MULTIVARIATE CONTROL CHARTS WITH A BAYESIAN

NETWORK

Sylvain Verron, Teodor Tiplica and Abdessamad Kobi

LASQUO/ISTIA, 62, avenue Notre Dame du Lac, 49000, Angers, France

Keywords:

SPC, Bayesian network, multivariate control charts, T

2

, MEWMA.

Abstract:

The purpose of this article is to present an approach allowing the fault detection of a multivariate process with

a bayesian network. As a discriminant analysis is easily modeled with a bayesian network, we will show that

we we can consider the multivariate T

2

and MEWMA control charts as particular cases of the discriminant

analysis. So, we give the structure of the bayesian network as well as the parameters of the network in order

to detect faults in the multivariate space in the same manners as if we used multivariate control charts. The

resulting bayesian network, with a computed threshold, is similar to the multivariate control charts.

1 INTRODUCTION

Nowadays, process control (or process monitoring) is

becoming an essential task. Indeed, processes are in-

creasingly complex and automatized (containing a lot

of sensors and actuators). As a consequence, the con-

trol of these processes is more and more difficult. In

(Chiang et al., 2001), authors give two principal ap-

proaches to perform the process control, namely, data-

driven techniques and analytical techniques. The an-

alytical technique is, in theory, the better approach. It

is based on analytical (physical) models of the sys-

tem and permits to simulate the system. Though, at

each instant, the theoretical value of each sensor can

be known for the normal operating state of the sys-

tem. As a consequence, it is relatively easy to see if

the real process values are similar to the theoretical

values. But, the major drawback of this approach is

the fact that it requires detailed models of the pro-

cess. An effective detailed model can be very dif-

ficult, time consuming and expensive to obtain, par-

ticularly for large-scale systems with many variables.

The data-driven approaches are a family of different

techniques based on the analysis of the real data ex-

tracted from the process. These methods are based on

rigorous statistical development of the process data.

We can principally cite control charts, methods based

on Principal Component Analysis (PCA), Projection

to Latent Structure (PLS) or Discriminant Analysis

(DA) (Chiang et al., 2001). The process control can

be viewed as a three-step procedure: the first one is

the fault detection that concludes on the presence of

a disturbance in the process; secondly, it is needed to

diagnosis the disturbance (fault diagnosis); finally, the

process must return in normal operation state (process

recovery).

Many data-driven techniques for the fault de-

tection can be found in the literature: univariate

statistical process control (Shewhart charts) (She-

whart, 1931), multivariate statistical process con-

trol (T

2

,Q MEWMA, MCUSUM charts) (Hotelling,

1947; Lowry et al., 1992; Pignatiello and Runger,

1990), and some PCA (Principal Component Anal-

ysis) based techniques (Jackson, 1985) like Moving

PCA (Bakshi, 1998). In (Kano et al., 2002), au-

thors make comparisons between these different tech-

niques. Other important approaches are PLS (Projec-

tion to Latent Structures) based approaches (MacGre-

gor and Kourti, 1995).

These fault detection techniques are able to detect

a fault (a disturbance) in a multivariate process. The

fault can be a shift of the mean affecting one or more

variables. For example, it can be a step or a trend.

The major drawback of these techniques is that they

do not give any indication about the root cause of a

detected fault, and so they are not fully exploitable in

228

Verron S., Tiplica T. and Kobi A. (2007).

MULTIVARIATE CONTROL CHARTS WITH A BAYESIAN NETWORK.

In Proceedings of the Fourth International Conference on Informatics in Control, Automation and Robotics, pages 228-233

DOI: 10.5220/0001641702280233

Copyright

c

SciTePress

the industry. In order to accomplish the fault diag-

nosis, many approaches have been proposed (Kourti

and MacGregor, 1996). The fault diagnosis proce-

dure can also be seen as a classification task. Indeed

today’s processes give many measurements that can

be stored in a database when the process is in con-

trol, but also in case of identified out-of-control states.

