A STRATEGY FOR ACCEPTING ORDERS IN ETO

MANUFACTURING WITH COMPETITIVE BIDDING

Analysis of Bidding Strategy and Expected Profits via Multi-Period Operations

Nobuaki Ishii

1

and Masaaki Muraki

2

1

Faculty of Information and Communication, Bunkyo University, Namegaya, Chigasaki, Japan

2

Graduate School of Decision Science and Technology, Tokyo Institute of Technology, Ookayama, Meguro-ku, Japan

Keywords: Engineer-To-Order Manufacturing, Project-Based Manufacturing, Sustainable Company, Cost Estimation

Accuracy.

Abstract: In Engineer-To-Order manufacturing with competitive bidding, improving cost estimation accuracy is

necessary for the contractor to gain highly expected profits from accepted orders. Thus, it is critical to

maintain the number of human resources required for cost estimation. However, the human resources are

also required for execution of the accepted orders. Namely, in the Engineer-To-Order manufacturing, a

balance of common resources for cost estimation in yielding the future profits and for execution of the

accepted orders is essential for making a stable profit. In this paper, we build a mathematical model

describing relations among cost estimation accuracy, order acceptance, sales, and profits through multi-

period operations in consideration of characteristics of competitive bidding. Using our model, we analyse

the relations between the volume of human resources allocated for the cost estimation and the expected

profits from the accepted orders as well as the effect of a strategy for accepting orders on the expected

profits through multi-period operations.

1 INTRODUCTION

Nowadays, the importance of Engineer-To-Order

(ETO) manufacturing (Kolisch, 2001) or project-

based manufacturing (Project Management Institute,

2008), where a selected contractor designs and

builds unique products or services based on the

client requirements, such as construction, civil

engineering, plant engineering, industrial machinery,

is widely recognized in practice.

In ETO manufacturing, a contractor is usually

selected by a client through a competitive bidding

process (Friedman, 1956; Ioannou and Leu, 1993;

Rothkopf and Harstad, 1994). Namely, the client

prepares a Request For Proposal (RFP) for the order

and invites several potential contractors to the

bidding. The client usually evaluates contractors on

the basis of the multi-attribute bid evaluation

criteria, such as bidding price, past experience, past

performance, company reputation, and the proposed

method of delivery and technical solutions. Then,

the client basically selects the contractor who

proposes the lowest price if there is not much

difference in other criteria.

In ETO manufacturing, accordingly, it is

necessary for any contractor to decide the bidding

price based on accurate cost estimation. If the

contractor’s bidding price is set higher than that of a

competitor due to cost estimation error, the

contractor could fail to receive the order.

Conversely, if the cost estimation error results in an

underestimation of the cost, the contractor would be

granted the order; however, he would eventually

suffer a loss on this order.

Cost estimation, however, is a highly

intellectual task of predicting the costs of products

or services to be provided in the future based on the

analysis of the client’s requirements and their tacit

knowledge. So, experienced and skilled human

resources, i.e., MH (Man-Hour) of skilled engineers,

are required for accurate cost estimation. Those

resources, however, are limited in any company;

furthermore, once the orders are successfully

accepted, the corresponding orders will also need

considerable MH to carry them out successfully.

If the contractor eventually accepts too many

380

Ishii N. and Muraki M..

A STRATEGY FOR ACCEPTING ORDERS IN ETO MANUFACTURING WITH COMPETITIVE BIDDING - Analysis of Bidding Strategy and Expected

Profits via Multi-Period Operations.

DOI: 10.5220/0003620403800385

In Proceedings of 1st International Conference on Simulation and Modeling Methodologies, Technologies and Applications (SIMULTECH-2011), pages

380-385

ISBN: 978-989-8425-78-2

Copyright

c

2011 SCITEPRESS (Science and Technology Publications, Lda.)

orders during a particular period and cannot

maintain the sufficient MH for estimating cost

accurately at the following periods to carry out the

accepted orders, the profits of orders to be accepted

at the following periods would decrease because the

probability of accepting lower profit orders increases

according to the decrease of cost estimation

accuracy in competitive bidding. Thus, the

contractor suffers unstable and low profits during

several periods.

For these reasons, it is important to realize the

appropriate balance of available MH for the cost

estimation and execution of accepted orders to result

in a stable profit through successive multi-period

operations. However, most of the literature dealing

with ETO manufacturing has assumed that the

contractor can select orders according to his criteria

by the contractor’s initiative without competitive

bidding. In practice, however, the contractor

basically offers a bidding price in competitive

bidding and then receives the order by the client’s

decision. In addition, most literature on the

competitive bidding does not consider the relations

between the cost estimation accuracy associated

with the cost estimation MH and the expected profits

from the accepted orders.

