Crypto Advisor: A Web Application for Spotting Cross-Exchange

Cryptocurrency Arbitrage Opportunities

Robert-Christian Oant

,

˘

a

a

and Adriana Mihaela Coroiu

b

Faculty of Mathematics and Computer Science, Babes¸-Bolyai University, Mihail Kog

˘

alniceanu, Cluj-Napoca, Romania

Keywords:

Cryptocurrency, Cross-Exchange Arbitrage, Centralized Exchanges, Trading Automation, Arbitrage

Opportunities Spotting, Web Application, Cloud Computing.

Abstract:

The subject of this paper revolves around cryptocurrencies and trading automation, more precisely, on a low-

risk trading strategy called cross-exchange arbitrage. An approach that capitalizes on market inefficiencies by

frequently buying and selling on two distinct exchanges in order to accumulate minor profits. Our solution is a

web application for identifying opportunities produced by this strategy and delivering them in a user-friendly

manner, as well as in a structured format for developers. The main objective was to develop a production-ready

tool that is useful for professional traders, utilizing real data in real-world circumstances.

1 INTRODUCTION

Cryptocurrencies are digital assets or currencies

based on blockchain technology, which enables pay-

ment and transaction verification in the absence of a

centralized custodian. Bitcoin, the most well-known

cryptocurrency, was first described in a paper by

Satoshi Nakamoto (Nakamoto, 2008) in 2008, and it

was launched in 2009. The cryptocurrency market

has changed significantly since then. On more than

100 exchanges around the world, more than 50 mil-

lion active investors trade bitcoin and other cryptocur-

rencies. We have long been fascinated by trading au-

tomation, not only on the cryptocurrency market but

also on the stock market. But as we all know, trad-

ing does not guarantee profits, particularly when trad-

ing without a strategy, therefore we tried to design

a system that minimizes risk and focuses on nearly

market-neutral strategies that can guarantee long-term

earnings. This paper aims to provide comprehensive

research on a specific low-risk cryptocurrency trading

strategy called cross-exchange arbitrage.

2 THEORETICAL BACKGROUND

Blockchain Technology. Blockchain, as explained

by Fang in (Fang et al., 2022), is a digital ledger of

a

https://orcid.org/0000-0002-5823-1827

b

https://orcid.org/0000-0001-5275-3432

economic transactions that can be used to record any-

thing with inherent worth, not simply financial trans-

actions. In its most basic form, a Blockchain is a col-

lection of immutable data entries with timestamps that

are maintained by a distributed network of machines.

A transaction is, for example, a file that says, ”A pays

X Bitcoins to B” and is signed using A’s private key.

This is the most fundamental form of public-key cryp-

tography, as well as the foundation for cryptocurren-

cies. On these networks, cryptocurrencies are the to-

kens used to send value and pay for transactions. They

can be regarded as Blockchain tools, but in certain sit-

uations, they can also act as resources or utilities.

Cryptocurrency Exchanges. A cryptocurrency ex-

change or Digital Currency Exchange (DCE) is a

business that allows customers to trade cryptocurren-

cies. The practical part of this thesis revolves a lot

around exchanges and the variation in prices of assets

on these exchanges, so it is important to understand

what type of markets exist and why there might be

a price discrepancy for similar assets. To expand on

the above statement, there are two primary sorts of

exchanges:

• Centralized exchanges (CEX): as the term im-

plies, CEXs are crypto exchanges founded by

centralized entities that control the exchange’s

ownership. The pricing of assets on central-

ized exchanges is determined by the most re-

cently matched bid-ask order on the exchange or-

der book.

238

Oant

,

˘

a, R. and Coroiu, A.

Crypto Advisor: A Web Application for Spotting Cross-Exchange Cryptocurrency Arbitrage Opportunities.

DOI: 10.5220/0011850400003470

In Proceedings of the 15th International Conference on Computer Supported Education (CSEDU 2023) - Volume 1, pages 238-246

ISBN: 978-989-758-641-5; ISSN: 2184-5026

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

• Decentralized exchanges (DEX): in contrast to

CEXs, DEXs rely on arbitrage traders to main-

tain prices in check. Instead of an orderbook

in which buyers and sellers are matched to trade

cryptocurrency assets, these exchanges utilize liq-

uidity pools.

To be noted, the practical application of this paper is

related mostly to CEXs.

Arbitrage Trading Strategies. Defining cryptocur-

rency trading in a simple form - is the act of buy-

ing and selling cryptocurrencies with the purpose of

profit. A trading strategy is an algorithm of prede-

fined rules and events that trigger buying and sell-

ing crypto assets on one or multiple markets (as men-

tioned in (Jothi and Oswalt Manoj, 2022)). There are

numerous trading strategies available, but the focus

of this thesis is on arbitrage trading. Furthermore,

arbitrage trading can be divided into multiple sub-

strategies as described in (Shynkevich, 2021), such as

cross-exchange arbitrage, spatial arbitrage, triangular

arbitrage, decentralized arbitrage, and statistical arbi-

trage. As mentioned previously, our focus is on the

cross-exchange arbitrage strategy.

3 CROSS-EXCHANGE

ARBITRAGE METHOD

Cross-exchange arbitrage is a low-risk strategy that

capitalizes on market inefficiencies by frequently

buying and selling on two distinct exchanges in order

to accumulate minor profits.

