The Role of Spirituality Workplace for Reducing Motivation

of Accounting Fraud

Sri Handayani¹, Adrie Putra

1

, Abdurrahman

1

and Rudianto

1

1

Accounting Department, Economic and Bussiness Faculty, Universitas Esa Unggul, Jakarta

Keywords: Earning Management Motivation, Spiritually Workplace, Meaningful Work, Sense of Community,

Alignment with Organizational

Abstract: The motivation of earnings management is more due to the general assumption that accounting figures,

especially profit are one of the important sources of information used by investors in valuing stock prices.

Existing business ethics cannot effectively prevent earnings management by corporate managers. The

development of spirituality in the workplace can transfer ethics and social justice into values, from within

individuals. This study aims to discuss the influence of spirituality workplace on earnings management

motivation.The subject of this research is a management accountant who works in a business company in

Jakarta. This study uses data derived from questionnaires that have been filled by 270 accountants. The

sampling method used is purposive sampling. Sample criteria are accountants who work more than one year

in a business company.The design of this study is explanatory causal. While the analysis tool used is

multiple regression analysis.The results of this study explain that workplace spirituality affects the

motivation of earnings management.While partially, the results of the study indicate that meaningful work

that represents individuals spiritually has a positive influence on motivation to commit fraud in the financial

reporting process. Organizational spirituality represented by harmony with organizational values influences

the decline in earnings management motivation, but the sense of community that represents group

spirituality does not have an impact on earnings management motivation.

1 INTRODUCTION

Economic activities reflect the will, experience, and

emotions of people, and thus reveal the human

nature and moral content (Chen,2012). Spirituality

can be explained as that every individual and

organization has the responsibility to build the

economic, social and environmental events in his

organization, which are related to the 'holy spirit'.

Therefore in the field of management studies,

discussion of spirituality has emerged, and it is

expected that spiritual management can be effective

in the era of knowledge economy (Sheep, 2006;

Moore and Casper, 2006)[2].

This is mainly due to the assumption that

accounting is only an activity related to the

counting-transaction of companies that are far from

the context of spirituality. The paradigm shift in the

information age has prompted many institutions to

begin the problem of exploring the spirituality and

spiritual feelings that exist from the workplace.

(Enough,2002) states that spirituality in the

workplace helps individuals to avoid attitudes and

actions that can jeopardize their career development.

Increased spirituality within the organization is

believed to increase the company's value and return

on investment. Earnings management is highly

relevant to human greed [Scott, 2006]. The goal of

earnings management is to give false beliefs to

operational performances that mislead interested

parties [Healy and Wahlen, 1999]. Therefore,

earnings management violates company ethics and

harms social justice. Forster [2008] explains that

modern enterprise management must come from

higher spiritual elements than simply manipulating

financial statements in order to explain maximum

benefits.

This study divides spirituality in the workplace

into three levels for analysis including the spiritual

awakening of the individual, group spirituality and

organizational spirituality. Spiritual awakening

refers to the value of life and meaning through work

experience or workplace, the process of

introspection in which individuals deeply connect

with others. Organizational spirituality is the

Handayani, S., Putra, A., Abdurrahman, . and Rudianto, .

The Role of Spirituality Workplace for Reducing Motivation of Accounting Fraud.

DOI: 10.5220/0009951327212727

In Proceedings of the 1st International Conference on Recent Innovations (ICRI 2018), pages 2721-2727

ISBN: 978-989-758-458-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

2721

formation of a shared identity and a sense of concern

in an organization. Accountants feel the meaning of

life in working through spiritual conversation,

listening, and overcoming pressure and challenges

through spiritual learning and growth (Chen, 2013).

The results of Bunia and Mukhuti (2011) and Chen

(2012) explains that there is a negative influence

between spirituality in the workplace and earnings

management. Spirituality in the workplace can

reduce the size of earnings management motivation.

