A CONSOLIDATED ENTERPRISE REFERENCE MODEL

Integrating McCarthy’s and Hruby’s Resource-Event-Agent Reference Models

Wim Laurier, Maxime Bernaert and Geert Poels

Department of Management Information Systems and Operations Management

Faculty of Economics and Business Administration, Ghent University, Tweekerkenstraat 2, 9000 Ghent, Belgium

Keywords: Reference Model, Resource-Event-Agent, Ontology.

Abstract: This paper introduces a new Resource-Event-Agent (REA) reference model that integrates the transaction

and conversion reference models provided by McCarthy, which aimed at designing databases for accounting

information systems, and Hruby, which aimed at software development for enterprise information systems,

into a single conceptual model that accounts for both inter-enterprise and intra-enterprise processes. This

consolidated reference model was developed to support data integration between multiple enterprises and

different kinds of enterprise information systems (e.g. ERP, accounting and management information

systems). First, the state of the art in REA reference models is addressed, presenting McCarthy’s and

Hruby’s reference models and assessing their ability to represent exchanges (e.g. product for money),

transfers (e.g. shipment) and transformations (e.g. production process). Second, the new, consolidated REA

enterprise reference model is introduced. Third, object model templates are presented, demonstrating that

the consolidated REA reference model is able to represent exchanges, transfers and transformations, where

McCarthy’s and Hruby’s reference models can each only represent two of these features.

1 INTRODUCTION

In the past, business modelling focused on the

enterprise’s value chain as the core structure in

business that needed to be supported by information

systems. These value chains consist of value

activities (e.g. a production process). The value

chain of a company is embedded in a value system,

which includes the value chains of suppliers and

customers. (Porter and Millar, 1985) The focus of

business modelling on the enterprise’s value chain

resulted in the development of enterprise-wide

information systems. However, a continuously faster

globalizing world economy and increasing

cooperation among supply chain partners increases

the need to model the entire value system (e.g.

supply chain) and not just individual players within

it. (Giachetti, 1999)

We can currently discriminate two kinds of

reference models. First, models that support intra-

enterprise processes and abstract from interactions

between trading partners. (Jansen-Vullers et al.,

2003) Second, models that support inter-enterprise

transactions and abstract from the internal business

of the involved partners. (Shin and Leem, 2002)

What is needed is a reference model that allows

each enterprise taking part in a value system to

develop its own value chain information system and

at the same time supports the creation of system

interoperability and information sharing amongst

supply chain partners.

In this paper, a new enterprise reference model

that is based on the REA enterprise ontology (Geerts

and McCarthy, 2002, Geerts and McCarthy, 2004) is

proposed. The reference model integrates both

enterprise perspectives (i.e. transactions and

processes) in a single reference model. This

reference model integrates the features of the

reference models in McCarthy’s (1982) foundational

REA article, which focuses on transactions between

individual enterprises by representing the exchange

of resources (e.g. money for product) and the

resulting resource transfers between trading partners,

and Hruby’s (2006) book on business patterns

design, which focuses on the processes inside an

enterprise by representing exchanges and

conversions (i.e. process input becomes process

output).

Section 2 discusses McCarthy’s and Hruby’s

REA reference models and their specific

159

Laurier W., Bernaert M. and Poels G. (2010).

A CONSOLIDATED ENTERPRISE REFERENCE MODEL - Integrating McCarthy’s and Hruby’s Resource-Event-Agent Reference Models.

In Proceedings of the 12th International Conference on Enterprise Information Systems - Information Systems Analysis and Specification, pages

159-164

DOI: 10.5220/0002871701590164

Copyright

c

SciTePress

characteristics. Section 3 presents the new,

consolidated REA reference model and a number of

object models for transfers, exchanges and

transformations that instantiate this consolidated

reference model. Section 4 presents conclusions.

2 STATE OF THE ART

The REA ontology knows three main primitives,

namely economic resource, economic event and

economic agent, which are abbreviated to resource,

event and agent in the remainder of this paper.

Resources in the REA ontology are defined as

goods, services or rights that have utility and are

scarce and under the control of a legal or natural

person (McCarthy, 1982, ISO/IEC, 2007). Events

are occurrences in time that relate subsequent

process states to each other and involve gaining (i.e.

increment) or losing (i.e. decrement) control over

economic resources (McCarthy, 1982, ISO/IEC,

2007). Agents are natural or legal persons (e.g.

employee, customer) that are accountable for,

participate in or initiate economic events.