3.1 Why Is this Strategy Low-Risk?

As described in (Lacity, 2020), traders that recognize

arbitrage opportunities and capitalize on them do so

with the expectation of making a fixed profit, rather

than assessing market sentiments or relying on other

predictive pricing strategies. Also, depending on the

resources available to traders, it is possible to enter

and exit an arbitrage trade in seconds or minutes. Al-

though this sounds good in theory, numerous factors

must be considered, such as fees, timing, availability,

and profitability.

On the majority of exchanges, we can distinguish

the following sorts of usual fees:

• Withdraw fees: These are the costs incurred when

withdrawing a crypto asset from an exchange’s

digital wallet. Typically, these fees are flat (set

amount) and determined by the coin you desire to

withdraw and the blockchain on which the with-

drawal activity is performed.

• Trading fees: These are the charges associated

with purchasing and selling crypto on an ex-

change. They are often based on percentages,

ranging from 0.05 percent to 0.5 percent, and are

primarily divided into two categories: maker fees

and taker fees, according to (Lansky, 2018).

3.2 Timing and Availability

Time is of the essence in arbitrage trading. The

pricing discrepancy between two exchanges tends to

shrink as more traders take advantage of a given ar-

bitrage opportunity, this is due to the law of supply

and demand. Some of the factors that could affect the

time it takes to execute a successful arbitrage trade are

listed below (as presented in (Fang et al., 2022)):

• Transaction speed: Because you must perform

cross-exchange transactions, the time it takes to

validate these transitions on the blockchain may

have an impact on the effectiveness of your arbi-

trage trading strategy.

• AML checks: Although arbitrage trading is not il-

legal in any kind of way, when substantial sums

of money are moved by a trader, exchanges fre-

quently conduct anti-money laundering (AML)

checks. Such examinations might take weeks in

some circumstances.

• Offline wallets: Crypto exchanges are prone to

outages. For one reason or another, crypto ex-

changes may restrict the withdrawal and deposit

of specific digital assets.

3.3 Algorithm Steps

This section presents the steps of executing a cross-

exchange arbitrage trade. An arbitrage opportunity

is spotted between exchange A and exchange B for

the coin BTC, pair BTC/USDT. First of all, assuming

we have a certain amount of USDT in our account on

exchange A.

1. Trade BTC/USDT pair on exchange A, effectively

buying on the ask price for how much USDT

amount we have. Therefore, we have successfully

converted our amount of USDT into BTC. By do-

ing this operation, we have incurred a trading fee.

2. Withdraw the amount of BTC we have to ex-

change B, making sure that the withdraw chain

from exchange A is the same with deposit chain

from exchange B. By doing this operation, we

have incurred a withdraw fee.

3. Once the BTC is deposited on exchange B, we

trade USDT/BTC, effectively selling on the bid

Crypto Advisor: A Web Application for Spotting Cross-Exchange Cryptocurrency Arbitrage Opportunities

239

price for how much BTC amount we have. There-

fore, we have successfully converted our amount

of BTC into USDT. By doing this operation, we

have incurred another trading fee.

4. Now we are left with more USDT than we first

started, effectively making a profit. This has been

a successful arbitrage cycle.

5. Optionally, we can repeat the cycle by withdraw-

ing our USDT back to exchange A. Note that this

operation is taxed by another withdraw fee.

E. Profitability The formula based on quantity,

rate, trade, and fee can be used to estimate the prof-

itability of an arbitrage opportunity (the result is

percentage-based on the initial quantity).

4 TECHNOLOGIES

In this section, we analyze the advantages and limi-

tations of our application’s underlying technologies.

We will cover web application architecture, client-

side and server-side frameworks, and cloud deploy-

ment.

Client-Server Architecture. A client–server archi-

tecture divides an application into client and server

components. This application type is executed across

a computer network connecting the client and the

server. The server provides the essential functionality

of such a design: any number of clients can connect to

the server and request that it accomplish a task. The

server accepts these requests, completes the requested

task, and returns any necessary results to the client,

according to (Fraternali, 1999).

Single-Page Applications. There are numerous sorts

of web applications, including static web applica-

tions, dynamic web applications, e-commerce appli-

cations, portal web applications, progressive web ap-

plications, etc. Our application is classified as a

Single-Page Application (SPA). Following (Hacker

and Hatemi-J, 2012), single-page web apps allow for

dynamic interaction by modifying the current page’s

content rather than loading entirely new pages from

the server whenever a user action is done. AJAX,

a condensed form of Asynchronous JavaScript and

XML, is the foundation for enabling page communi-

cations and, thus, for making SPAs a reality. Single-

page applications are similar to traditional desktop ap-

plications in that they do not disrupt the user experi-

ence.

FastAPI. FastAPI is a modern, fast (high-

performance), server-side web framework for

building APIs with Python 3.6+ based on standard

Python type hints. Despite Python’s reputation as

being a slower programming language because it is

interpreted rather than compiled, FastAPI provides

the same level of performance as typically quicker

languages. As depicted in Figure 1, we can see a

performance benchmark in comparison with other

frameworks written in Go, JavaScript and Python.

Figure 1: Performance Benchmark.

It may not be clear how FastAPI is able to achieve

this staggering performance only by looking under the

hood we can see that this framework makes use of the

asyncio package in Python. FastApi is capable of in-

tegrating so well with Asyncio because it is built atop

Starlette, a lightweight ASGI framework/tool that is

perfect for developing async web services. As a spiri-

tual successor to WSGI, ASGI is a standard interface.

