A2MO and ETREOSys

Analyzing, Modeling and Validation of Enterprise Training Programs

Fod´e Tour´e, Mouna Selmi and Esma A¨ımeur

Department of Computer Science and Operations Research (DIRO), Universit´e de Montr´eal, Montreal, Canada

Keywords:

Evaluation, Enterprise Training, Business Process Management, Business Activity Monitoring, Agile

Management, Return On Investment, Optimization, Machine Learning Algorithms.

Abstract:

Organizations and public authorities invest substantial sums in training, but rarely have data indicating the re-

sults of this investment. Because of the difficulties related to existing models, to the lack of valid instruments

and workable models, only a few organizations evaluate their training project in depth.

In this paper, we propose an approach of training project evaluation, based on Business Process Management

(BPM). This approach consists in Analyzing the needs, process Modelling, Monitoring the project progress and

ensuring the expectation of the objectives, Optimizing the global and personal yield by a series of simulation

(A2MO method). To facilitate the understanding and the use of A2MO, we develop a Business Process Man-

agement System named ETREOSys (Enterprise TRaining program Evaluation and Optimization System).

A2MO ensures the alignment between training activities and enterprise business objectives. It allows training

project monitoring, calculating tangible and intangible benefits of training (without additional costs). It also

allows making a training projects classification according to criteria bound to enterprise and employees, to

optimize training activities in order to answer the enterprise objectives and employees needs.

1 INTRODUCTION

Individual and collective skills are the most important

assets for an organization. They determine the pro-

ductivity, competitiveness and ability to adapt and to

be proactive in an uncertain economic environment.

A report published, in 2011, by the American Soci-

ety of Training & Development (ASTD) reveals that

Businesses in the United States spent $171.5 billion

on employee learning in 2010, 26% more than in

2009 (Green and McGill, 2011). The report confirms

that, despite economic challenges, organizations un-

derstand that a highly skilled workforce is a strategic

differentiator and they are willing to invest in the de-

velopment of their employees skills.

On the other side, a study led by ASTD and the In-

stitute for Corporate Productivity (i4cp), revealed that

the five-level Kirkpatrick/Phillips model (Kirkpatrick

and Kirkpatrick, 2006; Phillips and Phillips, 2003) of

learning evaluation is the most common practice. Ac-

cording to this study, the barriers that prevent com-

panies from using all the evaluation levels of Kirk-

patrick/Phillips’model are: the difficulty in isolating

learning as a factor that has an impact on corpo-

rate results; the lack of a useful evaluation system

within the learning management system; the lack of

standardized data to properly compare across train-

ing functions (Patel, 2010).

Thus, to bring a solution to enterprises needs, we

present, in this paper, an approach of training evalua-

tion and optimization, based on BPM.

BPM has become a critical success instru-

ment to improve the enterprise overall performance

(Mutschler and Reichert, 2013). The success regis-

tered by BPM solutions in managing enterprise pro-

cesses has inspired us in using it to manage train-

ing activities. Such a scenario supposes considering

training activities as being business process. In fact,

the design and execution of a training program sup-

poses a set of steps that go from the formulation of a

demand up to the implementation of new skills. All

these stages, enumerated by chronological order, con-

stitute a process as any other business process, and

can lead to a capital gain if everything took place cor-

rectly. So, they can be managed using BPM.

This paper presents a method of training project

management (A2MO method) based on BPM: going

from design to optimization, via the evaluation of the

financial and non financial yield.

In the following, we present, in section 2, the

Kirkpatrick/Phillips model for evaluating training

programs in organizations, the advantages and disfa-

310

Touré F., Selmi M. and Aïmeur E..

A2MO and ETREOSys - Analyzing, Modeling and Validation of Enterprise Training Programs.

DOI: 10.5220/0004558503100316

In Proceedings of the 15th International Conference on Enterprise Information Systems (ICEIS-2013), pages 310-316

ISBN: 978-989-8565-60-0

Copyright

c

2013 SCITEPRESS (Science and Technology Publications, Lda.)

vors of this model. Section 3 will be dedicated to a

brief presentation of A2MO method and ETREOSys.

In sections 3.1 and 3.2, we present, in details, the two

first steps of the A2MO method and ETREOSys’ cor-

responding modules. The section 4 is reserved for the

conclusion.

