Demo-based Cost Model

Marco Arede, Carlos Mendes and Miguel Mira da Silva

Instituto Superior Técnico, Technical University of Lisbon, Avenida Rovisco Pais, Lisboa, Portugal

Keywords: Enterprise Ontology (EO), Design Engineering Methodology for Organizations (DEMO), Enterprise

Complexity, Cost Model, Implementation Costs.

Abstract: The complexity of organizations has become difficult to manage and organizations have lost the traceability

between their essential transactions and the respective implementation costs. Most organizations do not

have a coherent, comprehensive and consistent vision of the costs directly or indirectly related to the

organization essential operations. This essential operations are based on networks of subjects that interact in

order to coordinate and perform work, contributing for global performance. The lack of understanding of

where costs occur leads to difficulties when taking decisions, limiting what can be achieved in a planned

way, reason for the need of a properly cost analyses. A solution could contribute to a better understanding of

where costs occur, providing managers with more information to support their decisions, so they can

improve organizations in order to be more profitable. In our research we propose a DEMO-based Cost

Model to address this problem, which intends to reduce the complexity of analysing costs, mapping the

implementation costs with the essence of organizations. Our proposal allows analysing costs from different

perspectives, by act, actor role, transaction and business process. The demonstration was applied to Invoice

Management of a research and development unit. This research was conducted using DSRM.

1 INTRODUCTION

Over time organizations become increasingly

complex and managing that complexity is a growing

challenge. Organizations complexity has been

described as the organized complexity: too

organized for statistics and too complex for analysis

(Weinberg, 2001). Since costs in organizations have

become too complex for analysis, organized

complexity also applies to costs (Wileman, 2008).

Complexity seems to be a common background

of enterprise problems (Association of Chartered

Certified Accountants & Institute of Management

n.d.). In a complex system, elements can interact

with others, moving into more elaborated structures

and increasing the number of the transactions. As a

consequence organizations also incur in more costs

that are hard to identify (Ray, 2013).

Costs are associated to the enterprise operations

and its processes. Costs are not only inherent of

enterprise operation but also of complexity, mergers,

search for growth, acquisitions, or other factors. One

of the top challenges nowadays, as revealed by

several surveys, is to identify cost reductions

(Association of Chartered Certified Accountants &

Institute of Management n.d.). However the

complexity of organizations has become

unmanageable (Schapper et al., 2005) and

organizations have lost the traceability between the

organization essence and the respective

implementation costs, meaning that most

organizations do not have a coherent, comprehensive

and consistent vision of the costs related to the

essential operations (Dietz, 2006). Organization

operations are performed by networks of subjects

that contribute to global performance, interacting

with others to coordinate and perform work (Cross

and Parker, 2004). A solution to approach this

problem should reduce the analysis complexity,

focus on the system and ignore the subsystems, to

separate enterprise essence from the implementation.

Our research focused on DEMO to overcome the

complexity of modelling organizations, allowing us

to separate the way organization are implemented

from its ontological essence, reducing the analysis

complexity. We also used Time-Driven Activity

Based Costing (TDABC) to allow reflecting the

complexity and variability of business processes

with time equations. TDABC is more simpler, less

costly and faster to implement than Activity Based

431

Arede M., Mendes C. and Mira da Silva M..

Demo-based Cost Model.

DOI: 10.5220/0004656204310441

In Proceedings of the International Conference on Knowledge Engineering and Ontology Development (SSEO-2013), pages 431-441

ISBN: 978-989-8565-81-5

Copyright

c

2013 SCITEPRESS (Science and Technology Publications, Lda.)

Costing (ABC) which adds more complexity, needs

large data estimates calculations, and not considers

the subjective time consumption of resources.

Therefore we propose a method based on DEMO

Methodology (Dietz, 2006) and on TDABC theory

(Kaplan and Anderson, 2007). This research was

conducted using the Design Science Research

Methodology, a framework commonly accepted to

produce of Design Science Research in Information

Systems.

The main contribution to solve the identified

problem is the understanding of where costs occur

relating the essential operations to their

implementation costs, and areas of responsibility.

This would provide information for managers to

support their managing decisions, making

organizations more profitable (Pesonen, 2001).

The remaining paper is structured as follows, in

Section 2 we present the related work. In Section 3

we explain our proposal. A demonstration of the

proposed artifact is shown in Section 4. In section 5

a conclusion, the achievements and the future work

are presented. In appendix we present the auxiliary

calculations tables (Appendix B).

2 RELATED WORK

In this section we detail the work that has been done

in this domain of investigation. We will describe

Enterprise Ontology and TDABC in Sections 2.1

and 2.2.

2.1 Enterprise Ontology

Enterprise Ontology (EO) is a comprehensive theory

that supports DEMO methodology and allows

overcoming organizations complexity.

This last is composed by methods and techniques

based on EO theory, so that organizations

conceptual model can be constructed showing only

the essence of the operations in way that is coherent,

comprehensive, consistent and concise (Dietz 2006).

EO is defined as the structure behind the

observable surface, the realization and

implementation independent essence of an

organization.

Competing methodologies do not guarantee to

produce implementation independent models, and in

addition the aspect models are not totally linked to

each other.

2.1.1 Theory

The PSI-Theory is the theory that supports the

notion of Enterprise Ontology. It is based on four

axioms (operation, transaction, composition,

distinction) and one theorem (organization theorem).

