The Civil Servants’ Intention to Be Whistle Blowers of Corruption

Cases in Government Sector

Badingatus Solikhah

1

, Agus Wahyudin

1

and Agung Yulianto

1

1

Faculty of Economics, Universitas Negeri Semarang, Semarang-Indonesia

Keywords: Whistle-blowing Intention, Attitudes, Organizational Commitment, Prosocial Theory.

Abstract: This study aims to describe the intentions of civil servant in Central Java Indonesia to do whistle-blowing.

This paper also examined the relationship of attitudes toward whistleblowing and organizational

commitment toward whistleblowing intention. The respondents within this study were 200 government civil

servants working on Audit Board of the Republic Indonesia Representative of Central Java Province and

Inspectorate of Central Java Province. This paper using closed questionnaire to collect the data. The

questionnaire developed from previous study using scale 1-5 and 135 questionnaires were analyzed using

IBM SPSS 21. The respondents were willing to become whistle-blowers in the event of fraud cases they

found out. The research findings indicated that the attitude and organizational commitment gave a positive

influence on whistle-blowing intentions. It can be concluded that in the formation of intentions to do

whistle-blowing influenced factor inside oneself to form the intention and required the existence of self-

control from various limitations.

1 INTRODUCTION

Over the past few decades, issues regarding whistle-

blowing have become a global concern since they

are proven effective for detecting fraud in

organizations. The whistle-blowing system, which is

effective, transparent and responsible, is highly

expected to overcome employee reluctance to report

suspected violations and to increase employee

participation in reporting suspected violations. Park

et al. (2008) suggested that whistle-blowing is a

means to report any violations to individuals or

organizations considered to have an authority to put

an end to them and there may be considerable

variation in the actual way in which employees can

become whistle-blowers. Referring to the Indonesian

ACFE report in 2016, the highest fraud prevention

method as much as 20.6% was the whistle-blowing

system method.

Most previous studies (Tavakoli et. al, 2003)

agreed that whistle-blowing is an internal

organizational structure that is significant to strive

against company mistakes and questionable actions

(Kaplan & Schultz, 2007). Near and Miceli (1995)

declared that fraud not disclosed to anyone will put

their organization in danger. Whistle-blowing

requires collective efforts within an organization

since it is effective in combating fraud as long as all

members of the organization actively participate.

Whistle-blowing is able to increase the effectiveness

and efficiency of the organization and therefore, can

be considered a mitigating factor to prevent

unexpected negative occurrence (Ahmad et.al, 2012;

Kaplan & Schultz, 2007; Winardi, 2013).

Thus whistle-blowing is a notable way to prevent

and deter any frauds, losses and misuses (Hwang

et.al, 2008). For the significance of the whistle-

blowing, a method is necessary to encourage the

effectiveness of fraudulent disclosures that occur

within the organization. The Sarbanes-Oxley Act

2002, Section 302 and 806, are specifically designed

to encourage whistle-blowing and provide protection

from retaliation for employees who disclose fraud or

who become whistle-blowers within the

organization.

In fact, being a whistle-blower is not an

effortless matter. Anyone who comes from an

internal organization will generally face an ethical

dilemma in deciding whether to report it or leave it

hidden. Some people view the whistle-blower as a

traitor violating the norms of organizational loyalty,

yet others view the whistle-blower as a heroic

protector of values which considered more important

Solikhah, B., Wahyudin, A. and Yulianto, A.

The Civil Servants’ Intention to Be Whistle Blowers of Corruption Cases in Government Sector.

DOI: 10.5220/0009498709630967

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 963-967

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

963

than loyalty to the organization. A person may be a

whistle-blower in order to get attention, fame,

promotion, and retainer for his whistle, even though

the organization may designate a whistle-blowing as

a mechanism to expose and control organizational

errors (Rothschild, 1999 and Hwang et al., 2008).

These conflicting views often make candidates for

whistle-blowers in a dilemma of uncertainty

determine attitudes that can ultimately distort the

interests of whistle-blowing (Bagustianto &

Nurkholis, 2015).

