A Case Study on Entropy Generation

during Business Process Execution

A Monte Carlo Simulation of the Custom Bikes Case

Peter De Bruyn, Philip Huysmans and Herwig Mannaert

Department of Management Information Systems, University of Antwerp, Prinsstraat 13, Antwerp, Belgium

{peter.debruyn, philip.huysmans, herwig.mannaert}@ua.ac.be

Keywords:

Business Process Design, Entropy, Monte Carlo Simulation, Normalized Systems, Cost Accounting.

Abstract:

Contemporary organizations require high-quality information to design and manage their business processes.

Important challenges in this context comprise (1) the decision regarding which information should be stored

and in what way, and (2) the need to allow adequate reporting for different organizational perspectives. To

tackle these issues, we proposed in previous work applying the concept of entropy as defined in statistical

thermodynamics to the domain of business process management. In this paper, we further elaborate on this

idea by performing a Monte Carlo simulation of the Custom Bikes case to show how guidelines are necessary

to control this entropy. In doing so, we extend previous theoretical contributions by releasing some simplifying

assumptions made earlier, while simultaneously proving its practical relevance in a case. Finally, this paper

discusses the important challenge for the need of adequate reporting from different organizational perspectives.

1 INTRODUCTION

Contemporary organizations require high-quality in-

formation to design and manage their business pro-

cesses. Recently, approaches for gathering and stor-

ing large amounts of data have improvedsignificantly.

For example, Radio Frequency Identification (RFID)

allows to systematically collect data at predefined lo-

cations. This data can be stored in “data warehouses”,

which can manage large amounts of data. However,

arbitrary data gathering and storage is not sufficient.

For example, the current interest in “Big Data” indi-

cates that many organizations have issues to extract

relevant information from the data available. Impor-

tant challenges in this context comprise (1) the de-

cision regarding which information should be stored

and in what way, and (2) the need to allow ade-

quate reporting for different organizational perspec-

tives (e.g., management versus operational versus ac-

counting purposes).

While many different approaches and tools are

suggested to handle these issues in practice (e.g., busi-

ness intelligence tools), a theoretical understanding of

its complexity is often lacking. Such a lack obstructs

the systematic research and development of methods

to address this issue in a scientific way, as proposed

by, for example, the Design Science methodology

(Hevner et al., 2004). Therefore, we previously in-

troduced entropy as a possible candidate for studying

the structure of data generated in business processes

(De Bruyn et al., 2012; Oorts et al., 2012). Within the

BMSD community, other engineering concepts such

as the concept of homeostasis have been suggested as

well (Regev et al., 2012). This fits within the Enter-

prise Engineering paradigm, which states that orga-

nizations should be purposefully designed, and that

engineering knowledge can be used to better under-

stand organizational phenomena or design organiza-

tional artifacts. Baring this in mind, we earlier intro-

duced a set of general prescriptive design guidelines

which can be derived from the application of entropy

to the design of business processes, resulting in a fine-

grained modular structure (De Bruyn et al., 2013).

In this paper, we further elaborate on this idea

by demonstrating these guidelines in a realistic case

study. This implies abandoning some of the simpli-

fications made in previous work (e.g., considering a

single process flow). Moreover,this approach enables

more realistic insights regarding which information

should be stored (and how), as well as the impact of

integrating multiple design perspectives. We employ

a case study of which fine-grained business processes

have been published previously (Van Nuffel, 2011).

First, we generate a realistic data set for the processes.

Next, we illustrate how violations against our design

principles (to ensure an adequate modularization of

187

De Bruyn P., Huysmans P. and Mannaert H.

A Case Study on Entropy Generation during Business Process ExecutionA Monte Carlo Simulation of the Custom Bikes Case.

DOI: 10.5220/0004775301870197

In Proceedings of the Third International Symposium on Business Modeling and Software Design (BMSD 2013), pages 187-197

ISBN: 978-989-8565-56-3

Copyright

c

2013 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

the registered data) result in an increase of entropy

during execution-time (thereby demonstrating theo-

retic relevance), resulting in a loss of certain organi-

zational insights (demonstrating practical relevance).

In the remainder of this paper, we first explain our

proposed application of the entropy concept to busi-

ness processes (Section 2). Next, we introduce the

case study (Section 3) and the data generation and set-

up (Section 4). Section 5 covers a discussion of our

findings and the implications for research and prac-

tice. Finally, we offer our conclusions in Section 6.

2 ENTROPY GENERATION

DURING BUSINESS PROCESS

EXECUTION

Entropy as expressed in the second law of thermody-

namics is considered to be a fundamental principle

in traditional engineering sciences. While many ver-

sions exist, all approaches have basically the intent

of expressing the (increasing) amount of complexity,

uncertainty (i.e., lack of information) and tendency of

particles to interact (i.e., couple) within a system. In

this paper, we use the statistical thermodynamics per-

spective towards entropy. Here, entropy was defined

as proportional to the number of possible microstates

(i.e., the whole of microscopic properties of the parti-

cles of a system) consistent with a single macrostate

(i.e., the whole of externally observable and measur-

able properties of a system) (Boltzmann, 1995). The

amount of microstate configurations which result in

the same macrostate is called the multiplicity of that

macrostate. A common way of dealing with entropy,

is to increase the structure or the knowledge of the

internals of the system. Structure can be used to con-

trol entropy by allowing less interaction between the

constituting components before the information is ob-

served. This way, as fewer microstate configurations

remain consistent with a single macrostate, less un-

certainty remains. The mechanisms related to en-

tropy reasoning have found their reflection in many

domains, including business and management topics

(Jacquemin and Berry, 1979). Even for the business

process management domain, some contributions can

be found (Jung et al., 2011).

