Analysis of Affecting Factors Accuracy of Financial Reporting Time

at the Middle School of City High Cliff

Efni Efridah

1

Faculty of Economics, Universitas Negeri Medan, Medan -Indonesia

Keywords: Human Resource Capacity, Information Technology Utilization, Internal Control, Compilation Motivation,

Leadership Commitment

Abstract: This study aims to analyze the factors that influence the timeliness of financial reporting as a form of

accountability for the management of School Operational Assistance (BOS) funds in high schools in the

City of Tebing Tinggi, North Sumatra Province. Factors tested in this study are human resource capacity,

utilization of information technology, internal control, compiler motivation, leadership commitment,

supporting infrastructure, complexity of company operations, professionalism, experience, and

compensation of report compilers, to the timeliness of financial reporting. The data used in this study is

primary data with the selection of samples using purposive sampling method. The sample of this study

consisted of the managers of BOS funds in high schools in the City of Tebing Tinggi. The data analysis

technique used is multiple linear regression analysis. The results of hypothesis testing show that the capacity

of human resources, utilization of information technology, commitment of leaders, supporting infrastructure

and experience have significant and partial effect on the timeliness of financial reporting. As for internal

control, compiler motivation, operational complexity, professionalism and compensation have no significant

effect on the timeliness of financial reporting in high schools in the City of Tebing Tinggi, North Sumatra

Province.

1 INTRODUCTION

The consequence of the reform era that took place in

Indonesia was the demand for the government to

organize autonomously in the regions. Therefore, in

1999 Law No.22 of 1999 concerning Regional

Government was enacted which regulated regional

authority in the implementation of regional

autonomy in a broad, real and responsible manner.

Often with this, the community's encouragement of

public accountability in local governments has also

increased. Public accountability is defined as a form

of obligation to account for the success or failure of

the implementation of the organization's mission in

achieving the goals and objectives that have been set

before, through a media of accountability carried out

periodically (Mardiasmo, 2006).

Furthermore, as one of the manifestations of

accountability stipulated in Law Number 32 of 2004

concerning Regional Government, the regional

central government is required to submit

accountability reports in the form of financial

statements. The Government Finance Report

produced must meet the principles on time and be

compiled in accordance with Government

Accounting Standards in accordance with

Government Regulation Number 2 of 2005.

Kawedar (2008) states, that to improve

accountability and transparency of the central and

regional government financial reports, an audit is

required by the Agency Financial Examiner (BPK).

The timeliness principle is indispensable in

relation to the period of examination conducted by

the BPK and the drafting process for the RAPBN for

the following year. In addition, the public's need for

financial statements in each year is also an urgency

regarding the importance of timeliness factors need

to be met by the compilers of financial statements.

As for several factors that can affect the timeliness

of financial reporting, among others, the capacity of

human resources, utilization of information

technology, internal control, compiler motivation,

leadership commitment, supporting infrastructure,

328

Efridah, E.

Analysis of Affecting Factors Accuracy of Financial Reporting Time at the Middle School of City High Cliff.

DOI: 10.5220/0009495203280336

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 328-336

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

complexity of operations, professionalism,

experience and compensation of report compilers.

The education sector is one of the most important

sectors that is the focus of development of the

central and regional governments. This is reflected

in the mandate of Law No. 23 of 2003 concerning

the National Education System which stipulates a

minimum education budget allocation of 20 percent

of the National Budget and Regional Budget. The

implication of this is accountability for the budget

that has been given to the government as the

executive, including the regional government. At

this stage, timely financial reporting becomes crucial

as a form of local government accountability to its

people.

The government has an obligation to finance the

education of its citizens as stated in the 1945

Constitution Article 31 paragraph 2. Therefore, since

July 2005 the School Operational Assistance (BOS)

program has been started to help the implementation

of 9-year compulsory education in Indonesia and has

played a significant role. School Operational

Assistance (BOS) is a government program which is

basically to provide funding for non-personnel

operating costs for elementary schools as

implementers of compulsory education programs. In

addition, the background to the emergence of this

program is to improve the condition of national

education (Rahayu, 2017).

The city of Tebing Tinggi is ranked sixth highest

in terms of the education index and budget sector

aspects of education from all regencies /

municipalities in North Sumatra (Girsang, 2012).