Operation axiom explains that operations are a

set of actor roles activities, either roles of authority

or responsibility, fulfilled by subjects, which

perform production acts or coordination acts. Their

results are production facts - goods and/or services -

and coordination facts - commitments with others.

2.1.2 Methodology

DEMO methodology consists of four aspect models

with particular diagrams, lists and tables:

The Construction Model (CM) specifies the

identified transaction types and the associated actor

roles, as well the information links between actor

roles and the information bank. The composition,

structure and environment of organizations can be

specified by the CM using two models: 1) The

Interaction Model (IAM) that shows active

influences between actor roles, i.e. the execution of

transactions; 2) The Interstriction Model (ISM)

showing the passive influences between actor roles;

The Process Model (PM) contains the specific

transaction pattern of the transaction type, also the

causal and conditional relationships between

transactions. Those relationships determine the

transaction patterns and the possible trajectories in

the Coordination-world (transition space and state

space);

The Action Model (AM) specifies action rules as

guidelines for actors deal with their agenda. Action

rules guide how the performing actor role should

respond to the reached status;

The State Model (SM) identifies the state space

of P-world: object classes and fact types, the result

types, and ontological coexistence rules. SM is ideal

to start developing and maintaining the data

dictionary of an organization, facilitating the

identification of business components (software

components), based on the fact types around

categories.

These models are illustrated in Figure 1 and

constitute the complete ontological model of the

organization. To produce the aspect models we use

the logical sequence anticlockwise, starting with

interaction model (IAM).

As business architectures approaches areas such

as management science, business administration,

logistics and informatics, they are unable to provide

integrated understandings of actors, communication,

KEOD2013-InternationalConferenceonKnowledgeEngineeringandOntologyDevelopment

432

production and their realizing technologies (Mulder

and Dietz n.d.).

Figure 1: DEMO ontological aspects models and diagrams

(Dietz, 2006).

Regarding this concerns, Enterprise Ontology

offers a new kind of understanding, brought by the

approach of Design & Engineering Methodology for

Organizations.

2.2 Tdabc

Time-driven activity-based costing is an alternative

approach to ABC model estimation, addressing its

limitations being: simpler, faster to implement, and

less costly.

TDABC allows overcoming transaction

complexity, by using time equations and time

consumption of process in the departments, basing

the cost driver rates on the practical capacity of

supplied resources (Kaplan & Anderson 2007).

This new approach considers the number of

times that an activity is performed (number of

production runs, setups, number of shipments,

purchase orders, and number of customer orders)

and resources effort that is required to perform

activities (setups that might be more complex or

difficult to do than others, time and effort spent).

In ABC, transactions heterogeneity is handled in

two ways: 1) Expanding the number of activities

(simple orders, average orders, and complex orders).

2) Using duration drivers to estimate the required

time to perform the task (example are the material

handling time, setup hours, direct labour hours and

machine hours).

The simplicity of Time Driven Activity-Based

Costing is essentially to measure and manage the

capacity of organization, requiring only two

estimates: 1) The unit cost of supplying capacity,

and 2) The consumption of capacity (unit times) by

the activities the organization performs for products,

services, and customers.

2.2.1 Estimating Unit Cost

For estimating the cost of supplying capacity,

various groups of resources that perform activities

must be identified (activities performed in

administration, front-line employees, their

supervisors and the support resources).

There are two possible ways of measuring

practical capacity. One is to estimate practical

capacity as a percentage of theoretical capacity,

including personnel time for breaks, arrival and

departure, communication and reading unrelated to

work, machine time for downtime due to

maintenance, repair, and scheduling fluctuations.

The other way is to measure practical capacity,

obtaining historical time of activities and taking in

consideration fluctuations that can occur in certain

periods (due to excessive delays, poor quality,

overtime, or stressed employees). This number is

then used as the estimate for capacity of resources

that perform that activity.

After estimating the 1) cost of supplied capacity

of each resource and 2) the practical capacity, the

analyst can calculate the unit cost using Eq. 1:

Unit Cost = (Cost of capacity Supplied) /

(Pratical Capacity supplied)

(1)

The numerator includes direct or indirect expenses

attributed to the unit and the denominator is the

available capacity time.

2.2.2 Estimating Unit Time

TDABC requires an estimation of the time an

activity takes to be performed. The procedure uses

an estimate of time, replacing the ABC process of

interviewing people. The time estimates can be

obtained either by direct observation or by

interviews, rough accuracy is sufficient.

An analysis to the results obtained by the model

can reveal the costs of both resource capacity used

and resource capacity unused. Rather than reducing

unused capacity in the present, managers can choose

to reserve that capacity to grow in the future.

Managers can forecast how much the business

can handle with the existing capacity and if capacity

shortages might happen.

2.2.3 Time Equations

Business processes activities have different

durations, being similar to requests, complains, or

performing other transactional activity. Companies

most of the times can predict the drivers that turn

transactions into simpler or more complex ones

Demo-basedCostModel

433

(Kaplan and Anderson, 2007).

For example, to dispatch a letter in the post

office the operation may take 2 minutes, but if the

item requires a special delivery then an additional 4

minutes might be required, also if the item has more

weight another 2 minutes is required to weigh in the

balance.

