Adoption of Innovation Internet Banking

Winda Feriyana

1

, Lisna Fitri Alviyah

2

, Dyah Sugandini

2

, and Yekti Utami

2

1

Sekolah Tinggi Ilmu Ekonomi Trisna Negara

2

Universitas Pembangunan Nasional Veteran Yogyakarta

Keywords: Attributes of innovation, adoption, internet banking.

Abstract: This study aims to determine the positive effect of the perception of banking innovation attributes on internet

banking adoption. Several indicators measure the perception of banking innovation attributes, namely

perceived ease, risk perception, conformity perception, perceived usefulness. Internet banking adoption

variable is measured by several indicators, namely customer awareness of the presence of internet banking,

customer interest in finding information about internet banking, customer assessment of internet banking,

experiments conducted to find out the benefits and uses of internet banking, adoption of internet banking

services. Data collection is done by distributing questionnaires. The research analysis unit is students in the

Management Department of the Yogyakarta "Veterans" National Development University. Respondents were

sampled as many as 95 respondents. The analytical method used in testing hypotheses is multiple regression.

The results of this study indicate that there is a significant influence between the perception of the attributes

of banking innovation together on internet banking adoption, and there is a significant positive effect between

risk perception, conformity perception, perceived benefits towards internet banking adoption.

1 INTRODUCTION

Innovation is an idea, practice, or object that is

understood as something new by each individual or

other user units. The innovation-decision process is,

in principle, an information search and processing

activity where individuals are motivated to reduce

uncertainty about the advantages and disadvantages

of innovation. The characteristics of innovation

consist of: relative advantages in the economic field,

(factors prestige social, comfort and satisfaction),

resilience/strength (the degree to which innovation is

perceived as being consistent with existing values,

past experiences, and the need for potential users),

complexity (the level at which innovation is

perceived as challenging to understand and use),

testing power (the level at which innovation within

certain limits can be tested), observability (the level

at which others can see the results of innovation,

Sugandini, 2014).

According to (Rogers, 1983), innovation is an

idea, idea, practice, or object that is realized and

accepted as something new by a person or group to be

adopted. Innovation is essential for the survival of

every business sector, including in financial services

such as banks. Technology is inseparable from the

supporting factors of innovation, current technology

has developed so rapidly, and the development of

information technology is felt to provide a variety of

benefits in the banking business world to be able to

develop faster. Banks that used to be only a place to

provide money exchange services have now

developed into a place to deposit money, or what we

often know as a safe place to save, then banks have

also developed again as a place to lend money. Until

now the bank continues to grow by utilizing

technology to facilitate and satisfy services to its

customers, such as the use of internet banking.

The presence of internet technology provides the

benefits of unlimited communication and time.

Indonesia is the fourth country in the world, with the

most population using internet services. The use of

the internet is not only for information but also for

economic transactions called e-commerce. In the

banking world utilizing technological developments

by presenting banking services in the form of internet

banking (Fita and Vidya, 2013). According to

Maharsi and Fenny (2006), internet banking provides

benefits for customers and banks. For internet

banking customers, it offers convenience and speed

in conducting banking transactions. The advantage

for banks is that internet banking can be an

Feriyana, W., Alviyah, L., Sugandini, D. and Utami, Y.

Adoption of Innovation Internet Banking.

DOI: 10.5220/0009962200230028

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 23-28

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

23

inexpensive solution for infrastructure development

compared to opening outlets ATM.

Gigih, (2015) adoption is the process through

which a person responds to a new product or

technology until the decision making a stage with the

aim that the technology can be adopted or used.

Internet banking is a new technology that is

introduced to customers with the aim that customers

can use the technology and can help or facilitate

customers in conducting banking transactions.

2 LITERATURE REVIEW

2.1 Behavior Adoption of Innovations

Understanding consumer behavior is an action that is

directly involved in obtaining, consuming, and

depleting products and services, including processes

that precede and follow up from this action. The main

problems found in marketing and consumer behavior,

namely consumer response to new services or

products. The basis for observing consumer responses

to new products is part of a study called innovation

diffusion (Sugandini, 2014).

Consumer researchers examine the diffusion of

innovation, which is divided into the diffusion

process and the adoption process. The diffusion

process is a macro process in which the process

focuses on the development and innovation of new

products or services carried out by a company aimed

at the market, how companies can see market needs,

and then determine an innovation for these markets

(Schifman and Kanuk, 2010).

2.2 Understanding Internet Banking

Internet banking is one of the banking services that

allow customers to obtain information, communicate

and conduct banking transactions through the internet

network, and is not a bank that only provides banking

services via the internet (Bank Indonesia, 2004).

