OUTLINING VALUE ASSESSMENT FOR SOFTWARE

REQUIREMENTS

Pasi Ojala

Hintanmutka 17 A 6, Oulu, Finland

Keywords: Software requirements, assessment, value, worth, cost and Value Engineering.

Abstract: Understanding software requirements and customer needs is vital for all SW companies around the world.

Lately clearly more attention has been focused also on the costs, cost-effectiveness, productivity and value

of software development and products. This study outlines concepts, principles and process of implementing

a value assessment for SW requirements. The main purpose of this study is to collect experiences whether

the value assessment for product requirements is useful for companies, works in practice, and what are the

strengths and weaknesses of using it. This is done by implementing value assessment in a case company

step by step to see which phases possibly work and which phases possibly do not work. The practical

industrial case shows that proposed value assessment for product requirements is useful and supports

companies trying to find value in their products.

1 INTRODUCTION

According to Ojala (2006) the objective of the

value-based approach is to explore ways to eliminate

value loss in software development, software

products, and software process improvement (SPI)

using the value assessment framework of Koskela

and Huovila (1997). Value-based approach uses

economic-driven tools, which are based on

economic studies including, for example, the areas

of cost estimation, cost calculation (for example

ABC and life cycle costing) and investment

calculation. The value-based approach prefers

calculating costs instead of estimating them, and

also considers software development and SPI as

investments, on which it is possible to spend too

much money. In practice, it takes care that the

customer requirements are met in the best possible

manner, ensuring quality, timeliness and value in

products as well as in processes, over their entire life

cycle.

The value-based approach indicates a clear

dependency between the process and products. It

sees that we need to develop and optimize process

activities so that processes produce the products

needed. Furthermore, it sees that we must analyze

products in order to reveal problems in processes

and develop processes from the product point of

view as well. This is vitally important, especially for

companies respecting customer opinions and aiming

to optimize costs in their processes, because the

customers are the ones paying for the products and

product-related services, and companies have to

allocate all costs to products to be able to price them.

The purpose of this study is to collect experiences

of using value assessment for product requirements

in an industrial case. In more detail the purpose is to

answer to following questions:

• How the proposed value assessment for

product requirements works in practice

• The strengths and weaknesses of value

assessment for product requirements

• Whether the company assessed sees the

value assessment for product requirements

useful

2 VALUE ENGINEERING

PROCESS

This study categorizes VE process into three main

phases: pre-study (orientation), value study

(information, function analysis, creativity,

evaluation, development, presentation), and post-

445

Ojala P. (2008).

OUTLINING VALUE ASSESSMENT FOR SOFTWARE REQUIREMENTS.

In Proceedings of the Tenth Inter national Conference on Enterprise Information Systems - DISI, pages 445-448

DOI: 10.5220/0001690204450448

Copyright

c

SciTePress

study (monitoring, implementation). These phases

are considered appropriate since they constitute

independent areas of VE and have been justified in

earlier discussion (Ojala, 2006).

According to Value Engineering, value is a

measure – usually in currency, effort or exchange, or

on a comparative scale – which reflects the desire to

obtain or retain an item, service or ideal. Cost is the

price paid or to be paid. It can be divided into

elements and, to some extent, functions. Park (1999,

50) defines cost as “an expenditure of money, time,

labor, etc., to obtain a requirement.” Worth is usually

defined as the lowest cost to perform the required

function, or the cost of the lowest-cost functional

equivalent. The most typical definition for value

(Ojala, 2006), is perhaps (1):

(1)

where:

Value = The value of some object, product, service

or process.

Worth = The least cost to perform the required

function (product, service or process), or the cost of

the least cost functional equivalent. If possible can

also be the worth in money, what customer sees in

product, service or process.

Cost = The life cycle cost of the object, product,

service or process (price paid or to be paid).

3 VALUE ASSESSMENT FOR

PRODUCT REQUIREMENTS

3.1 Background

Value assessment for product requirements was

implemented in a multinational company producing

electronic products in fall 2006. The basis of it was

the requirement list done by customer and vendor

together. The requirement list contained

requirements such as: picture call, emergency, user,

server, distance configuration, video, service,

camera and activities.