The objectives of this study was to examine

whether individual factors that consisting of

organizational attitudes and commitment influence

the auditor's intention to do whistle-blowing. This

study was conducted on government auditors who

worked for the Indonesian Financial Audit Agency

(BPK) representative of Central Java Province and

Inspectorate of Central Java Province. The

respondents were selected in government auditors

with the idea that they have already known the

systematic whistle-blowing and fraudulent reporting

system applied at their workplace.

2 THEORICAL FRAMEWORK

Pro-social Organizational Behavior Theory

Brief and Motowidlo (1986) suggested that pro-

social behavior is behavior carried out by members

of an organization, directed at individuals, groups, or

organizations with whom they interact when playing

their organizational roles in order to promote the

welfare of individuals, groups or organizations

targeted. Brief and Motowidlo (1986) mentioned

whistle-blowing as either the 13 forms of pro-social

organizational behavior. The relation of pro-social

theory with the intention of whistle-blowing is that

sometimes members of an organization see an urgent

need for change, for instance, due to certain orders,

procedures or policies that may be unethical, illegal,

or cause harm to the organization in long term, but

cannot suggest or bring change directly. If done with

sincere intention to help the organization, this is also

a pro-social behavior (Brief & Motowidlo, 1986).

This is in accordance with the opinion of Dozier and

Miceli (1985) which stated that whistle-blowing

behavior can be viewed as pro-social behavior since

in general these behaviors will provide benefits to

other people (or organizations) besides being useful

for the whistle-blowers themselves so that whistle-

blowing can be said to be pro-social behaviour.

Development of Hypotheses

Attitude against whistle-blowing

Park and Blenkinsopp (2009) stated that someone

develops his attitude based on his belief on the

behavior which was being considered connecting

that behavior with the certain consequences. The

first step in the process of making pro-social

decision is focal member (individual who will be

observed) consider whether focalactivity is

wrongdoing or not (Greenberger et al., 1987 in

Manafe, 2015). The attitude toward a behavior refers

to the extent to which a person has evaluation or

favorable judgment or unfavorable judgment to the

certain behavior (Ajzen, 1991, Solikhah, 2014).

Winardi (2013) stated that an employee more tends

to be whistle-blower if he believes that whistle-

blower brings positive results and the results is

important to be evaluated. For example, the results

of whistle-blowing could prevent serious damage on

the organization and help to eradicate a corruption.

If employee assumes that whistle-blower is as

corrective steps for organization, which could save

organization, it means this attitude bring positive

effect. The previous research done by Park and

Blenkinsopp (2009), Winardi (2013), Bagustianto

and Nurkholis (2015) stated that an attitude brings

positive effect to the intention whistle-blowing. So

that the hypothesis is

H

1

: The attitudes supportive against the whistle-

blowing system will bring positive effect to

intention of whistle-blowing.

The Commitment of Organization

Mowday et al. (1979) define the commitment of

organization is as relative power of identification

and individual involvement in an organization. This

component of organizational commitment show the

disposition of pro-social behavior, is individuals

committed to the organization will be willing to give

something of themselves to contribute to the welfare

of the organization (Brief and Motowidlo, 1986). In

Myers's book, (2012:196) the norm of social

responsibility is the belief that someone must help

those who need help regarding reciprocity, this is

corresponding with the principle of the commitment

of organization. For whom has high organizational

commitment will always be actively involved and

contribute to the organization, so that they have

more sense of belonging to the organization, then

they will do anything to protect their organization,

then that commitment bring positive effect to

intention of whistle-blowing. The previous research

result done by Napitupulu (2016) and Bagustianto

and Nurkholis (2015) stated that the organizational

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

964

commitment has a positive effect on whistle-

blowing intentions, thus, the hypothesis proposed:

H

2

: The Commitment of an Organization bring

positive effect N whistle-blowing intention.

3 RESEARCH METHOD

Sample

The samples of this research were civil servants

working in the Inspectorate of Central Java Province

and representative of BPK Central Java Province.

Both agencies were selected because the system

reporting of whistle-blowing was already presented

in those institutions /organizations. The sampling

technique used is Non-Probability, while in selecting

the sample the method used was purposive sampling

with the criteria ‘the employee has at least on year

working experience’. It was with the consideration

that respondents who have work at least one year

have proper knowledge, have understood to the

working environment, and have perception and

consideration of the comprehensive to whistle-

blowing intention. The research data was collected

through conducting 200 questionnaires. There were

135 questionnaires were returned (response rate

72%).