As our application of entropy to business pro-

cesses has been discussed in detail in previous pub-

lications (De Bruyn et al., 2012; Oorts et al., 2012;

De Bruyn et al., 2013), we only recall our reason-

ing here briefly. First, the run-time instantiation space

of a business process needs to be defined (De Bruyn

et al., 2013). The modular structure of a business

process has been defined to consist of process mod-

ules and task modules (Van Nuffel, 2011). Therefore,

the design of a business process (such as the

Order

Handling

process in Figure 1) and its constituting

tasks need to be defined (e.g., we used BP

1

for a busi-

ness process and t

1

for a task). Moreover, the run-time

instantiation space requires the identification of each

instantiation of the business (e.g., instantiation BP

1,1

process and its tasks). Therefore, a possible business

process instantiation space might be:

BP

1,1

= {t

1,1

, t

2,1

, t

3,1

, t

5,1

}

BP

1,2

= {t

1,2

, t

2,2

, t

4,1

, t

5,2

}

BP

1,3

= {t

1,3

, t

2,3

, t

3,2

, t

5,3

}

Second, the interpretation of microstates and

macrostates has been elaborated upon (De Bruyn

et al., 2012). A microstate of a process is the union of

values of properties for each individual process par-

ticle (i.e., a task instantiation). A macrostate refers

to the observable information of the process as a

whole (e.g., throughput time or quality measures).

Third, a set of aggregation dimensions has been pro-

posed, which indicate how the multiplicity of a busi-

ness process macrostate increases when information

of the task instantiations is aggregated. Fourth, four

principles have been discussed to structure the task

information: (1) Separation of States (SoS): states

should be introduced as measuring points through-

out a process; (2) Separation of Concerns (SoC): a

unique state should be introduced for separating infor-

mation regarding each individual relevant information

unit or concern; (3) Data instance Traceability (DiT):

each business process and task instance should be

linked to its information input and the information ob-

ject (specifics) it is operating on; (4) Action instance

Traceability (AiT): each task instantiation should be

linked to the specific business process instantiation

it is embedded in. Principles 1 and 2 relate to the

Normalized Systems (NS) principles (Mannaert et al.,

2011) at design-time. In contrast, principles 3 and 4

can only be applied in the run-time instantiation space

(Mannaert et al., 2012). While a conceptual example

was already discussed (De Bruyn et al., 2013), a call

was made for the application of the entropy concept to

a more realistic case, which will be part of the present

paper.

3 CASE DESCRIPTION

The “Custom Bikes case” used in this paper has orig-

inally been introduced by Van Nuffel (2011) and de-

scribes the business processes of a small company

producing customized bicycles. In order to adapt the

Third International Symposium on Business Modeling and Software Design

188

KƌĚĞƌ,ĂŶĚůŝŶŐWƌŽĐĞƐƐ

WĂƌƚWƌŽĐĞƐƐ

͘͘͘

ZĞŐŝƐƚĞƌ

KƌĚĞƌ

͘͘͘

ǀĂůƵĂƚĞ

KƌĚĞƌ

^ĞŶĚZĞũĞĐƚ

EŽƚŝĨŝĐĂƚŝŽŶ

ƌĞũĞĐƚĞĚ

ƐƐĞŵďůLJ

ƉƌŽĐĞƐ

͘͘͘

/ŶǀŽŝĐĞ

WƌŽĐĞƐƐ

ZĞƚƌŝĞǀĞ

YƵĂŶƚŝƚLJŽŶ

,ĂŶĚ

ĞƚĞƌŵŝŶĞ

ǀĂŝůĂďŝůŝƚLJ

ZĞƐĞƌǀĞƉĂƌƚǀĂŝůĂďůĞ

YƵŽƚŝŶŐ WƌŽĐƵƌĞWĂƌƚ

WĂƌƚWƌŽĐĞƐƐĐĐĞƉƚĞĚ

ƌĂĨƚWĂƌƚ

ZĞƋƵŝƌĞͲ

ŵĞŶƚƐ

EŽƚ

ǀĂŝůĂďůĞ

KƌĚĞƌ

ƌĞĐĞŝǀĞĚ

ZĞũĞĐƚĞĚ

&ŝŶŝƐŚĞĚ

WĂƌƚ

ZĞƋƵĞƐƚĞĚ

ZĞƐĞƌǀĞĚ

WĂƌƚZĞĐĞŝǀĞĚ

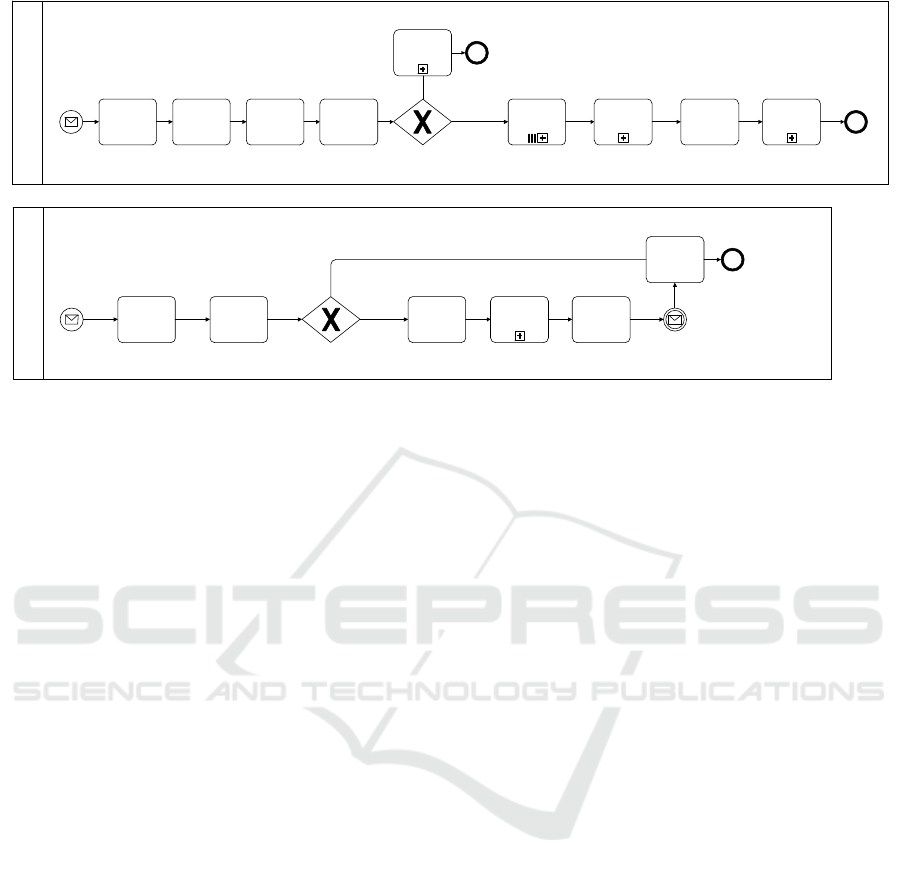

Figure 1: BPMN representations of the business process types

Order Handling

and

Part

.

complexity of the case to the available page limit, we

focus on the

Order Handling Process

. Further, a

set of assumptions were made to limit the complexity

added in the run-time analysis (see Table 1). The pro-

cess, depicted in Figure 1, describes the receipt of an

order, which triggers some administrative processes

or tasks (i.e., the first three tasks). Next, the order is

evaluated and, if it is accepted, the parts for the order

are reserved. Since a part is a differentconcern (i.e., it

is located on a different aggregation level(Van Nuffel,

2011, p. 199)), it is represented in a different busi-

ness process, i.e., the

Part Process

. For every part

which is requested, the stock availability is checked.

