Designing a Decision Support System for Predicting Innovation

Activity

Olga N. Korableva

1a

, Viktoriya N. Mityakova

2b

and Olga V. Kalimullina

3c

1

St. Petersburg State University, Institute of Regional Economic Studies of Russian Academy of Science,

S-Petersburg, Russian Federation

2

St. Petersburg Electrotechnical University "LETI" (ETU), S-Petersburg, Russian Federation

3

The Bonch-Bruevich Saint-Petersburg State University of Telecommunications, S-Petersburg, Russian Federation

Keywords: Decision Support System, Innovation Activity, Potential of Economic Growth, Ontology, Semantic Search.

Abstract: Decision support systems for predicting innovation activity at the macro level are not yet widely used, and

the authors have not been able to find direct analogues of such a system. The relevance of creating the system

is due to the need to take into account heterogeneous structured and unstructured information, including in

natural language, when predicting innovation activity. The article describes the process of designing a

decision support system for predicting innovation activity, based on the system for integrating macroeconomic

and statistical data (described by the authors in previous articles) by adding a module of decision-making

methods. The UML diagram of use cases and the UML diagram of the components of this module, the general

architecture of the prototype of the decision support system, are presented. It also describes an algorithm for

predicting innovation activity and its impact on the potential for economic growth using DSS.

1 INTRODUCTION

The progressive development of the country's

economy and its level of competitiveness are

inextricably linked to innovation activity. However,

the concept under study is extremely complex and for

its comprehensive assessment, it is necessary to

evaluate a variety of indicators, both quantitative and

qualitative. Innovation, investment, efficiency of

knowledge management, problems of transferring

knowledge from the fundamental to the practical

sphere, influence of intellectual capital, susceptibility

to innovations, as well as other factors need to be

taken into account in order to assess and predict

innovation activity.

Until now, the problem of automating the process

of collecting and processing heterogeneous

information in order to forecast innovation activity at

the macro level has only been partially solved.

The previous stage of the study described a system

for collecting macroeconomic and statistical data

based on the ontology of innovation activity and

a

https://orcid.org/0000-0002-2699-8396

b

https://orcid.org/0000-0003-3772-7943

c

https://orcid.org/0000-0002-7782-6148

economic growth potential (Korableva et al., 2018,

2019). Forecasting innovation activity and its impact

on the potential of economic growth is a labor-

intensive process that requires a lot of time and effort

to prepare parameters for models, as well as to

perform calculations. Creating a decision support

system that provides models for predicting innovation

activity at the macro level and its impact on economic

growth potential by analyzing data from various types

of sources (PDF, HTML, XLS, web services) would

significantly increase the accuracy of forecasts of

innovation activity, and, as a result, the effectiveness

of decision-making in the field of managing a

country's innovation development.

2 LITERATURE REVIEW

The most complete analysis of the DSS is given in the

article (Wagner, 2017), affecting 311 systems. Let us

consider the most important comparative

characteristics.

Korableva, O., Mityakova, V. and Kalimullina, O.

Designing a Decision Support System for Predicting Innovation Activity.

DOI: 10.5220/0009565706190625

In Proceedings of the 22nd International Conference on Enterprise Information Systems (ICEIS 2020) - Volume 1, pages 619-625

ISBN: 978-989-758-423-7

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

619

* The most popular areas of application of expert

systems are accounting and financial services,

manufacturing and medicine.

* The most popular way to acquire knowledge is to

interview an expert in the subject area, including

using questionnaires. Dependency diagrams,

knowledge maps, cognitive maps, and decision trees

are also used. The recent growth of popularity of

automated knowledge acquisition methods may be

related to increased interest in neural networks and

ontologies. In addition, the multi-criteria group

decision-making (MCGDM) method (Xue et al.,

2020) is noteworthy.

* Rules are widely usable way to represent

knowledge, while frames and cognitive maps are less

popular.

The most complete analysis of the DSS is given in the

article (Wagner, 2017), affecting 311 systems.

Consider the most important comparative

characteristics.

* The most popular areas of application of expert

systems were accounting and financial services,

manufacturing and medicine.