Table 1 describes about definition variable,

indicator or the way of measurement.

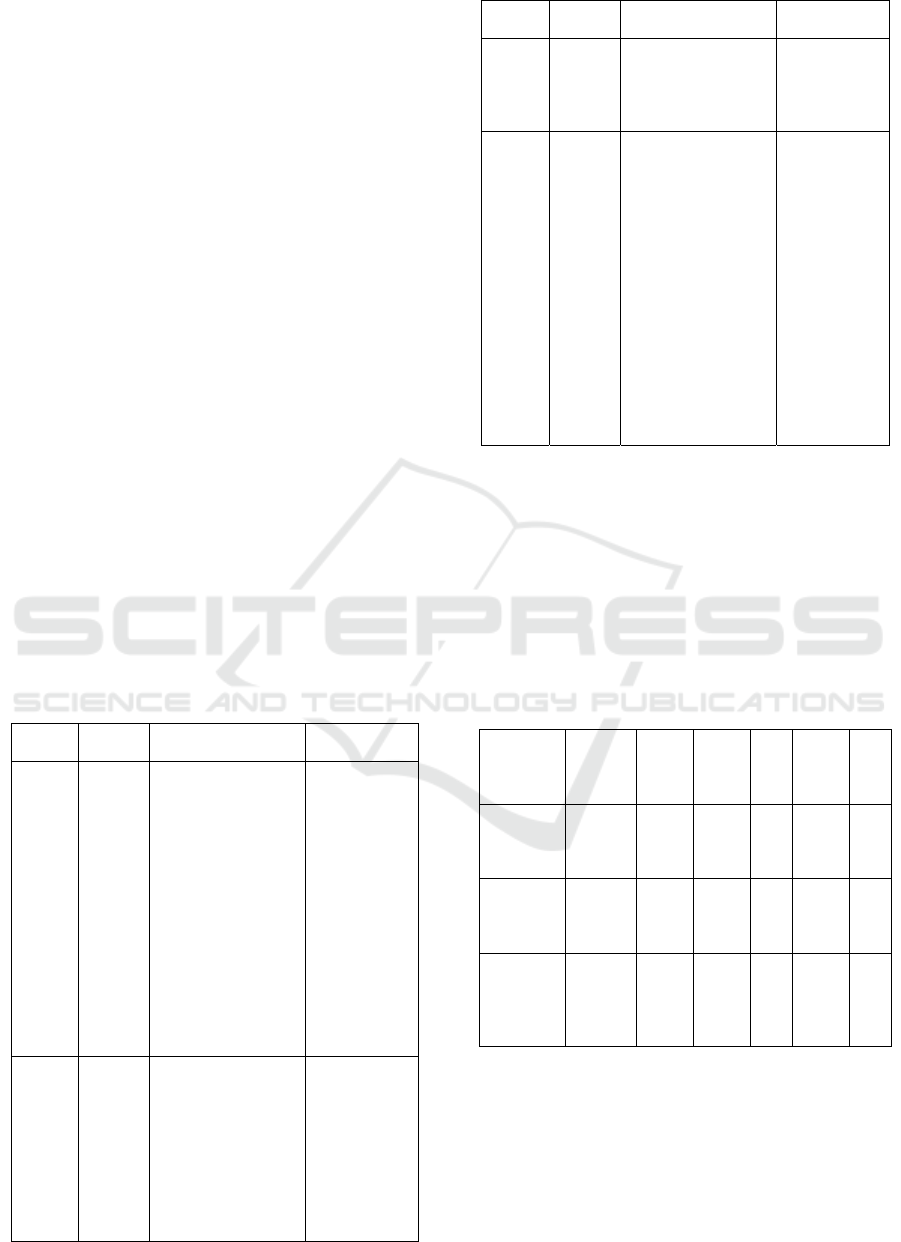

Table 1: The Variable Deskreption.

