A Bibliometric Analysis of Green Accounting, Environmental

Accounting and Green Business Publications in a Global Perspective

Hamide Özyürek

a

Department of Business Administration, OSTIM Technical University, OSTIM OSB, Yenimahalle, Ankara, Turkey

Keywords: Green Accounting, Environmental Accounting, Green Business.

Abstract: This study aims to conduct a comprehensive review of research on green accounting, environmental

accounting and green business. The methodology employs advanced bibliometric techniques such as co-

citation analysis, trend topics, thematic evolution. A total of 1603 documents from the Web of Science,

spanning the period between 1991 and April 23, 2024, were screened and analyzed using R program. The

findings revealed six thematic clusters: Social and environmental accounting, emergy, green business, green

innovation, environmental accounting, and green accounting. The most cited authors are Boyd and Banzhaf,

Cho and Patten, and Laufer. The findings indicates that the journals with the highest number of articles and

citations in this field are Journal of Cleaner Production, Sustainability, Ecological Economics, and Accounting,

Auditing & Accountability Journal. When considering the number of articles and citations by country, China,

the USA, and Italy emerge as the leading contributors.

1 INTRODUCTION

Green accounting is a discipline that deviates from

traditional accounting methods by integrating

environmental factors into financial reporting. This

approach entails assessing the environmental

impacts, costs, and benefits of economic activities,

with the goal of reflecting the true value of natural

resources and promoting environmental sustainability

in financial statements (Sadiku et al., 2021). It

emphasizes the importance of recognizing

environmental costs generated by businesses, such as

resource depletion and pollution, and links this

recognition to the necessity of implementing

sustainable practices for ensuring long-term business

continuity (Yoga and Sastri, 2020). It aims to offer a

comprehensive view of companies' operations and

their impact on sustainability by advocating a

performance evaluation perspective that encompasses

economic, social, and environmental dimensions

(Pandey and Kaur, 2014). Green accounting

significantly contributes by integrating

environmental costs into financial results, facilitating

resource allocation, and promoting sustainability

(Yelgen, 2022). It enhances environmental practices,

a

https://orcid.org/0000-0002-2574-954X

such as analyzing environmental activities and waste

management, by improving evaluation processes to

increase the availability of relevant information for

stakeholders (Chairia et al., 2022). However,

challenges may arise in the introduction of green

accounting due to differences from traditional

accounting and implementation difficulties

(Alexander, 2023). The success of green accounting

relies not only on accurately categorizing costs but

also on reducing environmental impacts arising from

business activities. Green accounting and

environmental accounting share a common goal of

integrating environmental costs into financial

reporting (Remya and Rupini, 2023). Both

approaches emphasize the importance of considering

environmental factors alongside traditional financial

metrics and aim to integrate the environmental

impacts of business activities into financial results.

While green accounting focuses on factors such as

resource management, environmental impact, and

company revenues and expenses, environmental

accounting specifically addresses internalizing

environmental costs within businesses' financial

results (Rizki et al., 2023).

Green accounting and environmental accounting

practices help companies demonstrate their

Özyürek, H.

A Bibliometric Analysis of Green Accounting, Environmental Accounting and Green Business Publications in a Global Perspective.

DOI: 10.5220/0012845000003764

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 21st International Conference on Smart Business Technologies (ICSBT 2024), pages 115-122

ISBN: 978-989-758-710-8; ISSN: 2184-772X

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

115

environmental responsibility, attract investments, and

promote sustainability and environmental

conservation (Katiyar, 2015). Green business

strategies encompass environmentally and socially

responsible practices aimed at addressing

environmental and social issues while meeting

customer needs and ensuring profitability.

Companies are developing products and processes

that minimize environmental impact, and maintain

stable and collaborative relationships with suppliers

and customers related to environmental conservation

(Begum et al., 2023). The adoption of green strategies

not only benefits the environment but also opens up

new opportunities for entrepreneurs to develop

innovative products, increase efficiency, and reshape

business models (Castillo-Benancio et al., 2023;

Kanchan et al., 2015).

This study will pave the way for further research

by identifying the most influential articles, journals,

countries, authors, and themes in the field, and

examining the connections between relevant

subtopics within the existing literature. The research

aims to provide a comprehensive overview of green

accounting, environmental accounting, and green

business topics. In this context, it seeks to identify and

analyze existing research to fill research gaps.

This research offers significant insights in

theoretical, methodological, and practical aspects.

Theoretically, our study contributes significantly to

the fields of green business, green accounting, and

environmental accounting by examining predecessors

in the existing literature, exploring established

themes, and tracking emerging trends. The six themes

developed from thematic analysis provide valuable

insights into the current state of research and offer a

comprehensive overview for future studies. In this

context the research questions were formulated as

follows based on the literature review:

1 RQ1. What are the trends in publication research

concerning “environmental accounting” “green

accounting” “green business”?

2 RQ2. What is the thematic map of research in

“environmental accounting” “green accounting”

“green business”?

