Research on Credit Card Default Prediction for Class-Imbalanced

Datasets Based on Machine Learning

Jinyang Liu

School of Physical and Mathematical Sciences, Nanyang Technological University Singapore, 637371, Singapore

Keywords: Credit Card Default, Machine Learning, Class Imbalance Correction, Credit Risk, Classification Model.

Abstract: It’s known that a robust credit relationship is advantageous for both parties involved. However, credit defaults

significantly amplify risk for financial institutions. Hence, default rate prediction stands as a crucial objective

for lending institutions and a well-functioning predictive model serves as a potent means to strengthen risk

control. To this end, this paper constructed multiple machine learning classification models to achieve credit

card default prediction. Feature selection, based on the importance of variables in the random forest, was

implemented to enhance the model performance. The results shown that, addressing the skewed nature of

credit default data, various SMOTE-based resampling methods were employed to improve data distribution

and further optimize accuracy. Compared to other models, the random forest model demonstrated superior

predictive effectiveness. After correcting the data distribution, there was a significant enhancement in the

predictive performance of all models, with K-Means SMOTE showcasing outstanding performance in data

correction and model accuracy optimization.

1 INTRODUCTION

As a convenient payment tool, credit cards have

prospered steadily, becoming a pillar business for

financial institutions and stoking the engine of

consumption. However, this trend has also increased

the challenges of risk management, as the probability

of defaults expand, exposing banks to significant risk.

According to a report from Wells Fargo, credit card

delinquency rates are surging among commercial

banks in 2023, with rates at smaller lenders even

approaching 8%. This trend may foreshadow a future

economic recession. Therefore, a well-performing

default prediction model has become a vital focus of

financial institutions. An accurate model can help

institutions balance economic risks and returns, avoid

overdue and bad debt, and ensure sustainable profits.

A large body of studies have shown great interest

in credit card default prediction. Traditional credit

risk measurement methods include discriminant

analysis and logistic regression based on statistical

principle (Yin et al 2013). In the past few years,

researchers have gained fresh insights due to the

significant potential offered by machine learning

algorithms. Different models, including those

founded on Logistic Regression, Decision Tree, and

Random Forest, were detailed by Butare et al (Leo et

al 2019). Through extensive and in-depth research,

Zhou et al. introduced a predictive model designed for

analyzing issues related to default (Butaru et al 2016).

The empirical results show that decision tree is a fast

and robust model to process high-dimension data with

strong evaluation ability and high accuracy. In the

study by Chen et al., the classification model

combining k-means and BP neural network

algorithms is formulated to training data and make

prediction (Zhou et al 2019). Zeng et al. applied

decision tree and random algorithms to establish

credit card warning model respectively and

concluded that the performance of random forest

model is better (Chen and Zhang 2021). There is also

a lot of research focused on exploring the strength of

ensemble learning (Zeng et al 2020 & Kim et al 2019).

Through a comparative analysis based on overdue

customer payment data, Hamori suggested that

boosting algorithms such as Random Forest,

Boosting, and Neural Network outperform other

conventional techniques (Ileberi, Sun and Wang

2021). Similarly, based on the analysis of financial

data from small Chinese institutions, Zhu et al.

considered that ensemble classifiers, which fully

utilized the knowledge learned by multiple single

Liu, J.

Research on Credit Card Default Prediction for Class-Imbalanced Datasets Based on Machine Learning.

DOI: 10.5220/0012818100004547

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st International Conference on Data Science and Engineering (ICDSE 2024), pages 441-447

ISBN: 978-989-758-690-3

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

441

classifiers, can effectively improve prediction

accuracy (Hamori et al 2018).