Previous research indicates the existence of

motivation and profit management strategies used in

providing information. Generally accepted earnings

management information in the company is not

specific information (casuistic). Komarudin et al.

(2007) explain that there is an increase in debt

covenant and political cost motivation will improve

earnings management practices This study aims to

analyze the influence of spiritually workplace which

includes the spiritual level of the individual, spiritual

level of the group and spiritual level of organization

toward earnings management motivation.

2 LITERATURE REVIEW AND

HYPOTHESES

DEVELOPMENT

2.1 Earnings Management

Earnings management is the choice by a manager of

accounting policies toachieve some specific

objective (Scott,2000). Healy (1985) explains that

two approaches can be used to detect manager

behavior in managing earnings, by controlling the

accrual transactions on income and loss statements

that are not represented by cash flows and secondly,

changes in accounting policies.

2.2 Earning Management Motivation

Earning management aims to achieve certain

objectives by manipulating accounting practices,

based on generally accepted accounting principles,

so that the income displayed on the financial

statements reaches predetermined targets. Relevant

literature can be divided into two categories: (1) risk

assessment, which aims to develop analytical or

predictive indicators to evaluate the level of earnings

management and assist in differentiating the quality

of profit information [Hansen et al: 1996],

[Summers and Sweeney: 1998] and (2) fraud

assessments, aimed at analyzing the intelligence

ability of auditors of immoral behavior [Bernardi:

1994; Reckers and Schultz: 1993]. Chen [2012]

explains that earnings management motivation can

be divided into the following categories:

2.2.1 Attitude and Belief

This category refers to the perceptions and trends of

individual behavior toward earnings management

practices that can be classified into altruism,ie

corporate interests for personal gain such as

bonuses, and behavioral beliefs, that is, the potential

pro and contra expectations resulting from

earningsmanagement behavior. [Fischer and

Rosenzweig: 1995] explain that accountants are

more sensitive to accounting manipulation, whereas

managers are more tolerant of manipulation of

operations.

2.2.2 Pressure from Affiliated Parties

This category refers to the tendency of management

to becomeinvolved in earnings management due to

pressure from financially affiliated parties, such as

supervisors, associates, accountants, shareholders,

creditors, or analysts. (Ayres:1994) argues that the

motivation for profit manipulation is likely to meet

shareholder expectations regarding dividend

payouts. (DeZoort and God,1994), Becker et al.

(1998), and Dezoort (2001) suggests that

accountants can engage in earnings management

under pressure from peers, clients, or superiors.

2.3 Workplace Spirituality

Workplace spirituality is a new concept in the

management model and institutional behavior,

especially organizational culture. This concept has

actuallybeen described in the concepts of

organizationalbehavior such as values and ethics.

This is explained by (Robbins,2005) The concept of

workplace spirituality draws on our previous

discussion of topics such as values, ethics,

motivation, leadership, and work/life balance. As a

new concept, many parties think workplace

spirituality is the management of religion

[Amalia:2012]. Spirituality is the innate capacity

based on the structures of the brain that give us the

basic ability to form meaning, values, and beliefs.

There are three main dimensions of workplace

spirituality (Milliman et al., 2003) quoted from

(Amalia:2012), i.e. purpose in one's work or

"meaningful work", having a "sense of community",

and being "aligned with the organization's values"

and mission. Each of these dimensions represents

ICRI 2018 - International Conference Recent Innovation

2722

the three levels of workplace spirituality, i.e.

individual level, group level, and organizational

level.

2.3.1 Meaningful Work Represents the

Individual Level

Meaningful work is a fundamental aspect of

workplace spirituality that consists of having the

ability to feel the deepest meaning and purpose of

one's work. This dimension represents how workers

interact with their work day by day on an individual

level.