In this paper, we analyse the relations among

cost estimation MH, order acceptance, and expected

profits through successive multi-period operations in

competitive bidding by using the Multi-Period Order

Acceptance (MPOA) and Profit model. In addition,

we discuss tools and techniques required to make a

stable profit and assure sustainability in ETO

manufacturing.

2 A MODEL OF COMPETITIVE

BIDDING PROCESS

There are several ways to select a contractor in

competitive bidding (Elfving et al., 2005; Helmus,

2008; Wang et al., 2009). In a generic competitive

bidding process, shown in Figure 1, the client

prepares RFP, and invites several potential

contractors to the bidding. The contractor first

carries out the preliminary analysis followed by the

bid or no-bid decision. In the preliminary analysis,

the contractor evaluates the RFP and estimates the

preliminary cost based on limited information such

as the order information included in the RFP and the

past project data of the contractor. In the bid or no-

bid decision, the contractor evaluates the order from

the viewpoints of profitability, technical feasibility

and so on, and makes a decision whether to bid or

not. If the contractor decides to place the bid, then

he starts the bidding price decision process, that is,

he estimates the cost more accurately and determines

the bidding price. At the end of the competitive

bidding, the client assesses the proposals offered by

contractors and selects a contractor as the successful

bidder. The selected contractor carries out the

accepted order using his resources.

Figure 1: An overview of competitive bidding and

execution of accepted orders.

3 MODELS OF ORDER

ACCEPTANCE AND PROFITS

IN ETO MANUFACTURING

3.1 A Cost Estimation Accuracy Model

Since the cost estimation requires a detailed analysis

conducted by experienced engineers, it can be seen

that the volume of MH for cost estimation affects the

cost estimation accuracy significantly. In fact,

Towler and Sinnott (2008), Gerrard (2000) suggest

that the cost estimation accuracy is positively

correlated with the volume of cost estimation MH. It

is also clear that the marginal rate of cost estimation

accuracy approaches zero according to the increase

of the volume of MH. Thus, in this paper, we define

the cost estimation accuracy (σ) as the function of

the cost estimation MH per order (PMH) based on

the logistic curve as follows:

min max

max min max

()

()

CPMH

PMH

e

σ

σ

σ

σσσ

−⋅

⋅

=

+−⋅

(PMH > 0.0)

(1)

where

σ

min

, σ

max

, and C are the minimum and the

maximum value of the standard deviation of the

bidding price or the order execution cost (OEC), and

a parameter of the logistic curve. These parameters

could be determined from the past records.

- Preparation of

Request For

Quotation (RFQ)

- Bid Evaluation

- Contractor

Selection

Preliminary

Evaluation

Bid or No-Bid

Decision

Bidding Price

Decision

Declination

of bid

- Past project data

- Competitive

environment

- Target total expected

orders

- Target profit rate

Preliminary cost

Bid

No-Bid

Bid reply

Order

Acceptance

Contractor selection

Preliminary cost

ContractorClient

Request For

Proposal (RFP)

Preparation of

Proposal &

Cost Estimation

Cost Estimation

MH

Estimated

Cost

Execution of

Accepted

Order

Products or Services

A STRATEGY FOR ACCEPTING ORDERS IN ETO MANUFACTURING WITH COMPETITIVE BIDDING - Analysis

of Bidding Strategy and Expected Profits via Multi-Period Operations

381

3.2 A Multi-Period Order Acceptance

and Profit Model

In this paper, as shown in Figure 2, we set the target

volume of orders (TCT

i

), and calculate the expected

total revenue (ER

i

), the expected total cost (EC

i

), the

expected total profits (EP

i

) of each i-th period using

the MPOA and Profit model based on the following

assumptions. EC

i

consists of materials and labour

cost, outsourcing MH cost, and fixed cost consisting

of in-house MH cost and overhead cost.

Model Assumptions:

MH can be divided into regular engineers’ MH

and senior engineers’ MH,

MH of a certain percentage or more must be senior

engineers’ MH for executing the accepted

orders,

Only senior engineers can estimate cost, and no

outsourcing MH is available for the cost

estimation.