If a part is available, it is reserved immediately. Oth-

erwise, quotes are requested from different suppliers,

and the part is ordered from of the suppliers. When

the part is received, it is reserved as well. As soon

as all the parts are reserved, the bicycle is assembled,

and an invoice is sent.

Our case selection was primarily motivated by

the fact that these business processes already exhibit

a highly fine-grained modular structure, designed to

prevent the occurrence of combinatorial effects. Such

effects are defined as the need to adapt multiple pro-

cesses when a single change is required. For ex-

ample, if the

Part Process

would be included in

the

Order Handling Process

, other processes re-

quiring parts (such as a

Repair Service Process

)

would need to include these process steps as well.

Consequently, a change to the

Part Process

(e.g.,

adding a task) would need to be applied in two differ-

ent processes. The elimination of combinatorial ef-

fects has been shown to be a prerequisite to achieve

systems theoretic stability (Mannaert et al., 2011).

Further, it has been shown that the fine-grained mod-

ular structures needed to obtain stability in the design,

also tend to reduce entropy at run-time (Mannaert and

Verelst, 2009). Therefore, while the run-time perspec-

tive of entropy might require the application of ad-

ditional principles, we hypothesize that the modular

business process design as proposed by Van Nuffel

already exhibits a low amount of entropy and consti-

tutes a good starting point for our case study on en-

tropy occurrence during business process execution.

4 SIMULATION SET-UP

In order to demonstrate entropy-related benefits when

adopting normalized business processes (i.e., exhibit-

ing stability and low entropy), a set of already nor-

malized business processes should be started from.

However, to our knowledge, no organizations seem to

employ fully normalized business processes. There-

fore, we chose to perform a simulation of the de-

scribed artificial case study as they were already nor-

malized in earlier work based on the concept of sta-

bility (Van Nuffel, 2011). In terms of data and pro-

cess simulation method, a Monte Carlo experiment

was conducted. Such method generally consists of

a certain type of computational algorithm, employ-

ing a (high volume) repeated random sampling with

the aim to obtain numerical data to mimic, for in-

stance, the probabilities of certain real-life processes.

The use of Monte Carlo experiments in the context of

business processes can be noted in literature as well

(Tumay, 1996). Typically, the Monte Carlo method

is adopted to solve mathematical or operational prob-

lems for which no straightforward analytical solutions

are within reach. While the Monte Carlo method is

A Case Study on Entropy Generation during Business Process Execution - A Monte Carlo Simulation of the Custom Bikes

Case

189

Table 1: Case assumptions.

1. A part represents the most atomic unit for assembling a bike (i.e., no “sub-assemblies” exist).

2. Each bike consists out of three part types (i.e., wheels, chain wheel and frame).

3. The case organization has a fixed supplier who delivers once in a month a limited set of the most frequently used parts.

However, as the organization is specialized in delivering highly-customized bikes, it frequently occurs that this monthly-based

inventory appears to be insufficient or that the part is so rarely used that it is not included in the monthly inventory fill-up.

When a part type is not available in stock, a quoting process takes place, in which a number of possible suppliers is asked to

make a quotation for delivering the considered part. The best supplier (based on a rather complex and human-based decision)

is chosen, after which a procurement order is placed.

4. For every part which is decided to be procured externally, at least one supplier will be available.

5. In case multiple parts are ordered from the same supplier, the same delivery duration for all parts is assumed.

6. A theoretically infinite amount of concurrent production capacity is assumed. Hence, no bottlenecks due to lacking manu-

facturing resources (i.e., place, personnel, etcetera) can occur.

7. No measuring errors are taken into account. Hence, all recorded data and possible extreme values are deemed to be correct.

8. Only accepted order instantiations are considered (i.e., only positively evaluated orders are considered in our data analysis),

this means that task 3 (i.e., “Send Reject Notification”) is typically not executed.

perfectly suited to generate samples of complex prob-

ability distributions, we chose to generate our data

primarily for variables assumed to be normally dis-

tributed, as this distribution seems both sufficient to

illustrate our entropy reasoning adequately and rather

realistic when analyzing aspects like throughput time

or costs related to (tasks of) a business process.

We will now successively discuss which parame-

ters were used as an input for the generation of the

data in the experiment (i.e., the “preprocessing”), the

different simulation scenarios which were set-up to be

able to demonstrate and analyze our entropy approach

(i.e., the “simulation”) and some overall observa-

tions regarding the eventually generated data (i.e., the

“postprocessing”). The actual discussion and analysis

of our findings will be described in Section 5.

4.1 Preprocessing

As stated earlier, we primarily assumed normally

distributed variables to generate data reflecting the

throughput time and costs associated with each

task instantiation in an instantiated business process.

Hence, for each of the task types we determined a

population mean for its throughput time variable, as

well as a standard deviation and an absolute minimum

(to prevent throughput times from becoming negative

in extreme cases). Consequently, for the task types

“Register Order”, “Evaluate Order”, “Retrieve Quan-

tity on Hand”, “Determine Availability”, “Draft Part

Requirements”, “Quoting”, “Procure Part”, “Reserve

Part”, “Assembly Process” and “Invoice Process”, the

mean, standard deviation and absolute minimum are

depicted in Table 2. For all these tasks, except “As-

sembly Process”, we assumed that the costs are pro-

portional to the duration of the activity (as these tasks

are solely relying on human activities). In such case,

the cost (expressed in euro) was equal to 30 times

the duration (expressed in number of individual man

days). For the tasks “Receive Part” and “Assembly

Process”, we modeled our simulation in such way that

costs were based on a distinct normal distribution as

they were assumed to be equal to the purchasing costs

(for “Receive Part”) or related to other resources than

pure manpower such as machinery (for “Assembly

Process”).

