Anomaly Detection in Real-Time Gross Settlement Systems

Ron Triepels

1,3

, Hennie Daniels

1,2

and Ronald Heijmans

3

1

Tilburg University, Tilburg, The Netherlands

2

Erasmus University, Rotterdam, The Netherlands

3

De Nederlandsche Bank, Amsterdam, The Netherlands

Keywords:

Anomaly Detection, Neural Network, Autoencoder, Real-Time Gross Settlement System.

Abstract:

We discuss how an autoencoder can detect system-level anomalies in a real-time gross settlement system by

reconstructing a set of liquidity vectors. A liquidity vector is an aggregated representation of the underlying

payment network of a settlement system for a particular time interval. Furthermore, we evaluate the perfor-

mance of two autoencoders on real-world payment data extracted from the TARGET2 settlement system. We

do this by generating different types of artificial bank runs in the data and determining how the autoencoders

respond. Our experimental results show that the autoencoders are able to detect unexpected changes in the

liquidity flows between banks.

1 INTRODUCTION

Financial market infrastructures play a vital role in the

smooth functioning of the economy. They facilitate

the clearing and settlement of monetary and other fi-

nancial transactions. A particular type of system in

these infrastructures is the Real-Time Gross Settle-

ment (RTGS) system. An RTGS system is a system

that settles transactions of its participants individually

(gross) and immediately (real-time).

It is important to supervise the activities of banks

in financial systems. This is because financial sys-

tems tend to exhibit a robust-yet-fragile nature (Gai

and Kapadia, 2010). Banks may be well capable of

absorbing financial imbalances. However, if they start

experiencing liquidity issues, than these issues can

quickly propagate to many other banks due to their in-

terconnectedness. For this reason, much research has

recently been devoted to study the topology of pay-

ment networks and its impact on systemic risk. Sys-

temic risk is the risk associated with any event that

threatens the stability of a financial system as a whole

(Berndsen et al., 2016). It is commonly measured by

concepts of network theory, e.g. the centrality or de-

gree of a payment network.

In this paper, we present a different approach to

measure systemic risk. We apply anomaly detection

on the payment data generated by a RTGS system.

Generally, an anomaly is defined as a pattern that does

not conform to expected behavior (Chandola et al.,

2009). Accordingly, anomaly detection is the task of

automatically identifying anomalies in data. In our

case, anomalies are particular configurations of a pay-

ment network that deviate considerably from the ex-

pected norm. They are caused by financial stress or

unwanted payment behavior.

The application of anomaly detection on payment

data is promising. Payment data provide an accu-

rate and system-wide overview of how banks man-

age their liquidity over time. Analyzing this data

with anomaly detection allows to automatically iden-

tify unusual payment behavior and may help super-

visors to initiate timely interventions. To the best of

our knowledge, this is the first time such analysis is

applied on payment data.

We define the anomaly detection task and discuss

how it can be performed by an autoencoder. An au-

toencoder is a feed-forward neural network that learns

features from data by compressing it to a lower di-

mensional space, and accordingly, reconstructing it

back in the original space. Furthermore, we evalu-

ate the performance of two types of autoencoders in a

series of bank run simulations. The simulations show

that the autoencoders are able to detect unexpected

changes in the liquidity flows between banks.

The remainder of this paper is organized as fol-

lows. Section 2 provides a brief overview of related

literature on payment systems and anomaly detection.

Section 3 defines the autoencoder and discusses how

it can be applied for anomaly detection. Section 4

Triepels, R., Daniels, H. and Heijmans, R.

Anomaly Detection in Real-Time Gross Settlement Systems.

DOI: 10.5220/0006333004330441

In Proceedings of the 19th International Conference on Enterprise Information Systems (ICEIS 2017) - Volume 1, pages 433-441

ISBN: 978-989-758-247-9

Copyright © 2017 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

433

describes the experimental setup of the bank run sim-

ulations. Section 5 discusses the results of the simu-

lations. Finally, section 6 concludes the paper.

2 RELATED LITERATURE

Many explanatory studies have been conducted on

payment data to study the properties and behavior

of banks in settlement systems. For example, algo-

rithms have been developed to detect loans in unse-

cured interbank markets (Furfine, 1999; Armantier

and Copeland, 2012; Arciero et al., 2016). Moreover,

network analysis has been applied to study the topol-

ogy of payment networks and its impact on financial

contagion and systemic risk (Allen and Gale, 2000;

Le

´

on and P

´

erez, 2014; Berndsen et al., 2016). The in-

sights gained from such studies are applied to develop

indicators of liquidity and systemic risk, see e.g. (Hei-

jmans and Heuver, 2014).