2.3.2 Sense of Community Represents the

Group Level

This dimension refers to the group level of human

behavior and focuses on the interaction between

workers and their co-workers. At this level,

spirituality consists of the mental, emotional, and

spiritual relationship of the worker in a team or

group in an organization. The core of this

community is the deep connection between people,

including support, freedom of expression, and

shelter.

2.3.3 Alignment with Organizational Values

that Represent the Level of the

Organization

This third aspect shows the experiences of

individuals who have strong alignments between

their personal values and the mission and goals of

the organization. This relates to the premise that the

organization's purpose is greater than itself and one

must contribute to the community or other parties.

We asked respondents about workplace

spirituality based on the dimensions presented

[Milliman et al., 2003] quoted from Amalia [2012],

i.e. purpose in one's work or meaningful work,

having a sense of community, and being in

alignment with the organization's values and

mission. Each of these dimensions represents the

three levels of workplace spirituality, i.e. individual

level, group level, and organizational level. Studies

on earning management motivation are focused on

behavioral perspectives. As quoted in (Chen,2012)

explains that earnings management motivation can

be divided into 1) Attitude and belief 2) Pressure

from affiliated parties. Earnings management is the

choice of accounting policies by managers for

specific purposes.

The research model used as the basis for

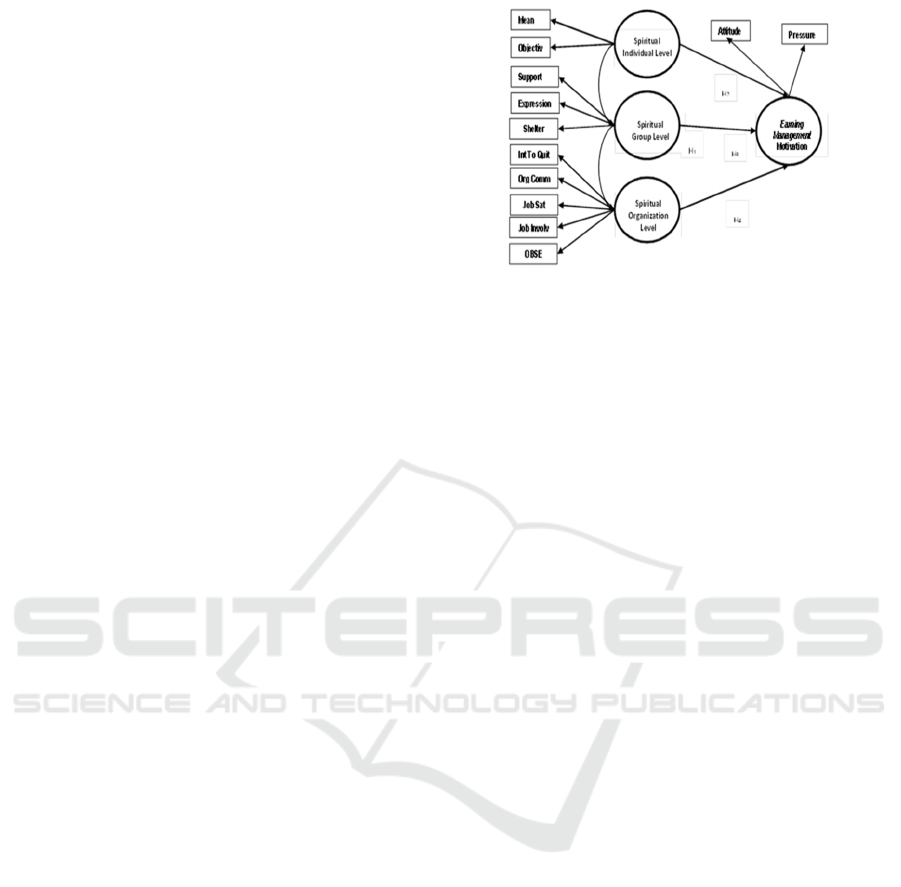

preparing the hypothesis is as follows:

Figure

1: Research Model

The motivation for earnings management can

also derive speculative motivation that refers to a

personal motive aimed at managing income arising

from the need to increase personal bonuses and

remuneration, to gain promotional opportunities, and

to meet annual profit targets. The tendency to

manage income may also be due to the requirements

of others such as supervisors, colleagues,

accountants, shareholders, creditors, and analysts.

