AN APPLICATION OF NON-LINEAR PROGRAMMING TO

TRAIN RECURRENT NEURAL NETWORKS IN TIME SERIES

PREDICTION PROBLEMS

M.P. Cuéllar, M. Delgado, M.C. Pegalajar

Department of Computer Science and Artificial Intelligence. E.T.S. Ingeniería Informática. Univerity of Granada, C/. Pdta

Daniel Saucedo Aranda, s.n.. Granada (Spain, Europe)

Keywords: Non-Linear Programming, Recurrent Neural Networks, Time Series Prediction

Abstract: Artificial Neural Networks are bioinspired mathematical models that have been widely used to solve many

complex problems. However, the training of a Neural Network is a difficult task since the traditional

training algorithms may get trapped into local solutions easily. This problem is greater in Recurrent Neural

Networks, where the traditional training algorithms sometimes provide unsuitable solutions. Some

evolutionary techniques have also been used to improve the training stage, and to overcome such local

solutions, but they have the disadvantage that the time taken to train the network is high. The objective of

this work is to show that the use of some non-linear programming techniques is a good choice to train a

Neural Network, since they may provide suitable solutions quickly. In the experimental section, we apply

the models proposed to train an Elman Recurrent Neural Network in real-life Time Series Prediction

problems.

1 INTRODUCTION

Artificial Neural Networks are bioinspired

mathematical models that have been widely used to

solve many complex problems, difficult to model

because of their non-linearity, lack of information,

or excessive difficulty. The most common neural

network models used to solve these problems have

mainly been feedforward networks (Haykin, 1999).

There are many training algorithms for this kind of

network and most are based on error propagation

methods: for instance, backpropagation algorithms

and similar ones. However, the disadvantage of

these algorithms is that the search for the best

solution is frequently trapped in a local optimum,

therefore making it difficult for the network to work

well.

In the case of Recurrent Neural Networks (D.P.

Mandic et al., 2001), there are not as many training

algorithms as for feedforward ones. These

algorithms (M. Hüsken et al., 2003; R.J. Williams et

al., 1989-1990) also share the same disadvantage as

those used to train feedforward networks in that they

get trapped in local optimal solutions very easily. In

fact, This problem is greater in recurrent neural

networks. Some evolutionary techniques have been

proposed as a good choice to train these kind of

networks (Blanco et al., 2001; M.P. Cuéllar et al.,

2004), because they can overcome the local optimal

solutions, but they have the drawback that the

training stage takes too much time.

In this work, we propose some non-linear

programming algorithms to train Recurrent Neural

Networks. These algorithms are the BFGS (C. Zhu

et al., 1997; R.H. Byrd et al., 1995) and the

Levenberg-Marquardt minimization methods. Both

algorithms are related to the Gauss-Newton method,

but the implementations used in this work may be

used to solve different kind of problems, as we will

show in section 3.

Related to Neural Network training, the BFGS

method has been used to train feedforward networks,

being hybridized with the evolutionary Scatter

Search algorithm (R. Martí et al., 2002), in order to

improve the solutions during the evolutionary

process, obtaining suitable results in function

approximation problems. On the other hand, the

Levenberg-Marquardt (LM) (D.W. Marquardt, 1963;

J.J More, 1977) method is a widely known algorithm

used to optimize Radial Basis Function Networks

(R. Zemomi, 2003). Some implementations have

adapted the LM algorithm to train feedforward

35

P. Cuéllar M., Delgado M. and C. Pegalajar M. (2005).

AN APPLICATION OF NON-LINEAR PROGRAMMING TO TRAIN RECURRENT NEURAL NETWORKS IN TIME SERIES PREDICTION PROBLEMS.

In Proceedings of the Seventh International Conference on Enterprise Information Systems, pages 35-42

DOI: 10.5220/0002515800350042

Copyright

c

SciTePress

networks (M.T. Hagan et al., 1994). Other

applications of both algorithms are ralated to solve

minimization problems.

In this work, we use the models proposed to train

an Elman Recurrent Neural Network (ERNN) (D.P.

Mandic et al., 2001) in real-life Time Series

prediction problems. The reasons to choose an

ERNN model are mainly related to the problem to

solve:

Time Series are, basically, a data chaining,

indexed in time. Such data chaining often has some

temporal properties, in the sense that the value of the

Time Series at the current time depends on some

unknown past values. The objective of Time Series

Prediction is to model the Time Series, and then to

predict the future values with minimum error. Many

approaches have been used to model a Time Series,

and to the date, it is still a great problem. Traditional

techniques, basically statistical methods, are very

limited, since the models used are mainly linear

regressions, and the temporal properties of the time

series are often non-linear ones. In recent works,

there are many approaches to model a Time Series

with non-linear models, and Neural Networks play a

great role in this field. The use of RBF Networks is

very common in Time Series Prediction (R. Zemomi

et al., 2003), but they have the disadvantage that the

analysis of the temporal properties must be done

manually, therefore increasing the number of

experiments. Recurrent Neural Networks is a

suitable approach to model a Time Series, since the

recurrence allows the network to learn the temporal

properties that the input data have, and the analysis

of the temporal properties is done automatically.