Varia

ble

Definit

ions

Indicators/Measure

ment

Reference

Whistl

e-

blowin

g

Report

the erro

r to the

trusted

individ

ual or

organiz

ation th

at has

power

to stop

it.

1. Report an error

with complete

identity.

2. The

anonymously

report

3. Report to the

internal

organization.

4. Report to the

external

organization.

The

measurement uses

likert scale 1-5

Park &

Blenkin-sopp,

(2009)

Attitud

e

The

individ

ual

attitude

toward

how

many h

e

approv

es or n

1. The confidence

behavior

2. Evaluation of

Importance

The

measurement uses

likert scale 1-5

Park &

Blenkin-sopp,

(2009)

Varia

ble

Definit

ions

Indicators/Measure

ment

Reference

ot appr

ove a

certain

behavi

or.

The

commi

tment

of

organi

zation

How

far the

involve

ment of

an

employ

ee to

the

organiz

ation.

1. Strong

confidence and

acceptance

goals and value

organization,

2. The

willingness for

exert

considerable eff

ort on nae of

organization,

and

3. loyalty.

The measurement

uses likert scale

1-5

Mowday

et al.

(1979)

4 ANALYSIS

Findings of Descriptive Statistical Analysis

Analysis statistics descriptive used for describing the

existing variables in the research seen from

minimum and maximum value and mean. The

analysis of statistics descriptive could be seen in

table 2 the results of analysis descriptive statistics:

Table 2: The results of analysis descriptive statistics.

Variable

Numb

er of

Respo

ndent

Min Max

M

ea

n

St.

Devi

ation

Ca

teg

or

y

Intention

of

Whistle-

blowing

135 1 5

3.4

2

0.76

It

ca

n

be

Attitude

toward

Whistle-

blowing

135 1 5

3.9

7

0.53

Ap

pr

ov

ed

The

commitm

ent of

organizati

on

135 2 5

3.6

1

0.56

Hi

gh

The findings of descriptive statistics showed that

the intention of the whistle-blowing variable fell into

the possible category. This means that research

respondents were willing to become whistle-blowers

in the event of fraud cases they found out. The

attitude variable towards the whistle-blowing was in

the agreed category in which the respondent's

organizational commitment variable got a high

The Civil Servants’ Intention to Be Whistle Blowers of Corruption Cases in Government Sector

965

category and the retaliation view variable is also

included in the fairly high category. The status of

offenders belonged to the quite powerful category;

the ethical environment was in the high category

while the ethnic groups included in a possible

category.

Findings of Hypothesis Test

All variables in this study passed the classic

assumption test. Classical assumption test shows that

the data is normal which is expressed with a

significance value of 0.537 or above 0.05.

Multicollinearity test shows that tolerance value is

more than 0.10 and VIF value is less than 10, so

there is no correlation between independent

variables and the regression model. Therefore, it

does not occur multicollinearity. The

heteroscedasticity test using the glejser test shows

that the significance is above 0.05 and the variable

does not occur with heteroscedasticity so that all

variables pass the classical assumption test.

The Result of Multiple Linear Regression is

shown in the table 3.

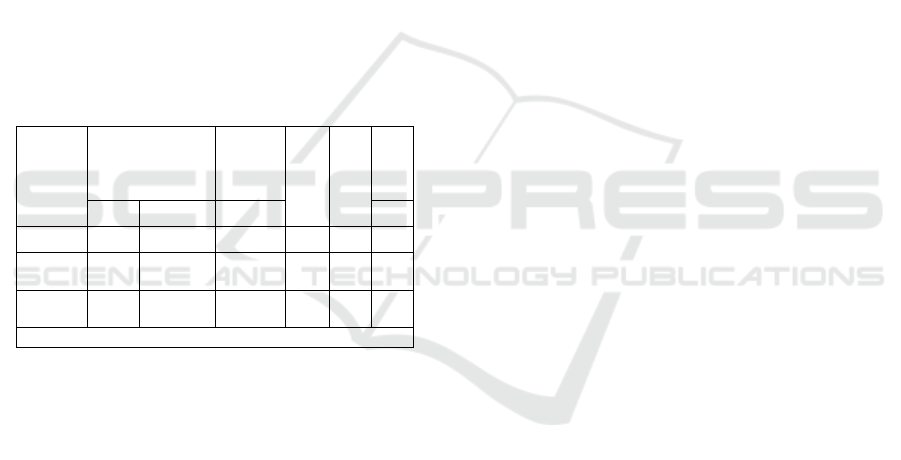

Table 3: The Result of Multiple Linear Regression

Model Unstandardized

Coefficients

Standardi

zed

Coefficien

ts

t Sig. Concl

usion

B Std. Error Beta

(Constant)

13.808 5.377 2.568 .011

Attitude

.574 .101 .494 5.661 .000 Accep

ted

Commitm

ent Org.