It allows for interoperability throughout the whole

Python async web stack, including servers, applica-

tions, middleware, and individual components. Con-

currency is applied at the request/response level; thus

your application will act in a non-blocking manner

throughout the stack. As a result, the performance

gains are significant. There are multiple other capa-

bilities in FastAPI’s toolbox, including the use of py-

dantic schemas, powerful dependency injection, and

Jinja2 integration, as detailed in (Kornienko et al.,

2021).

Vue. Vue is a client-side JavaScript framework for

building user interfaces and single-page applications

(SPAs). It is built on top of conventional HTML,

CSS, and JavaScript, and it is based on a declarative,

component-based programming model that helps you

create user interfaces quickly, no matter how basic or

complex they are. It mainly follows the architectural

pattern of model-view-viewmodel. Inspired by Vue’s

team comparison (Hanchett and Listwon, 2018), in

the following paragraphs we will compare it with two

other popular client-side frameworks React and An-

gular. React and Vue share some similarities such as

utilizing a virtual DOM and providing reactive and

composable view components. All React components

use JSX, a declarative XML-like syntax that oper-

ates withing JavaScript. Using JSX to render func-

tions has the benefit of harnessing the capability of a

full programming language (JavaScript) to build your

view. Despite supporting JSX, Vue’s default experi-

CSEDU 2023 - 15th International Conference on Computer Supported Education

240

ence is templates, a simpler alternative. The benefit

of templates is that they are more intuitive to under-

stand for developers that have worked with HTML,

and that existing applications can be progressively mi-

grated to make use of Vue’s reactivity features. Some

of Vue’s syntax will resemble that of AngularJS (e.g.

v-if vs ng-if). This is due to the fact that AngularJS

got a number of things right, and these were an early

source of inspiration for Vue. Both in terms of API

and design, Vue is considerably easier to use than

AngularJS. In most cases, learning enough to con-

struct non-trivial applications takes less than a day,

but this is not the case with AngularJS. Moreover, Vue

is a more flexible, modular solution than AngularJS,

which has firm convictions about how your applica-

tions should be constructed. While this makes Vue

more adaptable to a wider range of projects, we also

acknowledge that there are instances when it’s bene-

ficial to have some decisions made for you so you can

get straight to working.

4.1 Cloud Deployment

Cloud Deployment is the process of deploying an ap-

plication using one or more cloud-based hosting mod-

els, such as software as a service (SaaS), platform

as a service (PaaS), and/or infrastructure as a service

(IaaS). This covers designing, planning, executing,

and running cloud workloads.

4.1.1 Heroku Server-Side Deployment

Heroku is a platform as a service (PaaS) that enables

developers to build, run, and operate applications

entirely in the cloud. PaaS architectures typically

include operating systems, programming-language

execution environments, libraries, databases, web

servers, and connectivity to some platforms. The

Heroku cloud service platform is based on a managed

container (called dynos within the Heroku paradigm)

system. It has integrated data services and a powerful

ecosystem for deploying and running modern appli-

cations. Heroku is, in our opinion, a superior alter-

native for developers new to cloud deployment than

its IaaS competitors, Azure or AWS, due to the fact

that in a PaaS service, you do not have to worry about

managing containers, load balancers, or databases;

all are given as a managed service. Its pricing (free

500 hours of dyno usage each month), python build-

packs, and various add-ons, like free databases, SSL

certificates, custom domain names, smtp mail server,

among others, are a few of its attractions.

4.1.2 Netlify Client-Side Deployment

Similarly to Heroku, Netlify is also a PaaS, the main

distinction is that Netlify mainly focuses on host-

ing static websites with serverless backends, whereas

Heroku is built to host dynamic, server-side rendered

websites and apps. The way Netlify works is quite in-

novative as it aims to decouple the client-side from the

server-side part of an app. By the use of the Jamstack,

Netlify delivers a precompiled and optimized static

frontend which is deployed globally via the Edge

CDN. The server-side consists of multiple serverless

functions distributed as microservices, hence lower-

ing load. In addition, these functions are deployed to

AWS Lambda and turned into API endpoints. How-

ever, in our particular case, a serverless backend was

unnecessary, as all of the server-side code was de-

ployed to the aforementioned Heroku. Some of its

perks include making the deployment process fast

and intuitive, pricing (300 minutes of free build time

per month), and add-ons such as CD integration with

GitHub, free TLS encryption, a custom domain name,

and SPA integration.

5 SIMILAR SOLUTIONS

As the sector for arbitrage trading automation is not

highly developed, there are not as many similar pop-

ular solutions in this field. Although arbitrage trading

is quite popular, it is often conducted by individuals

using proprietary software or open-source bots, which

require specialized programming and cryptocurrency

skills to operate. To clarify, crypto trading automa-

tion is developed, however, crypto arbitrage trading

automation is not. There are numerous powerful bots

that trade cryptocurrencies on your behalf using typi-

cally straightforward tactics. Some of these general

bots are included on popular platforms such as Pi-

onex, Kucoin, and Coinrule, among others. Except

for Pionex, which offers some sort of arbitrage bot,

the rest of the mentioned platforms do not really offer

any solutions. Moreover, Pionex’s trading bot utilizes

spot-futures arbitrage, which is an entirely different

story from cross-exchange arbitrage. Although, in the

course of our extensive research, we have uncovered

a number of relatively obscure and somewhat popular

platforms that are comparable to our concept. Table 1

presents an unbiased comparison between these alter-

natives. Note that Crypto Advisor is our solution.