Spirituality in the workplace is an important

sense of self, energized and happy with work.

Accountants who feel the spiritual situation in the

workplace are intrinsically motivated as they

experience, be trusted, and have competence related

to their work. If they consider the task to be fun,

interesting or meaningful, then this condition will

affect speculative motivation which refers to

personal motives by making accountants motivated

to work for pleasing parties such as supervisors,

colleagues, accountants, shareholders, creditors, or

analyst (Chen,2012).

Hypothesis 1: Spiritual level of the individual,

Spiritual level of the group, and Spiritual level of

organization simultaneously influence toward

Earnings Management Motivation.

Individual spirituality can be defined as having

the ability to feel the deepest meaning and purpose

of one's work. This dimension represents how

workers interact with their work day by day on an

individual level. It is based on the assumption that

humans have their own deepest motivation, truth and

desire to carry out activities that bring meaning to

their lives and the lives of others. After all,

spirituality sees work not only as a fun and

challenging thing, but also about things like

searching for deepest meaning and purpose,

animating one's dreams, fulfilling one's life's needs

by finding meaningful work, and contributing to

others (Chen:2012).

The Role of Spirituality Workplace for Reducing Motivation of Accounting Fraud

2723

Hypothesis 2: Spiritual Individuals significant

effect on Earning Management Motivation.

The sense of community represents the group

level. This dimension refers to the group level of

human behavior and focuses on the interaction

between workers and their co-workers. Spirituality

at this level consists of the mental, emotional, and

spiritual relationships of workers in a team or group

in an organization the core of this community is the

deep connection between people, including support,

freedom of expression, and shelter. At this level the

accountant feels that everyone has a common goal,

with a good common goal, of course, will not make

the accountant be motivated to take actions that are

not mutual interests. Therefore, it can be said that

with strong group-level spirituality it will give full

awareness to accountants not to be motivated to

practice earnings management (Chen:2012).

Hypothesis 3: Group spirituality has significant

effect on Profit Management Motivation

The third fundamental aspect is alignment with

organizational Values representing the

organizational level. This third aspect shows the

experiences of individuals who have strong

alignments between their personal values and the

mission and goals of the organization. This relates to

the premise that the organization's purpose is greater

than itself and one must contribute to the community

or another. Therefore, with a strong level of

organizational level of spirituality, the accountant

will be aware of the ugliness of earnings

management actions for the survival of the

company, so with a high level of spirituality level of

the organization will decrease earning management

motivation (Chen,2012)..

Hypothesis 4: Organization Spirituality has a

significant effect on earnings Management

Motivation

3 RESEARCH METHOD AND

INSTRUMENTS

The population in this study is an accountant at

business firms in West Jakarta. The number of

business enterprises in West Jakarta is 795

companies (source: West Jakarta Business

Directory, 2015). The number of accountants is not

counted. The number of samples determined in this

study 5 x number of indicators = 5 x 54 that is equal

to 270 respondents [Hair:2007]. Sampling technique

conducted in this research is simple random

sampling technique, that is a sampling technique

where the sample in research is homogeneous. A

simple random sampling technique is used in

sampling where the sample in the study is

homogeneous. Data collection was carried out by

distributing questionnaires to accountants at the

companies where they worked.

Hypothesis testing of this research used multiple

linear regression analysis with Path Analysis

modification using 2S OLS (Two Stage Ordinary

Least Square). This analysis is used to determine the

direct and indirect effect of a set of independent

variables to the dependent variable with the pattern

of causality. Multiple linear regression analysis is

used to measure the influence between the

independent variable and the dependent variable.

