Stock Prediction Based on Principal Component Analysis Principal

Component Analysis and Long Term Short Term Memory

Wenxuan Liu

Baskin Engineering, University of California Santa Cruz, Santa Cruz, U.S.A.

Keywords: LSTM, Machine Learning, PCA, Data Prediction, Data Preprocessing.

Abstract: Nowadays, machine learning mode in financial markets has become popular. This experiment studied the

potential benefits of integrating Principal Component Analysis (PCA) with Long Short-Term Memory

(LSTM) neural networks for the prediction of stock prices. The data used in the experiment are collected from

Yahoo Finance, a reputable platform for collecting stock prices. Traditional methods for stock price prediction

by using LSTMs mostly just rely on the raw historical stock data. Raw data are high-dimensional and may

contain redundant information. The redundancy could reduce the model's predictive ability. The hypothesis

claims that the application of PCA can refine the data and enhance the predictive performance of LSTMs. To

prove the hypothesis, I employed three steps: Initially, I applied PCA on the historical stock data to pre-

process the principal components. In addition, use these components as inputs for the LSTM model. Lastly,

compare the performance of the PCA-integrated LSTM model with a traditional LSTM model that uses

unprocessed data. In the result, compared with the original stock data, the prediction accuracy of the LSTM

model trained using PCA-converted data has been significantly improved. The result not only can prove the

hypothesis but also underscores the advantages of combining dimensionality reduction techniques with the

LSTM method.

1 INTRODUCTION

1.1 Background

Financial markets have always been a research area

worthy of attention. Financial markets attract the

interest of academics, investors, and financial

analysts because of their potentially lucrative returns

and their significant impact on the global economy.

With the evolution of markets and the increased

complexity of financial instruments, the sheer volume

of data which is available for analysis has grown

exponentially.

1.2 Related Research

Dimensionality reduction techniques have been

applied in various fields to manage high-dimensional

data, among which PCA is a commonly used data-

processed method. PCA is a statistical technique that

can help to decrease data’s dimensionality. Due to the

help of employing an orthogonal transformation, the

original random vector can be transformed by PCA

(Gao et al 2021). Using PCA to preprocess data can

avoid clutter and allow the module to obtain results

with less data.

LSTM replaces the neurons in the hidden layer

of traditional neural networks with memory cells and

computing units. This LSTM can efficiently utilize

historical information in time series to achieve

reliable dynamic predictions (Liu 2021). Moreover,

LSTM can forget unnecessary information or store

information for a longer period with the support of

memory units (Srijiranon 2022). It has a forget gate,

an output gate, and an input gate. The Forget-Gate

helps judge whether the data from the previous unit

needs to be fed to the current unit or not, Also, it can

judge which data plays a role in information filtering

and control (Liu and Sun 2020). “The LSTM neural

network needs to determine which input information

needs to be forgotten and which does not need to be

forgotten through the 𝜎 function. The value range of

the σ layer output value is [0,1]. The closer to zero,

the more of the information is forgotten. Similarly,

closer to one, less information is forgotten. When

equal to 1, all information can be retained, and when

equal to 0, all information can be retained. The

information is discarded” (Gu and Wang 2022).

𝑓

= 𝜎(𝑤

×

ℎ

, 𝑥

+ 𝑏

(1)

392

Liu, W.

Stock Prediction Based on Principal Component Analysis Principal Component Analysis and Long Term Short Term Memory.

DOI: 10.5220/0012816500003885

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st International Conference on Data Analysis and Machine Learning (DAML 2023), pages 392-396

ISBN: 978-989-758-705-4

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

1.3 Objective

The primary objective of this study is to prove the

hypothesis that ‘using PCA to preprocess historical

stock data can improve the predictive performance of

LSTM neural networks. The goal is to find out

whether dimensionality reduction through PCA, can

effectively distill the data and provide more efficient

input to LSTM. By comparing the performance of

LSTM models trained on raw data versus PCA-

processed data, the hypothesis has been proved.

2 HYPOTHESIS

Compared to using raw stock data as inputs, using

PCA to reduce historical stock data’s dimensionality

will improve the predictive accuracy of LSTM neural

networks.

3 METHOD

3.1 Data Collection

This part is to get a dataset that collects the historical

stock prices and relevant metrics by using Python.

This part will extract historical stock data from Yahoo

Finance and Google Finance. Ensure that the data

includes opening prices, closing prices, and high, and

low, volume metrics. By providing different

indicators of stock behavior, the model has a broader

context and avoids overfitting. In addition,

incorporating multiple perspectives will allow

models to consider more details.