Legend for the table content: a - Automated Sys-

tem: the ability to automatically trade cryptocurrency

on your behalf. b - Spotter: continuous finder of ar-

bitrage opportunities without user input. c - Spotting

Crypto Advisor: A Web Application for Spotting Cross-Exchange Cryptocurrency Arbitrage Opportunities

241

Table 1: Solution APPs comparison.

Characteristics Crypto Advisor ArbiTool ArbiSmart Cryptohopper Coygo Hummingbot

Web Platform Yes Yes Yes Yes Yes No

Main Function Spotter Spotter Automated Platform Automated Platform Spotter and Automated Platform Terminal-like Bot and ecosystem

Automated Systema No No Yes Yes Yes Yes

Programmable Bot No No No No No Yes

Spotterb Yes Yes Yes Yes Yes Yes, but limited

Spotting tablec Yes Yes No No Yes No

History tabled Yes No No No No No

Wallet Statuse No Yes N/An N/A ? o Yes

Tx Timef No Yes N/A N/A ? No

Complex Filtersg Yes Yes N/A N/A Yes N/A

Email Alerts Yes Yes for Premium N/A N/A ? N/A

Market Depth Yes Yes No No Yes Yes

Orderbook Table No Yes No No ? ?

Public API Yes No No Yes Swapped for trading terminal N/A

Opportunities Endpointh Yes N/A N/A Something similar N/A N/A

History Endpointi Yes N/A N/A Yes N/A N/A

Opportunities WebSocketj Yes No No No N/A N/A

Subscription Free Free and premium Fee-based Free and premium Free and premium Open-source and Free

Nr of supported exchanges 10 35 20 9 11 33

DEX supportk No No No No No Yes

Nr of supported currencies 1000

?,probably

>1000

? 75 ?

?,probably

>1000

table: web or in-app/terminal presentation of current

arbitrage opportunities. d - History table: web or in-

app/terminal presentation of past arbitrage opportuni-

ties. e - Wallet Status: provides the wallet status (of-

fline, online) for multiple currencies and exchanges. f

- Tx time: estimated transaction time between two ex-

changes. g - Complex filters: complex filtering capa-

bilities for the spotting table. h - Opportunities End-

point: API endpoint for receiving JSON information

about current arbitrage opportunities. i - History End-

point: API endpoint for past arbitrage opportunities

or useful backtesting info. j - Opportunities Web-

Socket: 24/7 streaming WebSocket for current arbi-

trage opportunities. k - DEX support: supports the

usage of decentralized exchanges. l - Exchange Con-

nectors: how does the platform connect to various ex-

changes (automatic, no need for connection, private

API keys). m - Spotting/Trading latency: the delay in

spotting/trading an arbitrage opportunity. n - N/A, not

applicable. o - ?, unknown, no data.

6 PRACTICAL APPLICATION

6.1 Project Description

As presented in the previous section, our solution

is Crypto Advisor. A web application for spotting

cross-exchange cryptocurrency arbitrage opportuni-

ties. This application’s primary objective was to pro-

vide a robust public API solution that works as a data

collector, locating the values of cryptocurrencies on

many exchanges and spotting arbitrage opportunities

between them. Moreover, a public streaming Web-

Socket was developed, which essentially functions as

an extension of the API by continuously delivering

arbitrage opportunities to connected clients. In order

to present the API more effectively, we have also de-

signed a web application that is built upon it. The

client-side consumes the data supplied by our API

and displays it to the client in an easy-to-use format.

Additionally, we have also implemented user authen-

tication, email notifications, and OpenAPI standards

documentation.