However, a suitable model not only relies on

advanced algorithms, but is also affected by the

quality and distribution of the data. In the real world,

bad credit customers make up only a small proportion

of creditworthy customers. It has been shown that

class-imbalanced data leads to deterioration in model

performance (Zhu et al 2019). Therefore, effective

data processing and feature selection techniques are

necessary for skewed class scenarios (Abedin et al

2023). A large body of literature has addressed this

problem. In skewed class classification, the most

classical method is random resampling. However,

random under-sampling has the potential to lose

critical information about decision boundaries, while

simple replication during random oversampling

increases the likelihood of overfitting, both of which

can affect the results of classification models (Alam

et al 2020). More sophisticated heuristic approaches

have been developed. A renowned technique

proposed by Chawla et al., known as Synthetic

Minority Over-sampling Technique (SMOTE), has

found extensive applications across various domains

(Chawla et al 2002). It generates new and reasonable

samples for minority class based on the KNN

algorithm. On this basis, Chen et al. proposed an

improved algorithm that combines the SMOTE

technique with the KNN algorithm -- K-Means

SMOTE. Validation results demonstrate that this

technique significantly enhances the predictive

performance of the model (Chen and Zhang 2021). In

addition, the borderline-SMOTE, which takes full

account of the distributional characteristics of the

samples, overcomes the limitations of boundary value

processing and achieves the identification of noise

and boundary samples (Han et al 2005).

Therefore, this study aims to construct multiple

classification models and explore their application

feasibility. Predictive models base on massive data

and different artificial intelligence algorithms help

decision-makers develop adaptive strategies to

mitigate the adverse socio-economic impact of

defaults. In addition, given the class-imbalanced

nature of default data, various correction techniques

are evaluated, so as to explore valid and effective

processing methods to achieve further optimization of

model prediction performance.

2 METHODOLOGY

2.1 Data Source

The dataset for the study is sourced from the

Machine Learning Repositor of University of

California, Irvine (UCI).

2.2 Data Explanation and Preliminary

Analysis

The dataset contains 24 columns and 30,000 rows,

of which about one-fifth of the samples are in the

default category and the rest are in the non-default

category. Table 1 demonstrates all the features of

the dataset.