Many classifiers have been developed. We can cite

discriminant analysis like FDA (Fisher Discriminant

Analysis) (Duda et al., 2001), SVM (Support Vector

Machine) (Vapnik, 1995), kNN (k-nearest neighbor-

hood) (Cover and Hart, 1967), ANN (Artificial Neu-

ral Networks) (Duda et al., 2001) and bayesian clas-

sifiers (Friedman et al., 1997). The performances of

these classifiers are reduced in the space described by

all the variable of the process. So, before the classifi-

cation, a feature selection is often required in order to

obtain better performances.

We can see that the methods of detection and di-

agnosis are numerous. Moreover, all these methods

are heterogeneous. But, as their final goal is the same

(process recovery), they are complementary. So, it

will be of interest to have the possibility to detect and

to diagnose a fault with a single tool. An interesting

approach for the diagnosis can be the use of Bayesian

Networks (BN) (Friedman et al., 1997). In this article,

we will study a possibility to detect a fault in a multi-

variate process by modelling the multivariate control

chart with a BN. So, detection and diagnosis of a fault

would be possible on a same tool: a bayesian network.

The article is structured as follows: in the sec-

ond section, we will present the utilization of the

multivariate control charts for the detection of faults

in a multivariate process; the third section presents

some aspects on bayesian networks and particularly

on bayesian network classifiers; the fourth section

gives the procedure to model some multivariate con-

trol charts (T

2

and MEWMA), with a bayesian net-

work. In the last section, we conclude on the proposed

approach and give some outlooks.

2 MULTIVARIATE CONTROL

CHARTS

2.1 The Hotelling T

2

Control Chart

The first work in the field of fault detection in

multivariate processes began in 1947 with Hotelling

(Hotelling, 1947). He was the first to propose a mul-

tivariate control chart based on a statistical distance.

For a process with p variables, we can write the statis-

tic T

2

as:

T

2

= (x− µ)

T

Σ

−1

(x− µ) (1)

where: x is the observation vector of size 1 × p,

µ is the mean vector of size 1× p, Σ is the variance-

covariance matrix of size p× p and the symbol

T

rep-

resents the transpose of a vector or a matrix.

As we can see in the equation 1, the statistic T

2

is a scalar. So, we can plot the value of the T

2

for

different time instants, and with an appropriate con-

trol limit (computed by taking into account statistical

considerations), the T

2

control chart is obtained. On

this chart, each point represents the information ex-

tracted form all the p variables. A fault is detected

when a point is beyond the control limit.

As for the univariate Shewhart control chart, the

set up of the T

2

chart is made in two phases. During

the first phase, parameters of the process (µ and Σ)

are estimated. Concerning the computation of these

parameters estimations and the computation of the

control limit, readers can refer to the book of Mont-

gomery (Montgomery, 1997). Once the parameters

are estimated, the T

2

control chart can be drawn. It is

very important to verify that the process is in control

during the first phase. The second phase represents

the real monitoring of the process on the assumption

of a multivariate normal distribution.

2.2 The Mewma Control Chart

As in the case of the univariate Shewhart control

chart, the major drawback of the T

2

control chart

is his moderate performances to detect small mean

shifts. In order to solve this problem, other multi-

variate control charts have been proposed: MEWMA

(Multivariate Exponentially Weighted Moving Aver-

age) (Lowry et al., 1992) and MCUSUM (Multi-

variate CUmulative SUM) (Pignatiello and Runger,

1990). These charts are respectively the multivariate

analogous of the EWMA and CUSUM control charts.

The principle of the MEWMA control chart is to take

into account the process evolution in weighting past

observations extracted from the process, as indicated

in the equation 2:

y

t

= λx

t

+(I − λ)y

t−1

(2)

where λ is a p× p diagonal weighting matrix, I is

the p× p identity matrix, x

t

is the observation vector

(size 1× p) at instant t, y

0

= µ is the mean vector (size

1× p) of the p variables.

