The Influence of Local Tax, Local Retribution, General Allocation

Fund, and Special Allocation Funds on Capital Expenditure

Arthur Simanjuntak, Mitha Christina Ginting, and Duma Rahel Situmorang

Accounting Department Universitas Methodist Indonesia Medan, Indonesia

Keywords: Local Taxes, Local Retribution, General Allocation Fund, Special Allocation Fund, and Capital Expenditure

Abstract: The purpose of this study was to determine the influence of local taxes, Local Retribution, general allocation

fund, and special allocation funds on capital expenditure. This study includes 25 Districts and 8 Cities in

2013-2017. Analysis techniques used in this research is multiple linear regression to the data of observation

as much as 100. The results of the study showed that the local tax general allocation fund and special allocation

funds had significant positive influence on capital expenditure. Only Local Retribution had insignificant

capital expenditure. This shows that there is still the dependence of local governments to transfer funds from

the central government. The determinant coefficient showed 84.3 percent Capital expenditures could be

explained or controlled by the Local Taxes, Local Retribution, General Allocation Fund and Special

Allocation Fund while remaining 15.7 percent is explained or influenced by other variables outside our model.

1 INTRODUCTION

The implementation of local government is following

the mandate of the 1945 Constitution, that is, the local

government can regulate and manage its government

affairs to realize a just and prosperous Indonesian

society through improved living standards,

intelligence and the welfare of the whole people to

achieve national development. In Law of The

Republic Indonesia Number 32 Year 2004 explained

the division and formation of regions of the Republic

of Indonesia, which is autonomous and applies the

principle of decentralization. Local autonomy is a

manifestation of the delegation of authority and

responsibilities from the central government to local

governments where the local government has the

authority to regulate its regions both from the

financial sector and from the non- financial sector.

Local Governments are expected to be able to

manage their own finances through the Local

Expenditure Budget which is determined by local

regulations. Preparation of the provincial budget

begins with making agreements between the

executive (Local Government) and legislative (City

Council) on public policy Local Budget and Budget

Priorities, which will serve as guidelines for the

preparation of the budget revenue and expenditure.

The executive makes a draft of the Local Expenditure

Budget by the general policy of the Local

Expenditure Budget and the budget priorities, which

are then submitted to the legislative council to be

studied and discussed together before being

established as a Local Unity (Haryanto, et al. 2007).

The problem faced by the Local Government in

public sector organizations is about budget allocation.

Budget allocation is the sum of fund allocations for

each program. With limited resources, the Local

Government must be able to allocate the revenue

obtained for productive local expenditure. This is

supported by a statement (Felix, 2012) which states

that local governments should be able to allocate

capital expenditure that is higher than routine

spending. Local spending is an estimate of the local

expenditure burden that is allocated relatively and

evenly so that it can be relatively enjoyed by all

groups of people without discrimination, especially in

the provision of public services (Halim, 2007).

During this time, the Local Government uses

more local income for operational spending needs

rather than capital expenditure. Operational

Expenditures are Local Government expenditures

consisting of personnel expenditure, goods and

services expenditure, interest expenditure, subsidy

expenditure, and grant expenditure. When viewed in

terms of benefits, budget allocation to the capital

expenditure sector is advantageous and productive in

providing services to the public. Improving the

170

Simanjuntak, A., Ginting, M. and Situmorang, D.

The Influence of Local Tax, Local Retribution, General Allocation Fund, and Special Allocation Funds on Capital Expenditure.

DOI: 10.5220/0009201001700177

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 170-177

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

quality of public services can be enhanced through

improving the quality of management, namely by

efforts to minimize the gap between service levels

and consumer expectations (Bastian, 2006).

Capital expenditure is a component of direct

spending in the government budget that produces

output in the form of fixed assets. Capital expenditure

is generally allocated, can be used as a means of local

development, such as the development and

improvement of the education, health and

transportation sectors, so that people can enjoy the

benefits of local development. According to

Mardiasmo (2009) stated that the higher the level of

capital investment is expected to deny the public

participation rate with the event. The development of

industrial infrastructure has a real impact on local tax

increases because meeting the quantity and quality of

services and public facilities will make the

community feel comfortable and be able to run their

business efficiently and effectively to increase their

participation in growth. With the rapid development

of development, is expected that an increase in local

independence in financing its activities, especially in

terms of finance, with the rise in productivity of the

people who are in the area will have an impact on the

local economy along with increasing per capita

income.