.158 .056 .214 2.799 .006 Accep

ted

Dependent Variable: Whistle-blowing Intention

The results coefficient of determination test

shows that the amount of Adjusted R Square is

0.387 which means that 38.7% variable variation

from whistle-blowing intentions can be explained by

variable attitudes, organizational commitment,

retaliation views, offender status, ethical

environment, and ethnicity, while the remaining

62.3% explained by other variables outside the

model.

5 RESULTS

H

1

which stated that a supportive attitude towards

the whistle-blowing system would have a positive

effect on whistle-blowing intentions received. The

employee agreed to the benefits of whistle-blowing

and he agreed that the results after reporting became

an important matter. For instance, it could prevent

the loss of the organization and eradicate corruption.

As a state civil servant, he must also carry out his

obligations as a servant of the state, which were

protecting and maintaining the reputation of his

organization so that he could fulfil the public's desire

to make a clean organization, if he did a whistle-

blowing, and then makes a better organization.

This result was in accordance with the theory of

pro-social behaviour. The steps in the process of

making pro-social decisions were related to whistle-

blowing, which was to consider whether the whistle-

blowing is wrong. In the theory of planned of

behaviour proposed by Ajzen (1991), either

predictor in shaping intention is attitude. Attitude

towards whistle-blowing refers to the extent to

which a person has a favourable evaluation or

assessment of the attitude towards the question. The

results of this study were consistent with the

research of Park and Blenkinsopp (2009), Winardi

(2013), and Bagustianto and Nurkholis (2015) which

stated that attitudes had a significant positive effect

on the intention to do whistle-blowing.

H

2

was accepted which means that organizational

commitment has a positive effect on whistle-

blowing intentions. Employees had similarities with

the values applied in the organization, and they

would be glad and proud to be part of the

organization, so that they easily approved the

policies set by the organization. Employees were

also willing to work on a variety of tasks and will try

hard so that the organization could achieve its

objectives because it has a high level of concern for

how the organization is going. As well as employees

felt their current organization is the best

organization, so they would be pleased and fortunate

to be able to work at the BPK or Inspectorate.

This result was supported by pro-social

behaviour theory and the concept of organizational

commitment, that whistle-blowing is a positive

social behaviour that can provide benefits to the

organization in the form of protecting the

organization from the dangers of fraud (fraud). Brief

and Motowidlo (1986) mention one of the

antecedents of pro-social theory namely

organizational commitment. This component of

organizational commitment showed the disposition

of pro-social behaviour, which were individuals

committed to the organization would be willing to

contribute to the welfare of the organization.

Employees who had high organizational

commitment tent to have a sense of ownership and

had high loyalty and when the values existing in the

organization were inherent in the employees so that

the organization was a part of themselves, so that

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

966

they had high responsibilities to protect the

organization either by doing whistle-blowing. This

results were in line with the research conducted by

Napitupulu (2016) and Bagustianto and Nurkholis

(2015) which stated that organizational commitment

had a positive effect on the intention to do whistle-

blowing.

6 CONCLUSIONS

A total of 135 civil servants working at the Audit

Board of the Republic Indonesia Representative of

Central Java Province and Inspectorate of Central

Java Province responded that they had the intention

to become whistleblowers if they knew that fraud

had occurred in their workplace which caused losses

to the state. The conclusions from this study are;

partially attitudes towards whistle-blowing, and

organizational commitment, have a positive effect

on whistle-blowing intentions. It can be concluded

that in the formation of intentions to conduct

whistleblowing influenced factor from within

oneself to form the intention and required the

existence of self-control from various limitations.

