Green Innovation as Implementation of Sustainability Development

in Indonesia

Dian Agustia, Tjiptohadi Sawarjuwono and Wiwiek Dianawati

Universitas Airlangga, Indonesia

dian.agustia@feb.unair.ac.id

Keywords: Green Innovation, Sustainability Development, Firm Value.

Abstract: This research is conducted to examine the application of green innovation as implementation of Sustainability

Development in Indonesia and to know the effect of green innovation to firm value. Green innovation will

increase the firm value, increase the economic benefits, and improve the competitiveness of the company

which will ultimately help the company to reach the point of sustainability. The data used are secondary data

that is company's annual report and PROPER report of manufacturing sector and main sector listed on IDX

year 2012-2015. Sample determination was done by sampling technique with certain criteria and was obtained

277 companies. Independent variable in this research is green innovation measured by content analysis. The

dependent variables are firm values measured using Tobins Q. This study also discusses the application of

green innovation as implementation of sustainability development in Indonesia. The result of this study

indicates that green innovation has positive effect on firm value.

1 INTRODUCTION

Sustainability development is a long-term

development and taking into account the interests of

future generations by trying to use resources

adequately and create healthy environment.

Environmentalists are now beginning to change their

lifestyles as an effort to reduce environmental

damage. They are beginning to shift from consuming

unsustainable products to more environmentally

friendly products (green product). This is due to

increased awareness and acknowledgement that one

of contributors to environmental damage is product

that cannot be reused or recycled.

Green innovation is one of the environmental

strategies that can be undertaken to develop a

business without violating government regulations

(Özşahin et al., 2013). An innovative green product

innovation strategy will encourage companies to have

special capabilities that will ultimately be a source of

corporate competitive advantage (Sharma and

Vredenburg, 1998). This competitive advantage will

increase the value of the company in the future (Bech,

2013). High corporate productivity will increase

company's profit margin and will help companies to

grow faster and enhance the competitiveness of

companies that will ultimately help companies to

achieve sustainability.

Based on the description of background above,

problems in this study can be formulated as follows:

How is application of green innovation as

implementation of Sustainability Development

in Indonesia?

Does green innovation affect firm value in

public companies in Indonesia?

2 LITERATURE REVIEW

2.1 Sustainability Development

Resources available in nature are limited in number,

while human needs are endless. More effort is needed

to maintain environmental sustainability. There are

four important components in establishing

environmental sustainability namely economic

stability, social stability, environmental stability, and

culture stability (Scrimgeour and Iremonger, 2011).

In running the business process, a company must

be able to generate economic benefits as much as

possible according to its main objectives, but the

company must also be able to provide welfare for the

364

Agustia, D., Sawarjuwono, T. and Dianawati, W.

Green Innovation as Implementation of Sustainability Development in Indonesia.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 364-369

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

people around the plant and able to maintain

environmental sustainability.

2.2 Green Innovation

Innovation is an important thing for companies to

develop business processes. Innovation can be the

tool that will deliver the company to gain certainty of

sustainability. Green innovation or environmental

innovation is a new or modified technique, practice,

system and production process to reduce the impact

of environmental damage (Rennings and Rammer,

2009). Green innovation is also defined as new

technology (hardware or software) related to products

or production processes that will lead to energy

efficiency, pollution reduction, waste recycling,

green product design, and corporate environmental

management (Ar, 2012). Green innovation not only

aims to improve firm performance economically, but

also to reduce the negative impact on the environment

and create a competitive advantage for the company.

Another advantage of green innovation is to

encourage companies to convert waste production

into a product that is worth selling so that it can

generate additional profits for the company.

2.3 Firm Value

The main objective of the company is to maximize

the company's wealth or value for shareholders or

owners (Ross et al., 2008: 9). Value of company is

investors' perceptions of the company's success rate.

For companies that have gone public, the value of the

company can be reflected through the company's

stock price, while for the company that has not gone

public its value is reflected through the realizable

value of the company's assets at the time the company

will be sold (Margaretha, 2005: 1). High stock prices

make value of the company also high. High value of

the company will make the market believe not only in

company's current performance but also on future

prospects of the company.

In general, company value can be measured by

market value ratio. The market value ratio is the ratio

that correlates the firm's share price with its profit and

with the book value of the company (Margaretha,

2011: 27). This ratio gives an indication to

management relating to investors' opinions about past

corporate achievements and future prospects.