Therefore, financial reporting should be on time,

starting at the school level, including high school

(SMA) to the level of the City Government.

2 THEORICAL FRAMEWORK

Timeliness of Financial Reporting Time

The financial report is a structured presentation of

the financial position and financial performance of

an entity (PSAK 1, 2012). Financial reports are the

main means by which companies communicate

financial information to people outside the company.

Financial statements have an important meaning for

all users who need financial information of a

company, for example investors, creditors, and other

users. The purpose of the financial statements is to

provide information about the financial position,

financial performance, and cash flow of the entity

that is beneficial for most users of financial

statements in making economic decisions (PSAK 1,

2012).

Timely is the information available to be used before

losing the meaning of the users of financial

statements, and the capacity is still available in

decision making (Weygandt et. Al, 2013). If there

are undue delays in reporting, the information

produced will lose its relevance (PSAK 1, 2012).

Human Resource Capacity

Human resources (HR) are people who design and

produce goods or services, supervise quality, market

products, allocate financial resources, and formulate

all organizational strategies and objectives. Human

Resource Capacity is the ability of a person or

individual, an organization (institutional), or a

system to carry out its functions or authority to

achieve its objectives effectively and efficiently

(Zuliarti, 2012).

Information Technology Utilization

Information technology is a procedure or system

used by humans to convey messages or information

(Maryono and Patmi, 2007). Information technology

includes computers ( mainframes, mini, micro ),

software ( software ), databases , networks (internet,

intranet), electronic commerce , and other types

related to technology (Arfianti, 2011).

Internal Control

According to the Minister of Home Affairs No. 13

of 2006 concerning Guidelines for Regional

Financial Management, the definition of the

Government Internal Control System is a process

designed to provide adequate assurance regarding

the achievement of regional government objectives

as reflected in the reliability of financial statements,

efficiency and effectiveness of program and activity

implementation and compliance with laws and

regulations (Pemendagri No.13 of 2006). The

internal control system is an integral process for

actions and activities carried out continuously by the

leadership and all employees to provide adequate

confidence in the achievement of organizational

goals through effective and efficient activities,

reliability of financial reporting, safeguarding state

assets, and compliance with laws and regulations.

invitation. The Government's Internal Control

System, hereinafter referred to as SPIP, is an internal

control system that is carried out comprehensively in

the central and regional government (PP 60 of

2008).

Motivation

The term motivation comes from the Latin word "

movere " which means encouragement or

movement. Motivation questions how to direct

power and the potential to work towards the goals

set (Hasibuan, 2006). Work motivation is a

Analysis of Affecting Factors Accuracy of Financial Reporting Time at the Middle School of City High Cliff

329

motivation that occurs in the situation and work

environment contained in an organization or

institution. Basically, humans always want things

that are okay, so the driving or driving power that

motivates their work spirit depends on the

expectations that will be obtained in the future if that

hope becomes reality, then someone will tend to

increase their motivation.

Leadership Commitment

Decree of the Minister of Administrative Reform of

the Republic of Indonesia No. 25 / KEP / M / PAN /

2004 states that the notion of commitment is

determination, firm determination, and promise to

do or realize something that is believed. Effective

leaders will be able to carry out their functions

properly, not only shown by the power they possess

but also by the leader's attention to the welfare and

satisfaction of employees towards leaders and the

improvement of the quality of employees.

Supporting Infrastructure Facilities

Supporting facilities and infrastructure is a measure

of the level of service available at adequate facilities.

In government agencies must pay attention to the

needs and operational equipment because it is a tool

to support the success of a vision, mission and goals

in an organization (Zuliarti, 2012).

Operation Complexity

The complexity of operating an entity is a result of

the formation and division of work that has scope

with a number of different units. Increasingly

complex dependencies occur when organizations

with various types or numbers of jobs and units pose

more complicated managerial and organizational

problems. (Martius, 2012) As for Torang (2013)

shows complexity refers to the level of

differentiation that exists within an organization.

Differentiation means that an organization is

composed of many different units that do different

jobs and use different methods.

Professionalism

Professionalism is defined as the behavior, ways and

qualities that characterize a profession. Someone is

said to be a professional if his work has the

characteristics of a technical or ethical standard of a

profession. Professional characteristics include

competency, effectiveness, efficiency, and

responsibility (Sedarmayanti, 2010).