Further, in case a part should be ordered from a

supplier, the decision regarding which supplier would

be chosen was considered to be based on a rather com-

plex and purely human decision (cf. Table 1), and the

choice was hence modeled to be evenly distributed

among all suppliers (i.e., each having a 20% chance

for each procurement instance of a part type). We

can see that each supplier has its own mean deliv-

ery time and standard deviation. One can further no-

tice that, while the mean delivery time of supplier

5 is not spectacularly higher than that of the other

suppliers, its standard deviation is. In practical busi-

ness terms, this means that this supplier is the most

unreliable one based on its delivery policy. Clearly,

organizations aiming to offer their products or ser-

vices quickly,need to havereliable and fast-delivering

suppliers. Hence, for our considered bike producing

company,this is deemed to be a problematic situation.

The underlying question which we ask ourselves dur-

ing the analysis of the case study is: to which degree

can this problematic situation be observed and traced

in different possible business process designs?

In summary, the parameters as depicted in Table 2

served as input variables to generate a number of sim-

ulations, discussed in the next subsection.

4.2 Simulation Scenarios

In order to simulate the processes as depicted in Fig-

ure 1, a number of n = 100 process instantiations was

generated. Consequently, for each of the tasks t

1

, t

2

,

t

4

(being the result of tasks t

5

, t

6

, t

7

, t

8

, t

9

, t

10

and t

11

),

Third International Symposium on Business Modeling and Software Design

190

Table 2: Parameters used as input for the Monte Carlo simulation.

task duration (man days) cost (e)

mean st. deviation minimum mean st. deviation min

Register Order (t

1

) 0.0625 0.0125 0.00625 ∼ time

Evaluate Order (t

2

)

0.1250 0.0420 0.0125 ∼ time

Send Reject Notification (t

3

)

not relevant not relevant

Part Process (t

4

)

depends on tasks 5 till 11 depends on tasks 5 till 11

Retrieve Quantity on Hand (t

5

)

0.0500 0.0100 0.0050 ∼ time

Determine Availability (t

6

)

0.0500 0.0100 0.0050 ∼ time

Draft Part Requirement (t

7

)

0.2500 0.0950 0.025 ∼ time

Quoting (t

8

)

2.5000 0.4000 0.2500 ∼ time

Procure Part (t

9

)

0.2500 0.0800 0.1000 ∼ time

Receive Part (t

10

)

depends on supplier chosen 250 40 15

Reserve Part (t

11

)

0.0500 0.0100 0.0005 ∼ time

Assembly Process (t

12

)

0.5000 0.2000 0.0050 250 50 50

Invoice Process (t

13

)

0.1250 0.0420 0.00125 ∼ time

Delivery time supplier 1 3 0.3 0.3

Delivery time supplier 2

2.8 0.3 0.28

Delivery time supplier 3

2.6 0.4 0.26

Delivery time supplier 4

3.2 0.4 0.32

Delivery time supplier 5

3.6 4 0.36

t

12

and t

13

, a task instance duration and associated

cost had to be generated for each process instantia-

tion. This was done by associating a random number

x ∈ [0, 1] with each of these task instantiations. Next,

for each of these instances, the value z

t

was calculated

for which there is a probability of x in the normal dis-

tribution of the considered task t that a lower value is

generated, so that for instance: P(cost(t

1

) ≤ z

t

) = x.

Hence, by using this procedure, for each of the task

instantiations, a cost and throughput value is assigned

based on a random sampling from their normal distri-

bution. Also for supplier selection, a random number

x ∈ [0, 1] was generated. Based on this value, sup-

plier 1 was assigned if x ∈ [0;0, 25], supplier 2 was

assigned if x ∈ ]0, 25;0, 50], etcetera.

Based on these cost and throughputvalues per task

instance, a set of performance variables could eas-

ily be calculated, such as total cost price of a prod-

uct instance, total throughput time for a product in-

stance, mean cost price of a certain product type,

mean throughput time of a certain product type, mean

throughput time of a certain task type, etcetera. Three

different case study scenarios were considered based

on this initial simulation. Each time, the same set of

randomly generated “basis” data was used. However,

some different aggregations were performed in each

of the case scenarios (cf. infra), implying a different

degree of detail or granularity regarding their result-

ing variables/indicators and hence, as we will show,

entropy. Each of these aggregations was based on

one of the aggregation dimensions we proposed in

De Bruyn et al. (2013), in which we illustrated the

business relevance of each of them. Afterwards, for

each of the considered case study scenarios, the nec-

essary performance variables could be easily calcu-

lated by summing the respective task (instances). We

will now highlight each of these case study scenarios:

Scenario 1. This scenario represents the most fine-

grained variant of our case study and the regis-

tered information exactly mimics the granularity

as represented in Figure 1, applying the guidelines

as proposed in the work of Van Nuffel (2011).

Hence, no summation on top of these fine grained

tasks or their instances is made. Also, informa-

tion regarding the data used for each task instan-

tiation as well as the business process instance to

which it belongs, is persisted. Consequently, no

entropy should be able to occur as each of the

NS entropy principles is adhered to. This scenario

corresponds to an example of aggregation dimen-

sion 1 in De Bruyn et al. (2013).

Scenario 2. In this scenario two activities within the

Part Process

are combined (“Procure Part” and

“Part Received”) into a new task labeled t

19

. This

means that, for each process instance, no sepa-

rate state is kept between the execution of these

steps and, hence, no independent information on

the execution of these both tasks is available for

the observer. This scenario corresponds to an ex-

ample of aggregation dimension 2 in De Bruyn

et al. (2013). However, as this might cause in-

formation loss regarding two (arguably) relevant

parts in the process, this scenario is expected to

create a certain degree of entropy due to SoS and

SoC violations.

Scenario 3. In this scenario, the data regarding the

Part Process

execution does not include in-

stance specific information such as: for which

A Case Study on Entropy Generation during Business Process Execution - A Monte Carlo Simulation of the Custom Bikes

Case

191

Order Handling Process

instance was a par-

ticular

Part Process

instance carried out? Was

the

Part Process

instance aimed at providing

the wheels, frame or chain wheel? In case the

Part was externally procured, which supplier was

chosen to do so? In other words, information re-

garding the execution of each of the specific tasks

in the business process flow is mainly available

“at bulk” without any reference to the specifics

of each individual instance. This scenario corre-

sponds to an example of aggregation dimension 4

in De Bruyn et al. (2013). However, as this might

cause information loss regarding (arguably) rele-

vant information in the process, this scenario is

expected to create a certain degree of entropy due

to AiT and DiT violations.

