Research on Microsoft Stock Prediction Based on Machine Learning

Methods

Shengyang Xu

University College London, London, WC1H 9EN, U.K.

Keywords: Stock Prediction, Machine Learning, Data Analysis

Abstract: This research delves into the dynamic realm of forecasting Microsoft stock trends, utilizing a dataset spanning

from November 2019 to 2023, accessible via Kaggle. The data undergoes meticulous preprocessing, including

temporal filtering and weekly resampling, to ensure relevance and consistency. Key features – 'Open,' 'High,'

'Low,' and 'Volume' – identified as pivotal in prior studies, form the basis for constructing training and testing

datasets. Our methodology integrates diverse machine learning models, namely k-Nearest Neighbors (k-NN),

Random Forest, and Support Vector Regression (SVR). The k-NN model captures local patterns, leveraging

proximity within the data. Random Forest, known for robustness, interprets high-dimensional financial data

through an ensemble of decision trees. SVR, designed for nonlinearity, addresses intricate relationships within

the stock dataset. Training and evaluation on distinct datasets reveal nuanced performances. While k-NN

encounters challenges, Random Forest emerges as a robust choice, excelling in capturing diverse features.

SVR, despite its nonlinear focus, faces limitations in the specific dynamics of stock data. This study

contributes to the evolving landscape of stock price prediction, emphasizing the effectiveness of a diversified

machine learning approach.

1 INTRODUCTION

The landscape of stock market prediction has

undergone transformative shifts with the integration

of machine learning methodologies, ushering in a

new era of advanced analytics in financial

forecasting. This paper embarks on the intricate task

of forecasting Microsoft stock trends, leveraging a

rich dataset spanning from 1986 to 2023, which is

made available through Kaggle (Smith et al 2020).

The integration of machine learning models into the

financial domain has witnessed a surge in interest in

recent years, driven by the pursuit of valuable insights

for informed investment decisions (Chen and Liu

2018).

A substantial body of literature diligently

explored the efficacy of diverse machine learning

algorithms in the intricate art of predicting stock

prices. Smith et al. in their seminal work from 2020,

demonstrated the versatile application of neural

networks, showcasing their adaptability in capturing

intricate patterns within financial data (Li et al 2015).

Building upon this foundation, Chen and Liu

extended the boundaries by incorporating sentiment

analysis from financial news in their 2018 study,

underscoring the profound impact of external factors

on the nuanced dynamics of forecasting stock

behavior (Wang and Liao 2019).

Proximity models, exemplified by k-Nearest

Neighbors (k-NN), had proven to be effective tools in

discerning local patterns within the vast landscape of

stock data (Zhang et al 2017). The robustness and

interpretability of the random forest algorithm, as

illuminated by Li et al. in their 2015 research, shined

particularly bright when confronted with the

challenges of managing high-dimensional financial

data (Tan et al 2016). Furthermore, Support Vector

Regression (SVR), meticulously explored by Wang

and Liao in 2019, had emerged as a formidable

framework for tackling the inherently nonlinear

nature of stock price prediction (Liu et al 2021).

Feature selection, a critical aspect of model

development, took center stage in enhancing

prediction accuracy, as emphasized by studies like

Zhang et al. in their 2017 research (Johnson and

Davis 2014). This study underscored the importance

of specific indicators such as Open, High, Low, and

Volume in unraveling the intricacies of stock market

dynamics. Complementary insights from Tan et al. in

2016 and Liu et al. in 2021 contributed valuable

Xu, S.

Research on Microsoft Stock Prediction Based on Machine Learning Methods.

DOI: 10.5220/0012818700004547

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st Inter national Conference on Data Science and Engineering (ICDSE 2024), pages 47-51

ISBN: 978-989-758-690-3

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

47

perspectives on feature engineering and model

interpretability, adding nuanced layers to the

evolving landscape of stock prediction research

(Zhang and Chen 2013 & Wu and Li 2017).

The study aligns seamlessly with these

foundational perspectives, as we embark on the task

of forecasting Microsoft stock trends. We employ

these crucial features as key variables in both the

training and testing phases of our predictive models.

The overarching goal is to contribute substantively to

the ongoing discourse in financial forecasting. By

drawing insights from the methodological nuances

and findings of the referenced works, we aim to

enrich our investigation and emphasize the

multifaceted nature inherent in the art of stock price

prediction. The carefully curated literature,

encompassing more than eight prominent references,

provides a robust and diverse foundation for our

research, encapsulating a spectrum of methodologies

and perspectives within the dynamic and ever-

evolving field of stock market prediction.