6.2 Pre-Implementation Analysis

After analyzing the application’s requirements, we

have determined that its development lifecycle con-

sists of four major stages: Arbitrage algorithm im-

plementation and data collection, API Implementa-

tion, Front-End/UI Implementation, and Cloud De-

ployment. The development was conducted in the

presented order. To further highlight the features and

constraints of our application, we have prepared the

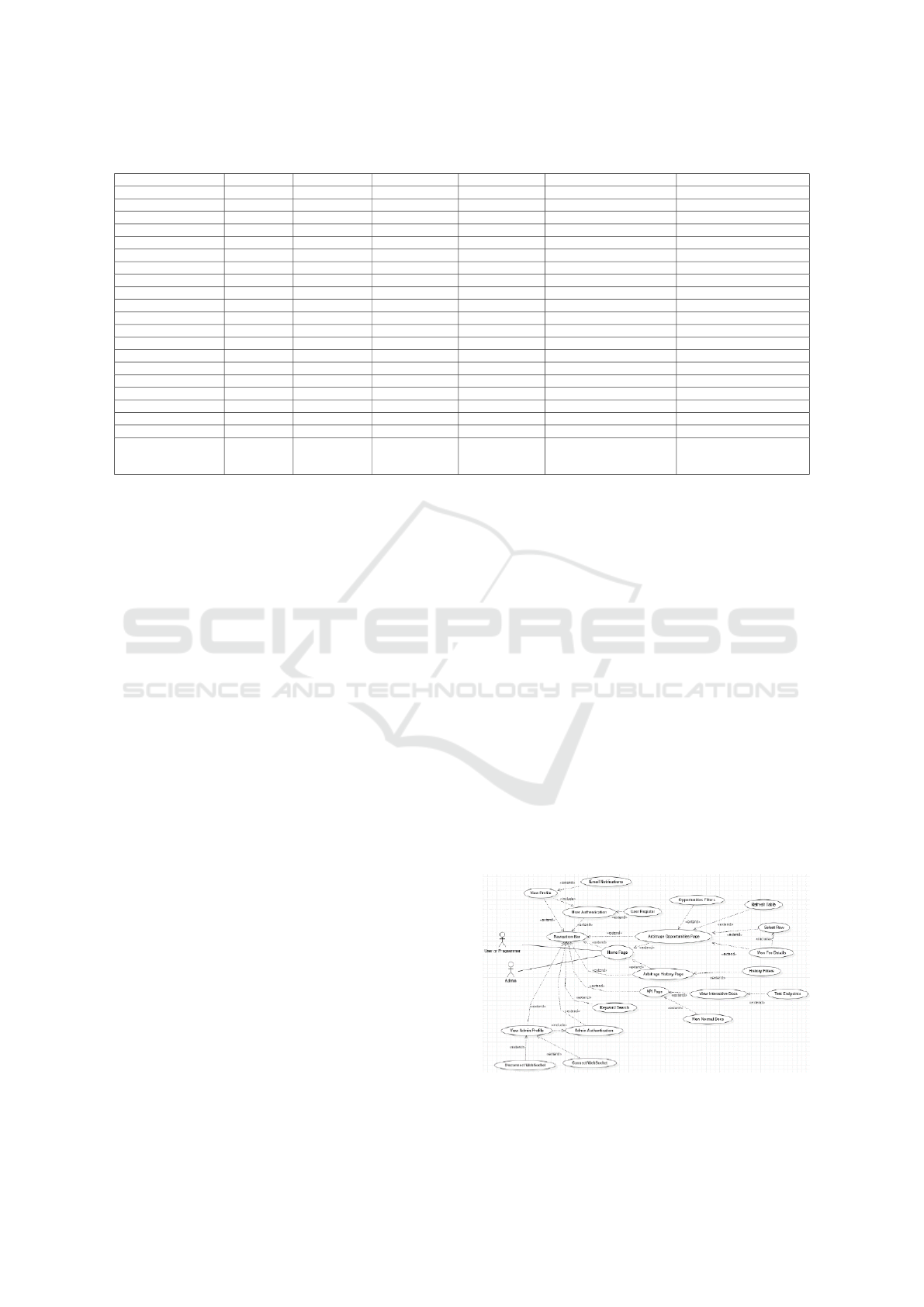

following use cases diagram, depicted in Figure 2.

Figure 2: Use cases diagram.