Simulations are also commonly applied to study

settlement systems. A well-known simulation envi-

ronment is the Bank of Finland simulator. It imple-

ments many types of settlement systems and allows

to resettle payment data under different conditions

(Leinonen and Soram

¨

aki, 2005). This is usually done

to measure the impact on a settlement system when

characteristics of liquidity flows, such as their value

or timing, are changed (Laine et al., 2013).

Anomaly detection, in particular, has been suc-

cessfully applied on other types of financial data such

as stock market data. The goal of stock fraud de-

tection is to detect trades that violate securities laws.

This includes the detection of unprofitable trades by

brokers (Ferdousi and Maeda, 2006) and abnormal

stock price changes caused by stock price manipula-

tion (Kim and Sohn, 2012). Stock market data has

also been combined with options data and news data

to detect trades that were made based on information

that was not available to the general public (Donoho,

2004). Multiple techniques were applied to detect

these ’insider’ transactions, including decision trees

and neural networks.

Another related application is credit card fraud de-

tection. In this case, anomaly detection is applied on

credit card transactions to detect suspicious spend-

ing patterns. Many techniques have been proposed

for this task including: neural networks (Ghosh and

Reilly, 1994; Maes et al., 2002), Bayesian networks

(Maes et al., 2002), self-organizing-maps (Zaslavsky

and Strizhak, 2006; Quah and Sriganesh, 2008), as-

sociation rules (S

´

anchez et al., 2009), and hidden

Markov models (Srivastava et al., 2008).

3 ANOMALY DETECTION IN

RTGS SYSTEMS

In this section, we define the problem of detecting

anomalies in RTGS systems based on lossy compres-

sion. Moreover, we describe how an autoencoder can

be employed for this task.

3.1 Definitions

Let B = {b

1

,...,b

n

} be a set of n banks participat-

ing in a RTGS system. The banks initiate payments

to each other which are settled by the settlement sys-

tem in real-time and without any netting procedures.

Furthermore, let T =< t

1

,...,t

m

> be an ordered set

of m time intervals, where t

1

= [τ

0

,τ

1

), t

2

= [τ

1

,τ

2

),

and so on. We assume that the time intervals in T are

consecutive and of equal duration. They might, for

example, denote the operating hours or minutes of the

settlement system.

The liquidity that banks transmit to each other

though the settlement system over time is recorded.

Let D = {A

(1)

,...,A

(m)

} be a set of m matrices where

each A

(k)

∈ D is the n by n matrix:

A

(k)

=

a

(k)

11

··· a

(k)

1n

.

.

.

.

.

.

.

.

.

a

(k)

n1

··· a

(k)

nn

(1)

Each element a

(k)

i j

∈ [0,∞) denotes the total amount

of liquidity that b

i

sends to b

j

in time interval t

k

. No-

tice that this also includes a

(k)

ii

. This liquidity flow

denotes the total liquidity transmitted by b

i

at time in-

terval t

k

between its own accounts. We also call A

(k)

a liquidity matrix. It can be interpreted as a payment

network consisting of banks (nodes) which are inter-

connected by liquidity flows (edges). The elements of

A

(k)

define the weights associated with the edges of

the payment network at time interval t

k

. For analysis

purposes, we derive from A

(k)

the vectorized repre-

sentation:

a

(k)

= [a

(k)

11

,...,a

(k)

n1

,...,a

(k)

1n

,...,a

(k)

nn

]

T

(2)

where, a

(k)

is a n

2

column vector consisting of all

columns of A

(k)

vertically enumerated. We also call

a

(k)

a liquidity vector.

3.2 Anomaly Detection Task

Anomalies in RTGS systems can be detected by de-

termining how well liquidity vectors can be recon-

structed after being compressed by lossy compres-

ICEIS 2017 - 19th International Conference on Enterprise Information Systems

434

sion. Lossy compression is a particular form of com-

pression in which data may not be entirely recovered.

Instead, only the essential features of data are com-

pressed. This makes lossy compression useful to de-

tect anomalous liquidity vectors. If the reconstruction

error of a liquidity vector is low, then it fits some fre-

quently recurring pattern that the compression model

has learned to compress well. However, if the recon-

struction error is large, then the model does not rec-

ognize the liquidity flows and fails to reconstruct their

values. One may conclude from this observation that

the liquidity vector is generated by a different under-

lying process, and thus, is an anomaly.