4.3 Postprocessing

Some descriptive statistics of the generated data can

be found in Figure 2. Obviously,these data and gener-

ated sample distributions highly approximate the pop-

ulation distributions as set out in Section 4.1. How-

ever, while this might initially occur to the reader as

a circular reasoning, the whole point of our reasoning

is exactly the fact that the observer in a realistic case

is not aware of the actual population distributions and

should perform his analysis solely based on the infor-

mation registered during the execution of the business

process instantiations. This allows to mimic the situ-

ation in which, for instance, extreme cases (e.g., high

throughput or delivery time) or other problems (e.g.,

an unreliable supplier) are generated by the simula-

tion model and a business analyst is aiming to trace

(i.e., diagnose) the origin (i.e., microstate) of this ob-

served fact (i.e., the macrostate).

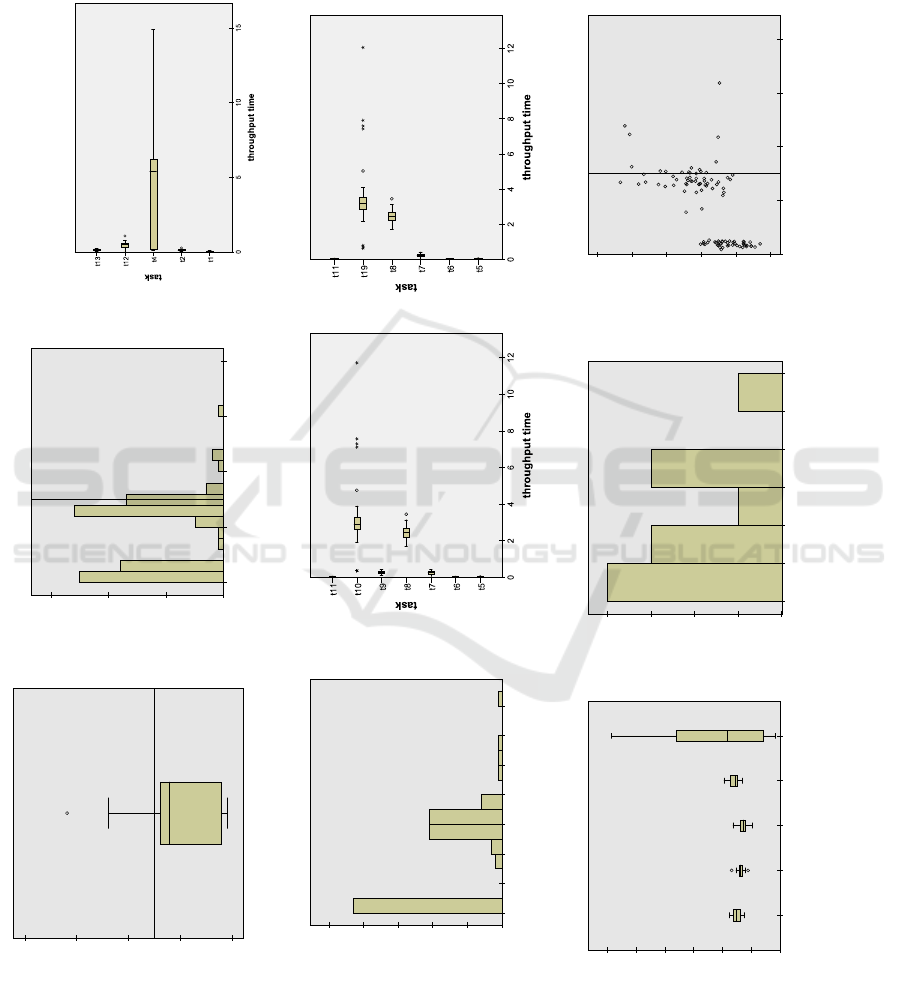

5 FINDINGS AND DISCUSSION

Let us assume that the manager of our simulated

bike selling company observes (macroscopically) that

too many deliveries of requested bike orders exceed

7.5 man days in order to be delivered. This can be

seen in Figure 2a en 2b, where a line is drawn at

this point. Indeed, the boxplot (a) is asymmetrical

and its upper whisker is rather long, indicating that

some outliers or extreme values are present. Also the

histogram (b) shows that at least 10 out of the 100

simulated bike order instantiations exceed this border

value. The manager considers this situation harmful,

as customers typically tend to file complaints starting

from this moment. Therefore, he wants to find out

what the cause of these extreme throughput values for

the

Order Handling Process

is. In Section 4.1, we

explained how we configured the parameters of our

simulation model in such way that the standard devi-

ation of the delivery time of supplier 5 is extremely

large, compared to the other four suppliers. In each

of the different case study scenarios, the process and

the possibility to fulfill the managers’ assignment to

locate this problem differ. We will consider each of

them consecutively.

5.1 Scenario 1: The Normalized Case

In scenario 1, all information depicted in Figure 2

(i.e., panels a till i) is (macroscopically) available for

the observer for solving his problem. Indeed, infor-

mation regarding all fine-grained tasks, as implied by

the application of the guidelines of Van Nuffel (2011),

and their instantiations is registered and available for

further inspection by the observer. First, panels a and

b indicate an asymmetric delivery time and a large

number of outliers or deliveries exceeding the desired

7.5 man days. For instance,

Order Handling

in-

stance 38 was indicated to have a delivery time of al-

most 15 man days.

In a next stage, the observer would logically opt

for splitting out the different tasks in the

Order

Handling Process

in order to dig down to the origin

of the observed problem. Here, panel c indicates that

task 4 —the “Part Process” (i.e., being the aggrega-

tion of the completion of the

Part Process

instances

needed to proceed with the “Assembly Process”

task)— not only represents the largest mean amount

of time for the whole

Order Handling Process

but

also, and probably more importantly, exhibits a very

large deviation. Indeed, the histogram of panel d

shows that a large amount of instances of task 4 has a

throughput time less than one man day (i.e., the cases

where all three parts are in stock). However, also a

relatively fair amount of instances require more than

6 man days to complete, implying a large chance that

the total delivery time will also exceed the target de-

livery time.