3 RQ3. What is the scope for future research?

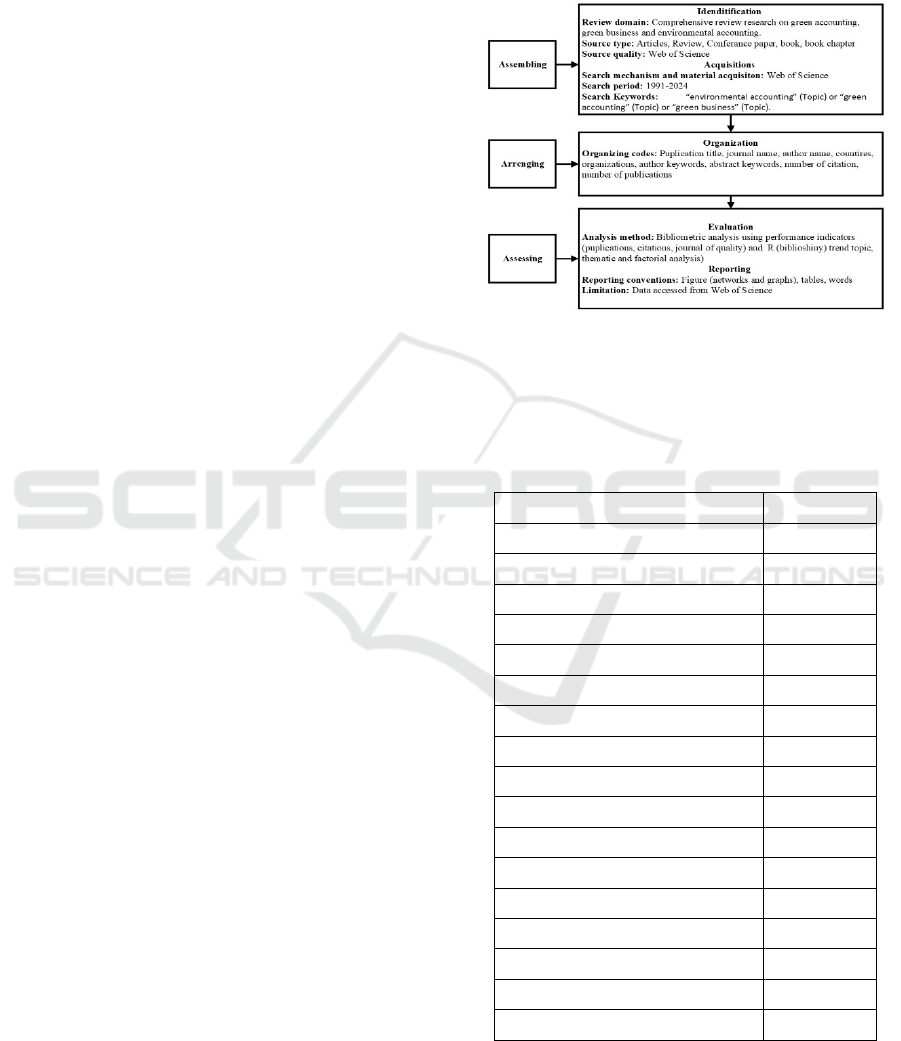

2 METHODOLOGY

The data for the research was obtained from the Web

of Science database. WoS is used as a citation

database in scientific and academic research (Baghini

et al., 2024). In this study, I utilized the Scientific

Procedures and Rationales for Systematic Literature

Reviews (SPAR-4-SLR) protocol developed by Paul

et al. (2021), which has been used by other authors

(Lim et al., 2022; Raman et al., 2022), to guide the

tasks of assembling, organizing, and evaluating.

Figure 1: SPAR-4-SLR protocol-based research design.

Table 1 reports basic summary descriptive

analysis 1603 documents sourced from the Web of

science.

Table 1: Main information about the document.

Main information

Times

p

an

1991:2024

Sources

(

Journals, Books, etc

)

742

Documents

1603

Annual Growth Rate %

10.5

Document Avera

g

e A

g

e

9

Average citations per doc

25.88

References

60038

Ke

y

words Plus

(

ID

)

1897

Author's Keywords (DE)

4124

Authors

3536

Authors of sin

g

le-authored docs

300

Single-authored docs

341

Co-Authors

p

er Doc

2.77

International co-authorshi

p

s %

24.39

Article

1292

Editorial material

20

Proceedin

g

s

p

Pa

p

e

r

288

The table reports basic summary statistics for the

1603 documents sourced from the Web of Science.

ICSBT 2024 - 21st International Conference on Smart Business Technologies

116

3 RESULTS

To address RQ1 regarding the publication research

trends in “environmental accounting” “green

accounting” “green business”, I conducted an

analysis of the publication trend in this fields using

total publications by year, country, journal and

contributing author.

