The Influence of Company’s Characteristics to Propensity to

Pay Dividend

Arief Yulianto

1

, Rini Setyo Witiastuti

1

, Siti Ridloah

1

, Siti Khotimah

1

, Heny Hendrayati

2

,

Murwatiningsih

2

1

Universitas Negeri Semarang

2

Unviersitas Pendidikan Indonesia

khotimah@yahoo.com, henyhendra@gmail.com, murwatiningsih@gmail.com

Keywords: Propensity to Pay Dividend, Company’s Characteristics

Abstract: The study aims at describing and analizing the influence of company’s characteristics to propensity

to pay dividen. The units of observation were 4530 companies recorded by Indonesia Stock

Exchange from 2008 up to 2017. In analizing the data, logit regression was implemented. The

finding shows that the greater the company’s profitability, the greater the propensity to pay

dividend will be. Further, the lower the asset growth and market to book ratio, the greater the

propensity to pay dividen will be.

1 INTRODUCTION

Baker and Wurgle (2004) explained that by having

the controll of company’s characteristics, the

company will share the dividend based on the

investor’s willingness. The manager will always

serve the investors’ demand by paying the dividend

when the investors determine the high price on

premium dividend of payers company, and he also

determines not to pay the dividend when the investors

prefer non-payers companies to the payers companies

(Baker & Wurgler, 2004a).

This theory emphasizes on investors’ demand on

dividend which is affected by market sentiment. The

main estimation of catering theory is that the

probability on dividend payment depends on

premium dividend. It can be measured by looking at

the difference on average logarithm of market to book

ratio of payers and non payers companies (Baker &

Wurgler, 2004a). The catering theory also states that

companies’ determination in sharing the dividend is

not only influenced by the investors’ demand, but also

considering the companies’ characteristic

Baker & Wurgler (2004b) implemented the

company’s characteristics as a control variable for

explainining the relationship between premium

dividend and propensity to pay dividend in their

research. Their finding shows that the company’s

characteristic is influential to the probability of a

company in paying the dividend. A company with a

firm size, great profitability, low asset growth, and

low market to book ratio considers more on the

investors’ willingness on dividend than a company

with a firm size, low profitability and high asset

growth, and high market to book ratio. This finding is

in line with the research conducted by Baker &

Wurgler (2004a), Fama & French (2001), Ferris,

Jayaraman, & Sabherwal (2009), Denis & Osobov

(2008), Li & Ã (2006), and Wang & Lin (2016). The

company should not only consider the investor’s

demand on dividend, but it should also asses the

company’s characteristic

However, Tangjitprom's research finding (2013)

is rather different. It illustrates that high growth of

company causes high probability of propensity to pay

dividend. The company still pays the dividend

although the company’s growth is high. This is

because the company has high performance. Suranta,

Eddy (2010) wrote that profitability and growth

opportunities do not influence propensity to pay

dividend. Nurhayati (2013) argued that firm size has

negative influence to dividend payout ratio, while

Situmorang (2017) found that firm size does not

influence dividend payout ratio. Moreover, the

company size does not impact the number of dividend

shared by the company. It has not been able to

become a guarantee yet for the company to give high

Yulianto, A., Witiastuti, R., Ridloah, S., Khotimah, S., Hendrayati, H. and Murwatiningsih, .

The Influence of Company’s Characteristics to Propensity to Pay Dividend.

DOI: 10.5220/0009203903450350

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 345-350

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

345

dividend. Then, the company can choose to keep its

profitability to fund the company’s growth rather than

giving the dividend. In fact, there are still research

gaps and they can be explored deeper to test the

impact of company characteristic to propensity to pay

dividend in Indonesia.

2 LITERATURE REVIEW

Catering Theory of Dividend

An alternative approach on propensity to pay

dividend is dividend catering theory proposed by

Baker & Wurgler (2004a). They argued that dividend

demanded by the investors encourage the company to

pay the feasible dividend for investors. This market

desire is called as “catering incentive”. They use

proxy to meet the investors’ needs on dividend;

premium dividend is the difference between the

average market ratio to book divodend payer and non

payer.

Catering theory is developed based on 3

assumptions. First, it is unknown. In other words, it

emerges because it may be because of psychological

or isntitutional reasons. Some investors lack of

information or stocks need various times to be levied

on dividend. Second, arbitration is failed to avoid the

demand to separate the price of payers not the payers.