The next logical step would be to split up the

steps constituting the

Part Process

as is depicted in

panel e. One can see that primarily the tasks “Draft

Part Requirements” and “Receive Part” take some

time to be executed, but that the “Procure Part” task

has large deviations. Having identified the most fine-

grained task responsible for the extremely delayed

Order Handling Process

instances, a process de-

sign exhibiting (data) instance traceability would al-

low an even more detailed analysis showing the

throughput time for this task, categorized by the sup-

plier chosen when the a part is externally procured

Third International Symposium on Business Modeling and Software Design

192

38

total throughput time

20

15

10

5

0

order handling process

(a)

total throughput time

20151050

Frequency

30

20

10

0

(b) (c)

Part Process throughput time

14121086420

Frequency

50

40

30

20

10

0

(d) (e) (f)

supplier

54321

throughput time - receive part

12

10

8

6

4

2

0

(g)

supplier 5 - throughput time receive order

121086420

Frequency

4

3

2

1

0

(h)

total costs

1100

1000

900

800

700

600

total throughput time

20151050

(i)

Figure 2: Some descriptive statistics of the Custom Bikes case simulation.

A Case Study on Entropy Generation during Business Process Execution - A Monte Carlo Simulation of the Custom Bikes

Case

193

(i.e., panels g and h). It is only at this stage of the rea-

soning, that one is able to identify the root cause of the

problem introduced in our simulation model (i.e., the

unreliability of supplier 5 in terms of delivery time).

Consequently, both the observability and trace-

ability of the introduced problem are rather straight-

forward in this scenario. Indeed, in case supplier 5

would be removed from the part suppliers portfolio,

the extremely irregular delivery time would almost

completely disappear, solving the originally identified

problem. Hence, the multiplicity in this scenario is

1 (and entropy 0) as the macrostate (i.e., the identi-

fied problem of a set of extreme throughput times of

the

Order Handling

Process) can be unambiguously

related to one microstate (i.e., the configuration in

which one task and its instance data (such as supplier

chosen) can be attributed as causing the problematic

macrostate, the other tasks being normal). This can

be seen at two distinct levels: (1) at the type level

of processes and tasks (i.e., identifying the process

and task type responsible for the deviations in the ob-

served total throughput time) and (2) at the instance

level of processes and tasks (e.g., to trace the fact that

for

Order Handling

instance 38, 11.7 man days of

the total throughput time were spent while waiting

for the delivery of Part 3 for which supplier 5 was

chosen). Finally, from panel i, we can derive that fo-

cusing on the cost perspective would not have been

sufficient to correctly diagnose this delivery related

problem as many extreme deliveries have only low or

moderate registered costs (e.g., the costs for

Order

Handling

instance 38 only amounts to 747 e).

5.2 Scenario 2: Violation Regarding

SoS/SoC

Scenario 2 represents the scenario in which a viola-

tion towards the principles SoS and SoC is introduced

as information regarding two independent informa-

tion units are combined, i.e., the “Procurement Part”

and “Part Received” tasks. Consequently, the infor-

mation (macroscopically) available for the observer

is restricted to panels a, b, c, d, and f in Figure 2. The

problem analysis in this scenario will proceed analo-

gously to the procedure outlined for scenario 1, until

the point that the different constituting tasks of the

Part Process

are to be examined for their respec-

tive throughput times. However, at this stage, the ob-

server will not be able to differentiate between poten-

tial problems regarding the “Procure Part” task (e.g.,

do the people at the procurement department face dif-

ficulties for drafting and placing the orders, or do they

have a bottleneck making each procurement wait for

a certain amount of time before it can be placed?) or

“Part Received” task (e.g., are there any kind of prob-

lems related to the delivery itself?). That way, one

cannot be sure whether the problem is situated under

ones own responsibility (i.e., the procurement depart-

ment) or an external party (i.e., the supplier) and en-

tropy clearly increases. Indeed, while the observer

in this example is still able to be aware of a problem

regarding the overall throughput time of the

Order

Handling Process

(the macrostate), multiple (i.e.,

minimum 2) independent causes (i.e., tasks) can be

deemed to be at the origin of this phenomenon (i.e.,

both procurement or delivery). As a consequence, for

each

Part Process

instantiation, multiplicity equals

2, entropy rises and the traceability of the problem

decreases. Consequently, in a good business process

design, these information units should be separated

into distinct tasks to allow for the above mentioned

analyses. Interestingly, the “Actor Task Responsibil-

ity” guideline proposed by Van Nuffel (2011) would

already recommend this separation as the procuring

and the delivery of parts are carried out by different

actors, in this case even from different organizational

entities.

5.3 Scenario 3: Violation Regarding

DiT/AiT

Scenario 3 represents represents the scenario in which

a violation regarding the DiT and AiT principles is

introduced. Indeed, DiT requires that the relevant

data for executing a task is registered and related to

the relevant state, whereas AiT implies that the ex-

ecution of a task instance should be unambiguously

traceable to the business process it is embedded in.

This requirement is not met for the

Part Process

in this scenario. Consequently, in this scenario, the

information (macroscopically) available for the ob-

server is restricted to panels a, b, c, d, and e in Fig-

ure 2. The problem analysis in this scenario will

therefore proceed analogously to the procedure out-

lined for scenario 1, until the point that the “Receive

Part” task becomes identified as being responsible for

the extreme values regarding overall throughput times

of the

Order Handling Process

. However, at this

stage, the observer will not be able to differentiate

between possible problems related to the specifics of

the different suppliers. That way, the only conclu-

sion which can be drawn from this data is that some

problems regarding the delivery of parts are present.

Indeed, while the observer in this example is again

able to be aware of a problem regarding the overall

throughput time of the

Order Handling Process

(the macrostate), multiple (i.e., minimum 5) indepen-

dent causes (i.e., suppliers) can be deemed to be at the

Third International Symposium on Business Modeling and Software Design

194

origin of this phenomenon (i.e., is the problem sup-

plier specific and if so, which supplier?). As a conse-

quence, for each

Part Process

instantiation, multi-

plicity equals 5, entropy rises and the traceability of

the problem decreases. In a good business process

design, these information aspects (i.e., data) should

be traceable to their corresponding task instance ex-

ecutions to allow for the above mentioned analyses.