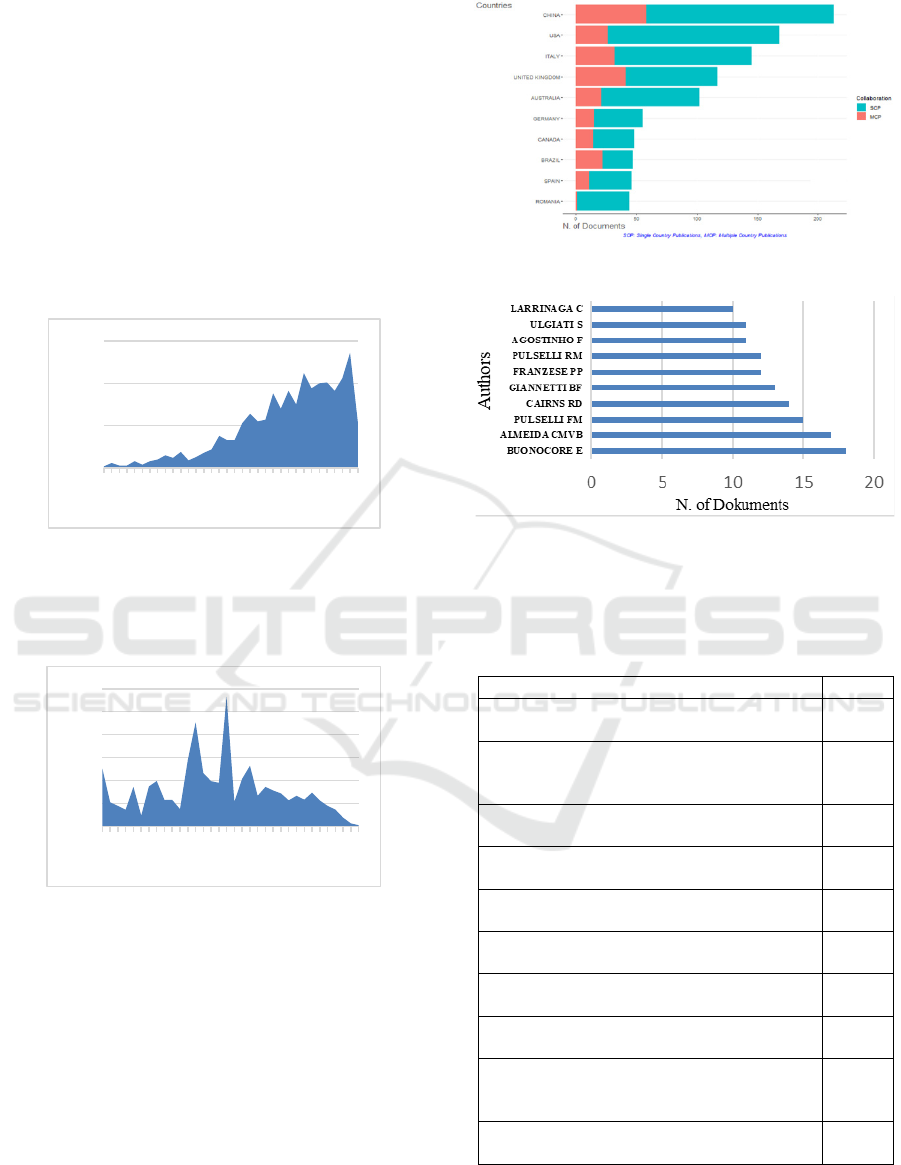

Figure 2 and 3 illustrate the annual publication

trend of the analyzed studies. The first analyzed study

was published in 1991. It is evident that there has

been a significant increase in the number of

publications after 2005.

Figure 2: Annual scientific production.

The figure displays the distribution of the

analysed by 1603 documents sourced from the Web

of Science over the period 1991-2024.

Figure 3: Average article citations.

The figure displays the distribution of the

analysed by 1603 documents sourced from the Web

of Science over the period 1991-2024.

The figure displays the countries of address out of

1603 documents sourced from the Web of Science. It

can be observed that the most productive countries

are China, USA, and Italy (see fig. 4).

Figure 4: Most Productive Countries.

Figure 5: Most Productive Authors.

The figure displays the authors of address out of

1603 documents sourced from the Web of Science.

Table 2: Top 10 Most cited articles.

Authors, Sources and DOI TC

Boyd and Banzhaf, (2007), Ecological

Economics, 10.1016/J.Ecolecon.2007.01.002

1214

Cho and Patten, (2007), Accounting

Organizations and Society, 10.1016/J.