Based on the same principle than a T

2

control

chart, one can monitor the process with the statistic

given in the equation 3:

T

2

t

= y

T

t

Σ

−1

y

y

t

(3)

MULTIVARIATE CONTROL CHARTS WITH A BAYESIAN NETWORK

229

where y

t

is the transformed observation vector at

instant t, Σ

−1

y

is the inverse of the variance-covariance

matrix of y

t

. It can be concluded that the process is out

of control as soon as the T

2

t

crosses the control limit.

Bodden (Bodden and Rigdon, 1999) proposed an al-

gorithm to find the control limit in order to respect a

given number of false alarm and a given λ.

These multivariate control charts (T

2

and

MEWMA) are efficient to detect a fault in a multi-

variate process. But, as we have already said, the

fault diagnosis cannot be made in the same time. So,

it seems to be an interesting approach to do the fault

detection and the fault diagnosis of a multivariate

process by using a single tool. Several works demon-

strated that bayesian networks are able to diagnose

correctly the fault of a multivariate process. So,

it is of interest to study if a bayesian network can

accomplish the fault detection in an efficient way.

3 BAYESIAN NETWORK

CLASSIFIERS

A Bayesian Network (BN) (Jensen, 1996; Pearl,

1988) is an acyclic graph where each variable is a

node (that can be continuous or discrete). Edges of the

graph represent dependence between linked nodes. A

formal definition is given here:

A bayesian network is a triplet {G, E, D} where:

{G} is a directed acyclic graph, G = (V,A), with V

the ensemble of nodes of G, and A the ensemble

of edges of G,

{E} is a finite probabilistic space (Ω, Z, p), with Ω a

non-empty space, Z a collection of subspace of Ω,

and p a probability measure on Z with p(Ω) = 1,

{D} is an ensemble of random variables associated

to the nodes of G and defined on E such as:

p(V

1

,V

2

,...,V

n

) =

n

∏

i=1

p(V

i

|C(V

i

)) (4)

with C(V

i

) the ensemble of causes (parents) of V

i

in

the graph G.

Bayesian network classifiers are particular BN

(Friedman et al., 1997). They always have a discrete

node C coding the k different classes of the system.

Thus, other variables X

1

,...,X

p

represent the p de-

scriptors (variables) of the system.

A famous bayesian classifier is the Na

¨

ıve

Bayesian Network (NBN), also named Bayes clas-

sifier (Langley et al., 1992). This bayesian classi-

fier makes the strong assumption that the descrip-

tors of the system are class conditionally indepen-

dent. Assuming the hypothesis of normality of each

descriptor, the NBN is equivalent to the classifica-

tion rule of the diagonal quadratic discriminant analy-

sis. But, in practice, this assumption of independence

and non correlated variables is not realistic. In order

to deal with correlated variables, several approaches

have been developed. We can cite the Tree Aug-

mented Na

¨

ıve bayesian networks (TAN) (Friedman

et al., 1997). These BNs are based on a NBN but a tree

is added between the descriptors. An other interesting

approach is the Kononenko one (Kononenko, 1991),

which represent some variables in one node. As in

(Perez et al., 2006) the assumption we will make is

that this variable follows a normal multivariate distri-

bution (conditionally to the class) and we will refer to

this kind of BN as Condensed Semi Na

¨

ıve Bayesian

Network (CSNBN).

a)

X

3

X

2

X

1

X

p

…

C

b)

X

3

X

2

X

1

X

4

C

c)

X

C

Figure 1: Different bayesian network classifiers: NBN (a),

TAN (b) and CSNBN (c).