The development of industrial infrastructure and

providing facilities to increase investment will have a

positive impact by increasing the Local Original

Revenue so that it can reduce the dependence of the

Local Government on the Central Government. Local

Original Income consists of local taxes, local

retribution, the results of the management of

separated local assets, and other legitimate local

original income (Kawedar, et al. 2008). In Law of The

Republic Indonesia Number 34 Year 2000 on taxes

and retribution, it is mentioned that the local tax is

obligatory contribution made by the individual or

entity to areas without direct payment balance, which

can be imposed by legislation applicable, which is

used to finance the local administration and local

development. Local tax for each districts/city be seen

from the post Local Revenue in the Realized Budget

Report. Sources of local income include, Motorized

Vehicle Tax, Motorized Vehicle Transfer Fee Tax,

Motorized Vehicle Fuel Tax, Surface Water Tax, and

Cigarette Tax.

Local retribution are an essential source of local

income to finance local government and local

development. In Law of The Republic Indonesia

Number 34 Year 2000 stated that local retribution, in

the future referred to as retribution, are local

retribution as payments for particular services or

permits that are expressly provided or provided by the

Local Government for the benefit of individuals or

entities. The ability of regions to grant funding from

areas is highly dependent on the ability to realize

economic potential into forms of economic activity

capable of creating revolving funds for sustainable

local development (Darwanto and Yustikasari, 2007).

Opinion (Yossi, et . Al., 2015) states that Local Tax

and Local Retribution do not influence Capital

Expenditures. The granting of authority from the

Central Government to the Local Government is

balanced with the transfer of funds, facilities and

infrastructure as well as human resources. The

removal of these funds manifests a balanced fund

which consists of the Special Allocation Fund, the

General Allocation Fund and the Revenue Sharing

Fund that has been explained in Law of The Republic

Indonesia Number 33 Year 2004 concerning financial

balance between the Central Government and the

Local Governments.

Special Allocation Funds are and an originating

from the State Revenue Budget, which is allocated to

specific regions to help to fund special activities

which are local affairs and following national

priorities. The use of Special Allocation Funds is

more directed at investment activities in the

development, acquisition, improvement, and

improvement of physical facilities and infrastructure

with a long economic life, including the procurement

of supporting physical facilities, and excluding

capital inclusion. With the allocation of Special

Allocation Fund is expected to affect capital

expenditure, as Special Allocation Funds tend to be

added to the fixed assets owned by the government to

improve public services. Research conducted

(Sumarmi, 2009) states that the Special Allocation

Fund has a positive and significant effect on capital

expenditure in this research area, which is also in line

with research conducted by Sudika and Budiartha

(2017).

General Allocation Funds are several funds

allocated to each Autonomous Region (Province and

Districts/City) in Indonesia each year as development

funds aimed at equitable distribution of financial

capacity between regions to fund the needs of the

Autonomous Region in the context of implementing

decentralization. Studies conducted by Legrenzi and

Milas (2001) to find empirical evidence that funds

transfers in the long-term effect on capital spending

and a decrease in the number of transfers of funds can

cause a reduction in capital expenditure spending.

The same thing also expressed by Holtz-Eaken et al.

(1985) which states that there is a close relationship

between transfers from the Central Government and

The Influence of Local Tax, Local Retribution, General Allocation Fund, and Special Allocation Funds on Capital Expenditure

171

local government spending. This opinion is supported

by the research conducted (Tuasikal, 2008) states

affect the General Allocation Fund Capital

Expenditures. This study aims to analyze the effect of

Local Taxes, Local Retribution, General Allocation

Funds, and Special Allocation Funds on Capital

Expenditures in Districtss/Cities in North Sumatra

Province from 2013 to 2017. Capital expenditure has

an essential role in running the government system,

namely, to improve public welfare and as a form of

good governance.

Research on the General Allocation Fund and

Special Allocation Fund is already done, with more

adding a variable previous research that details the

variables Local Own-Source Revenue Revenue into

Local taxes and Retribution and accompanied with

the use of the latest data, the researchers wanted to

know whether the unique variable will affect capital

expenditure and whether the findings of this study are

consistent with previous studies or even provide new

results.