Namely, we calculate ER

i

, EC

i

, and EP

i

,

repeatedly from the 1

st

to fp (>1) periods, based on

the accepted order data until the i-th period, such as

the number of orders satisfying TCT

i

and the cost

estimation accuracy at the i-th period. In addition,

we evaluate the cost estimation accuracy based on

the number of orders and the total cost estimation

MH (

est

i

TMH

) obtained by subtracting total order

execution MH (

exe

i

TMH

) from the total MH available

at the i-th period. We present the detailed

explanation of the model in APPENDIX.

Figure 2: An overview of Multi-Period Order Acceptance

(MPOA) and Profit model.

4 MODELS OF ORDER

ACCEPTANCE AND PROFITS

IN ETO MANUFACTURING

4.1 Cost Estimation Accuracy and

Expected Profit

We analyse the relations among cost estimation MH,

cost estimation accuracy, and expected profit based

on the case data shown in Table 1. Namely, we

calculate the cost estimation accuracy by Eq. (1), the

expected value of accepted order by Eq. (2), and the

expected profit by subtracting the OEC from the

expected order.

1

1

11111 1

0

2

1

0

2

(, , ) ( , , )

(, , )

n

kk k k k

x

awd

k

n

kk k k k

x

k

x

px p x dx dx

EPT

p x dx dx

μσ μσ

μσ

+∞ +∞

=

+∞ +∞

=

⋅

⋅⋅

=

⋅

∏

∫∫

∏

∫∫

(2)

where k is the contractor (k =1: his own company, k

>=2: competitors), p

k

(x

k

, μ

k

, σ

k

) is the probability

density of the bidding price (x

k

) of the contractor

(k), and its average value and standard deviation are

μ

k

and σ

k

(cost estimation accuracy), respectively. As

shown in Eq. (2), the expected value of the accepted

order is the average value of one’s own company’s

bidding price falling below those of all other

competitors (k>=2).