Third, managers rationally meet the investors’

demand (Baker & Wurgler 2004a )

Based on above assumption, Baker & Wurgler

(2004a) proposed that the decision to pay dividend is

motivated by the investors’ demand. The manager

serve the investors by paying the dividend when they

set high price on premium dividend of payers

company. Further, the manager chooses not to pay the

dividend when the investors pefer non- payers to

payers company.

Their study has empirically proven that the

changes of dividend paid to shareholders can be

explained by looking at the market demand.

Specifically, the study reveals the relationship

between dividend premi and the company’s decision

to pay dividend. Besides, dividend premi can clarify

the phenomena of dividend lost because of the

changes of company’s characteristic (Fama & French,

2001). Fama & French (2001) pointed out that payers

companies are the companies that have great

profitability and size, and low market to book ratio

and asset growth. Baker & Wurgler (2004) stated that

investors’ sentiment influences a company with great

profitability and firm size. The relationship between

dividend and life cycle can be explained by the theory

of life cycle. This theory views that optimum

dividend policy issued by the company depends on

the life cycle of company. The more mature the

company, the higher the dividend payment will be.

The dividend payers are the mature companies that

have the high ratio of profitability for capital

contribution, while new companies usually have high

growth, so that, they do not pay dividend. It can be

concluded, mature companies with low growth will

have high probability to pay dividend and new

companies with high growth will have low

probability to pay dividend.

Firm Size

Firm Size illustrates whether the company is small or

big. The big and settled company have easy access to

the capital market to rise their funds with low cost.

Further, new and small companies will have many

difficulties to access the capital market (Marietta &

Sampurno, 2013). The ease of accessing the capital

market means the ability of a company to atrract

investors to invest. The new fund can motivate the

company to pay its duty that includes dividend

payment to the shareholders. Wang & Lin (2016)

found that firm size influences the probability of

propensity to pay dividend positively. The bigger the

company, the bigger the probability of company to

pay dividend will be. That is also supported by Baker

& Wurgler (2004), Fama & French (2001), and Utami

(2015).

H1: Size influences propensity to pay dividend

positively

Profitability

Profitability is defined as the ability of a company to

yield profit for the company. The greater the profit

yielded by the company, the greater the probability of

dividend shared will be. This aims at giving trust for

the investors (Utami, 2015). That is also supported by

Baker & Wurgler (2004), Fama & French (2001), Adi

& Kunci (2018), dan Situmorang (2017).

H2: Profitability has positive influence to propensity

to pay dividendd

Asset Growth

Growth is company asset, and it is used as operational

asset of the company (Marietta & Sampurno, 2013) .

Baker & Wurgler (2004a) illustrated that the higher

the asset growth of company, the lower probability of

company to pay the dividend will be. The growing

company needs much fund to develop the company in

the future. The company prefers keeping its profit to

paying dividend for shareholders as it is stated by

EBIC 2019 - Economics and Business International Conference 2019

346

Marietta & Sampurno (2013), Fama & French (2001),

Wang & Lin (2016), and Chahyadi (2010).

H3: Asset growth influences propensity to pay

dividend negatively

Market to Book Ratio

The high chance to invest encourages the company to

have the probability for paying fewer dividend.

Residual theory says that the company will pay the

dividend when they do not have beneficial chance of

investment (Utami, 2015). Fama & French (2001),

argued that the higher the market to book ratio for a

company, the lower the probability of a company to

pay dividend will be. This is also supported by Baker

& Wurgler (2004 a b), Rahmawati (2017), and

Tangjitprom (2013).

H4: Market to book ratio has negative influence to

propensity to pay dividend.

3 METHOD

This study was quantitative. Besides, its design was

casuality that might have cause and effect between

variables. The data for this study was secondary data

collected from the financial report of companies

recorded at Indonesia Stock Exchange from 2008 up

to 2017 and Indonesian Capital Market Directory

(ICMD). The samples were 546 companies with 4530

companies as units of observation.

The probability of propensity to pay dividend in

this study was measured by using dummy variables

that have value of 1(one) for the companies that pay

the dividend and 0 (zero) for the companies that do

not pay the dividend (Fama & French, 2001).

The independent variables in this study was

companies’ characteristics that include firm size,

profitability, asset growth and market to book ratio.

Firm size was measured by looking at the ranking

percentage; company percentage that have market

capital less or equal to the comapnies(Fama &

French, 2001), (Baker & Wurgler, 2004). Firm size is

formulated as follow: Firm size = % rank market

capitalization

Profitability was calculated by comparing profit

before tax to the total asset owned by a company

(Fama & French, 2001), (Baker & Wurgler, 2004).