The literature covers the process of developing a

DSS (Kossiakoff et al., 2011), describes in detail the

process of elaborating a rules-based DSS. In (Dokas

and Alapetite, 2006), modifications are described for

developing DSS as a web application in order to

increase the availability of the system via the Internet.

In General, it can be concluded that the scientific

community is interested in DSS and actively

developing methods for their building, including

using neural networks and big data processing.

DSS are the most common in areas that have a

fairly limited set of input parameters (compared to the

model at the macro level). For example, the model for

predicting the behavior of future customers provides

key information for effectively directing resources to

sales and marketing departments, planning inventory

in the warehouse and at points of sale, and for making

strategic decisions in the production process

(Martínez et al., 2020). A model for predictive group

maintenance for multi-system multicomponent

networks (MSMCN) is also interesting (Liang and

Parlikad, 2020). The key innovation in the model is

that the developed approach combines analytical and

numerical methods to optimize the service policy of

predictive groups.

The article (Wu and Wu, 2020) presents a

decision support approach for the network structured

stochastic multi-purpose index problem. The authors

also suggest an optimization - based approach to

generating scenarios to protect against the risk of

evaluating parameters for SMILP (Stochastic Mixed

Integer Linear Program).

Building a decision support system at the macro

level involves a lot of difficulties, such as the need to

take into account a huge number of parameters, both

qualitative and quantitative. A complete analogue of

the developed system was not found. However,

platforms that support the construction of

macroeconomic models and forecasting are similar to

the function being developed, such as Dynare, which

is a software platform for processing a wide class of

economic models, in particular dynamic stochastic

general equilibrium (DSGE) and overlapping

generations (OLG) models. Dynare internally uses a

complex panel of applied mathematics and computer

technologies: multidimensional nonlinear solution

and optimization, matrix factorizations, local

functional approximation, Kalman filters and

smoothers, MCMC methods for Bayesian estimation,

graph algorithms, optimal control, etc.

(https://www.dynare.org/about/).

Also it is worth noting BI platform of a company

Prognoz http://www.prognoz.ru/platform.This is an

IT solution for creating applications that combines

modern technologies of data storage, visualization,

operational data analysis (OLAP), reporting,

modeling and forecasting of various economic

processes.

The approaches include vide range of analytical

tools and gives opportunity to make forecasts.

However, the set of tools used differs significantly

from the one designed for this study and does not

provide enough tools to evaluate qualitative non-

formalized parameters.

3 RESULTS AND DISCUSSION

3.1 The Architecture of the Prototype

of Decision Support System based

on Ontology

Decision-making process (Kossiakoff et al., 2011) in

the general case has 5 stages:

1. Planning the decision-making process, which

defines:

a. Goals and objectives

b. Type of solution

c. Solution context

d. Stakeholders

e. Legacy solutions

f. Additional data

ICEIS 2020 - 22nd International Conference on Enterprise Information Systems

620

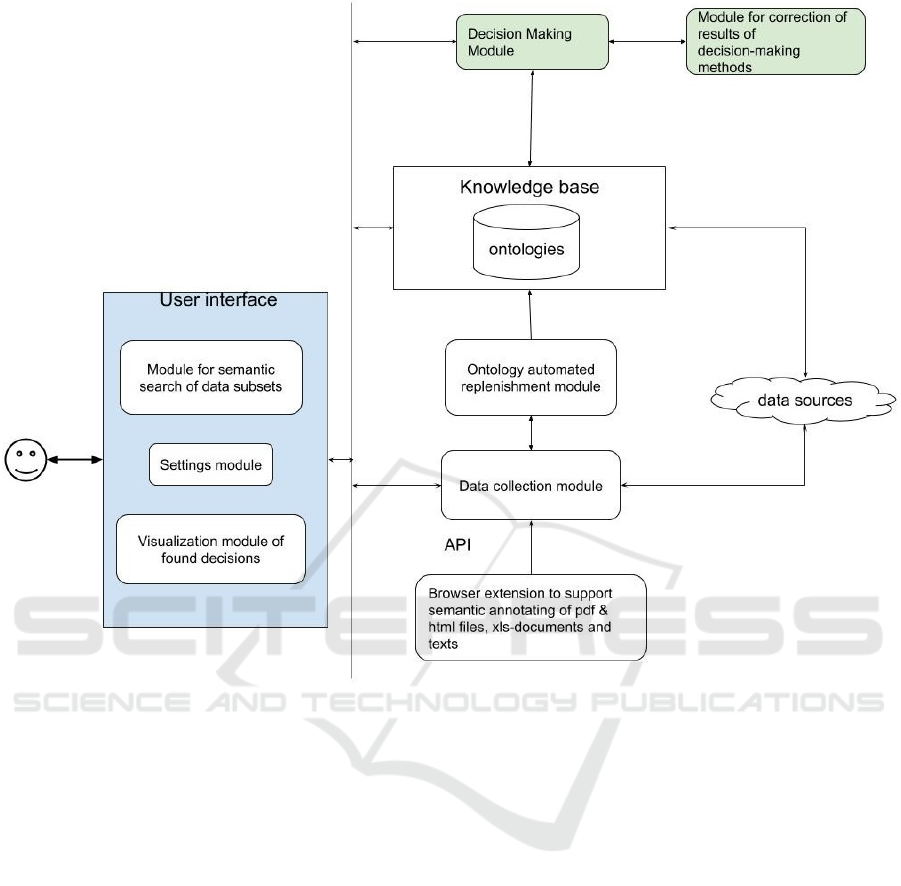

Figure 1: The General architecture of the DSS.

2. Data collection

3. Organization and processing of information

4. Taking decision

5. Implementation of decisions

In accordance with the logic of the study, point 1

was defined when determine the whole framework of

the study (Korableva et al., 2018). Then the tasks of

collecting macroeconomic and statistical data were

solved on the basis of an ontological approach and

building an ontology of innovative development and

its impact on the potential for economic growth

(automatic data aggregation system - ADAS).

At this stage, a decision support system (DSS) is

being built on the basis of the ADAS, which would

automate point 4, namely, provide models for

predicting innovation activity and its impact on the

potential for economic growth. At the current stage, a

decision support system (DSS) is being built on the

basis of ADAS, which would allow using automated

approaches for decision-making within the process of

forecasting innovation activity taking into account

multi-factor influence.

It is supposed that using this type of system will

increase the productivity of the decision-making

process and improve the quality of the decisions

themselves. The General architecture of the DSS is

shown in Fig. 1

To consider a variant of the approach to

automating forecasting, this paper describes the

process of building a prototype of a decision support

system based on the ontology of innovation activity

and economic potential growth.

Since the DSS is designed as an extension of the

ADAS, it is a client-server web application that the

user interacts with through a web interface. The web

application contains a module for collecting data from

various types of sources (PDF, HTML, XLS, web

services). Using this module, the web application

receives potential RDF triples, which are first

processed in the automated ontology replenishment

Designing a Decision Support System for Predicting Innovation Activity

621

module and stored in the knowledge base (KB). The

KB is built on the ontology of innovation activity and

economic potential. It also requests data to be

displayed in the web interface by the semantic search

system for subsets of data.

There are several types of classifications of

forecasting methods. According to one of them, all

forecasting methods can be divided into heuristic

methods, which are based on the predominance of

intuition, i.e. subjective principles, and economic and

mathematical methods, which are dominated by

objective principles (Sonina, 2014). To get a

completer and more objective picture when building

an empirical model for predicting innovation activity,

we will consider methods from both groups. The

vector autoregressive model and dynamic stochastic

model of general equilibrium are chosen as an

example of economic and mathematical approaches,

while the technological foresight method represents

heuristic methods.

Thus, several competing methods are used in the

decision-making module:

* Vector autoregressive model (VAR)

* Dynamic stochastic general equilibrium model

(DSGE)

• Neural network.

The module works as follows. The user of the DSS

submits the necessary parameters for input by

selecting them from the KB:

- For a neural network, the user selects a set of

economic indicators for the past years, based on

which it will be trained.