Instead of defining separate activities to each

procedure, the time-driven approach uses a simple

equation, Eq. 2:

Dispatch Time =

= 2 + 4 (if special delivery required)

+ 2 (if additional weight)

(2)

TDABC approach is a powerful framework and is

useful to apply in our proposal because: 1) it is more

accurate and can operate with fewer equations than

the number of activities in traditional ABC systems,

allowing a variety and complexity in products,

orders, and customers; 2) it gives information about

the unit cost and unit times, as consequence the

knowledge about possible improvements in

efficiency (Kaplan and Anderson, 2007).

With TDABC a time equation model can be

obtained, reflecting any business processes

complexity and variability. The complexity in

processes can be surpassed by modelling

departments as one process, in one time equation.

Time equations can also be expanded to add

more terms including variations of different types of

transactions, reflecting the actual activities during

each period (Kaplan and Anderson, 2007).

In our proposal time-equations can allow us to

calculate the costs of activities, based not only on

the used resources but also on the time consumed.

3 PROPOSAL

This section corresponds to objectives definition for

solution, design and development steps of DSRM.

3.1 Objectives of the Solution

The objectives for a solution have two major

concerns: first the need to obtain an artefact that

allows modelling an organization in a

comprehensive, consistent and concise way; second

the artefact should allow identifying and relating the

implementation costs with organization's essential

operations.

3.2 Proposed Method

We propose an artefact that uses contributions from

both TDABC and DEMO methodology. We choose

to use DEMO since it was conceived to overcome

complexity.

This methodology allow us to separate the way

organization is implemented from its ontological

essence, reducing the analysis complexity and allow

to be more focus on the system of interest (Dietz,

2006).

Organizations consist of people, interacting in

order to coordinate and perform work. The duration

of their activities should also be included when

modelling organization costs. To consider this aspect

we propose to use TDABC time equations, adapting

them to reflect not only the duration of essential

activities but also their dependencies.

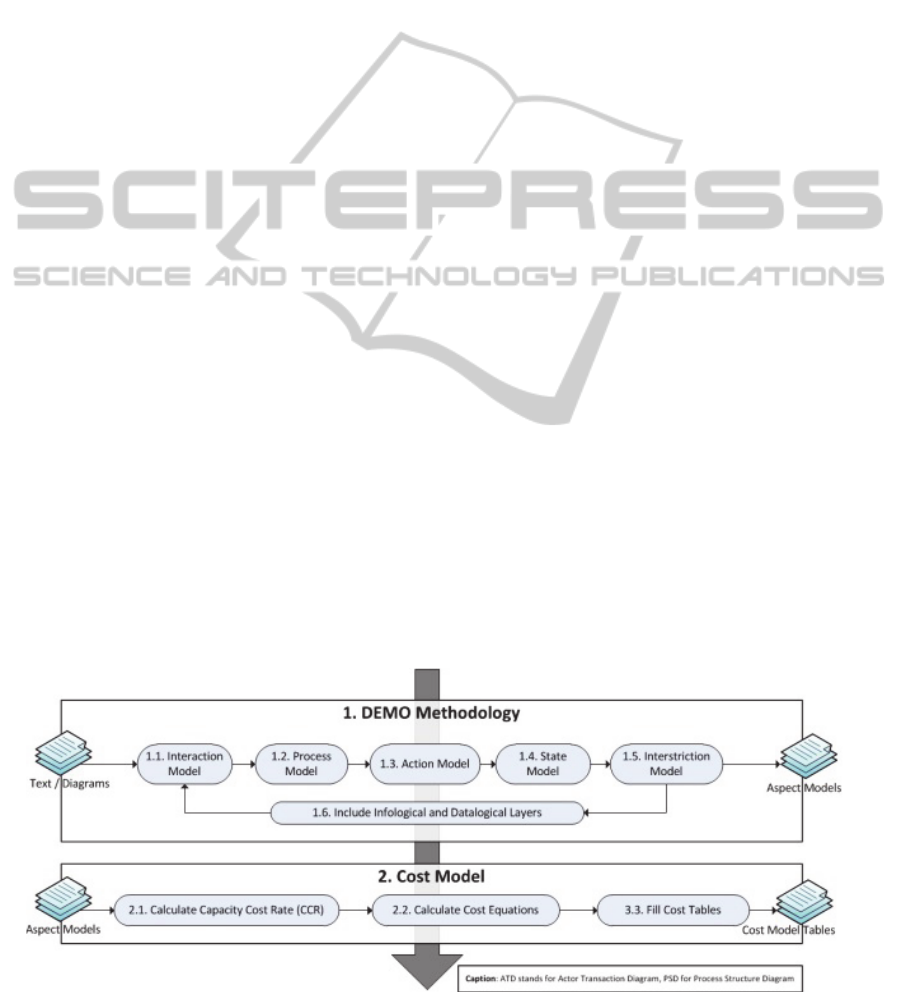

In Fig. 1 we introduce the proposed method with

a diagram, showing two phases each with several

steps. The first phase consists on DEMO

Methodology and the second phase is based on

TDABC theory.

Figure 1: Steps of the proposed method.

KEOD2013-InternationalConferenceonKnowledgeEngineeringandOntologyDevelopment

434

3.2.1 Demo Methodology

The first phase is based on DEMO Methodology and

is composed of six steps as shown in Fig. 1. Each

step consists on modelling the aspect models (Dietz,

2006), we propose to consider not only the

ontological transactions but also the infological and

datalogical transactions, identifying them with the

respective colours (accordingly to the distinction

axiom) and a letter "I" and "D" before the

designation of infological and datalogical

transactions respectively.