Let M be a lossy compression model. We measure

the reconstruction error of a

(k)

after it is compressed

and reconstructed by M by function RE:

RE : D → [0, ∞) (3)

RE(a

(k)

) is the non-negative reconstruction error ag-

gregated over all liquidity flows between the banks at

time interval t

k

. a

(k)

is considered anomalous if the

reconstruction error is high, i.e. RE(a

(k)

) ≥ ε where

ε > 0 is a threshold. The objective of our anomaly de-

tection task is to find all liquidity vectors in D whose

reconstruction error is higher than ε. We define this

task as:

Definition 1 (Anomaly Detection Task). Given a set

of liquidity vectors D, a lossy compression model M

θ

with parameters θ, and threshold ε, find the anomaly

set F = {a

(k)

∈ D|RE(a

(k)

) ≥ ε}.

3.3 Autoencoder

We employ a three-layer autoencoder (Rumelhart

et al., 1985; Hawkins et al., 2002) for M to compress

liquidity vectors. An autoencoder is an artificial feed-

forward neural network that is trained to reconstruct

the input layer at the output layer. It does this by pro-

cessing the input through a bottleneck layer in which

a set of neurons form a representation of the input in

a lower dimensional space. The architecture of the

autoencoder is depicted by Figure 1.

For input a

(k)

, the autoencoder estimates a recon-

struction

ˆ

a

(k)

of a

(k)

via a hidden layer consisting of l

neurons. The reconstruction mapping is composed of

two functions φ and ψ:

φ : R

n

2

→ R

l

(4)

ψ : R

l

→ R

n

2

(5)

Here, φ is also called the encoder function and ψ the

decoder function. First, a

(k)

is encoded by φ in l-

dimensional space by processing it through the hid-

den layer:

ˆa

(k)

1

.

.

.

ˆa

(k)

n

2

h

(k)

1

.

.

.

h

(k)

l

b

2

a

(k)

1

.

.

.

a

(k)

n

2

b

1

W

1

W

2

φ(a

(k)

) ψ(φ(a

(k)

))

Figure 1: The architecture of an autoencoder consisting of

an: input layer (left), hidden layer (middle), and output

layer (right).

φ(a

k

) = f

(l)

(W

1

a

(k)

+ b

1

) (6)

where, W

1

is a l by n

2

matrix of weights, b

1

is a

vector of l bias terms, and f

(l)

(y) = [ f (y

1

),..., f (y

l

)]

is a set of activation functions that are applied to y

element-wise. Potential functions for f are the linear

(identity) function or sigmoid function. The result of

the encoding φ(a

(k)

) = [h

1

,...,h

l

] is a vector of l hid-

den neuron activations forming a (compressed) repre-

sentation of a

(k)

in R

l

. Then, φ(a

(k)

) is decoded back

by ψ in n

2

-dimensional space by processing it through

the output layer:

ψ(φ(a

(k)

)) = g

(n

2

)

(W

2

φ(a

(k)

) + b

2

) (7)

where, W

2

is a n

2

by l matrix of weights, b

2

is a vec-

tor of n

2

bias terms, and g

(n

2

)

(y) is a set of activation

functions. The result of the decoding ψ(φ(a

(k)

)) =

[ ˆa

(k)

1

,..., ˆa

(k)

n

2

] is a vector of n

2

outputs forming a re-

construction of φ(a

(k)

) in R

n

2

.

The goal of the autoencoder is to learn a map-

ping from the input layer to the output layer such

that a

(k)

≈ ψ(φ(a

(k)

)) for all a

(k)

∈ D. The quality

of the reconstruction depends on the number of neu-

rons in the hidden layer. If the number of neurons is

too large, then the autoencoder may approximate the

identity mapping and simply copy inputs from the in-

put layer to the output layer. However, if the number

of neurons is limited, than the autoencoder is forced to

compress the liquidity vectors and approximate their

intrinsic structure.

Several variations have been proposed to prevent

autoencoders from approximating the identity map-

Anomaly Detection in Real-Time Gross Settlement Systems

435

ping. These include: sparse autoencoders (Ng, 2011),

denoising autoencoders (Vincent et al., 2008), and

contractive autoencoders (Rifai et al., 2011). How-

ever, as a first attempt, we only consider the classic

implementation of an autoencoder in this paper.