2 THE FIVE-LEVEL

KIRKPATRICK/PHILLIPS

MODEL

Kirkpatrick’s model began in 1959, with a series of

four articles on the evaluation of training programs

in the journal ”Training and Development”. These

four articles defined the four levels of evaluation that

would later have a significant influence on corporate

practices (Kirkpatrick and Kirkpatrick, 2006).

Level 1 - Students reaction

How did the trainees react after the training? Did they appre-

ciate it? Are they satisfied? What they thought and felt about

the training?

Level 2 - Learning

What they learnt after the training? What knowledge, skills

and/or attitudes have been acquired? Have educational objec-

tives been achieved? The resulting increase in knowledge or

capability.

Level 3 - Behavior

Do the trainees use what they learned in training at their

workstations? What new professional behaviors have been

adopted?

Level 4 - Results

What is the impact of the training on the results of the com-

pany? Example: decrease of the rate of absenteeism, occu-

pational accidents, growth of turnover, the productivity, cus-

tomer satisfaction, etc. The effects on the business or environ-

ment resulting from the trainee’s performance improvement.

According to Phillips, training yield calculation is

made by means of a process by stages which supplies

a plan detailed for the planning, the collection and

the data analysis, which includes the calculation of

Return On Investment (ROI). So Phillips suggests the

inclusion of a fifth level (Phillips and Phillips, 2003).

Level 5 - Return On Investment

Comparison between the profit obtained from the training and

the training costs. Profits and/or savings realized are they

superior to the total cost of the training (direct and indirect

costs)? Did the training generate a return on investment?

The ROI calculation process begins with a plan-

ning for training evaluation: where objectives are de-

fined and decisions are taken on the way the data will

be collected, treated, and analyzed. The data collec-

tion is made according to the training evaluation lev-

els 1 to 4.

However, in the literature, several criticism are

raised with regard to the Kirkpatrick/Phillips model.

According to Mumma and Thatcher (Mumma and

Thatcher, 2009), the entire notion of the Kirk-

patrick/Phillips model may not truly measure the im-

pact of the learning function on the organization, even

under the most optimistic scenarios. It measures only

the possible impact of isolated training events. Nagle

(Nagle, 2002) reports a series of criticism towards the

ROI calculating process: difficulty to have a faithful

measure, expensive process, complex process, process

that can take up to one year, presence of other factors

(independent from the training) that influence the per-

formance of the organization.

Concerning the methodological problems, Mc-

Cain (McCain, 2004) has established a list of bias

being able to have an impact on the observed results

and of which a professional of the training does not

always think. We can quote the bias of a sample (se-

lection of a non representative sample or too small

one), bias in the interviews, bias of acquiescence or

neutrality according to the presentation of questions.

Thus, to bring a solution to the enterprise needs,

we present, in the following section, an approach of

training yield evaluation, based on the business pro-

cess management.

3 A MODEL OF TRAINING

EVALUATION BASED ON

BUSINESS PROCESS

MANAGEMENT

All performance problem is not a problem of train-

ing, but a judiciously applied training can stimulate

skills and improve the performances of persons in

their jobs. The reality in most enterprises is that they

need to knowhowto calculate and improve the impact

of their spending on training more important on the

enterprise overall performance. When training costs

are considered with a critical eye, many organizations

realize that they simply did not have enough money

to train all employees. They need to focus their train-

ing spending on the roles which are most essential for

the success of the enterprise and which return more

value to the organization. For that purpose, managers

in training and development should collaborate with

A2MOandETREOSys-Analyzing,ModelingandValidationofEnterpriseTrainingPrograms

311

managers to clarify the essential points on which de-

pends the success of the organization, establishing

performance criteria and focusing training on these

criteria. By comparing the performance before and

after training, the value of learning activities can be

calculated on the basis of the impact on the business.