The default customer profile can be initially

analysed by observing the data distribution of several

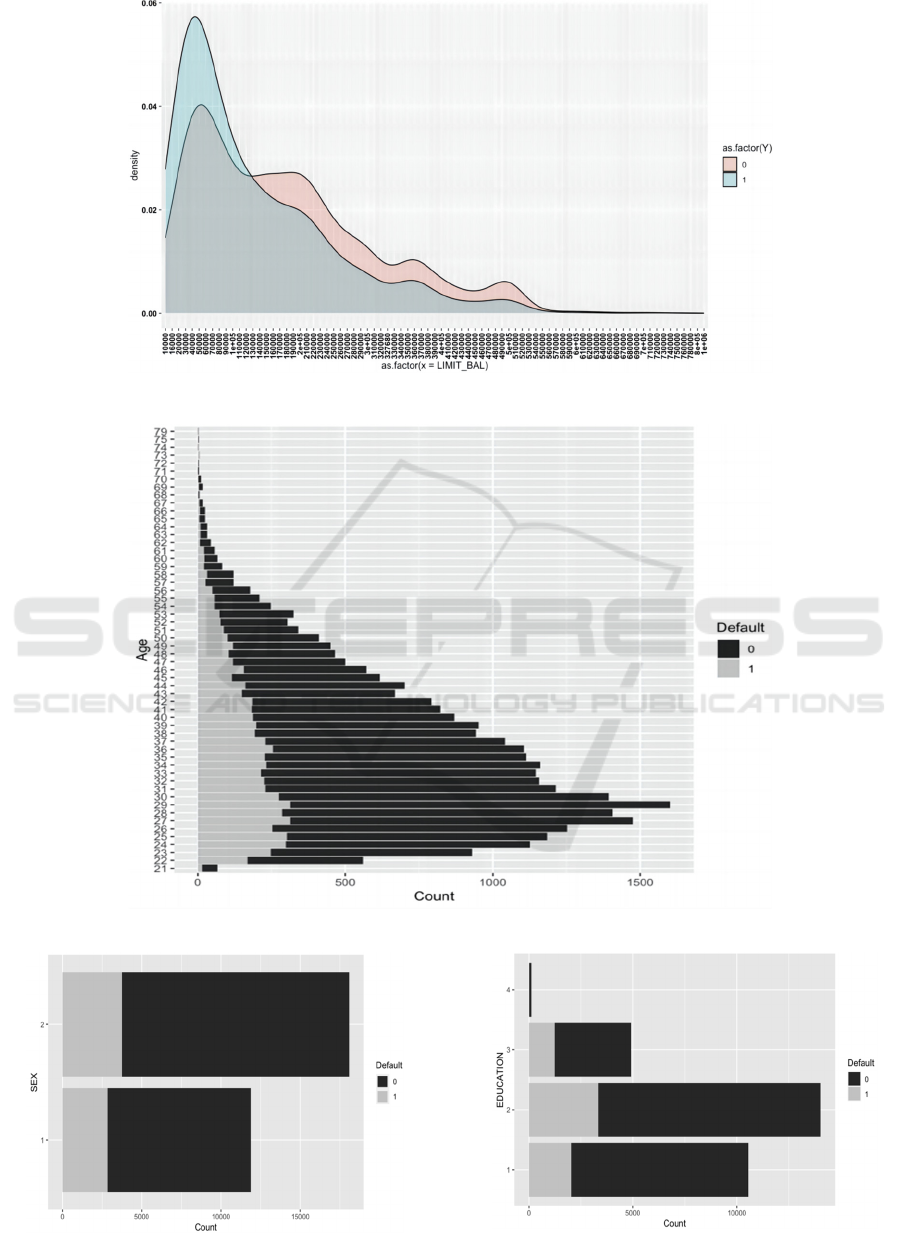

key attributes. As shown in Figure 1, the majority of

customers in arrears had relatively low limit balances,

ranging from 20,000 to 50,000. As seen in Figure 2,

20–40-year-olds were the largest proportion of

individuals in arrears in the dataset. Figures 3, 4 and

5 depict the gender, marital and educational status of

clients. While there were slightly more females than

males in the sample, females had slightly lower

delinquency rates than males, while single

individuals had slightly lower delinquency rates than

married individuals. Credit card delinquency rates

tended to decrease as educational attainment

increased.

Table 1: Variable Attributes.

Number Variable Explanation

1 Limit_bal Credit amount (NT$)

2 Sex 1 = male, 2 = female

3 Age Years of age

4 Education 1= graduate school, 2 = university, 3 = high school, 4 = unknow

5 Marrige 1 = married, 2 = single, 3 = others

6 —11 pay_1 -- pay_6 Monthly disbursements April to September 2005

12 —17 bill_amt1 --bill_amt6 Amounts billed from April to September 2005

18 —23 pay_amt1 — pay_amt6 Prior Period Payment Amount from April to September 2005 (NT$)

24 Default.payment.next.month A binary variable, as the response variable. Yes = 1, No = 0

ICDSE 2024 - International Conference on Data Science and Engineering

442

Figure 1: Density diagram of LIMIT_BAL (Picture credit: Original).

Figure 2: Density diagram of AGE (Picture credit: Original).

Figure 3: Bar chart of SEX (Picture credit: Original).

Figure 4: Bar chart of Education (Picture credit: Original).

Research on Credit Card Default Prediction for Class-Imbalanced Datasets Based on Machine Learning

443

Figure 5: Bar chart of Marriage (Picture credit: Original).

2.3 Modelling Techniques

2.3.1 Logistic Regression

The Logistic Regression is a linear model that maps

the linear combination of features into the logistic

function, transforming the real values into a range

between 0 and 1, representing the probability of

belonging to a particular class.

2.3.2 K-Nearest Neighbors

The K-Nearest Neighbors algorithm (KNN) is a non-

parametric supervised learning method widely

applied in pattern recognition and classification tasks.

Based on the principles of the algorithm, the category

of an object is not solely determined by the majority

vote of its neighbors but also involves considerations

of distance weights for each neighbor. This approach

excels in leveraging the local structural information

among samples, proving effective across a diverse

range of data types.

2.3.3 Decision Tree

A decision tree is a tree model that makes predictions

by splitting data into subsets based on features. The

goal is to select the best features to split at each node

with the aim of maximising information gain (for

classification) or minimising variance (for

regression). It can model complex non-linear data

relationships and also handle numerical and

categorical features.

2.3.4 Random Forest

Random forest is an integrated learning method, a

special form of Bagging, that makes predictions

based on a collection of decision trees. In constructing

each decision tree, random forest employs bootstrap

and random feature selection to increase the diversity

of the model. In this study, the final prediction was

obtained by majority voting.

2.4 Class Imbalance Correction

Techniques

Class imbalance creates significant challenges to the

results of most classification algorithms. This

emanates from the inherent constraint imposed on the

model's learning and analytical capabilities due to

uneven data distribution. Hence, three resampling

techniques were employed to investigate their

efficacy in handling skewed data and assess the extent

to which they could optimise model performance.