Together with the requirement lists, several other

documents were analyzed during the assessment as

well. These documents included strategy plans,

project plans, process descriptions, selling

agreement and different financial statements.

3.2 Information

The product to be assessed was a electronic product

containing software and hardware. It was developed

in collaboration, by the vendor and the customer. In

the assessment opening meeting, the purpose of the

assessment was discussed with the vendor and the

customer. The definition value=worth/cost was

discussed, and it was seen as extremely important to

find out which requirements of the product gave the

best value to the vendor without neglecting customer

needs. The customer had a strong interest in

analyzing priorities and worth in requirements, for

further product development work. After the

discussion, it was decided that value would be

calculated for the requirements described in the

product sales agreement. This decision was strongly

supported because the vendor’s cost accounting

system made it possible to track real costs for the

specified requirements.

As a final point of the initial meeting, vendor and

customer roles were discussed. The vendor

emphasized that it would like to undertake the

phases from creativity to presentation without the

customer being present, since these phases included

brainstorming to gain a new understanding of all the

processes used to develop products. This point of

view was clearly understood by both parties, as the

customer was primarily interested in evaluating

requirement priorities, in order to see how well the

vendor had understood their wishes.

3.3 Function Analysis

After the initial meeting it was easy to “start the

assessment”, because the requirements to be

assessed were agreed in the information phase. In

the first assessment meeting four customer

representatives (referred to as “customers”) and

three vendor representatives (referred to as

“vendors”) prioritized the requirements. Afterwards,

the customers allocated worth to each requirement

using a percentage scale from 0% to 100%. The idea

was to identify in percentages what kind of worth

the customer sees in the requirements. The vendors

allocated costs using the same percentage scale from

0% to 100%. As a result of this, the customers had

given worth percentages for all requirements, and

the vendors had given cost percentages for the same

items. The calculated worth and cost were later

compared, using percentages, to the real worth and

cost, to find out the difference between “belief” and

“reality”.

All the interviewees agreed that the prioritization

of requirements clearly helped in the next phase, in

which the same requirements were analyzed in terms

ICEIS 2008 - International Conference on Enterprise Information Systems

446

of worth and cost. The customers found it easy to

assign worth to their requirements, based on the

customer price. The vendors also considered it easy

to assign costs to requirements.