Considering some models of Recurrent Networks,

the ERNN has obtained the best experimental results

in our work.

This work is structured as follows: Section 2

introduces the Elman Recurrent Neural Neural

Network. In section 3, the non-linear programming

algorithms proposed are exposed. Section 4 shows

the experimenta results obtained. Finally, section 5

discusses the conclusions obtained.

2 ELMAN RECURRENT NEURAL

NETWORKS

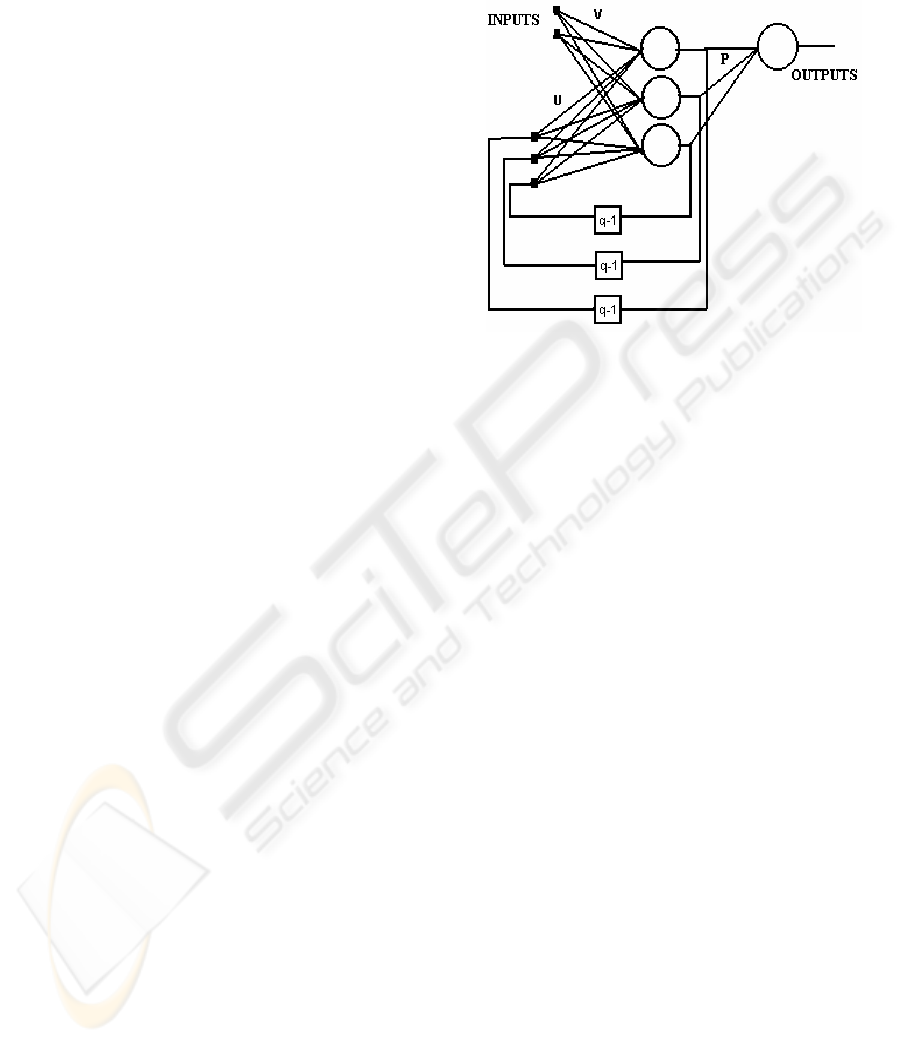

An Elman recurrent neural network has three neuron

layers: one is used for the input data, another is the

hidden neuron layer, and the other is the output

neuron layer. The network also has an additional

neuron layer, called the state neuron layer. There are

as many neurons in the state neuron layer as there

are in the hidden layer. Recurrence is carried out

from the hidden neurons to the state neurons so that

the output of a hidden neuron at time t is also input

to all hidden neurons at time t+1. This idea is

illustrated in Figure 1.

Figure 1 shows an example of an Elman recurrent

neural network with two inputs, one output, and

three hidden neurons. Therefore, the state neuron

layer also has three neurons, corresponding to the

values of the three hidden nodes at the previous

time. The equations of the network dynamics are:

(1)

(2)

(3)

(4)

where:

• Y

B

k

B(t) is the output of neuron k in the output

layer, at time t.

• Netout

B

k

B(t) is the output of neuron k in the

output layer, when the activation function has

not yet been applied.

• Neth

B

k

B(t) is the output of neuron k in the hidden

layer, when the activation function has not yet

been applied.

• S

B

k

B(t) is the output of neuron k in the hidden

layer.

• H is the number of neurons in the hidden layer.

• I is the number of neurons in the input layer.

• S

B

k

B(t-1) is the state value, corresponding to the

state neuron k, at time t.