In fact, the “Aggregation Level” guideline proposed

by Van Nuffel (2011), would at least suggest to sepa-

rate the delivery of parts in a distinct business process

of which the instances are logically linked to their

“parent” business process instance. Additionally, we

would recommend to register for each task instantia-

tion the business process instance it belongs to as well

as the argument data it employed for triggering its ex-

ecution.

Finally, imagining the scenario in which “Part

Process” is only considered as one atomic tasks,

clearly constitutes an example of a violation of both

the SoS/SoC and DiT/AiT design principles, thereby

combining the difficulties of traceability discussed for

scenarios 2 and 3 and further increasing the degree

of entropy. Further, while in all three case scenarios,

the observability of a problematic situation was still

present, we showed in De Bruyn et al. (2013) that an

increase in entropy might also lead to a lower degree

of traceability. In our case example, this might be

showup in case we did not include one unreliable sup-

plier, but instead one supplier having a higher mean

delivery time compared to all other suppliers in the

supplier portfolio: this would lead to unnecessarily

high (mean) delivery times without the manager or

process owner being necessarily aware of it because

no “extreme” cases or outliers would be apparent and

no supplier-specific analysis could be done.

5.4 Reflections

At the end of Section 5.1, we already briefly men-

tioned that a focus on different perspectives when

collecting data from business processes is necessary.

Different stakeholders in an organization require dif-

ferent kinds of information which should all be con-

sidered when collecting data. For example, busi-

ness process throughput optimization, cost account-

ing (e.g., requiring part costs and activity drivers) and

manufacturing perspectives all require different data.

In our case example it was for instance shown that

problematic high throughput times of a process do

not necessarily imply high execution costs and vice

versa, as can be seen from Figure 2i. The combina-

tion of these different perspectives is not straightfor-

ward, and is not focused on in many research projects.

In dedicated research domains (such as operations re-

search or management accounting), a degree of spe-

cialist expertise is needed which does not necessar-

ily allow insight in other fields. While we do not

claim to have extensive expertise in these domains,

the focus on multiple different perspectives demon-

strates the emergence of issues which are specific to

the integration of different domains. Such integration

issues represent wicked problems. Even in research

domains which focus on integration, it is claimed that

only local optimizations are known, or that integration

is studied based on one dominant perspective (Ethiraj

and Levinthal, 2004).

Such integration problems can be explained

clearly based on our theoretical framework. Consider

the application of the first two principles presented in

Section 2. These principles require the identification

of the different concerns of a certain perspective, and

separating them by explicitly keeping states. How-

ever, the concerns which are identified will vary for

different perspectives. The design of a business pro-

cess which needs to be analyzed in a business pro-

cess optimization perspective will focus on concerns

which influence the throughput of the process. How-

ever, when these different tasks all have the same ac-

tivity driver for an Activity-Based Costing system,

their separation is not required based on the applica-

tion of the Separation of Concerns principles from a

cost accounting perspective. For example, similar to

the aggregations performed in case scenario 2, the se-

quence of tasks regarding the smaller administrative

tasks (e.g., tasks “Register Order” and “Evaluate Or-

der”) could be combined from a cost accounting per-

spective, because (a) they do not need to be booked

in separate accounts, since only the cost of a prod-

uct as a whole is relevant; (b) they are all performed

by the same type of resource (i.e., a human resource),

which indicates a similar activity driver; and (c) the

costs of these tasks equals “labor time” times “la-

bor cost per time unit”. From a process optimization

perspective, different arguments for separating these

tasks could be raised. For example, different employ-

ees can perform these tasks, which can cause differ-

ent throughput times. Moreover, from an organiza-

tional diagnostic perspective, these tasks should be

separated as well: this would allow an often-occurring

erroneous process outcome to be traced back to a sin-

gle task, or a single employee. For instance, in our

Custom Bikes case, managers would typically like to

be informed when the “Register Order” and “Evalu-

ate Order” tasks have significantly different through-

put and/or success rates. In contrast, concerns which

need to be separated from a cost accounting perspec-

tive (e.g., tasks with different activity drivers) may

A Case Study on Entropy Generation during Business Process Execution - A Monte Carlo Simulation of the Custom Bikes

Case

195

not be relevant to the business process optimization

perspective (e.g., when they do not add to through-

put time). Additionally, similar to the aggregations

performed in case scenario 3, a manufacturing or as-

sembly viewpoint might consider the data regarding

which supplier delivered a specific part as irrelevant

(assuming that each of the 5 considered suppliers in

our case deliver identical parts). However, we showed

in our discussion that such (data) instance traceabil-

ity can be relevant for other perspectives (such as

business process optimization in terms of throughput

time) as it was actually at the core of our simulated

problem: one of the considered suppliers turned out

to be rather unreliable in terms of its delivery time.

Therefore, the only way to gather data which pro-

vides sufficient insights for different perspectives si-

multaneously, is by separating the union of all con-

cerns of these perspectives. Based on these “atomic”

information units, different aggregations can be de-

rived to provide the required information of each per-

spective. Such detailed data could be useful even for

perspectives where certain concerns do not need to be

separated at this moment. Consider an organization

which needs to switch from a European way of re-

porting to an American one. Different accounts may

be necessary in that case. However, the atomic infor-

mation units can be re-aggregated in a different way

to comply with the new regulations. Moreover, in Eu-

rope many organizations perform two sets of book-

keeping: a national and a European one. Instead of

requiring (partly duplicate) data input in separate sys-

tems, such systems should be built to be able to handle

the aggregation of the same atomic information units.

Of course, the selection of such type of data requires

a highly structured approach aiming at gathering con-

sistent and fine-grained data. However, regarding this

granularity in for instance the cost accounting field,

it has been acknowledged that the “activities” iden-

tified in Activity-Based Costing (ABC) systems, are

to be understood as being “composed of the aggrega-

tion of units of work or tasks” (Drury, 2007, p. 342).