CSEDU 2023 - 15th International Conference on Computer Supported Education

242

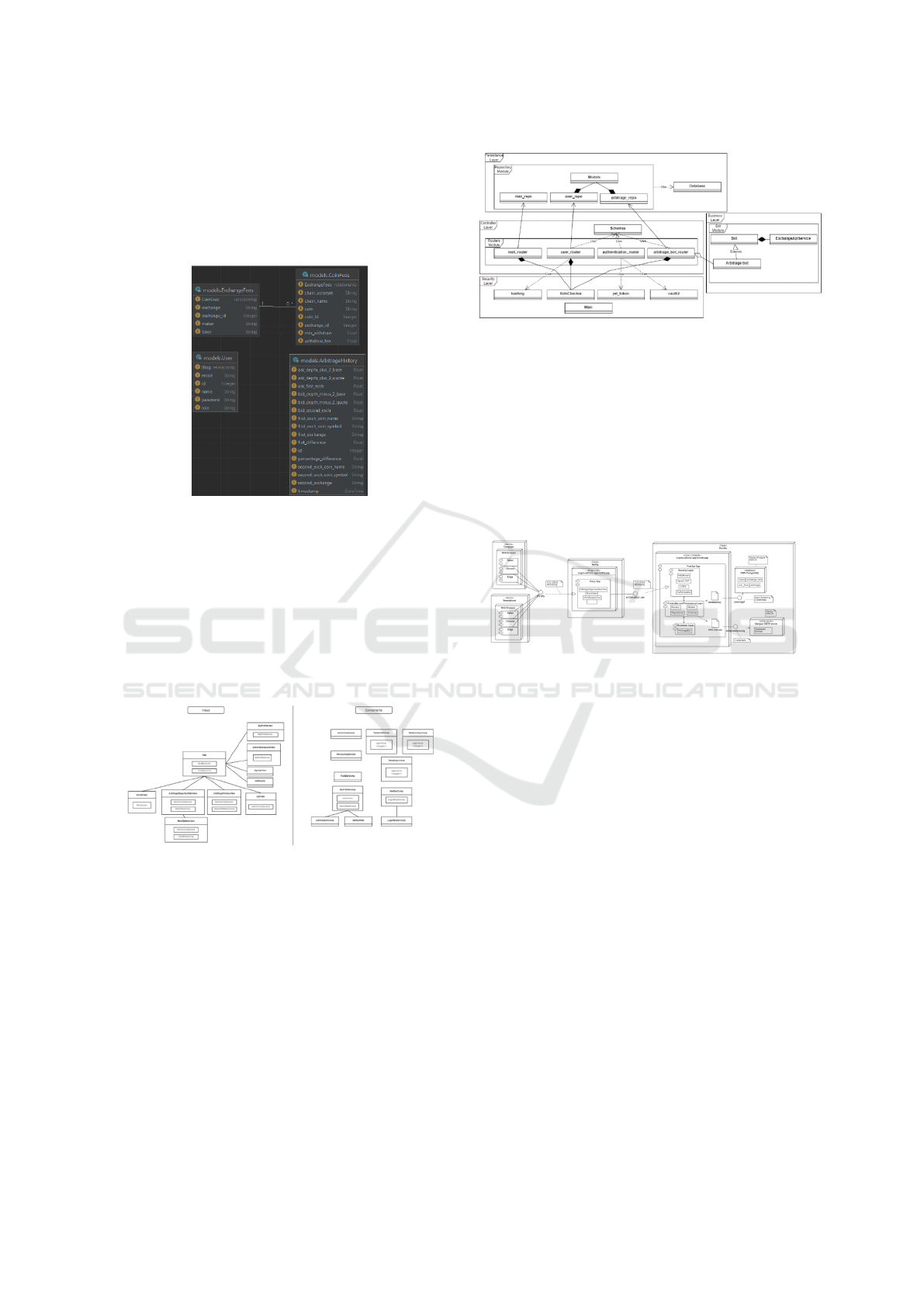

6.3 Domain Models

We have also constructed a diagram depicting the do-

main models of our application. SqlAlchemy ORM

creates the tables in our database based on these mod-

els (as we can see in Figure 3).

Figure 3: Domain Models Diagram.

6.4 Architecture

6.4.1 Client-Side Architecture

As Vue.js is a client-side component-based frame-

work employing the model-view-viewmodel pattern,

reusability is strongly encouraged, which is why com-

ponents are embedded in other components or views

in the diagram below: Figure 4.

Figure 4: Client-Side Architecture Diagram.

Views have the same capabilities as components,

but they are mostly utilized for routing; hence, you

could say that a distinct page is a view.

6.4.2 Server-Side Architecture

To illustrate how the layers communicate with each

other, we have constructed a diagram of the entire

server-side application: Figure 5.

Note that we omitted fields and methods because it

would make the diagram much more difficult to com-

prehend. Usually, python applications are difficult to

portray in a UML class diagram since python is not

as restrictive in OOP and classes are not mandatory.

Figure 5: Server-side Architecture Diagram.

Therefore, some of the so-called classes in figure 6

are essentially simple files with static attributes and

methods that behave similarly to a singleton class

6.4.3 Deployment Architecture

In order to better understand the security procedures

and layers of our application, we have created a de-

ployment diagram (we can see in Figure 6) depicting

how our services are distributed over different servers.

Figure 6: Deployment Architecture Diagram.

Essentially, any device with a browser can ac-

cess our system via the URL: https://crypto-advisor-

app.netlify.app/home

The front-end service then interacts with the

Heroku-deployed REST API. In addition, we have

utilized Heroku’s add-ons such as an AWS Post-

greSQL database and Mailgun SMTP server.

6.5 Business Layer

The Business layer of this application encapsulates

the module Bot-Folder where all the logic behind ar-

bitrage spotting is implemented. As shown in Figure

5, the module has high cohesiveness between its com-

ponents and is only loosely coupled to a Rest Con-

troller responsible for arbitrage endpoints. This mod-

ule can be easily isolated from the rest of the applica-

tion because it operates independently. The abstract

class Bot provides a generalization of the Arbitrage-

Bot class. This class mostly adheres to a Strategy-

like Pattern and has concrete methods for data col-

lecting and parsing that can be used in any kind of

Bot (Do This, ).

Crypto Advisor: A Web Application for Spotting Cross-Exchange Cryptocurrency Arbitrage Opportunities

243

6.5.1 Data Collecting and Parsing

The primary purpose of the ExchangeApiService

class is to connect to external APIs and scrape web-

sites. Multiple external services, such as the Coin-

MarketCap API, the CCXT library (onl, ), and the

CoinMarketFees website (Atzberger et al., 2022), are

present in the class and are actively utilized. The

CCXT library is responsible for collecting data such

as coin prices and order book details, users of this li-

brary will have direct access to the source (the API

endpoints of various exchanges), resulting in the most

accurate data available. The CoinMarketCap API is

mostly used for retrieving the topmost 1000 popular

currencies because these coins often have the highest

trading activity and are more likely to provide arbi-

trage opportunities.

As the ccxt library is not very reliable on fees, we

have used beautiful soup (a python library for web

scraping (Richardson, 2007)) to collect as much data

as possible from the CoinMarketFees website, where

fees are typically accurate.

6.5.2 Data Manipulation and Arbitrage Spotting

ArbitrageBot is an implementation of the generic Bot

class; its primary function is to manipulate received

data and identify arbitrage opportunities. The gather-

data method relies on the superclass’s methods in or-

der to retrieve data from the ExchangeApiService.

After that, a comparison is made between all ex-

changes, and then all pairs of the used exchanges,

under a predetermined threshold of percentage differ-

ence, and a JSON-style dictionary is constructed con-

taining all opportunities. Information about market

liquidity and fees is obtain through other methods.

6.6 Controller Layer

This layer’s purpose is to expose the Rest endpoints.