Synthetic minority oversampling technique

(SMOTE), is based on the KNN algorithm, which

measures the characteristics of the Kth nearest

neighbour of a particular sample and calculates the

characteristics to create a new sample based on the

degree of difference (Chawla et al 2002). Borderline-

SMOTE is an improved extension of the original

SMOTE algorithm, whose goal is to improve the

performance of the classifier by identifying samples

located at the border to generate new synthetic

samples (Han et al 2005). K-Means SMOTE is a

combination of K-Means clustering and SMOTE,

which clusters the sample data and filter clusters with

more minority categories for SMOTE oversampling

(Chen and Zhang 2021). This algorithm can reduce

the imbalance both between and within categories.

3 RESULTS AND DISCUSSION

3.1 Initial Model Prediction

Following fundamental steps of data preprocessing

and normalization, multiple classification models are

constructed base on Five-Fold Cross-Validation. The

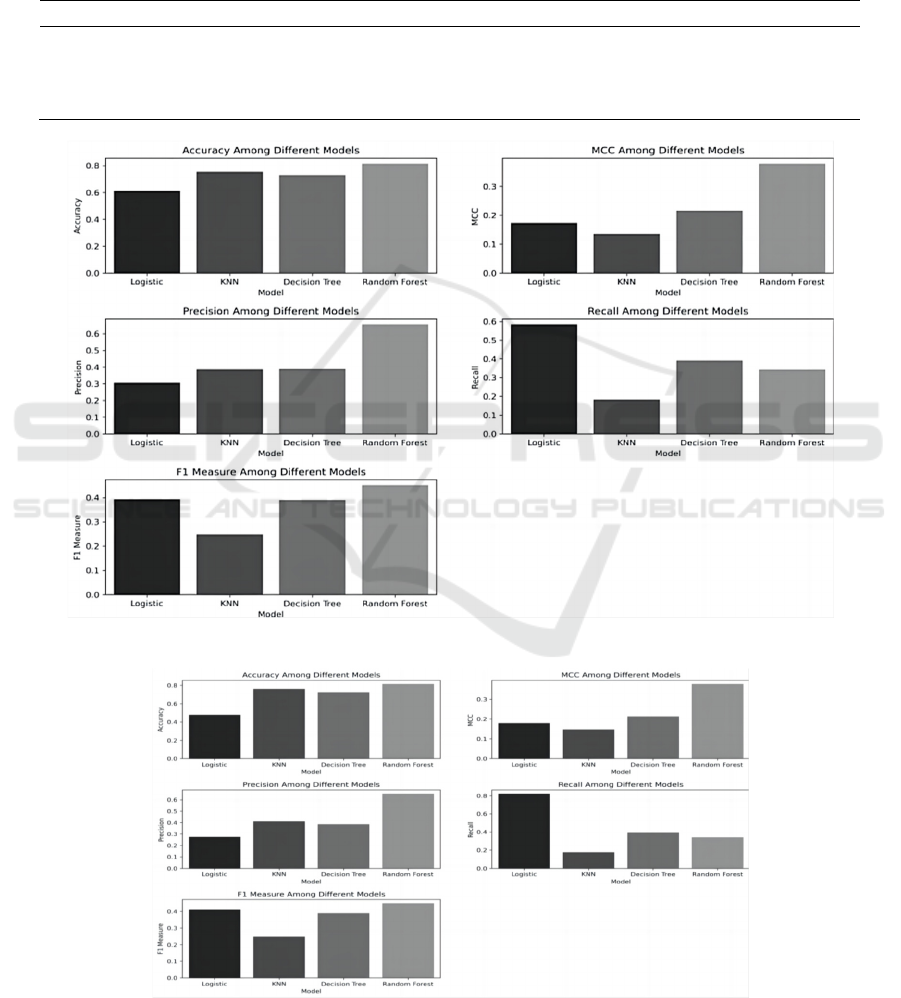

results of the model evaluation are shown in Table 2.

It can be observed from Figure 6 that among the

four models, the performance of the Random Forest

is relatively superior, with most evaluation metric

values distinctly surpassing those of the other models.