)G(netout(t)Y

kk

=

∑∑

==

+−=

H

1h

I

1i

ijihjhh

(t)XV1)(tSU(t)neth

(t))f(neth(t)S

jj

=

∑

=

=

H

0j

jkjk

(t)SP(t)netout

Figure 1: Example of an Elman recurrent neural

network with two intputs, three hidden neurons, and

one output

ICEIS 2005 - ARTIFICIAL INTELLIGENCE AND DECISION SUPPORT SYSTEMS

36

• F(·) is the activation function of the neurons in

the hidden layer.

• G(·) is the activation function of the neurons in

the output layer.

• V

B

ij

B is the weight of connection from neuron j in

the input layer to neuron i in the hidden layer.

• U

B

ij

B is the weight of connection from neuron j in

the state layer to neuron i in the hidden layer.

• P

B

ij

B is the weight of connection from neuron j in

the hidden layer to neuron i in the output layer.

• X

B

i

B(t) is the network input i at time t.

The traditional gradient-based training algorithm

used to train this kind of network is the

Backpropagation Through Time (BPTT) algorithm.

The main drawback of this algorithm, as shown in

section 1, is that the method gets trapped into local

optimal solutions very easily.

In the following section, the non-linear

programming algorithms proposed in this work, and

its application to Recurrent Neural Network training,

are introduced.

3 NON-LINEAR PROGRAMMING

ALGORITHMS

Before to explain the BFGS and the LM algorithms,

an introduction to non-linear programming is shown.

A non-linear program is a problem that can be

considered as a minimization task with the following

structure:

(5)

The function F is called objective function, x is a

vector of n variables to be optimized. The functions

g

B

i

B and hB

j

B are called constraint equations. The

constraint equations remark some conditions that

must be fulfilled for a set of variables in x. If the

value m=0, then there are no conditions or

dependencies in the variables in x, and the problem

is called unconstrained.

There are many reasons to choose the BFGS and

the LM algorithms in this work. These are:

- They have been applied to optimize

feedforward neural networks, obtaining good

results. Therefore, it may be interesting to

apply them to train recurrent networks,

where the training stage is more difficult.

- The versions of the algorithms implemented

in this work may be applied to problems with

different characteristics, as shown below.

Depending on the problem to solve, it may be

classified, considering the number of training data,

into underdetermined, determined, and

overdetermined problems. A problem is

underdetermined when there are less training

examples than variables to optimize; it is determined

when there are as many training examples as

variables to optimize, and overdetermined when

there are more training examples than variables to

optimize. The determined problems are not very

common, so that in this work we only consider the

underdetermined and the overdetermined problems.

Furthermore, in some applications of Recurrent

Neural Networks, it may be interesting to keep the

weight values belonging not to ℜ, but to a valid

interval in ℜ. An example of this situation is when

the neural network must be implemented in

hardware, and the number of bits to represent a

weight is fixed. We can see this situation as a

constrained situation, so that we can also classify the

problems into constrained and unconstrained

problems.

Attending to the previous classifications, the

BFGS and the LM algorithms proposed in this work

may be applied to a concrete kind of problems, as

shown in tables 1 and 2.

Unconstrain

ed problems

Constrained

problems

Underdetermined

problems

NO NO

Overdetermined

problems

YES NO

Table 2: Problems solved by BFGS

Unconstrain

ed problems

Constrained

problems

Underdetermined

problems

YES YES

Overdetermined

problems

YES YES

As we can see, the applications of BFGS also

include the problems solved by LM. However, in the

experimental section, we show that the solutions

provided by LM are much better than the ones

1

1

1j

1i

n

mm

0m

1,..mmj0,)x(h

1..mi0,)x(g

:tosubject

),xF(minimize

≥

≥

+=≥

==

ℜ∈x

Table 1: Problems solved by LM

AN APPLICATION OF NON-LINEAR PROGRAMMING TO TRAIN RECURRENT NEURAL NETWORKS IN TIME

SERIES PREDICTION PROBLEMS

37

provided by BFGS for overdetermined

unconstrained problems.

Below, subsections 3.1 and 3.2 explain the BFGS

and the LM algorithms, and their application to

Recurrent Neural Network training.

3.1 The BFGS algorithm

The BFGS algorithm was firstly proposed in 1970

by Broyden, Fletcher, Goldfarb and Shanno. Since

then, several approaches to improve the algorithm,

and also to apply it to a wider set of problems, have

been proposed. In this work, we use an adaptation of

this algorithm, called limited-memory bound-

constrained/unconstrained BFGS algorithm (L-

BFGS-B) (R. H. Byrd et al., 1995). The L-BFGS-B

algorithm solves a problem that is considered as

shown in equation 5, where the constraint equations

are basically bound constraints, it is said:

h

B

j

B(x)= lB

j

B ≤xB

j

B ≤uB

j

B, j=1..n

where l

B

j

B and uB

j

B are the lower and upper bounds for

the variable to optimize x

B

j

B, respectively. The main

scheme of the algorithm is shown below:

0. At the beginning, a solution x

B

k

B, k=0, and the

corresponding gradient for function F must

be provided as input data.