Problem Formulation:

1. Does the Local Tax Influence on Capital

Expenditures in the Districtss/Cities in North

Sumatra Province from 2013 to 2017?

2. Does the Local Retribution Influence on Capital

Expenditures in the Districtss/Cities in North

Sumatra Province from 2013 to 2017?

3. Does the General Allocation Fund Influence on

Capital Expenditures in Districtss/Cities in North

Sumatra Province from 2013 to 2017?

4. Does the Special Allocation Fund Influence on

Capital Expenditures in Districtss/Cities in North

Sumatra Province from 2013 to 2017?

5. Do Local Taxes, Local Retribution, General

Allocation Funds, and Special Allocation Funds

simultaneously Influence on Capital Expenditure

in the Districtss/Cities in North Sumatra province

from 2013 to 2017?

2 LITERATUR REVIEW

2.1 Capital Expenditures

According to Government Regulation Number 71

Year 2010, Capital Expenditures are budget

expenditures for the acquisition of fixed assets and

other assets that provide benefits over one accounting

period. Capital expenditure is intended to get the local

government's fixed assets, namely equipment,

buildings, infrastructure, and other fixed assets.

Capital expenditure is one component of direct

expenditure used to finance investment needs. Capital

expenditure is a local government spending that

benefits exceed one fiscal year and will add a wealth

of assets or regions and will further add to shopping

routine such as operating and maintenance costs.

2.2 Local Taxes

According to Hasbullah (2015), Tax is an

embodiment of state obligations and the role of

taxpayers to directly and jointly carry out tax

obligations for state financing and national

development. In Law of The Republic Indonesia

Number 34 Year 2000 concerning local taxes and

retribution, it is stated that local taxes are compulsory

contributions made by individuals or entities to the

region without balanced direct benefits, which can be

imposed based on applicable laws and regulations,

which are used to finance the implementation of the

Local Government and local development. Tax

collection in Indonesia refers to a self-assessment

system, which is a tax collection system that gives the

authority, trust, responsibility, to the taxpayer to

calculate, calculate, pay and report for themselves the

amount of tax that must be paid (Diana and Lilis,

2010).

2.3 Local Retribution

Local user fees are an important source of local

income to finance local government and local

development. In (Law of The Republic Indonesia

Number 28 Year 2009) it is stated that Local

Retribution is a local retribution as payment for

particular services or permits that are expressly

provided and given by the Local Government for the

benefit of individuals or entities and Local

Retribution is one of the essential sources of local

income, in order to finance the implementation of

local government.

2.4 General Allocation Fund

General Allocation Funds are several funds allocated

to each Autonomous Region (Province and

Districts/City) in Indonesia each year as development

funds aimed at equitable distribution of financial

capacity between regions to fund the needs of the

Autonomous Region in the context of implementing

decentralization. According to (Nordiawan and

Ayuningtyas, 2010) General Allocation Funds are

funds aimed at equitable distribution of financial

capacities between regions intended to reduce

EBIC 2019 - Economics and Business International Conference 2019

172

disparities in financial capabilities between regions

through acceptance of formulas that take into account

local needs and potentials.

2.5 Special Allocation Funds

Special Allocation Funds are funds sourced from the

State Budget which are allocated to specific areas to

help to fund special activities, which are local affairs

and following national priorities. According to

(Nordiawan and Ayuningtyas, 2010) Special

Allocation Fund is intended to help finance special

activities in specific areas which are local affairs and

following national priorities, expressly to finance the

needs of essential public facilities and infrastructure

that have not reached specific standards or to

encourage the acceleration of local development.