Experience

According to Hasan (2005) in the Big Indonesian

Dictionary the experience can be interpreted as

having been experienced (lived, felt, borne, etc.).

Asih (2006) states that an employee who has high

work experience will have advantages in several

things including detecting errors, understanding

errors, and finding the cause of the emergence of

mistakes.

Compensation

Compensation is something that employees receive

as a substitute for their service contribution to the

company or organization (Veithzal, 2005). The

provision of compensation is one of the

implementation of HRM functions that relate to all

types of individual rewards as an internal exchange

do organizational tasks. Compensation is the main

cost of expertise or work and loyalty in the

company's business.

HYPOTHESIS

The Influence of Human Resource Capacity on

the Timeliness of Financial Reporting

The relationship between the capacity of human

resources to the timeliness of financial reporting can

be stated that the higher the capacity factor of human

resources will increase the timeliness of financial

reporting. Conversely, if the capacity of human

resources is lower, then the timeliness of financial

reporting will also be lower. Therefore, the

following hypothesis can be stated:

H 1: The capacity of human resources

influences the timeliness of reporting finance.

Effect of Information Technology Utilization on

the Timeliness of Financial Reporting

The relationship between the use of information

technology to the timeliness of financial reporting

can be stated that the higher the utilization of

information technology, the more timeliness of

financial reporting. Conversely, if the utilization of

information technology is lower, then the timeliness

of financial reporting will also be lower. Therefore,

the following hypothesis can be stated:

H 2: The use of information technology

influences the timeliness of reporting finance.

The Influence of Internal Control on the Timeliness

of Financial Reporting

The relationship between internal control and

timeliness of financial reporting can be stated that

the higher the internal control factor, the more

timeliness of financial reporting will increase.

Conversely, if internal controls are lower, then the

timeliness of financial reporting will also be lower.

Therefore, the following hypothesis can be stated:

H 3: Internal controls affect the timeliness of

reportingfinance.

Effect of Motivation on Timeliness of Financial

Reporting

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

330

The relationship between motivation and timeliness

of financial reporting can be stated that the higher

the motivation factor, the more timeliness of

financial reporting will increase. Conversely, if

motivation decreases, then the timeliness of financial

reporting will also decrease. Therefore, the

following hypothesis can be stated:

H 4: Motivation affects the timeliness of

financial reporting.

Effect of Leadership Commitment to the

Timeliness of Financial Reporting

The relationship between the leadership commitment

to the timeliness of financial reporting can be stated

that the higher the leadership commitment factor, the

more timely the financial reporting. Conversely, if

the leadership commitment decreases, then the

timeliness of financial reporting will also decrease.

Therefore, the following hypothesis can be stated:

H 5: Leadership commitment influences the

timeliness of financial reporting.

The Effect of Supporting Infrastructure Facilities

on the Timeliness of Financial Reporting

The relationship between supporting infrastructure

and the timeliness of financial reporting can be

stated that the higher the supporting infrastructure

facilities, the more timely the financial reporting.

Conversely, if the supporting infrastructure

decreases, then the timeliness of financial reporting

will also decrease. Therefore, the following

hypothesis can be stated:

H 6: Support infrastructure facilities affect

the timeliness of financial reporting.

Effect of Operational Complexity on the

Timeliness of Financial Reporting

The relationship between the complexity of

operations and the timeliness of financial reporting

can be stated that the higher the factor of operational

complexity, the greater the timeliness of financial

reporting. Conversely, if the operating complexity

decreases, then the timeliness of financial reporting

will also decrease. Therefore, the following

hypothesis can be stated:

H 7: Operational complexity affects the

timeliness of financial reporting.

Professionalism Influence on the Timeliness of

Financial Reporting

The relationship between professionalism and

timeliness of financial reporting can be stated that

the higher the professionalism factor, the more

timeliness of financial reporting will increase.

Conversely, if professionalism decreases, then the

timeliness of financial reporting will also decrease.

Therefore, the following hypothesis can be stated:

H 8: Professionalism affects the timeliness of

financial reporting.

