Analysis of Business and Added Value of Cassava Agroindustry in

Harjowinangun Village Belitang Medang Raya District East Oku

Regency

Wenti Anggraini

Department of Management, STIETrisna Negara, South Sumatra, Indonesia

Keywords: Revenue, Benefits, Value Added

Abstract: Agroindustry using material cassava main. Kelanting is widely produced by the home industry (Home

Industry). In this home industry, the use of its workforce involves workers from inside and outside the family

to carry out production activities. The author wishes to conduct a business analysis and value-added of cassava

twigs with the formulation of the problem regarding: (1) how the system of processing of cassava twigs, (2)

how much the business value (costs, acceptance, and income) on the cassava branches, (3) how much is the

value-added (costs, receipts, and income) to cassava twigs. The purpose of this study is to find answers to the

formulation of the problem. Based on the results of the study it can be concluded as follows: (1) In one

production, the total cost of cassava wandering home industry is Rp 4,715.,000, - the total home industry

revenue of cassava wandering is Rp 9,450,000, -, the total profit of home industry cassava wandering Rp.

4,735,000. (3) Cassava twisting production can provide the added value of Rp.5,500 / kg with a value-added

ratio of 0.61% of the production value.

1 INTRODUCTION

1.1 Background

The agricultural sector, in its agribusiness

perspective, with its role in the national economy,

provides several things that show the advantages that

should be considered in national development. These

advantages include seeing the high added value of

agro-industry. With this contribution to the national

economy, the agribusiness sector is increasingly

driven by the development of existing technology.

The development of this technology is because there

is still something wrong faced by the agro-industry,

including:

a. Provision of regular raw materials in the form of

adequate quantity and quality, as well as

competitive prices which are still a complicated

issue for agro-industry. Moreover, these raw

materials must be purchased on the free market

from small farmers whose locations are scattered.

b. Marketing because the products produced are of

poor quality, it is often very difficult to market

products with attractive packaging and labels.

c. The transportation of agro-industrial products

tends to be expensive because of the matter of

long distances. Thus the development of agro-

industry located in the production center area or

in the area of raw material production itself needs

to be a concern.

Because the development of agro-industry is

related to the objectives of rural area development

and the involvement of rural human resources so that

it can introduce additional activities or treatments to

commodities after they are harvested, which can later

obtain added value from the commodity produced.

The potential of cassava to be a commodity should

not be underestimated. The development of the

cassava cultivation business is very open because

various types of industries use cassava as raw

material. Approximately 14 types of derivatives are

made from processed products made from cassava,

both gablek, chips, pellets, and tapioca flour. The

domestic market needs, for example, in the food and

beverage industry (chips, syrup), textile industry,

building materials industry (casts, ceramics), paper

industry, and animal feed industry. Whereas export

opportunities for export destinations of the European

Economic Community, Japan, Korea, China, United

States of America, are used as pharmaceutical raw

34

Anggraini, W.

Analysis of Business and Added Value of Cassava Agroindustry in Harjowinangun Village Belitang Medang Raya District East Oku Regency.

DOI: 10.5220/0009966300340038

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 34-38

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

materials, raw materials for the glue industry, raw

materials for the paper industry, raw materials for the

animal feed industry, or even as raw materials for fuel

alternative biofuels.

1.2 Problem Formulation

Some of the problems that want to be investigated

in this study include:

a. How is the processing of twigs from cassava?

b. 2. How big is the business value (cost,

revenue, income, and R / C ratio) on the twigs

of cassava?

c. How much is the added value to the twigs from

cassava?

1.3 Research Objectives

The objectives to be carried out are as follows:

a. Knowing the processing of cassava twigs that

have been applied.

b. Know the value of the business (cost, revenue,

income, and R / C ratio) on cassava branches.

c. Knowing the added value of cassava twigs.

1.4 Usefulness of Research

The results of this study are expected to be useful:

a. The cassava twigs industry, in particular, is

expected to open up insights and provide an

overview of their business in decision making.

b. As a source of information for interested civil

and private institutions.

c. As a comparison and reference material for

future researchers or similar researchers.