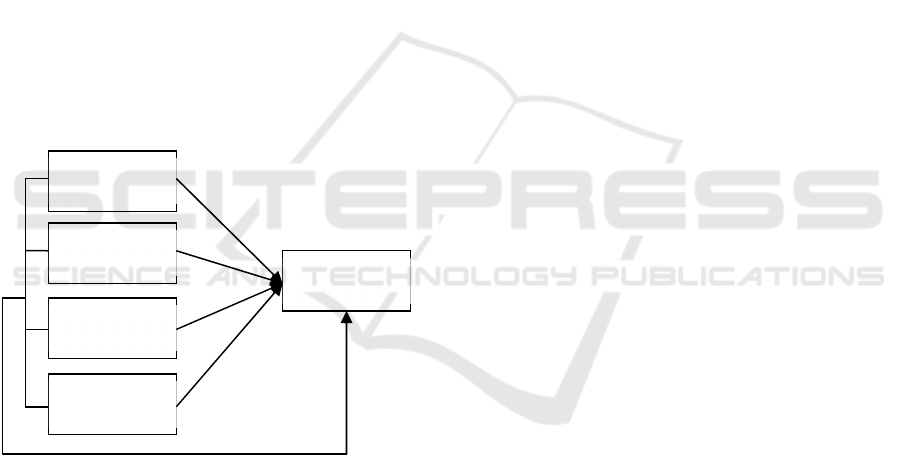

2.6 Conceptual Framework

Based on the above theoretical basis and problem

formulation, the researchers develop the research

framework. The conceptual framework to be studied

by the researcher is as the following.

2.7 Hypothesis

2.7.1 The Influence of Local Taxes on

Capital Expenditures

Local taxes substantial capital expenditure (Yossi et

al. 2015). Local tax is the local original income,

which is determined through local regulations. Local

taxes can be in the form of hotel charges, restaurant

taxes, entertainment tax, advertisement tax, class C

excavation tax, parking tax, and street lighting tax.

The Local Government has the authority to allocate

revenues in the direct expenditure sector or for capital

expenditure. From this description, the hypotheses

that can be formulated are:

H

1

: Local taxes Influence on Capital Expenditures

2.7.2 The Influence of Local Retribution on

Capital Expenditures

Improvement of services to the community can be

increased if the revenue owned by the Local

Government from retribution is also sufficient. Even

though the Local Government receives financial

assistance from the Central Government, the Local

Government must also be able to optimize its local

potential to be able to increase Local Own-Source

Revenue. Local independence can be realized in one

way, namely by increasing Local Own-Source

Revenue from the local retribution sector. If local

retribution increases, the Local Own-Source Revenue

will also increase to increase the allocation of capital

expenditure to improve services to the community.

From this description, the hypotheses that can be

formulated are:

H

2

: Local Retribution Influence on Capital

Expenditures

2.7.3 The Influence of General Allocation

Funds on Capital Expenditures

The General Allocation Fund originates from the

State Budget transfers, which are allocated with the

aim of equitable distribution of funds between regions

to finance their expenditure needs in the context of

decentralization. Research conducted by Wandira

(2013) found that local independence did not

improve; in fact, the opposite happened, namely the

dependence of local governments on central

government transfers (General Allocation Funds)

became higher. (Prakosa, 2004) provides empirical

facts where the General Allocation Fund has a

positive influence on local government capital

expenditure (Sudika and Budiartha (2017)) Show that

the General Allocation Fund has a significant effect

on the allocation of capital expenditure. This gives a

strong indication that the behavior of local spending,

especially capital spending, will be strongly

influenced by revenue sources (General Allocation

Funds). From this description, the hypotheses that can

be formulated are:

H

3

: General Allocation Funds Influence on Capital

Expenditures

2.7.4 The Influence of Special Allocation

Funds on Capital Expenditures

Special Allocation Funds are funds sourced from the

State Revenue Budget, which are allocated to local

Local

Taxes

Local

Retribution

General

Allocation

Special

Allocation

Capital

Expenditure

The Influence of Local Tax, Local Retribution, General Allocation Fund, and Special Allocation Funds on Capital Expenditure

173

governments to finance special activities which are

local affairs and national priorities. Research

conducted (Tuasikal, 2008) Special Allocation Funds

partially positive effect on capital expenditure. The

same thing was said by (Abdullah and Halim, 2004)

empirically said that the Special Allocation Fund had

a positive and significant effect on capital

expenditure. (Sumarmi, 2009) Stated that the Special

Allocation Fund significantly influences the Capital

Expenditure Allocation. This indicates that there is a

relationship between the provision of transfer funds

from the central government (Special Allocation

Funds) with local government capital expenditure.

From this description, the hypotheses that can be

formulated are:

H

4

: Special Allocation Funds Substantial Capital

Expenditures

2.7.5 The Influence of Local taxes, Local

Retribution, General Allocation Funds

and Special Allocation Funds on

Capital Expenditures

The Local Government has the authority to allocate

revenues in the direct expenditure sector or for capital

expenditure. Local tax is Local Original Revenue

whose tariff is determined through Local Regulation.