- For the vector autoregressive model, the user

chooses indicators for forecasting the innovation

activity of the economy as variables for building the

VAR model and the period on which the forecast will

be made.

- For DSGE, a list of parameters are selected. Some

of them are set as constants, taking into account

adaptation for the Russian economy.

This is followed by a prediction process, and

results that can be installed by the user in the decision

method adjustment module (for example, by

changing the values of input parameters or adding

them). The results obtained are used by experts in

determining forecast data, and can also be introduced

in the foresight system.

Despite the advantages of the DSGE model, there

is a criticism of it, which highlights the following

shortcomings (Andrianov et al., 2014):

* Using the concept of rational expectations, which

assumes that economic agents make the most

effective use of all available information and all

available experience when making decisions;

* Using the representative agent principle, which

reduces complex economic systems to separate

elements, and as a result neglects holistic basis of a

system;

* Applying filters depending on the selected method,

smoothing parameters, initial and final filtering

periods, and so on.

* Time-consuming procedure for deriving and

parameterizing equations.

Therefore, in the course of the study, it seems

appropriate to search for an analogue for this method,

which most fully meets the tasks set.

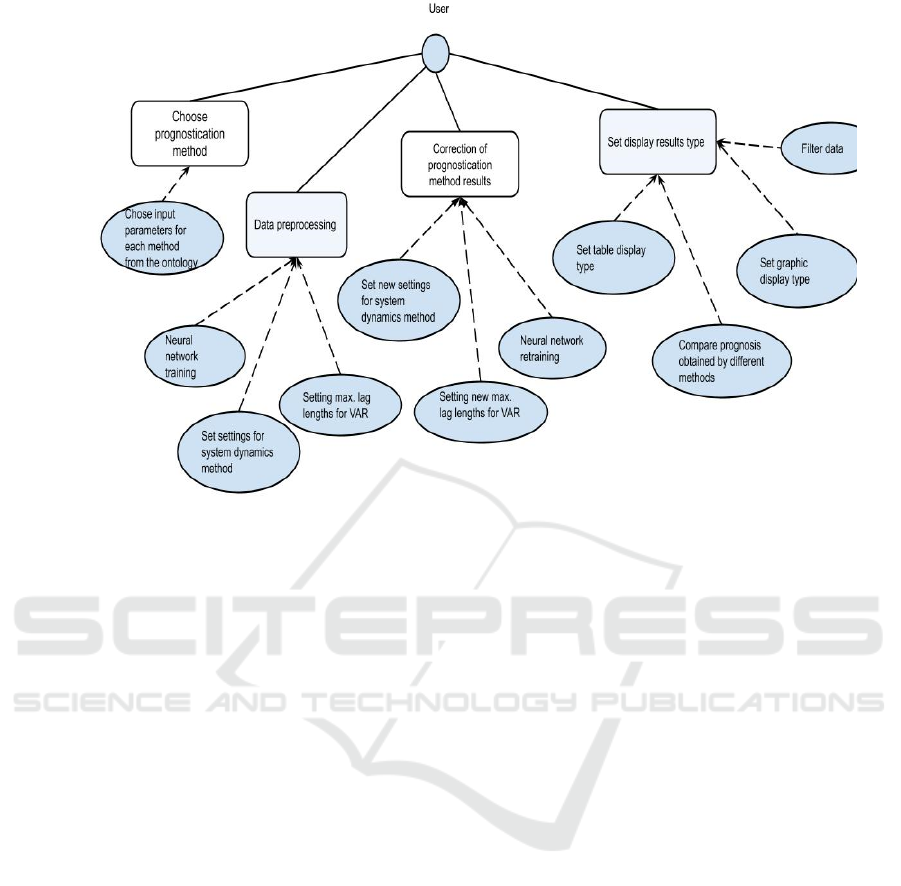

3.2 UML Diagram of Options for using

the Decision Methods Module

The UML diagram of the options for using the

decision-making methods module is shown in Fig.2.

Firstly, it is necessary to select the type of forecast

model.