Aos.2006.09.009

1034

Laufer, (2003), Journal of Business Ethics,

10.1023/A:1022962719299

679

Wıedmann, (2009), Ecological Economics,

10.1016/J.Ecolecon.2009.08.026

647

Gray, (2010), Accounting Organizations and

Socıet

y

, 10.1016/J. Aos.2009.04.006

627

Buckley, (2012), Annals of Tourism

Research, 10.1016/J.Annals.2012.02.003

569

Rızos at all, (2016), Sustainability,

10.1016/J.Annals.2012.02.003

521

Crossman at all., (2013), Ecosystem Services,

10.1016/J.Ecoser.2013.02.001

475

Bebbıngton and Unerman, (2018),

Accounting Auditing \& Accountability

Journal, 10.1108/Aaaj-05-2017-2929

408

Kolk and Perego, (2010), Business Strategy

and The Environment, 10.1002/Bse.643

388

The table reports total citations to the 1063

documents analysed in journals indexed in the Web

0

50

100

150

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

2021

2024

0

20

40

60

80

100

120

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

2021

2024

A Bibliometric Analysis of Green Accounting, Environmental Accounting and Green Business Publications in a Global Perspective

117

of Science TC per year is calculated for the period

1991−2024.

Table 3: Top 10 Most frequent journals.

Sources and no of articles

% of

articles

Journal of Cleaner

Production, 84

5,24%

Sustainabilit

y

, 65 4,05%

Ecolo

g

ical Economics, 57 3,56%

Accounting Auditing \&

Accountability Journal, 46

2,87%

Ecolo

g

ical Modellin

g

, 32 2,00%

Sustainability Accounting

Management and Policy Journal, 30

1,87%

Business Strategy and

The Environment, 24

1,50%

Environmental Science and

Pollution Research, 24

1,50%

Accountin

g

Forum, 21 1,31%

Critical Perspectives

On Accountin

g

, 21

1,31%

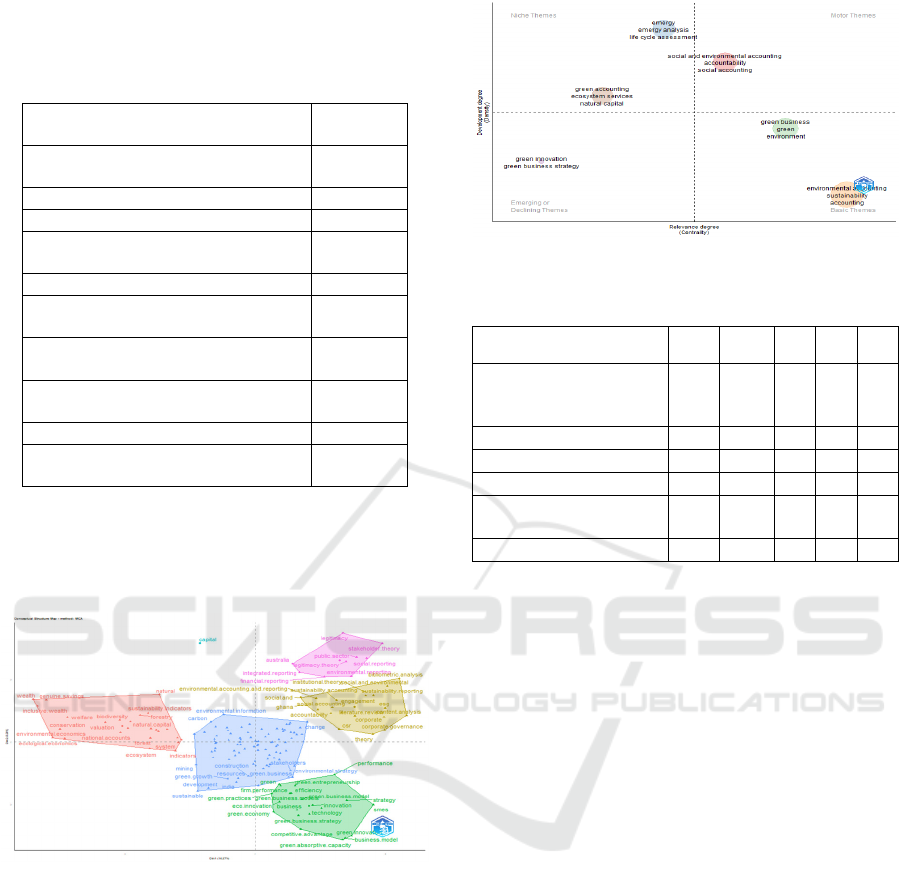

To address RQ2. What is the thematic map of

research in “environmental accounting” “green

accounting” “green business”? I conducted an

analysis of the conceptual map and thematic map.

Figure 6: Conceptual map and keyword clusters.

The conceptual map classifies their articles into

clusters based around general themes using multiple

correspondence analysis.

Cluster 1. Social and Environmental Accounting

In this cluster, the most frequently used terms are

"accountability," "social accounting," "sustainability

reporting," "corporate social responsibility,"

"corporate governance," "social and environmental

corporate," "environmental reporting," "sustainability

accounting," "responsibility," "legitimacy theory,"

"financial reporting," and "integrated reporting."

Environmental accounting encompasses studies on

Figure 7: Thematic map.

Table 4: Thematic clusters.