4 MULTIVARIATE CONTROL

CHARTS MODELIZED WITH

BAYESIAN NETWORK

The purpose of this article is to present a method

allowing the fault detection in a multivariate pro-

cess with the use of a BN. In the section 2, we

have presented the multivariate control charts T

2

and

MEWMA. It can be remarked that for these two

charts, one needs to compute a statistical distance on

ICINCO 2007 - International Conference on Informatics in Control, Automation and Robotics

230

the form of X

T

Σ

−1

X which is known as the square

Mahalanobis distance. This distance is also used in a

Discriminant Analysis (DA).

Indeed, one can distinguish two aspects of dis-

criminant analysis: the predictive and the classifica-

tion aspect. Given a system with p variables (descrip-

tors) and with k identified classes, the predictive dis-

criminant analysis (or Fisher discriminant analysis) is

generally used to find k − 1 new descriptors of a sys-

tem. These new k − 1 descriptors (which are a lin-

ear combination of the original descriptors) are sup-

posed to maximally discriminate between the k iden-

tified classes of the system. The other aspect of the

discriminant analysis is the classification one. The

purpose of the classification is principally to allocate

a new observation to one of the k identified classes of

the system. In the remainder of the article, the Dis-

criminant Analysis (DA) will be viewed only as a su-

pervised classification method (Duda et al., 2001).

DA is based on the Bayes decision rule. This rule

allocates a new observation x to the class C

i

with the

maximum a posteriori probability p(C

i

|x) giving the

value of each descriptor, as defined in the equation 5.

x ∈ C

i

, if i = argmax

i=1,...,k

{p(C

i

|x)} (5)

This decision rule is named ”Bayes decision rule”

because it is based on the Bayes rule which gives the

value of p(C

i

|x) as stated in 6.

P(C

i

|x) =

p(C

i

)p(x|C

i

)

p(x)

(6)

where p(C

i

) is the marginal probability of belong-

ing to the class C

i

. We can see that for each class,

the denominator of the equation 6 is the same, so, it

is not implicated in the discriminant function. Then,

equation 5 can be rewritten as:

x ∈ C

i

, if i = argmax

i=1,...,k

{p(C

i

)p(x|C

i

)} (7)

In industrial systems, it is usual to assume that

data follow multivariate normal distribution. The den-

sity function conditionally to a class C

i

can be written

as in equation 8, where µ

i

is the mean vector of the

class C

i

, Σ

i

is the covariance matrix of the class C

i

and |Σ

i

| represents the determinant of the matrix Σ

i

.

φ(x|C

i

) =

exp(−

1

2

(x− µ

i

)

t

Σ

−1

i

(x− µ

i

))

(2π)

p/2

|Σ

i

|

1/2

(8)

We remind that, for n samples, the Maximum

Likelihood Estimation (MLE) gives (Duda et al.,

2001):

ˆµ =

1

n

n

∑

i=1

x

i

(9)

and:

ˆ

Σ =

1

n− 1

n

∑

i=1

(x

i

− ˆµ)(x

i

− ˆµ)

t

(10)

So, if our system has k classes, the different prob-

abilities can be computed with equation 11.

p(x|C

i

) =

φ(x|C

i

)

k

∑

j=1

p(C

j

)φ(x|C

j

)

(11)

So, the equation 7 can be rewritten by the equation

12.

x ∈ C

i

, if i = argmax

i=1,...,k

p(C

i

)φ(x|C

i

)

k

∑

j=1

φ(x|C

j

)

(12)

At the first view, we can tell that the DA is well

suited for the fault diagnosis of industrial systems.

But, we will show that we can also realize the fault

detection methods of the multivariate control charts

with a DA, and particularly with a BN. So, to do that

we will consider the multivariate control charts as a

DA where the goal is to attribute a class (in or out of

control) to a new observation of the system. Realising

a DA with a BN is very simple. The structure of the

network will be composed of a class node (discrete

variable) with two modalities (in or out of control). In

order to represent the different descriptors of the sys-

tem, we use only one normal multivariate variable.

This normal multivariate variable will represent the x

for the T

2

chart and the y

t

for the MEWMA chart.

