Measurement of the Quality of Financial Accounting Information

Systems through Top Management Support and Leadership

Effectiveness

Jufri Darma

1

, Azhar Susanto

2

, Sri Mulyani

2

and Jadi Suprijadi

3

1

Faculty of Economics, Universitas Negeri Medan, Indonesia

2

Faculty of Economics and Business, Universitas Padjadjaran, Indonesia

3

Faculty of Mathematics and Natural Sciences, Universitas Padjadjaran, Indonesia

Keywords: Quality of Financial Accounting Information System, Top Management Support, Effective Leadership

Abstract: Researchers previously conducted research on top management support and leadership and in information

systems. This study aims to examine the influence of top management support and effective leadership on

the quality of financial accounting information system. Surveys are conducted on 270 respondents in 76

ministries and institutions of the Republic of Indonesia. The respondents are the users of financial

accounting information systems. Data is collected by using questionnaires. For data analysis we applied the

SEM-PLS Software. The results indicate that top management support and effective leadership have

significant influence on quality of financial accounting information system.

1 INTRODUCTION

Financial accounting information systems is crucial

to the operation of all organization (Gray &

Bebbington, 2001). Quality of financial accounting

information systems referring to characteristics that

describe the ability of information systems in

processing data to be financial information that

meets user expectations (DeLone & McLean, 1992;

Mandl, 2008: 112; Pham Thi & Helfert, 2009).

Financial accounting information system has quality

characteristics such as: reliability, integration and

accessibility (Bocij et al., 2015, Heidmann, 2008).

The reliability is the ability of financial accounting

information systems function properly and produce

accurate information (Bocij et al, 2015; Baltzan,

2014). Further integration is the integration of

subsystems, information systems with other systems,

and data from various sources (Valacich &

Schneider, 2016; Baltzan, 2014). While the

accessibility is information system can bes accessed

from anywhere and anytime by various users (Bocij

et al., 2015; Avison & Fitzgerald, 2006:).

In fact, accounting information system until now

can’t fully applied to various types of organizations

in Indonesia (Susanto, 2017) such as: universities

(Susanto, 2016 & 2017), higher educations

(Puspitawati, 2016), colleges (Susanto, 2018),

hospital (Fitrios, 2017), financial institutions

(Mulyani et al., 2016; Darma, 2017), government

owned company (Mulyani & Endraria, 2017;

Ladewi et al., 2017), National Zakat Management

Institutions (Nurhayati & Susanto, 2017).

The existing phenomenon that financial

accounting information systems in ministries and

institutions has not been reliable The tax system has

not had good financial accounting information, it is

still manual, so much so that fictitious invoices to

the taxpayer's tax record so it may not be optimal

(Brojonegoro, 2015). The problems in the

administration area of computer application system

are not optimal in supporting the preparation of

financial statements (Azis, 2015). In addition,

financial accounting information systems has not

been integrated. Budget user in ministry and

institution and the Ministry of Finance could not

perform their duties independently and own

themselves but must work together to ensure an

Darma, J., Susanto, A., Mulyani, S. and Suprijadi, J.

Measurement of the Quality of Financial Accounting Information Systems through Top Management Support and Leadership Effectiveness.

DOI: 10.5220/0009502210351042

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1035-1042

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1035

orderly budget execution and accountability

(Budiarso, 2014). Besides, financial accounting

information system is easily accessible. Towards the

deadline of SPT reporting on 31 March the server of

Directorate General of Taxes is disturbed because

many people reporting (Utama, 2016).

Management support is important component to

information systems success (Langer, 2008). Top

management support guarantees the availability of

the resources needed by the information system

(Olson, 2004). The availability of human resources,

hardware, software, data and networks is an

information system requirement (Marakas &

O’Brien, 2014). Management support in providing

various resources is needed in the implementation of

information systems (Stair & Reynolds, 2016)

Information systems will succeed optimally if they

get support from top management (Bocij, Greasley

& Hickie, 2015; Olson, 2015; Zaied, 2012; Laudon

& Laudon, 2016)

Top management support in this research are:

providing human resources, providing hardware,

providing software, and providing funds needed to

operate financial accounting information systems

(Bocij, Greasley & Hickie, 2015; Laudon & Laudon,

2016; Palvia & Palvia, 2003; Boonstra, 2013; Dong,

Neufeld & Higgins, 2009;Compean & Higgins,

1995).