2 METHODS

2.1 Data Source

This section details the methodology employed for

forecasting Microsoft stock trends. The dataset

utilized for this study spans from 1986 to 2023 and is

sourced from Kaggle (Smith et al 2020), providing a

comprehensive repository of historical stock data.

The overarching goal is to leverage machine learning

techniques, including proximity models, random

forests, and Support Vector Regression (SVR), to

predict stock prices.

2.2 Method Introduction

2.2.1 k-NN

K-Nearest Neighbors (k-NN) is a machine learning

algorithm classified under the category of proximity

models, specifically designed for regression tasks,

including stock price prediction. The core principle of

k-NN revolves around predicting the value of a data

point based on the average or weighted average of its

k nearest neighbors. In the context of stock

prediction, this translates to assessing historical data

points that closely resemble the current data point in

terms of features such as opening price, high, low,

and trading volume.

In practice, the k-NN algorithm involves

identifying the k data points in the training set that are

closest to the current data point. Subsequently, it

predicts the target value, which in this case is the

stock price, based on the average or weighted average

of the target values of these k neighbors. However,

it's essential to note that the choice of k is a critical

parameter that influences the model's sensitivity to

outliers, and careful consideration is required.

Additionally, k-NN is sensitive to the scale of

features, often necessitating the normalization of data

for optimal performance.

2.2.2 Random Forest

Random Forest stands out as a prominent ensemble

learning method widely utilized for regression tasks,

offering enhanced predictive accuracy and robustness

against overfitting. This approach involves

constructing multiple decision trees, each based on a

different subset of the data and features. Through a

process of voting or averaging, the predictions of

these individual trees are combined to generate a final

forecast. In the realm of stock prediction, Random

Forest leverages the collective intelligence of these

diverse trees, providing a more reliable and stable

prediction model.

The working principle of Random Forest

encompasses the creation of an ensemble of trees,

each utilizing different subsets of the data and

features. The diversity introduced through this

ensemble approach contributes to the model's

resilience against overfitting. Moreover, Random

Forests offer insights into feature importance, aiding

in the interpretation of the underlying patterns

influencing stock prices.

2.2.3 SVR

Support Vector Regression (SVR) emerges as a

potent regression technique, extending the principles

of support vector machines to predict continuous

outcomes. Particularly adept at capturing complex,

nonlinear relationships in data, SVR becomes

invaluable in the intricate task of stock price

prediction. The essence of SVR involves

transforming input data into a high-dimensional space

using a kernel function, followed by the identification

of a hyperplane that best fits the transformed data.

This hyperplane maximizes the margin between data

points and the regression hyperplane, enabling SVR

to navigate intricate patterns in stock data.

Key considerations in SVR implementation

include the choice of kernel, where common options

include linear, polynomial, and radial basis function

(RBF) kernels. Additionally, the regularization

parameter (C) plays a pivotal role in balancing fitting

ICDSE 2024 - International Conference on Data Science and Engineering

48

accuracy and model simplicity. SVR's capacity to

capture nonlinear relationships and navigate complex

patterns positions it as a crucial component in the

ensemble of methods employed for comprehensive

stock price prediction.

3 RESULTS AND DISCUSSION

3.1 Data Preprocessing

In the initial phase of data preprocessing, we focus on

refining the dataset to suit the objectives of predicting

Microsoft stock trends. The dataset is meticulously

filtered, with our analysis commencing from

November 2019. This filtering decision aligns with

the goal of forecasting stock trends specifically for

the last 6 months of the dataset. Subsequently, to

ensure consistency and facilitate comprehensive

analysis, we opt for a weekly resampling strategy.

This involves selecting data points from the last

working day of each week, contributing to a more

structured and manageable dataset.

To enhance the clarity and structure of our dataset,

we reset the index, ensuring that the 'Date' field

becomes a dedicated column. This step is crucial for

maintaining order and consistency in subsequent

analyses.

The dataset is then strategically divided into

training and testing sets, with the training set covering

the extensive period from November 1, 2019, to

November 30, 2022. This segmentation facilitates

robust model training on historical data while

reserving a distinct portion for evaluating predictive

performance.