To resume, we will obtain a structure similar to the

CSNBN.

However, an essential question we remain con-

cerning the parameters of the network. We have to

fix a normal multivariate distribution for each classes

of the problem. The distribution of the ”in control”

state will be N(µ, Σ). In order to obtain a decision

boundary between the two states of the process, we

fix the distribution of the ”out of control” state to

N(µ,c × Σ), where c is a coefficient different than 1.

These two distributions will have same center (µ) and

same shape (because c× Σ is simply a scale extend-

ing of the shape of Σ). The difference between the two

states can be expressed as: scattering about the ”out

of control” state (OC) is more important than scatter-

ing about the ”in control” state (IC). We can represent

MULTIVARIATE CONTROL CHARTS WITH A BAYESIAN NETWORK

231

−5 −4 −3 −2 −1 0 1 2 3 4 5

−5

−4

−3

−2

−1

0

1

2

3

4

5

Out of Control

"OC"

In Control

"IC"

Control Limit

Figure 2: Example of the classification areas.

the classification areas of the two states of the system

for a bivariate example like in the figure 2.

Usually, in the frame of Statistical Process Con-

trol (SPC) techniques, one has to choose a risk factor

α in order to correctly control the process. In the case

of the BN, we have to fix a probability threshold τ al-

lowing to not badly reject some situations ”in control”

(false alarms).

Otherwise the threshold τ is computed in order to

have similar classification areas than those of the mul-

tivariate control chart. We will name CL the control

limit for the control charts and we supposed that CL is

known for each chart, see (Montgomery, 1997; Lowry

et al., 1992). The τ probability limit corresponds to

the probability, for the class ”OC”, of the x

CL

value

which is an observation giving a T

2

equal at the con-

trol limit CL. We will assume that the marginal prob-

abilities of the two classes are unknown and so are

fixed to 0.5 each. So, p(IC) = p(OC) = 0.5.

τ = p(IC|x

CL

)

=

p(OC)φ(x

CL

|OC)

p(IC)φ(x

CL

|IC) + p(OC)φ(x

CL

|OC)

=

φ(x

CL

|OC)

φ(x

CL

|IC) + φ(x

CL

|OC)

(13)

By using equation 8 in the previous equation, and

after simplification, we will obtain the equation of τ

as:

τ =

exp(−0.5

CL

c

)

c

p/2

exp(−0.5CL) +

exp(−0.5

CL

c

)

c

p/2

(14)

In conclusion, for the BN, we will obtain the fol-

lowing decision rule: if p(OC|x) ≥ τ, then the pro-

cess is out-of-control (OC), otherwise the process is

in control (IC).

In order to use the previous result, we have taken

a simple example of a 5 variables system. The param-

eters of the system is given as:

µ = [510]