Local independence can be realized in one way,

namely by increasing Local Original Revenues from

the local retribution sector. If local retribution

increases, the Local Original Revenue will also

increase to increase the allocation of capital

expenditure to improve services to the community.

The General Allocation Fund originates from the

transfer of the State Revenue Budget allocated for

equitable distribution of funds between regions to

finance its expenditure needs in the context of

decentralization whereas the Special Allocation Fund

is a fund sourced from the State Revenue Budget

which is allocated to local governments to finance

special activities which are local affairs and national

priorities.

H

5

: Local Taxes, Local Retribution, General

Allocation Funds, and Special Allocation Funds

Affect Capital Expenditures

3 RESEARCH METHODOLOGY

3.1 Types of Research

This type of research is causal design. This research

is a replication of previous research. The difference

between this research and previous research lies in the

data in the form of Realization Report of the

Districts/City government budget in North Sumatra

Province for the period 2013-2017.

3.2 Population and Research Samples

Population is "a generalization area consisting of

objects or subjects which become specific quantities

and characteristics determined by researchers to be

studied, and then conclusions can be drawn (Erlina,

2011). The population in this study is the report on

the realization of the Districts/City Local Revenue

Budget in North Sumatra in 2013-2017 In North

Sumatra, there, are 33 Districtss/Cities. The sample,

according to Erlina (2011) is "part of the population

used to estimate population characteristics.”

Sampling is done by purposive sampling method,

which is sampling based on specific criteria.

The criteria used to determine the sample are as

follows:

a. Districtss/Cities in North Sumatra Province have

submitted Reports the Realization of Local

Revenue Expenditures to the North Sumatra

Statistics Office (www.sumut.bps.go.id).

b. Districtss/Cities in North Sumatra Province that

include Special data, and Capital Expenditures

respectively in the realization report of the Local

Expenditure Budget from 2013 to 2017.

Based on the considerations mentioned above, the

researchers used 14 (fourteen) districts governments

and 6 (six) municipal governments as research

samples. To obtain a sample of 100 observations

where there are 20 Districts/City governments (with

details of 14 (fourteen) districts governments and 6

(six) municipal governments) X 5 years of

observation.

3.3 Operational Definition of the

Variable and Measurement Scale

Variable Definition Scale

Local tax (X

1

) Mandatory

contributions to Regions

owed by individuals or

entities that are coercive

based in Law of The

Republic of Indonesia.

Ratio

Local

Retribution (X

2

)

Local retribution as

payments for specific

services or permits that

are expressly provided

and/or granted by the

Local Governmen

t

Ratio

EBIC 2019 - Economics and Business International Conference 2019

174

General

Allocation Funds

(X

3

)

Funds sourced from

the revenue of the State

Expenditure Budget

allocated for equitable

distribution of financial

capacity between regions

to fund local needs in the

context of implementing

Decentralization

Ratio

Special

Allocation Funds

(X

4

)

Funds sourced from

the State Budget

Revenues are allocated to

specific areas to help fund

special activities

Ratio

Capital

Expenditures (Y)

Expenditures used

for procurement of

tangible fixed assets that

have a value of more than

12 (twelve) months for

use in government

activities

Ratio

4 DATA ANALYSIS MODEL

The multiple linear regression model is a regression

model that has more than one independent variable.

In this study, there are four independent variables,

namely Local Tax, Local Retribution, General

Allocation Fund, and Special Allocation Fund. The

multiple linear regression model is said to be a good

model if the model has an assumption of data

normality, and is free from classical statistical

assumptions both multicollinearity, autocorrelation

and heteroscedasticity.

The multiple linear regression equation is:

Y = β

0

+ β

1

X

1

+ β

2

X

2

+ β

3

X

3

+ β

4

X

4

+ ε

5 FINDINGS

N

Minimum Maximum Mean Std.

Deviation

Local taxes

10

0

14.6

5

1329261

8.18E4

361341.57

5

Local Retribution

10

0

23.6

8

274512

4.25E4

62185.57

4

General

Allocation Fun

d

10

0

364.68

5

1316714

7.68E5

371315.66

0

Special Allocatio

n

Fun

d

10

0

37.28

3

245000

6.97E4

43676.43

2

Capital

Expenditure

10

0

107.53

4

1104423

3.75E5

316824.46

6

Valid N (listwise)

10

0

Sumber: processed data SPSS, 2019

In the Descriptive Statistics indicates the

description of the research variables that shows the

minimum value, maximum value, average value, and

standard deviation. In this study, the standard

deviation value is smaller than the average value so it

can be concluded that the survey is distributed

normally.