3.4 Reconstruction Error

The autoencoder estimates the reconstruction error

at different aggregation levels. For an individual

liquidity flow a

(k)

i j

, the reconstruction error is esti-

mated by taking the squared difference between its

reconstructed transaction value and original transac-

tion value:

RE(a

(k)

i j

) =

1

2

(ψ(φ(a

(k)

))

i+n( j−1)

− a

(k)

i j

)

2

(8)

Similarly, the reconstruction error of all liquidity

flows combined at time interval t

k

can be estimated

by taking the squared `

2

-norm of the difference be-

tween the reconstructed liquidity vector and original

liquidity vector:

RE(a

(k)

) =

1

2

||ψ(φ(a

(k)

)) − a

(k)

||

2

(9)

Finally, by taking the mean of the reconstruction er-

ror of all liquidity vectors in D we obtain the overall

Mean Reconstruction Error (MRE):

MRE(D) =

1

m

m

∑

k=1

RE(a

(k)

) (10)

3.5 Model Learning

The parameters θ = {W

1

,W

2

,b

1

,b

2

} of the autoen-

coder are estimated from historic liquidity flows. We

do this by minimizing the MRE, i.e.:

θ = argmin

W

1

,W

2

,b

1

,b

2

MRE(D) (11)

There are many approaches to solve the optimiza-

tion problem in 11. One approach is to apply

(stochastic) gradient descent in conjunction with

back-propagation to efficiently calculate all gradients

during the optimization process (Werbos, 1982; Bot-

tou, 2004). In this case, the parameters are iteratively

updated proportional to the negative gradient of the

MRE. This process is repeated until the parameters

converge to a configuration for which the MRE is (lo-

cally) minimum.

4 EXPERIMENTAL SETUP

In this section, we describe an experiment in which

two autoencoders were evaluated on real-world pay-

ment data. We elaborate on the characteristics of

the payment data, the implementation of the autoen-

coders, and the way they were evaluated in a series of

bank run simulations.

4.1 Payment Data

A sample of payment data was extracted from the

TARGET2 settlement system. TARGET2 is the

RTGS system of the Eurosystem. It facilitates the set-

tlement of large domestic and cross-border payments

in euros for most European countries.

The sample focused on the Dutch part of the

settlement system. It included about two million

client payments which were settled between January

and October 2014 among the twenty largest banks

1

.

These are payments that were initiated in TARGET2

by the banks on behave of their customers. The ac-

counts of the Dutch Ministry of Finance and De Ned-

erlandsche Bank were excluded from the sample.

We aggregated the payments over 8,561 time in-

tervals that each spanned fifteen minutes and derived

the corresponding liquidity vectors. The liquidity

flows in these vectors were transformed by a log trans-

formation to make their highly skewed distribution

less skewed. Min-max normalization was in turn per-

formed to normalize their values to the [0,1] interval.

Accordingly, we partitioned the liquidity vectors

in separate sets for training and evaluation purposes.

The parameters of the autoencoders were learned

from a training set. This set contained 5081 liquid-

ity vectors corresponding to six months (March until

August). A holdout set containing 1680 liquidity vec-

tors corresponding to the first two months (January

and February) was set aside to optimize the number

of neurons of the autoencoders. Finally, we evalu-

ated the autoencoders on a test set which contained

1800 liquidity vectors corresponding to the final two

months (September and October).

4.2 Implementation

We implemented two autoencoders: one having linear

activations in the hidden layer and sigmoid activations

in the output layer, and the other, having sigmoid ac-

tivations for both the hidden layer and output layer.

We refer to these networks as the linear autoencoder

1

The size of the banks were determined based on their

total turnover.

ICEIS 2017 - 19th International Conference on Enterprise Information Systems

436

and sigmoid autoencoder respectively. The initial pa-

rameters of the networks were sampled from a normal

distribution with zero mean and a variance of 0.1 for

symmetry breaking. Stochastic gradient descent (Bot-

tou, 2004) in conjunction with back-propagation was

in turn applied to learn the parameters from the train-

ing set. This was performed for 30 iterations through

the training set with a fixed learning rate.

The number of hidden neurons was optimized

by a grid-search. During the grid search, a set of

autoencoders having a different number of neurons

l ∈ {10, 20, . . . , 400} in the hidden layer were learned

from the training set. The MRE of these networks

were evaluated on the holdout set. In particular, we

investigated the point were adding more neurons did

not yielded a better error.