1. If the search has converged, stop.

2. Find an initial local solution, by mean of

calculating the Cauchy point.

3. Compute a search direction, called d

B

k

B.

4. Perform a line search along d

B

k

B, subject to the

bound constraints, in order to compute the

step length λ

B

k

B, and set xB

k+1

B=xB

k

B+λB

k

B dB

k

B.

5. Compute

∇

F(xB

k+1

B)

6. Update the limited-memory matrices, if

necessary.

7. Set k= k+1, and go to Step 1.

Firstly, the algorithm computes an initial solution

and a search direction, d

B

k

B. Then, the solution is

modified according to d

B

k

B. The algorithm also apply a

Quasi-Newton algorithm to approximate the Hessian

matrix. In (C. Zhu et al., 1997; R.H. Byrd et al.,

1995), you can find an in-depth explanation about

this algorithm.

Now, the use of the L-BFGS-B algorithm to train

an ERNN is explained. Firstly, an ERNN is

considered as a non-linear program (equation 5).

After that, we show how to calculate the gradient of

the variables to be optimized.

When training a neural network, the objective is

to minimize the output error. One of the most

common procedures used to do this, is to minimize

the Mean Square Error (MSE) between the network

output, and the desired output for the network. In the

case of recurrent neural networks, the MSE must be

minimized across the time, as equation 6 shows.

(6)

where w is a vector containing the network weights,

T is the number of training samples in the time, O is

the number of network outputs, d

B

o

B(t) is the desired

output for neuron o at time t, and Y

B

o

B(t) is the

network output provided by neuron o at time t (see

equation 4). According to the notation introduced in

Section 2, the vector w is structured as follows:

Thus, equation 5 may be rewritten as follows:

(7)

The area in brackets is optional, and it contains the

bound constraints in constrained problems.

The gradient value for a variable w

B

r

B, denoted qB

r

B,

that must be provided to the algorithm, is calculated

in the following way:

Now, a vector Q, with the gradient values for the

variables in vector w, may be defined as follows:

∑

∑

=

=

−=

=

O

1o

2

oo

T

1t

(t))d(t)(Yt),wSE(

t),wSE(

T

1

)wMSE(

})w{MSE(min

)...P..PP..PP...U...U

..U..UU...VV..VV(Vw

OH2H211H11HH2H

211H11HI211I1211

=

⎥

⎦

⎤

⎢

⎣

⎡

=≤≤

ℜ∈

∑

=

njuwl

w

jjj

..1,

:tosubject

},t),wSE(

T

1

{minimize

n

T

1t

r

r

w

)wMSE(

q

∂

∂

=

1..nr),(qQ

r

==

ICEIS 2005 - ARTIFICIAL INTELLIGENCE AND DECISION SUPPORT SYSTEMS

38

The gradient value for each variable in w, using

the notation from Section 2, is calculated below:

Where 1≤i≤I, 1≤j≤H, 1≤o≤O. Thus, the gradient

vector Q may be rewritten, following the same order

defined for the vector w, as follows:

You can find a Fortran free source code of the L-

BFGS-B algorithm in the web site

http://www.ece.northwestern.edu/~nocedal/lbfgsb.ht

ml. In this work, we have translated it to C language,

and also to adapt such source code in order to train

ERNN.

3.2 The LM algorithm

The basic LM algorithm was proposed by D.W.

Marquardt in (D.W. Marquardt, 1963). Since then,

there are many approaches to solve a non-linear

program using the LM algorithm.

The algorithm tries to fit n parameters x

B

1

B...xB

n

B, in a

non-linear problem. The initial assumption is that,

sufficiently closed to the minimum of the function F

to be minimized, F may be approximated by a

quadratic form:

where h is a n-dimensional vector, and H is the

Hessian matrix. If the approximation is good, then

the optimal values for w may be calculated.

Otherwise, the algorithm iterates using the steepest

descent method (S. Haykin, 1999) in order to

improve the current solution. The main scheme of

the algorithm is structured as follows:

0. At the beginning, a solution x

P

k

P

, k=0, and a

step-length parameter λ, must be provided as

input data.

1. Compute F(x

P

k

P

)

2. Update the Hessian matrix, and calculate

δ

xP

k

P

3. Compute F(x

P

k

P

+

δ

xP

k

P

).

4. If (F(x

P

k

P

+

δ

xP

k

P

)

≥

F(xP

k

P

)), increase λ by a factor

of 10

5. If (F(x

P

k

P

+

δ

xP

k

P

) < F(xP

k

P

)), then

5.1. decrease λ by a factor of 10

5.2. set x

P

k+1

P

= xP

k

P

+

δ

x

6. Set k= k+1

7. If the algorithm has converged, stop.

Otherwise, go to step 1.

The implementation used in this work solves an

overdetermined set of non-linear equations by mean

of a modification of the LM algorithm. You can find

a good explanation of the implementation of this

algorithm in (J.J. More, 1977).