Σ =

1 1.2

1.2 2

We have simulated the system during 30 observa-

tions, but at the observation number 6, a step of mag-

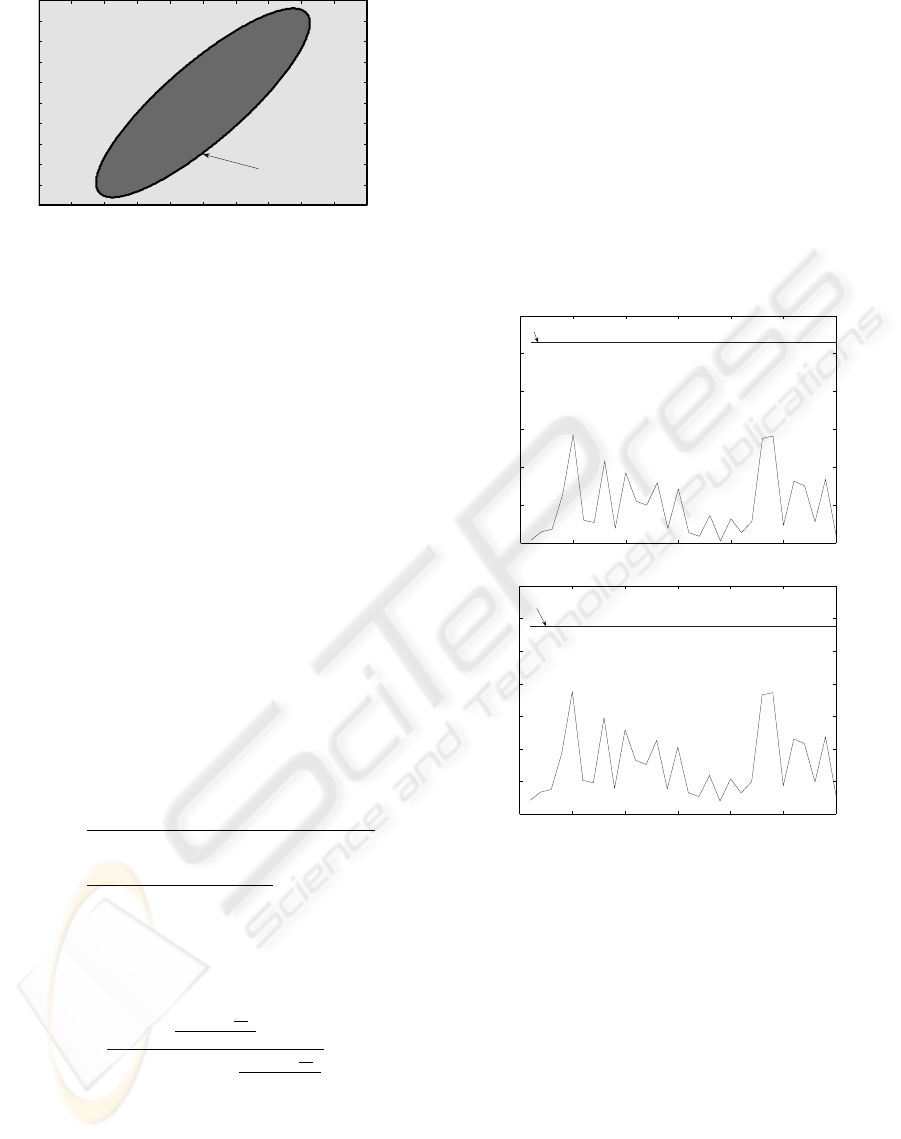

nitude 0.5 is introduced in the process. In the figure

3 we are presenting the detection of the fault with the

control chart (upper graph) and with the BN approach

(lower graph). In a similar way, the figure 4 represents

the result of the MEWMA approach.

0 5 10 15 20 25 30

0

2

4

6

8

10

12

Observations

T

2

CL

T

2

0 5 10 15 20 25 30

0.4

0.5

0.6

0.7

0.8

0.9

1

Observations

p(OC|x)

τ

Figure 3: Results with the T

2

chart and the T

2

chart by BN

apporach.

On the figure 3 and 4, we can see that for each

multivariate charts, the BN approach gives the same

results than the specified chart (with a scaling factor).

So, we can conclude that the different multivariate

control charts (T

2

and MEWMA) can be easily mod-

eled with a BN.

5 CONCLUSIONS AND

OUTLOOKS

In this article, after an introduction on the process

control (and particularly on the data-driven tech-

niques for the detection and the diagnosis), we have

ICINCO 2007 - International Conference on Informatics in Control, Automation and Robotics

232

0 5 10 15 20 25 30

0

2

4

6

8

10

12

14

Observations

T

2

mewma

CL

mewma

0 5 10 15 20 25 30

0.4

0.5

0.6

0.7

0.8

0.9

1

Observations

p(OC|y)

τ

mewma

Figure 4: Results with the MEWMA chart and the

MEWMA chart by BN approach.

outlined the problem that there is not a single tool able

to perform both: the fault detection and the fault di-

agnosis of a system. As a bayesian network can be an

efficient way to diagnosis a fault, it is natural to see

how this tool can also execute the fault detection task.

