Evaluation of Internal Control Design and Implementation of

Revenue Cycle: Case Study on Hotel ABC

Dafne Etty Melinda Malau and M. Malik

Master of Accounting, Faculty of Economics and Business, Universitas Indonesia, Jl. Salemba Raya 4 Salemba, Jakarta,

Indonesia 10430

Keywords: Internal Control, Revenue Cycle, Hotel.

Abstract: The hospitality industry in Indonesia continues to grow along with the increase popularity of tourism sector

in Indonesia. This caused the hospitality industry to become competitive. Therefore the hotel must be able to

manage the overall source of income to be able to create a stable profit stream. For this reason, supervision

of internal control is needed. With good internal control, the hotel can avoid threats in carrying out its

operational activities. This study aims to evaluate the design and implementation of the internal control system

in the revenue cycle. . The method in this research is descriptive analysis in the form of the case study. The

data obtained through observation, interview and analysis on the company internal documents. The results

show that there were weaknesses in Hotel ABC’s internal control design, where giving discounts, room

pricing, complimentary rooms are not monitored properly, and there are some sales recording procedures that

are done manually that had an impact on company's profits. Therefore this study provides recommendations

for improvements of internal control activities that will address those issues.

1 INTRODUCTION

Hospitality industry in Indonesia shows a significant

increase in the recent years. Based on data from the

Central Bureau of Statistics, the number of star-rated

hotel accommodations in Indonesia in 2016

increased 8.6% compared to 2015, while the number

of non-star hotel accommodations in 2016 also

increased 1.8% compared to 2015. The hospitality

industry continues to grow along with the increasing

popularity of tourism sector in Indonesia. e-tourism

created new phenomena related to hotel sales.

Among them is the creation of new distribution

channels to increase hotel room sales. These include

OTA sales, social media, events and conference

organizers, all of which aim to provide more options

in room sales (Stangl et al., 2016 in Xu et al., 2017).

This caused the hospitality industry to become

competitive. Therefore, hotels must be able to

manage their overall source of income better than

competitors, in order to create a stable profit stream

by investing in sources of income that provide the

greatest income and also maintain integrity in

carrying out pricing strategies to achieve business and

financial goals that established (Green & Lemono,

2012 in Dolasinski et al., 2018).

Hotel ABC has been actively running its

operations since 2011. The main source of income

including:

1. Room sales

2. Sales of F & B (restaurant and banquet)

3. Spa package sales

4. Playground ticket sales

Where the percentage of each sales unit against total

income is described as in table 1.

Table 1: Sales Percentage Table.

Room

F&B

Spa

Playground

2017

31%

60%

2%

7%

2016

30%

57%

3%

10%

2015

27%

64%

2%

7%

2014

27%

52%

1%

19%

According to the table above, it can be seen that

Hotel ABC's biggest income currently comes from

F & B sales, while the sales of rooms at ABC Hotels

which should be the main source of income for the

hospitality business has not yet given maximum

results.

Malau, D. and Malik, M.

Evaluation of Internal Control Design and Implementation of Revenue Cycle: Case Study on Hotel ABC.

DOI: 10.5220/0008431403730379

In Proceedings of the 2nd International Conference on Inclusive Business in the Changing World (ICIB 2019), pages 373-379

ISBN: 978-989-758-408-4

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

373

In a study conducted by Russo, 1991 in Morgan

(2018) it was found that hotel revenue was created

from (1) pricing for each room and type of room,

and (2) changes in room occupancy. There are two

indicators in measuring the performance of hotel

room sales. The first indicator is Average Room

Rate (ARR) = Total room income / Total rooms sold

and second indicator Revenue per Room Available

(RevPar) = Total room income / Total rooms

available, where ideally the number of ARRs =

RevPar which indicates that the occupancy rate

reaches 100% . Following are the ABC Hotel ARR

and RevPar calculations:

Table 2: ARR and RevPAR Calculation Tables.

ARR

RevPAR

2017

313.342,92

107.100,61

2016

337.841,50

106.926,84

2015

309.688,96

143.231,14

2014

333.301,26

123.754,76

2013

388.231,32

138.055,06

According to the table 2, it appears that RevPAR

Hotel ABC for the past 5 years is far below its ARR

which indicates that the sales performance of hotel

rooms is not good.

Hotel ABC continues to make various efforts to

increase the potential of room sales, including by

cooperating with OTA, providing monthly promos,

and giving discounts for group stays. In its

implementation, problems arise, especially in terms

of price discounting and the provision of

complimentary rooms carried out by the marketing

department that are not according to the rules created

by management.