Moreover, we determined whether the autoen-

coders approximated the identity mapping by evaluat-

ing their MRE on a set of uniformly sampled liquid-

ity vectors. In the optimal case, the MRE of the au-

toencoders on these random liquidity vectors equals

a lower bound. Let X = {x

(1)

,...,x

(m)

} be a set of

m liquidity vectors for n banks. Each x

(k)

∼ U(0,1)

is sampled from a uniform distribution. An autoen-

coder achieves the lowest error when it reconstructs

the mean

ˆ

x

(k)

= [

1

2

,...,

1

2

] for all x

(k)

∈ X. The corre-

sponding lower bound of the MRE is:

MRE

l

=

1

2

E(

1

m

m

∑

k=1

||c − x

(k)

||

2

) (12)

=

1

2

Z

1

0

1

m

m

∑

k=1

||c − x

(k)

||

2

dx

(k)

(13)

=

1

24

n

2

(14)

where, c = [

1

2

,...,

1

2

]

T

is a column vector of n

2

ele-

ments. In the case an autoencoder achieves an error

MRE(X) < MRE

l

, it is modeling noise because X is

random. This is only possible if it is approximating

the identity mapping.

4.3 Bank Run Simulation

We evaluated the performance of the autoencoder in

a series of simulations. In particularly, we evaluated

how well they were able to detect different types of

artificial bank runs.

We simulated a bank run as follows. First, choose

a bank b

i

as the subject bank. Then, add additional

liquidity to the outgoing liquidity flows from b

i

to the

remaining banks according:

a

(k)

i j

:= a

(k)

i j

+ P(k) ·C(k) (15)

where, P(x) ∈ {0, 1} denotes whether liquidity is

added at time interval t

x

and C(x) ∈ [0, ∞) denotes the

Table 1: The parameters of the simulated bank runs.

Bank Run d r p

s

p

e

λ

s

λ

e

A 196 2 0 0.8 10

−4

10

−7

B 196 6 0 0.8 10

−4

10

−7

C 392 2 0 0.8 10

−4

10

−7

D 392 6 0 0.8 10

−4

10

−7

amount of additional liquidity. We sampled P(x) ran-

domly from a binomial distribution with probability

p

x

. This probability increased exponentially during

the bank run:

p

x

=

(

p

s

+ (p

e

− p

s

)(

x−s

d

)

r

, if s ≤ x ≤ s + d

0, otherwise

(16)

Here, s is the time interval t

s

at which the bank run

starts, d is the duration of the bank run, r controls the

rate of increase, and p

s

and p

e

are start and end val-

ues of p

x

respectively. Moreover, we sampled C(x)

from an exponential distribution with rate parameter

λ

x

. This parameter also increased exponentially dur-

ing the bank run:

λ

x

=

(

λ

s

+ (λ

e

− λ

s

)(

x−s

d

)

r

, if s ≤ x ≤ s + d

0, otherwise

(17)

Here, λ

s

and λ

e

are the rate parameters at the start and

end of the bank run respectively.

Table 1 summarizes the parameters of the simu-

lated bank runs. We chose a large commercial bank

as the subject bank. All bank runs started at the end

of the test set and lasted d = 196 or d = 392 time in-

tervals. This corresponds to seven and fourteen oper-

ational days respectively. Furthermore, we applied a

rate parameter of r = 2 to mimic a bank run which de-

veloped slowly over time and r = 6 to mimic a bank

run which developed more radically over time. The

probability that liquidity was added during the bank

runs increased from p

s

= 0 to p

e

= 0.8.

The liquidity rate parameters were adjusted to the

magnitude of the liquidity flows of the subject bank.

It increased from λ

s

= 10

−4

to λ

e

= 10

−7

in all sim-

ulations. This means that at the start of the bank run

on average 10,000 euro was added to the outflow of

the subject bank which increased to 10,000,000 euro

in the final time interval.

5 RESULTS

Figure 2a shows the MRE of the holdout set esti-

mated by the autoencoders while having a different

number of neurons in the hidden layer. Initially, the

Anomaly Detection in Real-Time Gross Settlement Systems

437

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

10 60 110 160 210 260 310 360 400

Neurons

MRE (Holdout Set)

Linear

Sigmoid

(a)

15

20

25

30

35

40

45

50

55

10 60 110 160 210 260 310 360 400

Neurons

MRE (Random Set)

Linear

Sigmoid

(b)

Figure 2: (a) The MRE of the holdout set estimated by the linear and sigmoid autoencoder having a different number of

neurons in the hidden layer. (b) The same graph as (a) but instead estimated on a set of random liquidity vectors. The dotted

line represents the lower bound of the MRE.

