Internalization of Values Academic Integrity and Its Effect on

Performance of Financial Management at Universitas Tanjungpura

Pontianak Indonesia

Witarsa Witarsa

Universitas Tanjungpura, Pontianak, Indonesia

witnessed@yahoo.com

Keywords: Internalization, Academic Integrity Value, Performance.

Abstract: The Research Problems came from Universitas Tanjungpura, Pontianak Indonesia because in 2016 managing

funds amounting to 100 billion Rupiah and managed by 9 faculties, agencies and unit. Management of these

funds need to be escorted to the values of academic integrity. The purpose of the study (1) to determine the

process of internalizing the values of academic integrated, (2) to determine the effect of partial and

simultaneous honesty, fairness, trust, respect, and commitment on the performance of financial management

staff. The method used is survey method with explanation approach. The research sample as many as 30

people. The results showed (1) the process of internalizing the values of academic integrity conducted by

three processes, namely the transformation, transaction, internalization, (2) there is a partial effect and

simultaneous values of academic integrity which includes honesty, fairness, trust, respect, and commitment

on the performance of financial management staff.

1 INTRODUCTION

The value of academic integrity in the context of life

developing in someone's personality. Personal values

evolve from a State to the outside world and can

change from time to time. Integrity in the application

of the values it refers to continuity; people have

integrity if they apply their values appropriately

regardless of arguments or negative reinforcement

from others. Values are applied appropriately when

they are applied in the right area. For example, it

would be appropriate to apply religious values in

times of happiness as well as at the moment of

despair. Similarly, the value of academic integrity is

practiced in most educational institutions, known in

the mission statement and represented in the code of

honor.

Factors integrity of the academic community is

determined by the performance of employees in

charge of implementing academic service. Bruce et

al. (2012) which conducts research on Academic

Integrity: a review of the literature, Studies in Higher

Education, shows that of the Review 115 articles and

reality that occurs in universities in Hong Kong that

values academic integrity is very important in

improving academic services.

Ishak et al. (2016) conducted a study on The

Effect of Job Satisfaction, Integrity and Motivation

on Performance. Research results indicate that among

job satisfaction, integrity and motivation, integrity is

a variable turns the dominant influence on the

performance of 78.10%. While the influence of job

satisfaction and motivation by 18.90% amounting to

14.90% of the performance.

Baharom (2014) conducted a study on The Role

of Integrity as Mediator between Satisfaction Work

and Work Performance in the Perspective of Islam:

An Empirical Approach using SEM / Amos Model.

The results showed that the Mediator Integrity

Influence on work satisfaction in the perspective of

Islam Spiritual, Intellectual, Social, Materials, and

Work Performance.

Pay attention to the results of the study, the value

of the value of academic integrity is very important to

note because the effect on the performance of

employees. The value of academic integrity value

attached to the personality of employees who daily

carry out services at Universitas Tanjungpura that

drive performance improvements.

The Center for Academic Integrity (CAI) (2006)

defines academic integrity as a commitment, even in

the face of adversity, to five fundamental values:

Witarsa, W.

Internalization of Values Academic Integrity and Its Effect on Performance of Financial Management at Universitas Tanjungpura Pontianak Indonesia.

In Proceedings of the 2nd International Conference on Sociology Education (ICSE 2017) - Volume 2, pages 207-211

ISBN: 978-989-758-316-2

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

207

honesty, trust, fairness, respect, and responsibility.

From these values flow principles of behavior that

enable academic communities to translate ideals into

action.

Academic integrity is the commitment to five

fundamental values: honesty, trust, fairness, respect

and responsibility. This view of integrity as a

"clustering of values beyond honesty" (Davis and

Bertram, 2009), involves much more than a

commitment from students not to cheat. The Center

for Academic Integrity (CAI) (2006) makes explicit

that academic integrity is multi-dimensional and is

enabled by all those in the educational enterprise,

from students to parents, instructors and

administrators.

Institutional Framework for Promoting Academic

Integrity among Students (2015) state that: Academic

integrity is important because, without its core values,

true academic discourse becomes impossible,

learning is distorted and the evaluation of student

progress and academic quality is seriously

compromised. Consequently, the University is

committed to: (1) defending the academic credibility

and reputation of the University; (2) protecting

student achievement standards and the standards of its

awards; (3) ensuring that students receive due credit

for the work they submit for assessment; (4) making

reasonable adjustments to assessment that maintain

the integrity of the University’s courses and awards;

(5) protecting the interests of those students who do

not cheat; (6) advising its students of the need for

academic integrity, and providing them with guidance

on best practice in studying and learning; and (7)

educating students about what is intellectual property,

why it matters, how to protect their own, and how to

legitimately access other people's work. (Institutional

Framework for Promoting Academic Integrity among

Students, 2015).