2 RESEARCH METHOD

2.1 Types and Data Sources

The type of data collected includes primary data and

secondary data. Primary data obtained using the

method of direct interviews with respondents with a

list of questions that have been prepared. The primary

data taken in this study are data on costs, revenues,

and processing revenue from cassava and business

profile or background.

Secondary data is data or information derived

from village documentation, libraries, relevant

literature, and agencies such as Balai or Dinas

Offices, as well as the results of previous research

relating to the topic to be examined.

2.2 The Research Methods

The Research was carried out in KarangBinangun

Village, Belitang Madang Raya District, East OKU

Regency with a quantitative method, namely

describing the results using Cost Analysis and Value

Added Analysis. With both analyzes to determine the

decision of the processing industry of cassava twigs.

2.3 Data Analysis Method

With the data that has been collected in accordance

with the formulation and objectives of the study, then

checking the nature of the data by tabulating the data.

Data obtained from the results of the research are

processed and analyzed using the following methods:

2.3.1 Cost Analysis Cost

The analysis is used to determine the number of

production costs incurred by producers of twigs from

cassava and to determine the total costs incurred.

Systematically it can be calculated using the formula:

TC = FC + VC ……………….…………………. (1)

Where:

TC = Total Cost (stated in Total Cost)

FC = Fixed Cost, e.g., Depreciation of Equipment,

Land and Building Leases, expressed in Rp.

VC = Variable Cost (Variable Costs / Non-Fixed

Costs, e.g., Raw Materials, Labor, Electricity, and

Fuel, expressed in Rp)

2.3.2 RevenueRevenue

The analysis used to determine the amount of revenue

received by cassava producers in KarangBinangun

Village. To find out the total revenue, mathematically

it can be calculated using the formula:

TR = P x Q …………………………….………... (2)

Where:

TR = Total Revenue (Total Revenue, expressed in

Rp)

P = Price (stated in Rp)

Q = Quantity (Production amount)

2.3.3 RevenueRevenue

The analysis used to determine the amount of income

received by producers of cassava twigs. To find out

the total income mathematically can be calculated

using the formula:

π = TR - TC ……………………………...……… (3)

Where:

π = Profit / Revenue

TR = Total Revenue (Total Revenue, stated in Rp)

TC = Total Cost (Total Cost, expressed in Rp)

Analysis of Business and Added Value of Cassava Agroindustry in Harjowinangun Village Belitang Medang Raya District East Oku

Regency

35

2.3.4 Business Efficiency Analysis

To measure the level of business efficiency in the

production process of cassava, twigs used R / C ratio

analysis with the formula:

R / C ratio = TR / TC ………………………….... (4)

Where:

TR = Total Revenue

TC = Total Cost

If the analysis results:

R / C ratio> 1, then the business is efficient and

profitable to be attempted.

R / C ratio = 1, then the business has no loss and no

profit (break-even).

R / C ratio <1, then the business is inefficient or

unprofitable to be attempted.

2.3.5 Value Added

The amount of added value due to the processing

process is obtained from the reduction in the cost of

raw materials plus other inputs to the value of the

product produced. Added value is a reward for labor

and processing profits. To test the hypothesis that

processing raw materials provides added value

revealed by Hayami et al. (2007).

Table 1. Value Added Analysis Format

No Variable Notation

1. Production Results (Kg / Day) a

2. Raw Materials (Kg / Day) b

3. Labor (hours / Day) c

4. Conversion Factors (1/2) a / b = m

5. Labor Coefficient (3/2) c / b = n

6.

Average Product Prices (Rp /

Hour)

d

7. Average Wages (Rp / Hour) e

8. Raw Stock Prices ( Rp / hour) f

9.

Other input contributions (Rp /

kg)

g

10. Production Value (4x6) (Rp / kg) mxd = k

11.

Added value (9-8) (Rp / kg)

Value Added Ratio (11a / 10) (%)

kfg = l

l / k = h

12.

Employee Benefits (5x7) (Rp /

Kg)

Labor (12a / 11a) (%)

nxe = p

p / l = q

13.