Linear

Sigmoid

0.2

0.4

0.6

0.8

6770 7070 7370 7670 7970 8270 8560 6770 7070 7370 7670 7970 8270 8560

Time Interval

Reconstruction Error

Figure 3: The reconstruction error of the original test set estimated by the linear and sigmoid autoencoder for each time

interval. The error curves are smoothed with a rolling average of ten time intervals to make their trend more clearly visible.

MRE quickly decreased when increasing the number

of neurons. Then, after about 160 neurons, it sat-

urated. Figure 2b shows the same graph estimated

on the random set. The linear autoencoder recon-

structed the random set better than the sigmoid au-

toencoder. After 160 neurons, it achieved an optimal

reconstruction as its MRE closely approximated the

lower bound. It even crossed the lower bound several

times which suggests that, in these particular cases, it

was approximating the identity mapping. Given these

results, we chose to use 160 neurons in the hidden

layer of the autoencoders.

Moreover, the results show that liquidity vectors

contain distinctive payment patterns which an autoen-

coders is able to pick up very well. If we compare the

MRE of the holdout set and the random set, then we

see that the autoencoders achieve a much lower error

on the holdout set. This would not be possible if the

ICEIS 2017 - 19th International Conference on Enterprise Information Systems

438

Bank Run A

Bank Run B

Bank Run C

Bank Run D

0.2

0.4

0.6

0.8

1.0

1.2

0.2

0.4

0.6

0.8

1.0

1.2

6770 7070 7370 7670 7970 8270 8560 6770 7070 7370 7670 7970 8270 8560

Time Interval

Reconstruction Error

Figure 4: The reconstruction error of the manipulated test sets estimated by the linear autoencoder for each time interval. We

simulated the bank runs at the final time intervals. The error curves are smoothed with a rolling average of ten time intervals

to make their trend more clearly visible. Moreover, the dotted line represents the anomaly threshold ε = 0.5.

holdout set was also randomly generated.

Before running the actual simulations, we deter-

mined how well the autoencoders were able to recon-

struct the original test set. Figure 3 shows the recon-

struction error estimated by the autoencoders for each

time interval. The error curves of the autoencoders

are quite similar and exhibit fluctuations. Moreover,

they display a short period of time, around time inter-

val 7670, were both autoencoders had difficulties re-

constructing the liquidity vectors. Closer inspection

revealed that these high errors were caused by a few

very large liquidity flows. No clear signs of stress

could be identified. Instead, we suspect that the large

errors were caused by random influences that are sub-

ject to the financial intermediation process.

We simulated the bank runs at the end of the test

set. Figure 4 shows the reconstruction error of the

manipulated test sets estimated by the linear autoen-

coder for each time interval

2

. The error curves were

smoothed by a rolling average of ten time intervals to

make their trend clearly visible. In addition, we ap-

plied an anomaly threshold of ε = 0.5.

The error curves clearly highlight the artificial

bank runs at the final time intervals. During these time

intervals, the reconstruction error increased rapidly as

the payment network started to change unexpectedly.

In particular, the stressed bank became more centrally

positioned having high outgoing liquidity flows to the

remaining banks in the payment network. We can see

2

The error curves of the sigmoid autoencoder are very

similar and omitted for brevity.

this when inspecting the reconstruction error of the

final liquidity matrices, see Figure 5. The high out-

going liquidity flows of the stressed bank could not

be accurately reconstructed and caused a high recon-

struction error during the bank runs.

6 CONCLUSIONS

We have introduced a method to detect system-level

anomalies in a RTGS system. This method involves

training an autoencoder to reconstruct a set of liquid-

ity vectors. Our experimental results show that liquid-

ity vectors contain distinctive features of a payment

network which an autoencoder is able to capture very

well. Furthermore, the reconstruction error made by

a well-trained autoencoder after compressing and re-

constructing the liquidity vectors reflects anomalous

changes in the liquidity flows between banks.

In the future, we plan to further improve our work

in several aspects. This includes: evaluating the pro-

posed method on larger payment networks that are

subject to real-world stress, explaining the most likely

cause of anomalies, and incorporating time dependen-

cies between liquidity vectors.