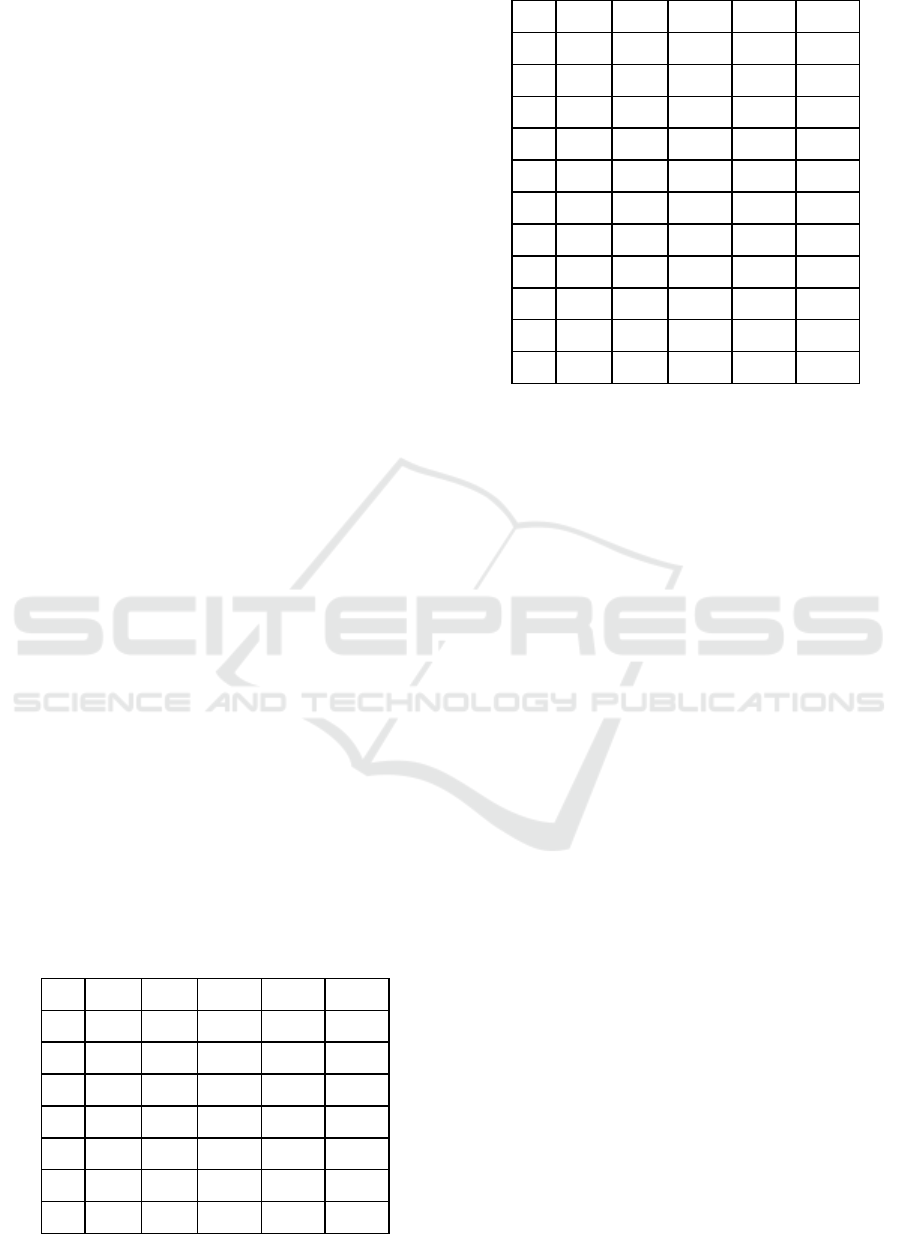

The following table 1 collects the stock opening

price, highest price, lowest price, closing price and

volume metrics of "Gold Dec23" from August 28th to

September 10th.

Table 1: Collected Stock Price Data.