2.1 McCarthy’s Reference Model

Fig. 1 shows a modernised version of McCarthy’s

foundational reference model (McCarthy, 1982) as it

appears in ISO’s business transaction scenario

standard (ISO/IEC, 2007). This model differs from

the initial model by decomposing the n-ary ‘control’

relation in two binary participation (i.e. agent-event)

relations, conforming to Weber’s critique (Weber,

1986), and the merger of the economic agent and its

subclass economic unit in the A

GENT

class.

Figure 1: McCarthy’s REA Reference Model.

The S

TOCK

-F

LOW

association between the

R

ESOURCE

and E

VENT

classes in fig. 1 shows which

resources are involved in and affected by which

events. The I

NCREMENT

-D

ECREMENT

association in

fig. 1 represents the duality relationship between two

events (i.e. one increment and one decrement). This

duality balances the changes in resources due to

events representing the principle of economic

reciprocity, which requires adequate compensation

(i.e. increment event) (e.g. payment received) for

lost resources (i.e. decrement event) (e.g. resource

shipments). (McCarthy, 1982) The E

XCHANGE

-

I

NSIDE

_P

ARTY

association reveals the agent whose

view determines which events are increments and

which are decrements. The E

XCHANGE

-

O

UTSIDE

_P

ARTY

association relates the inside

party’s counterparty to the economic event.

With McCarthy’s foundational reference model,

exchange and transfer object models can be

constructed. Fig. 2 shows a template that integrates

the views of both trading partners. We recognise two

resource transfers with opposite directions (i.e. one

represents a cash inflow for the vendor and a cash

outflow for the buyer; one represents inventory

goods inflow for the buyer and a goods outflow for

the seller). We also discriminate two mirrored

exchange templates (i.e. ‘cash for goods’ in the

buyer’s purchase and cash disbursement duality,

‘goods for cash’ in the vendor’s sale and cash receipt

duality).

Modelling a transfer of resources between the

inventories of two trading partners, a transfer model

relates the corresponding mirrored events in an

exchange with each other. This mirroring relation is

mediated by a resource object for which one event

represents an inflow (e.g. P

URCHASE

) and the

mirroring event represents and outflow (e.g. S

ALE

).

Although the agents connected to the mirrored

events are the same, the inside and outside party

roles are switched, which represents the opposing

economic interests of the trading partners (i.e.

S

ELLER

and B

UYER

). Also note that the mirroring

relation between the buyer’s view on an event and

the vendor’s view on the same event is implicit in

fig. 2. The downside of this representation is that

real events are artificially decomposed (e.g.

purchase and sale are actually two views on the

same event).