Several previous research results show the effect

of top management support on information systems.

Support from top management is essential for

effective implementation of information systems

(Thong, Sing Yap & Raman, 1996). Top

management support is positively related to the

effectiveness of information systems (Seliem, et al,

2003). Top management support relates directly or

indirectly to the performance of information systems

(Ragunathan, et.al, 2004). Top management support

is significantly related to the quality of information

systems (Husein, et.al, 2007). Top management

support influences the use of management

accounting information systems (Gil & Hartman,

2007). The level of management support is related to

the level of quality of information systems (Medina

& Chaparro). Top management support has the most

powerful influence on information systems

(Rouibah, et.al, 2009). Management support very

helpful to improve the quality of information

systems (Zaied, 2012). Top management support is a

key factor for the success of information systems

(Chen, Zhao & Wang, 2012). One of the factors

consistently found to influence the success of

information systems is top management support

(Petter, DeLone & McLean, 2013). Top

management support has a strong effect on the

operation of information systems (Khan, Lederer &

Mirchandani, 2013). Top management support has

an effect on information systems (Al-Mamary,

Shamsudin & Aziati, 2014). Support from top

management is an important point for the success of

corporate information systems (Shao, Feng & Hu

(2015).

Leadership is key component in realizing the

government's financial accounting information

system of quality, so it takes the role of a leader who

can give an example (Budiarso, 2014). Leadership is

an important aspect to success of financial

accounting information system (Ward & Peppard,

2003). Leadership style is one of the features that

affect the financial accounting information system of

an organization (Laudon & Laudon, 2016).

The influence of leader on individual subordinate

i.e., leader improves: quality of subordinate life,

subordinate confidence, subordinate skills, and

development of subordinates (Yukl, 2013). The

influence of leaders in groups, i.e., leaders improve:

team work, group commitment, confidence of group

members in achieving goals, problem solving by

groups, and decision making by groups (Yukl,

2013). The influence of leader to organization i.e.,

leader help to: resolve disputes constructively,

efficiency of organizational activities, resource

accumulation, and organizational readiness in the

face of change (Yulk, 2013).

Previous research shows the influence of

leadership on information system. Stone (1994)

proves that leadership style is a significant factor in

influencing the successful application of information

systems. Thite (2000) found evidence that

transactional leadership effectiveness leads to a

successful level of information systems projects. Shi

(2007) proves that the leadership of information

systems have a positive impact on the performance

of information systems. Cho, Park & Michel (2011)

proves that transformational leadership is positively

associated with the success of information system

users. Fitriati & Mulyani (2015) found evidence that

leadership influences the success of accounting

information systems. Carolina (2015) found

evidence that transformational leadership has a

significant effect on accounting information

systems. Rapina (2015) also found evidence that

transformational leadership influences the successful

implementation of accounting information systems.

Mulyani & Endraria (2017) found evidence that

leadership style have significant effect on the

implemetantion enterprise resource planning system.

Fitrios (2017) found evidence that leadership

behavior significantly influences to accounting

information systems. Nurhayati & Susanto (2017)

found evidence that transformational leadership has

significant influence on success of accounting

information systems

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1036

This study aims to examine effect of top

management support and the effective leadership on

the quality of financial accounting information

systems in ministries and institutions of the Republic

of Indonesia.

Based on the above statement and the results of

previous research, the hypothesis in this study is :

1. Top management support significantly influence

on the quality of financial accounting

information system

2. effective leadership significantly influence on the

quality of financial accounting information

system

2 METHODOLOGY

This study uses descriptive and verification method.

The population in this study are all users of financial

accounting information system consisting of head of

finance bureau, head of finance department,

accounting department head and data entry staff in

86 units Reporting & Accounting in Ministry and

Institution of Republic of Indonesia. The sampling

technique used is simple random sampling to

obtained 270 respondents. The instrument that is

used for the collection data is questionnaire. The

questionnaires using Likert scale on five choices of

responses ranging from strongly disagree (1) and

strongly agree (5)

The questionnaire includes two variables

namely: top management support (TMS), leadership

effectiveness (LE) and quality of financial

accounting information system (QoFAIS). TMS

consists of four dimensions namely providing of

human resources (TMS1), hardware (TMS2),

software (TMS3), and fund (TMS4) as needed. The

dimensions of providing of human resources as

needed consists two indicators ie the suitability of

the data entry personnel (TMS11) and technical

(TMS12) to needs. Further, the dimensions of

providing of hardware as needed consists two

indicators i.e., the suitability of computer hardware

(TMS21) and communications network hardware

(TMS22) to needs. Furthermore, the dimensions of

providing of software as needed consists two

indicators ie the suitability of the operation systems

software (TMS31) and application software

(TMS32) to needs. While the providing of fund as

needed consists three indicators ie suitability of the

budget amount for: maintenance and replacement

hardware (TMS41), software (TMS42), and training

of data entry personnel (TMS43) to needs.