The International Center for Academic Integrity

states that there are core values of integrity includes:

(1) honesty, (2) trust, (3) fairness, (4) respect, (5)

responsibility. Academic Integrity Guidelines (2006)

Academic Integrity is a mode of conduct based on an

individual and institutional commitment to the

principles of honesty, trust, fairness, respect, and

responsibility, to be Terrenes through (1) Honest and

ethical conduct in all activities Relating to the life of

the College, (2) Truthful, complete, and accurate

representation of all personal and academic

information, (3) Integrity of products of the academic

process, such as tests, essays, research papers,

laboratory reports, and any other class of course-

related preparations produced by individuals or

explicitly specified as group assignments, (4)

Universal application of the principles of the

Academic Integrity throughout the institution [4].

Gary (1997), Director of Judicial Programs and

Student Ethical Development, University of

Maryland stated that "Promoting student moral

development requires affirming shared values. More

colleges are starting to focus on one value that goes

to the heart of the academic enterprise: a commitment

to honesty in the pursuit of truth."

Academic Integrity relates to new management

techniques included in financial management. Ian

(2005) states The liberal, collegial values of the

Dearing Committee, listed above, contrast with the

expectations of New Managerialism. Pollitt (1990)

argues that the new managerialism can be seen as a

generic package of management techniques the which

include: (1) Strict devolved financial management

and budgetary controls. (2) Efficient use of resources

with an emphasis on productivity. (3) Extensive use

of quantitative performance indicators. (4) The

development of consumerism and the discipline of the

market. (5) The manifestation of consumer charters as

mechanisms of accountability. (6) The creation of a

disciplined, flexible workforce, using flexible /

Individualized contracts, staff appraisal systems and

performance related pay. (7) The assertion of

managerial control and managers' right to manage

(Ian, 2005). Referring to the expert opinion of the

above, the core values of integrity includes: (1)

honesty, (2) trust, (3) fairness, (4) respect, (5)

Commitment. The core values of integrity are very

important in maintaining the performance of the

individual so that the resulting performance as the

embodiment of earnest sincerity to implement quality

of service.

Bernardin and Russel provide an understanding of

the performance as follows: "performance is defined

as the record of the outcomes produced on a specified

job function or activity during time period. Bernadin

(1997) suggests performance is the systematic

description of the job relevant strength and

weaknesses of an individual and organization. The

performance is "A way of measuring the contribution

of individuals to Reviews their organization".

According to J. Campbell (1990) written by Jex

(2002): Performance should be distinguished from

effectiveness, productivity, and utility. Effectiveness

is defined as the evaluation of the results of an

employee's job performance. This is an important

distinction Because employee effectiveness is

determined by more than just job performance. For

example, an employee who is engaging in many

forms of productive behavior may still receive a poor

performance rating (a measure of effectiveness)

ICSE 2017 - 2nd International Conference on Sociology Education

208

because of performance rating errors, or simply

Because he or she is not well liked by the person

assigned to do the rating. Productivity is closely

related to both performance and effectiveness, but it

is different Because productivity takes into account

the cost of Achieving a given level of performance or

effectiveness.

From the opinion of experts, it can be concluded

that the performance is a performance of the functions

of the job or the activities of a particular person in

carrying out the duties charged to him based upon

know-how, experience and commitment within a

certain period.

2 RESEARCH METHODS

The method used is survey method with approach

explanatory research that explain the causal

relationship associative between Honesty (X1), Trust

(X2), Fairness (X3), Respect (X4), and commitment

(X5) with Employee Performance Financial (Y),

good quality of causality partially or simultaneously

through hypothesis testing. The study population was

an employee of the financial management and Acting

Commitment (KDP) in the university environment

Tanjungpura totaling 30 people. Because of the

relatively small population, then the population is

decided taken all as a sample. Tests using the research

instrument validity and reliability. test results of

research instrument of the subject supposed to know

about the variables studied showed that the variables

of honesty (X1), variable trusts (X2), variable fairness

(X3), variable respect (X4), variable commitment

(X5) and variable performance financial officer (Y)

indicates that the value of the validity of each

variable> 0.30, and the value of reliability Cronbach's

Alpha or Ri> 0.60. Data analysis technique used is the

technique of multiple linear regression analysis.