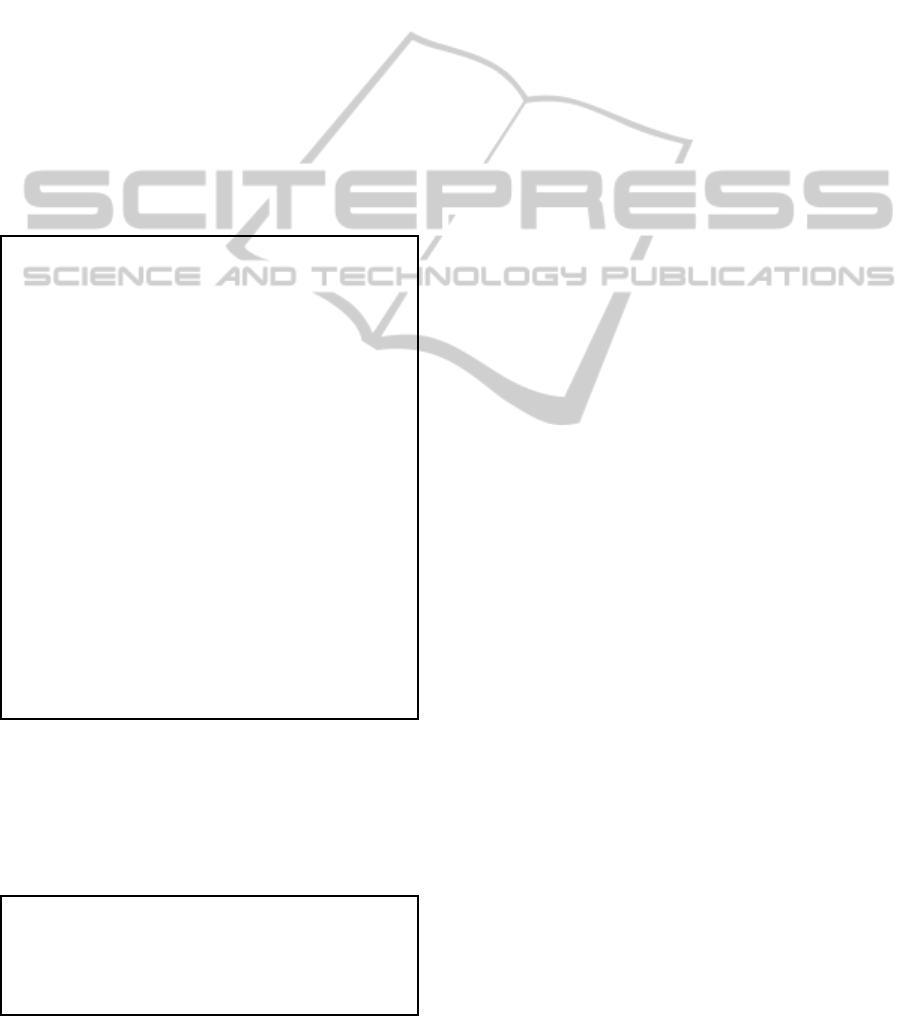

Thus, we propose a four-step approach of enter-

prise training program management. This approach

consists in Analyzing the need, process Modelling,

Monitoring the project progress and guaranteeing the

expectation of the objectives, Optimizing the global

and personal yield by a series of simulation (Fig. 1).

Figure 1: The stages of A2MO method.