LE consists of three dimensions namely

influence of leader on individual subordinate (LE1),

influence of leader on group (LE2) and influence of

leader on organization (LE3). LE1 consists four

indicator i.e., leader improves the quality of

subordinate life (LE11), leader build subordinate

confidence (LE12), leader improve subordinate

skills (LE13), and leader contribute to the

development of subordinates (LE14). LE2 consists

five indicators i.e., leader enhance teamwork

(LE21), leader increase group commitment (LE22),

leader increase members group confidence in

achieving goals (LE23), leader improve problem

solving by group (LE24), and leader improve

decision making by group (LE25). LE3 consists four

indicators i.e., leader help to resolve disputes

constructively (LE31), leader contribute to the

efficiency of organizational activities (LE32), leader

contribute to resource accumulation (LE33), and

leader contribute to organizational readiness in the

face of change (LE34).

QoFAIS consists of three dimensions namely

reliability of financial accounting information

system (QoFAIS1), integration of financial

accountig information system (QoFAIS2) and

accessibility of finnancial accounting information

system (QoFAIS3). QoFAIS1consists two indicators

i.e. ability of financial accounting information

system function properly (QoFAIS11) and ability of

financial accounting information system to produce

accurate information (QoFAIS12). QoFAIS2

consists three indicators i.e., the integration

subsystem in the financial accounting information

system (QoFAIS21), integration financial of

accounting information system with other

information systems (QoFAIS22) and integration of

data from various sources (QoFAIS23). QoFAIS3

consists two indicators i.e., the ability ability of

financial accounting information system accessed

anytime by user (QoFAIS31) and the ability of

financial accounting information system accessed

from various place by user(QoFAIS32).

All causal relationships between indicators and

constructs in this study used a reflective

measurement model. The data analysis we applied

the variance based structural equation modeling

method.

3 RESULT AND DISCUSSION

Demography of Respondent: Based on the answers

of the respondents on questions relating to gender,

age, education level, and educational background.

The gender of male dominated respondents as much

as 154 respondents or 57.04%, based on age of

respondents dominated age between 30-39 years that

is as much as 118 respondents or 43.70%, based on

education level most respondents are bachelor that

Measurement of the Quality of Financial Accounting Information Systems through Top Management Support and Leadership Effectiveness

1037

is as much as 155 respondents or 57.41%, and based

on the educational background of most respondents

background accounting that is as much as 158

respondents or 58.52%

Assessment of Measurement Model: The reflective

measurement model is considered to meet validity if

the extracted average variance (AVE) is higher than

0.5 and the outer load indicator on the construct

must be higher than all the cross loads with the other

constructs. The reflective measurement model is

considered reliable if the composite reliability and

outer load indicator is higher than 0.708 (Hair,

et.al.,2014). The of evaluation first order on outer

model, we found that the outer loading of all items

used to measure each dimension of top management

support, leadership effectiveness and quality of

financial accounting information systems is above

0.7. Average variance extracted above 0.5 it’s

concluded that the reflective measurement model is

valid. Likewise, composite reliability and all

indicator outer loading higher than 0.708, it’s

concluded that the reflective measurement model is

reliable (see Table 1)

Table 1: Result of Validity and reliability Test

Variabel Indicator

Composite

Reliability

(CR)

Average

Variance

Extracted

(AVE)

Top

Management

Support

(TMS

TMS 0,929 0.596

TMS1 0,919 0,850

TMS2 0,955 0,914

TMS3

0,973 0,948

TMS4

0,915 0,784

Leadership

Effectiveness

(LE)

LE

0,871 0,501

LE1

0,836 0,603

LE2

0,803 0,741

LE3

0,844 0,758

Quality of

Financial

Accounting

Information

System

(QoFAIS)