The Effect of Experience on the Timeliness of

Financial Reporting

The relationship between experience with the

timeliness of financial reporting can be stated that

the higher the experience factor will increase the

timeliness of financial reporting. Conversely, if the

experience is lower, then the timeliness of financial

reporting will experience even lower. Therefore, the

following hypothesis can be stated:

H 9: Experience affects the timeliness of

financial reporting.

Effect of Compensation on the Timeliness of

Financial Reporting

The relationship between compensation for financial

reporting timeliness can be stated that the higher the

compensation factor will increase the timeliness of

financial reporting. Conversely, if compensation

decreases, then the timeliness of financial reporting

will also decrease. Therefore, the following

hypothesis can be stated:

H 10: Compensation affects the timeliness of

financial reporting.

Effect of Simultaneous Independent Variables on

the Timeliness of Financial Reporting

The relationship between independent variables

simultaneously on the timeliness of financial

reporting can be stated that the higher the capacity

factor of human resources, the use of information

technology, internal control, motivation,

commitment of leaders, supporting infrastructure,

complexity of operations, professionalism,

experience and simultaneous compensation will

further increase the timeliness of financial reporting.

Conversely, if the capacity of human resources,

utilization of information technology, internal

control, motivation, leadership commitment,

supporting infrastructure, operational complexity,

professionalism, experience and compensation are

simultaneously lower, then the timeliness of

financial reporting will also be lower. Therefore, the

following hypothesis can be stated:

H 11: Capacity of human resources, utilization

of information technology, internal control, ,

leadership commitment, supporting

infrastructure, complexity of operations,

professionalism, experience and compensation

simultaneously affect timeliness of financial

reporting.

Analysis of Affecting Factors Accuracy of Financial Reporting Time at the Middle School of City High Cliff