REFERENCES

ACFE. (2016). Report to the Nations on Occupational

Fraud and Abuse 2016 Global Fraud Study. USA.

Ahmad, S. A., Smith, M., & Ismail, Z. (2012). Internal

whistle-blowing intentions: A study of demographic

and individual factors. Journal of Modern Accounting

and Auditing, 8(11), 1632.

Ajzen, I. (1991). The theory of planned behavior.

Organizational Behavior and Human Decision

Processes, 50(2), 179–211.

Bagustianto, R., & Nurkholis, N. (2015). Factors

Affecting the Interest of Civil Servants to Take

Whistle-Blowing Actions (Study of BPK RI Civil

Servants). EKUITAS (Jurnal Ekonomi Dan

Keuangan), 19(2), 276–295.

Brief, A. P., & Motowidlo, S. J. (1986). Prosocial

organizational behaviors. Academy of Management

Review, 11(4), 710–725.

Dozier, J. B., & Miceli, M. P. (1985). Potential predictors

of whistle-blowing: A prosocial behavior perspective.

Academy of Management Review, 10(4), 823–836.

Hwang, D., Staley, B., Te Chen, Y., & Lan, J. (2008).

Confucian culture and whistleblowing by

professional accountants: an exploratory study.

Managerial Auditing Journal, 23(5), 504–526.

https://doi.org/doi:10.1108/02686900810875316

Kaplan, S. E., & Schultz, J. J. (2007). Intentions to report

questionable acts: An examination of the influence of

anonymous reporting channel, internal audit quality,

and setting. Journal of Business Ethics, 71(2), 109–

124. https://doi.org/10.1007/s10551-006-0021-6

Manafe, M. W. N. (2015). Effects of Moral Reasoning,

Retaliation and Gender on the Trend of Internal

Whistleblowing. SUSUNAN REDAKSI JURNAL

WAHANA, 113.

Mowday, R. T., Steers, R. M., & Porter, L. W. (1979). The

measurement of organizational commitment. Journal

of Vocational Behavior, 14(2), 224–247.

Myers, D. G. (2012). Social Psychology, Issue 10.

Translator by Tusyani, A. Jakarta: Salemba

Humanika.

Napitupulu, G. B. (2016). Pengaruh Faktor

Organisasional, Faktor Individual, Dan Faktor

Demografi Terhadap Intensi Whistleblowing.

Simposium Nasional Akuntansi XIX Lampung.

Near, J. P., & Miceli, M. P. (1995). Near, Janet P Miceli,

Marcia P. The Academy of Management Review,

20(3), 679–708.

Park, H., & Blenkinsopp, J. (2009). Whistleblowing as

planned behavior–A survey of South Korean police

officers. Journal of Business Ethics,

85(4), 545–556.

Park, H., Blenkinsopp, J., Oktem, M. K., &

Omurgonulsen, U. (2008). Cultural orientation and

attitudes toward different forms of whistleblowing: A

comparison of South Korea, Turkey, and the UK.

Journal of Business Ethics, 82(4), 929–939.

Rothschild Miethe, Terance, J. (1999). Whistle-Blower

Disclosures and Management Retaliation. WORK

AND OCCUPATIONS, 26(1), 107–128.

Solikhah, B. (2014). An Application of Theory of Planned

Behavior towards CPA Career in Indonesia. Procedia

- Social and Behavioral Sciences, 164, 397–402.

https://doi.org/https://doi.org/10.1016/j.sbspro.2014.11

.094

Tavakoli, A. A., Keenan, J. P., & Crnjak-Karanovic, B.

(2003). Culture and Whistleblowing an Empirical

Study of Croatian and United States Managers

Utilizing Hofstede’s Cultural Dimensions. Journal of

Business Ethics, 43(1/2), 49–64.

https://doi.org/10.1023/A:1022959131133

Winardi, R. D. (2013). The Influence of Individual And

Situational Factors on Lower-Level Civil

Servants’whistle-Blowing Intention In Indonesia.

Journal of Indonesian Economy and Business: JIEB.,

28(3), 361.

The Civil Servants’ Intention to Be Whistle Blowers of Corruption Cases in Government Sector

967