Management Commitment and Competencies of Asset

Administrators on Asset Management: A study in Government Units

of South Sumatera Province

Kartika Rachma Sari

1

, Didik Susetyo

2

, Inten Meutia

3

and Sa’adah Siddik

4

1

Department of Accounting, Sriwijaya State Polytechnic, Palembang , Indonesia

2

Department of Economic, Sriwijaya University, Palembang , Indonesia

3

Department of Accounting, Sriwijaya University, Palembang , Indonesia

2

Department of Accounting, Muhammaddiyah University, Palembang , Indonesia

Keywords: Management Commitment, Competencies of Asset Administrator, Asset Management.

Abstract: This study aims to analyze the influence of asset administrator competencies and management commitment

on asset management. The research was conducted on 50 Government Units in 4 city governments of South

Sumatera Province in 2017. The research data is primary data collected through a questionnaire. The

analytical tool is Partial Least Square (PLS); the determination of the sample is the head asset administrator

at each of the Government Units. The results of this research show that: (1) Management commitment has a

positive effect on asset management at Government Units in the city governments of South Sumatera

Province, (2) Competencies of asset administrators have positive effects on asset management at

Government Units in the city governments of South Sumatera Province. The implications of this study are

expected to contribute to help the heads of Government Units in South Sumatera Province to improve the

performance of asset management by performing a skilled asset administrator and management commitment

with the best of the assets.

1 INTRODUCTION

There are still many Local Government Financial

Reports (LCFR) which produce unqualified audit

opinions. There are only 252 (46.75%) of 539 LCFR

in 2016 (BPK, 2016). Asset still has the highest

percentage (30%) of the problems in the accounts on

the balance sheet that were presented not in

accordance with government accounting standards in

2015 (BPK, 2016). Many audit findings were found

which involved inequality in the management of

regional property and inadequate administration of

regional property.

Local governments must handle and utilize

public assets efficiently and effectively to optimize

the sources of regional revenues, including the

optimization and utilization of existing assets, as

referred to in law number 23 of 2014 concerning

regional governance. Public asset management must

be managed in order to cause these assets to be

developed as initial capital for local government to

strengthen their financial capabilities. To achieve

optimal benefits from an asset, good management of

the asset’s lifecycle is needed. Asset management is

a way of managing, planning, designing, and

monitoring the process of updating, acquiring,

maintaining, and disposal of all forms of technical

assets and infrastructure to support procurement of

public services. Management assets are a structured

and systematic process which cover the entire life of

a physical asset (AAMCoG, 2012)

The Indonesian Government has issued the

Regulation of Minister of Home Affairs Number 19

of 2016 concerning Technical Management of

Regional Assets which is used as a reference in

managing the assets. Local Governments should be

able to manage assets well, starting from needs

planning, budgeting, procurement, use, utilization,

Rachma Sari, K., Susetyo, D., Meutia, I. and Siddik, S.

Management Commitment and Competencies of Asset Administrator on Asset Management: Study in Government Units of South Sumatera Province.

DOI: 10.5220/0008444006850692

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 685-692

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

685

administration, maintenance and security to their

supervision so that regional assets can provide

benefits and optimal contribution to the relevant

regional government.

Mardiasmo (2004) states that the strategic

objectives which must be achieved in the

management of assets include: (1) the creation of an

administrative order regarding regional wealth, (2)

the creation of efficiency and effectiveness in the

use of regional/local assets; (3) the safeguarding of

regional assets; (4) availability of accurate data/

information regarding the amount of regional

wealth. The Department of Communities and Local

Government (2007) states that effective asset

management directly links with the efficiency

strategy and national improvement. It means that

better asset management improves better public

services and value for money.

These statements are in line with the research

conducted by (Bond, S & Dent, 1998) the

importance of efficient asset management for

financial reporting and asset management will

enhance the role in meeting community services

efficiently, which is reflected in the assessment and

reporting. Related studies which support the

importance of asset management are (Pekei &

Hadiwidjojo, 2014); (Shepherd, 2013); (Krisindarto,

2012); (White, 2012); (Jolicoeur & Barrett, 2005).

Performance within the organization is carried

out by all human resources within the organization,

by both leaders and employees. This is in line with

the research by (Cooper, 2006) who defined that

management commitment is to maintain and engage

in behaviours to help others achieve a goal.