Basic decision making:

if P-Value (sig) <α (5%), then Ha is

accepted

if P-Value (sig)> α (5%), then Ha is

rejected

4 RESULTS AND DISCUSSION

Data collection randomly by distributing

questionnaires to management accountants who

work manufacturing companies in West Jakarta and

collected data totaling 270 complete data.

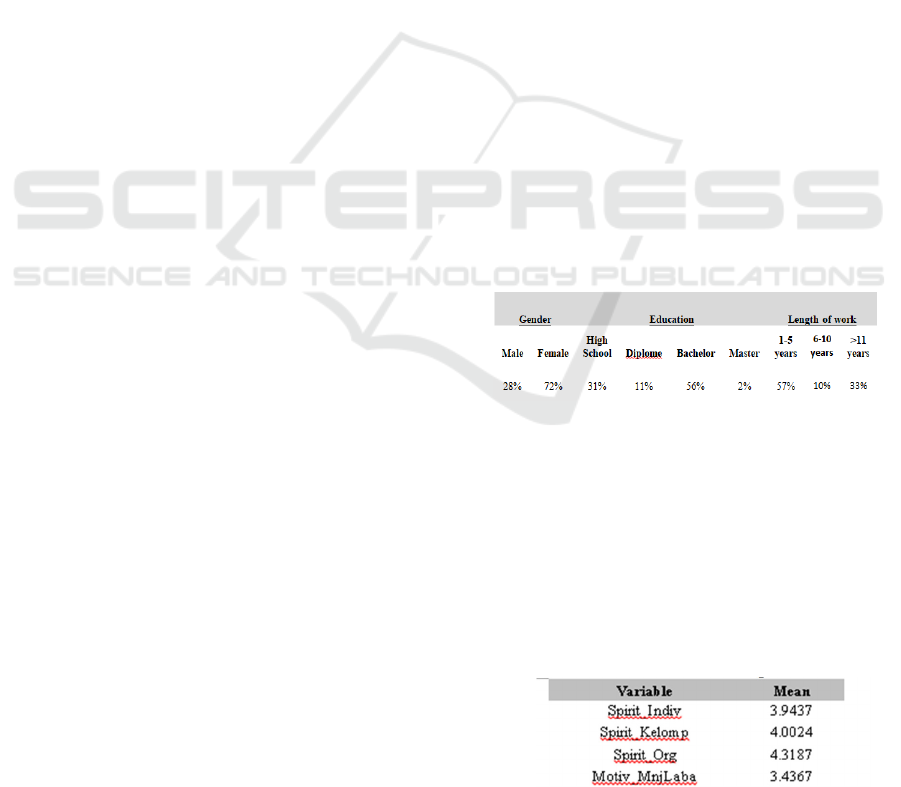

Table

1: Respondent Demographic

From the table above can be explained that the

majority of research respondents are women, with an

undergraduate degree and have worked for one to

five years.

The following table shows the descriptive

statistics of research variables from the sample of

270 data derived from questionnaires as much as

270 respondents. The following is an explanation of

descriptive data.

Table 2:

Statistic

Descriptive

ICRI 2018 - International Conference Recent Innovation

2724

Table 2 above shows that Individual Spirituality

shows an average score of 3.94. This number shows

that accountants have high meaningful work, Sense

of community and Alignment with organizational

values. While the motivation of earnings

management measured by the average score

presented in the table is 3.43. This figure shows that

the motivation for respondents to do earnings

management is categorized as moderate.