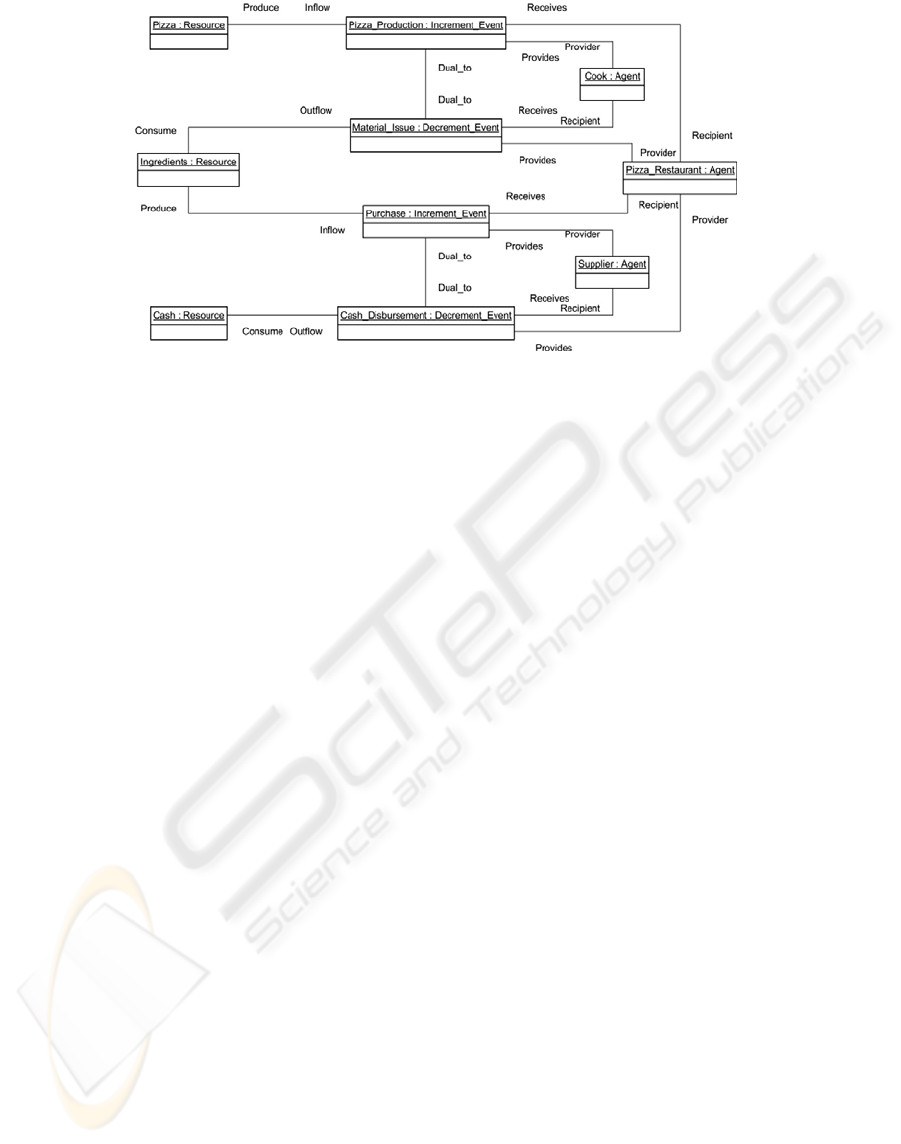

2.2 Hruby’s Reference Model

Fig. 3 shows Hruby’s (2006) reference model. By

explicitly discriminating increment and decrement

events, it differs from McCarthy’s reference model,

which chooses to represent increment and decrement

as roles of events and not as kinds of events.

Hruby’s reference model also incorporates

provide (i.e. P

ROVIDER

-P

ROVIDE

) and receive (i.e.

R

ECIPIENT

-R

ECEIVE

) relationships that connect

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

160

Figure 2: McCarthy’s Integrated View Exchange.

Figure 3: Hruby’s REA Reference Model.

agents with increment and decrement events. The

provide relationship relates the event to the agent

that experiences a resource decrement and the

receive relationship relates the event to the agent

that experiences a resource increment.

Consequently, a provide relationship relates a

decrement event to the agent that experiences the

decrement (i.e. inside party in McCarthy’s model)

and a receive relationship relates an increment event

with the agent that experiences the increment (i.e.

inside party in McCarthy’s model). Table 1

summarises these view relations between agents and

events, and the conceptual differences for the

participation relation (i.e. agent-event) in

McCarthy’s and Hruby’s reference models.

Table 1: Provider and Recipient as Inside and Outside

Agent.

Agent

Event

Increment Decrement

Provider Outside Part

y

Inside Part

y

Recipient Inside Party Outside Party

The duality (i.e. D

UAL

_

TO

-D

UAL

_

TO

) relation

between the I

NCREMENT

_E

VENT

and

D

ECREMENT

_E

VENT

classes is identical to the

duality in McCarthy’s model except for the fact that

it relates distinct classes and not one event class that

plays distinct roles. Finally, Hruby decomposes

McCarthy’s stock-flow relation into consume (i.e.

O

UTFLOW

-C

ONSUME

), use (i.e. O

UTFLOW

-U

SE

) and

produce (i.e. I

NFLOW

-P

RODUCE

) relations. The

difference between the use and consume outflow

relations is that use relations temporary occupy a

resource without affecting its ability to participate in

subsequent decrement events, while consume

relations indicate that a resource is no longer

available for further decrements. Hence, Hruby

incorporates part of McCarthy’s model logic in his

reference model (i.e. events in an outflow role are

decrement economic events and events in an inflow

role are increment economic events).

The basic value creating processes in an

enterprise can be categorised as acquisition,

conversion and revenue generating processes, which

construct an enterprise’s value chain (McCarthy,

2003). Fig. 4 integrates an acquisition process with

A CONSOLIDATED ENTERPRISE REFERENCE MODEL - Integrating McCarthy's and Hruby's Resource-Event-Agent

Reference Models

161

Figure 4: Hruby’s REA Value Chain.

a conversion process. The acquisition process shows

how ingredients are purchased in return for cash.