5.1 Inferential Statistics Analysis.

Inferential statistical analysis has been done by doing

convensional assumption test. The aim of standard

assumption test is to have a useful dataset of

enormous importance for applied economic research.

The the conventional assumption tests aims of a

normality test, multicollinearity test, autocorrelation

test, and heteroscedasticity test.

Normality test is used to determine if a data set is

well-modeled, be normally distributed and to

compute how likely it is for a random variable

underlying the data set to be normally distributed.

The empirical distribution of the data should be bell-

shaped and resemble the normal distribution.

From the results of processing the data of One-

Sample Kolmogorov-Smirnov test, the value of

Kolmogorov-Smirnov is 0.564 and the Asymp value.

Sig-2 Tailed is 0.843 . Significant value greater than

0,05, then H

0

accepted which means that the data

residual normal distribution. Data that are normally

distributed can also be viewed through histogram

graphs and normal PP-plot data graphs.

Model

Unstandardized

Coefficients

Collinearity

Statistics

B Std.

Error

Tolerance VIF

1

(Constant)

5.214 3.136

Local taxes .33

2

.125 .215

8.215

Local Retribution .11

6

.146 .510

3.256

General

Allocation Fun

d

-.03

5

.314 .226

8.267

Special Allocatio

n

Fun

d

.51

3

.231 .718

3.236

a.

Dependent Variable: Capital Expenditure

Multicollinearity measurement in this study is

seen from the tolerance value, and variance inflation

factor (VIF). If the tolerance value is > 0.1 and the

VIF value is < 10, then the regression model is free

from multicollinearity problem (Ghozali, 2013).

From the table 4 has shown that the data in this study

is free from the multicollinearity problems.

The Influence of Local Tax, Local Retribution, General Allocation Fund, and Special Allocation Funds on Capital Expenditure

175

In the scatterplot chart, it is seen that the points

spread randomly and are spread both above and

below the number 0 on the Y-axis. North Sumatra is

based on the input of the independent variable Local

Tax, Local Retribution, General Allocation Fund, and

Special Allocation Fund.

Mode

l

R

R

Square

Adjusted

R

Square

Std. Error o

f

the

Estimate

Durbin

-

Watso

n

1

.912

a

.869 .843 .4136

4

2.114

a.

Predictors: (Constant), Special Allocation Fund, Local

Retribution, Local taxes, General Allocation Fund

b.

Dependent Variable: Capital Expenditure

The autocorrelation test results above show the

Durbin Watson ( dw ) statistical value of 2,114. This

value will be compared with the value of the

researcher’s, table using 5% significance, the number

of observations (n) of 100, and the number of

independent variables 4 (k = 4). So based on the

Durbin Watson table, it can be concluded that there is

no autocorrelation, both positive, and negative.

Model

Unstandardized

Coefficients

Standardized

Coefficients

t

Sig.

B Std. Erro

r

Beta

1

(

Constant

)

6.243 2.816 2.124 .244

Local taxes .365 .067 .770 3.645 .002

Local

Retribution

.031 .126 .145 4.814 .024

General

Allocation Fun

d

-.023 .351 -.220 -4.104 .035

Special

Allocation Fun

d

.615 .214 .470 4.325 .000

a. Dependent Variable: Capital Expenditure

Based on Table 4.5, the linear regression equation

is obtained as follows:

Y = 6.243 + 0.365X

1

+ 0.031X

2

– 0.023X

3

+

0.615X

4

+ ε

6 CONCLUSIONS

Based on the results of hypothesis testing, it shows

that simultaneously Local Tax, Local Retribution,

General Allocation Funds and Special Allocation

Funds had significant positive influence on the

Capital Expenditure in Districts/City Government

North Sumatra. Based on the results of hypothesis

testing, partially shows that Local Tax, Local

Retribution, and Special Allocation Funds had

significant positive influence on the Capital

Expenditure in Districts/City Government North

Sumatra while the General Allocation Fund had

significant negative influence on the Capital

Expenditure in Districts/City Government North

Sumatra.