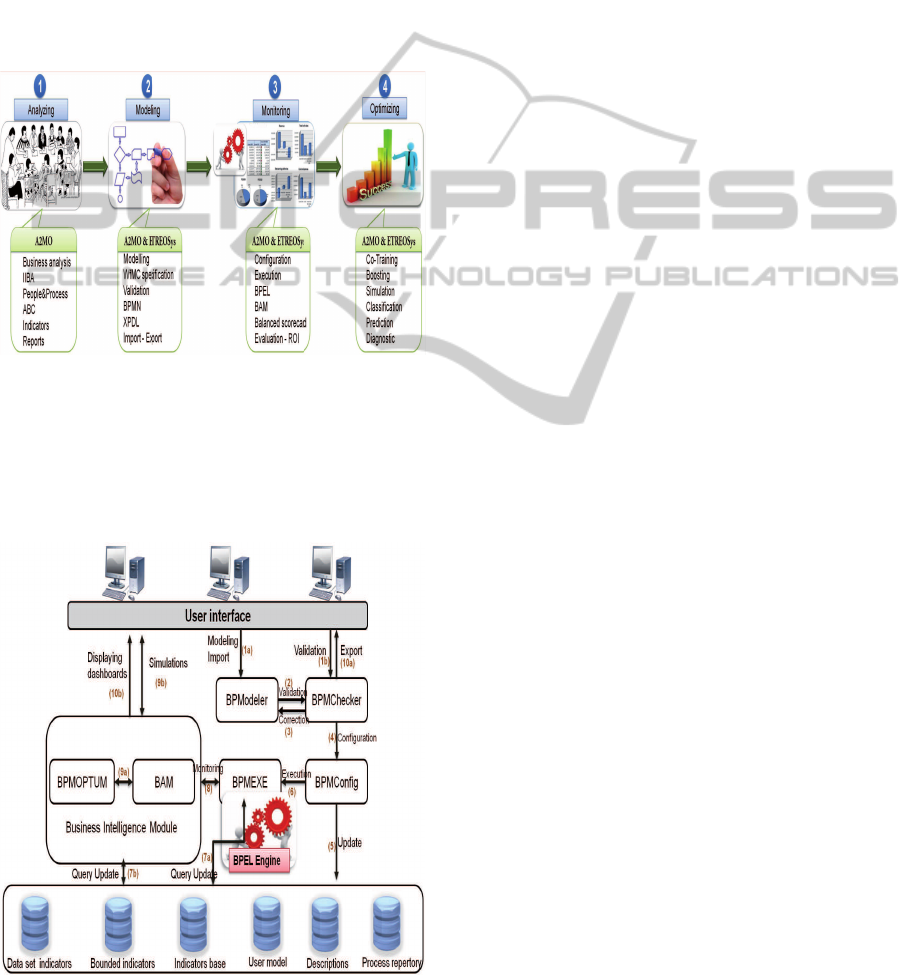

To facilitate the understanding and the use of

A2MO, we develop a Business Process Manage-

ment System(BPMS) named ETREOSys (Enterprise

TRaining program Evaluation and Optimization System),

characterized by the following architecture (Fig. 2).

Figure 2: Architecture of our enterprise training processes

management system.

In the sections 3.1 and 3.2, we present the two first

steps of the A2MO method and ETREOSys’ corre-

sponding modules.

3.1 Stage 1 - Analysis

The training in enterprise consists in a series of spe-

cific actions intended to resolve a problem with which

the enterprise is confronted. Thus, the first stage of

A2MO focuses on analyzing the demand for training

and associating it to performance elements of the en-

terprise. This stage is translated by a certain num-

ber of actions such as: conversations of demand ex-

ploration, definition of a change plan, needs anal-

ysis, definitions of the objectives, choice and defini-

tion of performance indicators. Therefore, we use a

business analysis process combining the guide of In-

ternational Institute of Business Analysis (IIBA), the

method ”People&Process” and the method Activity-

Based Costing (ABC method).

IIBA maintains and publishes a referential con-

taining a description of the activities of the busi-

ness analysis. The referential is published as a book

entitled ”A Guide to the Business Analysis Body of

Knowledge (Brennan, 2009)”. This latter provides

a description of a typical business analysis activities

into six chapters: Analysis of enterprise initial sit-

uation; Planning and management of prerequisites,

needs and expectations; Harvest of the information;

Analysis and documentation of needs and expecta-

tions; Communication of information to stakeholders;

Evaluation and validation of the proposed solutions.

The development of systems and their compo-

nents is based on needs description. The needs de-

termination depends on the form and the structure of

the demand. IIBA provides an initial classification of

forms of expression of needs and expectations into six

levels (see IIBA guide (Brennan, 2009)).

The analysis of the current situation produces a

report containing a structured presentation of har-

vested information and details of the objectives, the

means and available resources, improvement propos-

als, risks and potential impacts. Managers evaluate

the strengths, weaknesses, opportunities and risks for

the organization.

A business process model is therefore based on the

identification of key elements in the conduct of affairs

such as endogenous and exogenous factors directly

acting on the fluctuations of the functioning mode of

the enterprise. This last point solves the problem of

isolation of training impacts on the overall perfor-

mance of the organization (highlighted in the Kirk-

patrick/Phillips model, see section 2). Indeed, using

the process of IIBA, we define the indicators related

ICEIS2013-15thInternationalConferenceonEnterpriseInformationSystems

312

to the expected effects of the training and the factors

that may influence these effects. This means that we

also define the situations and indicators that can pro-

duce the same effects as training.

The second method that we use at this stage is the

”People&Process” method (Briol, 2008). The man-

agers fixe the high-level objectives according to their

visions. These objectives are then formulated in the

lower level objectives. An achieved goal answers the

criteria of successes expressed with indicators offer-

ing a means of measuring and verifying the gaps to

the initially set values. The Objectives formalized in

dashboards are used in the design and supervision of

business processes.