Encapsulating the routers module, which contains the

API’s controllers for its many functionalities (user

router, authentication router, mail router and arbitrage

router). This module primarily defines the URLs, pa-

rameters, dependencies, and response schemas of our

endpoints. In addition, by utilizing dependency in-

jection, unauthorized access to the resources is pre-

vented. The database connection is also provided us-

ing injections by referencing a function from our con-

nection file which yields a Session object that can be

later used for queries (Copeland, 2008). In order to

maintain a clean separation between our layers, end-

point functionality is delegated to the repository mod-

ule of the persistent layer.

Endpoints. One of the top objectives in creating

our endpoints was to ensure full synchronicity be-

tween them so that time-intensive endpoints, such

as the endpoint for identifying opportunities, would

not cause the application to underperform. Thus,

endpoints will function optimally when several si-

multaneous calls are made without any time delays.

The arbitrage router contains endpoints primarily as-

sociated with our business layer, such as endpoints

for identifying opportunities, storing scrapped fees

in our database, retrieving past arbitrage opportuni-

ties from our database, obtaining trading fees for spe-

cific coins and exchanges, a WebSocket for contin-

uous streaming our opportunities, and endpoints for

internal connection and disconnection from the Web-

Socket (Pterneas, 2013). The authentication router is

mostly associated with the security layer, where all

functionality is outsourced, and its primary job is to

expose a login endpoint. Similarly, to the authentica-

tion router, the Mail router has the primary purpose

of exposing an endpoint related to the email notifica-

tions for our users. Lastly, the User router is related to

CRUD operations on our users, namely creating (reg-

istering), reading, updating, and deleting user infor-

mation.

WebSocket. Due to challenges in gathering data in

the client-side portion of this application, as time-

intensive endpoints would be terminated on refresh-

ing, losing crucial information, our solution is a Web-

Socket that continuously broadcasts the most recently

computed list of opportunities. Thus, when required,

the client-side can obtain all data almost instantly.

Note that this WebSocket, as well as a few arbitrage

endpoints, are publicly accessible via our API solu-

tion. Several setbacks have occurred throughout the

development of this websocket. Typically, websock-

ets should be a separate service that operates indepen-

dently from the rest of the application. However, this

is not possible in our case, thus our websocket is es-

sentially incorporated as an endpoint, which has led

to numerous difficulties in maintaining synchronic-

ity. For the rest of the endpoints, synchronicity is

assured by design, as the FastApi framework inserts

the endpoint functions in a self-managing thread or

event pool, but this is not the case with websockets.

We had to manually obtain the running event loop and

inject the websocket’s functionality, which proved to

be quite challenging, but we were ultimately success-

ful. However, additional optimizations are required as

the number of external clients connecting to our web-

socket affects its performance.

CSEDU 2023 - 15th International Conference on Computer Supported Education

244

6.7 Persistance Layer

The persistence layer consists primarily of the ORM

models (Figure 4) that are used to generate database

tables, as well as the repository module. As indicated

before, the repository module is responsible for ac-

cessing the database tables utilizing the injected Ses-

sion object and defining the endpoint functionality.

Essentially, each Rest Controller has its own associ-

ated repository. Typically, functions are divided into

computational functions and database manipulation

functions. In addition, common HTTP exceptions

such as 404 not found error, 500 internal server er-

ror and 409 conflict error are raised here (Zhu et al.,

2015).

6.8 Security Layer

As this application is distributed on the web, we have

invested a great deal of work ensuring that it has a

solid security foundation. This module consists of

functionalities for user authentication through RBAC

(Sandhu, 1998) and oauth2’s JWT (Bucher and

Christensen, 2019; MAN, ), as well as middleware

(Middleware, 2006)and CORS (Abdelhamied, 2016).

Firstly, in order to assure that our user’s credentials

are safe we have used OAuth2PasswordRequestForm

and OAuth2PasswordBearer from FastAPI’s library

(Bansal and Ouda, 2022), which is mainly repre-

sented through a form-data in the endpoint request

body. Furthermore, user’s credentials are stored in

the database in an encrypted format using the bcrypt

hashing algorithm which ensures that brute force and

rainbow table attacks are not feasible (Sriramya and

Karthika, 2015). Our login endpoint from the authen-

tication router verifies through bycrpt that the sup-

plied credentials match those stored in the database.

After that, it returns the JWT token with the expira-

tion date, username, email and the role of our user

embedded in itself. This token can be later decrypted

using the Secret Key. All of our critical endpoints

necessitate an Authorization header with a valid un-

expired token in order to function. Furthermore,

role-based access to resources is ensured by check-

ing the provided token and matching it to the cur-

rent user token. Even though a common user has

a valid token, RBAC prevents him from accessing

admin-specific endpoints. Although middleware is

generally a separate server that operates as a proxy,

we only have some sort of middleware that intercepts

API calls and runs a specific validation code segment.

Our middleware function validates client IP addresses

based on a whitelist of allowed addresses, returning

a 400 Bad Request Error otherwise. As our client-

side and server-side are placed on separate servers,

we have assured via CORS that only calls from our

specific client-side resource, namely crypto-advisor-

app.netlify.app, are permitted. This is achieved by

specifying an origin header, which CORS can after-

ward validate. The psycopg2 adapter for database

connection is provided by the SQLAlchemy package,

and besides transporting credentials or other sensi-

tive information such as host or port number, it en-

sures that the queries are properly sanitized and do not

contain any kind of hidden compromising commands

that might affect our database (N

¨

ust and Ostermann,

2020). Both client-side and server-side resources are

accessible through https with TLS encryption [31],

with certificates issued by the PaaS provider. The

providers also offer active DDoS [32] monitoring,

which is another popular form of cyberattack.