4.1 Test of Validity and Reliability of

Research Instruments

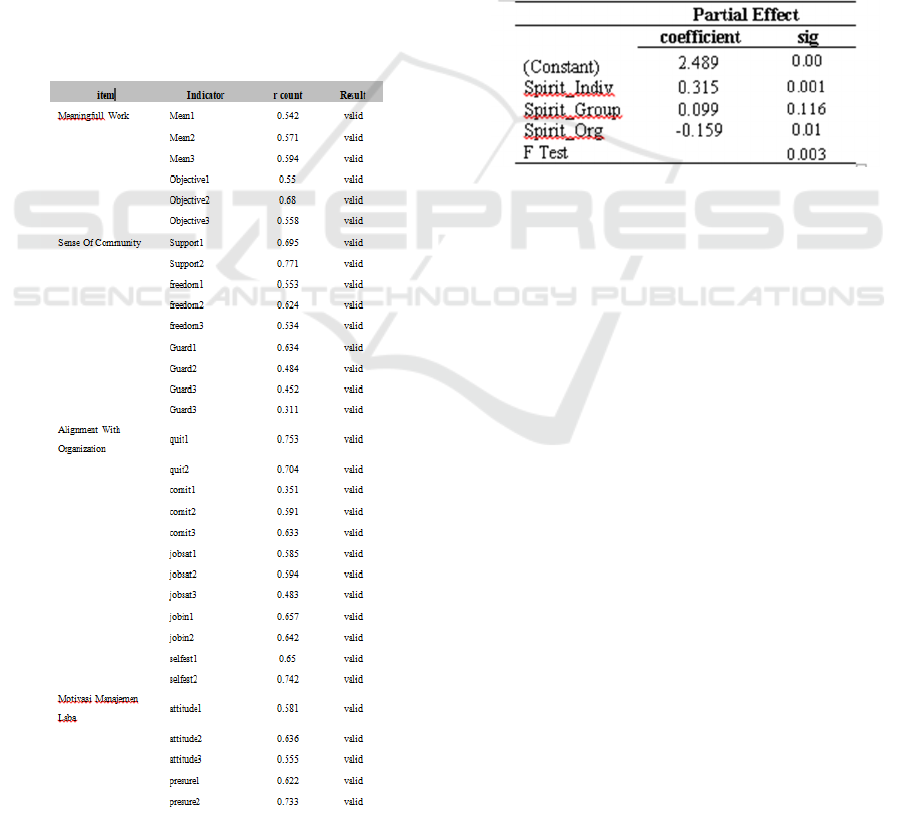

Test this validity using Pearson Product Moment.

Test results validity of each item in the questionnaire

declared valid with a value above 0.3. While the

reliability test used Cronbach alpha, and reliable

with the value of Cronbach alpha above 0.7.

Table

3: Test of Validity

4.2 Hypothesis Testing

4.2.1 Spiritual

Level of Individual,

Spiritual Level of Group and

Spiritual Level of Organization

Influence to Earnings Management

Motivation

Before performing hypothesis testing, normality test

of data and classical assumption test as a

requirement of multiple regression analysis and all

stated have passed the test.

Table 3 Multiple Linear Regression Test of

Spiritually workplace toward earning management

motivation.

Table 4: Multiple Linear Regression Test of Spiritually

Then Ha1 is accepted. From table 3 above the

test results of influence Simultaneously Spiritual

level Individual, Spiritual level of Group and

Spiritual level Organization to Management

Motivation Profit obtained evidence that

significance value 0.003 <α (0.05) means

simultaneously Spiritual Individual, Spiritual Level

Group and Spiritual level Organization influence to

Earnings Management Motivation. The results of the

analysis means that increasing spirituality in the

workplace will increase motivation. Collins &

Porras in Kompas (2008) expresses the benefits the

organization gains when it underlies the values of

spirituality in the workplace, that is, a value-based

organization is judged more successful by modern

writers. The benefit that needs to be emphasized as a

conclusion is that the work spirituality perspective

provides the deepest values for the individual to

support the work. Also, spirituality in the workplace

also provides hope for a deep and balanced

fulfillment, so that workers will experience joy and

meaning in their work, to see themselves as part of a

community that can be trusted, to experience

personal development as part of the community in

which they feel appreciated and supported. When

organizations provide opportunities for workplace

spirituality by building shared values, it makes

people feel equal and enables them to live in a fear-

free environment, sharper in intuition and creativity,

The Role of Spirituality Workplace for Reducing Motivation of Accounting Fraud

2725

and a sense of belonging to the organization.