The translation of an objective in indicators form

depends on its formulation. For example, the objec-

tive ”... make more results next year ...” could pos-

sibly be subject to diverse interpretations. Generally,

these interpretations are reflected in several indicators

distributed among the entities or functions of the orga-

nization such as finance function, production, human

resources, etc. There are two types of performance

indicators in a cause and effect relationship:

• Indicators directly allocated to outcome of actions

already executed such as financial or social indi-

cators of the enterprise.

• Indicators influencingor controlling the indicators

of the first category. For example, the ”number

of products sold” directly influences the indicator

”turnover”.

Furthermore, there are two categories of indicators:

qualitative indicators such as social values and quan-

titative indicators taking a digital or symbolic form.

The indicators, by measuring performance of the

organization, play an important role in verifying its

alignment with enterprise strategy. They are deduced

either directly from objectives or key success factors

influencing the strategy success.

In A2MO, the description of the training intan-

gible yield is based on the values of qualitative in-

dicators. As these indicators are directly linked to

some objectives, then the reached (or the not reached)

of these objectives will be deducted from the values

of the corresponding indicators. The same reasoning

applies to the calculation of financial yield of train-

ing. This yield is calculated by mathematical formu-

las (cost/benefit ratio), after deducting costs associ-

ated with quantitative indicators values. For that pur-

pose, we use the ABC method (Activity-Based Cost-

ing).

The ABC method allows to determine costs as-

sociated with a set of business activities prior to a

change and the gain due to the change (Richard Or-

wig and Flather, 2012).

The ABC method considers the goods and ser-

vices as objects of costs in exchange for a definite

and organized effort. This method is structured by an-

swering three questions: What is spent? How it was

spent? What has been produced?

The activity concept is at the center of ABC

method. An activity is a set of elementary tasks per-

formed by an individual or a group,appealing to spe-

cific set of cognitive capacities (knowledge, know-

how, skills), more or less homogeneousfrom the point

of view of their performance behavior. An activity is

described using an action verb followed by an object

(ex. make something). Each activity has a recogniz-

able production (an output), one or more customers

and uses identified resources. The impacts of an ac-

tivity, on the growth of the enterprise, can be quantifi-

able or of social order.

The performances of the organization depend di-

rectly on resources consumed at the origin of the

costs. The resources cost takes into account the ex-

penses associated to the human effort, raw materials,

equipments of production, indirect costs of produc-

tion and to the overheads. The inductors of resources

are used in the affectation of the costs in the activ-

ities by associating the resources with the activities.

The inductors of resources are expressed in cost per

minute of activity. It can be also expressed by qualita-

tive values (qualitative indicators) spread over several

periods of observation. Each type of resource used

in an activity becomes a cost element. The cost el-

ements associate an activity with an inductor which

measures the utilization level of these elements in the

activity. The ABC method offers the means to ver-

ify the resources consumption of business processes

in the organization.

This first stage of A2MO supplies the process

model, the information required to configure this

model, the initial values of indicators. It ensures the

alignment of the training program to the growth strat-

egy of the enterprise.

At the end of this stage, we shall have isolated all

the indicators associated to the problem. As example

of indicators we can quote: cost of the delivery delay,

the number of item (or service) delivered late, accu-

mulated delay ....

We also isolate the indicators which can influence

those quoted previously (with or without training pro-

gram). For example: rate of staff turnover, rate of

employees absenteeism, number of absence per em-

ployee, cause of absence, cost of the rotation, cost

engendered by absenteeism, cost of absence per em-

ployee, degree of job satisfaction, degree of personal

initiative, staff productivity, level of collaboration be-

tween employees within the enterprise, level of col-

A2MOandETREOSys-Analyzing,ModelingandValidationofEnterpriseTrainingPrograms

313

Figure 3: A possible process model for training planning ”Consumer behavior”.

laboration per employee ....

In the next sections, we present the second stage of

A2MO. This stage is strongly related to ETREOsys.

3.2 Stage 2 - Modelling

This stage is supported by modules BPModeler and

BPMChecker of ETREOSys. To model a business

process, BPModeler uses graphic objects developed

by Workflow Management Coalition (WFMC, 1999).