Barry, Yayla, Papastathis in Yemer (2017)

explained that poor income performance is a result of

the low quality of service, absence of a system that

creates long-term relationships with customers, and

results from weak internal controls. Therefore there is

a management tool that can control and supervise the

income from each hotel source of income.

The quality of internal controls can be assessed by

reviewing the design and implementation through the

COSO Integrated Framework. COSO Integrated

Framework. Therefore, the components of the COSO

framework must be implemented and enabled so that

the internal control system can run optimally. This is

the background of the author to raise the title

"Evaluation of Design and Implementation of Internal

Control in the Revenue Cycle (Case Study on ABC

Hotels)"

2 LITERATURE REVIEW

2.1 Internal Control

According to the Institute of Internal Auditors (2016)

internal control is a process that is influenced by the

board of directors, management and other personnel

of the company designed to provide reasonable trust

regarding the achievement of objectives of

operational activities, reporting and compliance.

2.1.1 Internal Control According to COSO

Internal control according to COSO Internal Control

- Integrated Framework 2013 has three categories of

objectives: operations, reporting and compliance and

consists of five components of internal control:

Control Environment, Risk Assessment, Control

Activities, Information and Communication, and

Monitoring Activities.

Figure 1: COSO's Internal Control.

This integrated COSO 2013 internal control

framework, as in figure 1, views each component of

internal control as appropriate and relevant for the

entire company, therefore stipulating that all

components must be present and functioning

simultaneously in an integrated system.

2.2 Accounting Information Systems

Romney and Steinbart (2017) explain that accounting

information systems are systems that collect, record,

store and process data to produce information for

decision making. This includes people, procedures,

instructions, data, software, information technology

infrastructure and internal controls and system

security.

Romney and Steinbart (2017) added that a well-

designed accounting information system could create

values for companies by improving quality and

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

374

reducing production costs due to increased efficiency

and effectiveness in conducting operational activities.

2.2.1 System Documentation Technique

The design of a system needs to be documented to

explain how the system works. In his book, Romney

and Steinbart (2017) explain there are several

methods for documenting a system:

1. Data flow diagram (DFD) that displays

graphically the origin of the data, data flow, data

transformation process, data storage and final

destination data.

2. A flowchart that displays graphically a system,

where there are 2 (two) types of flowcharts, including

document flowchart to describe a system graphically

related to the flow of documents and information

between divisions or departments responsible and

flowchart programs to show logical operational

sequences when the computer runs a program.

3. Business process diagrams that will make

graphical descriptions related to the business

processes of an entity. Some of the symbols used to

make DFD and flowcharts are as follows:

2.3 Revenue

According to IAI in PSAK 23 Paragraph 7: Revenue,

revenue is defined as gross inflows of economic

benefits arising from the entity's normal activities

during a period if the inflows result in an increase in

equity that does not originate from the contribution

of investors. In this case, recognized revenue does

not include amounts that are billed for the benefit of

third parties, such as value added tax or sales tax. In

the hospitality industry, the revenue received is

mostly related to the sale of services. Paragraph 20 of

PSAK 23 states that the requirement for recognition

of service sales revenue is if the transaction results

related to the sale of such services can be estimated

reliably with reference to the level of transaction

settlement at the end of the reporting period.

2.4 Definition of Revenue Cycle

Romney and Steinbart (2017) define the revenue

cycle as a series of business activities and repetitive

data processing operations related to the supply of

goods and services to customers and collect

payments for those sales.

3 RESEARCH METHODOLOGY

3.1 Research Methods

This research is a case study research that uses an

evaluation method with a descriptive qualitative

approach. Denzin and Lincoln, 2004 in Sri Wahyuni

(2015) say qualitative research is a multi-focus

method, involving an interpretive, naturalistic

approach to the subject matter. This method was

chosen with the consideration that the purpose of this

study is to explore a process and phenomena that

occur in the field and then draw conclusions from the

phenomena that occur.

3.2 Case Selection

This study selects cases originating from the income

cycle. This is based on the consideration that the

income post always receives special attention from

the management because it affects the business

continuity of an entity. Therefore, the authors assess

that this study can have a positive impact on the

object of research, Hotel ABC.