7 CONCLUSION AND FUTURE

DEVELOPMENTS

The objective of this thesis was to assess the efficacy

of the cross-exchange arbitrage strategy and build a

web application with an underlying API that facili-

tates this approach. We can proudly say this was ac-

complished. We have developed a robust API that de-

livers precise data with low latency. Our API solution

is highly specialized in cross-exchange arbitrage for

centralized exchanges, making it rather distinctive in

terms of its capabilities. Obviously, there are other

APIs that provide similar data, but we were unable to

discover one that incorporates every aspect required

to perform an arbitrage trade, as our API does. We

hope to eventually expand our solution in the follow-

ing ways: Firstly, we would like to incorporate addi-

tional exchanges, especially decentralized ones, and

also more coins. We would also like to make our

system more efficient by utilizing graph networks and

cost-based pathfinding algorithms, such as Dijkstra’s

algorithm. As stated in the first section, we have only

considered one of the several arbitrage approaches;

therefore, we would like to develop solutions for ad-

ditional strategies in the future.

ACKNOWLEDGEMENTS

The publication of this paper was supported by the

2022 Development Fund of the Babes¸-Bolyai Univer-

sity (UBB).

The extended version of this paper and large ex-

planations were part of the bachelor thesis of Robert

Crypto Advisor: A Web Application for Spotting Cross-Exchange Cryptocurrency Arbitrage Opportunities

245

Oanta, study program Mathematics and Computer

Science, UBB.

REFERENCES

Abdelhamied, M. A. H. (2016). Client-side security using

cors.

Atzberger, D., Scordialo, N., Cech, T., Scheibel, W., Trapp,

M., and D

¨

ollner, J. (2022). Codecv: Mining expertise

of github users from coding activities. In 2022 IEEE

22nd International Working Conference on Source

Code Analysis and Manipulation (SCAM), pages 143–

147. IEEE.

Bansal, P. and Ouda, A. (2022). Study on integration of

fastapi and machine learning for continuous authenti-

cation of behavioral biometrics. In 2022 International

Symposium on Networks, Computers and Communi-

cations (ISNCC), pages 1–6. IEEE.

Bucher, P. P. and Christensen, C. J. (2019). Oauth 2.

Copeland, R. (2008). Essential sqlalchemy. ” O’Reilly Me-

dia, Inc.”.

Do This, W. W. Refactoring, design patterns and extreme

programming.

Fang, F., Ventre, C., Basios, M., Kanthan, L., Martinez-

Rego, D., Wu, F., and Li, L. (2022). Cryptocurrency

trading: a comprehensive survey. Financial Innova-

tion, 8(1):1–59.

Fraternali, P. (1999). Tools and approaches for developing

data-intensive web applications: a survey. ACM Com-

puting Surveys (CSUR), 31(3):227–263.

Hacker, S. and Hatemi-J, A. (2012). A bootstrap test for

causality with endogenous lag length choice: theory

and application in finance. Journal of Economic Stud-

ies, 39(2):144–160.

Hanchett, E. and Listwon, B. (2018). Vue. js in Action. Si-

mon and Schuster.

Jothi, K. and Oswalt Manoj, S. (2022). A comprehen-

sive survey on blockchain and cryptocurrency tech-

nologies: Approaches, challenges, and opportunities.

Blockchain, Artificial Intelligence, and the Internet of

Things: Possibilities and Opportunities, pages 1–22.

Kornienko, D., Mishina, S., and Melnikov, M. (2021). The

single page application architecture when developing

secure web services. In Journal of Physics: Confer-

ence Series, volume 2091, page 012065. IOP Publish-

ing.

Lacity, M. (2020). Crypto and blockchain fundamentals.

Ark. L. Rev., 73:363.

Lansky, J. (2018). Possible state approaches to cryptocur-

rencies. Journal of Systems integration, 9(1):19.

MAN, B. J. User interface for ddos mitigation configura-

tion.

Middleware, R. H. (2006). Hibernate: Relational persis-

tence for java and .net. Red Hat Middleware.

Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic

cash system. Decentralized business review, page

21260.

N

¨

ust, D. and Ostermann, F. (2020). Reproducibility review

of: Window operators for processing spatio-temporal

data streams on unmanned vehicles. Open Science

Framework, 10.

Pterneas, V. (2013). Getting Started with HTML5 Web-

Socket Programming. Packt Publishing.

Richardson, L. (2007). Beautiful soup documentation.

Sandhu, R. S. (1998). Role-based access control. In Ad-

vances in computers, volume 46, pages 237–286. El-

sevier.

Shynkevich, A. (2021). Bitcoin arbitrage. Finance Research

Letters, 40:101698.

Sriramya, P. and Karthika, R. (2015). Providing password

security by salted password hashing using bcrypt al-

gorithm. ARPN journal of engineering and applied

sciences, 10(13):5551–5556.

Zhu, J., He, P., Fu, Q., Zhang, H., Lyu, M. R., and Zhang,

D. (2015). Learning to log: Helping developers make

informed logging decisions. In 2015 IEEE/ACM 37th

IEEE International Conference on Software Engineer-

ing, volume 1, pages 415–425. IEEE.

CSEDU 2023 - 15th International Conference on Computer Supported Education

246