However, it is noteworthy that, despite the accuracy

of all four models not being excessively low—except

for Logistic Regression, where the accuracy of the

other three models exceeds 70%—the metrics such as

MCC, Precision, Recall, and F1 score are relatively

low, mostly falling below 0.5. This indicates a

diminished predictive capability of the models for

classifying the minority class in this scenario.

ICDSE 2024 - International Conference on Data Science and Engineering

444

3.2 Model Prediction After Feature

Engineering

Feature engineering constitutes an effective

technique aimed at diminishing model complexity

and alleviating noise interference. In this study,

feature selection relies on the variable importance

calculated by random forest model, using the Gini

coefficient as a metric to gauge the contribution of

each feature. As shown in Table 3 and Figure 7, there

is no substantial improvement in various metrics,

with only marginal fluctuations.

Table 2: Comparison results of four models.

Model Accuracy MCC Precision Recall F1 score

Lo

g

istic 0.611 0.174 0.306 0.584 0.393

KNN 0.755 0.135 0.386 0.182 0.247

Decision Tree 0.729 0.216 0.388 0.391 0.390

Random Forest 0.815 0.379 0.655 0.343 0.450

Figure 6: Comparative evaluation of models (Picture credit: Original).

Figure 7: Comparative evaluation after feature engineering (Picture credit: Original).

Research on Credit Card Default Prediction for Class-Imbalanced Datasets Based on Machine Learning

445

Table 3: Model comparison after feature engineering.

Model Accurac

y

MCC Precision Recall F1 Score

Logistic 0.479 0.179 0.274 0.822 0.411

KNN 0.762 0.148 0.410 0.177 0.247

Decision Tree 0.726 0.213 0.385 0.394 0.389

Random Forest 0.814 0.377 0.654 0.342 0.449

Table 4: Model comparison after oversampling.

Oversampling

Methods

Performance Measure Logistic KNN Decision Tree Random Forest

SMOTE

Accurac

y

0.601 0.746 0.814 0.884

MCC 0.211 0.509 0.628 0.771

Precision 0.637 0.696 0.806 0.922

Recall 0.473 0.873 0.827 0.839

F1 score 0.535 0.535 0.816 0.879

Borderline-SMOTE

Accurac

y

0.588 0.755 0.813 0.882

MCC 0.185 0.528 0.626 0.768

Precision 0.627 0.702 0.806 0.920

Recall 0.437 0.887 0.823 0.838

F1 score 0.511 0.783 0.815 0.877

KMeans-SMOTE

Accurac

y

0.722 0.810 0.820 0.886

MCC 0.450 0.624 0.640 0.775

Precision 0.718 0.782 0.813 0.922

Recall 0.737 0.861 0.832 0.844

F1 score 0.725 0.819 0.822 0.881

3.3 Model Prediction after Handling

Class Imbalance

Table 4 below illustrates the updated performance

metrics of all models after applying three resampling

techniques to address the class imbalance problem.

As shown in the table, there is no significant change

in the accuracy rates. This is primarily attributed to

the skewed distribution of the majority class in the

imbalanced data, which tends to keep the accuracy

consistently at a high level. However, it is evident that,

after correcting the data distribution, we have

successfully narrowed fown the errors of the mosels

across different classes, enabling them to accurately

capture complex patterns present in the real world.

This process has brought substantial benefits to the

performance enhancement of the models, especially

the Precision, Recall, and F1 scores of the Decision

Tree and Random Forest models exceeded 0.8, which

were even less than 0.4 before the class correction.

This suggests a substantial enhancement in the

predictive accuracy of the models for the minority

class, laying a solid groundwork for further practical

applications.

Among the three correction techniques,

K-Means

SMOTE

exhibits the most favorable performance,

achieving a greater degree of optimization in model

predictive performance while addressing data

distribution imbalances.

3.4 Discussion

Before addressing the class imbalance problem,

although the prediction accuracies of all four models

exceed 60%, the models' prediction performance for

minority class (defaulting customers) in skewed

categorization is not satisfactory. The main reason is

that it is misleading to focus solely on the precision

rate in the case of a severe imbalance of positive and

negative category samples. It is necessary to establish

comprehensive "unbiased" evaluation metrics, such

as Precision, Recall, and MCC (Matthews correlation

coefficient), to avoid the partiality of a single metric

and enhance a holistic understanding of model

performance (Boughorbel et al 2017).