331

3 RESEARCH METHOD

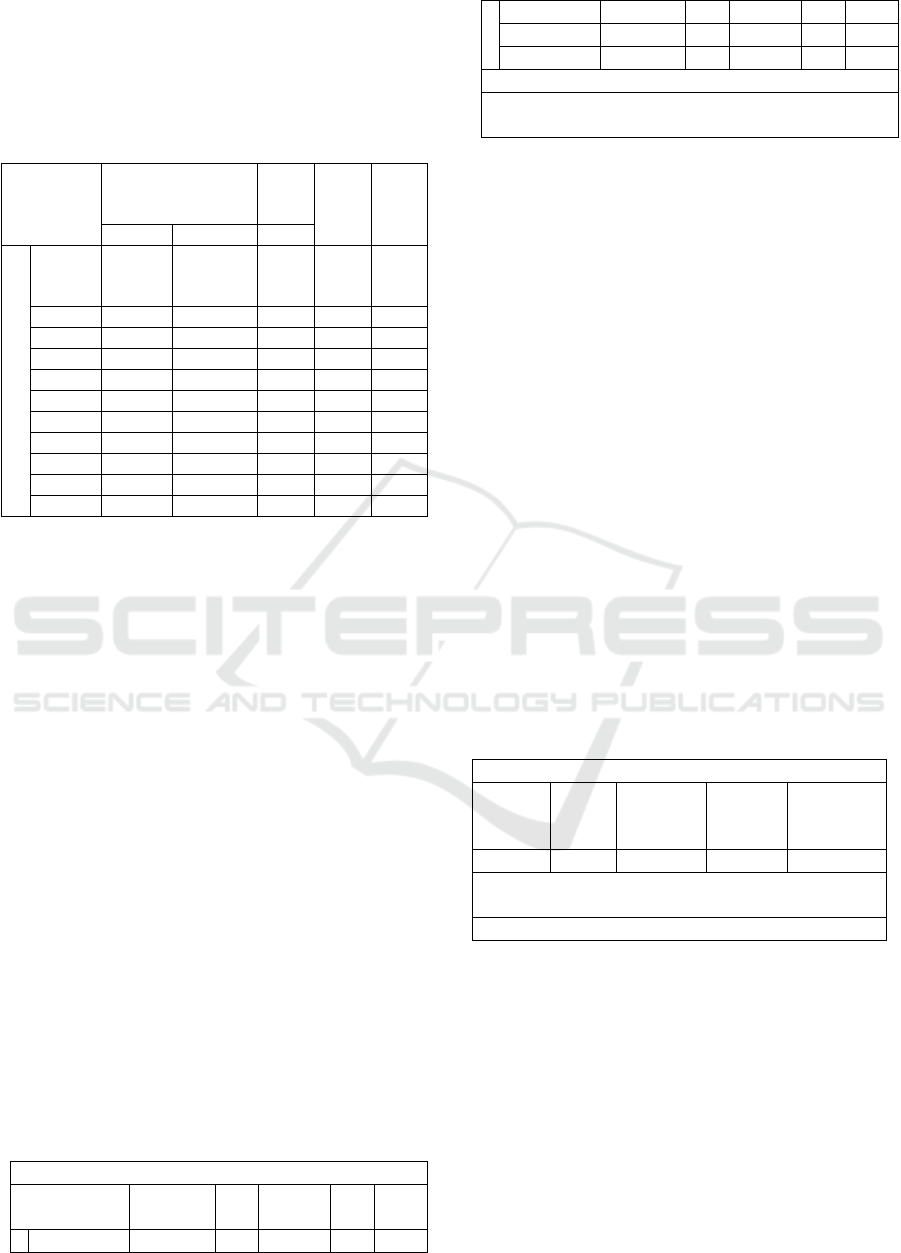

Table 1: Variables affect timeliness of financial

reporting

a. Dependent Variable: TIMELINESS

Source: Processed Data of Researchers, 2018

Based on Table 1 it can be seen that the variable

capacity of human resources (X 1 ), utilization of

information technology (X 2), commitment of

leaders (X 5 ) supporting infrastructure (X 6 ), and

experience (X 9 ) have a significance value <0, 05

which means that these variables affect the

timeliness of financial reporting. The internal control

variables (X 3 ), compiler motivation (X 4),

operational complexity (X 7 ), professionalism (X

8), and compensation (X 10 ) have a significance

value> 0.05, which means that these variables affect

timeliness of financial reporting.

Simultaneous Test (Test F)

The F test is used to test the simultaneous effect on

factors that affect the dependent variable. The

guidelines used to accept or reject the hypothesis

are:

1. Ha is accepted if the p-value value is in the sig

column . < level of significant (α) 5%.

2. Ho is accepted if the p-value value is in the sig

column . > level of significant (α) 5% .

Following are the results of partial testing in this

study:

Table 2: Simultaneous Test Results (Test-F)

ANOVA

a

Model

S

um of

Squares

df Mean

Square

F Sig.

Regression 179,764 10 17,976 50, .000

234

b

Residual 22,903 64 .358

Total 202,667 74

a

. Dependent Variable: Y

b

. Predictors: (Constant), X10, X1, X7, X8, X9, X4, X2,

X6, X5, X3

Source: Processed Data of Researchers, 2018

Based on Table 2 that significant value 0.000

<0.05 so that it can be stated that simultaneously the

human resource capacity variable (X 1), use of

information technology (X 2), internal control (X 3),

motivation constituent (X 4), Leader commitment (X

5 ), supporting facilities and infrastructure (X 6 ),

operational complexity (X 7 ), professionalism (X 8

), experience (X 9 ), and report compiler

compensation (X 10 ) have a significant effect on the

timeliness of financial reporting (Y).

Determination Coefficient

The coefficient of determination (R 2 ) measures

how far the ability of the model in explaining the

variation of the dependent variable. The coefficient

of determination is between zero or one. A small R 2

value means the ability of independent variables to

explain the variation of the dependent variable is

limited. A value close to one means that independent

variables provide almost all the information needed

to predict the variation of the dependent variable.

Here are the results of the coefficient of

determination in this study:

Table 3: Determination Coefficient

Summar

y

Model

b

Model R R Square

A

djusted

R Square

Std. Error

of the

Estimate

1 .942

a

.887 .869 .9821

a. Predictors: (Constant), X10, X1, X7, X8, X9,

X4, X2, X6, X5, X3

b

. Dependent Variable: Y

Source: Processed Data of Researchers, 2018

Based on Table 3 obtained coefficient value (R)

of 0.942 which shows the magnitude of the

relationship between variables, with the coefficient

of determination ( Adjusted R square ) of 0.869 or

86.9%. This means the variable capacity of human

resources (X 1 ), utilization of information

technology (X 2 ), internal control (X 3 ), motivation

of compilers (X 4 ), commitment of leaders (X 5 ),

supporting facilities and infrastructure (X 6 ) , the

complexity of operating the company (X 7 ),

Model Unstandardized

Coefficients

Stand.