The profitability is also formulated as follow :

Asset Growth is calculated based on the

relationship between total assets (t) minus total assets

before (t-1) to total assets before (t-1) (Fama &

French, 2001), (Baker & Wurgler, 2004). Asset

Growth is formulated as follow:

Market to book ratio is measured by comparing

market value equity plus book value of liability to

book value of asse (Baker & Wurgler, 2004). The

formula of Market to book ratio is written bellow

3.1 Data Analysis

3.1.1 Selection of Estimation Model

This study implemented qualitative respond

regression since the dependent variable used was

biner(Gujarati, 2013:172). There are three

approaches of qualitative respond regressions; they

are Linear Probability Model, Logit and probit.

The best estimation model can be done by

implementing these two ways

(1) requirement fulfilment 0 ≤ E (Yi │Xi) ≤ 1, and

(2) Normality test.

The Linear Probability Model was chosen as

estimation if model the two requirements above are

fulfilled. Further, the score should be between 0 and1;

and data was normally distributed. However, if one of

the requirements can not be met, the estimation model

that should be chosen was logit or probit model. Even

though those models can be implemented easily, but

there are some weaknesses; they are (1) upnormal

residual (galat ), (2) heteroskedasticity (3) the

possibility of Y value is not at the range of 0-1, and

(4) is usually low (Gujarati, 2013:175).

The model of logit estimation interprets the

results by using the value of odd ratio. While the

model of probit estimation interprets the results by

using standard normal table to transform the Z score

to the opportunity. Basically, the difference betwen

logit and probit is Logit means Cumulative standard

logistic distribution (F), while Probit means

Cumulative standard normal distribution (Φ).

However, those two models actually have the same

result

3.1.2 Reression Model

Regression analysis with logit model in Eviews 9 was

used in this study. The regeression equation used is

written bellow

The Influence of Company’s Characteristics to Propensity to Pay Dividend

347

Explanation:

PTPi = Dependent Variable (= 1 if the company

pay dividend and has 0 value, if the company does not

pay dividend)

Pi = probability of a company to pay dividend

X

1

= Firm size

X

2

= Profitability

X

3

= Asset Growth

X

4

= Market to book ratio

µi = error standard

Goodness-of-Fit Test

Feasibility Test can be done by two ways; they are

by looking at (1) Hosmer value and Lemeshow’s

Goodness-of-fit-test statistic, and (2) value of

McFadden R-Square (3) multicolinearity test

3.2 Hypothesis Test

In testing the hypothesis, Hα on the estimation of

logit or probit regression, and the estimation of

maximum likelihood (ML), not OLS were

implemented. The significance level applied was 0,05

(α= 5%). This means that researchers believed 100%

on samples. The probability of samples that did not

have the population’s characteristics was 5%. The

hypothesis, Hα was accepted if the significance value

was less than 5. This means that dependent variables

influences dependent variables

4 FINDINGS AND DISSCUSSION

Table 1. The Percentage of Payers Company

Year Payers Non-Payers Total Payers

2008 144 216 360 40.00%

2009 143 226 369 38.75%

2010 158 233 391 40.41%

2011 186 234 420 44.29%

2012 190 250 440 43.18%

2013 204 267 471 43.31%

2014 208 289 497 41.85%

2015 215 294 509 42.24%

2016 183 344 527 34.72%

2017 217 329 546 39.74%

Sources: The Processed Secondary Data

The above table illustrates the percentage of

companies that pay the dividend from 2008 to 2017.

The number of payers companies are fluctuated each

year. Generally, the trend decreases. The lowest

percentage was in 2014 which was amouted to

34.72% and the highest was in 2011 which reached

44.29%. The average percentage of payers company

from 2008 up to2017 was 40.85% and it could not

reach 50% of the total companies listed at Indonesia

Stock Exchange

4.1 Descriptive Statistics

Table 2. The descriptive Statistics of Variables

Varia

bel

Mea

n

Med

ian

Maxi

mum

Mini

mum

St

d.

D

ev

.

SIZE

0.09

9944

0.02

3

1

0.000

1

0.

18

48

59

PRO

F

0.00

2486

0.03

78

170.5

933

-

265.1

907

4.

98

72

6

GRO

WTH

16.2

8846

0.09

56

6576

7.7

-12.3

97

7.