Date Open High Low Close Volume

8.1 1948.4 1953.6 1933.2 1937.4 652

8.2 1934.2 1936.5 1928.00 1932.00 773

8/3 1934.9 1945.0 1920 1939.6 290

8/6 1941.0 1941.0 1929.8 1933.5 376

8/7 1931.7 1933.2 1923.0 1924.1 555

8/8 1925.4 1928.8 1913.7 1915.4 451

8/9 1921.1 1927.8 1911.4 1914.4 178

8/10 1913.0 1916.6 1911.8 1912.9 57

8/13 1909.3 1912.6 1903.3 1910.6 46

8/14 1906.0 1907.7 1895.0 1902.5 73

8/15 1904.5 1904.5 1890.3 1896.1 22

8/16 1893.7 1902.4 1884.0 1884.1 245

8/17 1891.8 1891.8 1886.1 1886.1 19

8/20 1893.6 1893.6 1893.3 1893.3 876

8/21 1894.6 1896.8 1892.8 1896.4 46

8/22 1909.6 1918.5 1909.6 1918.5 547

8/23 1920.0 1920.8 1918.2 1918.2 337

8/24 1919.8 1919.8 1911.1 1911.1 195

8/27 1915.5 1921.5 1915.5 1917.9 99

3.2 Data Pre-Processing

3.2.1 Data Cleaning

The datasets we've gathered may include various

inconsistent elements, such as missing values,

outliers, and erroneous entries. The inconsistencies

can impact the performance of the algorithms. It will

cause misleading or inaccurate experimental results

during the research. Accordingly, it is very important

to do data processing after data collection to improve

the reliability of the data. One way to process the

missing data is to remove the affected data.

Alternatively, interpolation methods can be employed

to estimate and fill in the absent values, to ensure the

dataset remains comprehensive.

3.2.2 Data Transformation

Stock prices can be significantly variable between

different periods and different stocks. Normalizing

the data can be beneficial in making sure that the

values fall within the range of 0 to 1, so that the

variables are in a common scale without distorting

differences in the range of values. This facilitates

efficient training of LSTM networks and ensures

stable convergence.

3.3 Data Analysis

3.3.1 PCA

PCA is a tool that helps to reduce the dataset’s

dimensionality, which can help in decreasing the

number of dimensions in the data. It can summarize

the information content in large data sets to achieve

the goal of reducing dimensionality.

Stock Prediction Based on Principal Component Analysis Principal Component Analysis and Long Term Short Term Memory

393

PCA is an important step when starting data

analysis by solving “high-dimensionality” problems

in financial datasets. Stock data includes multiple

variables, such as opening price, closing price,

volume, and various technical indicators. Managing

all these dimensions without losing the integrity of

the data can be a great challenge. PCA can simplify

the complexity of high-dimensional datasets by

creating new variables, which are named “principal

components” (Wen et al 2020). The principal

components are the original variables’ linear

combinations. Also, they are uncorrelated with each

of the variables. Therefore, each of the principal

components is able to get unique information from

data without overlapping with the others. After this,

we can obtain a good representation of the original

data by considering fewer principal components. By

reducing dimensions, PCA makes data visualization

easier and more efficient. These linear combinations,

principle components, can be used to summarize

datasets and do not need to lose large amounts of

information. PCA also analyzes relationships

between variables by calculating a correlation matrix

for the entire data set (Kim et al 2021).

In addition, PCA is a good method to reduce the

noise and reduce the risk of overfitting when training

the data-predicted model. The variables from the

original stock market have a large amount of noise. If

the noises are not managed, the predictive ability of

the model will be distorted. When PCA is used to

preprocess the data, typically only the first few

principal components are retained. By discarding the

components associated with the smallest eigenvalues,

PCA effectively filters out some noise from the data.

3.3.2 LSTM

LSTM is a deep-learning network. It allows

information to persist. Also, LSTM is a variant of

RNNs. The primary aim of LSTM is to capture the

interrelationships among extracted features in order

to make accurate predictions (Zhang et al 2021).

The LSTM unit includes by a Storage-Gate unit,

an Input gate, a Forgetting gate, and an Output gate. In

the LSTM's process, some errors are passed directly to

the subsequent layer via the input gate, while others are

discarded through the forget gate. This mechanism

allows LSTM to address the issues of exploding and

vanishing gradients (Zheng and Xiong 2022). Also, it

allows LSTM networks to learn and judge the

information that needs to be stored, utilized, or

discarded. During this step, the LSTM unit’s

Forgetting Gate decides the amount of information to

forget based. The decision was made by the sigmoid-

activation function. Then Creates new feature data as

candidate values (Zhang et al 2021).