REFERENCES

Abdullah, Syukriy dan Abdul Halim. 2004. “The Effect of

the General Allocation Fund and Local Original

Revenue on Local Government Spending: Case Study

of Regencies/Cities in Java and Bali.” Proceeding on

the National Accounting Symposium VI, 16-17 October

2003. Surabaya.

Bastian, Indra. 2006. Public Sector Accounting: An

Introduction. Jakarta: Erlangga.

Darwin and Yulia Yustikasari, 2007. Effect of Economic

Growth in Local Original Revenue, and General

Allocation Funds on the Allocation of Capital

Expenditure Budget, National Symposium on

Accounting X. Makassar.

Diana, Anastasia and Lilis Setiawati (2011). Accounting

Information System. Andi Offset: Yogyakarta.

Erlina, 2011. Research Methodology: For Accounting.

USU PRESS: Medan.

Felix, Olurankinse. 2012. Analysis of the effectiveness of

capital expenditure budgeting in the local government

system of Ondo State, Nigeria. Journal of Accounting

and Taxation, 4 (1), pp: 1-6.

Ghozali, Imam. 2014. Multivariate Analysis Application

with SPSS Program. Semarang: Diponegoro University

Publisher Agency.

Halim, Abdul. 2004. Local Financial Accounting : Revised

Edition . Salemba Empat.

Halim, Abdul. 2007. Public Sector Accounting : Local

Financial Accounting. Salemba Empat, Jakarta.

Haryanto, et al. (2007). Public Sector Accounting . First

edition. Diponegoro University.

Hasbullah. 2015. Fundamentals of Educational Sciences .

Jakarta: PT Raja Grafindo Persada.

Holtz-Eakin, Douglas, Harvey S & Schuyley Tilly, 1994.

Temporal Analysis of State A Local Government

Spending: Theory and Tests. Journal of Urban

Economics 35: 159 - 174.

EBIC 2019 - Economics and Business International Conference 2019

176

Kawedar, Warsito, Abdul Rohman, and Sri Handayani.

2008. Public Sector Accounting: Local Budgeting

Approaches and Local Financial Accounting.

Semarang: UNDIP Publishing Agency.

Legrenzi, Gabriella & Costas Milas. 2001. Non-Linear and

Asymmetric Adjustments The Local Revenue-

Expenditure Models: Some Evidence from The Italian

Municipalities. University of Milan, Working Paper.

Mardiasmo. 2009. Public Sector Accounting. Yogyakarta:

Andi.

Nordiawan, Deddi, and Ayuningtyas Hertianti. 2010.

Public Sector Accounting. Second Edition. Jakarta:

Salemba Empat.

Prakosa, Kesit Bambang. 2004. Analysis of the Effect of

General Allocation Funds (DAU) and Local Original

Revenues on Local Expenditure Prediction (Empirical

Study in Central Java Province and DIY). Indonesian

Journal of Accounting & Auditing, 8. (pp. 101–118).

Sudika, I Komang and I Ketut Budiartha. 2017. The Effect

of Local Taxes, Local Retribution, General Allocation

Funds, and Special Allocation Funds on Bali Province

Capital Expenditures. E-Journal of Udayana University

Accounting . Vol.21.2. November (2017): 1689-1718.

Sumarmi, Saptaingsih. 2009. The Effect of Local Revenue,

General Allocation Funds, and Special Location Funds

on Districts/City Local Capital Expenditure Allocation

in Yogyakarta Province. Akmenipa Journal . UPY, Vol

4, 2009.

Tuasikal, Askam, 2008. Effect of DAU, DAK, PAD, and

GRDP on Capital Expenditures of Districts/City

Governments in Indonesia. Journal of Accounting

Studies & Research . Vol. 1, No. 2, July 2008. p . 142-

155.

Wandira, Arbie. 2013. The Effect of PAD, DAU, DAK, and

DBH on Capital Expenditures. Journal of Accounting.

Yossi, Sandri Mamonto, JB Kalangi and Krest D. Tolosang,

2015 The Effect of Local Taxes and Local Retribution

on Capital Expenditures (Study in Bolaang

Mongondow Regency for the Period 2004-2013).

Journal of Accounting , Sam Ratulangi University.

Manado

The Influence of Local Tax, Local Retribution, General Allocation Fund, and Special Allocation Funds on Capital Expenditure

177