3 RESEARCH METHOD

3.1 Research Approach

The research approach used in this research is

quantitative approach. The method used in this

research is at the level of explanation. This study

identifies the relationship between application of

Green Innovation as implementation of Sustainability

Development in Indonesia and firm value.

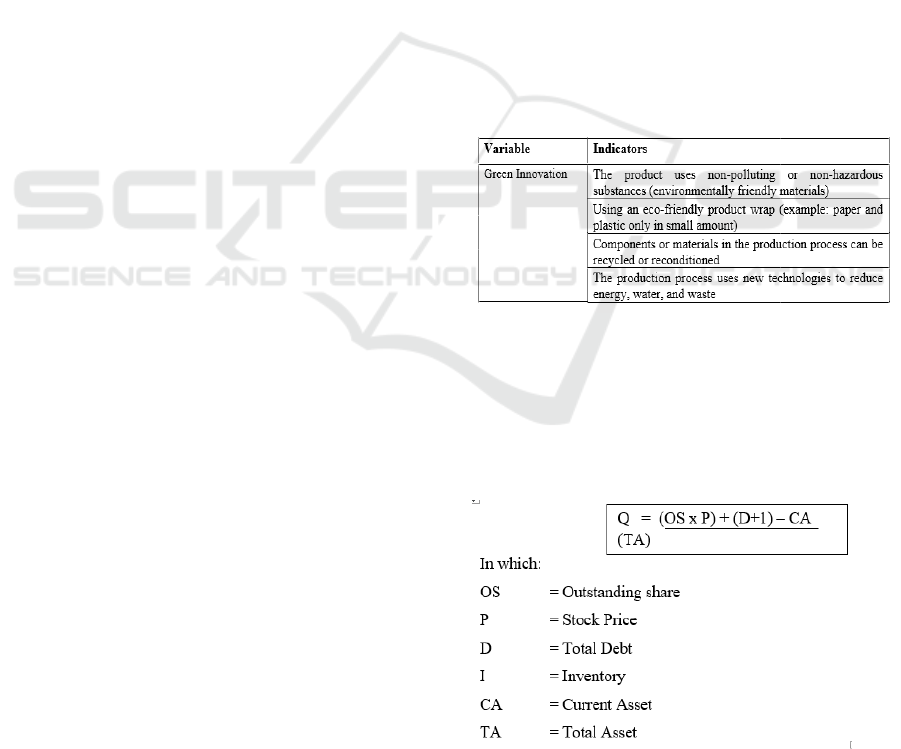

3.2 Operational Definitions

The independent variable in this research is Green

Innovation (X). In this study, green innovation is a

variable obtained through content analysis in the

company's annual report. Some indicators will be

used to determine whether the company has applied

green innovation. The study was conducted by Ar

(2012) and Qamarullah and Dorina (2015). The

indicators to be used in content analysis are as

follows:

Table 1: Variable assessment indicator.

Dependent variable in this research is firm value.

Firm value is stakeholder perception, especially

investors to company’s success rate which is

associated with stock market price and measured by

percentage. Firm value in this research is measured

by using Tobins'Q ratio. Tobin's Q Ratio is calculated

by the following formula (Chang and Wang, 2007):

Green Innovation as Implementation of Sustainability Development in Indonesia

365

3.3 Population and Sample

The population in this research is companies in the

manufacturing sector and the main sector listed in

Indonesia Stock Exchange (IDX) starting from 2012-

2015 which are as many as 287 companies.

Determination of sample in this research is done by

using certain consideration. The prescribed criteria

are as follows: a. The annual reports of manufacturing

and main sector companies are published on the

Indonesia Stock Exchange from 2012 to 2015 and

register PROPER programs for three consecutive

years. b. Companies in manufacturing sector and

main sector present complete and related data to the

research variables.

Out of 287 companies that publish the financial

statements in IDX since 2012 until 2015, there are

277 companies that meet the criteria set.