Internet banking opens a new paradigm, new

structures, and new strategies for retail banks, where

banks face new opportunities and challenges

(Mukherjee and Nath, 2003).

2.3 Innovation Characteristics

Factors considered by adopters in making decisions

to accept or reject a product if it is associated with

Rogers (1995) are influenced by 5 (five)

characteristics of innovation namely, (1) perception

of relative superiority, (2) perception of suitability, (

3) perception of complexity or complexity, (4)

perception of probation, and (5) perception of

visibility. Each aspect is used as a benchmark in the

acceptance of innovative products because they are

considered to be able to represent all aspects of the

ability of individuals to receive innovative products.

The perceived characteristics of innovation have an

essential role in the stage of persuasion because at the

stage of persuasion, an individual or other decision-

making unit forms a liking or dislike of innovation

and seeks to reduce dissatisfaction and risk of the

innovation by finding relevant information. However,

only complexity or complexity negatively influences

the adoption of innovation because the more

complicated or complicated an innovation is, the less

likely it is to be adopted.

a. Advantage Relative

Relative superiority is an innovation considered more

or superior than ever before. This can be measured

from several aspects, such as economic aspects, social

prestige, comfort, satisfaction, and others. The higher

the relative superiority felt by adopters, the faster the

innovation can be adopted. The concept of relative

excellence indicates that the rate of adoption of

innovative products will be high if individuals feel the

benefits or benefits offered by innovative products.

Relative advantage is innovation perceived better

than replaced. The relative advantage of adopting

innovation is perceived as the availability of more

significant benefits for adopting innovation than

maintaining the status quo (Kwon and Zmud, 1987).

b. Suitability(Compatibility)

This concept shows that the rate of adoption of

innovative products will be high if the individual

perceives the similarity of values or beliefs offered by

innovative products (Gahtani, 2003). This definition

implies two types of conformity, namely normative

or cognitive conformity that refers to conformity with

what is felt or thought about innovation, and practical

or operational suitability that refers to conformity to

what is done by the user.

c. Complexity

This concept shows the extent to which an innovation

is prepared that is difficult to understand and use. The

rate of adoption of innovative products will be high if

individuals feel the ease of use of the products offered

by innovative products (Marshall, Rainer, and Morris,

2003). There are specific innovations that can be

easily understood and used by adopters, and some are

the opposite. The more easily understood and

understood by adopters, the faster an innovation can

be adopted.

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

24

d. Trialability

This concept shows that the rate of adoption of

innovative products will be high if individuals feel the

ease of trying the innovative products offered first

(Reiss and Wacker, 2000). The ability to be tested is

a degree where innovation can be tested to a certain

extent. An innovation that can be tested in actual

settings will generally be adopted more quickly.

e. Visibility or observability

This concept shows that the rate of adoption of

innovative products will be high if individuals feel the

ease of seeing the benefits of the innovative product

attributes offered (Rogers, 1995: Karahanna, Straub

and Chervany, 1999).

3 HYPOTHESIS

Based on the formulation of the problem is there, then

researchers formulate following hypotheses:

H1: Perceived ease, risk perception, perception of

suitability, benefits perception effect together

towards adoption of Internet banking.

H2a: Perceived convenience has a positive effect

on Internet banking.

H2b: Risk perception has a positive effect on the

adoption of Internet banking.

H2c: Conformity perception has a positive effect

on the adoption of Internet banking.

H2d: Perceived benefits have a positive effect on

the adoption of Internet banking.

4 RESEARCH METHOD

4.1 Samples and Sampling Techniques

Samples in this study are some of the Management

Department Students of the "Veteran" National

Development University of Yogyakarta. The

sampling used is Non-probability technique sampling

that is purposive sampling and convenience sampling.

As for the criteria for selecting samples, are students

majoring in University Management The "Veteran"

Yogyakarta National Development that uses internet

banking While convenience sampling is a method of

selecting samples based on convenience, in this

method the sample members are chosen based on the

ease of getting the data needed by researchers

4.2 Data Analysis Techniques

The model used in this study is quantitative

analysis. The method used is multiple linear

regression analysis that functions to measure the

effect between more than one predictor variable (the

independent variable) to the dependent variable.