The conversion process represents the conversion of

ingredients into pizza. The acquisition part of fig. 4

shows the exchange of C

ASH

and I

NGREDIENTS

between the P

IZZA

_R

ESTAURANT

and its S

UPPLIER

.

The conversion part of fig. 4 shows the

transformation of I

NGREDIENTS

into P

IZZA

that is

performed by the C

OOK

for the P

IZZA

_R

ESTAURANT

.

Hruby’s exchange template is fairly identical to

McCarthy’s articulation (i.e. part of fig. 2). The

main difference is that the increment and decrement

roles in McCarthy’s model are replaced by specific

classes. The inside and outside party roles on the

participation relations in McCarthy’s model have

also been replaced by provider and recipient roles.

The conversion model that represents (part of) a

production process, on the other hand, is not

incorporated in McCarthy’s version of REA. The

conversion is represented as an implicit exchange

between process inputs (i.e. I

NGREDIENTS

) and

process outputs (i.e. P

IZZA

), where the employer (i.e.

P

IZZA

_R

ESTAURANT

) provides the inputs and

receives the outputs from the employee (i.e. C

OOK

)

and the employee receives the inputs and provides

the outputs to the employer. The conversion process

itself is modelled as a duality between one or more

decrement events that use or consume input

resources and one or more increment events that

produce output resources. The downside of this kind

of representation is that conversion processes are

represented as exchanges, while employees never

own the resources they work with, and that

conversion processes are artificially decomposed in

a collection of increment and decrement events.

3 CONSOLIDATED REFERENCE

MODEL

A remarkable feature of both McCarthy’s and

Hruby’s reference models is that they both use the

agent concept to model trading partners and event

performers. The downside of this choice is that

trading partners cannot be explicitly discriminated

from pure event performers (e.g. the trucker cannot

be discriminated from the enterprise that ships the

goods). To allow for this discrimination, we

reintroduce the concept of economic unit that was

removed from McCarthy’s original reference model

as a synonym for the agent concept. Therefore, the

agent and economic unit concepts need to be

redefined. We redefine an Agent as the natural

person that executes the event and an Economic Unit

as the legal or natural person that loses or gains

control over resources in decrement and increment

events respectively. Consequently, economic units,

which were originally defined as a subclass of

Agents (McCarthy, 1982), determine the scope of

the context in which economic activities take place.

This new definition also fits McCarthy’s original

model, where economic units are inextricably bound

with the inside party role that determines which

events are classified as increments (i.e. gaining

control over resources) and decrements (i.e. losing

control over resources). Therefore, we consider our

economic unit and agent definitions more robust

descriptions of semantics that were already

implicitly present in the original REA model.

Fig. 5 reflects the key role of the economic unit

concept in our reference model. In this reference

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

162

Figure 5: Our REA Reference Model.

Figure 6: REA Consolidated View Exchange Model.

model, the economic unit defines the duality that

connects the explicitly modelled increment and

decrement roles for the event that forms the centre of

our reference model. The agents in this reference

model participate in events, meaning that they

execute events without experiencing their economic

consequences (i.e. gaining or losing control over

resources). These consequences are experienced by

the economic units and explicitly represented by the

I

NCREMENT

and D

ECREMENT

classes in the reference

model that mediate between the E

CONOMIC

_U

NIT

and the R

ESOURCE

over which it gains or loses

control. The reference model (fig. 5) also reveals

that a single E

VENT

can be viewed as an increment

and decrement at the same time, by the same or

different economic units.