3 RESEARCH RESULTS

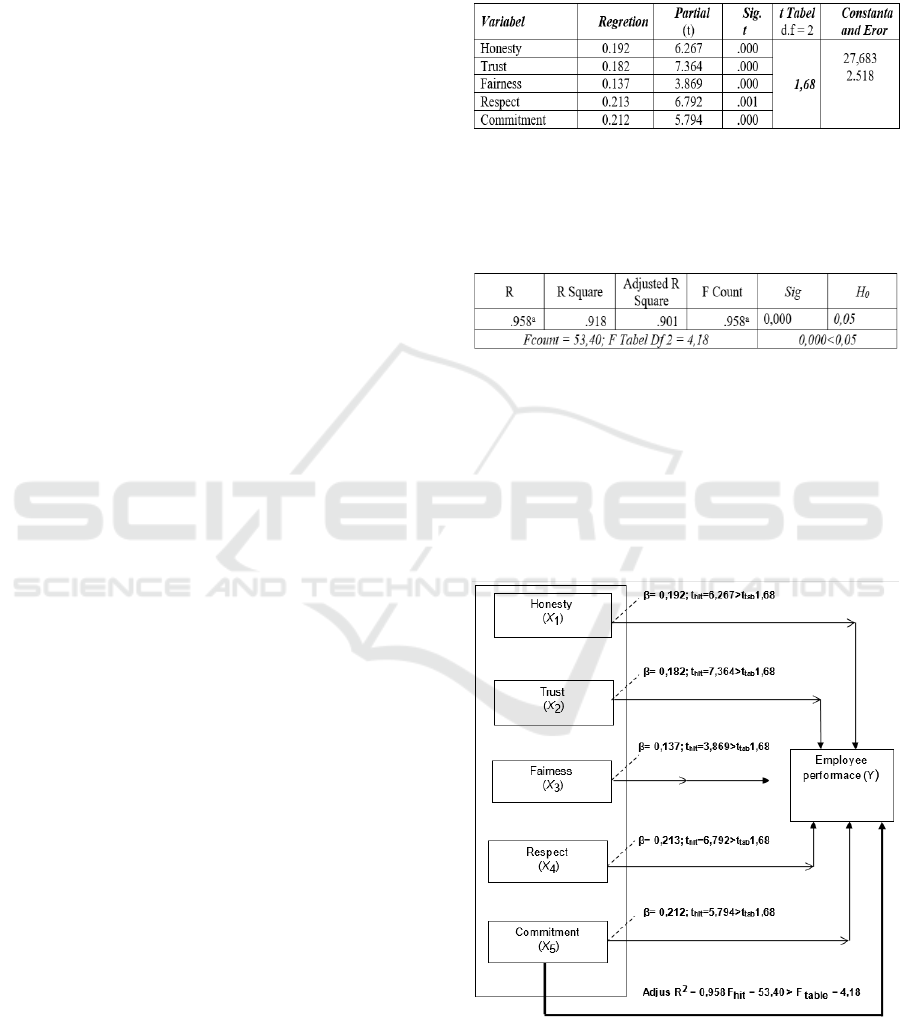

Analysis of the influence of partial as in table 1, it can

be seen that there is a partial influence of variable

Independent variable i.e. honesty (X 1), variable trust

(X 2), fairness (x 2) variables, variable respect (X 2),

variable commitment (X 2), against Financial

Manager officer performance variable (Y), can be

seen in the following table 1:

Table 1: Influence of Partial variables of honesty (X 1),

variable trust (X 2), fairness (x 2) variables, variable respect

(X 2), variable commitment (X 2), partially against the

employee who manages the financial performance of the

variable (Y).

Table 2. The simultaneous influence of Independent

variable that is honesty (X 1), variable trust (X 2), fairness

(x 2) variables, variable respect (X 2), variable commitment

(X 2), partially against the employee who manages the

financial performance of the variable (Y).

The results of adjusted R-Square acquired for

0.901. This shows that simultaneously there is a

strong influence of the variable honesty (X 1),

variable trust (X 2), fairness (X 3) variables, variable

respect (X 4), variable commitment (X 5), against

financial manager officer performance variables (Y)

of 90.10 percent While the rest of 9.90 percent

affected by other variables which are not examined in

this study.

Figure 1: The influence of Simultaneous and partial of

Honesty Variables (X 1), variable Trust (X 2), Fairness (X

3) Variables, variable Respect (X 4), variable Commitment

(X 5), against Financial Manager Officer Performance

Variables (Y).