96

95

MTB

2.43

99

1.09

01

885.0

296

0.004

5

18

.5

12

55

Sources: The Processed Secondary Data

Based on the data description, the growth of

companies under study have greater various data than

MTB, size and profitability.

Table 3. Hosmer and Lemeshow’s

H-L Statistic Prob. Chi-Sq(8)

263.2044 0.000

Source: The Processed Secondary Data

Table 3 shows that the value of H-L statistic is

263.204 with the significamce value less than 0.01 (

0.000<0.01). It can be said that the model is not

accepted ( the model is not fit), so that the above

indeppendent variables can not be used to estimate

the status of propensity to pay dividend.

EBIC 2019 - Economics and Business International Conference 2019

348

Table 4. McFaddenR-squared Testing

Dependent Variable: PTP

Method: ML- Binary Logit

McFadden R-squared 0.079457

LR statistic 486.7106

Prob (LR statistic) 0.0000

Source: The processed Secondary Data

Table 4 illustrates the value of McFadden R

Square that is at 0.079457. This means that

dependent variables can be explained by independent

variables, 7.94 %. Generally, all of independent

variables have significant impacts to propensity to

pay dividend as they are shown by the statistic of LR

value, 486.7106 with the probability of less than 5%.

4.2 Hypothesis Test

Based on table 5, it can be seen that all significance

values of independent variables are less than 5%

(α=0.05). This means that all firm size variables,

profitability, asset growth and market to book ratio

have significant impact to the probability of

propensity to pay dividend.