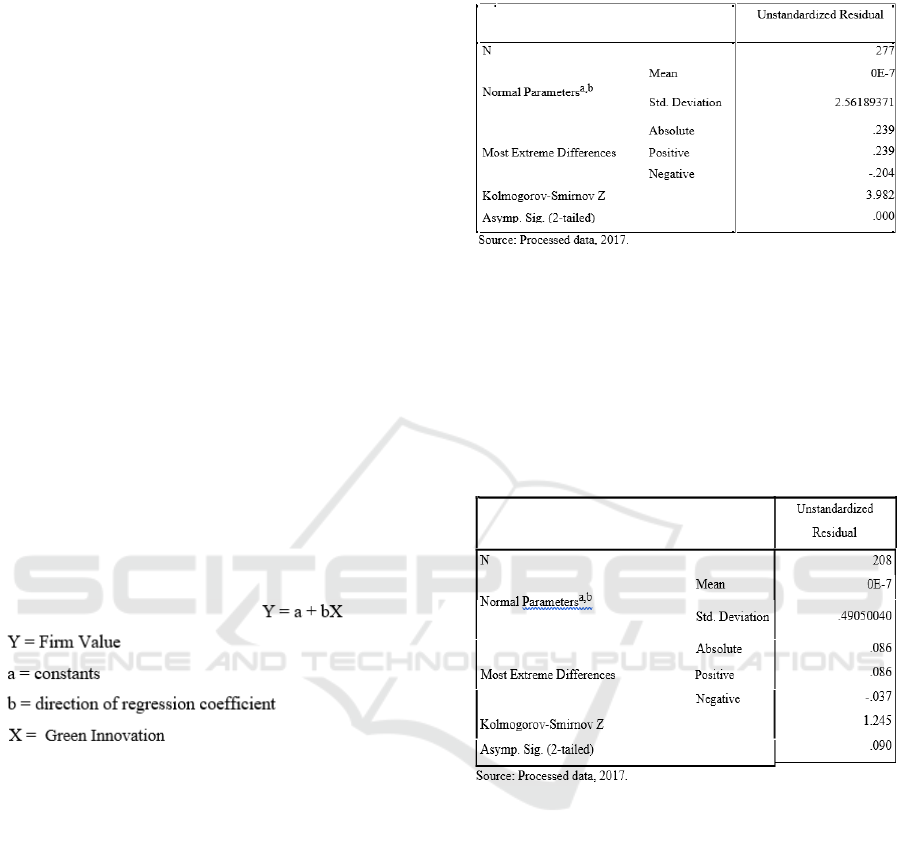

3.4 Analysis Technique

This descriptive statistic will be used to describe

statistically the variables in this study. Normality test

in this study is using Kolmogorov-Smirnov test. In

Kolmogorov- Smirnov test if significance > 0.05 then

the data is normally distributed (Ghozali, 2013: 164).

The equation obtained from simple regression

result is:

4 RESULTS AND DISCUSSION

4.1 Model Analysis

This study uses a simple regression model. Normality

test is done by using Kolmogorov-Smirnov test by

looking at the level of significance. The residual is

otherwise normally distributed if the significance

value of Kolmogorov-Smirnov > 0.05. Normality test

result is shown in table 2 below:

Table 2: Normality test result on initial data one-sample

Kolmogorov-Smirnov test.

The result of normality test in table 2 shows that

the value of Kolgomorov-Smirnov is 3,982 and

asymp. Sig. (2-tailed) of 0.000. This indicates that

the distribution of data is not normal. Therefore, it is

necessary to normalize the data by eliminating the

outlier value of the data by doing the elimination of

data that has the highest residual value.

Table 3: Normality test result on final data one-sample

Kolmogorov-Smirnov test.

Normality test results after normalization of data

has been presented in Table 3. The result of normality

test shows that the value of Kolgomorov-Smirnov

was 1,245 and asp. Sig. (2-tailed) of 0.090. Therefore,

it can be concluded that the residual data of both

models has been normally distributed as indicated by

the value of asymp. Sig. (2-tailed)> 0.05 or said to be

significant.