Internalization of Values Academic Integrity and Its Effect on Performance of Financial Management at Universitas Tanjungpura Pontianak

Indonesia

209

4 DISCUSSION

The Effect of honesty variable (X1), significantly

affect the financial manager of employee

performance variable (Y). Empirical results find that

honesty in a positive effect on employee performance

variable financial manager. The results of this study

are supported by Frederick, et al., (2008). There are

two reasons why we undertake a further investigation

into the effects of honesty on budgeting. First,

previous studies such as Evans et al. (2001) and

Hannan et al. (2006) have difficulty isolating the

effects of honesty Because The reporting behavior of

the subordinate directly Affects the distribution of

wealth between the superior and subordinate.

Therefore, deviations from self-interested behavior

can be Attributed either to honesty or to other no

pecuniary motivations such as preferences for the

distribution of wealth. Evans et al. (2001) recognizes

the importance of the subordinate's concerns for the

distribution of wealth between the superior and

subordinate and note the need for further research to

refine our understanding of the factors that influence

the extent of honesty. We address this issue by

manipulating the subordinates' mode of budget

communication, including one treatment where a

factual assertion is required and another treatment

where no factual assertion is required. While other-

regarding preferences may operate and in both cases,

only in the former case should be relevant honesty

Because only in that case is it possible to make-an

UNTRUE representation. By exploring both forms of

communication, we are Able to estimate the

incremental effect of honesty (Frederick et al., 2008).

The Effect of trust variables (X2), significantly

affect the financial manager of employee

performance variable (Y). Empirical results find that

trust has positive influence on employee performance

variable financial manager. This was confirmed by

Amena and Shahid (2013) which states "Trust must

be treated as precious, highly Admired, and a

cherished organizational trait. Trust is an extremely

substantial commodity to any affiliation. A point that

needs to be promoted, is that trust is a dainty property

of human relationships, in that is powered by conduct

far more than by words, it may take time to constitute,

but is can be Abolished very quickly intervening.

Integrity is imperative to personal success and for

expanding leadership skills. Individuals that have

integrity build trust in their relations with others;

Become precious and they are respected as friends,

colleagues, mentors, and supervisors. They are

respected and counted on to do what is right. They are

Able to balance dignity and accountability, and they

are Able to Reviews their share values with others

(Amena and Shahid, 2013). Charles (2014) states The

research highlights five fundamental skills and

qualities that leaders need in order to be trusted.

The Effect of fairness variable (X3), significantly

affect the financial manager of employee

performance variable (Y). The results of the empirical

finding that fairness has positive influence on

employee performance variable financial manager.

The results of this study are supported by Sara et al.

(2012) which states; We have taken two variables in

our research Initially. The independent variable is

"fairness" the which leads towards "organizational

performance". By "fairness" we will be measuring

fairness in the working environment, sustainable

amount of work load for the employees, fairness in

providing them with required facilities to work

comfortably and fairness in appraisal system. After

carrying out a thorough literature review we have

found that "fairness" encompasses such virtues as

moral rightness, equity, honesty, and impartiality.

Fairness, or justice, is one of the most fundamental

concerns in society (Sara et al., 2012).

Influence respect variable (X4), significantly

affect the financial manager of employee

performance variable (Y). The results of the empirical

finding that respect positive influence on employee

performance variable financial manager. Respect is a

form of self-efficacy. Jacob and Jolly (2013), Success

in a realm is closely linked to self-efficacy in the

realm (Bandura, 1997). Higher self-efficacy in a

realm is associated with good outcomes, ranging from

greater job satisfaction and performance (Judge and

Bono, 2001), to better physical and mental health

(Bandura, 1997), to better academic performance

(Bandura, 1997; Robbins et al., 2004). For example,

students with higher academic self-efficacy show

better academic performance (Robbins et al., 2004).

Priming a high self-efficacy component of a self-

schema for a realm Might result in outcomes similar

to Reviews those found for individuals who have

characteristically high self-efficacy in a realm.

Related to this notion, previous research in other areas

indicates that manipulating individuals' perceptions

with respect to motivation will have an impact on

their performance (DeDonno and Demaree in Jacob

and Jolly, 2013).