We have selected two fault detection techniques: the

T

2

chart and the MEWMA chart. We have demon-

strated that these charts can be viewed as a discrimi-

nant analysis and so can be implemented in a simple

bayesian network.

The evident outlook to this work is the full study

of the use of BN in order to monitor and control a

multivariate process.

REFERENCES

Bakshi, B. R. (1998). Multiscale PCA with application

to multivariate statistical process monitoring. AIChE

Journal, 44(7):1596–1610.

Bodden, K. and Rigdon, S. (1999). A program for approxi-

mating the in-control arl for the mewma chart. Journal

of Quality Technology, 31(1):120–123.

Chiang, L. H., Russell, E. L., and Braatz, R. D. (2001).

Fault detection and diagnosis in industrial systems.

New York: Springer-Verlag.

Cover, T. and Hart, P. (1967). Nearest neighbor pattern clas-

sification. IEEE Transactions on Information Theory,

13:21–27.

Duda, R. O., Hart, P. E., and Stork, D. G. (2001). Pattern

Classification 2nd edition. Wiley.

Friedman, N., Geiger, D., and Goldszmidt, M. (1997).

Bayesian network classifiers. Machine Learning,

29(2-3):131–163.

Hotelling, H. (1947). Multivariate quality control. Tech-

niques of Statistical Analysis, :111–184.

Jackson, E. J. (1985). Multivariate quality control. Com-

munication Statistics - Theory and Methods, 14:2657

– 2688.

Jensen, F. V. (1996). An introduction to Bayesian Networks.

Taylor and Francis, London, United Kingdom.

Kano, M., Nagao, K., Hasebe, S., Hashimoto, I., Ohno,

H., Strauss, R., and Bakshi, B. (2002). Comparison

of multivariate statistical process monitoring methods

with applications to the eastman challenge problem.

Computers and Chemical Engineering, 26(2):161–

174.

Kononenko, I. (1991). Semi-naive bayesian classifier. In

EWSL-91: Proceedings of the European working ses-

sion on learning on Machine learning, pages 206–

219.

Kourti, T. and MacGregor, J. F. (1996). Multivariate spc

methods for process and product monitoring. Journal

of Quality Technology, 28(4):409–428.

Langley, P., Iba, W., and Thompson, K. (1992). An analy-

sis of bayesian classifiers. In National Conference on

Artificial Intelligence.

Lowry, C. A., Woodall, W. H., Champ, C. W., and Rig-

don, S. E. (1992). A multivariate exponentially

weighted moving average control chart. Technomet-

rics, 34(1):46–53.

MacGregor, J. and Kourti, T. (1995). Statistical process

control of multivariate processes. Control Engineer-

ing Practice, 3(3):403–414.

Montgomery, D. C. (1997). Introduction to Statistical Qual-

ity Control, Third Edition. John Wiley and Sons.

Pearl, J. (1988). Probabilistic Reasoning in Intelligent Sys-

tems: Networks of Plausible Inference. Morgan Kauf-

mann Publishers.

Perez, A., Larranaga, P., and Inza, I. (2006). Super-

vised classification with conditional gaussian net-

works: Increasing the structure complexity from naive

bayes. International Journal of Approximate Reason-

ing, 43:1–25.

Pignatiello, J. and Runger, G. (1990). Comparisons of mul-

tivariate cusum charts. Journal of Quality Technology,

22(3):173–186.

Shewhart, W. A. (1931). Economic control of quality of

manufactured product. New York : D. Van Nostrand

Co.

Vapnik, V. N. (1995). The Nature of Statistical Learning

Theory. Springer.

MULTIVARIATE CONTROL CHARTS WITH A BAYESIAN NETWORK

233