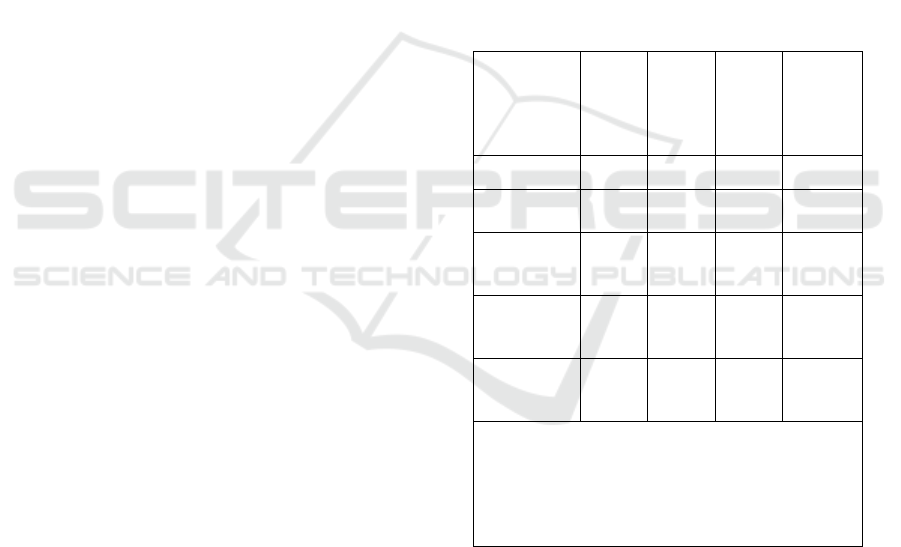

5 RESULTS

5.1 Results of the Regression Equation

Analysis

Analysis of the effect of perception variables on

attributes of banking innovation which include

perceptions of ease, perceptions of risk, perceptions

of conformity, and perceptions of benefits to internet

banking adoption are presented as follows:

Independen

t variables

Regre

ssion

Coeff

icient

s

tarith

metic

Sig. Decree

Constant 5,205 3,827 .000 -

Perceived

Ease (X1)

.274 2,821 .005

Signific

ant

Risk

Perception

(X2)

.293 3229 .001

Signific

ant

Perception

Conformity

(X3)

.322 3,968 .000

Signific

ant

Perception

Benefit

(X4)

.308 3739 .000

Signific

ant

Dependent Variable: Adoption of Internet

Banking

R2adj = 0.582

Fcalculate = 33.708

.

Sig, F = 0.000a

5.2 Results of Research

5.2.1 Testing the F Test

Hypothesis The first hypothesis was tested using the

F test to test the significance of the regression

coefficients of all the predictors (variables

independent) in the model simultaneously or together.

The effect of perceived ease, risk perception,

conformity perception, and perceived benefits

towards adoption internet banking. Testing through

Adoption of Innovation Internet Banking

25

the F test is to compare the probability of error

Fcalculated with significance that can be tolerated (α

= 5%. Based on Table 1 can be seen the calculation

results obtained Fcount of 33,708 with a significance

level of 0,000 which is smaller than α (0,000 <0.050)

means Perceived ease, risk perception, conformity

perception, perceived benefit have a significant effect

jointly on the adoption of internet banking, thus the

first hypothesis stating that ease perception, risk

perception, conformity perception, and perceived

benefit have a joint effect on adoption of supported

internet banking. .

5.2.2 Test Coefficient of Determination

The results of data analysis showed that the

coefficient of determination (R2adj)of 0582, which

means that about 58.20% of the variation in the

variable adoption bank-in internet capable of is

explained by variables perceived ease, risk

perception, perception of suitability, the perception of

benefits while the rest viz of 41.80% explained by

variations of variables outside the model.

5.2.3 Testing the t-Test

The test is used to test the significance of the

regression coefficient of the effect of perception of

ease, risk perception, perception of suitability, and

perception of benefits, partially affecting the adoption

of internet banking. Testing via the t-test is to

compare the error probability

t

with a significance that

can be tolerated (α = 5%). The calculation results

obtained for:

1) Variable perception of ease (X1) has a tcount

of 2,821 with a significance level of 0.005,

which is smaller than α (0.005 <0.050). This

means that perceived convenience has a

significant effect on internet banking adoption.

Thus H2a states that the perception of ease

partially influences the adoption of supported

internet banking.

2) The risk perception variable (X2) has a count

of 3222 with a significance level of 0.001,

which is smaller than α (0.001> 0.050). This

means that risk perception has a significant

effect on internet banking adoption. Thus H2b,

which states that risk perception partially

influences the adoption of internet tires

supported.

3) The conformity perception variable (X3) has a

tcount of 3,968 with a significance level of

0,000, which is smaller than α (0,000> 0.050).