With the Process Structure Diagram (PSD), the

Actor Transaction Diagram and Result Structure

Chart, in particular, we can understand which

dependencies exist between acts and continue to the

second phase.

3.2.2 Cost Model

The second phase is based on TDABC theory

(Kaplan and Anderson, 2007). Having as output the

diagrams of first phase we can proceed to the steps

of Cost Model.

Capacity Cost Rate. The first step of this phase is

to calculate Capacity Cost Rate (CCR) for each

Actor Role using Eq. 3. The variable (x) belongs to

Actor domain and (y) belongs to Actor Role

domain.

CCR (x,y) = (Expenses Attributable to (x)

who fulfill (y)) / (Available Capacity of (x)

who fulfills (y))

(3)

The Eq. 3 gives actor role cost for unit of time, the

numerator includes expenses related to the time

period in consideration.

Some examples of Portuguese organization

expenses that can be divided in two categories are

personnel expenses (salary, social security, holiday’s

subsidy, Christmas subsidy, sickness subsidy, meal

subsidy, taxes) and operation expenses (space rent,

electricity, water, equipment, services, training, and

taxes). The denominator is calculated as the

available capacity of resource.

We start with the number of days in one year,

then we subtract non-working days (to get the

number of working days in a month) and finally we

multiply this last value with the available hours per

day of work. Available hours per day of work are

obtained by subtracting to daily work hours the non-

work times. Some examples of non-work days/times

are holidays, breaks, vacations, expected

personal/sick leave, and training.

Cost Equations. The second step of Cost Model

phase is to calculate cost equations, starting by act

cost equation, Eq. 4.

Act_cost = CCR_ActorRole

+ estimated_time + number_ocurrences +

specific_cost + dependencies_cost

(4)

Eq. 4 is calculated having as basis several

parameters:

CCR_ActorRole is the capacity cost rate

calculated previously;

estimated_time the average estimation time of

act;

number_ocurrences as the number of times act

was performed;

specific_cost are the act costs not included in

CCR (x,y) numerator expenses. Taking an

example of a pharmacy, when a medicine is

dispensed, the specific costs is the medicine cost;

dependencies_cost are costs of other acts costs

that must be performed before, dependencies can

be captured following the conditional lines in

PSD diagram.

After calculating Acts Cost we calculate transaction

cost using Eq. 5. Transaction_cost which is the sum

of both Executor_(cost) and Initiator_Cost.

Table 1: Table model to represent Transaction Costs.

Transaction

rq dc qt pm ex st rj sp ac Txsum

Initiator

€a €b €c €d €e €f €g €h €i €j

Executor

€k €l €m €n €o €p €q €r €s €t

Table 2: Table model to represent Business Process Costs.

A01 A02 (…) A0M Sum

T1 €c11 €c12 € (…) €c1M €c1

T2 €c21 €c22 € (…) €c2M €c2

(…) € (…) € (…) € (…) € (…) € (…)

TN €cN1 €cN2 € (…) €cNM €cN

Sum €c01 €c02 € (…) €c0M

€BP

We consider participations from Initiator acts

times in some Executor acts time, meaning that in

some business processes we might want to assume

that initiator and executor have both the same act

time duration.

For example in a Pharmacy when a client makes

a request that is being heard by the pharmacist, the

duration of the request will be the same for initiator

and executor, so we will differentiate this as it can

be seen represented in cost tables (Table 1).

Transaction_cost =

= Initiator_Cost + Executor_(cost) =

= (Sum of Initiator Acts_cost)

+ (Sum of Executor Acts_cost)

(5)

Demo-basedCostModel

435

The Business Process Cost BP_cost can be obtained

with Eq. 6 for ontological transactions T1 to TN.

Here we only consider ontological transactions

that have their result at the end of the result structure

chart, since we don't want to include costs that

already were considered, due to dependencies (Eq.

4).

BP_cost = T1cost + T2cost + ...+ TNcost (6)

Cost Tables. The third step of phase two is to fill

cost tables. In Table 1 we represent the Transaction

Costs, which we only consider transactions that are

parameters of Eq. 6. Here two rows represent

Initiator and Executor Actor Role, their acts are in

columns and each cell will have the correspondent

Act Cost (calculated using Eq. 4).

In Table 2 we represent Business Process Costs,

but only those that are parameters of Eq. 6. Here we

can represent also how each Transaction Cost is

related to each Actor Role responsibility area,

understanding the implementation cost for the

organization when providing a service or product.

DEMO models show actor roles and their area of

responsibility (represented in Fig. 4 with a grey

colour rectangle). Since the limit of actor roles

responsibility areas is well defined, we can trace

costs between actor roles and their acts. The

advantage of associating costs to actor roles is the

overview about specific roles costs, understanding

which ones are more costly.

The Cost Model is the last phase of the proposed

method. With this method we have a direct

correspondence between ontological acts costs and

their implementation costs. Then analysis can be

made, concerning which transactions are more

costly, who is responsible for them, or even make

other conclusions about the organization costs.

4 DEMONSTRATION

This section corresponds to the Demonstration step

of Design Science Research Method. The

application of the artefact is presented using Invoice

Management of a Portuguese research group.