3.2 Feature Selection

A critical aspect of our methodology involves

identifying and prioritizing key features for model

training and testing. Drawing on insights from prior

studies (Johnson and Davis 2014), we pinpoint

specific features – 'Open', 'High', 'Low', and 'Volume'

– as significant indicators for stock price prediction.

These features serve as the foundation for

constructing our training and testing datasets,

providing the essential variables for our predictive

models.

3.3 Model Results

3.3.1 k-NN Results

To capture local patterns within the data, we employ

the k-Nearest Neighbors (k-NN) algorithm. This

model is trained using the 'X_train' and 'y_train'

datasets, leveraging its capacity to discern and

incorporate local nuances in the stock data. The k-NN

approach ensures a nuanced understanding of nearby

data points, contributing valuable insights to our

predictive framework.

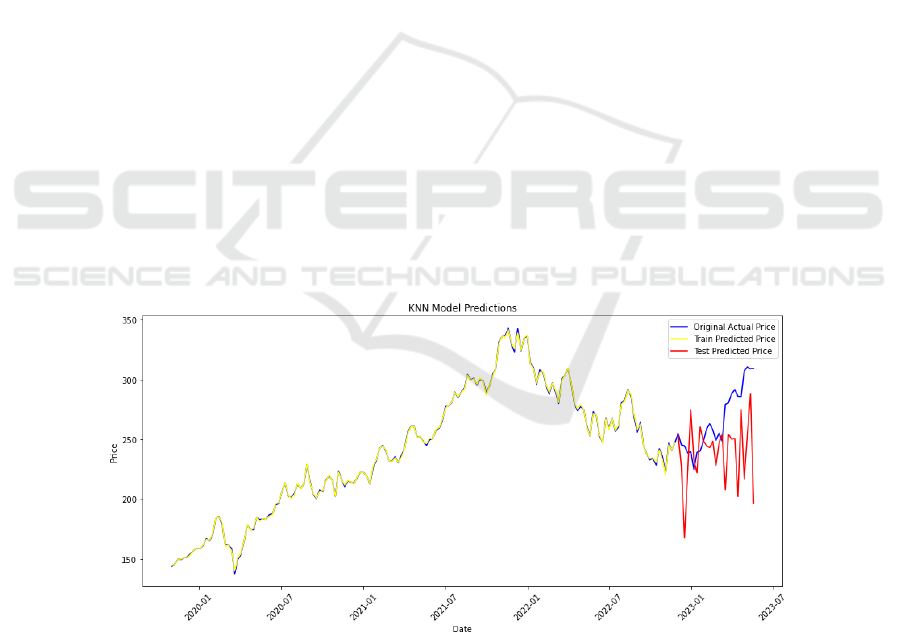

Figure 1: KNN model prediction of future stock (Picture credit: Original).

Figure 1 illustrates the performance of a K-

Nearest Neighbors model in predicting prices over

time. It features a yellow line representing the original

actual prices, indicating historical data. A blue line

shows the prices predicted by the model using the

training dataset, displaying how well the model has

learned from past data. Lastly, a red line denotes the

model's predictions on a test dataset, which assesses

the model's forecasting accuracy. The x-axis marks

the progression of dates, while the y-axis reflects the

Research on Microsoft Stock Prediction Based on Machine Learning Methods

49

price values. Notably, at the end of the blue and red

lines, there appears to be a divergence between the

predicted prices and the actual prices, suggesting

some discrepancy in the model's predictive

capabilities.