The coefficient of firm size and profitability are

positive. This means that the greater the firm size and

the profitability, the higher the probability of

company to pay dividend will be, and vice versa. The

asset growth coefficient and market to book ratio are

negative. This means that the probability of company

to paay dividend will be lower

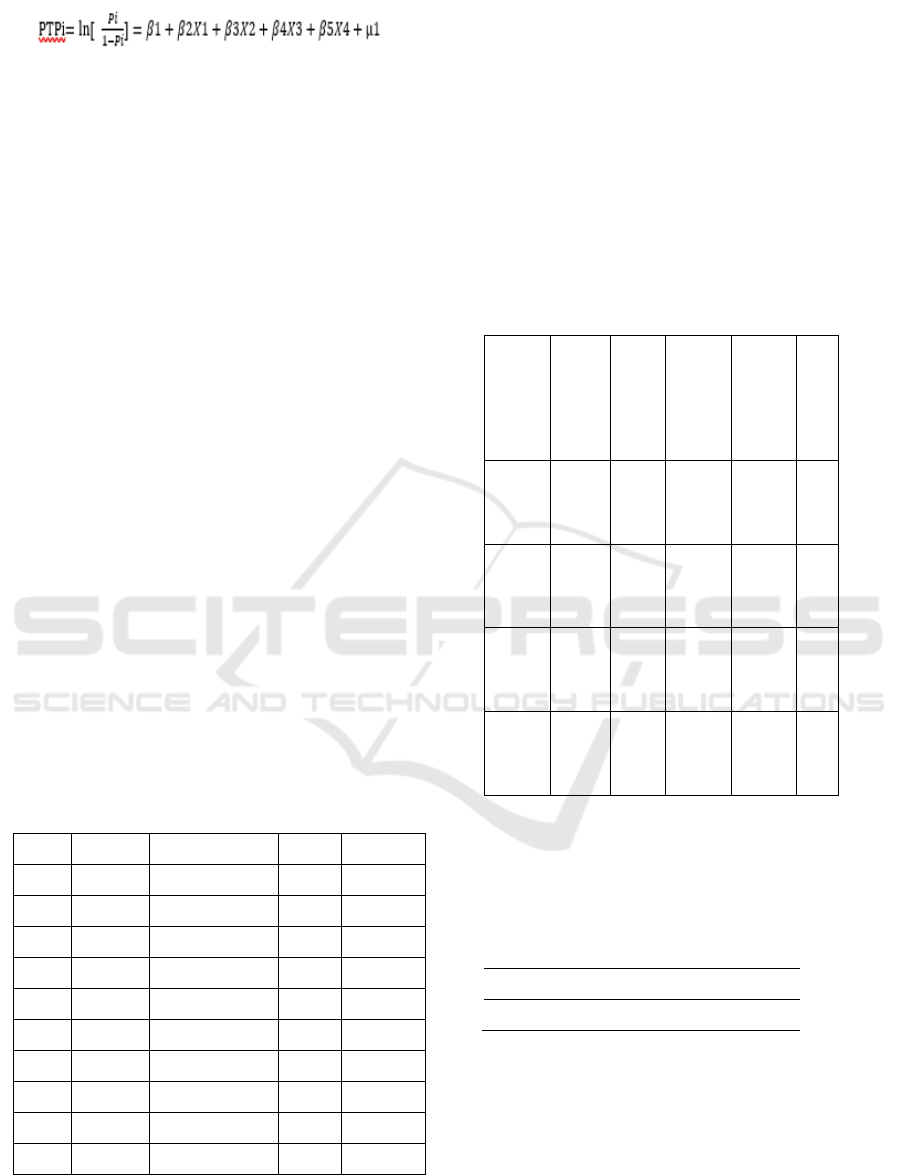

Table 5. The Result of Logit Regression

Variab

le

Coeffic

ient

Std.

Error

z-

Statis

tic

Pro

b.

Odd

Ratio/

Exp

(

β

)

SIZE

2.0672

2

0.200

43

10.31

383

0 7.9132

PROF

4.4663

2

0.335

91

13.29

611

0

87.281

8

GRO

WTH

-

0.1329

3

0.035

78

-

3.715

21

0.00

02

0.8755

MTB

-

0.1620

2

0.022

39

-

7.234

89

0 0.8503

C

-

0.5069

64

0.045

465

-

11.15

06

0 0.6021

Source: The Processed Secondary Data

Based on above table, a regresssion equation can

be formulated; and it is written as follow:

The interpretation of logit model equation uses

odd ratio or Exp(β) (See Table 5). From the equation,

it can be seen that the coefficient of firm size is

2.06722 with the odd ratio value of 7.9132. This

means the probability of company to pay the dividend

increases as many as 7.9132 times when there is a rise

of 1 unit on firm size.

Firm Size to Propensity to Pay Dividend

The findings show that firm size influences positively

and significantly to the probability of propensity to

pay dividend. The greater the firm size, the greater the

total assets will be. Further, the lower the investment

to meet the needs of asset, the greater the probability

of propensity to pay dividend will be. These findings

are in line with the researches conducted by Baker &

Wurgler (2004 a b), Elisabete & Neves (2018),

Tangjitprom (2013), and Utami (2015). The

companies with great total assets may have lower

possibility to purchase more asset. Then, the profit

can be allocated to the dividend share

Profitability to Propensity to Pay Dividend

The findings show that the profitability influences

the probability of propensity to pay dividend

positively and significantly. The higher the

profitability gained by a company, the higher the

probability of propensity to pay dividend. The aim is

for getting investors’ trust. This finding is in line with

Utami(2015), (Tangjitprom, 2013), Ferris,

Jayaraman, & Sabherwal (2009), and Denis &

Osobov (2008).

The company with high profitability is usually at

mature stage, so that, it does not need much fund for

investment. It will impact on the probability of higher

dividend payment

Asset Growth to Propensity to Pay Dividend

The finding shows that asset growth has negative and

significant impact to the probability of propensity to

pay dividend. The company with high growth needs

money to fund the growth of company in the future

both investment and expansion, so that, the

probability of company to share the dividend is low.

Those are also argued by Chahyadi (2010), Fama &

French (2001), Baker & Wurgler (2004), and

Simbolon & Sampurno (2017). A company with high

growth needs much fund for investment, so that, the

probability to pay the dividend is low

The Influence of Company’s Characteristics to Propensity to Pay Dividend

349

Market to book ratio to Propensity to Pay Dividend

The finding explains that market to book ratio of a

company influences the propensity to pay dividend

significantly and negatively. The higher the market to

book ratio of company, the lower the probability of

propensity to pay dividend. It is suitable with the

residual theory that says a company will pay the

dividend if it does not have an opportunity to have

beneficial investment. In other words, the companies

with high opportunites to expand will keep their

current asset as their profit will be kept and allocated

more for investment than dividend sharing as it is

stated by Fama & French (2001), Tangjitprom (2013),

and Ferris, Jayaraman, & Sabherwal (2009).

5 IMPLICATION

The greater the firm size, the higher the probality of a

company to pay dividend will be. The higher the asset

growth, and the market to book ratio of a company,

the lower the probaility of company to pay dividend

will be. These findings support Baker & Wurgler

(2004a) that is about trade-off. When the investor

will increase the value of a company at the market

because of dividend sharing, then, the company

should pay the dividend. However, if the investors

prefer non-payer to payer, then the company do not

need to pay the dividend. This study does not only

discuss how much dividend that should be paid, but

also the possibility of company to pay the dividend.