4.1 Modelling Phase

The research group is a Portuguese private group

composed by thirty persons, dedicated to the

research, innovation and development of new

solutions to problems in the IT Governance and

digital services areas. The invoice department is a

shared service company that provides financial

services to the research group, including invoice

management.

Next we describe the invoice management

process, making DEMO analysis. In red we colour

Performa items, green Informa items, and for Forma

items. Brackets enclose parts of text, namely “[“ and

“]” indicate an actor role, “(“ and “)” indicate a C-

act/result, and the brackets “<” and “>” indicate a P-

act/result.

The process is conducted by e-mail. It starts

when the [chief of the research and development

unit] needs to (send an invoice) to a [customer].

He then (e-mails) [someone at the invoice

department], belonging to the shared services

company that provides financial services. This e-

mail contains information about the date, value,

address or description that should be present in

the invoice. After receiving the e-mail, the

[invoice department] <has to create the invoice>

and <send> it to the [customer], adding in

carbon copy (CC) the chief of the research and

development unit. When the invoice is paid, the

research group leader receives an e-mail

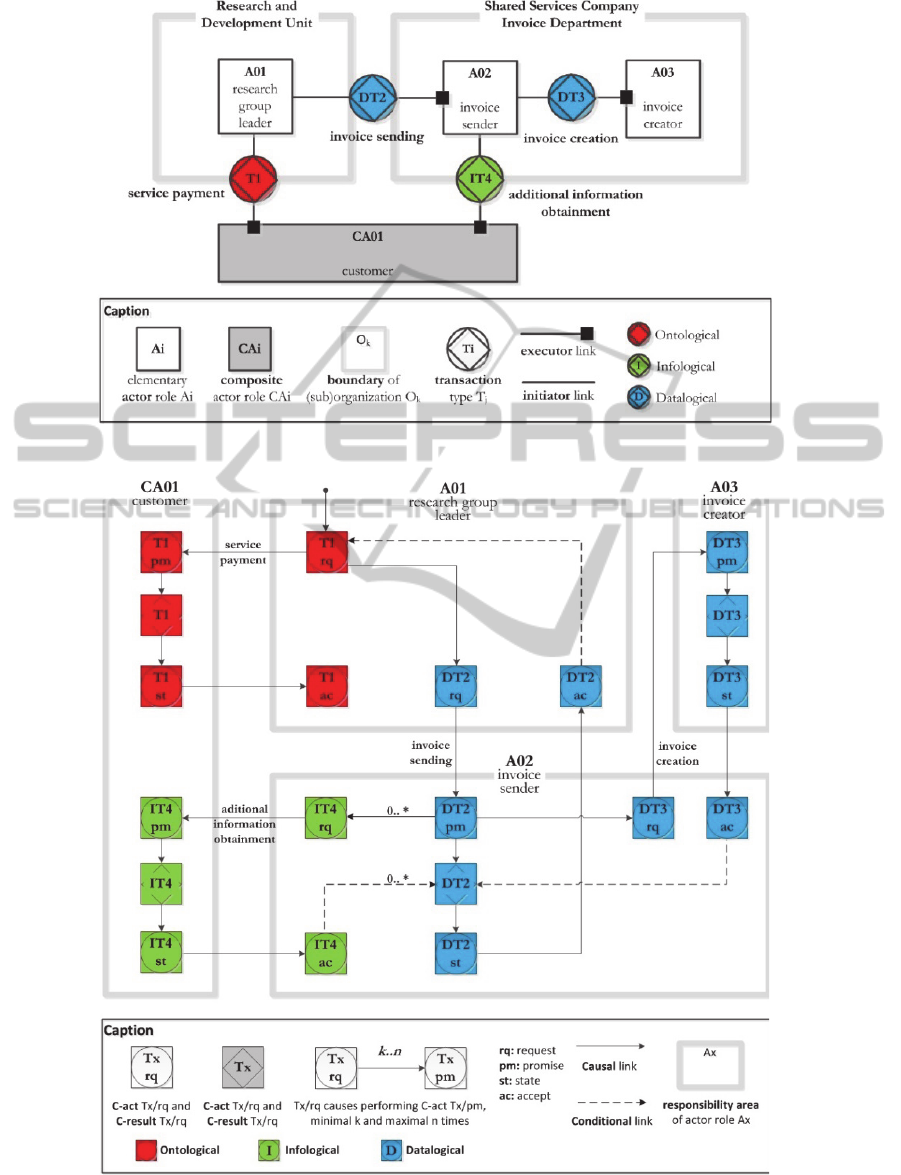

In Table 3 we present all identified transactions,

their result, and then we colour them accordingly to

each transaction type. Note that transactions that are

not ontological are identified as DT or IT, meaning

that they are datalogical transaction or infological

transaction, the same for transactions results.

Table 3: Transaction Result Table (TRT) with transaction

types and result types.

Transaction Result Type

T01 service payment R01 service P has been paid

DT02 invoice sending

DR02 invoice I has been sent

on date D

DT03 invoice creation

DR03 invoice I has been

created on date D

IT04 additional

information obtainment

IR04 additional information for

invoice I has been obtained

The Result Structure Analysis allows us to

identify dependencies and in this case three

dependencies are identified.

Figure 2: Result structure chart.

KEOD2013-InternationalConferenceonKnowledgeEngineeringandOntologyDevelopment

436

Figure 3: Actor Transaction Diagram (ATD).