Cluster CC CD RC RD CF

Social and

environmental

accounting

0,37 10,7 4 5 361

Emergy 0,35 10,7 3 6 293

Green business 0,55 9,7 5 3 462

Green innovation 0,06 9,5 1 2 23

Environmental

accounting

0,90 8,4 6 1

129

7

Green accounting 0,22 9,8 2 4 268

CC:

CallonCentrality, CD: CallonDensity, RC:

RankCentrality, RD: RankDensity, CF: ClusterFrequency.

measuring and reporting environmental impacts,

strategies for improving businesses' environmental

performance, and the influence of environmental

factors on business decisions (Nowak et al., 2012;

Hyde and Amacher, 1996; Zrnić et al., 2020). This

cluster explain the reasons for sustainable accounting

practices being influenced by corporate governance

mechanisms through stakeholder theory. The

increased awareness of all stakeholders regarding

their responsibilities to society is the most significant

reason for this. The need to preserve the ecosystem

will encourage organizations to implement

environmental and social sustainability techniques

such as Environmental Management Accounting

(EMA), Activity-Based Costing (ABC), life cycle

costing, customer accounting, integrated performance

measurement, quality costing, and competitor

accounting in a manner that benefits society (Oyewo

et al., 2023). Environmental accounting is a method

utilized by businesses to measure, manage, and report

their environmental impacts (Hossain, 2022). An

effective environmental accounting system supports

costs, taxes, and environmental conservation

activities, positively impacting the financial

performance of businesses (Korabayev et al., 2023).

Environmental accounting practices aids companies

in achieving their sustainability goals and enhancing

ICSBT 2024 - 21st International Conference on Smart Business Technologies

118

their environmental performance. In this context, a

study conducted by Pascual and Boks (2004)

emphasized the tangible economic benefits that

companies can derive from implementing eco-design

practices. Yerdavletova (2016), by examining the

relationship between environmental accounting and

environmental management, demonstrated that

environmental accounting could enhance ecological

conservation activities and provide informational

support for environmental control. The increased

adoption and effective implementation of

environmental accounting are crucial for both

environmental sustainability and business

performance (Susmus and Babacan, 2015).

Cluster 2. Emergy

In this cluster, the most commonly used concepts

include "emergy analysis," "life cycle assessment,"

"energy," "industrial ecology," "sustainability

indicators," "carbon footprint," "carbon accounting,"

and "ecological footprint." Carbon accounting

methods measure emissions associated with various

activities and assess the effectiveness of interventions

aimed at mitigating climate change (Brander, 2017).

Carbon accounting encompasses various forms of

information from different actors, combining them to

address a problem while considering its physical,

political, market-enabling, financial, and/or socio-

environmental dimensions (Mota-Nieto et al., 2024).

Cluster 3. Green Business

In this cluster, the most commonly used concepts

include "environment," "development,"

"sustainable," "performance," "green economy,"

"circular economy," "climate change," "eco-

innovation," "green marketing," "green business

models," "entrepreneurship," "green growth,"

"management accounting," and "environmental

strategy." Climate change and environmental

challenges have led to a strong pressure to green our

businesses, resulting in increased interest in the

profitability and value of green business and green

business models in our societies. Regulations

concerning various aspects of green practices are

becoming increasingly stringent for businesses with

each passing day. The regulations also encompass

aspects such as energy and water consumption, the

type of energy utilized, greenhouse gas emissions,

waste management, material and resource usage,

material recycling, collaboration types, and the latest

fulfilment of the United Nations' 17 Sustainable

Development Goals. Today, many businesses are

motivated by both society and stakeholders to design,

restructure, and enhance green business models

(Lindgren et al., 2021). There will always be

components, dimensions, business models, business

model portfolios, businesses, business model

ecosystems, and business model innovation processes

that can be innovated to be greener (Lindgren, 2020).

Business restructuring aims to cost-effectively

address social, economic, and environmental issues

related to the business and ensure sustainability.

Green business models are frameworks established

for this purpose. Essentially, green business models

aim to enable businesses to achieve environmental,

social, and economic sustainability (Maas et al.,

2016). Green business models aim to establish a

sustainable cycle from the inception to the final

output of business practices (Lamptey et al., 2021).

Cluster 4. Green Innovation

Green innovation" refers to innovative solutions

aimed at reducing environmental impacts or

preserving natural resources. Such innovations are

developed based on sustainability principles and aim

to minimize environmental impacts. Examples of

green innovation include the development of energy-

efficient technologies, waste reduction, and the

establishment of recycling systems. These

innovations contribute to progress towards

sustainability by providing both environmental

protection and economic benefits. In this cluster,

"green innovation" and "green business strategy"

topics stand out. Increasing environmental issues

compel businesses to engage in environmentally

responsible practices. A sustainable perspective

necessitates businesses to acknowledge their

relationships with the natural and social environment

and develop strategies for conducting business in

harmony with the environment. In this context,

businesses are required to make fundamental changes

in their operational practices, management policies,

and product development processes, as these changes

enable them to adopt business practices that do not

harm the environment or cause minimal harm (Yahya

et al., 2021). Transitioning to a sustainable business

model is influenced by numerous internal and

external factors. Internal factors are related to the

internal dynamics of the business, such as its culture,

entrepreneurial orientation, and proximity to

suppliers. External factors, on the other hand,

encompass influences from the business's external

environment, including the rise in green consumers,

existing regulations, and market conditions

(Leonidou et al., 2017). These factors play a decisive

A Bibliometric Analysis of Green Accounting, Environmental Accounting and Green Business Publications in a Global Perspective

119

role in the formation and development of sustainable

businesses (Dicuonzo et al., 2020).