QoFAIS

0,946 0,580

QoFAIS1

0,854 0,720

QoFAIS2

0,934 0,578

QoFAIS3

0,926 0,732

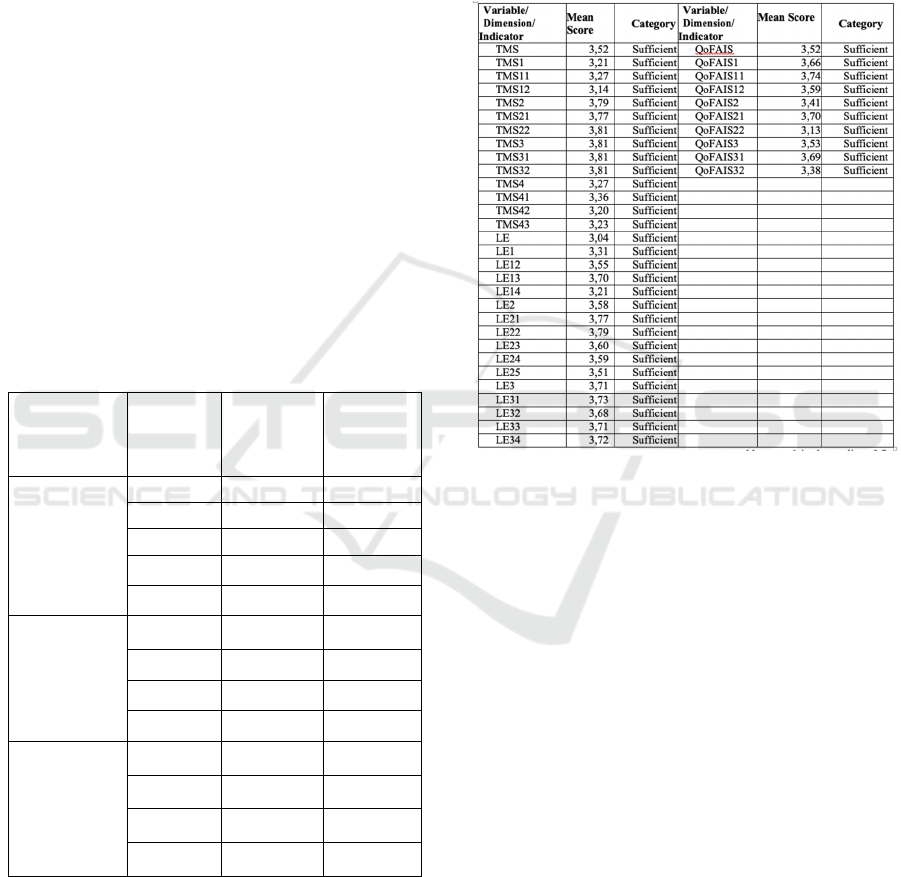

Descriptive Statistics: Two hundred seventy

questionnaires from user of financial accounting

information systems at 76 Ministries and Institutions

of Republic of Indonesia (78.49%) were returned

and completed. Inter-quartile range (IQR) was used

to categorize the respondents’ responses (Cooper &

Schindler, 2014). The category of respondents’

responses are : an mean score : 1,00-1,99 (poor),

2,00-2,99 (less), 3,00-3,99 (sufficient) and 4.00-5,00

(good). Descriptive statistics show that all

dimensions and indicators have mean scores

between 3.04 - 3.79 or below 4 so that the categories

are “sufficient” (see Table 2)

Table 2: Descriptive Statistics

Hypothesis Testing: The hypothesis to be tested in

this study are:

Ho1: Top management support have not significant

influence on the quality of financial accounting

information systems.

Ha1: Top management support have significant

influence on the quality of financial accounting

information systems.

Ho1 is accepted if significance level <5%. Based

on result of the analysis we found the significance

level is 0,039 (see Table 3). This means that Ho1 is

rejected or in other words top management support

have significant influence on quality of financial

accounting information system. Path coefficient

between top management and quality of financial

accounting information systems is 0.128, coefficient

determination (R2) is 0,016. this means that top

management able to explain the quality of financial

accounting information system equal to 1,6%,

Ho2: Effective leadership have not significant

influence on the quality of financial accounting

information systems.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1038

Ha2: Effective leadership have significant influence

on the quality of financial accounting information

systems.