4.2 Hypothesis Proof: Effect of Green

Innovation on Firm Value

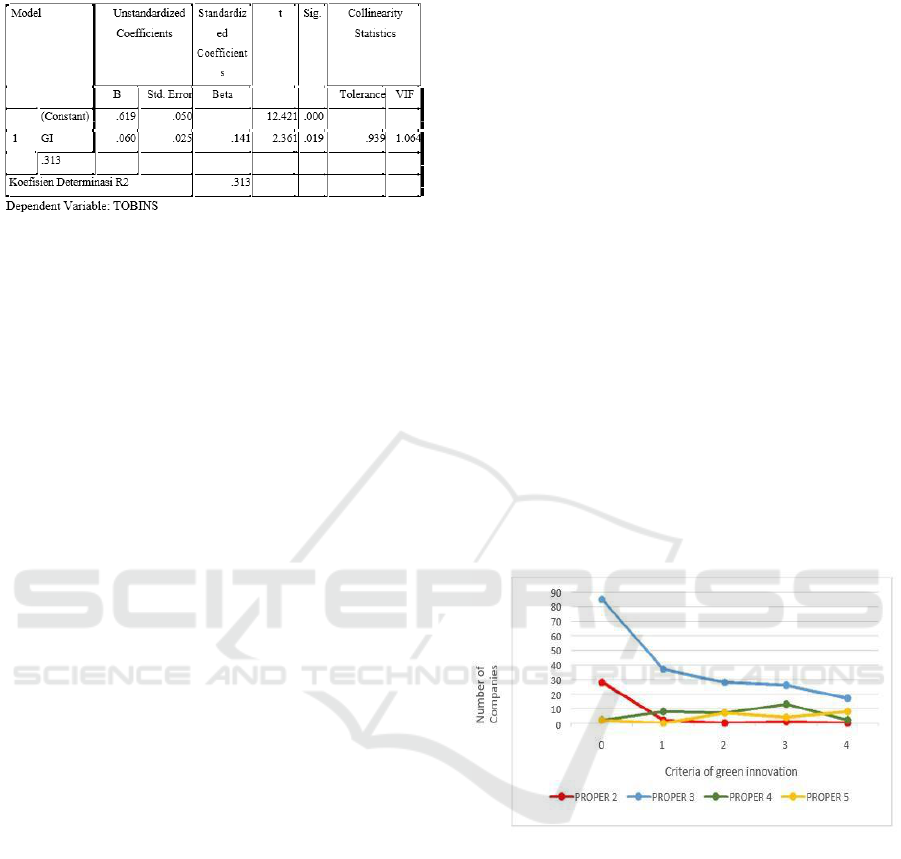

Table 4 below is the result of multiple linear

regression for model 1:

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

366

Table 4: Results of linear regression analysis coefficients.

ACKNOWLEDGEMENTS

If any, should be placed before the references section

without numbering.

From result of data analysis, hence result of

structural equation is as follows:

Firm Value = 0.619 +0.141 GI +e

Based on the result in Table 4.3, it can be

concluded that green innovation has significant effect

on firm value. It can be seen based on the value of

green innovation significance of 0.019 which is less

than the significance level of 0.05. The positive sign

on the beta coefficient of 0.141 indicates that green

innovation positively affects the firm value. Test of

Coefficient of Determination (R2) generates result of

.313 or 3.13%. With this result, it can be concluded

that is firm value is able to explain independent

variable of green innovation equal to 3.13%.

4.3 Discussion

4.3.1 Green Innovation as Implementation

of Sustainability Development in

Indonesia

Subject of this research is companies in the

manufacturing sector and the main sector listed on the

Indonesia Stock Exchange (IDX) and follow the

Program Performance Rating Company in

Environmental Management (PROPER) in the period

of observation in 2012 until 2015.

According to the Regulation of the Minister of

Environment Number 18 year 2012, PROPER ratings

are grouped into 5 ranking colors with 5 categories,

where each rating reflects the company's

performance. The best structuring performance

sequentially is Gold (PROPER 5) and Green

(PROPER 4); Blue (PROPER 3), given to the

business that have undertaken environmental

management efforts in accordance with the

requirements as stipulated in the regulation. Then Red

(PROPER 2), while the worst environmental

performance is black. Gold (PROPER 5), awarded to

a business that has consistently demonstrated

environmental excellence in the production and/or

serving process, conducting ethical business, and is

responsible to the community.