3.3 Unit Analysis

This research will be conducted with a case study

approach on one object of research. The object of

research chosen was Hotel ABC, an entity engaged

in hospitality. The selection of ABC Hotels as a place

to conduct research because, in general, there is

limited access to hotel financial information. This

study will conduct observations on Hotel ABC, with

the consideration that Hotel ABC has problems in its

internal control which affect the overall revenue of

the hotel.

3.3.1 Overview of Hotel ABC

ABC Hotel stands on 4.3 hectares of land consisting

of 47 villas with 4 room types, spa, restaurant,

multifunctional room and playground. The ABC

hotel carries the concept of a private villa with a

touch of traditional furniture with a wooden stage

house feel that describes the authentic characteristics

of West Kalimantan.

Hotel ABC's revenue comes from 4 (four) main

activities,including revenues from hotel sales,

revenues from food and beverages sales, spa sales,

and playground ticket sales. Below will be described

the business processes of the four activities listed

below:

Evaluation of Internal Control Design and Implementation of Revenue Cycle: Case Study on Hotel ABC

375

a. Hotel room sales

Guests make hotel room reservations through a

variety of booking options (walk in, online travel

agents, marketing). The reservation will

automatically enter the ABC Hotel reservation

system and guests will get proof of reservation in

the form reservation form. At check in Front

Office (FO) will request proof of reservation to be

matched with Reservation Form. After the check-

in process is complete, the FO will provide the

room key, access card, and breakfast coupons to

guests.

At check out, the room key is handed over to the

front office and housekeeping will check the room

to check the furniture condition again. if

everything is safe, then the check-out process can

continue.

b. Food and beverages sales

Visitors make orders, which will be inputted to

the system, at the time of payment, the cashier

will print bills and visitors will make payments.

c. Spa sales

Visitors do maintenance with a spa package that

has been selected, which will be inputted to the

system, at the time of payment, the cashier will

print the bill and the visitor will make a payment.

d. Playground ticket sales

Visitors make a purchase for a playground ticket,

the number of tickets sold will be input to the

system, at the time of payment, the cashier will

print the bill and the visitor will make a payment.

3.4 Data Collection Techniques

The data used in this study consisted of primary data

and secondary data.

1. Primary data

Primary data is obtained directly from Hotel ABC

during the data collection process. This primary

data includes:

a. Data from interviews

Interviews were conducted with the ABC

division of finance and sales division.

b. Internal documentation obtained from Hotel

ABC is as follows:

• Hotel ABC sales report

• Organizational structure

• SOP

2. Secondary Data

Secondary data obtained from publicly published

data, including legislation and other data related

to the company's operations.

3.5 Analysis Methods

This study uses data obtained to analyze accounting

information systems and internal control practices in

the income cycle at ABC Hotels. The analysis will

produce information on the comparison of internal

control practices with existing formal procedures.

The results of interviews, observation and analysis of

the company's internal documents will produce an

overview of current operational activities and the

design of system development which can be the basis

for the preparation of a framework for accounting

information systems and internal controls.

4 RESEARCH RESULTS

4.1 Analysis of Control Activities

In the Hotel ABC revenue cycle, there are several

external parties that interact with the system,

including guests, banks, management and accounting

information systems owned by Hotel ABC. Each type

of sales will be discussed in the revenue cycle at ABC

Hotels, including hotel room sales, food and

beverages sales, spa sales and playground ticket

sales.

4.1.1 Hotel Room Sales

These internal control activities are grouped based on

the business processes found in the Hotel ABC

learning cycle, namely the order process, service

delivery process, billing process, and the process of

receiving money.

This study finds weaknesses include:

1. Pricing, discounts and complementary rooms

are still done manually. This causes the risk of

the billed value not to be in accordance with the

value that should be billed in accordance with

the room price set by the company and causes

the risk of rising occupancy without an increase

in revenue which will further reduce RevPAR.

Based on the results of interviews with senior

marketing, this is because there are no rules that

explicitly determine the maximum discount and

complementary rooms so that the marketing

division provides a large discount and a number

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

376

of complementary rooms so that group guests

want to hold an event at the ABC Hotel.

2. Lack of control activities in the billing process.

Especially for guests from government

agencies. Based on the results of interviews

with financial staff, this was due to government

agencies contributing large margins to ABC

hotel sales as a whole, so Hotel ABC decided

not to be too aggressive in billing.