Gains ( 11a-12a) **

Profit Rate (13a-11a) (%)

lp = r

r / l = o

Source: Sudiyono (2001) The

The basis for calculating this value-added analysis

is per kilogram of production. The standard price of

raw materials and production results used are

standard prices at the processor (producer) level. The

amount of added value due to the processing is

obtained from the reduction of raw materials and

other inputs from the value of the product produced,

not including labor, in other words, the added value

describes the rewards for labor, capital, and

management which can be stated as follows:

Value Added = f (K, B, T, U, H, h, L)

Note:

K: Production Capacity

B: Amount of raw materials used

T: Labor involved.

U: Labor wages

H: Output Price

h: Price of Raw Materials

L: Value of other inputs (the value of all sacrifices

that occur during the treatment process to add value)

From the calculation results will be produced as

follows:

a. Estimated value added (in Rupiah)

b. The ratio of value-added to the value of the

product produced (in Percent)

c. Employee benefits (in Rupiah)

d. Benefits for capital and management (in

rupiah).

2.4 Scope

This research is focused on added value and business

feasibility. The object being studied is cassava

producers.

3 RESULTS

3.1 Receipts

Receipts represent the number of products produced

in the production process multiplied by the selling

price of the product. Each producer of cassava twigs

has a different reception. This difference is due to

varying production capacities. With a different selling

price of each respondent between Rp. 16,000 up to

Rp. 20,000, the average selling price obtained from

each respondent is Rp. 18,000 per kg. The acceptance

of cassava twigs is Rp 9,450,000, with a production

capacity of 525 kg in one production.

3.2 Revenue / Profit

Revenue or profit will be obtained after knowing the

cost and revenue value. All cassava twig business

owners have positive (profitable) income. The total

income of the cassava twig business is Rp 4,715,000

in one production for 5 cassava twig business owners.

The lowest to the largest income in a single

production is Kosim (Rp. 666,000) with a percentage

of 1.6%, Topic (Rp. 774,000), Slamet (Rp. 900,000),

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

36

Kasiman (Rp. 1,150,000,), and finally Bolot (Rp.

1,225,000) with the highest percentage of 52.8%.

3.3 R / C Ratio

BC ratio analysis is used to determine the level of

efficiency in the processing of cassava twigs

financially. The efficiency of the home industry can

be determined by calculating the per cost ratio, which

is the division between the revenue of a business and

the total cost of production.

Table 1. Total Revenue and Total Cost Kelanting Once

Cassava in Process

No. Description Value (US $)

1.

2.

Total Revenue

Total Cost

9.45 million, -

4.735 million, -

Source: Primary Data Processed, 2019.

After learning the value of receipts and cost value,

then the R / C ratio value can be calculated.

R / C Ratio = IDR 9,450,000 / IDR 4,735,000

= 1.9957 or equivalent

= 2

R / C ratio on cassava branches at 1.9957 or 2, which

means R / C ratio> 1, the business is efficient, and this

business is profitable. An R / C ratio of 1.9957 or 2

means that spending 1 unit will generate revenue of

1.9957 or 2 units. For example, if you pay a fee of Rp

100,000, - it will generate revenue of Rp 199,570, or

Rp 200,000, -.

3.4 Value-added Analysis

In the processing industry of agricultural products can

create added value and labor benefits. The purpose of

this analysis is to measure how much-added value is

found in 1 (one) kg of cassava branches. The results

of the figure show how much of 1 (one) kg of cassava

twigs provide work benefits for workers. If the added

value is high, then agro-industry will have more role

in providing workers' income. As a basis for

calculating added value is per kilogram of raw

materials. For clarity, an analysis of the value-added

of cassava twigs can be seen in the table.

In the home industry of cassava twigs, it can be

seen that using cassava as much as 1,313 kg can

produce 625 kg of cassava twigs. Cassava twig

business uses 25 HK labor/ day. Thus, the labor

coefficient needed to process 1,313 kg of cassava is

0.01. The average product price is IDR 18,000 / kg,

with a conversion factor of 0.5. This can be

interpreted that 1 kg of cassava can produce cassava

twigs by 0.5 kg. Thus, the production value in this

cassava twig business is Rp. 9,000. This production

value can be allocated for cassava raw materials in the

amount of Rp 1,500 and other input contributions

(cassava spice material) in the amount of Rp 2,000.