Ho is accepted if significance level <5%. Based on

result of the analysis we found the significant level

is 0,777(see Table 3). This means that Ho2 is

rejected or in other words effective leadership have

significant influence on quality of financial

accounting information system. Path coefficient

between effective leadership and quality of financial

accounting information systems is 0.777, coefficient

determination (R2) is 0.603 this means that effective

leadership able to explain the quality of financial

accounting information system equal to 60,3%

Table 3: Result of Data Analysis

No

Variable

Path

Coefficiet

P

Value

Significant

1

QFAIS TMS 0,128 0,039

2

LE 0,777 0,000

The results of testing the hypothesis about the

influence of top management support on the quality

of financial accounting information systems indicate

that the path coefficient value is

0.128 with a significance of 0.39 so it can be

decided that H0 is rejected, so it can be concluded

that top management support has a positive effect on

the quality of financial accounting information

systems. The results of this study provide empirical

evidence that the better the top management support,

the more appropriate human resources, hardware,

software and existing funds with needs, the more it

will improve the quality of financial accounting

information systems. In other words, the quality of

the financial accounting information system will

increase if the support of top management is getting

better.

The results of this study are in line with the

statements of several experts. Management support

will lead to improved system quality (Zaied, 2012).

The success of the application of information

systems is due to the high support of top

management (Laudon & Laudon, 2016: 590). Top

management support has often proven to be an

important factor for the success of information

systems (Olson, 2015: 11).

Top management support, namely top

management guarantees the availability of resources

needed by information systems (Olson, 2004: 13).

Top management support for the quality of the

financial accounting information system in the

ministries and institutions of the Republic of

Indonesia is realized in the form of providing

various resources that are in accordance with the

operational requirements of the financial accounting

information system.

The quality of financial accounting information

systems in ministries and institutions depends on the

suitability of various existing resources with needs

such as: human resources (personnel), hardware,

software and funds. This is in line with the

statements of several experts. Information systems

depend on human resources, hardware, software, and

networks (Marakas & O’Brien 2014: 28). Resources

needed in the implementation of accounting

information systems include: enthusiastic resources,

hardware, software and funds. Management support

ensures that information systems receive sufficient

funds and resources for their success (Laudon &

Laudon, 2016: 591). Furthermore, top management

support related to resources is the provision of funds

needed for hardware, software and others (Dong,

Neufeld & Higgins, 2009).

Empirical evidence about the influence of top

management support on the quality of financial

accounting information systems in ministries and

institutions, in line with the results of previous

studies conducted by: Thong, Sing Yap & Raman

(1996), Seliem, et al. (2003), Ragunathan, et al.

(2004), Husein, et al. (2007), Gil & Hartman (2007),

Medina & Chaparro (2008), Rouibah, Hamdy & Al-

Enezi (2009), Zaied (2012), Chen, Zhao & Wang

(2012), Petter, DeLone & McLean (2013 ), Khan,

Lederer & Mirchandani (2013), Al Mamary,

Shamsudin & Nor Aziati (2014), and Shao, Feng &

Hu (2015).

Furthermore, the results of testing the hypothesis

about the effect of leadership effectiveness on the

quality of financial accounting information systems

indicate that the path coefficient value is 0.777 with

a significance of 0.000 so that it can be concluded

that leadership effectiveness has a positive effect on

the quality of financial accounting information

systems. The results of this study provide empirical

evidence that the more effective leaders in

influencing subordinate individuals, groups and

organizations will lead to increased quality of

financial accounting information systems. In other

words, the quality of financial accounting

information systems will increase if leadership

becomes more effective.

The results of this study are in line with the

statements of several experts. Leadership is an

important aspect in achieving success in financial

accounting information systems (Ward & Peppard,

2003: 369). The same thing, leadership is one

Measurement of the Quality of Financial Accounting Information Systems through Top Management Support and Leadership Effectiveness

1039

feature that influences financial accounting

information systems (Laudon & Laudon, 2016: 116).

Then strong effective leadership is needed in order

to achieve successful implementation of financial

accounting information systems (Stair & Reynold,

2016: 399)

Empirical evidence about the effect of leadership

effectiveness on the quality of financial accounting

information systems in the accounting and reporting

section of the ministries and institutions of the

Republic of Indonesia is in line with the results of

previous studies such as: Stone (1994), Thite (2000),

Shi (2007), Cho, Park & Michel (2011), Azmi

Fitriati & Mulyani (2015), Carolina (2015) and

Rapina (2015).