Now, the training process for ERNN, using the

LM algorithm, is explained. The training of an

Elman Recurrent Neural Network may be

considered as the fitting of set of m non-linear

equations, being m the number of training samples:

(8)

Considering equation 8, m=T·O, where T is

the number of training samples, and O is the number

of network outputs; d

B

o

B(t) is the desired output for

neuron o at time t, and Y

B

o

B(t) is the network output

provided by neuron o at time t.

Being considered an Elman Recurrent Neural

Network as a set of m equations as shown in (8), the

LM algorithm minimizes the sum of the squares for

such m equations. Thus, equation 5 may be rewritten

as follows:

(9)

Thus, equation 9 shows the function to be

minimized, and the LM algorithm may be applied

directly.

There is an important advantage in the LM

algorithm, being compared with BFGS. To explain

it, we must take a look at equations 7 and 9. In (7),

the function to minimize is the MSE across the time.

Please note that the minimization is carried out for

the sum of the errors in output values. On the other

hand, equation (9) minimizes the errors for each

⎩

⎨

⎧

=

=

−=

1..Oo

1..Tt

(t);d(t)Yt),w(F

ooo

}t)),w((F{min

T

1t

O

1o

2

o

∑∑

==

xHx

2

1

xhγF +−≈

∑

∑

∑

∑

=

=

=

=

−=

=

∂

∂

−=

∂

∂

−=

∂

∂

O

1o

ooojjj

T

1t

ji

ji

T

1t

jk

jk

T

1t

joo

oj

(t))d(t)(YP(t))(nethf'

T

2

(t))δ(S

(t)))(S(t)(X

V

t),wMSE(

(t)))(S1)(tS

U

t),wMSE(

(t)(t))Sd(t)(Y

T

2

P

t),wMSE(

δ

δ

)

dP

t),wMSE(

..

dU

t),wMSE(

..

dV

t),wMSE(

(Q

okjkji

∂∂∂

=

AN APPLICATION OF NON-LINEAR PROGRAMMING TO TRAIN RECURRENT NEURAL NETWORKS IN TIME

SERIES PREDICTION PROBLEMS

39

output separately. This fact allows the LM algorithm

to improve the minimization for each output

individually, meanwhile the BFGS algorithm

minimizes the global error for the whole set of

outputs. Because of this, the LM algorithm may find

better solutions as shown in the experimental

section.

4 EXPERIMENTAL RESULTS

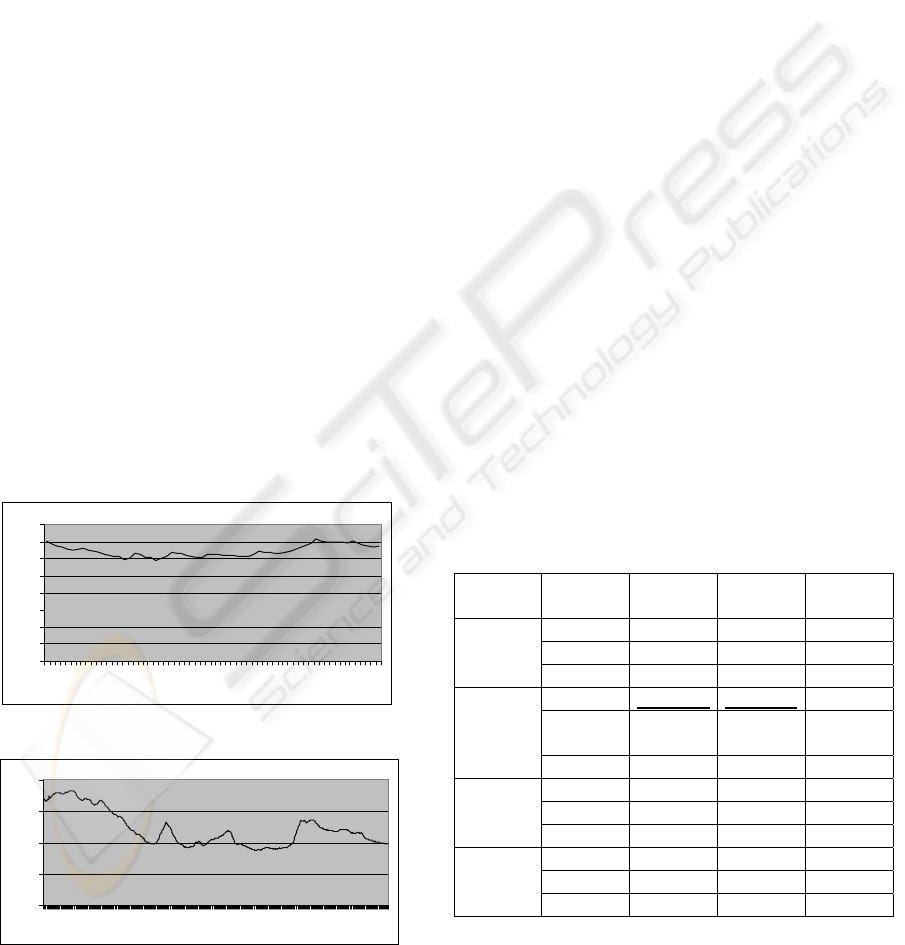

In this section, we show an example of the

application of the model exposed in the previous

section, to time series prediction problems. A time

series is a sequence of values or observations, taken

in time. The purpose of time series prediction is to

predict the next values of such observations. In this

work, we apply the model to two time series, taken

from the web page www.economagic.com:

- Series1: ECB reference exchange rate, UK

pound sterling-Euro, 215 pm (C.E.T.) UK Pound

Sterling. Total values: 65, taken monthly from 1999

to 2004-May. We predict the 5 last values,

corresponding to the monthd of 2004.

- Series2: Total Population of the U.S.;

Thousands. Percentage variation from 1953 until

2004-March. Total values: 615, taken monthly from

1953. We predict the 3 last values, corresponding to

the months of 2004.

Figures 2-3 show the values of the time series.

The parameters to be used in the algorithms are

the following:

- Number of Input Neurons: 1

- Number of Hidden Neurons: 8

- Number of Output Neurons: 1

- Stopping criteria: To reach 500 iterations

- Initial value for λ: 0.0001

- Weight interval (constrained BFGS): [-0.5,

0.5]

Considering the Network exposed in Section 2,

the number of variables to be optimized is I·H + H·H

+ O·H, where I is the number of input units, H is the

number of hidden units, and O is the number of

output units. Therefore, according to the previous

specifications, the number of variables to optimize

in each problem is 80. Thus, the problems to solve

may be classified (following the criteria exposed in

section 3), into underdetermined, and

overdetermined. As the number of training data are

60 for Series1, and 613 for Series2, then Series1 is

classified as an underdetermined problem (LM

cannot be applied in this problem, in consequence),

and Series2 as an overdetermined problem.

We make 30 experiments for each algorithm in

each Time Series. Tables 3 and 4 shows the results

obtained. Column 1 means the algorithm. Column 2

exposes the kind of solution (average, best or worse

solution). Finally, columns 3, 4 and 5 shows the

traning and test Mean Square Error of the solution,

and the time taken to obtain it. The best solutions

over the whole set of algorithms are underlined

Algorithm

Solution Training

MSE

Test MSE Time (in

seconds)

Best 6.7291e-04

8.0037e-04

0.23

Average 8.0126e-04

9.6046e-04

0.27

BFGS

(Constrai-

ned)

Worse 1.3150e-03

1.5769e-03

0.14

Best U9.4695e-05U U1.0391e-04U 0.71

Average 6.0206

e-04

6.9697e-04

0.65

BFGS(unc)