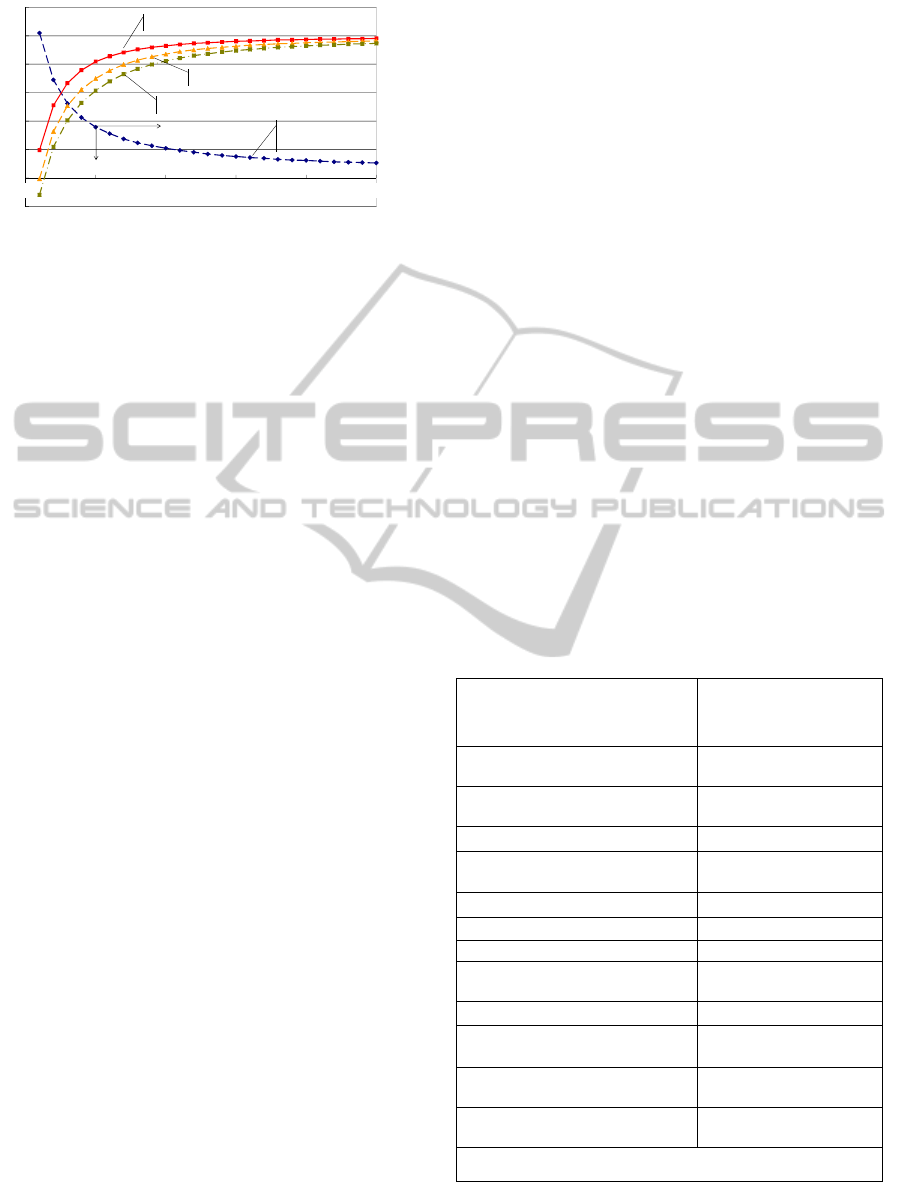

Figure 3 shows the results of the calculations.

We can see that the higher accuracy of cost

estimation, i.e., lower deviation, increases the

expected profits. The expected profits decrease

according to the increase of the number of

competitors. Namely, we can conclude that the

probability of accepting lower profit order increases

according to the decreasing cost estimation MH and

cost estimation accuracy. On the other hand, the

contractor can expect improved profit by investing

MH for the cost estimation under the severe

competitive environment with many competitors.

Table 1: Case data for evaluation of cost estimation

accuracy and expected profit.

The number of bidders

(n)

2 or 3 bidders including one’s

own company

Probability density of the

bidding price

Normal distribution

Order execution cost

(OEC)

100 [MM$/Order]

Parameters of Eq. (1)

σ

min

:0.5% of OEC, σ

max

:

20% of OEC, C:0.25

Parameters of Eq. (2)

μ

k

(including profit): 110, σ

k

(k>=2): 5 [MM$ ]

Calculate ER

i

Accepted order

data until the i-th

period

Calculate EC

i

Calculate EP

i

Calculate

Calculate

the Volume of Orders

Total in-house MH (MH

s

)

TCT

i

The number of bidders

Competitors’ cost estimation accuracy

i = i + 1

ER

i

EC

i

EP

i

Start

i =1

i <= fp Stop

exe

i

TMH

est

i

TMH

Ye s

No

SIMULTECH 2011 - 1st International Conference on Simulation and Modeling Methodologies, Technologies and

Applications

382

Figure 3: Relations among cost estimation MH, cost

estimation accuracy, and expected profits.

4.2 Multi-Period Evaluation on Order

Acceptance and Expected Profits

We analyse the relations between the order

acceptance and the expected profits through

successive multi-period operations using the MPOA

and Profit model, shown in Figure 2 and

APPENDIX. Table 2 shows the conditions of a

model company for this analysis.

We use two scenarios to compare profits based

on two different strategies for accepting orders, i.e.,

the high-order strategy (Case A), and the stable-

order strategy (Case B). The contractor tries to get

orders as many orders as possible at every period

under the high-order strategy. In contrast, the

contractor controls the volume of accepted orders at

a certain level via a multi-period basis in the case of

stable-order strategy. Namely, in Case A, the

volume of the order acceptance is set to 1,800

[MM$] at the 3

rd

period and to 1,200 [MM$] at other

periods. In Case B, the volume of the order

acceptance is set to 1,800 [MM$] at the 3

rd

period, to

600 [MM$] at the 4th period, and to 1,200 [MM$] at

other periods, to control the accepted orders through

entire periods as the 1,200 [MM$/Period] level.

Figures 4 and 5 show the orders, revenues, and

total costs over the periods, respectively, in Cases A

and B. In addition, Figure 6 shows a comparison of

profits in Case A and Case B over the periods.

As shown in Figures 4 and 6, in Case A, the

increased accepted orders at the 3

rd

period improves

revenues of the following three periods. Profits also

increase at the 4

th

period. However, profits start

decreasing from the 5

th

period, and it takes seven

periods to recover the profits at the 3

rd

period level.