Coeffic

ients

t Sig.

B Std. Error Beta

(C

onst

ant)

-2.488 1,304

-1.907 .061

X1 .116 .054 .134 2,128 .037

X2 .172 .060 .232 2,894 .005

X3 -.073 .058 -130 -1.242 .219

X4 .010 .024 .032 .397 .693

X5 .367 .073 .512 5,022 .000

X6 .199 .069 .263 2,902 .005

X7 -.023 .084 -.026 -270 .788

X8 .045 .033 .183 1,393 .168

X9 .151 .051 .183 2,972 .004

X10 -111 .029 -.024 -.371 .712

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

332

professionalism (X 8 ), experience (X 9 ), and

compensation for the report compiler (X 10 ) can

explain the variable timeliness of reporting by

86.9%. While the remaining 13.1% is explained by

other variables outside this estimation model.

4 RESULTS

Based on the tests that have been carried out in this

study, the discussion of the results of each

hypothesis can be explained as follows:

The Influence of Human Resource Capacity on

the Timeliness of Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .037 (less than 0.05) in the

variable human resource capacity which means that

H 0 is rejected H a accepted. Therefore, it can be

concluded that partially the capacity of human

resources has a significant effect on the timeliness of

financial reporting in high schools in the city of

Tebing Tinggi.

The existence of a positive influence means that

the higher the capacity factor of human resources,

the greater the timeliness of financial reporting.

Conversely, if the capacity of human resources is

lower, then the timeliness of financial reporting will

also be lower. Therefore, senior high schools in the

city of Tebing Tinggi need to increase the capacity

of human resources to be able to improve the

timeliness of financial reporting. Efforts that can be

made include conducting routine technical guidance

to the compilers of financial statements.

Effect of Information Technology Utilization on

the Timeliness of Financial Reporting

Based on the results of testing partially obtained a

significant value of 0 .005 (less than 0.05) on the

variable utilization of information technology which

means that H 0 is rejected H a accepted . Therefore,

it can be concluded that partially the use of

information technology has a significant effect on

the timeliness of financial reporting in high schools

in the city of Tebing Tinggi.

The existence of a positive influence means that

the higher the utilization of information technology ,

the more timeliness of financial reporting.

Conversely, if the utilization of information

technology is lower, then the timeliness of financial

reporting will also be lower. Therefore, high schools

in Tebing Tinggi need to increase the use of

information technology so as to improve the

timeliness of financial reporting. Efforts that can be

made include conducting information technology

training routinely to the compilers of financial

statements.

The Influence of Internal Control on the

Timeliness of Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .219 (greater than 0.05) in the

variable internal control means H a rejected H 0

accepted. Therefore, it can be concluded that

partially internal control has no significant effect on

the timeliness of financial reporting in high schools

in the city of Tebing Tinggi.

From these results it can be stated that internal

control carried out is not a significant factor in

influencing the timeliness of financial reporting of

High Schools in the City of Tebing Tinggi. Based on

observations made, this is possible because the

financial report compilers have independent

awareness to produce timely financial statements, so

that internal control does not significantly affect the

performance of financial reporters.

Effect of Motivation on Timeliness of Financial

Reporting

Based on the partial test results significantly the

value obtained by 0 .693 (greater than 0.05) in the

variable motivation means H a rejected H o

accepted. Therefore, it can be concluded that

partially motivation has no significant effect on the

timeliness of financial reporting in high schools in

Tebing Tinggi.

From these results it can be stated that the

motivation of the compilers of the financial

statements is not a significant factor in influencing

the timeliness of financial reporting of High Schools

in the City of Tebing Tinggi. Based on observations

made, this can occur because the financial report

compilers have sufficient understanding and

awareness of the tasks that must be done, so that

personal motivation does not have a significant

influence on the timeliness of financial reporting in

high schools in Tebing Tinggi.

Effect of Leadership Commitment to the

Timeliness of Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .000 (less than 0.05) in the

variable management commitment which means that

H 0 is rejected H a accepted. Therefore, it can be

concluded that partially the leadership commitment

has a significant effect on the timeliness of financial

reporting in High Schools in the City of Tebing

Tinggi.