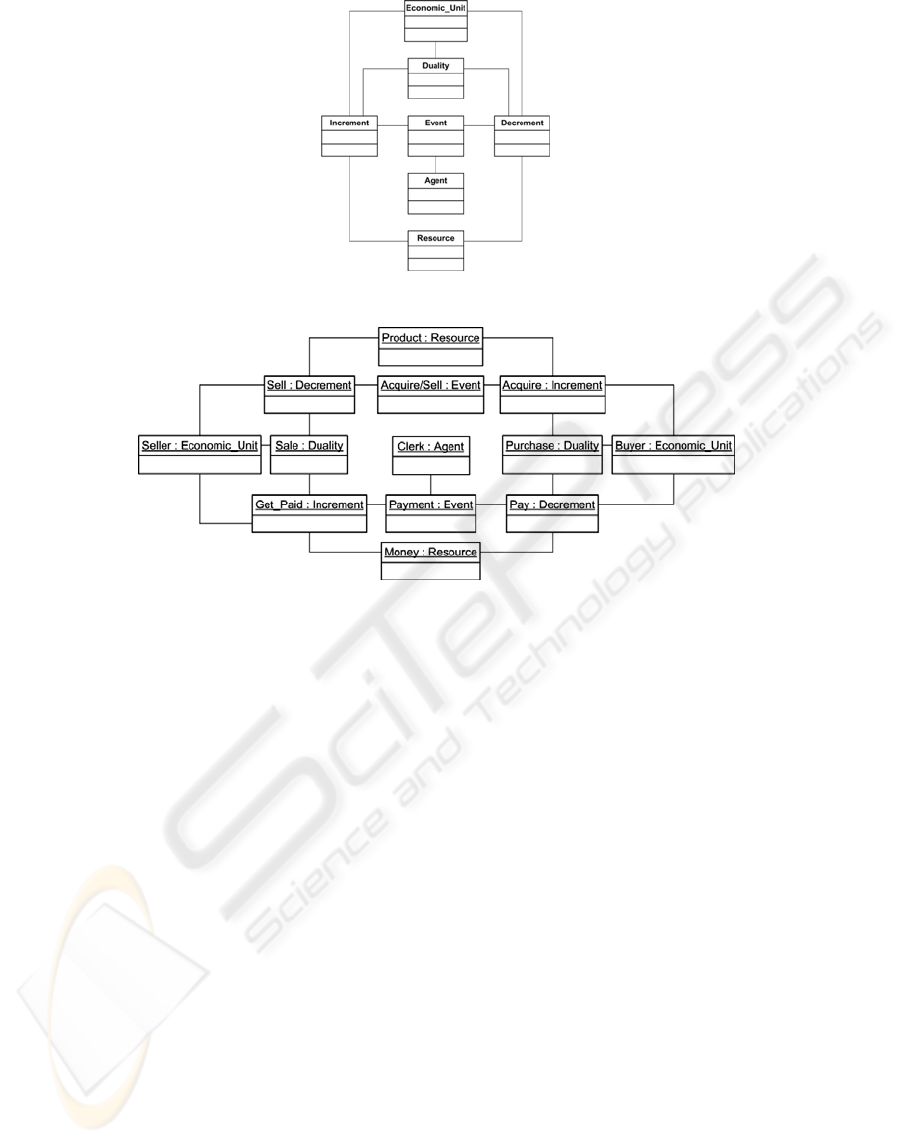

Fig. 6 shows the integration of a transfer and an

exchange into a consolidated view exchange model.

It shows two mirrored dualities (i.e. P

URCHASE

and

S

ALE

) and two transfer events that connect them to

each other (i.e. A

CQUIRE

/S

ELL

and P

AYMENT

). The

P

URCHASE

duality shows how the B

UYER

exchanges

M

ONEY

for P

RODUCT

, where the S

ALE

duality

represents how the S

ELLER

exchanges P

RODUCT

for

M

ONEY

. The A

CQUIRE

/S

ELL

event shows that

A

CQUIRE

and S

ELL

are in fact two roles of the same

event. Similarly P

AY

and G

ET

_P

AID

are two roles of

P

AYMENT

. The A

CQUIRE

role is assigned to the

A

CQUIRE

/S

ELL

event by the B

UYER

, while the S

ELL

role is assigned by the S

ELLER

. Likewise, the

G

ET

_P

AID

role is assigned by the S

ELLER

and the

P

AY

role by the B

UYER

.

The exchange duality models the exchange (e.g.

P

URCHASE

), which involves a resource inflow (i.e.

A

CQUIRE

) and a resource outflow (i.e. P

AY

), from

the viewpoint of a single economic unit. Taking the

buyer perspective, the economic unit (i.e. B

UYER

)

defines the D

UALITY

and the I

NCREMENT

and

D

ECREMENT

roles for the resource transfer events

involved. Such a transfer event (e.g. a M

ONEY

transfer (i.e. the P

AYMENT

event)) is perceived by a

B

UYER

and a S

ELLER

. The P

AY

/G

ET

_P

AID

decrement/increment role represents the

B

UYER

/S

ELLER

‘s view on the P

AYMENT

event. The

C

LERK

object represents the person that executes the

payment regardless of whether he/she experiences

the economic consequences of this action.