Based on the analysis above, this study will re-

describe the business activities of selling hotel rooms

with the addition of internal control activities. This is

done to facilitate Hotel ABC in implementing the

proposed improvements from this research that are

related to business processes and operational

activities of ABC Hotels. The following are proposed

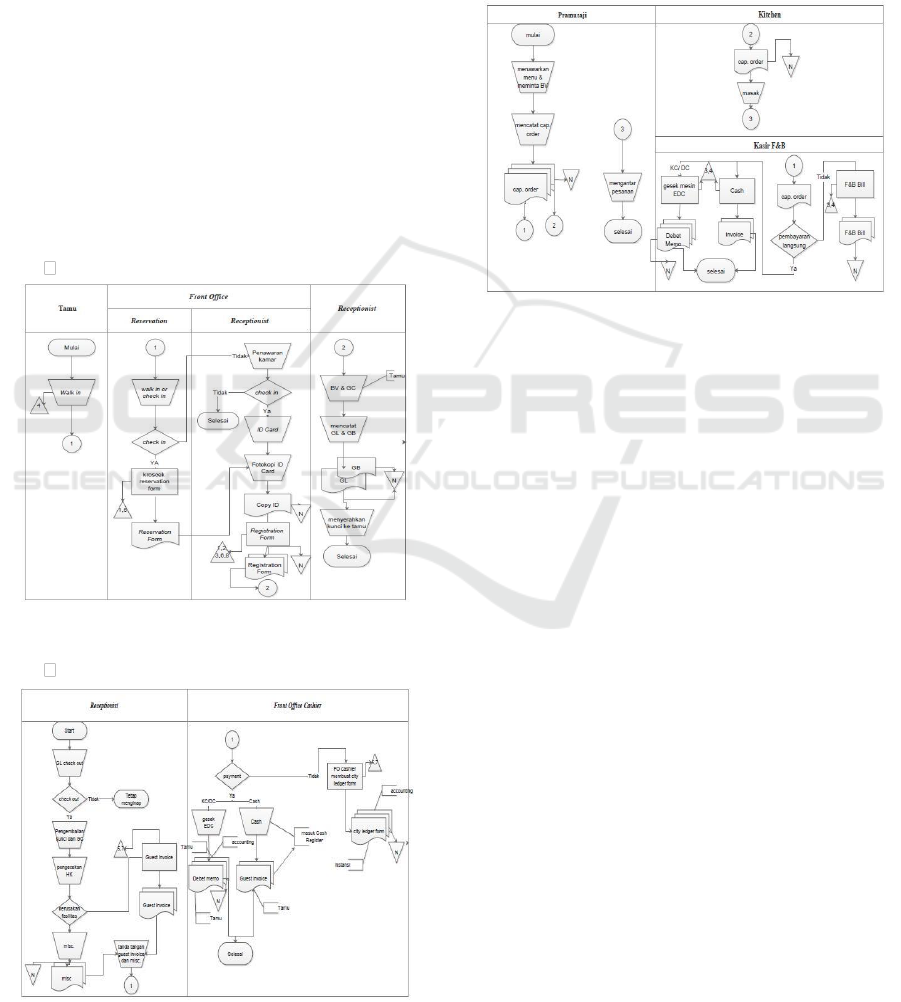

hotel room sales flowcharts, as in figure 2 and figure

3, which are divided into 2 main activities:

Check In Process

Figure 2: Proposed Flowchart for check in process.

Check Out Process

Figure 3: Proposed Flowchart for check out process.

Based on the analysis above, this study will re-

describe the business activities of food and beverages

sales with the addition of internal control activities

referring to the weaknesses above. This was done to

facilitate Hotel ABC in implementing the proposed

improvements from this research that were linked to

the business processes and operational activities of

the ABC Hotel. The proposed flowchart is described

as follows:

Figure 4: Proposed Flowchart for Food and Beverages

Sales.

4.1.2 Food and Beverages Sales

These internal control activities are grouped based on

the business processes found in the Hotel ABC: the

order process, service delivery process, the billing

process, and the process of receiving money.

It is known that the control activities in food and

beverages sales are running quite well, but there are

still some control activities that have not been

implemented which have resulted in weaknesses:

1. Non-strict supervision related to existing raw

material inventories.

2. Recording of visitor payment methods is still

done manually, so there is a possibility of

recording errors that may result in possible

billing errors.

4.1.3 Spa Sales

These internal control activities are grouped based on

business processes found in the Hotel ABC revenue

cycle: the order process, service delivery process,

billing process, and the process of receiving money.