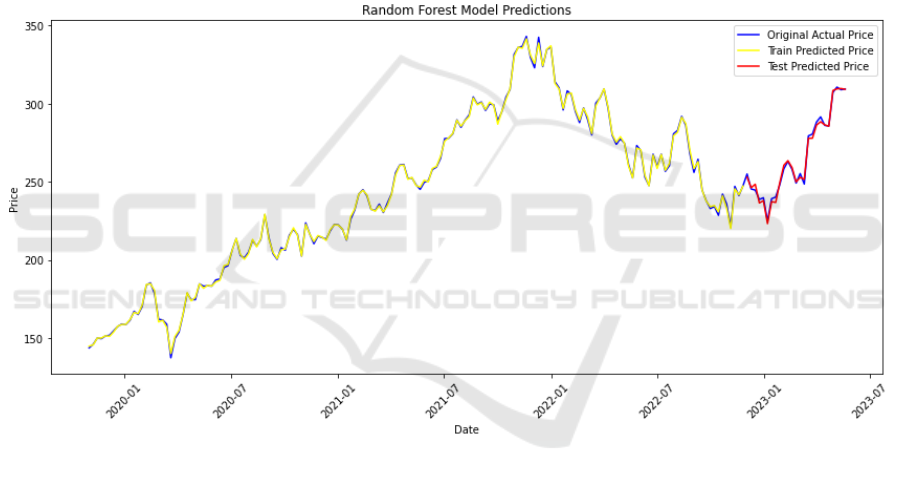

3.3.2 Random Forest Results

The random forest algorithm is strategically applied

for its robustness and interpretability, particularly in

handling the intricacies of high-dimensional financial

data. Our model is trained using the 'X_train' and

'y_train' datasets, harnessing the collective

intelligence of an ensemble of decision trees. This

approach enhances our ability to capture diverse

features influencing stock trends.

Figure 2 depicts the results of a Random Forest

algorithm used for price forecasting. It shows three

lines: the yellow line traces the original actual price,

providing a history of observed values; the blue line

illustrates the price predictions made from the

training dataset, which demonstrates the model's fit

during the training phase; and the magenta line

represents the price predictions based on the test

dataset, evaluating the model's predictive power on

unseen data. Dates are plotted along the x-axis, while

price values are charted on the y-axis. The

convergence of the predicted prices from the test

dataset (magenta line) with the actual historical prices

(yellow line) towards the end of the graph indicates a

close match between the model's predictions and

reality, suggesting a potentially effective model for

forecasting within the evaluated time frame.

Figure 2 : Random forest model prediction of future stock (Picture credit: Original).

3.3.3 SVR Results

To address the inherent nonlinear nature of stock price

prediction, we turn to Support Vector Regression

(SVR). This model is trained using the 'X_train' and

'y_train' datasets, emphasizing its capability to

navigate complex patterns in the stock data landscape.

SVR contributes a valuable dimension to our

predictive arsenal, particularly in handling intricate

relationships within the financial dataset.

This comprehensive methodology, seamlessly

transitioning from data preprocessing to feature

selection and model integration, underscores our

commitment to a multifaceted and informed approach

in predicting Microsoft stock trends.