Analysis of Affecting Factors Accuracy of Financial Reporting Time at the Middle School of City High Cliff

333

The existence of a positive influence means that

the higher the leadership commitment factor , the

more timeliness of financial reporting will be.

Conversely, if the leadership commitment is lower,

then the timeliness of financial reporting will be

lower. Therefore, senior high schools in the city of

Tebing Tinggi need to continue to improve the

commitment of leaders in order to build an

atmosphere and a supportive work environment for

the compilers of financial statements.

The Effect of Supporting Infrastructure Facilities

on the Timeliness of Financial Reporting

Based on the results of partial testing obtained

significant value of 0 .005 (less than 0.05) on the

supporting infrastructure facilities, which means that

H 0 is rejected H a accepted . Therefore, it can be

concluded that partially supporting infrastructure has

a significant effect on the timeliness of financial

reporting in high schools in Tebing Tinggi.

The existence of a positive influence means that

the higher the factor of supporting infrastructure

means that it will increase the timeliness of financial

reporting. Conversely, if the supporting

infrastructure is getting lower, then the timeliness of

financial reporting will be even lower. Therefore,

high school in Tebing Tinggi needs to continue to

improve supporting infrastructure, including through

the procurement and maintenance of facilities and

supporting facilities for the compilers of financial

reports in high schools in Tebing Tinggi.

Effect of Operational Complexity on the

Timeliness of Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .788 (greater than 0.05) in the

variable complexity of the operation, which means

H a rejected H o accepted. Therefore, it can be

concluded that partially operating complexity has no

significant effect on the timeliness of financial

reporting in high schools in Tebing Tinggi.

From these results it can be stated that the

complexity of operations in school entities is not a

significant factor in influencing the timeliness of

high school financial reporting in the City of Tebing

Tinggi. Based on observations made, this can occur

because of the existence of an adequate Standard

Operating Procedure (SOP) for financial report

compilers in each stage and process of preparing

financial statements, so that various situations that

can occur can be anticipated by financial report

compilers.

Professionalism Influence on the Timeliness of

Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .168 (greater than 0.05) in the

variable professionalism which means that H a

rejected H o accepted. Therefore, it can be

concluded that partially professionalism has no

significant effect on the timeliness of financial

reporting in high schools in Tebing Tinggi.

From these results it can be stated that

professionalism in school entities is not a significant

factor in influencing the timeliness of high school

financial reporting in Tebing Tinggi City. Based on

observations made, this can occur because actually

the compilers of financial statements have had an

adequate level of professionalism. This is possible

because in order to obtain a position as a compiler of

financial statements, professional criteria must first

be fulfilled, so that if an employee is unprofessional

it is not feasible to obtain a position as a compiler of

financial statements at High Schools in Tebing

Tinggi City.

The Effect of Experience on the Timeliness of

Financial Reporting

Based on the results of testing partially obtained a

significant value of 0 .004 (smaller than 0.05) in the

experience variable, which means that H 0 is

rejected H a accepted . Therefore, it can be

concluded that partially the experience has a

significant effect on the timeliness of financial

reporting in high schools in the city of Tebing

Tinggi.

The existence of a positive influence means that

the higher the experience factor , the greater the

timeliness of financial reporting will be. Conversely,

if the leadership commitment is lower, then the

timeliness of financial reporting will be lower.

Therefore, senior high schools in Tebing Tinggi

need to maintain the turnover rate of the compilers

of financial statements so that the compilers of the

financial statements who have experience do not

move much to other units.

Effect of Compensation on the Timeliness of

Financial Reporting

Based on the partial test results significantly the

value obtained by 0 .712 (greater than 0.05) in the

variable compensation means H a rejected H o

accepted . Therefore, it can be concluded that

partially compensation has no significant effect on

the timeliness of financial reporting in high schools

in the city of Tebing Tinggi.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

334

From these results it can be stated that

compensation is not a significant factor in

influencing the timeliness of financial reporting for

High Schools in the City of Tebing Tinggi. Based on

observations made, this can occur because the

compilers of financial statements in high schools in

the city of Tebing Tinggi view the timeliness of

financial reporting as an obligation inherent in his

position, so that compensation is not a major factor

consideration of the compilers of financial

statements in producing timely financial statements .