Based on analysis it is known that the weakness

of control activities in sales is caused by the existing

control activities that have not been adequately

designed through adjusting the internal procedures of

the ABC Hotel. These disadvantages include:

Evaluation of Internal Control Design and Implementation of Revenue Cycle: Case Study on Hotel ABC

377

1. Lack of supervision on spa package booking

activities and supervision of spa supplies so as to

enable potential fraud committed by therapists.

2. Recording of visitor payment methods is still

done manually, so there is a possibility of

recording errors that may result in possible billing

errors.

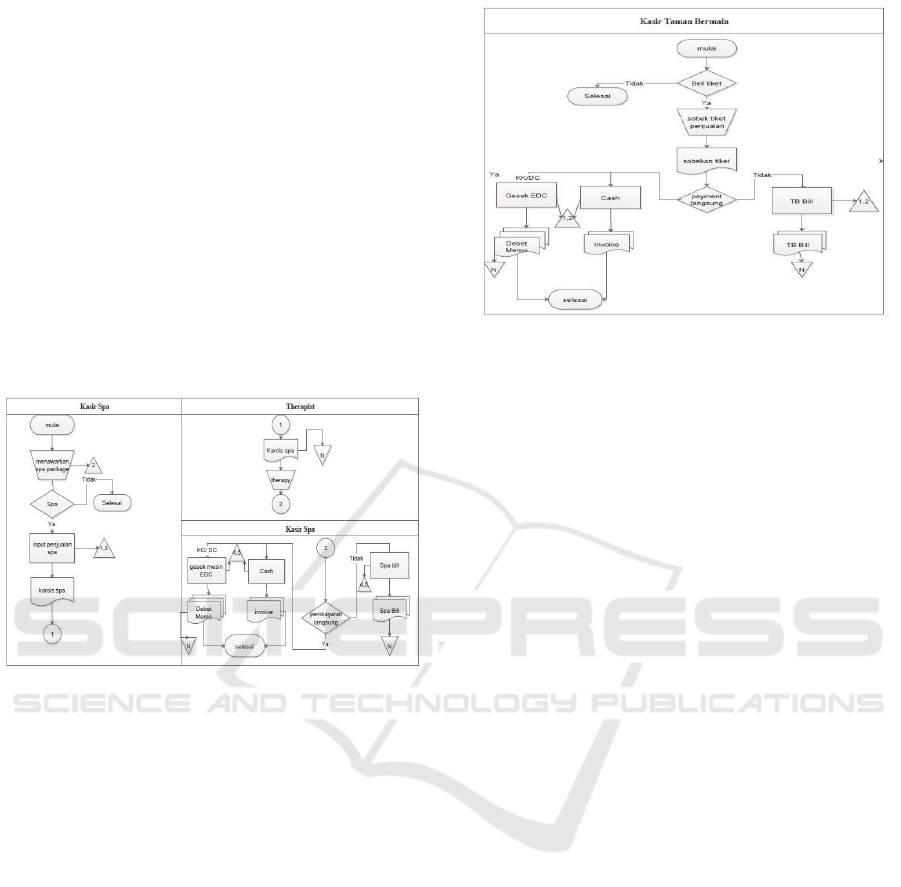

Based on the analysis above, this study will

describe the spa sales business activities with the

addition of internal control activities. This was done

to facilitate Hotel ABC in implementing the proposed

improvements from this research that were linked to

the business processes and operational activities of

the ABC Hotel. The following figure 5 is the

proposed flowchart described as follows:

Figure 5: Proposed Flowchart Spa Package Sales.

4.1.4 Playground Ticket Sales

These internal control activities are grouped based on

the business processes found in the Hotel ABC: the

order process, service delivery process, the billing

process, and the process of receiving money.

Based on the results of observations in the field

and interviews with informants during the study, it

was found that not all internal control activities were

implemented. There are still a number of control

activities that have not been implemented which have

resulted in weaknesses, including recording the

method of selling a playground ticket and recording

payments is still done manually, so that the error of

recording and fraud is possible.

Based on the analysis above, this study will

describe the playground sales business activities with

the addition of internal control This was done to

facilitate Hotel ABC in implementing the proposed

improvements from this research that were linked to

the business processes and operational activities of

the ABC Hotel. The proposed flowchart is as follows:

Figure 6: Proposed Flowchart Playground Ticket Sales.

5 CONCLUSIONS AND

SUGGESTIONS

5.1 Conclusions

This research was conducted to analyze internal

control activities in the ABC Hotel revenue cycle.