4 CONCLUSION

This study aims to measure the quality of financial

accounting information systems that are influenced

by top management support and effective leadership.

The results of this study show evidence that top

management support and leadership effectiveness

influence the quality of financial accounting

information systems. It can be concluded that this

model can be used to measure the quality of

financial information systems..

ACKNOWLEDGEMENT

The researcher would like to thank the ministers and

heads of the Republic of Indonesia's institutions and

all respondents who have supported this research.

REFERENCES

Al-Mamary, Y.H., Shamsuddin, A., and Nor Aziati, A.H.

(2014). Key factors enhancing acceptance of

management information systems in Yemeni

companies. Journal of Business and Management

Research, 5 (2014) 108-111.

Avison, D. And Fitzgerald, G. (2006). Information

Systems Development – Methodologies. Techniques

and Tools. Fourth Edition. New York: The McGraw-

Hill

Azis, H.A. (2015).

http://nasional.kontan.co.id/news/keuangan-

pemerintah-masih-bermasalah. Azis, H.A. 2016.

http://ekbis.sindonews.com/read/1114372/33/bpk-

ungkap-6-masalah-laporan-keuangan-pemerintah-

2015-1465191938

Baltzan, P. (2014). Business Driven Information System.

Fourth Edition. New York: The McGraw- Hill

Bocij, P., Greasley, A. and Hickie, S. (2015). Business

Information Systems Technology, Development and

Management for the E-Business. Fifth edition.

London: Pearson Education Limited

Brojonegoro, B. (2015)

http://bisniskeuangan.kompas.com/read/2015/07/14/11

2059526/Menkeu.Banyak.Faktur.Fiktif.Penerimaan.N

egara.Tergerus

Budiarso, T. (2014).

http://www.kemendagri.go.id/article/2014/02/27/imple

mentasi-sistem-keuangan-pemerintah.

Carolina, Y. 2015. How to Attain Accounting Information

Systems Quality? (Empirical Evidence from

Manufacturing Company in Bandung – Indonesia).

Australian Journal of Basic and Applied Sciences.

Vol. 9 (9) pp.87-94.

Chen, X.C., Zhao, Z. and Wang, Y.F. (2012). The Effects

of Top Management Support on Information System

Success: Manufacturing Industry Cases. Applied

Mechanics and Materials Vols 157-158 (2012) pp 344-

348.

https://doi.org/10.4028/www.scientific.net/AMM.157-

158.344

Cho, J., Park, I. and Michel, J.W. (2011). How does

leadership affect information systems success? The

role of transformational leadership. Information &

Management 48: 270–277.

Cooper, D.R. and Schindler, P.S. (2014). Business

Research Methods. Twelfth Edition. New York:

McGraw-Hill Education.

Darma, J. (2017). How the Clarity of Business Vision

Affect the Quality of Business Intelligence Systems

and It’s Impact on the Quality of decision Making

(Evidence from North Sumatera- Indonesia). Journal

of Engineering and Applied Sciensce. 12 (9): 2461-

2466

DeLone, W.H. and McLean, E.R. (1992). Information

System Success: The Quest for The Independent

Variable. Information System research. 3 (1): 60-95

Dong, L., Neufeld, D. and Higgins, C. (2009).Top

management support of enterprise systems

implementations. Journal of Information Technology

24, pp.55–80. DOI: https://doi.org/10.1057/jit.2008.21

Fitriati, A. dan Mulyani, S. (2015). Factors That Affect

Accountinng Information System Success and It’s

Implication on Accounting Information Quality. Asian

Journal of Information Technology 14 (5). Pp.154-

161. DOI: 10.3923/ajit.2015.154.161

Fitrios, R. 2017. Leadership Behavior and Accounting

Information System ( An Empirical Study at the

Hospitals in Riau Province-Indonesia. Journal of

Engineering and Applied Sciences. 12 (22): 6062-

6068.

Gil, D.N. and Hartmann, F. (2007). Management

accounting systems, top management team

heterogeneity and strategic change. Accounting,

Organizations and Society 32. Pp. 735–756.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1040

http://www.sciencedirect.com/science/article/pii/S036

1-3682(06)00078-X

Gray, R and Bebbington, J. (2001). Accounting for the

environment. Second Edition. London: SAGE

Publications Ltd.