If the same profit levels are maintained at the same

level of those of the 3

rd

period for 12 periods, the

total profits are 335 [MM$]. However, the increased

accepted orders at the 3

rd

period reduce profits

during the 6

th

to the 12

th

periods, and the total profits

for 12 periods are 190 [MM$] in Case A. In contrast,

as shown in Figures 5 and 6, the total profits for 12

periods are 318 [MM$] in Case B. The decline in

profits after the 4

th

period in Case A occurred

because of the reduced cost estimation MH by the

increased MH requirements for executing the orders

accepted at the 3

rd

period. Namely, the reduced cost

estimation MH decreases the cost estimation

accuracy, and thus the profits are reduced as

presented in the previous section. In Case B, since

the order acceptance at the 4

th

period is controlled,

and cost estimation MH is sufficiently maintained to

estimate cost accurately, the loss of profits is

reduced in comparison to that of Case A.

We can conclude based on these observations

that the strategy for accepting an adequate volume of

orders via multi-period operations is effective to

avoid decreasing cost estimation MH and cost

estimation accuracy, and thus a stable profit is the

end result.

Most contractors, in practice, tend to take a high-

order strategy. However, this strategy could reduce

cost estimation accuracy and reduce profits as

presented in this section. Namely, contractors in

ETO manufacturing should establish a strategy for

accepting orders in consideration of the balance of

MH for the cost estimation and execution of the

accepted orders via multi-period operations.

Table 2: Conditions of model company.

Rate of the i-th period revenue

on the accepted orders at the j-

th period (

j

i

ROER

)

0.333

The number of bidders (n)

including one’s own company

3 bidders

Periods for sales of accepted

order (NST)

3 Successive periods

Evaluation period -2 (1-NST) to 12

Probability density of the

bidding price

Normal distribution

Order execution cost (OEC) 100 [MM$ /order]

Rate of profit (ROP)

10%

Rate of MH cost (α

1

) 10%

Rate of materials & labour cost

(α

3

)

80%

Total in-house MH (MH

T

)

1,100 [M MH/period]

In-house senior engineer MH

(MH

S

)

440 [M MH/period]

Rate of senior engineer MH for

carry out orders (α

2

)

30%

In-house and out sourcing MH

rate (β

1

, β

2

)

100 [$/MH]

Parameters of Eq. (1) and Eq. (2) are shown in Table 1.

-2

0

2

4

6

8

10

12

00.511.522.5

Expected Profit per Order [MM$]

Cost Estimation MH [M MH/Order]

50 10 15 20 25

Cost Estimation

Accuracy

Expected Profit (Two Competitors)

Expected Profit (Three Competitors)

Expected Profit (Four Competitors)

1

2

0

Cost Estimation Accuracy [σ]

High

Low

A STRATEGY FOR ACCEPTING ORDERS IN ETO MANUFACTURING WITH COMPETITIVE BIDDING - Analysis

of Bidding Strategy and Expected Profits via Multi-Period Operations

383

Figure 4: Orders, revenues, and costs over the periods

(Case A).

Figure 5: Orders, revenues, and costs over the periods

(Case B).

Figure 6: Comparison of profits (revenue-total cost of each

period) in Case A and Case B over the periods.

5 CONCLUSIONS

In this paper, we analyse the relations among cost

estimation MH, order acceptance, and expected

profits through successive multi-period operations in

ETO manufacturing with competitive bidding by

using the Multi-Period Order Acceptance (MPOA)

and Profit model.

Namely, we reveal that the cost estimation

accuracy affects the expected profits from the

accepted orders, and the contractor needs to

maintain MH for cost estimation to make a stable

profit through successive multi-period operations in

ETO manufacturing. Furthermore, we show that

accepting too many orders by the high-order strategy

decreases the expected profits at the following

periods. This is because the contractor needs more

MH to carry out the accepted orders, and thus the

MH for cost estimation at the period is reduced, and

then the low cost estimation accuracy results in the

low expected profits from the accepted orders based

on the estimation in competitive bidding.

For these reasons, we conclude that the

contractor should manage the volume of accepting

orders in consideration of the MH allocation for the

cost estimation and the execution of accepted orders

through successive multi-period operations, such as

the stable-order strategy to make a stable profit.

There are several issues which require further

research. For example, the strategy for accepting

orders effectively to maximize expected profits

through successive multi-period operations in ETO

manufacturing with competitive bidding should be

examined in detail. The bidding price decision

process to maximize the expected profits with MH

constraint should also be established. In addition,

tools and techniques to support the strategy and the

bidding process should be studied and implemented

in practice.

REFERENCES

Elfving, J. A., Tommelein, I. D., Ballard, G., 2005.

Consequences of competitive bidding in project-based

production. Journal of Purchasing & Supply

Management. 11 (4), 173-181.

Friedman, L., 1956. A competitive-bidding strategy. The

journal of the operations research society of America,

4 (1), 104-112.