One conclusion of discussions was that worth and

cost allocations for all requirements were seen as

relevant for both sides, even if only stated as

percentages. According to customer they also had

their own idea about the actual costs of production,

and since they knew the worth they were satisfied

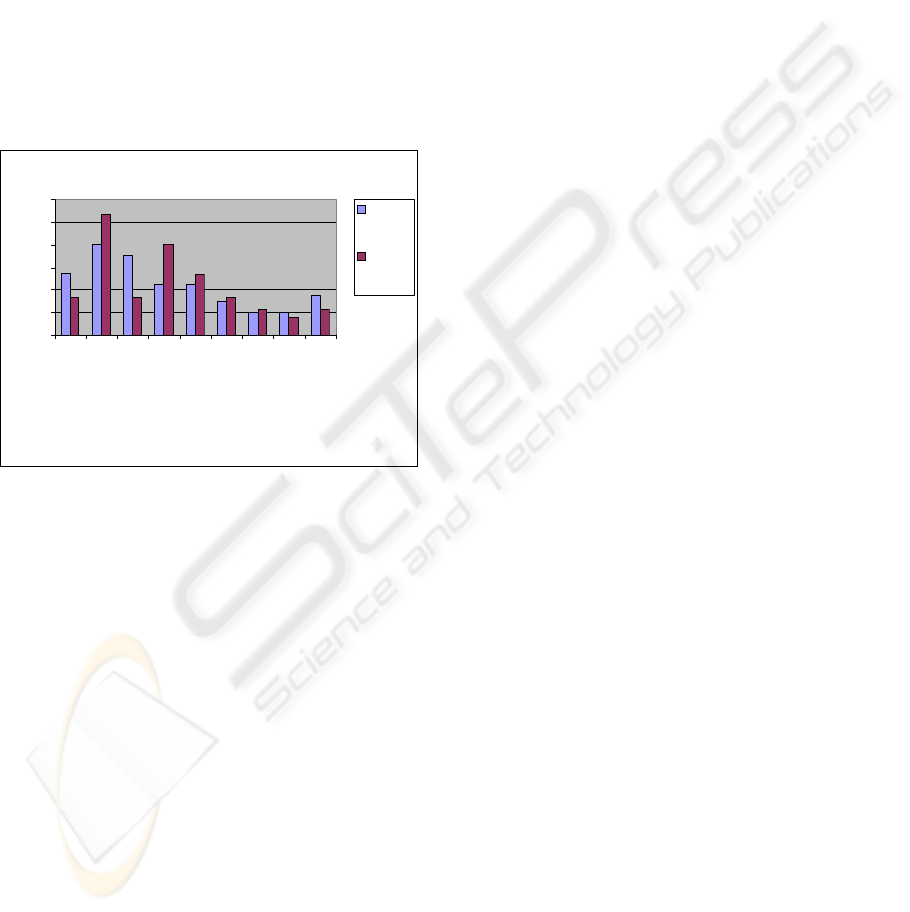

for the situation. Figure 1 presents the average worth

and cost for requirements. In this figure we can

observe how, for example, the customer has

evaluated the worth of picture call function as being

noticeably higher than the vendor’s estimation of its

production cost. In practice, this means value for the

vendor.

Figure 1: Average worth and cost for requirements

including all interviewees (AV=average, C=customer,

V=vendor).

On the whole, the experiences of using

prioritization in ranking requirements were positive.

Even more interest was seen in the analysis of worth

and cost for each requirement, and especially in the

differences identified between customer and vendor,

as well as between technical- and user-oriented

personnel.

3.4 Creativity

In accordance with the agreement between the

customer and the vendor, only the vendor

participated in the phases from creativity to

presentation. The first step in the creativity phase

was to allocate costs to all requirements. According

to the vendor it was easy to allocate costs to the

requirements.

Based on the figures and discussion it was noted

that certain requirements did not create good value.

After discussion of this, the project members shared

the opinion that this was because of the unfinished

architectural plan.

Project members could also see from the charts

presented how time-consuming it was to start using

new technical environments, without good planning.

The new technical environment delayed the

implementation of certain requirements

significantly. New technical challenges, such as

developing software for multiprocessor

environments, were also named as one reason for

delays. This was because project personnel did not

have sufficient training in working in the

multiprocessor environment.

3.5 Evaluation

At the beginning of the evaluation phase the project

team discussed criteria for the evaluation of

improvement ideas. The calculated weighted

averages for criteria based on discussion were as

follows: system stability 25 %, safety 20 %,

optimized functioning 7.5 %, ease of use 20 %,

maintainability 15 %, and profitability 12.5 %.

After thus defining the weightings of the criteria,

the project personnel gave points to each

improvement proposal on a scale of one to six,

where six indicated maximum points and one,

minimum. The points allocated were multiplied by

the calculated weighting percentages.

The most surprising result was that the importance

of the technical environment was as high as third

place. Problems in design and architectural planning

were expected, as were problems related to project

management. Estimation and multiprocessing got

the least points, so their importance to the project

was not considered to be as high.

3.6 Development

In the development phase, the improvement ideas

were separately developed further, in order to

examine their practical implications.

Architectural Plan and Design Plans. One

proposed change was that the number of reviews for

the architectural and design plans had to be

increased. Project personnel also identified a clear

need to develop criteria for these review rounds.

Project members did not see any disadvantages to

the proposal. They calculated that if there had been

support resources for making more comprehensive

plans and reviewing them, the project would have

been 440 working hours shorter. The potential cost

savings would have been about 26 000 €.