Аlso, economic indicators and forecast period are

chosen. The indicators are submitted to the model as

input data. In the DSS, these indicators are stored in

the previously created ontology of macroeconomic

and statistical data.

Next, preliminary steps before forecasting are

performed. For DSGE models it is the calibration of

input parameters, for the VAR model – definition of

the maximum length of the lag, for the Neural

network - training on selected economic indicators

during the particular time period.

After that, the user receives the result of the

selected forecasting models, which can be viewed in

tabular and graphical form, filtered by different

criteria. The results obtained by different methods

can be compared with each other.

The models are built iteratively: each run can be

followed by a process of adjusting the results, which

changes the input parameters, and for the neural

network – training on the adjusted data.

Thus, the decision-making module works as a

"black box" for the end user: the user selects

economic indicators to submit for input (the

indicators themselves and their values for N years are

stored in the ontology), and at the output receives the

result of forecasting indicators.

3.3 UML-diagram of the Class of the

Decision Methods Module

UML-diagram of the class of the decision methods

module is shown in Fig. 3. Let us look at it

ICEIS 2020 - 22nd International Conference on Enterprise Information Systems

622

Figure 2: The UML diagram of the options for using the decision-making methods module.

in more detail. The main class for the decision module

is Solutions. The class defines functions for getting

all the getMethods () methods defined in the DSS, a

function for selecting user-defined prediction

methods for a specific case, setUserMethods (), and a

function for starting the executePrognosis ()

prediction. The app interface get accesses to these

features through the app API.

The Solutions class also stores a set of prediction

methods described using the method classes in Fig. 3.

This is DSGE, VAR, NeuroNetwork. Prediction

methods implement the Method interface. Each

method class contains a setMethodParams function to

install input parameters for the method and an

executeMethod () that performs method prediction

(used in the executePrognosis).

The input parameters for each method are

described by the DSGESettings, VARSettings, and

NeuroNetworkSettings classes, which are inherited

from the Settings interface. They contain collections

of input parameters with values for each prediction

method.

The prediction results for each method are also

described by separate classes (DSGEResult,

VARResult, and NeuroNetworkResult) and

implement the Result interface. They contain

collections of predicted parameters with values for

each method.

The classes of the prediction result correction

implement the ResultCorrection interface and contain

functions for correcting the prediction results of a

particular method by changing input parameters

(setMethodParams).

The relationships between the prediction method and

its settings, results, and correction class are shown

only for the DSGE class for clarity as sample.

3.4 Algorithm for Predicting

Innovation Activity and Its Impact

on the Potential for Economic

Growth using the DSS

Let’s take a closer look at the steps that need to be

taken when predicting innovation activity using the

DSS. Steps 1-3 were described in more detail in the

paper (Korableva et al., 2019).

1. Setting up the DSS by the operator. For the step, it

is necessary to specify:

* Initial data sources of selected types (PDF and XLS

documents, HTML pages, web services, and

ontologies);

• System parameters for collection: the frequency of

automatic collection, the need for automatic source

search, and so on;

* Queries to find new data sources.

2. The data collection system collects data

according to the algorithm depending on the types of

sources and leads to the structure of the ontology.

3. The automated ontology replenishment system

brings

data to the ontology structure and saves it to

Designing a Decision Support System for Predicting Innovation Activity

623

Figure 3: UML-diagram of the class of the decision methods module.

the knowledge base.

Steps 1-3 are realized iteratively for updating data and

adding new sources.

4. An operator selects economic indicators (from

those presented in the ontology) and the forecast

period, and the information is passed as input

parameters to the forecasting systems used in the DSS

(DGSE model, VAR model, neural networks).

5. The operator initiates forecasting of innovation

activity using the selected methods. The output

provides results that characterize the forecast of

macroeconomic activity (depending on the settings in

the previous step and methods).

6. Experts make adjustments to the results

obtained. In this case, the input parameters can be

changed in order to check the response of the model,

as well as to cut off the boundary values of the

predicted indicators by a specific model. For a neural

network, repeated training can occur on corrected

input data.

Steps 5-6 are also undertaken iteratively until

prediction models that satisfy the experts are got.