Therefore, the “activities” proposed can probably not

be considered as the “atomic” information units, cer-

tainly if one’s aim is to reuse these information units

for deriving insight from the different perspectives

mentioned above. Further, it has been reported that

the collection of fine-grained data for an Activity-

Based Costing system can become highly complex

(Kaplan and Anderson, 2004). However, consider

the structured way of designing software architec-

tures using Normalized Systems theory (Mannaert

and Verelst, 2009). Reusable building blocks for cer-

tain software functionality, called elements, describe

the modular structure of all concerns from different

relevant perspectives (such as remote access, security,

etcetera) which need to be handled for performing, for

example, a software action. This forces designers to

develop software based on such fine-grained modular

elements. The incorporation of a reporting concern

within these software elements (typically supporting

a set of business processes) could for example provide

possibilities to obtain the required fine-grained data in

organizations, as suggested in this paper. The design

of such elements on an organizational level itself has

been explored as well (De Bruyn, 2011; De Bruyn and

Mannaert, 2012). To obtain such elements, reusable

building blocks should be designed which perform a

generic organizational action and which handle rele-

vant cross-cutting concerns, such as logging relevant

data. In our example, the part reservation process

could be such a reusable element, which keeps data

concerning a.o. its throughput time, and the cost of

the reserved part.

6 CONCLUSIONS

In this paper, we aimed to provide evidence for en-

tropy generation during the execution of business pro-

cesses if NS theory principles are not adhered to, by

performing a Monte Carlo simulation of the Custom

Bikes case. Hence, this paper has several contribu-

tions. First, this paper validates in a more practi-

cal and empirical way conceptualizations proposed in

earlier work. Second, we extended this conceptualiza-

tion of entropy reasoning for business process model-

ing by releasing several simplifying assumptions (i.e.,

considering multiple (interacting) business processes

and allowing different mean (duration or cost) param-

eters for each task type). Third, we elaborated on

the need to split tasks and business processes up to

the level of so-called “atomic tasks”, which should be

able to be considered as atomic from several perspec-

tives simultaneously (e.g., cost accounting and oper-

ational business process optimization perspectives).

In future research, it might be interesting to propose

a set of more specific (business-oriented) guidelines

to delineate business processes and their constituting

tasks, as Van Nuffel (2011) did for the stability rea-

soning in NS, and contrast both approaches Clearly,

the aim of this paper was not at all to employ com-

plex or advanced statistical methods to perform data

mining on the information traces delivered by busi-

ness process execution. Instead, we consciously em-

ployed only the most basic statistical reasoning tech-

niques to show that the identification and registration

of the basic (“atomic”) data regarding business pro-

cess execution needs a sufficient amount of attention

Third International Symposium on Business Modeling and Software Design

196

from multiple perspectives, before entropy reduction

and relevant data analysis can occur.

ACKNOWLEDGEMENTS

P.D.B. is supported by a Research Grant of the

Agency for Innovation by Science and Technology in

Flanders (IWT).

REFERENCES

Boltzmann, L. (1995). Lectures on gas theory. Dover Pub-

lications.

De Bruyn, P. (2011). Towards designing enterprises for

evolvability based on fundamental engineering con-

cepts. In On the Move to Meaningful Internet Systems:

OTM 2011 Workshops, volume 7046 of Lecture Notes

in Computer Science, pages 11–20. Springer, Berlin,

Heidelberg.

De Bruyn, P., Huysmans, P., Mannaert, H., and Verelst, J.

(2013). Understanding entropy generation during the

execution of business process instantiations: An il-

lustration from cost accounting. In Advances in En-

terprise Engineering VII, Lecture Notes in Computer

Science. Springer Berlin Heidelberg. in press.

De Bruyn, P., Huysmans, P., Oorts, G., and Mannaert, H.

(2012). On the applicability of the notion of entropy

for business process analysis. In Shishkov, B., editor,

Proceedings of the second international symposium

on Business Modeling and Software Design, pages

128–137.

De Bruyn, P. and Mannaert, H. (2012). On the generaliza-

tion of normalized systems concepts to the analysis

and design of modules in systems and enterprise engi-

neering. International journal on advances in systems

and measurements, 5(3&4):216–232.

Drury, C. (2007). Management and Cost Accounting.

South-Western.

Ethiraj, S. K. and Levinthal, D. (2004). Bounded ratio-

nality and the search for organizational architecture:

An evolutionary perspective on the design of organi-

zations and their evolvability. Administrative Science

Quarterly, 49(3):404 – 437.

Hevner, A. R., March, S. T., Park, J., and Ram, S. (2004).

Design science in information systems research. MIS

Quarterly, 28(1):75–105.

Jacquemin, A. P. and Berry, C. H. (1979). Entropy measure

of diversification and corporate growth. The Journal

of Industrial Economics, 27(4):359–369.

Jung, J.-Y., Chin, C.-H., and Cardoso, J. (2011). An

entropy-based uncertainty measure of process models.

Information Processing Letters, 111(3):135–141.

Kaplan, R. S. and Anderson, S. R. (2004). Time-driven

activity-based costing. Harvard business review,

82(11):131–8.

Mannaert, H., De Bruyn, P., and Verelst, J. (2012). Ex-

ploring entropy in software systems: towards a precise

definition and design rules. In Proceedings of the Sev-

enth International Conference on Systems (ICONS)

2012, pages 93–99.

Mannaert, H. and Verelst, J. (2009). Normalized Systems—

Re-creating Information Technology Based on Laws

for Software Evolvability. Koppa.

Mannaert, H., Verelst, J., and Ven, K. (2011). The

transformation of requirements into software primi-

tives: Studying evolvability based on systems theo-

retic stability. Science of Computer Programming,

76(12):1210–1222.

Oorts, G., Huysmans, P., and De Bruyn, P. (2012). On ad-

vancing the field of organizational diagnosis based on

insights from entropy - motivating the need for con-

structional models. In Shishkov, B., editor, Proceed-

ings of the second international symposium on Busi-

ness Modeling and Software Design, pages 138–143.

Regev, G., Hayard, O., and Wegmann, A. (2012). Home-

ostasis - the forgotten enabler of business models. In

Shishkov, B., editor, Proceedings of the second inter-

national symposium on Business Modeling and Soft-

ware Design, pages 13–24.

Tumay, K. (1996). Business process simulation. In Charnes,

J., Morrice, D., Brunner, D., and Swain, J., editors,

Proceedings of the 1996 Winter Simulation Confer-

ence, pages 93–98. ACM Press.

Van Nuffel, D. (2011). Towards Designing Modular and

Evolvable Business Processes. PhD thesis, University

of Antwerp.

A Case Study on Entropy Generation during Business Process Execution - A Monte Carlo Simulation of the Custom Bikes

Case

197