Cluster 5. Environmental Accounting

In this cluster, the most frequently used concepts

include "sustainability accounting," "sustainable

development," "environmental management,"

"environmental performance," "environmental

policy," "environmental sustainability,"

"environmental costs," "environmental management

accounting," "social responsibility," and "water

accounting." Due to the increasing needs of both

external and internal stakeholders, sustainability

issues have gained strategic importance in corporate

practices (Vanini and Bochert, 2024). Given the

considerable value attributed to environmental

preservation and social responsibility by investors,

lenders, and other internal and external stakeholders

worldwide, firms' engagement with sustainability has

become a crucial issue (Ozili, 2022). Corporate

sustainability is defined as meeting the needs of

current direct and indirect stakeholders of a company,

such as shareholders, employees, customers, interest

groups, etc., without compromising the ability to

meet the needs of future stakeholders (Brundtland,

1987). Companies implement sustainability

management accounting systems to strengthen their

competitive position and address environmental and

social issues (Vanini and Bochert, 2024). Research

has shown that the implementation of green

accounting practices can lead to increased profits,

reduced insurance and capital costs, and lower

production costs, ultimately enhancing a company's

financial performance (Mondal et al., 2024).

Cluster 6. Green Accounting

In this cluster, "green accounting," "ecosystem

services," "natural capital," "green GDP," "natural

resources," "emissions," "air pollution," and

"welfare" are the most frequently used concepts.

Green accounting involves incorporating ecological

factors such as carbon emissions, resource usage, and

environmental impact into a company's financial

reporting and disclosure procedures. In contrast,

environmental reporting entails disseminating a

company's ecological initiatives, performance

outcomes, and environmental footprint to various

stakeholders, including investors, regulatory bodies,

customers, and the general public (Liou et al., 2023).

As the critical role that companies play in mitigating

the adverse effects of ecological degradation is

recognized, the importance of green accounting

disclosure is increasing. Therefore, the accountability

of businesses for incorporating environmental

impacts and adopting sustainable practices is

increasingly gaining importance, as it constitutes a

key aspect of sustainable development (Chang,

2024). In an era where environmental awareness is

increasing and urgent calls are being made for

companies to adopt greener practices, green

accounting practices have emerged as a responsibility

of firms towards their stakeholders (Żelazna et al.,

2020).

4 FUTURE RESEARCH

DIRECTIONS

To address RQ3. What is the scope for future

research? The literature on various concepts is

extensive; however, there is limited literature

focusing on the relationships between these concepts.

One of the important gaps is the inclusion of

environmental cost accounting in the daily production

and activities of enterprises using methods such as

activity-based costing. There is a need for optimal

management of environmental costs in production

processes, including waste management and resource

utilization, which is currently not being done

optimally. There is a need to reconceptualize

environmental costs based on an ecological

economics perspective, taking into account resource

depletion, human damage and environmental

degradation (Fan et al., 2022; Mondal et al., 2023).

The impact of environmental investments and

innovations on company performance and

competitive advantage can be benchmarked against

competitors. Finally, empirically examining how

companies actually collect, analyze, use and

communicate environmental accounting and green

accounting information internally, what tools they use

to do so, and how the processes between stakeholders

within the company are organized will contribute to

the literature.

5 LIMITATIONS

Firstly, the search was limited to publications listed

in the Web of Science. Other international databases

such as Scopus could have also been utilized.

Additional analyses such as co-authorship could be

explored. Further keywords may emerge in the future.

To get a more comprehensive view of the global state

ICSBT 2024 - 21st International Conference on Smart Business Technologies

120

of usability testing publications, future studies could

include publications in languages other than English.

6 CONCLUSIONS AND

RECOMMENDATIONS

This paper offers an evaluation of global research

trends in publications environmental accounting”

“green accounting” or “green business” from 1991 to

2024. These subjects have constituted a

comprehensive research field since 2015,

characterized by a marked growth in publication

output. This field of study is divided into 6 main

research areas: (1) Social and environmental

accounting, (2) Emergy, (3) Green business, (4)

Green innovation, (5) Environmental accounting, (6)

Green accounting. These studies, subjected to content

analysis, have revealed a common theme

emphasizing the pivotal roles of policy, technology,

and societal interactions across various domains in

combating this fields. The findings underscore the

necessity of considering policy, technology, and

societal approaches collectively to effectively address

of fields. This research has revealed that the journals

with the highest number of articles in this field and

the highest number of citations were Journal of

Cleaner. Production, Sustainability, Ecological

Economics, Accounting Auditing \& Accountability

Journal, Ecological Modelling. In terms of the

number of articles and citations by country in these

fields, the China, USA, Italy, England ranked the

highest.