Stock prices exhibit sequential dependence,

which means that the future price of a stock will be

affected by a series of past prices. The memory unit

of the LSTM model enables it to learn and remember

patterns over time which helps it manage the

dependencies. The architecture of LSTM networks

allows LSTM networks to learn and judge the

information that needs to be stored, utilized, or

discarded.

4 DATA

In the research, I compared the stock price prediction

results obtained by using the PCA method with the

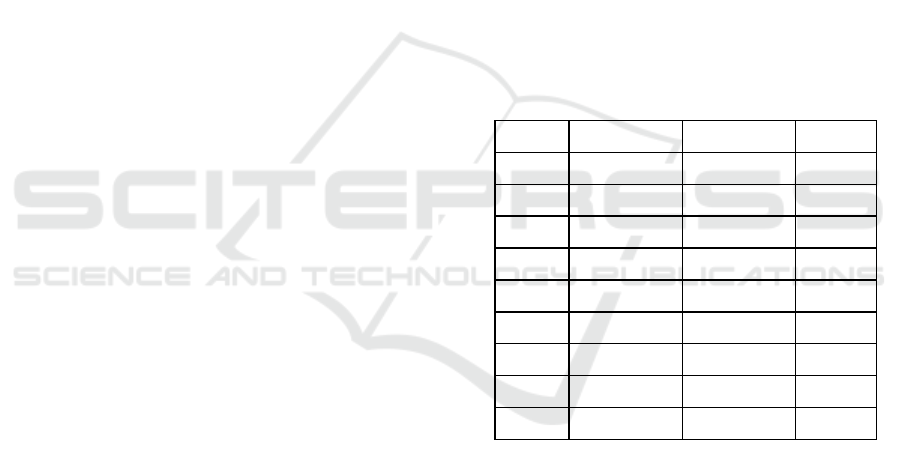

results that did not use PCA. The following table 2

collects the actual closing prices of stocks and the

closing prices of stocks predicted using the model for

"Gold Dec23" from August 28th to September 10th.

Table 2: Predicted Price.

Date With PCA Not with PCA Real price

8/28 1897.4 1906.1 1936

8/29 1910.0 1907.4 1944

8/30 1914.3 1918.1 1938.2

8/31 1921.8 1919.0 1939.8

9/4 1921.6 1935.8 1926.2

9/5 1920.9 1925.3 1918.1

9/6 1924.9 1930.6 1917.5

9/7 1927.9 1932.9 1918.4

9/10 1931.3 1928.5 1923.3

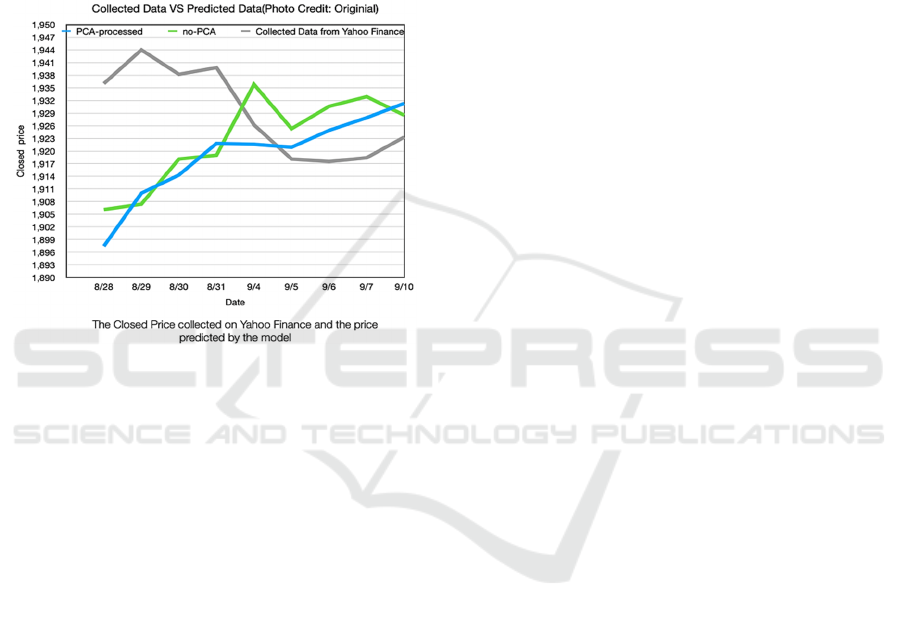

The picture below is the image obtained from

experimental data. The time period of the data is

between August 28th and September 10th. The gray

line represents the actual daily stock price data. It's

clear that the trend of the gray line changes from

continuously changing up and down to a sharp

decline and then to a slow rise. The green line is the

price predicted by the model without using PCA to

preprocess the data. The blue line is the price

predicted by the model using the PCA model to

preprocess the data.