(Simamora & Halim, 2013) stated that management

commitment is more critical in affecting asset

management. Top management must focus on its

employees with empowerment, involvement,

training, and appreciation to provide the best service

to beneficiaries. Employees will be given more

resources for training to improve asset management

skills when management is committed to improve

asset management. Chin et al. (2003) found that top

management commitment is the most important

factor for the successful implementation of ISO

9000. In line with this research, (Pheng & Teo,

2004) argued that top management commitment is

one of the elements reflecting TQM performance

measures. The commitment of top management

shown by the level of visibility and support in

implementing a total quality environment is very

important for the success of TQM implementation.

(Haupt & Whiteman, 2004); (Taylor & Wright,

2003); (Moorman, Niehoff, & Organ, 1993) argued

that commitment management has the potential to

influence organizational performance.

(Pate, Martin, & Robertson, 2003) stated that

competence provides a useful development

framework for those employees participating in a

program. He argued that competence can be seen

from two aspects. The first, competence, is a set of

specific attributes used in carrying out a job related

to the characteristics of high-performing employees

which can be learned through education, experience

or vocational training. This competence deals with

the behavior of particular individuals and how they

act in an organizational environment. The second,

competency, consists of a person's experience and

personality combined with job related factors that

stem from formal and informal organization. It

focuses on the interaction between the individual

and the job.

Yusuf (2013) suggested that knowledge about

asset management is needed for administrators in

utilizing assets to make asset management decisions

which benefit government operations. The

importance of an employee’s competence in an

organization is being able to support the

improvement of employee performance and

contribute to determining the future of the

organization (Wahyudi, 2014). In line with this,

(Qiao & Wang, 2009) suggested the critical

competencies for the success of middle managers in

China are team-building, communication,

coordination, execution and continual learning.

Some researchers have claimed that employees’

competencies provide an effective method for

predicting job performance (McClelland, 1973);

(Levenson, Van der Stede, & Cohen, 2006); (Darno,

2012).

Administrators of assets at the Regional

Government Organization are employees who work

in government agencies in Law Number 5 of 2014.

This concerns the State Civil Apparatus referred to

as the State Civil Apparatus that acts as a planner,

implementer, and supervisor of the implementation

of the general tasks of national governance and

development through the implementation of policies

and professional public services, free from political

intervention, and free from corruption, collusion and

nepotism.

In order to produce even high-quality asset

management, there is a need for reliable

management personnel. The audit board of the

Republic of Indonesia (BPK RI, 2016) found that the

problems in asset management occur partly because

the responsible officials/implementers are negligent

and not optimal in carrying out their duties and

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

686

responsibilities according to their respective duties

and responsibilities, have not fully understood the

applicable provisions, and are weak in supervising

and controlling activities. Based on the background

above, it is interesting to test the influence of

management commitment and competencies of asset

administrators on asset management in Government

Units of South Sumatra Province.

2 METHOD

This research is quantitative research and was

conducted at 50 Government Units in the city

governments of South Sumatra Province which

consist of 4 city Governments, they are Palembang,

Pagar Alam, Prabumulih and Lubuk Linggau. The

population used in the study is the official

administration of local assets that have the authority

and play an active role in the management of assets

at Government Units in the city government of

South Sumatra Province. The sampling technique to

find the Government Units used in this research is

random sampling.

By using Stewardship Theory (Donaldson &

Davis, 1991), Asset Management as dependent

variable in this study is a way of managing,

planning, designing, and monitor the process of

acquiring, maintaining, updating, and disposal of all

forms of infrastructure and technical assets; to

support procurement of public services (AAMCoG,

2012). In this study, the writers evaluate the

performance of asset management’s procedure in

accordance with the Government’s Regulations.

The independent variables are management

commitment and competencies of asset

administrators. Management commitment in this

study carries a strong belief and support from

management to carry out and implement asset

management policies in accordance with established

regulations so that the objective of implementing

these policies can be achieved for the benefit of the

organization (Cooper, 2006); (Tan, C. and Hamzah,

2008); (Caroline, Harriet, & Anne, 2016). We used

the dimensions studied by (Tan, C. and Hamzah,

2008) which are quality goals, priority, efforts,

involvement, resource allocation and attitude to

change. The competencies of asset administrators

are the technical ability in asset management

through the dimension of knowledge, skill and work

attitude. (Boyatzis, 2008); (Qiao & Wang, 2009);