Worth & Cost in Requirements

0.0

5.0

10.0

15.0

20.0

25.0

30.0

P

ic

t

u

re

ca

l

l

E

m

er

ge

n

cy

User

S

e

rve

r

D

i

stan

c

e

c

onf

i

g

u

ra

t

ion

Vi

d

e

o

Service

Cam

e

ra

Ac

t

i

vi

t

i

e

s

Requirement

%

C AV

Worth

(%)

V AV

Cost (%)

OUTLINING VALUE ASSESSMENT FOR SOFTWARE REQUIREMENTS

447

Technical Environment. At the moment, the ability

to use the existing characteristics of technical tools

is weak. The use of pre-existing components is also

rather poor. The result is that code has to be written

from start to finish each time.

The project group evaluated that if basic

components for development work had existed, 100

fewer working hours would have been required. If

there had been sufficient technical training

concerning the new environments (dotNET and ATL

7) for key personnel, 150 fewer working hours

would have been required. In total, the potential cost

savings would have been approximately 9 000 €.

Project Management. From a project management

point of view, it is problematic that all the

employees are always assigned one hundred percent

to a given project. As a consequence, there is not

enough support available if needed, and “the wheel

is invented several times in different projects.”

The project team evaluated that with satisfactory

support in evaluating the architectural plan, the

design plans, and the extra need for time in starting

to use new technologies, 100 fewer working hours

would have been required. In financial terms, this

would have meant a saving of about 6 000 €.

3.7 Presentation

The results of the product value assessment were

presented phase by phase to the high-level

management. In the presentation, a clear emphasis

was placed on presenting customer needs and wants,

and the corresponding costs to the company. The

value indexes were used to outline the existing

value-increasing opportunities. The potential cost

saving proposed was approximately 26% of product

price.

As a whole, the assessment strongly emphasized

collaboration between the customer and the vendor,

and all the improvement proposals were in line with

the customer’s interests as well. All customer and

vendor representatives considered product

assessment an interesting method for the

development of product quality and value, and

process capability.

4 CONCLUSIONS

Presented product assessment for requirements

worked very well in practice. All participants agreed

that the value assessment process was clear and

practical for their use. Vendor saw it important that

the customer was involved to the assessment as it

increased the efficient use of resources and brought

more business point of view to the assessment,

which was considered to be extremely important.

The product assessment for requirements gave

more customer-oriented improvement proposals than

process assessments. Product assessment also

involved the customer in the decision process so that

described requirements were in a more solid basis to

be implemented. All participants also emphasized

that if value assessment is done in the planning

phase of a product, it is cheaper for any company

than making changes after several months of

development work.

There were also weaknesses in the proposed value

assessment for requirements. Firstly, the empirical

findings of this study are rather limited as this study

bases on one industrial case. Secondly, some costs

had to be estimated instead of having calculated

actual costs.

Generally, all the assessment results in this

assessment are reliable. The reliability of the results

was also improved significantly because the assessor

interviewed several people and went through the

same questions with all of them. The interview

results were also compared to existing written

material to check that they matched.

REFERENCES

Erdogmus H, Cusumano MA, Kontio JG & Raffo D

(2004). The sixth International Workshop on

Economics-Driven Software Engineering Research

(EDSER-6). Proceedings of the 26th International

Conference on Software Engineering (ICSE 04).

Edinburg, Scotland. IEEE Computer Society. 761-762.

Koskela, L., Huovila, P., “On foundations of Concurrent

Engineering in Construction CEC’97. London, 3-4

July. London, The Institution of Structural Engineers,

1997, pp. 22-23.

Ojala, P., Implementing a Value-Based Approach to

Software assessment and Improvement. Doctoral

dissertation. University of Oulu, 2006.

Park R Value Engineering. A Plan for Invention. New

York, St. Lucie Press, 1999.

Solingen R Measuring ROI of Software Process

Improvement. IEEE Software May, 2004, pp. 32-38

ICEIS 2008 - International Conference on Enterprise Information Systems

448