After September 4th, the predicted values

obtained using the two methods (whether using PCA

or not) are relatively close to the actual stock price.

This shows that whether the PCA method is used or

DAML 2023 - International Conference on Data Analysis and Machine Learning

394

not, the ability of the basic model to capture key stock

price drivers is relatively good.

On most dates, the difference between the data

obtained using the PCA method and the data obtained

without using the PCA method is not very large.

However, as can be seen from the icon below, most of

the time the data obtained using the PCA method has a

smaller gap with the real price. Moreover, the data

graph using the PCA method is smoother.

The price error before 9/4 was very obvious. This

reflects that the performance of the model is not stable.

Figure 1: Collected Data, Predicted Data (PCA processed

and non-processed) (Photo credit: Original).

5 DISCUSSION

The performance of the stock price predictive model

is very easy to be influenced by many different factors,

especially under the economic background. The

analysis of stock prices is very complex and difficult.

That’s because the stock price can be affected by

many different factors, such as new policies, the news,

and new technologies.

According to the experimental results, it can be

proved that the model’s performance after using the

PCA method is indeed better but not obvious. The

performance of both models is unstable. For example,

in the experiment, the error in the prediction data

before 9/4 is obvious and difficult to ignore. The

difference is that the data after 9/4 has a smaller error.

Also, the changing trend (up and down) of the PCA-

processed graph is closer to the graph of the collected

data.

After analysis, I sorted out the following factors

that may cause errors:

1) Insufficient data used for training results in the

model's judgment ability being insufficient to deal

with noises.

2) The stock price of gold fluctuates greatly,

making it difficult to predict accurately.

3) No analysis of the impact of external factors on

stock prices.

The period of the data collection and the diversity,

and sufficient quantity of the data are very important

for the stock price prediction experiment. A dataset

with a limited amount of data may not have enough

ability to capture all possible anomalies and patterns

in stock price trends. That will make the module

cannot predict the trends correctly even if its

performance is excellent. In addition, financial data is

always full of noise, it can be influenced by many

variable factors. Without enough data, the model

might not exclude the noise. This will lead to the

appearance of overfitting and reduce the accuracy.

The price of gold is constantly fluctuating rather

than stable. Gold is a precious metal that has intrinsic

value. The stock price of it can be influenced by

various global events. Effects may be sudden.

Reduced appeal to investors, the Federal Reserve, war,

inflation, and banks around the world continue to

purchase gold on a large scale, all of which are the

factors that can sufficiently affect the price of gold.

For example, if conflict or war breaks out in gold-

producing areas, the facilities that mine gold may be

damaged. And maybe because of the war, the miners

who dig up gold will not go to work. This will lead to

a shortage of gold supply, thereby pushing up gold

prices. The impact of the war on gold prices was

sudden and significant. These unexpected impacts

can make forecasting gold prices a difficult challenge.

Insufficient data in the database used for training

is a very common problem in artificial intelligence.

The same problem also exists in AI applications in

dermatology. Dr. Roxana Daneshjou and her research

team tested the dermatological diagnosis

performance of “ModelDerm”, “DeepDerm” and

“HAM10000” in the study. After research, it was

found that these three artificial intelligences all have

insufficient information about dark-skinned patients,

which leads to a significant decline in their

performance in diagnosing dark-skinned patients

(Daneshjou et al 2022). This is an urgent challenge

that artificial intelligence needs to overcome.

To make the model perform better and make more

accurate stock price judgments, more data sets need to

be used when training the model. and to include the

influence of external factors in the analysis (Hu 2022).

First of all, the most important step to optimize the

module is to obtain more historical stock price data

Stock Prediction Based on Principal Component Analysis Principal Component Analysis and Long Term Short Term Memory

395

with a longer period in Yahoo Finance. This can fix the

problem of the lack of data used to train the model.

Furthermore, macroeconomic data including GDP,

unemployment rate, inflation rate, etc. can be added to

the database to help analyze stock prices. Adding these

factors that affect stock prices makes it easier and more

accurate for the module to predict stock prices.