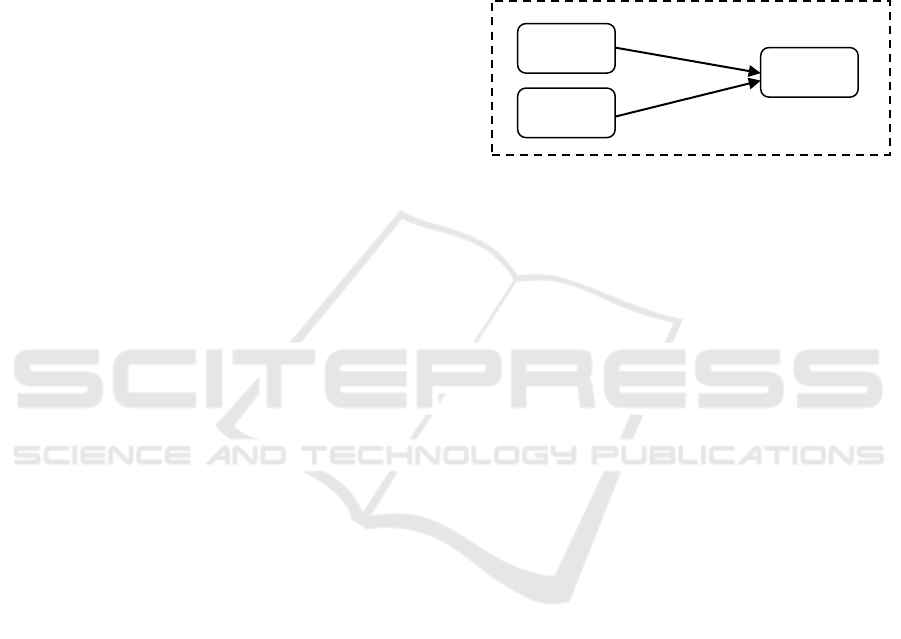

(Yusuf, 2013). The Conceptual Research framework

image is seen in figure 1.

The required research data are primary data

collected through questionnaires by providing a

written set of questions. The analytical tool used is

Partial Least Square with the aim to determine the

effect of the relationship between latent variables. In

this study the writers want to know the influence of

Management Commitment and the competencies of

asset administrators on asset management in

Government Units of South Sumatra Province.

Figure 1: Conceptual Research Framework.

3 RESULT AND DISCUSSION

The full model of SEM equation using the Smart

PLS 3.0 program is obtained by two models, namely

the standardized model (PLS Algorithm) and the t-

values model (Bootstrapping), each model is shown

in the following figure.

There are two steps in the measurement model.