After correcting the data distribution using the

resampling technique, the model’s performance

significantly improved, especially the prediction

accuracy for the minority class. Among the three

methods, KMeans-SMOTE had a more positive

impact on the model’s performance, possibly because

KMeans-SMOTE is better at generating synthetic

samples with intrinsic distributional characteristics

after clustering (Chen and Zhang 2021).

Among all classification models, the superiority

of random forest has been thoroughly validated. The

ensemble algorithm combines ideas by aggregating

multiple weak classifiers and introduces randomness

to prevent the model from overly relying on specific

ICDSE 2024 - International Conference on Data Science and Engineering

446

data, thereby improving its generalization

performance when faced with real-world complex

data. However, a number of studies have shown that

determining a universally effective model that

performs well across a majority of institutions is

challenging due to variability in customer

information and credit metrics (Butaru et al 2016).

Therefore, the final model selection and data

processing should depend on the dataset

characteristics, sample distribution, and performance

requirements. In future research, it is recommended

to explore various variants of traditional algorithms

for further enhancement. Simultaneously, expanding

the scope of the study by including a broader range of

economic indicators and user behavioural metrics

into the training data, it is more likely to establish a

model that integrates multiple perspectives,

thoroughly considers data diversity.

4 CONCLUSION

In summary, based on machine learning principles,

this study constructed classification models including

logistic regression, KNN, decision trees and random

forests for predicting credit card default. This study

also compared various SMOTE-based resampling

techniques to correct the data distribution and

evaluate their impact on improving the performance

of predictive models. From the results, the model

based on the random forest algorithm had higher

generalisability and prediction accuracy. The

research also indicates that dealing with class

imbalance data can significantly enhance the

prediction accuracy for minority categories while

maintain robustness for majority groups. Therefore,

the key to building effective default prediction

models lies in the use of sound and superior

algorithms combined with efficient data processing

methods. Future explorations can further delve into

more advanced algorithms and techniques to uncover

more robust results. This will help financial

institutions construct a comprehensive credit risk

prediction and credit assessment system to lower

financial risk. With the continuous strengthening of

financial regulations, default prediction is poised to

become a vital tool in risk management, offering

financial institutions judgment criteria and decision

support, thereby fostering the stable operation and

healthy development of financial markets.

REFERENCES

L. Yin, Y. Ge, K. Xiao, X. Wang, X. Quan,

Neurocomputing, 105, 3-11 (2013).

M. Leo, S. Sharma, K. Maddulety, Risks, 7(1), 29 (2019).

F. Butaru, Q. Chen, B. Clark, et al.,J. Banking & Finance,

72, 218-239 (2016).

J. Zhou, W. Li, J. Wang, S. Ding, C. Xia, Physica A: Stat.

Mech. Appli., 534, 122370 (2019).

Y. Chen, R. Zhang, Complex, 1-13 (2021).

X. Zeng, L. Lu, X. Lu et al. Wireless Internet Tech., 17(18),

166-168 (2020).

E. Kim, J. Lee, H. Shin, et al., Expert Syst Appl, 128, 214-

224 (2019).

E. Ileberi, Y. Sun, Z. Wang, IEEE, 9, 16528-165294 (2021).

S. Hamori, M. Kawai, T. Kume, Y. Murakami, C.

Watanabe, J. Risk Finan. Manage., 11(1), 12 (2018).

Y. Zhu, L. Zhou, C. Xie, G.J Wang, T.V. Nguyen, Int J Prod

Econ, 211, 22-33 (2019).

M. Z. Abedin, C. Guotai, P. Hajek, T. Zhang, Comp. Intel.

Sys., 9(4), 3559-3579 (2023).

T.M. Alam, K. Shaukat, I.A. Hameed, et al., IEEE, 8,

(2020).

N. Chawla, K. Bowyer, L. Hall, J. Arti. Intel. Res., 16, 321-

357 (2002).

H. Han, W. Y. Wang, B. H. Mao, Inter. Conf. Intel. Comp.,

Berlin, Heidelberg: Springer Berlin Heidelberg, (2005).

S. Boughorbel, F. Jarray, M. El-Anbari, PloS one, 12(6),

(2017).

Research on Credit Card Default Prediction for Class-Imbalanced Datasets Based on Machine Learning

447