Figure 4: Process Structure Diagram (PSD).

Demo-basedCostModel

437

In Fig. 2 we can see the first dependency is that

in order to pay for the service, an invoice has to be

sent first, but for that it has to be created (second

dependency).

The third dependency is the result of additional

information to pay the service. Since this

dependency is optional, the minimum number is

zero and the maximum number is variable.

4.1.1 Interaction Model

The interaction model is presented next, where

transactions are coloured accordingly to the

distinction axiom.

In Fig. 3 the actor role A01 (research group

leader) represents the person who want the service to

be paid (Transaction T1) by the customer,

represented by the actor role CA01. The actor roles

A02 and A03 represent the person who works in the

Invoice Department, responsible for sending

(transaction DT2) and creating the invoice

(transaction DT3). Actor role A02 can also request

to customer additional information (transaction IT4).

4.1.2 Process Model

In figure 4 we present the Process Structure Diagram

(PSD) for invoice management.

In PSD we colour the acts accordingly to the

distinction axiom. Transaction T1 represents a

request for service payment, by the Research Group

Leader to customer. Transaction DT2 is initiated and

leads to a request for invoice sending, by the

Research Group Leader to the invoice sender. If

more information was needed, IT4 request would be

initiated by the invoice sender and executed by

customer, this demonstration consider that IT4 do

not happen. In Transaction DT3 there is a request for

invoice creation, by the invoice sender to invoice

creator.

We could continue to present the other diagrams,

but ATD and PSD are enough for this

demonstration, since they have all the information

we need to proceed to the Cost Model phase.

4.2 Cost Model

The second phase of the demonstration continues

with Cost Model, which is composed by three steps:

1) Calculate Capacity Cost Rate; 2) Calculate Cost

Equations; 3) Fill Cost Tables.

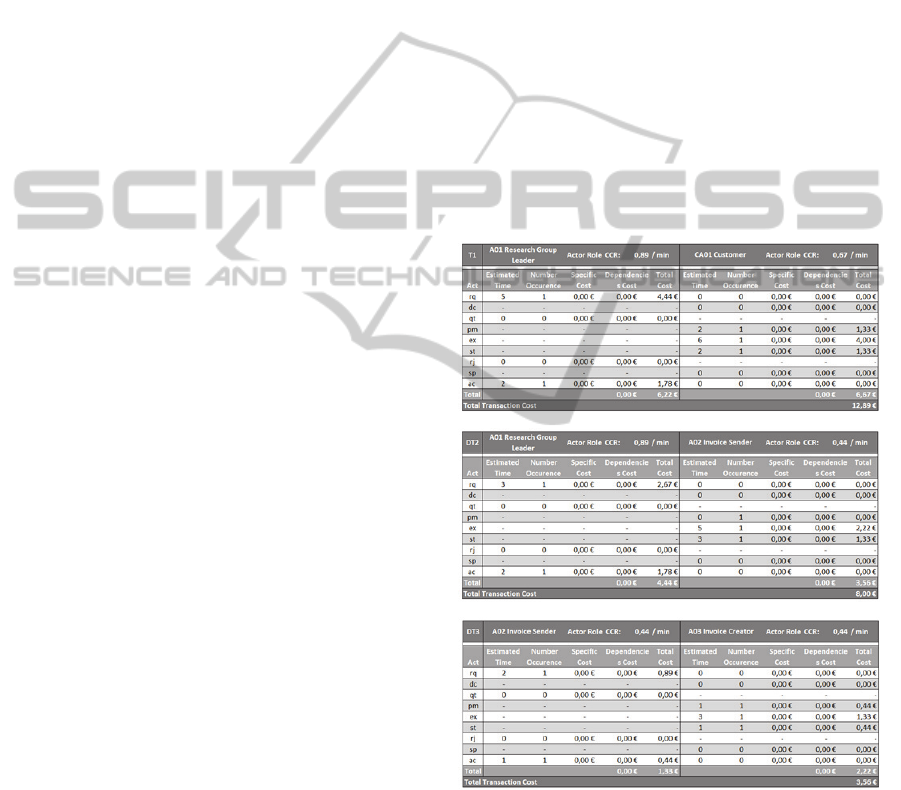

4.2.1 Capacity Cost Rate

Based on the PSD of Fig. 4 we construct Table 4 to

show CCR for Actor Roles, using Eq. 3 in which the

expenses and available capacity indicated are only

estimates (considered to be four times more than the

cost of a salary).

Table 4: Capacity cost rate calculation.

Actor Role

Expenses

Attributable

by month

Available

Capacity in

minutes

CCR

€/min

CA01

Customer

€ 6000 9000 minutes 0.67

A01 Research

Group Leader

€ 8000 9000 minutes 0.89

A02 invoice

Sender

€ 4000 9000 minutes 0.44

A03 Invoice

Creator

€ 4000 9000 minutes 0.44

4.2.2 Cost Equations

In this step we calculate the cost equations, which

calculations are in attachment (see Appendix).

KEOD2013-InternationalConferenceonKnowledgeEngineeringandOntologyDevelopment

438

Table 5: Transaction T1 Costs.

T1

rq dc qt pm ex st rj sp ac €24.44

A01 Research Group Leader €16 - €0 - - - €0 - €1.78 €17.78

CA01 Customer €0 €0 - €1.33 €4 €1.33 €0 €0 €0 €6.67

Table 6: Unitary Transaction Cost for each Actor Role.