They are the convergence validity and discriminant

validity. factor loading, and average variance

extracted (AVE) which were computed to get

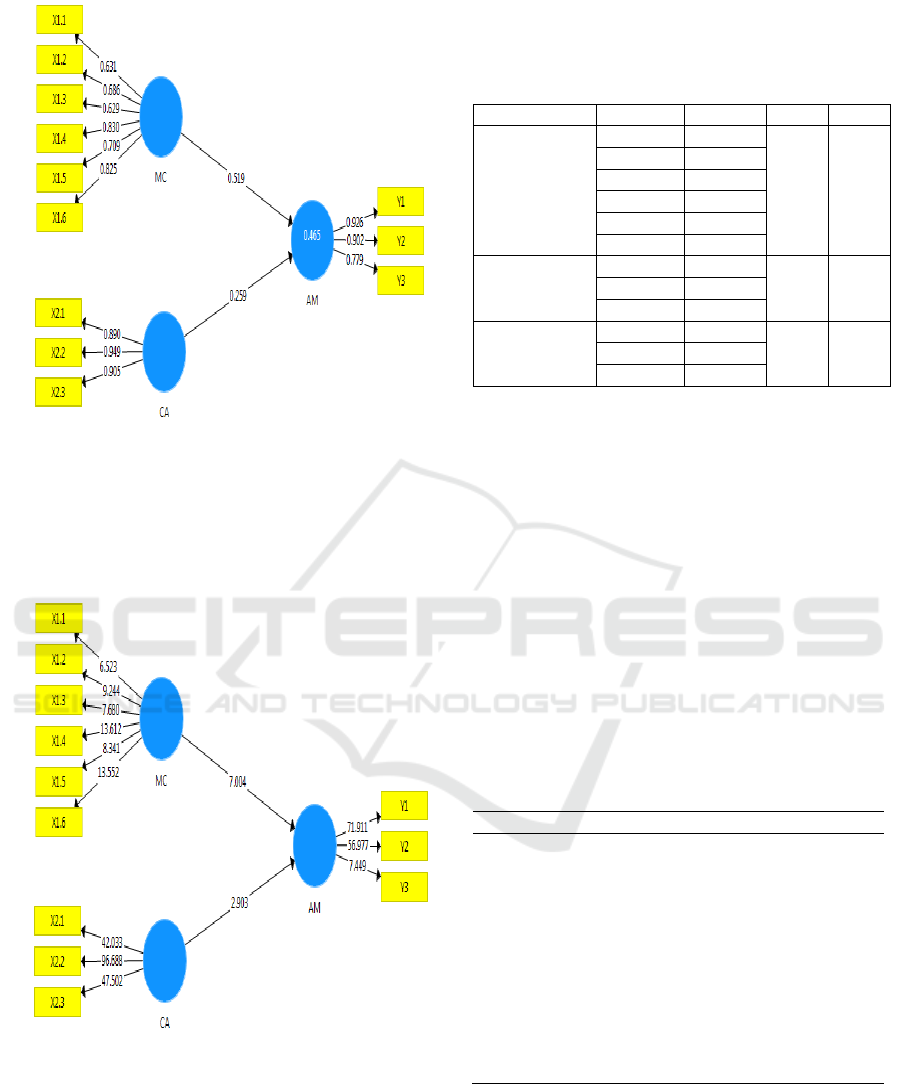

convergence validity. Based on Figure 2 the range of

loading factor (0,629 to 0,949) is more than 0,6 (≥

0,6). All latent constructs demonstrate adequate

convergence validity.

MC

CA

AM

Management Commitment and Competencies of Asset Administrator on Asset Management: Study in Government Units of South Sumatera

Province

687

Figure 2: Algorithm Model

Figure 3: Bootstrapping Model shows that the

value of t-statistic for the correlation among

indicators are considered valid where t-statistic > t-

table (1.96). All latent constructs demonstrate

adequate convergence validity.

Figure 3: Bootstrapping Model

From Table 1, AVE values in range from 0,522

to 0,838, meanwhile the CR value for the latent

variable (0,866 to 0,939) was above Hair et al (2010)

threshold value of 0,7, suggesting significant

homogeneity. It means that the indicators are

considered valid. The loading factor is a correlation

between indicators and their construct. The higher

the correlation, the better the level of validity is.

Table 1: Convergence Validity

Indicator

Loading

CR

AVE

Management

Commitment

X1.1

0,631

0,866

0,522

X1.2

0,686

X1.3

0,629

X1.4

0,830

X1.5

0,709

X1.6

0,825

Competencies

Asset

Administrator

X2.1

0,890

0,939

0,838

X2.2

0,949

X2.3

0,905

Asset

Management

Y1

0,926

0,904

0,759

Y2

0,902

Y3

0,779

Discriminant validity is used to prove that latent

constructs predict the size of the construct is better

than the size of the other constructs. Discriminant

validity was tested by analyzing the cross-loading

value for each variable in which the construct being

measured is greater than the other constructs.

Discriminant validity can be seen through the value

of cross-loading, as seen in Table 2. Table 2 shows

that the indicator of each variable has resulted in

discriminant validity. This can be seen from the

value of the management commitment (MC)

competencies of asset administrator (CA) and asset

management (AM) that have cross load values

greater than other cross loading values, it means that

all variables have met the discriminant validity.