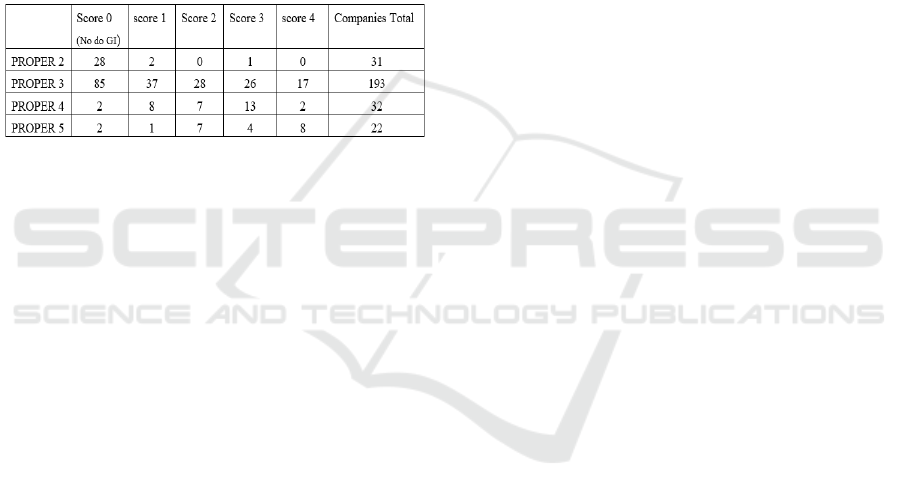

Based on the results of research in table 4.1, Green

innovation has the lowest value of zero (0) which

means the company has not made innovations or

renewal activities in order to reduce the impact of

environmental damage, both in terms of operational

processes and the final product. There are 117

companies that have not done green innovation or

equal to 42.23% of the total samples. The highest

value of green innovation is 4 which means the

company has fulfilled all criteria in doing green

innovation both for the process and final product. The

company that has done the perfect green innovation

is PT. Semen Indonesia Tbk, PT. Medco Energy Tbk.,

PT. Holcim Indonesia Tbk., PT. Pelat Timah

Nusantara Tbk, PT. Asahamimas Flat Glas Tbk, PT.

Kalbe Farma Tbk, PT. Ultrajaya Milk Industri Tbk,

PT. Sampoerna agro Tbk, PT. Indofood Sukses

Makmur Tbk.

Overall, the average value of green innovation in

the sample company is 1.34 with a standard deviation

of 1.41. This shows that the spread of green

innovation data has a variation rate of 105%.

Figure 1: Graph of PROPER 1, 2, 3, 4, 5 on green

innovation.

Source: Processed data, 2017.

Based on Figure 1 and table 5 above, the

Company PROPER 1 (black) does not exist due to not

entering sample research. Company PROPER 2 (red)

consists of 31 companies. The result of the company

PROPER 2 (red) is linear that the lower the PROPER

rank, the lower the green innovation level the

company performs.

Company PROPER 3 (blue) is the majority

consisting of 193 companies. Companies rated

PROPER 4 (green) consists 32 companies.

Companies incorporated in the PROPER 4 (green)

rankings proved quite concerned about the use of

environmentally friendly products and production

Green Innovation as Implementation of Sustainability Development in Indonesia

367

processes. It can be seen from the number of

companies. Most are found in number 3 which is the

company has made 3 of 4 criteria of green innovation.

Companies that are ranked PROPER 5 (gold) are

21 companies. This indicates that the number of

companies listed in PROPER 5 (gold) has been

concerned deeply for green innovation as proven by

the most number of companies that do all the green

innovation criteria in which there are 8 companies.

Green Innovation is one strategy that can be used

to achieve corporate goals by considering

environmental aspects and social responsibility. By

bringing together the company's goals by taking

environmental aspects into business strategy, the

company will remain and continue in the future.

Table 5: Relation PROPER with green innovation score.

Source: Processed data, 2017.

4.3.2 Effect of Green Innovation on Firm

Value

Green innovation variable influences firm value,

shows t test significance value equal to 0,019 (<

0.05). This is in accordance with the theory of

stakeholders proposed by Freeman (2010) that the

company's goal is not only to create value to

stockholders, but to create value for all stakeholders.

Creating value for all stakeholders require managers

to improve their financial performance, social

performance and environmental performance also

ensuring that the company remains sustainable in the

future. The company can continue to survive

(sustainable) if the company is able to adapt its

business processes to the rules or norms in the

community (O'Donovan, 2002). This also

corresponds to the theory of competitive advantage

proposed by Porter (1985: 1) which states that

competitive advantage aims to form a sustainable

position in order to survive in industrial competition.

Strategy is a very important tool to achieve

competitive advantage.

Green innovation has a positive impact. For the

environment, green innovation can reduce CO2,

increase biodiversity and reduce pollution. For the

company, green innovation improves productivity,

expands market share, creates an image that the

company cares about the environment, improves

efficiency. Low production cost and high competitive

advantage will lead the company to get high

profitability.

The result of this study supports the result of

research conducted by Salvadó, et al., (2015),

Küçükoğlu and Pınar (2015) and Ar (2012). The

innovation can create value for the company, both

new companies and old companies. Innovation

requires high initial investment and is a high-risk

activity.

This study does not support research conducted by

Özşahin et al., (2013) which concluded that green

product innovation has no effect on firm

performance. This is due to the company's low ability

to innovate. The low ability to innovate will

undermine the company's competitiveness.

4.4 Limitations of Research

Based on the research discussion, limitations of

research are as follows:

The study was limited to manufacturing firms

only for a period of 3 years.