When viewed from the analysis of control

activities carried out, it can be concluded that:

a. At current hotel room sales pricing, discounting

and complementary rooms made by marketing

are carried out with minimum supervision from

the General Manager, this causes a difference

between occupancy and revenue levels. This

can be seen from the calculation of ARR and

RevPar for the past 5 years.

b. At the sales of food and beverages, spa and

playground recording the sales transaction

method and payment method are still done

manually.

5.2 Suggestions

Based on the results of the analysis of internal control

on Hotel ABC and identification of

existing weaknesses, this study provides

suggestions:

For Hotel ABC:

1. Improvement of control activities starting from

the improvement of sales recording procedures,

especially for recording procedures that are still

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

378

running manually, pricing procedures, giving

discounts, complementary rooms and billing

procedures.

2. In the long term, considering the expected

volume of transactions that will increase, it is

necessary to consider improving or developing

the accounting information system that

currently implemented.

For Academics and Future Research:

Future research is expected to broaden the scope of

research not only for the revenue cycle but also

expand the scope of the entire business cycle of the

company.

REFERENCES

Addey, Josephine Nana Ama. (2012). An assessment of

internal control system on the image of the hospitality

industry in Royal Mac-Dic Hotel and Capital View

Hotel: http://hdl.handle.net/123456789/4833

Badan Pusat Statistik (2017), (online), (https://bps.go.id )

Cheng, Qiang and Goh, Beng Wee and Kim (January 16,

2017). Internal Control and Operational Efficiency.

Contemporary Accounting Research

Chris Guilding (2014). Accounting Essentials

forHospitality Managers. New York: Routledge

COSO Internal Audit Integrated Framework. (2013).

(www.coso.org)

Creswell W. John (2013). Research Design Pendekatan

Kualitatif, Kuantitatif, dan Mixed. Yogyakarta: Pustaka

Pelajar.

Hall, J.A. (2011). Accounting Information System Seventh

Edition. Ohio: South-Western

Ikatan Akuntan Indonesia. (2015). Standar Akuntansi

Keuangan per efektif 1 Januari 2015. Jakarta: Ikatan

Akuntansi Indonesia

Jo Dolasinski, Mary & Roberts, Chris & Zheng, Tianshu.

(2018). Measuring hotel channel mix: A Dea-Bsc

Model. Journal of Hospitality & Tourism.

Karagiorgos, Theofanis and Drogalas, George and

Giovanis, Nikolaos. (2011). Effectiveness of Internal

Audit in Greek Hotel Business. International Journal of

Economic Sciences and Apllied Research, Vol. 4, No.

1, pp. 19-34: https://ssrn.com/abstract=1806943

Kementerian Pariwisata. (2017). Jumlah Kunjungan

Wisatawan Mancanegara Menurut Pintu Masuk dan

Kebangsaan, (online), (http://kemenpar.go.od/asp/detil.

asp?c=110&id=350

Romney, M. B., & Steinhart, P. J (2015). Accounting

Information Systems (13th Edition). Kendallville:

Pearson

Romney, M. B., & Steinhart, P. J (2017). Accounting

Information Systems (14th Edition). Kendallville:

Pearson

Moeller, R. R. (2014). Executive Guide to COSO Internal

Control: Understanding and Implementing the New

Framework. John Wiley and Sons,

Morgan, Kevin. (2018). An Empiral Study in the U.S Hotel

Industry: How Quality Assurance, Customer

Satisfaction, Brand Signaling, And Guest Loyalty

Impact Revenue. Dissertation, Georgia State University

(https://scholarworks.gsu.edu/bus_admin_diss/94 )

Wahyuni, S. (2015). Qualitative Research Method: Theory

and Practice 2nd Edition. Jakarta: Salemba Empat

Yemer Maefin, Chekol Firew. (2018). The effect of internal

controls systems on hotel revenue. A case ofhotels in

Bahir Dar and Gondar Cities. Oman. Chapter of

Arabian Journal of Business and Management Review

2017 Vol.6 Issue 6, pp. 19-37

Xu, X. and Li, Y. (2017). Maximising hotel profits with

pricing and room allocation strategies. Int J. Services

and Operations Management, Vol. 28, No.1, pp.46-63.

Zekeriya Yetis, Huseyin Cetin. (2017). Evaluation of the

Effectiveness of the Internal Control System in Hotel

Businesses. ISBN: 978-1-943579-61-7

Evaluation of Internal Control Design and Implementation of Revenue Cycle: Case Study on Hotel ABC

379