The value-added from the production of cassava

twigs is Rp.5,500 / kg. This value is obtained from the

value of the product, reduced the price of raw

materials, and the contribution of other inputs. So

when making cassava twigs 100 kg of cassava raw

materials, it will get an added value of Rp 550,000, -

with a value-added ratio of 61% of the production

value.

From the results of data processing in this study,

it was found that labor costs Rp. 715 / kg. So it means

that every use of 1 kg of cassava raw materials, the

workers get a reward of Rp. 71500 or 13% of the

added value. While the profit gained from the cassava

twisting business is Rp 4,785 / kg of raw materials

with a profit rate of 87% of the added value in the

cassava twisting business.

4 CONCLUSIONS

Based on the results of research conducted, business

analysis and value-added analysis of cassava twigs

can be concluded that:

a. The total receipts of each household

production in one production are as follows:

Kasim (Rp. 666,000, -), Topics (Rp. 774,000,

-), Slamet (Rp. 900,000), Kasiman (Rp.

1,150,000), and Bolot (Rp. 1,225,000).

b. The total profits from each household

production in one production are as follows:

Kasim (Rp. 203,500, -), Topics (Rp. 367,366,

-), Slamet (Rp. 412,150, -), Kasiman (Rp.

546,752, -), and Bolot (Rp. IDR 580,924.

c. The R/ C value of the cassava crackers ratio is

1.9967 or 2. This indicates the return on

investment is almost or close to 100%.

d. The value-added from the production of

cassava crackers is Rp5,500 / kg, with a value-

added ratio of 61% of the production value. So

when making cassava crackers 100 kg of

cassava raw materials, it will get an added

value of Rp 550,000.

e. Employee benefits for cassava crackers are

IDR 715 / kg or 13% of the added value, while

the benefit to business owners is IDR 4,785 /

kg or a percentage level of 87% of the added

value in the cassava twisting business.

Analysis of Business and Added Value of Cassava Agroindustry in Harjowinangun Village Belitang Medang Raya District East Oku

Regency

37

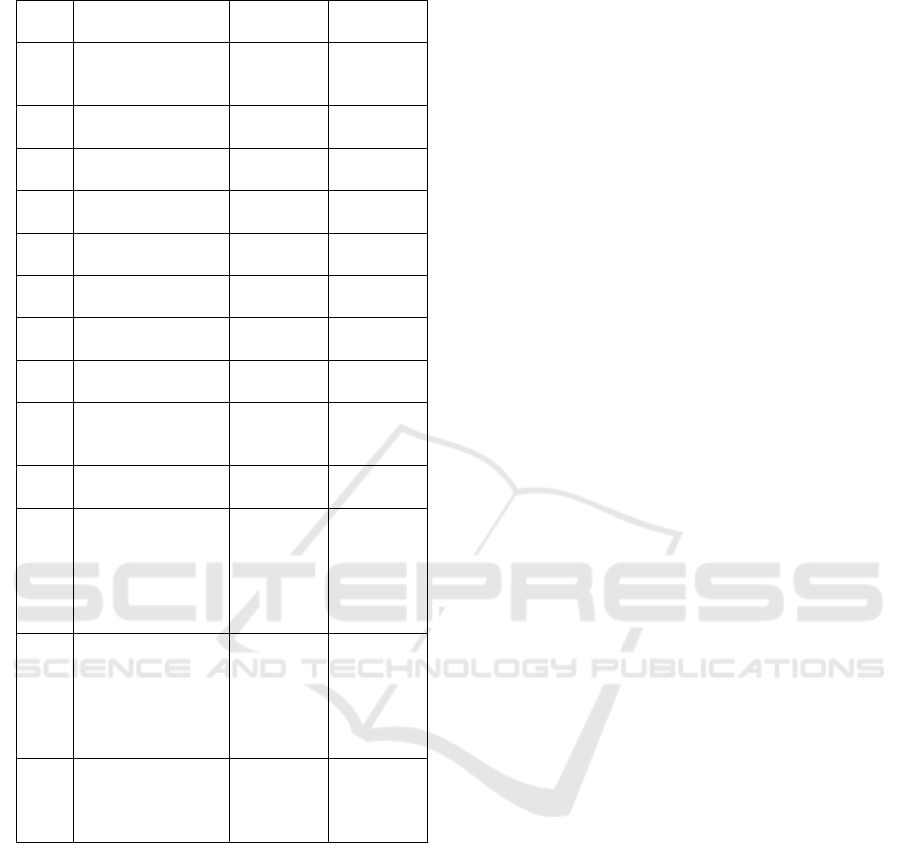

Table 2. Value Added Analysis Format

No Variable Notation

Value /

Amount

1.

