Information

Technology Companies

165

ference on Acoustics, Speech, and Signal Processing,

ICASSP 2004, Montreal, Quebec, Canada, May 17-

21, 2004, pages 521–524.

Bouguila, N. and Ziou, D. (2004b). A powerful finite

mixture model based on the generalized dirichlet dis-

tribution: Unsupervised learning and applications.

In 17th International Conference on Pattern Recog-

nition, ICPR 2004, Cambridge, UK, August 23-26,

2004., pages 280–283.

Bouguila, N. and Ziou, D. (2006). A hybrid SEM algorithm

for high-dimensional unsupervised learning using a fi-

nite generalized dirichlet mixture. IEEE Trans. Image

Processing, 15(9):2657–2668.

Bouguila, N. and Ziou, D. (2012). A countably infinite mix-

ture model for clustering and feature selection. Knowl.

Inf. Syst., 33(2):351–370.

Boutemedjet, S., Ziou, D., and Bouguila, N. (2007). Unsu-

pervised feature selection for accurate recommenda-

tion of high-dimensional image data. In Advances in

Neural Information Processing Systems 20, Proceed-

ings of the Twenty-First Annual Conference on Neural

Information Processing Systems, Vancouver, British

Columbia, Canada, December 3-6, 2007, pages 177–

184.

Cantner, U., Kr

¨

uger, J. J., and S

¨

ollner, R. (2012). Product

quality, product price, and share dynamics in the ger-

man compact car market. Industrial and Corporate

Change, 21(5):1085–1115.

Carri

`

ere-Swallow, Y. and Labb

´

e, F. (2013). Nowcasting

with google trends in an emerging market. Journal

of Forecasting, 32(4):289–298.

Chang, W.-Y., Gupta, R. D., and Richards, D. S. P. (2010).

Structural properties of the generalized dirichlet dis-

tributions. Contemp. Math, 516:109–124.

Choi, H. and Varian, H. (2012). Predicting the present with

google trends. Economic Record, 88:2–9.

Draper, N. R. and Smith, H. (2014). Applied regression

analysis, volume 326. John Wiley & Sons.

Dussauge, P., Garrette, B., Mitchell, W., et al. (2002). The

market-share impact of inter-partner learning in al-

liances: evidence from the global auto industry. Co-

operative strategies and alliances, pages 707–727.

Fan, W. and Bouguila, N. (2013a). Online learning of

a dirichlet process mixture of beta-liouville distribu-

tions via variational inference. IEEE transactions on

neural networks and learning systems, 24(11):1850–

1862.

Fan, W. and Bouguila, N. (2013b). Variational learning of a

dirichlet process of generalized dirichlet distributions

for simultaneous clustering and feature selection. Pat-

tern Recognition, 46(10):2754–2769.

Fan, W., Bouguila, N., and Ziou, D. (2011). Unsupervised

anomaly intrusion detection via localized bayesian

feature selection. In 11th IEEE International Confer-

ence on Data Mining, ICDM 2011, Vancouver, BC,

Canada, December 11-14, 2011, pages 1032–1037.

Fan, W., Bouguila, N., and Ziou, D. (2013). Unsuper-

vised hybrid feature extraction selection for high-

dimensional non-gaussian data clustering with vari-

ational inference. IEEE Trans. Knowl. Data Eng.,

25(7):1670–1685.

Ferrari, S. and Cribari-Neto, F. (2004). Beta regression for

modelling rates and proportions. Journal of Applied

Statistics, 31(7):799–815.

Fox, J. and Monette, G. (2002). An R and S-Plus companion

to applied regression. Sage.

Haaf, C. G., Michalek, J. J., Morrow, W. R., and Liu, Y.

(2014). Sensitivity of vehicle market share predictions

to discrete choice model specification. Journal of Me-

chanical Design, 136(12):121402.

Hijazi, R. H. (2006). Residuals and diagnostics in dirichlet

regression. ASA Proceedings of the General Method-

ology Section, pages 1190–1196.

Hijazi, R. H. and Jernigan, R. W. (2009). Modelling compo-

sitional data using dirichlet regression models. Jour-

nal of Applied Probability & Statistics, 4(1):77–91.

Hutcheson, G. D. (2011). Ordinary least-squares regres-

sion. The SAGE Dictionary of Quantitative Manage-

ment Research, pages 224–228.

Kullback, S. and Leibler, R. A. (1951). On information

and sufficiency. The annals of mathematical statistics,

22(1):79–86.

Lancaster, H. (1965). The helmert matrices. The American

Mathematical Monthly, 72(1):4–12.

Maier, M. J. (2014). Dirichletreg: Dirichlet regression for

compositional data in r.

Martin-Fernandez, J. A., Bren, M., Barcelo-Vidal, C., and

Pawlowsky Glahn, V. (1999). A measure of differ-

ence for compositional data based on measures of di-

vergence. Proceedings of IAMG, 99:211–216.

Morais, J., Thomas-Agnan, C., and Simioni, M. (2018).

Using compositional and dirichlet models for mar-

ket share regression. Journal of Applied Statistics,

45(9):1670–1689.

Moraisab, J., Thomas-Agnana, C., and Simionic, M.

(2016). A tour of regression models for explaining

shares.

Tay, R. S. and Mc Carthy, P. S. (1991). Demand ori-

ented policies for improving market share in the us

automobile industry. International Journal of Trans-

port Economics/Rivista internazionale di economia

dei trasporti, pages 151–166.

Tsagris, M. (2015). Regression analysis with composi-

tional data containing zero values. arXiv preprint

arXiv:1508.01913.

Tsagris, M. and Stewart, C. (2018). A dirichlet re-

gression model for compositional data with zeros.

Lobachevskii Journal of Mathematics, 39(3):398–

412.

Vosen, S. and Schmidt, T. (2011). Forecasting private con-

sumption: survey-based indicators vs. google trends.

Journal of Forecasting, 30(6):565–578.

Watt, J., Borhani, R., and Katsaggelos, A. K. (2016). Ma-

chine Learning Refined: Foundations, Algorithms,

and Applications. Cambridge University Press.

Zhang, Y., Zhou, H., Zhou, J., and Sun, W. (2017). Regres-

sion models for multivariate count data. Journal of

Computational and Graphical Statistics, 26(1):1–13.

ICEIS 2019 - 21st International Conference on Enterprise Information Systems

166