Hair Jr., J.F., Hult, G.T.M., Ringle, G.M. & Sarsted, M.

(2014). A Primer Partial Least Squares Structural

Equation Modeling (PLS-SEM), Los Angeles: Sage

Publications, Inc

Heidmann, M. (2008). The Role of Management

Accounting Systems in Strategic Sensemaking.

Germany: Deutscher Universitats-Verlag Wiesbaden

Husein, R., Abdul Karim, N.S., Mohamed, N., & Ahlan,

A.R. (2007). The Influence Organizational Factors on

Information Systems Success in E-Government

Agencies in Malaysia. The Electronic Journal on

Information System in Developing Countries 29, 1, 1-

17. https://doi.org/10.1002/j.1681-

4835.2007.tb00195.x

Khan, S.A., Lederer, A.L., and Dinesh A. Mirchandani.

(2013). Top Management Support, Collective

Mindfulness, and Information Systems Performance.

Journal of International Technology and Information

Management. Volume 22, Number 1 pp.95-122.

http://scholarworks.lib.csusb.edu/jitim/vol22/iss1/6

Laudon, K.C., and Laudon, J.P.( 2016). Management

Information System: Managing the Digital Firm,

Fourteenth Edition, London: Pearson Education

Limited

Ladewi, Y., Susanto, A., Mulyani, S. & Suharman, H.

(2017). Effect of Organizational Commitment on the

Quality of Accounting Information Systems and their

Impact on the Quality of Accounting Information.

Journal of Engineering and Applied Sciences, 12

(24):7649-7655

Langer, A.M. (2008). Analysis and Design of Information

Systems. Third Edition. London: Springer-Verlag

Limited

Mandl, T. (2008). Automatic Quality Assessment for

Internet Pages. Munoz, C.C., Moraga, A., and Piattini,

M.(eds.). Handbook of Research on Web Information

Systems Quality. New York: Information science

reference.

Marakas, G.M. & O’Brien, J.A. (2014). Introduction To

Information Systems. International Edition. New

York: The McGraw-Hill Companies, Inc.

Medina, M.Q. and Chaparro, J.P. (2008). The Impact Of

The Human Element In The Information Systems

Quality For Decision Making And User Satisfaction.

Journal of Computer Information Systems. Winter

pp:44-52.

https://www.tandfonline.com/doi/abs/10.1080/088744

17.2008.11646008

Mulyani, S., Darma, J. & Sukmadilaga, C. (2016). The

Effect of Clarity of Business Vision and Top

Management Support on the Quality of Business

Intelligence Systems: Evidence from Indonesia. Asian

Journal of Information Technology 15 (16): 2958-

2964

Mulyani, S., Hasan, R. & Anugrah, P. (2016). The Critical

Factors for the Use of Information Systems and its

Impact on the Organizational Performance.

International Journal Management, 10 (4): 552-560.

Mulyani, S. & Endraria. (2017).The Empirical Testing for

the Effect of Organizational Commitment and

Leadership Style on the Implementation Success of

Enterprises Resource Planning Systems and Its

Implications onn the Quality of Accounting

Information. Journal of Engineering and Applied

Sciences. 12 (20): 5196-5204.

Nurhayati, N & Susanto, A. (2017). The Influence of

Transformational Leadership on the Success of

Accounting Information Systems Implementation

(Survey on National Zakat Management Institution of

West Java). Journal of Engineering And Applied

Sciences. 12. (17): 4534-4539

Olson, D.L. (2004). Information System Project

Management. Second Edition. New York. The

McGraw-Hill Companies, Inc.

Olson, D.L. (2015). Information System Project

Manajemen. New York: Business Expert LLC.

Petter, S., DeLone, W. and McLean, E.R. (2013).

Information System Success: The Quest for the

Independent Variables. Journal of Management

Information Systems/ Spring Vol 29, No.4, pp.7-61.

DOI: 10.2753/MIS0742-1222290401

Pham Thi, T.T. and Helfert, M. (2009). An Information

System Quality Framework Based on Information

System Architectures. Barry; C., Conboy, K., Lang,

M., Wojtkowski, G., and Wojtkowski, W. (Editors).