ACKNOWLEDGEMENTS

We would like to thank Ron Berndsen for his helpful

suggestions and feedback.

Anomaly Detection in Real-Time Gross Settlement Systems

439

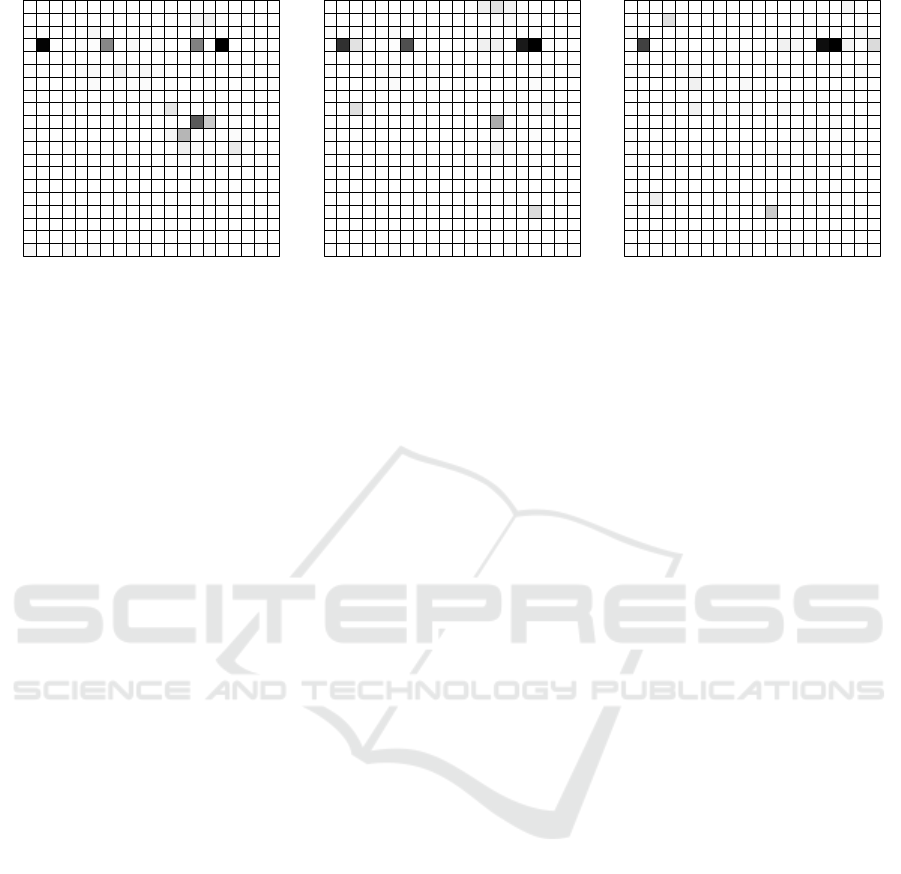

(a) (b) (c)

Figure 5: The reconstruction error of the liquidity matrices at (a) t

8528

, (b) t

8529

, and (c) t

8530

of bank run C estimated by the

linear autoencoder. The intensity of each element indicates the error made by the autoencoder for the corresponding liquidity

flow. The fourth row from the top represents the outgoing liquidity flows of the stressed bank.

REFERENCES

Allen, F. and Gale, D. (2000). Financial Contagion. Journal

of Political Economy, 108:1–33.

Arciero, L., Heijmans, R., Heuver, R., Massarenti, M., Pi-

cillo, C., and Vacirca, F. (2016). How to Measure the

Unsecured Money Market? The Eurosystem’s Imple-

mentation and Validation using TARGET2 Data. In-

ternational Journal of Central Banking, March:247–

280.

Armantier, O. and Copeland, A. (2012). Assessing the

Quality of Furfine-based Algorithms. Federal Reserve

Bank of New York Staff Report, 575.

Berndsen, R. J., Le

´

on, C., and Renneboog, L. (2016). Fi-

nancial Stability in Networks of Financial Institutions

and Market Infrastructures. Journal of Financial Sta-

bility.

Bottou, L. (2004). Stochastic Learning. In Advanced lec-

tures on machine learning, pages 146–168. Springer.

Chandola, V., Banerjee, A., and Kumar, V. (2009).

Anomaly Detection: A Survey. ACM Comput. Surv.,

41(3):15:1–15:58.

Donoho, S. (2004). Early Detection of Insider Trading in

Option Markets. In Proceedings of the tenth ACM

SIGKDD international conference on Knowledge dis-

covery and data mining, pages 420–429. ACM.