CA01 A01 A02 A03 Sum

T1 €6.67 €6.22 €0.00 €0.00 €12.89

DT2 €0.00 €4.44 €3.56 €0.00 €8.00

DT3 €0.00 €0.00 €1.33 €2.22 €3.56

IT4 €0.00 €0.00 €0.00 €0.00 €0.00

Sum €6.67 €10.67 €4.89 €2.22 €24.44

Since Transaction IT4, corresponding to

additional information obtainment, was not initiated

the cost equations for this transaction were not

presented.

4.2.3 Cost Tables

Next we fill the first cost table to calculate each act

cost. Notice that we only have one transaction

represented in Table 5, since there is only one

transaction that has result at the end of result

structure chart.

The reasoning to obtain implementation costs of

T1rq was:

T1rq_cost = T1rq_(unit.cost) + DT2_cost +

DT3_cost = €4.44 + €8.00 + €3.56 = €16.00

(7)

We do not present a similar table to Table 2 to

represent this Business Process Costs, since there is

only one ontological transaction. However, we

choose to represent in Table 6 the cost of each

unitary transaction (without its implementation cost)

for each actor role.

In Table 6 we can observe that Business Process

Cost is €24.44, but if we exclude CA01 cost, the

client participation on costs, we can calculate

organization invoice management cost: €24.44 -

€6.67 = €17.78.

5 EVALUATION

This evaluation assesses the demonstration we made

at Invoice Department. We have collected feedback

from practitioners, applied the Moody & Shanks

Framework and used the Österle principles.

5.1 Evaluation Strategy

In this subsection we identify what is actually

evaluated, how it is evaluated and when the

evaluation takes place. To do so we illustrate the

answers in three questions proposed by the

framework (Pries-Heje 2004):

What is actually evaluated? The artifact to be

evaluated is the method proposed, Section 3.2;

How is it evaluated? We used feedback gathered,

the Moody & Shanks and the Österle Principles

to evaluate the DEMO-based Cost Model. This

represents a naturalistic evaluation, it was

conducted in a real organization, using a real

artefact;

When was it evaluated? It was evaluated ex post,

after the design artefact was developed.

To evaluate the proposed artifact, using the eight

quality factors of the Moody & Shanks Framework,

the following results are presented:

Completeness: our focus is on one specific part

of the organization, however we consider that the

Transaction Result Table and the Actor

Transaction Diagram can represent consistently

the description of the Invoice and Research

Departments;

Integrity: we have identified dependencies

between the transactions which are illustrated in

the Process Structure Diagram (PSD), and

expressed the organization business process;

Flexibility: this aspect of quality decreases with

the increase of the number of transactions, actor

roles and dependencies;

Understandability: the models at the beginning

are difficult to understand because the

stakeholders must know DEMO in order to

model the organization with the models proposed

in this methodology;

Correctness: DEMO and TDABC have strong

theoretical foundation, that allows to model

correctly organizations and trace the

implementation costs of essential operations;

Simplicity: DEMO and TDABC allow to

overcome the complexity of organizations;

Demo-basedCostModel

439

Integration: with the description of the

organization we have enough information to

construct the Transaction Result Table (TRT),

the Result Structure Chart and to model the

organization. We think that these models are

consistent with organizations reality and allow to

model the organization in a consistent way, by

easily integrating DEMO and TDABC;

Implementability: this artifact can be

implemented since DEMO allows to model the

organizations implementation operations details

and focuses on organization essence.

As results of applying Moody & Shanks Framework,

the negative aspects were Flexibility and

Understandability, the other aspects have a positive

result.

5.2 Österle Principles

We present the evaluation of the proposed artifact,

based on the feedback received from academics and

practitioners. This research was presented at a

workshop, attended by experts who gave some

positive feedback of our proposal, allowing us to

answer the Österle principles:

Abstraction: this artifact can be applied to

different organizations and operations,

considering the ontological, infological and

datalogical layers. Organizations operations can

be identified through interviews, documents and

from a given description;

Originality: the proposed artifact has the novelty

of combining DEMO and TDABC. This new

approach allows to aggregate implementation

details into actor roles, regarding time equations

in transaction acts;

Justification: the artifact is justified by the

”Theorical Background” of DEMO and TDABC,

with a strong conceptual foundation allowing to

eliminate all the inconsistencies and limitations

occurring in other solutions. Also, our artifact

was validated by the positive feedback gathered

when communicating our findings to

practitioners, as explained before;

Benefit: the DEMO-based Cost Model allows to

identify and trace the costs of implementing the

organizations essential operations in a fast and

easy way. The feasibility of aggregating costs

especially between actor roles and their

responsibility in acts, transactions and business

process cost, gives an important contribution to

solving the identified problem.

6 CONCLUSIONS

Managing organizations is a growing challenge due

to their complexity. The traceability between the

organization essence and the respective

implementation costs has been lost. Most

organizations do not have a coherent, comprehensive

and consistent vision of the costs related to the

essential operations (Dietz, 2006).

In this research we have presented a DEMO-

based cost model solution. We expect that this

solution can give a contribution to the understanding

of essential operations costs, relating them to their

implementation costs and areas of responsibility. So

far we found several aspects: it is possible to have a

traceability between the enterprise essence, the

implementation costs and responsibility areas costs;

an association is possible between TDABC terms

and DEMO terms; a composite cost structure can be

constructed in DEMO, relating acts cost,

transactions cost and business process cost.