7. Data is transmitted to all interested parties for

use in the technological foresight and creation of the

most probable forecasting scenarios.

The developed system has been tested. The

algorithm for predicting innovation activity and its

impact on the potential for economic growth using the

DSS was used by experts to forecast macroeconomic

indicators for 2017-2019. During testing, insufficient

accuracy was revealed due to deviations in the DSGE

model. That is why further research is needed on how

to more correctly simulate expectations in DSGE

models or replace this model in the DSS.

4 CONCLUSION

This paper describes the process of designing a

decision support system for predicting innovation

activity, based on the system for integrating

macroeconomic and statistical data (described by the

authors earlier) by adding a module of decision-

making methods. The UML diagram of use cases, the

ICEIS 2020 - 22nd International Conference on Enterprise Information Systems

624

UML diagram of the components of this module, and

the General architecture of the prototype of the

decision support system are presented. It also

describes an algorithm for predicting innovation

activity and its impact on the potential for economic

growth using the DSS.

The presented DSS for forecasting of innovative

activity allows to develop a knowledge base to build

models to predict the target macroeconomic

indicators (in particular indicators of the growth

potential of the Russian Federation and innovative

activity). It also gives opportunity to automate the

process of building forecasting models for the target

macroeconomic indicators, improving the quality of

the results of the technological foresight with experts,

and make the assessment more objective and reduce

the time of forecasting.

The algorithm for predicting innovation activity

and its impact on the potential for economic growth

using the DSS has been subject to validation in the

field of forecasting of the macroeconomic indicators

for 2017-2019. In the future, it is planned to improve

the models already used, as well as finalize the

prototype of the DSS as the release version.

REFERENCES

Andrianov D.L., Schulz D.N., & Oshchepkov I.A. (2014).

Dynamic stochastic models of general economic

equilibrium. UEkS. No7 (67).

Dokas, I. & Alapetite, A. (2006). Risø-R-1570(EN) A

development process meta-model for Web based expert

systems: the Web engineering point of view.

Kossiakoff A, Sweet W. N., Seymour S. J., Biemer S. M.

(2011). Systems Engineering Principles and Practice.

Korableva, O. N., Kalimullina, O. V., & Mityakova, V. N.

(2018). Innovation activity data processing and

aggregation based on ontological modelling. Paper

presented at the 2018 4th International Conference on

Information Management, ICIM 2018, 1-4.

doi:10.1109/INFOMAN.2018.8392659

Korableva, O.N., Kalimullina, O.V., & Mityakova, V.N.

(2019). Designing a System for Integration of

Macroeconomic and Statistical Data Based on

Ontology. Advances in Intelligent Systems and

Computing, 998, p. 157-165

Liang, Z., & Parlikad, A. K. (2020). Predictive group

maintenance for multi-system multi-component

networks. Reliability Engineering and System Safety,

195 doi:10.1016/j.ress.2019.106704

Martínez, A., Schmuck, C., Pereverzyev, S., Jr., Pirker, C.,

& Haltmeier, M. (2020). A machine learning

framework for customer purchase prediction in the non-

contractual setting. European Journal of Operational

Research, 281(3), 588-596.

doi:10.1016/j.ejor.2018.04.034

Sonina O.V. (2014). Methods of forecasting the national

economy in market conditions. Diskurs-Pi. No4.

Wagner, W. P. (2017). Trends in expert system

development: A longitudinal content analysis of over

thirty years of expert system case studies. Expert

Systems with Applications, 76, 85-96.

doi:10.1016/j.eswa.2017.01.028

Wu, D., & Wu, D. D. (2020). A decision support approach

for two-stage multi-objective index tracking using

improved lagrangian decomposition. Omega (United

Kingdom), 91 doi:10.1016/j.omega.2018.12.006

Xue, M., Fu, C., & Yang, S. -. (2020). Group consensus

reaching based on a combination of expert weight and

expert reliability. Applied Mathematics and

Computation, 369 doi:10.1016/j.amc.2019.124902

Designing a Decision Support System for Predicting Innovation Activity

625