The Effect of commitment variable (X5),

significantly affect the financial manager of

employee performance variable (Y) The results

empirically found that the commitment has positive

influence on employee performance variable

financial manager. This result is supported by the

opinions Luthans et al. (2007) which states, others

ICSE 2017 - 2nd International Conference on Sociology Education

210

where there are moderating effects between

organizational commitment and performance. A

study by the Association of Professors of Pakistan

Institute of Business Administration, University of

the Punjab by Mubbsher and Mubbsher (2012) who

studied The Impact of Employees Commitment On

Employee Satisfaction Role of Employee

Performance as a Moderating Variable. Research

results show that there is a difference between job

satisfaction among employees who have high

performance with employees who are not high

performance. Commitment direct influence on

employee performance.

5 CONCLUSIONS

The process of internalizing the values of academic

integrity are: honesty, fairness, trust, respect, and

commitment on employee financial manager at the

Universitas Tanjungpura Pontianak conducted by

three stages: (1) the process of transformation as a

process undertaken to inform good value and the bad.

(2) Transaction Process in this process the value of

academic integration is done through two-way

communication so that automatically there is a

process of interaction between researchers and

employees. (3) internalization process. At this stage

of internalization is not only carried out with verbal

communication but also the mental attitude and

personality. So at this stage personality who played

an active role communication.

There are partial and simultaneous influence of

variable independent variable variables i.e. honesty,

trust, fairness, respect variables variables, variable

commitment to financial manager officer

performance variables.

REFERENCES

Amena, S., Shahid, M. A., 2013. Integrity & Trust: The

Defining Principles of Great Workplaces. Journal of

Management Research. ISSN 1941-899X 2013, Vol. 5,

No. 4, pp 64-75.

Academic Integrity Guidelines, (2006) Chattanooga State

intra web. 25 Apr.

Baharom, 2014. The Role Integrity as Mediator between

Work Sutisfaction and Work Performance in the

Perspective of Islam: An Empirical Approach Usin

SEM/Amos Model International Journal of Research in

Applied. Natural and Social Sciences. 2321-8851;

ISSN(P): 2347-4580 Vol. 2, Issue 1, Jan 2014, 71-84.

Bernadin, H. J., Russel, E. A., 1997. (Human Resources

Management, An Experiential Approach, Mc Graw Hill

International Editions, Mac Graw Hill Book Co.

Singapore 1997) h, 379.

Bruce, M., Jingjing, Z., Annie, P., 2012. Academic

integrity: a review of the literature, Studies in Higher

Education, University of Hong Kong Libraries On: 02

August.

Charles, E., 2014. The truth about trust: Honesty and

integrity at work. The Institute of Leadership and

Management. London. pp 1-16.

Frederick, W. R., Steven, T. S., Richard, A. Y., 2008. The

Effect of Honesty and Superior Authority on Budget

Proposals. American Accounting Association. The

Accounting Review. Vol. 83, No. 4. 2008 pp. 1083–

1099.

Ian, M., 2005. Values, Principles and Integrity: Academic

and Professional Standards in Higher Education.

Higher Education and Management, University of

Greenwich. London, United Kingdom.

Institutional Framework for Promoting Academic Integrity

among Students, 2015. Document URL, Griffit

Universty.

Ishak, A., La, O. B. A., Sri, W. M., 2016. The Effect of Job

Satisfaction, Integrity and Motivation on Performance.

The International Journal of Engineering and Science.

Volume 5 Issue 1 PP -47-52.

Jacob, C., Jolly, J., 2013. Impact of Self Efficacy on

Motivation and Performance of Employees.

International Journal of Business and Management.

Vol. 8, No. 14; 2013, pp 80-88.

Jex, S. M., 2002. Organizational psychology: a scientist-

practitioner approach, John Wiley & Son. Canada.

Luthans, F., Youssef, C. M., Avolio, B. J., 2007.

Psychological capital: Developing the human capital

edge, Oxford University Press. New York.

Mubbsher, M. K., Zia-ur-Rehman, Muhamma, W. A.,

2012. The Impact of Employess Commitment On

Employee Satisfaction Role of Employee Performance

as a Moderating Variable. Singaporean Journal of

Business Ecnomics, and Management Studies. Vol 1,

No 2, 2012. hh. 1-13.

Sara, A., Rabiya, A., Mushtaq, A. B., 2012. The impact of

fairness in Working Condition on Organizational

Performance in Pakistas Telecommunication

Company, Limited, Islamabad. International Journal of

Economics and Management Sciences Vol. 2, No. 4,

2012, pp. 10-19.

Steven, L. M., Mary, A. V. G., 2009. Organizational

Behavior, Irwin McGraw-Hill. New York.

Internalization of Values Academic Integrity and Its Effect on Performance of Financial Management at Universitas Tanjungpura Pontianak

Indonesia

211