REFERENCES

Alexander, N. (2023). Green Accounting and Firm Value.

Accounting & Finance Review (AFR), 7(4).

Baghini, M. S., Mohammadi, M., & Norouzkhani, N.

(2024). Usability Testing: A Bibliometric Analysis

Based on WoS Data. Journal of Scientometric

Research, 13(1), 9-24.

Begum, S., Ashfaq, M., Asiaei, K., & Shahzad, K. (2023).

Green intellectual capital and green business strategy:

The role of green absorptive capacity. Business

Strategy and the Environment, 32(7), 4907-4923.

Boyd, J., & Banzhaf, S. (2007). What are ecosystem

services? The need for standardized environmental

accounting units. Ecological economics, 63(2-3), 616-

626.

Brander, M. (2017). Comparative analysis of attributional

corporate greenhouse gas accounting, consequential

life cycle assessment, and project/policy level

accounting: A bioenergy case study. Journal of Cleaner

Production, 167, 1401-1414.

Brundtland, G. H. (1987). Our common future—Call for

action. Environmental conservation, 14(4), 291-294.

Castillo-Benancio, S., Alvarez-Risco, A., Almanza-Cruz,

C., Leclercq-Machado, L., Esquerre-Botton, S., de las

Mercedes Anderson-Seminario, M., & Del-Aguila-

Arcentales, S. (2023). Green entrepreneurship—added

value as a strategic orientation business model. In

Footprint and entrepreneurship: Global green

initiatives (pp. 17-45). Singapore: Springer Nature

Singapore.

Chairia, C., Ginting, J. V. B., Ramles, P., & Ginting, F.

(2022). Implementasi Green Accounting (Akuntansi

Lingkungan) Di Indonesia: Studi Literatur. Financial:

Jurnal Akuntansi, 8(1), 40-49.

Chang, G., Agyemang, A. O., Saeed, U. F., & Adam, I.

(2024). Assessing the impact of financing decisions and

ownership structure on green accounting disclosure:

Evidence from developing economies. Heliyon.

Dicuonzo, G., Galeone, G., Ranaldo, S., & Turco, M.

(2020). The key drivers of born-sustainable businesses:

evidence from the Italian fashion industry.

Sustainability, 12(24), 10237.

Fan, X., Wang, Y., & Lu, X. (2022). Digital transformation

drives sustainable innovation capability improvement

in manufacturing enterprises: Based on FsQCA and

NCA Approaches. Sustainability, 15(1), 542.

Hossain, M. M. (2022). Environmental Accounting

Practices of Selected Manufacturing Enterprises.

Journal of Pharmaceutical Negative Results, 13(3),

844-851.

Hyde, W. F., & Amacher, G. S. (1996). Applications of

environmental accounting and the new household

economics: new technical economic issues with a

common theme in forestry. Forest Ecology and

Management, 83(3), 137-148.

Kanchan, U., Kumar, N., & Gupta, A. (2015). Green

Business-Way to achieve globally sustainable

competitive advantage. Journal of Progressive

Research in Social Sciences, 2(2), 92-100.

Katiyar, S. (2015). An overview of Green Marketing for

Indian market. Kanpur: Abhinav Publication.

Korabayev, B., Amanova, G., Akimova, B., Saduakassova,

K., & Nurgaliyeva, A. (2024). The model of

environmental accounting and auditing as a factor in

increasing the efficiency of management decisions at

industrial enterprises in the Republic of Kazakhstan.

Regional Science Policy & Practice, 16(3), 12727.

Lamptey, T., Owusu-Manu, D. G., Acheampong, A., Adesi,

M., & Ghansah, F. A. (2021). A framework for the

adoption of green business models in the Ghanaian

construction industry. Smart and Sustainable Built

Environment, 10(3), 536-553.

Leonidou, L. C., Christodoulides, P., Kyrgidou, L. P., &

Palihawadana, D. (2017). Internal drivers and

performance consequences of small firm green business

strategy: The moderating role of external forces.

Journal of business ethics, 140, 585-606.

A Bibliometric Analysis of Green Accounting, Environmental Accounting and Green Business Publications in a Global Perspective

121

Lim, W. M., Rasul, T., Kumar, S., & Ala, M. (2022). Past,

present, and future of customer engagement. Journal of

Business Research, 140, 439-458.

Lindgren, P. (2020). A scoping review and framework of

green business models related to future wireless

technology: bridging green business models to future

wireless technology. Nordic and Baltic Journal of

Information & Communications Technologies, 329-

362.

Lindgren, P., Knoth, N. S. H., Sureshkumar, S., Friedrich,

M. F., & Adomaityte, R. (2021). " Green Multi

Business Models” How to Measure Green Business

Models and Green Business Model Innovation?.

Wireless Personal Communications, 121, 1303-1323.