In this modelling language, we use two object types:

node and flow. The nodes are classified in two cate-

gories: task and choice (condition). A task, graphi-

cally represented by a rectangle, represents the work

to be made to achieve some objectives. A choice,

graphically represented by a circle, is used to build

conditional structures. A flow links two nodes in

graph and is graphically represented by an arrow.

The use of invalid process models (bad combina-

tions the objects) leads to syntactic errors. Semantic

errors happen because of the non-compliance (lack of

strategic alignment) at the expected business needs.

For checking the syntactic validity, we analyze the

structure of the process graph. In order to insure the

structural validity of process models, we use the hy-

brid algorithm of Tour´e et al. (Tour´e et al., 2008).

On the other hand, to check the semantic valid-

ity, we need to analyze the information treated by the

tasks and the behavior of the latter (if the first stage of

A2MO, see section 3.1, is made with precaution, the

semantic errors will be avoided).

For the training project management, there are at

least two process models: the process model related

to training planning and the process model related

to the stages of data collection and training perfor-

mance evaluation.

The training planning is a graphical representation

of the training organization (course outline). To illus-

trate this concept, let us take the example of an enter-

prise which would like to improve the performances

of its customers service department. For that purpose,

the enterprise would like that the employees of this

department can make a complex analysis of consumer

behavior and communicate results to managers and

strategic advisors. This means that employees must

be trained on consumer behavior. Figure 3 shows a

process model of the planning of this training.

It is possible to have more granularity depending

on the task (for example, there might be a process

model corresponding to the decomposition of the ac-

tivity Decision process (see Fig 3). Ditto for the ac-

tivity Perception (see Fig 3)).

In A2MO, we associate to this graph (see Fig 3):

the actors of each activity and their roles, the descrip-

tion of incoming and outgoing data, the temporal as-

pect and the performance indicators related to train-

ing (see section 3.1). As indicators, we can quote: av-

erage emotional state by learner, average emotional

state by training session, general emotional state by

training, satisfaction of the organization with regard

to the training program, Employees’ satisfaction with

regard to the content, satisfaction towards the trainer,

relevancy of perception, the usefulness of training,

training capacity to reach enterprise objectives, the

notes of the examinations, the average score of the

learning....

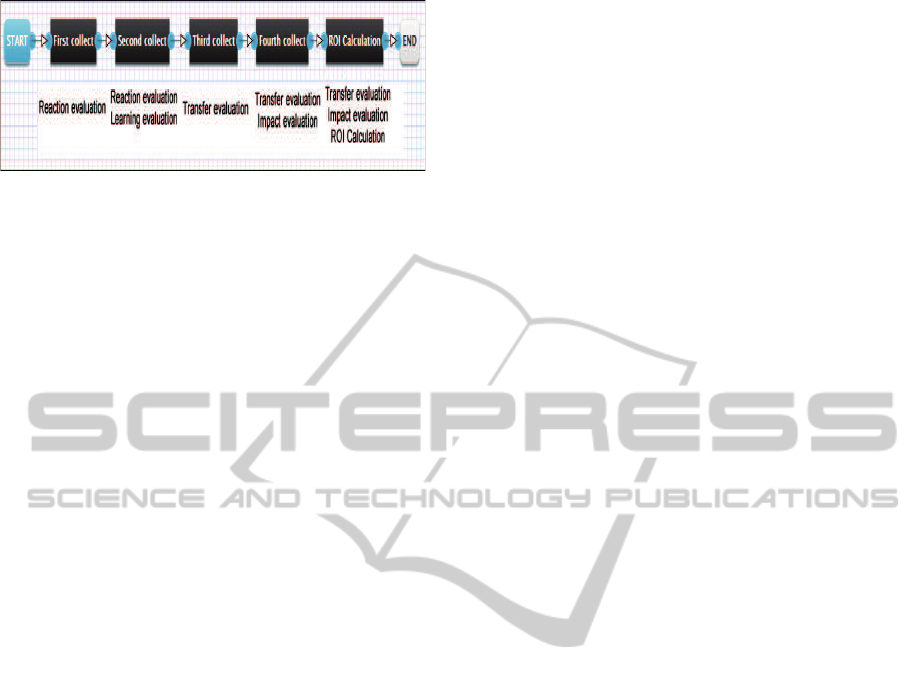

The planning of the collection and training evalu-

ation is a representation of the steps of collecting in-

formation before, during and after the training (Figure

4). In A2MO, for each step (activity of the process

in the Figure 4), we define the means of collection,

dates, the objectives, the actors and the corresponding

indicators. All these informations are kept in ETRE-

OSys to facilitate the management of the training pro-

ICEIS2013-15thInternationalConferenceonEnterpriseInformationSystems

314

Figure 4: A possible process model for training evaluation

planning.