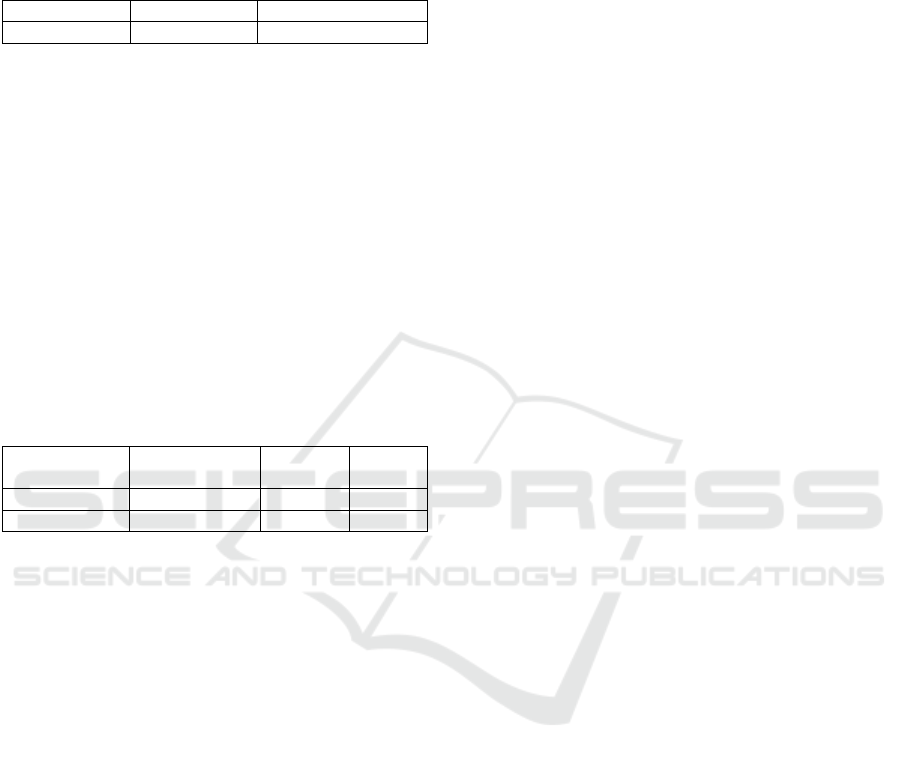

Table 2: Convergence Validity

Indicator

MC

CA

AM

X1.1

0,631

0,355

0,420

X1.2

0,686

0,349

0,409

X1.3

0,629

0,369

0,464

X1.4

0,830

0,364

0,525

X1.5

0,709

0,244

0,405

X1.6

0,825

0,371

0,536

X2.1

0,481

0,890

0,446

X2.2

0,446

0,949

0,503

X2.3

0,378

0,905

0,437

Y1

0,617

0,488

0,926

Y2

0,611

0,487

0,902

Y3

0,421

0,321

0,779

The following is the results of the R-Square

analysis in Table 3. It can be seen that R-Square

shows that the value of R-Square (R²) for construct

asset management (AM) is 46.5 or 46,5%. It belongs

to moderate model based on opinion of Chin (1998).

Variable management commitment (MC) and

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

688

competencies of asset administrator (CA) are able to

explain variable asset management (AM) equal to

46,5% while 53,5% is explained by other variables.

Table 3: R.Square Analysis

R Square

R Square Adjusted

AM

0,465

0,454

Hypothesis testing can be done by analyzing the

value of path coefficients after the bootstrapping

process. To see hypothesis testing done by

comparing t-statistic value with t-table value. The

hypothesis is accepted if the value of t-statistic > t-

table (1.96), but if the value of t-statistic < t-table

(1.96) then the hypothesis be rejected. In addition, to

test that the hypothesis can be done by analyzing the

significance of p-value compared with the error rate

set in this research is one-tailed test with alpha 5%

(0.05). The p-values < 0.05 then the hypothesis is

accepted, however, if p-values > 0.05, then the

hypothesis can be rejected. The results of path

coefficients analysis are presented in Table 4.

Table 4: The Result of Path Coefficients Analysis

Variable

Original

Sample

t-

Statistic

p-

Value

CA > AM

0,259

2,903

0,004

MC > AM

0,519

7,004

0,000

Table 4 described the analysis research

hypothesis testing. The hypotheses are:

H1: Management commitment (MC) has a positive

effect on asset management (AM) at

Government Units in the city governments of

South Sumatra Province.

H2: Competencies of asset administrator (CA) has a

positive effect on asset management (AM)

Government Units in the city governments of

South Sumatra Province.

The explanation of the results of hypothesis

testing based on Table 4 is as follows. The first

Hypothesis states that variable management

commitment (MC) has a positive effect on asset

management (AM) at Government Units in the city

governments of South Sumatra Province. Table 4

describes that MC testing with AM has a t-statistic

value of 7,004 greater than the value of t-table at

alpha 5% of 1,96. Thus, it can be said that the

hypothesis is accepted. The value of p-values

between MC and AM of 0.000 indicates a significant

level at alpha 0.05 (5%). It means that Management

Commitment (MC) has a significant effect on Asset

Management (AM). Meanwhile, to analyze the

direction of the relationship variable is by looking at

the path coefficient value (original samples) between

the variables of management commitment (MC)

with asset management (AM) of 0.519 with a

positive direction.

Thus, it can be concluded that the variables of

management commitment (MC) have a significant

positive effect on asset management (AM) at

Government Units in the city governments of South

Sumatra Province. It means that the first hypothesis

is accepted. This is in line with the research by

(Cooper, 2006) that defined management

commitment is to maintain and engage in behaviors

that can help others achieve a goal. He found that

senior management commitment played a primary

role in shaping employee behaviors and a secondary

role by shaping lower management behavior that

acts in turn on employee behavior.

Other researchers that clarify the relationship

between management commitment and performance

are (Tan, C. and Hamzah, 2008), (Pheng & Teo,

2004); (Taylor & Wright, 2003), Chin et al. (2003).

In an effort to improve the performance of asset

management, it is expected that management must

fully understand and support the management of

assets and actively participate in its implementation ,

rather than delegate it.