Variables used in this study also consist only

green innovation and firm value. The low level

adjusted R square indicates that there are many

other variables that can affect the relationship

between these variables.

5 CONCLUSIONS

5.1 Conclusions

Based on the research discussion, the conclusions are

as follows:

The result of the company PROPER 2 (red) is

linear that the lower the PROPER rank, the

lower the green innovation level the company

performs. Company PROPER 3 (blue) is the

majority consisting of 193 companies.

Companies incorporated in PROPER 4 (green)

rankings proved to be quite concerned about the

use of environmentally friendly products and

production processes. Companies listed in

PROPER 5 (gold) are already deeply concerned

about green innovation.

Green innovation has significant effect on firm

value. This is in line with the stakeholder theory

proposed by Freeman (2010) that the company's

goal is not only to create the value of its

stockholders, but to create value for all its

stakeholders. Value creation for all stakeholders

requires managers to improve their financial

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

368

performance, social performance, and

environmental performance and ensure that the

company remains sustainable in the future.

5.2 Suggestions

Based on the research that has been done, the

researchers provide some suggestions for the next

researchers as follows:

The next researcher can use the data for more

than 3 years in the hope that the results obtained

will be more accurate and significant.

Taking into account other independent variables

that affect firm value, such as environmental

management accounting.

REFERENCES

Ar, I. M., 2012. The Impact of Green Product Innovation

on Firm Performance and Competitive Capability: The

Moderating Role of Managerial Environmental

Concern. Procedia - Social and Behavioral Sciences,

62, 854–864.

Bech, B., 2013. Quadruple Bottom Line for Sustainable

Prosperity. Retrieved February 17, 2016, from

http://cambridgeleadershipdevelopment.com/quadrupl

e- bottom-line-for-sustainable-prosperity/

Chang, S-C., Wang, C-F., 2007. The Effect of Product

Diversification Strategies on the Relationship between

International Diversification and Firm Performance.

Journal of World Business. 42: 61- 79.

Freeman, R. E., 2010. Strategic Management, Cambridge

University Press. New York, Second Edition.

Ghozali, I., 2013. Aplikasi Analisis Multivariate dengan

Program IBM SPSS 21, Badan Penerbit Universitas

Diponegoro, Semarang. Cetakan Ketujuh.

Küçükoğlu, M. T., Pınar, R. İ., 2015. Positive Influences of

Green Innovation on Company Performance. Procedia

- Social and Behavioral Sciences, 195, 1232–1237.

Margaretha, F., 2005. Teori Dan Aplikasi Manajemen

Keuangan Investasi dan Sumber Dana Jangka Pendek,

Grasindo Gramedia Widiasarana Indonesia. Jakarta.

Margaretha, F., 2011. Manajemen Keuangan, Erlangga.

Jakarta.

Özşahin, D. M., Sezen, B., Çankaya, S. Y., 2013. Effects of

Green Manufacturing and Eco-innovation on

Sustainability Performance. Procedia - Social and

Behavioral Sciences, 99, 154–163.

Porter, M. E., 1985. Competitive Advantage: Creating and

Sustaining Superior Performance. Free Press: New

York.

Qamarullah, D. H., Dorina, W., 2015. Analisis pengaruh

green innovation terhadap green product competitive

advantage pada perum perhutani. Jurnal Manajemen

Trisakti (E-Journal), 2, 45–60.

Rennings, K., Rammer, C., 2009. Increasing Energy and

Resource Efficiency through Innovation - An

Explorative Analysis Using Innovation Survey Data.

SSRN Electronic Journal.

Ross, S. A., Westerfield, R. W., Jordan, B. D., 2008.

Corporate Finance Fundamentals, McGraw- Hill

Education. New York.

Salvadó, J. A., de Castro, G. M., López, J. E. N., 2015). The

importance of the complementarity between

environmental management systems and environmental

innovation capabilities: A firm level approach to

environmental and business performance benefits.

Technological Forecasting and Social Change, 96,

288– 297.

Scrimgeour, F., Iremonger, C., 2011. Maori Sustainable

Economic Development in New Zealand: Indigenous

Practices for the Quadruple Bottom Line.

Development, (August).

Sharma, S., Vredenburg, H., 1998. Proactive corporate

environmental strategy and the development of

competitively valuable organizational capabilities.

Strategic Management Journal, 19(8), 729–253.

Green Innovation as Implementation of Sustainability Development in Indonesia

369