gram. Consequently, besides the already mentioned

indicators, we define other indicators allowing to esti-

mate the achievement of the training objectives in the

enterprise. These indicators relate to the employees’

lives in the enterprisebefore and after the training. We

can quote as indicators: increase of the innovation de-

gree of an employee, the increasing of the innovation

degree in the enterprise generally, the improvement of

the product quality, work climate, the meetings num-

ber of the committee, customers loyalty, the profit by

employee....

For the particular case of the formation modeled

in Figure 3, we must take into account the influence

of environmental factors on consumer behavior such

as culture, reference groups, social class or family.

Therefore, it is necessary to define indicators allowing

to isolate the influence of these external elements.

The process model, related to the evaluation, fixes

periods of gathering information order to proceed

with of evaluations and simulations leading to predict

the results tendency. These last informationwill allow

to make decisions leading to the success of the train-

ing program. Through to the indicators, the process

model associated with the evaluation will allow to re-

act in real time to avoid any situation leading to the

failure of training (non-realization of the objectives).

For that purpose, it is just enough to compare the ini-

tial values, the collected values and the expectations

of the enterprise.

The first and second stages of A2MO are impor-

tant because they insure a best management of the

training program and the basis for the success of the

stages 3 and 4.

3.3 Stage 3: Monitoring

This stage of A2MO consists in controlling the

progress of the processes. A control based on precise

indicators and relevant in order to have dashboards al-

lowing making quickly the good decisions. The dash-

board of the training has to cover two big dimensions:

the efficiency and the efficacy. The training process

said to be efficient if it gives the maximum of results

by consuming the minimum of resources and said to

be effective if it gives the expected results.

The dashboard of the efficiency of the training

will be composed of indicators of consumption of re-

sources and of activities output allowing measuring

the efficiency of each of the three stages of the pro-

cess, as well as the general efficiency of the train-

ing project. The following indicators allow building

the dashboard of the efficiency of a training program:

time dedicated to the identification and to the needs

analysis (combined time of the employee, his supe-

rior and the training manager), perceived usefulness

of the training/time dedicated, the gap enters what the

employee masters and what he has to master, the ad-

equate level of training to reduce or cancel the gap

(beginner, intermediate, advanced), mode of training

(external, intern, coaching, e-learning, tutoring, etc.),

time to design and the elaboration of the program, etc.

These indicators can be analyzed by sex, seniority, so-

cial status, type of training, or operational unity (ser-

vice, department, store, etc.). The dashboard of the

effectiveness focuses either on the effectiveness of a

training, or on the global effectiveness of the training

system. Its structure includes the model of training

evaluation and contains more indicators than the effi-

ciency dashboard.

This stage allows us to calculate the tangible and

intangible training benefits (without additional costs)

by using indicators values.

3.4 Stage 4: Optimization

In this stage of A2MO, we use machine learning algo-

rithms (example, logistic regression, neural networks

or support vector machines) to classify training activ-

ities according to defined criteria (example, financial

yield) and to do simulations to increase the efficiency

and efficacy of training activities. To do that, we re-

alize a pretreatment on the indicator values to have

a data set for a supervised learning algorithm, unsu-

pervised or semi-supervised. The stages of monitor-

ing and optimization constitute our module of busi-

ness intelligence because they allow: improving per-

sonal efficiency, speeding up the process of decision

making, increasing organizational control, encourag-

ing exploration and discovery on the part of the deci-

sion maker, speeding up problem solving in an organi-

zation, facilitating interpersonal communication, pro-

moting learning or training, generating new evidence

in support of a decision, creating a competitive ad-

vantage over competition, revealing new approaches

to thinking about the problem space, and helping au-

tomate managerial processes.

When the training evaluation process is com-

pleted, the enterprise training programs will be clas-

A2MOandETREOSys-Analyzing,ModelingandValidationofEnterpriseTrainingPrograms

315

sified in two categories: profitable and unprofitable.

Hence, we will have a dataset D

n

that can be used in

training of a machine learning algorithm.