Finally, fig. 7 shows a transformation template in

which transformation inputs are transformed into

outputs. The template shows that the

T

RANSFORMATION

event takes place inside a single

economic unit (i.e. E

MPLOYER

) and that both the

A CONSOLIDATED ENTERPRISE REFERENCE MODEL - Integrating McCarthy's and Hruby's Resource-Event-Agent

Reference Models

163

inputs and outputs are owned by the E

MPLOYER

,

without a transfer of ownership during the

conversion process. This representation is closer to

reality than Hruby’s implicit ownership transfer

during the conversion process. The template also

shows that an E

MPLOYEE

performs the

T

RANSFORMATION

event. For representing an entire

production process, subsequent events can be

modelled using the transformation template, creating

multiple events that are all related to the same

economic unit (i.e. the enterprise in which they take

place) and share one or more resources (i.e. the

output of one conversion process is the input for a

subsequent one). At the start of such a process

model we find one or more exchange templates (fig.

6) that represent the acquisition of the process inputs

and at the end we find one or more exchange

templates that represent how revenue is generated

from process outputs.

Figure 7: REA Transformation Event Model.

4 CONCLUSIONS

The consolidated reference model presented in this

paper supports inter-enterprise (e.g. for transaction

recording systems) and intra-enterprise (e.g. for

production process monitoring systems) data, as

both kinds of systems can now rely on the same

reference model.

Key to the integration of the existing REA

reference models was the partial redefinition of the

economic unit and agent concepts. The redefinition

of the economic unit concept allows models to

represent previously implicit semantics related to the

control over resources. Where previously the view

of every enterprise was represented in a separate

model, the scope of different enterprises can now be

represented in a single model via the economic unit

concept and its relations with resources, events and

agents. This explicit representation of enterprise

boundaries allows for a central administration of

transactions between and transformations within

enterprises.

Where the redefinition of the economic unit and

agent concepts facilitates the integration of data

across enterprise boundaries, the intuitive event

concept eases process modelling. Together, they can

help improve product traceability by identifying the

event chains (i.e. transfer and transformation events)

that lead to the products, irrespective of the number

of enterprises (and enterprise information systems)

in which products and their constituents have their

origin. Such product tracing infrastructure might

support product authentication in the battle on

counterfeit and other supply chain intrusions (e.g.

food safety scandals) (Bechini et al., 2008). It may

also help to trace the origin of money (e.g. drugs

money) in the battle against money laundering.

REFERENCES

Bechini, A., Cimino, M. G. C. A., Marcelloni, F. &

Tomasi, A. (2008) Patterns and technologies for

enabling supply chain traceability through

collaborative e-business. 50, 342-359.

Geerts, G. L. & Mccarthy, W. E. (2002) An ontological

analysis of the economic primitives of the extended-

REA enterprise information architecture. International

Journal of Accounting Information Systems, 3, 1-16.

Geerts, G. L. & Mccarthy, W. E. (2004) The Ontological

Foundation of REA Enterprise Information Systems.

Michigan State University.

Giachetti, R. E. (1999) A standard manufacturing

information model to support design for

manufacturing in virtual enterprises. Journal of

Intelligent Manufacturing, 10, 49-60.

Hruby, P. (2006) Model-driven design using business

patterns, Berlin, Springer.

ISO/IEC (2007) Information technology - Business

Operational View Part 4: Business transaction scenario

- Accounting and economic ontology. ISO/IEC FDIS

15944-4: 2007(E).

Jansen-Vullers, M. H., Van Dorp, C. A. & Beulens, A. J.

M. (2003) Managing traceability information in

manufacture. International Journal of Information

Management, 23, 395-413.

Mccarthy, W. E. (1982) The REA Accounting Model: A

Generalized Framework for Accounting Systems in a

Shared Data Environment. Accounting Review, 57,

554-578.

Mccarthy, W. E. (2003) The REA Modeling Approach to

Teaching Accounting Information Systems. Issues in

Accounting Education, 18, 427-441.

Porter, M. E. & Millar, V. E. (1985) How information

gives you competitive advantage. Harvard Business

Review, 63, 149-160.

Shin, K. & Leem, C. S. (2002) A reference system for

internet based inter-enterprise electronic commerce.

Journal of Systems and Software, 60, 195-209.

Weber, R. (1986) Data Models Research in Accounting:

An Evaluation of Wholesale Distribution Software.

Accounting Review, 61, 498.

ICEIS 2010 - 12th International Conference on Enterprise Information Systems

164