Ashmos (2000) defines spirituality in the workplace

as an introduction that employees have an "inner

life" that nurtures and is nurtured by meaningful

work that takes place in the context of the

community. If an accountant feels that his or her

work is related to what matters in life, the

accountant will tend to be motivated to contribute to

improving the company's financial performance

through financial reporting.

Spiritual level individual positively influences

earnings management motivation. This means that

the Ha2 hypothesis is accepted. Spiritual level

individual can be defined as having the ability to feel

the deepest meaning and purpose of one's work. This

state represents how workers interact with their work

day by day. It is based on the assumption that

humans have their own deepest motivation, truth and

desire to carry out activities that bring meaning to

their lives and others. After all, spirituality sees

work not only as something fun and challenging, but

also about things such as finding the deepest

meaning and purpose, animating one's dreams,

fulfilling one's life's needs by finding meaningful

work, and contributing to others. If the work is

considered something that is meaningful in life, then

the accountant will tend to be motivated to

contribute in the process of financial reporting

byorganizational goals, or it can be said that the

accountant will be motivated to manage earnings.

Spiritual group level does not affect earnings

management motivation. This means that the Ha3

hypothesis is rejected. The sense of community

represents the group level. This dimension refers to

the group level of human behavior and focuses on

the interaction between workers and their co-

workers. Spirituality at this level consists of the

mental, emotional, and spiritual relationships of

workers in a team or group in an organization. The

core of this community is the deep connection

between people, including support, freedom of

expression, and shelter. At this level, the accountant

feels that everyone has a common goal, with a good

common goal, of course, will make the accountant

be motivated to perform actions that are of mutual

interest. Therefore, it can be said that with strong

group-level spirituality it will give full awareness for

accountants to be motivated to improve

organizational performance, or motivated to manage

a profit.

The spiritual level organization has a negative

effect on earnings management motivation. This

means that the Ha4 hypothesis is accepted. The third

fundamental aspect is alignment with organizational.

This third aspect shows the experiences of

individuals who have strong alignments between

their personal values and the mission and goals of

the organization. This value relates to the premise

that the organization's purpose is greater than itself

and one must contribute to the community or

another. Earnings management is an action to affect

reported profits and provide false economic benefits

to the company and misleads stakeholders so that in

the long run it will be very disturbing and even

harmful to the company. Therefore, with a strong

level of organizational level spirituality, the

accountant will be aware of the ugliness of earnings

management actions for the survival of the

company, so with a high level of spirituality level

organization will reduce the earning management

motivation.

5 CONCLUSIONS AND

IMPLICATIONS

The results of research on accountants in business

firms show that Workplace spirituality has a strong

influence and relationship with employee work

attitudes. Workplace spirituality must be understood

clearly, comprehensively, and practiced at the

individual, group and organizational level in order to

achieve positive results in the future. It is important

to translate the workplace spirituality concept into

organizational change and development programs

(Amalia and Yunizar, 2012).

Accountant behavior based on a good spiritual

situation in the company will not cause the

accountant to reduce the earnings management

motivation. Because the accountant realizes that the

earnings management action is the thing to do to

improve the company's financial performance, even

if the accountant realizes that the action will actually

harm the institution itself.

Some limitations in this study are primarily not

yet look more deeply about what motivates the

accountant in doing earnings management practices.

Also, this study also has not measured whether the

accountant has known and perform profession ethics

more deeply. With the weakness in this research, it

is expected in the next research can add the variable

type of motivation expected by an accountant and

ethical orientation factor as moderator of accountant

performance.