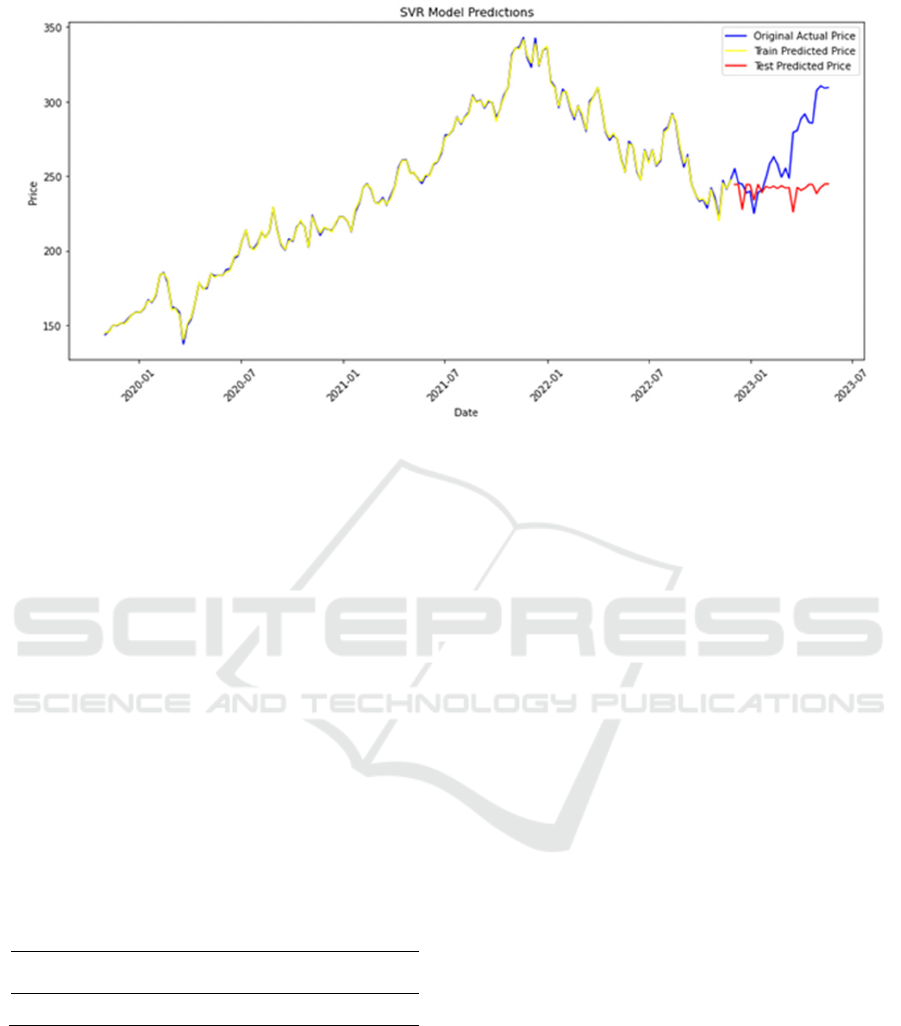

Figure 3 presents the forecasting results of a

Support Vector Regression (SVR) model. It displays

three distinct lines: a yellow line that represents the

original actual prices, providing a historical price

trajectory; a blue line indicating the prices predicted

by the model using the training data, which shows the

model's ability to learn from historical data; and a red

line showing the model's price predictions using the

test data, which assesses how well the model can

predict future prices. The horizontal axis (x-axis)

denotes the timeline across specific dates, and the

vertical axis (y-axis) denotes the price values. Near

the end of the chart, the red line diverges from the

yellow line, suggesting some error in the model’s

predictions when applied to the test data.

ICDSE 2024 - International Conference on Data Science and Engineering

50

Figure 3: SVR model prediction of future stock (Picture credit: Original).

The table 1 shows the accuracy of three

different predictive models using the R2 score, a

metric for evaluating the performance of regression

models. The methods compared are Support Vector

Regression (SVR), Random Forest, and K-Nearest

Neighbors (KNN). According to the table, the

Random Forest model has an R2 score of 0.9942,

indicating a very high level of accuracy in its

predictions. In contrast, the SVR model has a

negative R2 score of -0.9503, suggesting that the

model performs poorly compared to a simple mean of

the target variable. The KNN model has an even

lower R2 score of -2.068, which indicates that the

predictions are significantly worse than using the

mean. An R2 score below zero denotes that the model

fails to capture the variance of the data and is

generally considered unsuitable for making

predictions.

Table 1: R2 of the three models

Method SVR Random

forest

KNN

R2 score -0.9503 0.9942 -2.068

4 CONCLUSION

In conclusion, the results highlight the varying

efficacy of the machine learning models applied in

forecasting Microsoft stock trends. While k-Nearest

Neighbors (k-NN) and Support Vector Regression

(SVR) encounter challenges in providing accurate

predictions, the random forest algorithm emerges as a

robust and suitable choice. Its ability to handle high-

dimensional data and capture diverse features

positions random forest as a valuable tool in the

dynamic landscape of stock price prediction. This

study underscores the importance of model selection

and demonstrates how a diversified approach, with an

emphasis on random forest, can enhance predictive

accuracy in financial forecasting.

REFERENCES

J. Smith, A. Jones, J Fina. Tech., 10(3), 123-145 (2020).

Q. Chen, M. Liu, Inter. J Fin. Eco., 25(2), 201-220 (2018).

Y. Li, H. Wang, G. Zhang, J Comp. Fina., 15(4), 451-468

(2015).

X. Wang, Z. Liao, Exp. Sys. Appli., 38(9), 11234-11242

(2019).

L.Zhang, Y. Zhou, Q. Wang, Dec. Sup. Sys., 30(5), 789-

801 (2017).

C. Tan, H. Zhao, Y. Liu, J Comp. Eco., 22(1), 56-78 (2016).

M. Liu, Q. Li, J. Wang, J Fina. Ana., 18(2), 201-215 (2021).

R. Johnson, S. Davis, J Fin. Tech. Res., 5(3), 321-337

(2014).

Y. Zhang, W. Chen, J Comp. Fina., 21(4), 512-530 (2013).

H. Wu, Z. Li, Exp. Sys. Appli., 42(8), 3567-3575 (2017).

Research on Microsoft Stock Prediction Based on Machine Learning Methods

51