Moreover, since news and social media data also

affect the predictive power of the model, they should

also be added to the database as data for analysis (Li et

al 2014). Using natural language processing (NLP)

technology can help extract company or market-related

information from news articles or social media posts

(Ding 2015). Next, by preprocessing these data, the

accuracy of the model can be improved.

6 CONCLUSION

In the study, I compared the stock price predictions

obtained using the PCA method with the stock price

predictions obtained without using the PCA method.

In the experiment, the LSTM model was trained on

20 data sets containing the opening price, high price,

low-price, closing price, and the volume of the stock

"Gold Dec23". After experimental research, it was

found that the model using the PCA method has fewer

errors than the model without the PCA method.

However, the performance of both models is unstable,

and the output results may be accompanied by large

errors. These issues may be caused by insufficient

data in the database used to train the model. Moreover,

the large price fluctuations of "Gold Dec23" and other

external factors such as policies and government

controls will make the stock price difficult to infer.

To make the accuracy of the production more stable

and excellent, the database used to train the model

should have more data for training the model. When

making stock predictions, factors that may affect

stock prices should be analyzed to optimize the model.

This research can provide a reference for

improving the performance of the neural network

LSTM. After experimental analysis, using the PCA

method to preprocess the data can indeed slightly

improve the data analysis and prediction performance

of the neural network LSTM. It is helpful to help

people who need to use LSTM for data analysis (not

just stock analysis) to analyze data and make the

results more accurate.

The database of this study is not large enough,

and the experiment needs to be improved by adding

more databases. In future research, more influencing

factors and reference data will be added to improve

the experiment.

REFERENCES

Y. Wen, P. Lin, and X. Nie, “Research of stock price

prediction based on PCA-LSTM model,” in IOP

Conference Series: Materials Science and

Engineering, vol. 790, no. 1, Mar. 2020, p. 012109.

X. Zheng and N. Xiong, “Stock price prediction based on

PCA-LSTM model,” in Proc. 2022 5th Int. Conf.

Mathematics and Statistics, Jun. 2022, pp. 79–83.

Y. Gao, R. Wang, and E. Zhou, “Stock prediction based on

optimized LSTM and GRU models,” Scientific

Programming, vol. 2021, pp. 1-8, 2021.

H. Liu, “A research on stock forecasting based on principal

component LSTM model,” in Proc. 2021 IEEE Int.

Conf. Advances in Electrical Engineering and

Computer Applications (AEECA), Aug. 2021, pp.

684–688.

K. Srijiranon, Y. Lertratanakham, and T. Tanantong, “A

hybrid framework using PCA, EMD and LSTM

methods for stock market price prediction with

sentiment analysis,” Applied Sciences, vol. 12, no. 21,

p. 10823, 2022.

J. Liu and D. Sun, “Stock price prediction based on principal

component analysis and long short-term memory

network,” Advances in Applied Mathematics, vol. 9, p.

1954, 2020.

W. Hu, “Stock price prediction based on IndRNN-LSTM

model,” Advances in Applied Mathematics, vol. 11, p.

209, 2022.

L. Gu and X. Wang, “Research on stock price prediction

based on LSTM model: A case study of Poly

Development,” Advances in Social Sciences, vol. 11,

p. 4517, 2022.

G. B. Kim, C. I. Hwang, and M. R. Choi, “PCA-based

multivariate LSTM model for predicting natural

groundwater level variations in a time-series record

affected by anthropogenic factors,” Environmental

Earth Sciences, vol. 80, p. 1-21, 2021.

X. Zhang, X. Lu, W. Li, and S. Wang, “Prediction of the

remaining useful life of cutting tool using the Hurst

exponent and CNN-LSTM,” The Int. Journal of

Advanced Manufacturing Technology, vol. 112, pp.

2277-2299, 2021.

R. Daneshjou, K. Vodrahalli, R. A. Novoa, M. Jenkins, W.

Liang, V. Rotemberg, A. S. Chiou, "Disparities in

dermatology AI performance on a diverse, curated

clinical image set," Science Advances, vol. 8, no. 31,

pp. eabq6147, 2022.

X. Li, H. Xie, L. Chen, J. Wang, and X. Deng, "News impact

on stock price return via sentiment analysis,"

Knowledge-Based Systems, vol. 69, pp. 14-23, 2014.

X. Ding, Y. Zhang, T. Liu, and J. Duan, "Deep learning for

event-driven stock prediction," in Twenty-fourth

International Joint Conference on Artificial

Intelligence, June 2015.

DAML 2023 - International Conference on Data Analysis and Machine Learning

396