Ferdousi, Z. and Maeda, A. (2006). Unsupervised Out-

lier Detection in Time Series Data. In 22nd Inter-

national Conference on Data Engineering Workshops

(ICDEW’06), pages 51–56. IEEE.

Furfine, C. (1999). The Microstructure of the Federal Funds

Market. Financial Markets, Institutions and Instru-

ments, 8:24–44.

Gai, P. and Kapadia, S. (2010). Contagion in financial net-

works. In Proceedings of the Royal Society of London

A: Mathematical, Physical and Engineering Sciences,

page rspa20090410. The Royal Society.

Ghosh, S. and Reilly, D. L. (1994). Credit card fraud de-

tection with a neural-network. In System Sciences,

1994. Proceedings of the Twenty-Seventh Hawaii In-

ternational Conference on, volume 3, pages 621–630.

IEEE.

Hawkins, S., He, H., Williams, G., and Baxter, R. (2002).

Outlier Detection Using Replicator Neural Networks.

In International Conference on Data Warehousing

and Knowledge Discovery, pages 170–180. Springer.

Heijmans, R. and Heuver, R. (2014). Is this Bank Ill? The

Diagnosis of Doctor TARGET2. Journal of Financial

Market Infrastructures, 2(3).

Kim, Y. and Sohn, S. Y. (2012). Stock fraud detection us-

ing peer group analysis. Expert Systems with Applica-

tions, 39(10):8986–8992.

Laine, T., K., K., and & Hellqvist, M. (2013). Simulations

Approaches to Risk, Efficiency, and Liquidity Usage in

Payment Systems. IGI Global.

Leinonen, H. and Soram

¨

aki, K. (2005). Optimising Liq-

uidity Usage and Settlement Speed in Payment Sys-

tems. In Leinonen, H., editor, Liquidity, risks and

speed in payment and settlement systems - a simula-

tion approach., Proceedings from the Bank of Fin-

land Payment and Settlement System Seminars 2005,

pages 115–148.

Le

´

on, C. and P

´

erez, J. (2014). Assessing financial mar-

ket infrastructures’ systemic importance with author-

ity and hub centrality. Journal of Financial Markt In-

frastructures.

Maes, S., Tuyls, K., Vanschoenwinkel, B., and Mander-

ick, B. (2002). Credit Card Fraud Detection Using

Bayesian and Neural Networks. In Proceedings of the

1st international naiso congress on neuro fuzzy tech-

nologies, pages 261–270.

Ng, A. (2011). Sparse autoencoder. CS294A Lecture notes,

72:1–19.

Quah, J. T. and Sriganesh, M. (2008). Real-time credit card

fraud detection using computational intelligence. Ex-

pert systems with applications, 35(4):1721–1732.

Rifai, S., Vincent, P., Muller, X., Glorot, X., and Bengio, Y.

(2011). Contractive Auto-Encoders: Explicit Invari-

ance During Feature Extraction. In Proceedings of

ICEIS 2017 - 19th International Conference on Enterprise Information Systems

440

the 28th international conference on machine learn-

ing (ICML-11), pages 833–840.

Rumelhart, D. E., Hinton, G. E., and Williams, R. J. (1985).

Learning Internal Representations by Error Propaga-

tion. Technical report, DTIC Document.

S

´

anchez, D., Vila, M., Cerda, L., and Serrano, J.-M. (2009).

Association rules applied to credit card fraud detec-

tion. Expert Systems with Applications, 36(2):3630–

3640.

Srivastava, A., Kundu, A., Sural, S., and Majumdar, A.

(2008). Credit Card Fraud Detection Using Hidden

Markov Model. IEEE Transactions on dependable

and secure computing, 5(1):37–48.

Vincent, P., Larochelle, H., Bengio, Y., and Manzagol, P.-A.

(2008). Extracting and Composing Robust Features

with Denoising Autoencoders. In Proceedings of the

25th international conference on Machine learning,

pages 1096–1103. ACM.

Werbos, P. J. (1982). Applications of Advances in Non-

linear Sensitivity Analysis. In System modeling and

optimization, pages 762–770. Springer.

Zaslavsky, V. and Strizhak, A. (2006). Credit Card Fraud

Detection Using Self-Organizing Maps. Information

and Security, 18:48.

Anomaly Detection in Real-Time Gross Settlement Systems

441