The second hypothesis states that the Variable

Competencies of Administrator (CA) have a positive

effect on Asset Management (AM) at Government

Units (OPD) in the city governments of South

Sumatra Province. Table 4 shows that the test CA

with AM has a value of 2,903 t-statistic greater than

t-table at alpha 5% by 1.96. Thus, it can be said that

the hypothesis is accepted. The value of p-values

between CA and AM of 0,004 indicates a significant

level in alpha 0.05 (5%), which means competencies

of administrator (CA) has a significant effect on

asset management (AM)). The direction of the

relationship of variables is analyzed by looking at

the value of path coefficient (original sample)

between competencies of administrator variable

(CA) with asset management (AM) of 0.259 with

positive direction.

Thus, it can be concluded that the competencies

of administrator (CA) variable has a significant

positive effect on asset management (AM). It means

that the second hypothesis is accepted, which is in

line with research conducted by Sedarmayanti

(2007) that the organizational goals can be achieved

because of the efforts of the actors found in the

organization. Competence is a fundamental

characteristic possessed by someone who has a

direct influence or can predict good performance. In

this case there is a close relationship between

employee competencies and institutional

performance. In other words, if the employee's

competence is good, then it is likely that

organizational performance is also good. Employee

Management Commitment and Competencies of Asset Administrator on Asset Management: Study in Government Units of South Sumatera

Province

689

competence will be better if you have high

knowledge, established skills and a good work

attitude.

Other research which clarifies the relationship

between competencies and performance are (Qiao &

Wang, 2009); (Ryan, Emmerling, & Spencer, 2009);

(Boyatzis, 2008); (Levenson et al., 2006); Dainty

(2004). In an effort to improve the performance of

asset management, it is expected that the

management of assets can be given adequate training

to improve performance in asset management.

3.1 The influence of management

commitment on asset management

at Government Units in the city

governments of South Sumatra

Province.

(Cooper, 2006) stated that management

commitment is defined as maintaining and engaging

in behavior that helps others achieve a goal.

Management Commitment is direct management

participation in important aspects and programs of

an organization and must be driven by the power of

desire to improve the quality of all organizations’

businesses. Top management has the power and

motivation to influence a change. Leadership that is

shown in the top management commitment and

supported by all members of the organization will

change towards a better direction.

In line with (Tan, C. and Hamzah, 2008) top

management commitment towards quality

management, it is generally perceived as one of the

key factors in determining its success. The research

conducted by (Munaim, 2012) found the existence

of management commitment in the implementation

of technical regulation of asset management is a

contributing factor to the implementation of good

asset management policies in each OPD to the

Government of West Nusa Tenggara Province. In

line with the results of research by Chin et al.

(2003), (Simamora & Halim, 2013) also stated that

management commitment factors are more critical to

affect asset management. Management commitment

is needed in overcoming problems related to asset

management. This is indicated by the information

obtained indicating that of managers who do not pay

attention to asset issues makes asset management a

complicated matter.

Other studies that support the results of this study

are (Caroline et al., 2016); (Javed, 2015);

(Abomaleh & Zahari, 2014); (Namada, Aosa,

Awino, & Wainaina, 2014); (Yousaf, 2006); (Taylor

& Wright, 2003); (Pheng & Teo, 2004); Samson et

al. (1999).

3.2 The influence of Asset

Administrator’s Competencies on

Asset Management at Government

Units in the city governments of

South Sumatra Province.

Implementation of asset management requires

asset administrators with adequate competencies.

The competencies possessed by the asset

administrator will determine the ability of the

organization in achieving the objectives of asset

management. According to Yusuf (2013), the key to

successful management of regional property is the

availability of competent employees in the

management of regional property. It is necessary to

have competent employees who have knowledge

about regional assets, skills in managing regional

assets, and attitudes towards managing local assets.

Knowledge about asset management will be very

helpful in making asset management decisions that

provide space for administrators to empower/utilize

an asset for the benefit of government operations

(Yusuf, 2013)

(Darno, 2012) found empirical evidence of the

influence of the ability of human resources on the

quality of local asset reports. According to

(Supriyadi, 2008), improving the quality of human

resources that carry out inventory and management

of regional property needs to be pursued in the form

of education, training, or technical guidance. With

this kind of activity, it is expected that the quality of

asset administrators will increase and impact upon

the quality of asset management.