Worse 4.9304e-02

5.8125e-02

0.30

Best 1.6103e-04

1.7559e-04

1.09

Average 1.2020e-03

1.5151e-03

1.00

Genetic

Algorithm

Worse 6.9654e-03

8.1305e-03

0.97

Best 6.2092e-02

7.7774e-02

1.12

Average 8.2314e-02

1.0431e-01

1.03

BPTT

Worse 9.8027e-02

1.2536e-01

0.95

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

1 5 9 1317212529333741454953576165

Figure 2: Values of Series1 Time Series

0

0,5

1

1,5

2

1 50 99 148 197 246 295 344 393 442 491 540 589

Figure 3: Values of Series2 Time Series

Table 3: Results for Series1

ICEIS 2005 - ARTIFICIAL INTELLIGENCE AND DECISION SUPPORT SYSTEMS

40

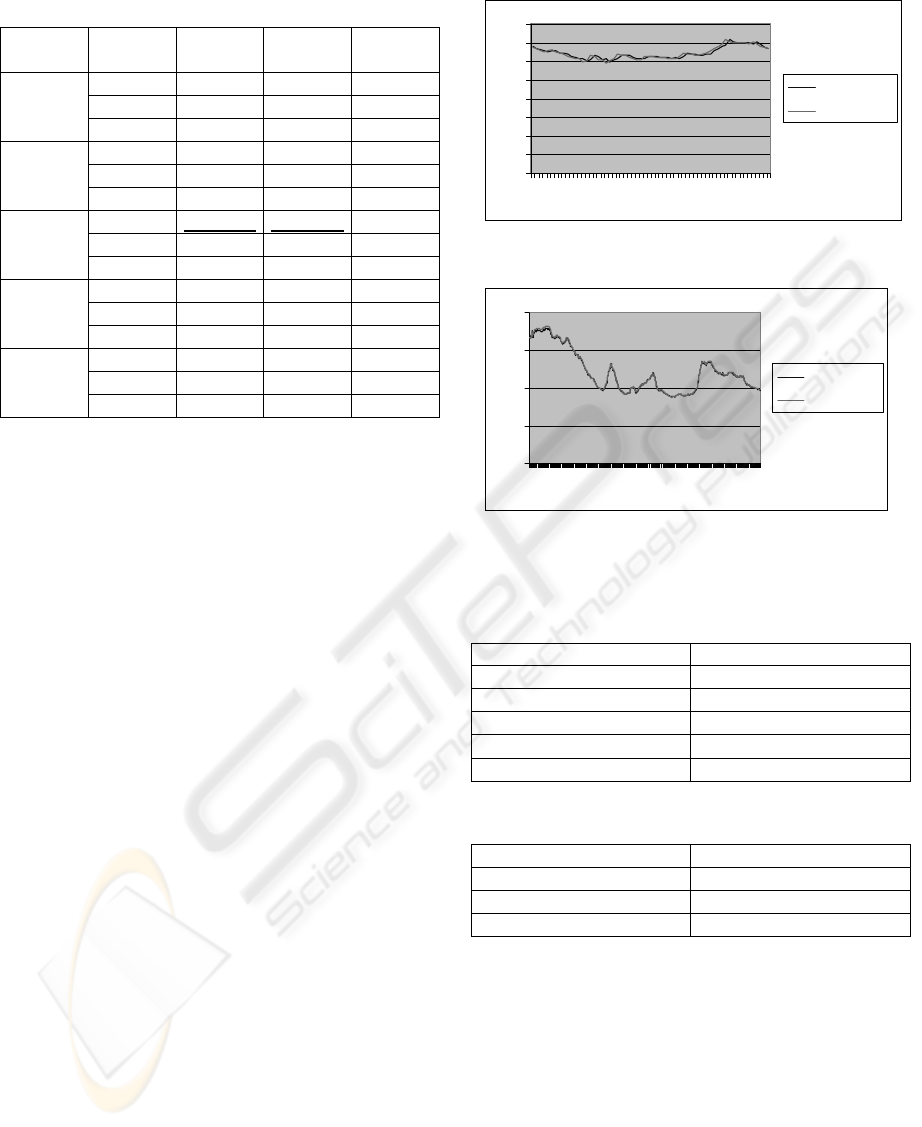

Algorithm

Solution Training

MSE

Test MSE Time (in

seconds)

Best 4.0093e-03

4.1564e-03

1.31

Average 1.8302e-02

1.8788e-02

1.25

BFGS

constrained

Worse 4.8057e-02

4.9673e-02

1.14

Best 1.2444e-04

1.2707e-04

1.40

Average 1.0259e-03

1.0462e-03

1.36

BFGS

Unconstrai

-ned

Worse 5.3909e-02

5.4949e-02

1.27

Best U8.5914e-05U U8.8928e-05U 3.05

Average 2.2811e-03

2.3152e-03

2.82

LM

Worse 1.3597e-02

1.4481e-02

2.58

Best 3.6713e-04

3.8023e-04

2.90

Average 4.7275e-03

4.8265e-03

2.79

Genetic

Algorithm

Worse 3.7482e-02

3.9969e-02

2.76

Best 4.7391e-02

4.9600e-02

1.41

Average 6.3998e-02

6.6973e-02

1.36

BPTT

Worse 8.8101e-02

9.1760e-02

1.33

As we can see in tables 3-4, the non-linear

programming algorithms obtain the best results. We

also can see the difference in the constrained and the

unconstrained BFGS: The unconstrained BFGS

obtain better solutions, since the constrained can

only take values in the bound intervals for the

weights. For this reason, it is better to choose the

unconstrained version than the unconstrained one,

unless that bounds over the network weights are

required.

On the other hand, for the overdetermined

problem, we can observe that the LM algorithm

reach better solutions than BFGS, as we introduced

in section 3.2. The LM algorithm can get more

information about the problem because it tries to

optimize each output value for each output neuron,

since the BFGS only tries to minimize the output

error for the whole set of output neurons (see

equations 7 and 9).

In tables 3-4, we also can see that the time taken

to reach the solutions by the BFGS algorithm, is

smaller than the time taken by the other algorithms,

and it obtains suitable solutions. On the other hand,

the LM algorithm spends more time than the rest of

algorithms, but it can also obtain better solutions.

Below, figures 4-5 show the adjustment and the

prediction carried out by the best solutions in tables

3 and 4 (the BFGS and the LM algorithm,

respectively). Also, tables 5-6 expose the values of

the real data and the prediction given by the

solutions. Column 1 shows the real data, and

Column 2 exposes the prediction given by the

Network trained.

REAL DATA PREDICTION

0,69215 0,702707

0,67690 0,690901

0,67124 0,674261

0,66533 0,668534

0,67157 0,672251

REAL DATA PREDICTION

0,975 0,972407

0,974 0,969408

0,973 0,969410

Now, a statistical t-test, with 0.05 of confidence

level, is carried out in order to compare the BFGS

and the LM algorithms. Tables 7-8 show the results

of the t-test for the problems Series1 and Series2,

respectively. We use (+) to mark the cells where the

algorithm of Column x is better than the algorithm in

Row y, (-) means that the algorithm of Column x is

worse than the algorithm in Row y, and no sign

means that there is no statistical difference between

the models.