As trade-off matter, the company will consider the

characteristic of company

REFERENCES

Adi, A. R., & Kunci, K. (2018). Karakteristik Finansial dan

Kecenderungan Pembayaran Cash Dividen pada

Perusahaan di Bursa Efek Indonesia, 9(1), 1–12.

Baker, M., & Wurgler, J. (2004). A Catering Theory of

Dividends, LIX(3).

Baker, M., & Wurgler, J. (2004). Appearing and

disappearing dividends : The link to catering incentives

$, 73, 271–288.

https://doi.org/10.1016/j.jfineco.2003.08.001

Chahyadi, C. S. (2010). Not paying dividends ? A

decomposition of the decline in dividend payers,

(April). https://doi.org/10.1007/s12197-010-9132-0

Denis, D. J., & Osobov, I. (2008). Why do firms pay

dividends ? International evidence on the determinants

of dividend policy $, 88(1), 62–82.

https://doi.org/10.1016/j.jfineco.2007.06.006

Elisabete, M., & Neves, D. (2018). Payout and firm ’ s

catering. https://doi.org/10.1108/IJMF-03-2017-0055

Fama, E. F., & French, K. R. (2001). Disappearing

dividends : changing " rm characteristics or lower

propensity to pay ? ଝ, 60, 3–43.

Ferris, S. P., Jayaraman, N., & Sabherwal, S. (2009).

Catering effects in corporate dividend policy : The

international evidence. Journal of Banking and

Finance, 33(9), 1730–1738.

https://doi.org/10.1016/j.jbankfin.2009.04.005

Gujarati, D. N. dan D. C. P. (2013). Dasar-dasar

Ekonometrika. Jakarta: Salemba Empat.

Li, W., & Ã, E. L. (2006). Dividend changes and catering

incentives $, 80, 293–308.

https://doi.org/10.1016/j.jfineco.2005.03.005

Marietta, U., & Sampurno, D. (2013). Analisis Pengaruh

Cash Ratio , Return On Assets , Growth , Firm Size ,

Debt to Equity Ratio Terhadap Dividend Payout Ratio :

( Studi Pada Perusahaan Manufaktur Yang Terdaftar di

Bursa Efek Indonesia Tahun 2008-2011 ), 2(1999), 1–

11.

Nurhayati, M. (2013). Jurnal Keuangan dan Bisnis Vol. 5,

No. 2, Juli 2013, 5(2).

Rahmawati, C. H. tri. (2017). Pengaruh Set Kesempatan

Investasi dan Kepemilikan Manajemen terhadap

Pembayaran Dividen pada Perusahaan yang Terdaftar

di Bursa Efek Indonesia 37, (1), 37–48.

Simbolon, K., & Sampurno, D. (2017). Analisis Pengaruh

Firm Size , DER , Asset Growth , ROE , EPS , Quick

Ratio dan Past Dividend terhadap Dividend Payout

Ratio ( Studi pada Perusahaan Manufaktur yang

Terdaftar di BEI Tahun 2011- 2015 ), 6, 1–13.

Situmorang, A. . (2017). “ pengaruh profitabilitas, debt to

equity ratio , firm size , growth , dan cash ratio terhadap

devident payout ratio pada sektor barang konsumsi

yang terdaftar di bursa efek indonesia periode 2011-

2014 ,” 5.

Suranta, Eddy, et all. (2010). EFFECT OF DIVIDEND

CATERING THEORY TO THE COMPANY’S

DIVIDEND PAYOUT PROPENSITY. Malaysia-

Indonesia International Conference on Economics,

Management and Accounting, 25–26.

Tangjitprom, N. (2013). Propensity to pay dividends and

catering incentives in Thailand. Studies in Economics

and Finance

, 30(1), 45–55.

https://doi.org/10.1108/10867371311300973

Utami, G. K. dan R. (2015). ANALISIS FAKTOR-

FAKTOR YANG MEMPENGARUHI. Jurnal

Manajemen, 15(1), 41–58.

Wang, M., & Lin, F. (2016). Dividend policy and the

catering theory : evidence from the Taiwan Stock

Exchange. https://doi.org/10.1108/MF-05-2015-0132

EBIC 2019 - Economics and Business International Conference 2019

350