Production

Results (Kg /

Day)

a 625

2.

Raw Materials

(Kg / Day)

b 1,313

3.

Labor (hours /

days)

c 25

4.

Conversion

Factors (1/2)

a / b = m 0.5

5.

Labor Coefficient

(3/2)

c / b = n 0.01

6.

Average Product

Prices (Rp / Hour)

d 18,000

7.

Average Wages

(Rp / Hours)

e 70,000

8.

Price of Raw

Baha (Rp / Hour)

f 1,500

9.

Other Input

Donations (Rp /

Kg)

g 2,000

10.

Production Value

(4x6) (Rp / Kg)

mxd = k 9,000

11.

a. Value added

(9 -8) (Rp /

Kg)

b. Value Added

Ratio (11a /

10) (%)

kfg = l

l / k = h

5,500

61%

12.

a. Labor Benefits

(5x7) (Rp /

Kg)

b. Labor Section

(12a / 11a )

(%)

nxe = p

p / l = q

700

0.13

13.

a. Profit (11a-

12a) **

b. Profit Rate

(13a-11a) (%)

lp = r

r / l = o

4,800

0.87

Source: Sudiyono( 2001)

REFERENCES

Amin Wijaya Tunggal, Management An Introduction,

Matter of Unity, Publisher GunungAgung, Jakarta, 200

Andi Efendi, 2007. The Added Value of Banana Embuk

and Its Distribution Case Study of Burno Village,

Senduro Village, Lumuro District. Agribusiness

Department, Faculty of Agriculture, University of

Muhammadiyah Malang.

BasuSwasta DH and Irawan, Modern Marketing

Management, Leberti Yogyakarta, 2005

EstiningtyasBudiasih, 2003. Analysis of the Value Added

Agroindustry of Passion Fruit Passion Case Studies in

Kopermas, Rembang District, Rembang Regency.

Agribusiness Department, Faculty of Agriculture,

University of Muhammadiyah Malang.

Lia Anggraini, 2004. Analysis of Jobong Household

Industry Costs and Revenues (Case Study of Sukodono

Village, Gresik District, Gresik Regency). Agribusiness

Department, Faculty of Agriculture, University of

Muhammadiyah Malang.

Entrepreneur Magazine, 2008. Business Opportunities and

Solutions - Great Potential of Cassava. Issue 89.

Jakarta.

Ningsih, GumoyoMumpuni, 2001. Analysis of Added

Value of JenangBeras Rice (Case in Nogolaten Village,

Jetis District, Ponorogo Regency). The University of

Muhammadiyah Malang.

Widyastuti, DyahErni et al., 1999. Study of Farming and

Added Value of Garut Agroindustry

(MarantaArundinacea L) in the Provision of Wheat

Flour Substitution Products in East Java. The

University of Muhammadiyah Malang.

www.wikipedia Indonesian, Free Encyclopedia - Cassava.

YayatHarujito, Fundamentals of Management, Jakarta:

PT.Grasindo 20011

Flippo, Principles of Personnel Management, Erlangga

Publisher, Jakarta, 2002.

George R. Terry, Management Principles, Publisher of

Earth Literacy, Jakarta, 2005.

Malayu SP Hasibuan , Human Resource Management,

Earth Literacy Publisher,

Dale Yoder, Management Services, BPFE UGM

Yogyakarta, 2002.

HelisiaMghGaraika, et al. Guidelines for Writing Thesis /

Scientific work and Procedures for Comprehensive

Examination, STIE Trisna Negara, Belitang OKU

Timur, 20017.

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

38