This means that the perception of suitability has

a significant influence on internet banking

adoption. Thus H2c, which states that the

perception of conformity partially influences

the adoption of internet banking supported.

4) Variable perceptions of benefits (X4)have

atcount equal to 3,739with a significance level

of 0.000, which is smaller than α (0,000>

0,050). This means that the perception of

benefits has a significant effect on internet

banking adoption. Thus H2d, which states that

perceived benefits partially affect the adoption

of internet banking, is supported.

6 DISCUSSION

The results of research using Multiple Regression

Analysis show that ease of perception, risk

perception, conformity perception, and perceived

benefit have a significant effect jointly on internet

banking adoption. The results of this study are in line

with research conducted by Pertiwi, Adhivinna

(2013) showing that perception risk, perceived

benefits, and perceived ease of use simultaneously

(together) to the dependent variable, namely the trust

of customers of Bank Mandiri internet banking users.

The hypothesis is proven and can be accepted.

The results of the study using Multiple Regression

Analysis show that ease of perception has a positive

and significant effect on internet banking adoption.

This means that what if ease of perception increases

then will increase internet banking adoption and vice

versa. The results of this study are in line with

research conducted by Fita Pertiwi, Vidya Vitta

Adhivinna (2013), which shows that the ease of use

of internet banking has a positive relationship with

customers' trust in using internet banking. This

hypothesis is proven and can be accepted. The results

of this study imply that the ease of use is the second

construct that gives a positive influence on a person's

interest in adopting technology (Jogiyanto, 2007).

The ease of innovative internet banking products

means the ease of understanding when transacting

through internet banking media. A technology that is

often used shows that the technology is readily known

and easily understood in its use. When the application

is easier to use than others, it will be more likely to be

accepted by its users so that the level of adoption of

internet banking adoption will increase.

The results of research using Multiple Regression

Analysis show that risk perception has a positive and

significant effect on internet banking adoption. This

means that what if risk perception increases then will

increase internet banking adoption and vice versa.

The results of this study are in line with research

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

26

conducted by Pertiwi et al., (2013), showing that the

risk perception variable influences customer

confidence in using internet banking. The hypothesis

is proven and can be accepted. Implications of the

results of this study that shows that the elements of

risk such as financial loss, loss of time, and so on have

been proven to affect risk perception. So, in this case,

the level of customer confidence in using innovative

banking products internet banking will increase if,

with the anticipation in managing high risks,

transaction security, timeliness, transaction

convenience, and facility security can provide

benefits in meeting customer needs.

The results of the study using Multiple Regression

Analysis show that conformity perception has a

positive and significant effect on internet banking

adoption. This means that what if conformity

perception increases then will increase internet

banking adoption and vice versa. The results of this

study are in line with research conducted by Domeher

et al. (2014), showing that the ease of use of internet

banking has a positive relationship to the customer's

trust in using internet banking. The hypothesis is

proven and can be accepted. The results of this study

imply that the perception of suitability is the

perceived suitability of internet banking users to be

able to adjust customer needs, adjust service desires

to customers, and as an evaluation to make changes

to development. So that in this case, the use of

innovative internet banking products has conformity

to the expectations and needs of customers, it will

create the trust and interest of customers in using

internet banking as a banking service that they adopt

in meeting their needs.

The results of the study using Multiple Regression

Analysis show that the perception of benefits has a

positive and significant effect on internet banking

adoption. This means that if the perception of benefits

increases, then it will increase internet banking

adoption and vice versa. The results of this study are

in line with research conducted by Fita Pertiwi, Vidya

Vitta Adhivinna (2013), showing that perceived

benefits are positively related to customers' trust in

using internet banking. The hypothesis is proven and

can be accepted. The results of this study imply that

the usefulness of innovative internet banking

products such as services, effectiveness, and so on has

been proven to influence the perception of benefits to

customer trust that is the expectation of each

customer in conducting transactions. The benefits and

ease of use influence on customers' interest in

adopting new technology, in this case, internet

banking adoption. The more customers can feel the

benefits of internet banking adoption, and it will make

customers continue to use the service.

7 CONCLUSIONS

Based on the results of research and analysis carried

out, the following conclusions can be drawn:

Perception of ease, perception of risk, perception of

suitability, perceived usefulness together have a

significant effect on the adoption of internet banking.

Perception of convenience, risk perception,

perception of conformity, perception of benefit

positive and significant effect partially on internet

banking adoption. The perception of convenience has

a positive and significant effect on internet banking

adoption. Risk perception has a positive and

significant effect on internet banking adoption. The

perception of suitability has a positive and significant

effect on internet banking adoption. Perceived

benefits have a positive and significant effect on

internet banking adoption.