The research was conducted using the Design

Science Research Methodology. The evaluation of

our proposal uses several methods as the Moody and

Shanks Quality Management Framework, the

Österle et al. principles and communication to

scientific community. As future work, we intend to

apply and validate our proposal in several

organizations in the next months. Also we intend to

submit papers, communicating our findings to the

scientific community and other interested audience.

REFERENCES

Association of Chartered Certified Accountants & Institute

of Management, Finance leaders survey report:

December 2012, viewed April 2013,

<http://www.imanet.org/PDFs/Public/Research/pol-af

b-fls01.pdf>.

Blocher, E., 2005, Cost Management: A strategic

emphasys, McGraw-Hill/Irwin, viewed 2005.

BusinessBalls, Business Process Modelling History,

viewed April 2013, <http://www.businessballs.com/

business-process-modelling.htm>.

Chinosi, & Trombetta, A., 2012, 'BPMN: An introduction

to the standard', Computer Standards & Interfaces, vol

34, pp. 124--134.

Cross, R. & Parker, A., 2004, The Hidden Power of Social

Networks: Understanding How Work Really Gets

Done in Organizations, Harvard Business School

Press.

Dietz, J., 2003, 'Generic recurrent patterns in business

processes', Business Process Management, pp. 200--

215.

KEOD2013-InternationalConferenceonKnowledgeEngineeringandOntologyDevelopment

440

Dietz, J., 2006, Enterprise Ontology: Theory and

Methodology, Springer.

e3value, The e3value methodology: Exploring innovative

e-business ideas, viewed April 2013,

<http://e3value.few.vu.nl/e3family/e3value/>.

Gordijn, J., Akkermans, H. & Vliet, V., 2001, 'Designing

and evaluating e-business models', IEEE intelligent

Systems, vol 16, pp. 11--17.

Hevner & March, S 2004, 'Design Science in Information

Systems Research', MIS Quarterly, vol 28, pp. 75--

105.

Kaplan , R & Porter, , Why Medical Bills Are a Mystery,

viewed May 2013, <http://www.nytimes.com/2012/

04/15/opinion/sunday/why-medical-bills-are-a-myster

y.html?_r=3&>.

Kaplan, R & Anderson, S 2007, Time-Driven Activity

Based Costing, Harvard Business School Publishing

Corporation.

Kaplan, R. & Anderson, S., 2007, Time-Driven Activity-

Based Costing: A simpler and more powerful path to

higher profits, Harvard Business School Press.

Management and Technology Consultancy, B 2013, Spend

Management: Key Elements for Realising Cost

Savings in Procurement, <http://www.bearingpoint.

com/en-other/download/Spend_Mgmt_WP_FI_8p.pdf

>.

Moody L., & Shanks, G., 2003, 'Improving the quality of

data models: empirical validation of a quality

management framework', Information Systems, vol 28,

pp. 619--650.

Muehlen, M., 2008, 'Getting started with business process

modeling', IIR BPM Conference, Orlando, Florida.

Mulder, H. & Dietz, J., 'Business Architecture based on

the integration of Communication, Actors and

Production'.

Nuffel, Mulder & Kervel, 2009, 'Enhancing the formal

Foundations of BPMN by Enterprise Ontology',

Advances in Enterprise Engineering III, 2009, pp.

115--129.

Osterle, H., 2010, 'Memorandum on design-oriented

information systems research', European Journal of

Information Systems, vol 20, pp. 7-10.

Pesonen, L., 2001, Implementation of design to profit in a

complex and dynamic business context, viewed April

2013, <http://herkules.oulu.fi/isbn9514264509/isbn95

14264509.pdf>.

Pries-Heje, J., 2004, 'Strategies for Design Science

Research Evaluation', 16th European Conference on

Information System (ECIS).

Ray, L., 2013, Overhead Costs in a Service Industry,

<http://smallbusiness.chron.com/overhead-costs-servic

e-industry-20984.html>.

Richardson, K., 2008, 'Managing complex organizations:

Complexity thinking and the science and art of

management', Emergence, vol 10, pp. 13--26.

Roberts, & Silvester, K. J., 1996, Why ABC failed and

how it may yet succeed, viewed April 2013,

<http://maaw.info/ArticleSummaries/ArtSumRoberts9

6.htm>.

Schapper, J., Cieri, H. & Cox, J., 2005, The Ontological

and Epistemologicla Dimensions of Complex

Organisations.

Scheer, A. W., 2000, ARIS: business process modeling.

Tuunanen, T, Rothenberger, M & Chatterjee, K 2008, 'A

Design Science Research Methodology for

Information Systems Research', Journal of

Management Information Systems, vol 24, pp. 45--77.

Weinberg, G 2001, An Introduction to General Systems

Thinking, Dorset House Publishing.

Weinberg, G. M., 2001, An Introduction to General

Systems Thinking, Dorset House Publishing.

WFMC 1999, Workflow Management Coalition -

Terminology and Glossary, viewed May 2013,

<http://www.wfmc.org/standards/docs/TC-1011_term

_glossary_v3.pdf>.

Wileman, A., 2008, Driving Down Cost: How to Manage

and Cut Costs - Intelligently, Nicholas Brealey

Publishing.

APPENDIX

Demo-basedCostModel

441