ICRI 2018 - International Conference Recent Innovation

2726

REFERENCES

Atia Rahma Nabila, 2013, Deteksi Kecurangan Laporan

Keuangan Dalam Perspektif Fraud Triangle (Studi

Empiris Pada Perusahaan Manufaktur Yang Terdaftar

Di Bursa Efek Indonesia Tahun 2010-2011) Fakultas

Ekonomika Dan Bisnis Universitas Diponegoro

Semarang

Amalendu Bhunia1 And Sri Somnath Mukhuti2,

2011,Spirituality On Motivations For Earnings

Management-An Empirical Analysis, Business

Management Dynamics Vol.1, No.4, Oct 2011

Amalendu Bhunia, Sri Amit Das, 2012, Explore The

Impact Of Workplace Spiritually n Motivation For

Earnings Management-An Empirical Analysis,

International Journal Of Scientific And Research

Publication, Volume 2

Amalendu Bhunia and Sri Somnath Mukhuti, 2011,

Workplace Spirituality on Motivations for Earnings

Management-An Empirical Analysis, Business

Management Dynamics Vol.1, No.4, Oct 2011, pp.73-

78

Chen Ming-Chia, 2012, The Influence of Workplace

Spirituality on Motivations for EarningsManagement:

A study in Taiwan’s Hospitality Industry, Journal of

Hospitality Management and Tourism Vol. 3(1), pp. 1-

11, January 2012

Eko Ganis Suharsono, 2010, Metamorfosa Akuntansi

Sosio Spiritual, Prasetya Online, Universitas

Brawijaya

FilhaqAmaliaa& Yunizarb, 2013, Perilaku Dan

Spiritualitas Di Tempat Kerja A Bank Indonesia,

Fakultas Ekonomi, Universitas Padjadjaran

I Nyoman Wijana Asmara Putra, 2012, Manajemen

Laba:Perilaku Manajemen Opportunistic Atau

Realistic ? Jurusan Akuntansi, Fakultas

EkonomiUniversitas Udayana

Malia, 2010, Pengaruh Orientasi Etika Dan Pengalaman

Akuntan terhadap Persepsi Etis Praktik Manajemen

Laba, Jurusan Akuntansi, Fakultas Ekonomi dan Ilmu

Sosial, Universitas Islam Syarief Hidayatullah, Jakarta

Komarudin Achmad Imam Subekti dan Sari Atmini, 2007,

Investigasi Motivasi Dan Strategi

Manajemen LabaPada Perusahaan Publik Di Indonesia,

TEMA, Universitas Brawijaya Volume 8, Nomor 1,

Maret 2007

Margaret Benefiel Louis W. Fry And David Geigle, 2014,

Spirituality And Religion In The Workplace: History,

Theory, And Research Psychology Of Religion And

Spirituality, Texas A&M University Central Texas,

American Psychological Association

Ming-Chia Chen, 2013, Workplace Spirituality And

Earnings Management Motivations Department Of

Hospitality Management Ming Dao University,

Taiwan .

Mohammad Hossein Vadieiet all, 2012, Survey Effects of

Intent and Materiality Earnings Management on

Ethical Judgment of Students in Iran, Scholarly

Journal of Business Administration, Vol. 2(6) pp. 123-

131, October 2012.

Mohammad Shadiq Khairi (2013), Memahami Spiritual

Capital Dalam Organisasi Bisnis Melalui Perspektif

Islam Jurnal Akuntansi Multiparadigma, Volume 4,

Nomor 2, Agustus 2013, Hlm 286-307.

Syaikhul Falah, 2006, Pengaruh Budaya Etis Organisasi

Dan Orientasi Etika Terhadap Sensitivitas Etika (Studi

Empiris Tentang Pemeriksaan Internal Di Bawasda

Pemda Papua), Program Studi Magister Sains

Akuntansi Program Pascasarjana Universitas

Diponegoro.

The Role of Spirituality Workplace for Reducing Motivation of Accounting Fraud

2727