Information Systems Development. Challenges in

Practice, Theory and Education. Volume 2. New York:

Springer Science+Business Media, LLC.

Puspitawati, L. (2016). The Analysis Of Effectiveness

Measurement In Accounting Information Systems

Through Competence Factor Of Information System

User (Research on Higher Education in Bandung).

IJABER. 14 (1): 313-339

Ragunathan, B.S., Apigian, C.H., Ragu-Nathan, T.S. and

Tu, Q. (2004). A Path Analytic Study of The Effect of

Top Management Support for Information System

Performance. Omega. International Journal of

Management Science, 32, pp: 459-471.

https://kundoc.com/pdf-a-path-analytic-study-of-the-

effect-of-top-management-support-for-information-

sy.html

Rapina. (2015). Factors that Affect Accounting

Information Systems and Accounting Information

(Survey on Local Bank in Bandung-Indonesia).

Australian Journal of Basic and Applied Sciences.

Vol. 9 (9) pp.78-86

Rouibah, K., Hamdy, H.I., and Al-Enezi, M.Z. (2009).

Effect of Management Support, Training, and User

Involvement on System Usage and Satisfaction in

Kuwait. Industrial Management and Data Systems.

Vol. 109. No.3. pp.338-356.

Seliem, A.A.M., Ashour, A.S., Khalil, O.E.M and Millar,

S.J. (2003). The Relationship of Some Organizational

Factors to Information Systems Effectiveness: A

Measurement of the Quality of Financial Accounting Information Systems through Top Management Support and Leadership Effectiveness

1041

Contingency Analysis of Egyptian Data. Journal of

Global Information Management. 11 (1) pp.40-71,

Jan-Mar. DOI: 10.4018/jgim.2003010103

Shao, Z., Feng, Y. and Hu, Q. (2015). Effectiveness of top

management support in enterprise systems success: a

contingency perspective of fit between leadership style

and system life-cycle. European Journal of

Information Systems (2015), pp.1–23. DOI:

10.1057/ejis.2015.6

Shi, Z..( 2007). An Empirical Test of IS Leadership as The

Driving Force in Improving IS Performance. Journal

of Information, Information Technology, and

Organizations. 2: 61- 77

Stair, R.M., and Reynolds, G.W. (2016). Fundamentals of

Information Systems. Eighth Edition. USA: Cengage

Learning.

Stone, R.D. (1994). Leadership and Information System

Management: A Literature Review. Computer in

Human Behavior.Vol.10. No.4 pp:559-568

Susanto, A. (2016). The Empirical Testing How the

Quality of Accounting Information Systems Affected

by Organizational Culture. Research at Universities in

Bandung. Asian Journal of Information Technology.

15 (6): 1098-1105.

Susanto, A. (2017). How the Quality of Accounting

Information System Impact on Accounting

Information Quality (research on Higher Education in

Bandung. Journal of Engineering and Applied

Sciences. 12 (14): 3672-3677.

Susanto, A. (2018). How Internal Control and

Organizational Structure Impact on Accounting

Information System. Journal Engineering and Applied

Sciences, 13 (8):1935-1941

Thite, M. (2000). Leadership Styles in Information

Technology Projects. International Journal of Project

Management. 18: 235-241

Thong, J.Y.L., Sing Yap, C. and Raman, K.S. (1996). Top

Management Support, External Expertise and

Information Systems Implementation in Small

Businesses. Information Systems Research. Vol 7. No.

2 Juni. Pp.248-267.

Utama, M.S. (2016).

http://www.beritakepo.com/2016/03/situs-djp-sulit-

diakses-e-filing-spt.html Valacich, J. and Schneider,

C. 2016. Information Systems Today Managing in the

Digital World, Seventh Edition, England: Pearson

Education, Limited

Valacich, J. and Schneider, C. (2016). Information

Systems Today Managing in the Digital World,

Seventh Edition, England: Pearson Eduction Limited

Ward, J. and Peppard, J.. (2003). Strategic Planning for

Information Systems. Third Edition. England: John

Wiley & Sons

Yukl, G. (2013). Leadership in Organization. Eighth

Edition. England: Pearson Education Limited..

Zaied, A.N.H. (2012). An Integrated Success Model for

Evaluating Information System in Public Sectors.

Journal of Emerging Trends in Computing and

Information Sciences. Vol. 3 No.6 July. page: 814-825

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1042