The results of this study are in line with the

research conducted by (Wahyudi, 2014) that

competence shows skills and knowledge

characterized by professionalism. Competency

enhancement is certainly supported by the level of

the employee’s education, specialization (skills),

work experience and work attitude. (Zaim, Yaşar, &

Ünal, 2013) analyzed the effects of individual

competencies on performance in the services

industries in Turkey. He found that competencies

have a positive relationship to individual

performance. Furthermore, core competencies have

the most significant effect on individual

performance. In line with (Zaim et al., 2013) and

(Wahyudi, 2014), asset management competencies

are the most significant factor, when it comes to

asset management performance.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

690

4 CONCLUSIONS

Based on the results of this study, it can be

concluded as follows: 1) Management commitment

has a significant positive effect on asset management

at Government Units in the city governments of

South Sumatra Province, meaning that Management

Commitment has a strong influence on the

optimization of asset management. 2) the

competencies of an asset administrator have a

positive influence on asset management, it means

that competencies of asset administrators are needed

to assist the asset management to be carried out

optimally at Government Units in the city

governments of South Sumatra Province.

This research has been conducted on the

influence of management commitment and

competencies of asset administrators on asset

management. However, there are still some

limitations in this study to be an input for further

researchers especially on optimizing asset

management. The limitations in this study are as

follows : 1) The scope of this study is only limited to

4 city governments of South Sumatra Province,

while there are 17 cities/districts in South Sumatra

Province which were not included in this study; 2)

two variables that influence asset management in

this study are able to explain equal to 46,5%, while

53,5% is explained by other variables, thus, there is

still less exploration of other factors that affect asset

management; 3) The sample used in this study is

only limited to the head of Asset Administrator, so

that the information obtained is only limited to the

perception of the head of asset administrator in

Government Units .

In order to get better results, further researchers

are expected to do, as follows: 1) It is expected to

expand the research area to whole cities and districts

in this province. 2) To add the number of variables

that influenced asset management. 3) To include all

of the officials of asset management in Government

Units.

5 REFERENCES

AAMCoG. (2012). Pedoman Sistem Terpadu Pengelolaan

Aset yang Strategis (Vol. IS: 978-0-).

Abomaleh, A., & Zahari, I. (2014). The impact of

management commitment to service quality and

customer satisfaction : A Review of Saudi Arabia

public service sector, 3(1), 1–9.

Bond, S & Dent, P. (1998). Efficient management of

public sector assets The call for correct evaluation

criteria and techniques. Journal of Property Valuation

and Investment, 16(4), 369–385.

Boyatzis, R. E. (2008). Competencies in the 21st century,

27(1), 5–12.

https://doi.org/10.1108/02621710810840730

Caroline, N., Harriet, K., & Anne, N. (2016). Top

management commitment for successful small and

medium-enterprises ( SMEs ): A hoax or a reality ?,

12(4), 259–267.

https://doi.org/10.19044/esj.2016.v12n4p259

Cooper, D. (2006). The Impact of Management ’ s

Commitment on Employee Behavior : A Field Study.

American Society of Safety Engineers, 1(317), 7–14.

Darno. (n.d.). Analisis Pengaruh Kemampuan Sumber

Daya Manusia dan Pemanfaatan Teknologi Informasi

Terhadap Kualitas Laporan Barang Kuasa Pengguna

(Studi pada Satuan Kerja di Wilayah Kerja KPPB

Malang).

Donaldson, L., & Davis, J. H. (1991). Stewardship Theory

or Agency Theory: Australian Journal of

Management, 16(June 1991), 49–66.

https://doi.org/10.1177/031289629101600103

Haupt, T. C., & Whiteman, D. E. (2004). Inhibiting factors

of implementing total quality management on

construction sites. The TQM Magazine, 16(3), 166–

173. https://doi.org/10.1108/09544780410532891

Javed, S. (2015). Impact of Top Management

Commitment on Quality Management. International

Journal of Scientific and Research Publication, 5(8),

1–5.

Jolicoeur, P. W., & Barrett, J. T. (2005). Coming of age:

Strategic asset management in the municipal sector.

Journal of Facilities Management, 3(1), 41–52.

https://doi.org/10.1108/14725960510808383

Krisindarto, A. (2012). Pengelolaan Aset Tanah Milik

Pemerintah Kota Semarang. Jurnal Pembangunan

Wilayah & Kota, 8(4), 403–411.

Levenson, A. R., Van der Stede, W. A., & Cohen, S. G.

(2006). Measuring the Relationship Between

Managerial Competencies and Performance. Journal

of Management, 32(3), 360–380.

https://doi.org/10.1177/0149206305280789

McClelland, D. C. (1973). Testing for competence rather

than for “intelligence”. The American Psychologist,

28(1), 1–14. https://doi.org/10.1037/h0034092

Moorman, R. H., Niehoff, B. P., & Organ, D. W. (1993).