5 CONCLUSIONS

Based on the results of the research and discussion

carried out, it can be concluded as follows:

1. The capacity of human resources has a

significant effect on the timeliness of financial

reporting in high schools in the city of Tebing

Tinggi.

2. The use of information technology has a

significant effect on the timeliness of financial

reporting in high schools in the city of Tebing

Tinggi.

3. Internal control has no significant effect on the

timeliness of financial reporting in high schools

in the city of Tebing Tinggi.

4. The motivation of the compiler has no

significant effect on the timeliness of financial

reporting in high schools in the city of Tebing

Tinggi.

5. Leadership commitment has a significant effect

on the timeliness of financial reporting.

6. Supporting infrastructure has a significant effect

on the timeliness of financial reporting in high

schools in the city of Tebing Tinggi.

7. Operating complexity has no significant effect

on the timeliness of financial reporting in high

schools in the city of Tebing Tinggi.

8. Professionalism has no significant effect on the

timeliness of financial reporting.

9. Experience has a significant effect on the

timeliness of financial reporting in high schools

in the city of Tebing Tinggi.

10. Compensation of the report compiler has no

significant effect on the timeliness of financial

reporting in high schools in the City of Tebing

Tinggi.

11. The capacity of human resources, utilization of

information technology, internal control,

motivation, leadership commitment, supporting

infrastructure, operational complexity,

professionalism, experience and compensation

simultaneously influence the timeliness of

financial reporting in high schools in Tebing

Tinggi .

REFERENCES

Arfianti, Dita. (2011). Analysis of Factors Affecting the

Value of Information on Local Government

Financial Reporting (Studies in the Regional Work

Unit in Batang District) . Diponegoro University

Semarang.

Asih. (2006). The Effect of Experience on Enhancing

Auditor Skills in Auditing . Indonesian Islamic

University.

Girsang, Beryl Artesian. (2012). Regional Budget

Allocation in human development District / City in

North Sumatra Province 2001-2009 . Gadjah Mada

University Journal.

Hasan, Alwi et al. (2005). Large Indonesian Dictionary .

Jakarta: Ministry of National Education Balai

Pustaka.

Hasibuan, Malayu SP (2006). Basic Management,

Understanding, and Problems Revised Edition ,

Bumi Aksara: Jakarta.

Indonesian Accounting Association (2012), Financial

Accounting Standards . Jakarta: Salemba Empat.

Kawedar, Warsito et al. 2008. Public Sector Accounting

(Regional Budgeting Approach and Regional

Financial Accounting / Book 1. Semarang: Salemba

Empat.

Mardiasmo. (2006). Realization of Public Transparency

and Accountability through Public Sector

Accounting: A Good Governance Tool .

Government Accounting Journal, 2: 1. (1-17).

Martius. (2012). Analysis of Management Accounting

Practices in Manufacturing Companies (Empirical

Studies in Kawaan Industri Batam) . Article. Post

Sajana Science Master Program Andalas University.

Padang

Maryono, Y. and B. Patmi Istiana. (2007). Information &

Communication Technology 1. Yudhistira Publisher.

Rahayu, Anisa. Endang Larasati Setianingsih. (2017).

Supervision of the School Operational Assistance

Fund (BOS) for Primary Schools (SD) in the

Temanggung District Education Office. eJournal

Diponegoro University.

Sedarmayanti, (2010), Human Resources and Work

Productivity, the second print . Publisher: Mandar

Maju. Bandung.

Torang, Syamsir. (2013). Organization and Management .

First Mold. Bandung: CV Alfabeta

Analysis of Affecting Factors Accuracy of Financial Reporting Time at the Middle School of City High Cliff

335

Veithzal, Rivai. (2005). Human Resource Management .

Jakarta: Raja Grafindo Persada

Weygandt, Kimmel and Kieso. (2013). Financial

Accounting: IFRS Edition . Hoboken: John Wiley &

Sons, Inc.

Zuliarti. (2012). The Influence of Human Resources

Capacity, Information Technology Utilization, and

Accounting Internal Control Against the Value of

Information of Local Government Financial

Reporting: Studies in the Government of Kudus

Regency , MuhMuria Kudus University.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

336