Gerrard, A. M., 2000. Guide to Capital Cost Estimating.

Institute of Chemical Engineers. Warwickshire, 4th

edition.

Helmus, F. P., 2008. Process plant design: project

management from inquiry to acceptance, Wiley-VCH.

Weinheim.

Ioannou, P. G., Leu, S. S., 1993. Average-bid method –

competitive bidding strategy. Journal of constriction

engineering and management, 119 (1), 131-147.

Kolisch, R., 2001. Make-to-order Assembly Management,

Springer-Verlag. Berlin.

Project Management Institute, 2008. A guide to project

management body of knowledge, Project Management

Institute. PA, 4th edition.

Rothkopf, M. H., Harstad R. M., 1994. Modeling

competitive bidding: A critical essay. Management

Science, 40 (3), 364-384.

1,000

1,200

1,400

1,600

1,800

2,000

123456789101112

Period

Orders

Revenue

Tot al Cost

[MM$]

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

123456789101112

[MM$]

Period

Orders

Revenue

Total Cost

-40

-30

-20

-10

0

10

20

30

40

50

60

123456789101112

Expected Profit [MM$]

Period

Case A

Case B

SIMULTECH 2011 - 1st International Conference on Simulation and Modeling Methodologies, Technologies and

Applications

384

Towler, G., Sinnott, R., 2008, Chemical Engineering

Design Principles, Practice and Economics of Plant

and Process Design. Elsevier. MA.

Wang, J., Xu, Y., Li, Z., 2009. Research on project

selection system of pre-evaluation of engineering

design project bidding. International Journal of

Project Management, 27 (6), 584-599.

APPENDIX

EP

i

, ER

i

, and, EC

i

at the i-th period are determined

as follows:

iii

ECEREP −=

(A1)

∑

−

−=

⋅=

1i

NSTij

i

jji

ROERTCTER

(A2)

∑

−

−=

+⋅+⋅⋅⋅=

1

23

i

NSTij

i

i

jji

FCOSROERNAPOECEC

βα

(A3)

where

NST is the periods for sales of the accepted

order;

i

j

ROER

is the rate of the i-th period revenues on

the accepted orders at the j-th period;

α

3

is the rate

of materials & labour cost; OEC is the order

execution cost determined by Eq. (A4); NAP

j

is the

positive real value meaning the number of orders

satisfying

TCT

j

at the j-th period; β

2

is the out

sourcing MH rate; OS

i

is the out sourcing MH

determined by Eq. (A5); and FC is the fixed cost.

Since NST is the same positive integer for all orders

in this model,

i

j

ROER

is determined as

NSTROER

i

j

/1=

.

)1/(

1

ROPOEC +=

μ

(A4)

T

est

i

exe

ii

MHTMHTMHOS −+=

(A5)

s.t. OS

i

=0 in case of

T

est

i

exe

i

MHTMHTMH ≤+

where μ

1

is the bidding price without cost estimation

error; ROP is the rate of profit;

exe

i

TMH

is total order

execution MH at the i-th period as determined by

Eq. (A6);

est

i

TMH

is the total cost estimation MH at

the i-th period as determined by Eq. (A7); and MH

T

is the total in-house MH at the i-th period.

∑

−

−=

⋅⋅⋅=

1

11

/

i

NSTij

i

jj

exe

i

ROERNAPOECTMH

βα

(A6)

exe

iS

est

i

TMHMHTMH ⋅−=

2

α

(A7)

s.t.

0=

est

i

TMH

in case of

exe

iS

TMHMH ⋅≤

2

α

where α

1

is the rate of MH cost, β

1

is the in-house

MH rate; α

2

is the rate of senior engineer MH to

carry out orders.

NAP

j

is determined by the Eq. (A8):

awd

jjj

EPTTCTNAP /=

(A8)

where

awd

j

EPT

is the expected value of accepted

order determined by Eq. (2).

In the Eq. (2), σ

1

is determined by Eq. (1) as the cost

estimation accuracy at PMH

j

determined by Eq.

(A9).

j

est

jj

NPTMHPMH /=

(A9)

where NP

j

is the positive integer showing the

number of bidding orders which maximizes the

expected profit at TCT

j

condition.

A STRATEGY FOR ACCEPTING ORDERS IN ETO MANUFACTURING WITH COMPETITIVE BIDDING - Analysis

of Bidding Strategy and Expected Profits via Multi-Period Operations

385