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

1 7 13 19 25 31 37 43 49 55 61

Series1

Adjustment

Figure 4: Real data and Adjustment of the best solution

for Series1

Table 5: Values of Prediction for Series1

Table 6: Values of Prediction for Series2

0

0,5

1

1,5

2

1 73 145 217 289 361 433 505 577

Series2

Adjustment

Figure 5: Real data and adjustment of the best

solution for Series2

Table 4: Results for Series1

AN APPLICATION OF NON-LINEAR PROGRAMMING TO TRAIN RECURRENT NEURAL NETWORKS IN TIME

SERIES PREDICTION PROBLEMS

41

BFGS (Unconstrained)

BFGS (Constrained) 0.3118

BFGS

(Unconstr.)

0.4271

LM 0.3251 0.3251

BFGS

(Constrained)

BFGS

(Unconstr.)

As shown in Tables 5-6, the statistical t-test has

concluded that there is no statistical difference in the

non-linear programming algorithms. However,

tables 3-4 expose that the results using an algorithm

may provide better results. What we recommend to

solve a problem, is to make a set of experiments

with each non-linear programming algorithm, and

then choose the one that better results provide, in

average.

5 CONCLUSIONS

In this work, we have introduced some non-linear

programming algorithms to train Recurrent Neural

Networks: the BFGS and the LM algorithms. After

considering the training of an Elman Recurrent

Neural Network as a non-linear programming

problem, the models have been applied to some

Time Series prediction problems in the experimental

section, obtaining suitable results. The non-linear

programming algorithms have improved the

solutions provided by the traditional training

algorithm for ERNN. They also have obtained better

results than other recent techniques, such Genetic

Algorithms, and those solutions have been reached

in less time than the GA and the traditional

algorithms. In addition, it also may be used when

bound constraints are a requirement over the

network weights, meanwhile this situation cannot be

solved using traditional training algorithms. In

conclusion, the use of non-linear programming

techniques may be a good tool to be considered

when training Recurrent Neural Networks.

REFERENCES

Blanco, Delgado, Pegalajar. 2001. A Real-Coded genetic

algorithm for training recurrent neural networks.

Neural Networks, vol. 14, pp. 93-105.

C. Zhu, R. H. Byrd and J. Nocedal. 1997. L-BFGS-B:

Algorithm 778: L-BFGS-B, FORTRAN routines for

large scale bound constrained optimization, ACM

Transactions on Mathematical Software, Vol 23, Num.

4, pp. 550 - 560.

Cuéllar M.P., Delgado M., Pegalajar M.C.. 2004. A

Comparative study of Evolutionary Algorithms for

Training Elman Recurrent Neural Networks to predict

the Autonomous Indebtedness. in Proc. ICEIS, Porto,

Portugal, pp. 457-461.

Danilo P. Mandic, Jonathon A. Chambers. 2001.

Recurrent Neural Networks for Prediction. Wiley,

John & Sons, Incorporated.

D. W. Marquardt. 1963. An algorithm for least-squares

estimation of nonlinear parameters, Journal of the

Society for Industrialand Applied Mathematics, pp.

11431–441.

Martin T. Hagan, Mohammed B. Menhaj. 1994. Training

FeedForward networks with the Marquardt algorithm,

IEEE transactions on Neural networks, vol 5, no. 6,

pp. 989-993.

Michael Hüsken, Peter Stagge. 2003. Recurrent Neural

Networks for Time Series classification,

Neurocomputing, vol. 50, pp. 223-235.

More, J. J. 1977. The Levenberg-Marquardt algorithm:

Implementation and theory. Lecture notes in

mathematics, Edited by G. A. Watson,

SpringerVerlag.

R. H. Byrd, P. Lu and J. Nocedal. 1995. A Limited

Memory Algorithm for Bound Constrained

Optimization, SIAM Journal on Scientific and

Statistical Computing , 16, 5, pp. 1190-1208.

R. Martí, A. El-Fallahi. 2002. Multilayer Neural

Networks: An experimental evaluation of on-line

training methods. Computers and Operations Research

31, pp. 1491-1513.

Ryad Zemomi, Daniel Racaceanu, Nouredalime Zerhonn.

2003. Recurrent Radial Basis fuction network for

Time Seties prediction, Engineering appl. Of Artificial

Intelligence, vol. 16, no. 5-6, pp. 453-463.

Simon Haykin. 1999. Neural Networks (a Comprehensive

foundation). Second Edition. Prentice Hall.

Williams R.J., Peng J. 1990. An efficient Gradient-Based

Algorithm for On-Line Training of Recurrent Network

trajectories,” Neural Computation, vol. 2, pp. 491-501.

Williams R.J., Zipser D. 1989. A learning algorithm for

continually running fully recurrent neural networks,

Neural Computation, vol. 1, pp. 270-280.

Table 7: T

-

Test for the algorithms, in Series1

Table 8:

T

-

Test for the algorithms, in Series2

ICEIS 2005 - ARTIFICIAL INTELLIGENCE AND DECISION SUPPORT SYSTEMS

42