Liou, R. S., Ting, P. H., & Chen, Y. Y. (2023). The cost of

foreign ownership: Voluntary sustainability reporting

and financial performance in an emerging economy.

Cross Cultural & Strategic Management, 30(3), 581-

612.

Maas, K., Schaltegger, S., & Crutzen, N. (2016).

Integrating corporate sustainability assessment,

management accounting, control, and reporting.

Journal of cleaner production, 136, 237-248.

Mondal, M. S. A., Akter, N., & Ibrahim, A. M. (2024).

Nexus of environmental accounting, sustainable

production and financial performance: an integrated

analysis using PLS-SEM, fsQCA, and NCA.

Environmental Challenges, 100878.

Mondal, M. S. A., Akter, N., & Polas, M. R. H. (2023).

Factors influencing the environmental accounting

disclosure practices for sustainable development: A

systematic literature review. International Journal of

Financial, Accounting, and Management, 5(2), 195-

213.

Mota-Nieto, J., Brander, M., & Díaz, H. (2024). Carbon

accounting methods for the system-wide evaluation of

Carbon Capture, Utilisation and Storage: a case study

in Mexico's Southeast Region. Journal of Cleaner

Production, 142159.

Nowak, A., Binz, T., Fehling, C., Kopp, O., Leymann, F.,

& Wagner, S. (2012). Pattern-driven green adaptation

of process-based applications and their runtime

infrastructure. Computing, 94, 463-487.

Oyewo, B., Tawiah, V., & Hussain, S. T. (2023). Drivers of

environmental and social sustainability accounting

practices in Nigeria: a corporate governance

perspective. Corporate Governance: The International

Journal of Business in Society, 23(2), 397-421.

Ozili, P. K. (2022). Sustainability accounting. In Managing

Risk and Decision Making in Times of Economic

Distress, Part A (pp. 171-180). Emerald Publishing

Limited.

Pandey, V. K., & Kaur, H. (2014). Green accounting: a

sustainable growth path. Asian Journal of Research in

Social Sciences and Humanities, 4(12), 20-28.

Paul, J., Lim, W. M., O’Cass, A., Hao, A. W., & Bresciani,

S. (2021). Scientific procedures and rationales for

systematic literature reviews (SPAR‐4‐SLR).

International Journal of Consumer Studies, 45(4), O1-

O16.

Raman, R., Subramaniam, N., Nair, V. K., Shivdas, A.,

Achuthan, K., & Nedungadi, P. (2022). Women

entrepreneurship and sustainable development:

bibliometric analysis and emerging research trends.

Sustainability, 14(15), 9160.

Remya, S. & Rupini, T.S., (2023). A Study on Awareness

of Environmental Accounting and Reporting with

Special Reference to Employees of Thrissur District.

International Journal of Engineering Technology and

Management Sciences Website: ijetms.in Issue: 3

Volume No.7.

Rizki, N., Priyambodo, V. K., Sukma, P., & Aryawati, N.

P. A. (2023). Komparasi Praktik Green Accounting

Pada Perusahaan di Indonesia: Perspektif Perusahaan

Jasa Dan Perusahaan Dagang. Waisya: Jurnal Ekonomi

Hindu, 2(1), 12-26.

Sadiku, M. N., Ashaolu, T. J., Adekunte, S. S., & Musa, S.

M. (2021). Green accounting: A primer. International

journal of scientific advances, 2(1), 60-62.

Susmus, T., & Babacan, O. (2015). Research on The

Determination of The University Students'

environmental Accounting Perspective: The Case of

EGE University. Economic and Social Development

(Book of Proceedings), 5th Eastern European

Economic and Social Development, 21, 223.

Vanini, U., & Bochert, S. (2024). Integration of

sustainability issues into management accounting

textbooks. Journal of Accounting Education, 66,

100886.

Yahya, S., Jamil, S., & Farooq, M. (2021). The impact of

green organizational and human resource factors on

developing countries' small business firms’ tendency

toward green innovation: A natural resource‐based

view approach. Creativity and Innovation

Management, 30(4), 726-741.

Yelgen, E. (2022). Yeşil Muhasebe ve Uygulama Örnekleri

Üzerine Bir Çalışma. Yönetim Bilimleri Dergisi, (Özel

Sayı), 100-126.

Yoga, I. G. A. P., & Sastri, I. I. D. A. M. (2020). Green

Accounting: An Environmental Pollution Prevention

Effort to Support Business Continuity. Jurnal Ekonomi

& Bisnis JAGADITHA, 7(2), 128-137.

Żelazna, A., Bojar, M., & Bojar, E. (2020). Corporate

Social Responsibility towards the Environment in

Lublin Region, Poland: A comparative study of 2009

and 2019. Sustainability, 12(11), 4463.

Zrnić, A., Starčević, D. P., & Mijoč, I. (2020). Evaluating

environmental accounting and reporting: The case of

Croatian listed manufacturing companies. Pravni

vjesnik, 36(1), 47-63.

ICSBT 2024 - 21st International Conference on Smart Business Technologies

122