D

n

= {Z

1

, Z

2

, . . . , Z

n

}

∀i ∈ {1, 2, . . . , n}, Z

i

= (x

(i)

, y

(i)

) with x

(i)

∈ R

d

and y

(i)

∈

{0, 1}

Each Z

i

is associated to a particular training pro-

gram in the enterprise. The x

(i)

are the indicators

(see 3.1 and 3.2) related to the training. Hence, we

can have indicators which take numerical values (for

example,number of committee meeting) and others

that take categorical values (for example, climate at

work). y

(i)

represents the training class (profitable or

unprofitable), profitable corresponds to 1 and its op-

posite corresponds to 0. n is the number of completed

training program and d is the number of indicators.

It is obvious that to use this data set with a ma-

chine learning algorithm, it is necessary to make a

pretreatment to standardize or normalize the inputs

x

(i)

.

In our approach, the purpose of the classifica-

tion is to be able to predict the achievement or none

achievement of the training objectives by observing

only the indicators behavior. Furthermore, we must

be able to determine the indicators which have more

weight in the realization of training objectives. That’s

why we may use a parametric machine learning algo-

rithm like logistic regression, neural networks or the

support vector machines.

The optimization consists of a simulation allow-

ing guiding the training process towards objectives

achievement. To do this we may use semi-supervised

learning.

4 CONCLUSIONS

The advantages obtained through our approach can be

seen from two angles. In the domain of business pro-

cess management, we add a new category of business

process and extend BPMS by adding the validation

pre-execution (through ETREOSys).

Concerning the evaluation of enterprise training,

we propose a complete approach of training project

management facilitating decision-making and the cal-

culation of the tangible and intangible profits.

With regard to the existing training evaluation

models, we propose A2MO method. This approach

consists in Analyzing the need, process Modelling,

Monitoring the project progress and guaranteeing the

expectation of the objectives, Optimizing the global

and personal yield by a series of simulation. We add

a particular level of diagnostic (classification and op-

timization) allowing to understand the dysfunctions

related to the attainment or not attainment of training

objectives. Our approach ensures the training activi-

ties alignment with business needs and allows the ROI

calculation without additional investment.

REFERENCES

Brennan, K. (2009). A guide to the Business Analysis Body

of Knowledge (BABOK guide), version 2.0. Interna-

tional Institute of Business Analysis.

Briol, P. (2008). Ing´enierie des processus m´etiers: De

l’´elaboration `a l’exploitation. Lulu.com.

Green, M. and McGill, E. (2011). State of the industry,

2011. Astd’s annual review of workplace learning and

development data, American Society of Training &

Development (ASTD).

Kirkpatrick, D. L. and Kirkpatrick, J. D. (2006). Evalu-

ating Training Programs: The Four Levels (3rd Edi-

tion). Berrett-Koehler Publishers, 3rd edition.

McCain, D. (2004). Evaluation basics. ASTD, 1st edition.

Mumma, S. and Thatcher, C. (2009). The learning profit

chain ”connecting learning investments to financial

performance”. Corporate University Xchange.

Mutschler, B. and Reichert, M. (2013). Understanding

the costs of business process management technol-

ogy. In Glykas, M., editor, Business Process Manage-

ment, Studies in Computational Intelligence, pages

157–194. Springer Berlin/Heidelberg.

Nagle, B. (2002). Roi gives a way to roe. Candian HR

Reporter,, 15(13):7.

Patel, L. (2010). Overcoming barriers and valuing eval-

uation. Learning Circuits - ASTD’s Source for E-

Learning. American Society for Training & Devel-

opment.

Phillips, J. J. and Phillips, P. P. (2003). Using action plans

to measure roi. Performance Improvement, 4:24–33.

Richard Orwig, J. B. and Flather, W. (2012). Marrying busi-

ness activity modeling with activity-based costing for

measuring systems’ cost savings. In AMCIS.

Tour´e, F., Ba¨ına, K., and Benali, K. (2008). An efficient

algorithm for workflow graph structural verification.

In Meersman, R. and Tari, Z., editors, OTM Confer-

ences (1), volume 5331 of Lecture Notes in Computer

Science, pages 392–408. Springer.

WFMC (1999). Workflow management coalition interface

1: Process definition interchange process model.

ICEIS2013-15thInternationalConferenceonEnterpriseInformationSystems

316