Treating employees fairly and organizational

citizenship behavior: Sorting the effects of job

satisfaction, organizational commitment, and

procedural justice. Employee Responsibilities and

Rights Journal, 6(3), 209–225.

https://doi.org/10.1007/BF01419445

Munaim. (2012). Kebijakan Pengelolaan Barang Milik

Daerah pada Pemerintah Provinsi Nusa Tenggara

Barat.

Namada, J. M., Aosa, E., Awino, Z., & Wainaina, G.

(2014). Management Participation and Firm

Performance, (March), 113–122.

Pate, J., Martin, G., & Robertson, M. (2003). Accrediting

competencies: a case of Scottish vocational

qualifications. Journal of European Industrial

Management Commitment and Competencies of Asset Administrator on Asset Management: Study in Government Units of South Sumatera

Province

691

Training, 27(2/3/4), 169–176.

https://doi.org/10.1108/03090590310468976

Pekei, B., & Hadiwidjojo, D. (2014). The Effectiveness Of

Local Asset Management ( A Study On The

Government Of Jayapura ), 3(3), 16–26.

Pheng, L. S., & Teo, J. A. (2004). Implementing total

quality management in construction firms. Journal of

Management in Engineering, 20(1), 8–15.

https://doi.org/10.1061/(ASCE)0742-

597X(2004)20:1(8)

Qiao, J., & Wang, W. (2009). Managerial competencies

for middle managers: some empirical findings from

China. Journal of European Industrial Training,

33(1), 69–81.

https://doi.org/10.1108/03090590910924388

RI, I. I. B. (n.d.). IHPS I Tahun 2016.

Ryan, G., Emmerling, R. J., & Spencer, L. M. (2009).

Distinguishing high‐performing European executives.

Journal of Management Development, 28(9), 859–

875. https://doi.org/10.1108/02621710910987692

Shepherd, E. (2013). Why are records in the public sector

organizational assets? Records Management Journal,

16(1), 6–12. https:

//doi.org/http://dx.doi.org/10.1108/MRR-09-2015-

0216

Simamora, R., & Halim, A. (2013). Faktor-Faktor yang

Mempengaruhi Pengelolaan Aset Pasca Pemekaran

Wilayah di Kabupaten Tapanuli Selatan. Jurnal

Ekonomi Dan Bisnis, 13(September), 29–43.

Tan, C. and Hamzah, A. (2008). Top Management

Commitment Towards Quality Management, 1–13.

Taylor, W. A., & Wright, G. H. (2003). The impact of

senior managers’ commitment on the success of TQM

programmes. International Journal of Manpower,

24(5), 535–550.

https://doi.org/10.1108/01437720310491071

W. Supriyadi. (2008). Evaluasi Proses Inventarisasi

Barang Milik Daerah di dalam pengelolaan barang

milik daerah di Pemerintah Kabupaten Lampung Barat

dalam mendukung pengelolaan barang milik daerah

yang efektif dan efisien.

Wahyudi, F. (2014). Peran Kompetensi Dalam

Meningkatkan Kinerja Pegawai Bagian Sosial

Sekretariat Daerah Kabupaten Kutai Timur Firman

Wahyudi, 3(2), 186–197.

White, A. D. (2012). A review of UK public sector real

estate asset management. Journal of Corporate Real

Estate International Journal of Operations &

Production Management Iss International Journal of

Manpower, 14(7), 94–104. Retrieved from

http://dx.doi.org/10.1108/14630011211261696%5

Yousaf, N. (2006). Impact of Organizational Culture on

TQM Program, 1–11.

Zaim, H., Yaşar, M. F., & Ünal, Ö. F. (2013). Analyzing

the Effects of Individual Competencies on

Performance: a Field Study in Services Industries in

Turkey. Journal of Global Strategic Management,

2(7), 67–67.

https://doi.org/10.20460/JGSM.2013715668

Badan Pemeriksa Keuangan (BPK RI). 2015. Ihtisar

Hasil Pemeriksaan Semester Satu dan Dua Tahun

2014, Indonesia.

Peraturan Pemerintah No. 27 Tahun 2014 tentang

Pengelolaan Barang Milik Daerah

Peraturan Menteri Dalam Negeri Nomor 19 Tahun 2016

tentang Pedoman Teknis Pengelolaan Barang Milik

Daerah

Undang-undang Nomor 23 Tahun 2014 tentang

Pemerintahan Daerah

Undang-undang Nomor 5 Tahun 2014 tentang Aparatur

Sipil Negara

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

692