REFERENCES

Achmadi and Narbuko (2009). Research Methodology.

Jakarta: Earth Literacy.

Bank Indonesia (2004). Circular Letter No.6 / 18 /

DPNP.Regarding the application of risk management to

the activities of bank services through internet

banking.Jakarta: Bank, Indonesia.

Daniel Domeher, Joseph M. Frimpongand Thomas Appiah.

(2014). Adoption of financial innovation in the

Ghanaian banking industry.The Author (s) and African

Finance and Economics Consult 32African Review of

Economics and Finance Vol. 6, No. 2.

Eze, UC, JK Manyeki, LH Yaw & LC Har. (2011). Factors

Affecting Internet Banking Adoption among Young

Adults: Evidence from Malaysia. International

Conference on Social Science and Humanity.

Fita Pertiwi, Vidya Vitta Adhivinna. (2013). Effects of

Risk, Benefits, and Ease of Use on Customer Trust in

Using Internet Banking in Yogyakarta (Case Study of

Bank Mandiri Customers).Yogyakarta: PGRI

Yogyakarta University.

Gahtani, USA (2003), "Computer Technology Adoption in

Saudi Arabia: Correlates of Perceived Innovation

Attributes," Information Technology for Development.

10: 57–69.

Ghozali, Imam. (2001). Multivariate Analysis Application

with SPSS Program. Diponegoro University Publisher

Agency. Semarang.

Gigih, Niko P. (2015). Determinants of Adoption of

Internet Banking Services at Bank Mandiri Customers

Adoption of Innovation Internet Banking

27

in Surabaya.Surabaya: Perbanas STIE Scientific Article

Surabaya.

Husein Umar. (2005). Research Methods. Jakarta: Four

Salemba.

Jogiyanto. (2007). Business Research Methodology:

Misguided and Experiences. First printing. Yogyakarta:

BPFE

Karahanna, E., Straub, DW, & Chervany, NL

(1999).Information technology adoption across time: A

cross-sectional comparison of pre-adoption and post-

adoption beliefs. MIS Quarterly, 23, 183-213.

Maharsi, Sri and Fenny. (2006). Analysis of Factors

Affecting Trust and Effect of Trust on Internet Banking

User Loyalty in Surabaya.Journal of Accounting and

Finance, Vol 8, No 1.pp35-51. Petra Christian

University, Surabaya.

Marshall, TE, Rainer, RK, and Morris, S. A

(2003)."Complexity and Control as Determinants of

Performance with Information Technology

Innovations." Journal of Computer Information

Systems, 43 (3, Spring): 1-9.

Molesworth, Mike and Jukka-Petteri Suortti

(2001)."Buying Cars Online: The Adoption of the Web

for High-involvement, High-cost Purchases." Journal

of Consumer Behaviour , Volume 2, Number 2, 155-

168.

Mukherjee, A. and Nath, P. 2003. A Model of Trust in

Online Relationship Banking. The International Journal

of Bank Marketing Bradford, 21 (1), 5. March 10,

2005.http: //proquest.umi, com / pqdweb? did =

289865501 Fmt = 4 & clientId = 46969 & ROT = 309

& Vname = PQD (Proquest) database.

Polasek, M. and Wisniewski, TP 2009.An empirical

analysis of internet banking adoption in Poland.

InternationalJournal of Bank Marketing. 27 (1): 32-52.

Embrace it, Freddy. (2002). The Power of Brands.

Jakarta: Gramedia.

Reiss, MLR and Wacker, RR (2000), "Assistive

Technology Use and Abandonment Among College

Students with Disabilities," International Electronic

Journal, 3 (23) for Leadership in Learning.

Robertson, KM, and SJChivers. (1997). Prey Occurrence in

Pantropical Spotted Dolphins, Stenella attenuate, From

the Eastern Tropical Pacific.Fisheries Bulletin.95.

Washington, DC: 334-348.

Rogers, Everett M., & F. Floyd Shoemaker (1971).

Communication of Innovation A Cross-Cultural

Approach.The Free Press. New York.

Rogers, Everett M (1995), Diffusion of Innovation, The

Free Press, A Division of Macmillan Publishing C., Inc.

New York.

Sugandini, D and Effendi, I (2014), "Influence of Belief,

Knowledge, Integrative Marketing Communication,

Risk Perception, Perception of Relative Excellence in

Postponement of Adoption of Pertamax", Benefit

Journal, Faculty of Economics, Muhammadiyah

University, Solo, Vol: 17, no 2 years 2014

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

28