A Study on Multi-Arm Bandit Problem with UCB and Thompson

Sampling Algorithm

Haowen Yang

a

Department of Electrical and Computer Engineering, University of Florida, Gainesville, Florida, U.S.A.

Keywords: Reinforced Learning, Bandit Algorithm, Probability, Regret Analysis, Algorithm, Machine Learning,

Decision-Making, Applied Mathematics.

Abstract: Multi-Armed Bandit (MAB) problem is a sequential decision-making process with wide influence in many

fields across medical, and commercial application. In MAB problem, the initial reward distribution was

unknown, and observed during the process. In MAB application, Upper Confidence Bound algorithm and

Thompson Sampling algorithm are widely used for great performance. This work briefly review the basic

concept of MAB problem. Also, this work reviews the formulation of Upper Confidence Bound (UCB) and

Thompson Sampling (TS) algorithm. This work shows that UCB algorithm demonstrate a logarithmic

relationship. This work also review that TS is a Bayesian method solution of MAB problem. This work carried

out a brief test on the cumulative regret on UCB and Thompson sampling algorithm. The testing result shows

that TS algorithm was able to generate a lower cumulative regret compared to UCB algorithm under the same

scenario. The testing result also show that under a small probability difference and large number of arms TS

has similar performance compared to UCB algorithms.

1 INTRODUCTION

The Multi-Armed Bandit problem (MAB) is a

decision-making process with a series of constrained

actions. The MAB problem is a sequential process

where each action was taken and selected with the

result of that action being observed. The term bandit

derives from the slot machine as each time the arm on

the machine there could be a payoff or loss to the

investment to that event. In the MAB scenario, the

player is facing instead of one, but many arms, each

has individual reward distribution. The MAB aims to

seek the answer of the maximum reward from set of

arms (Bubeck & Cesa-Bianchi, 2012) (Mahajan &

Teneketzis, 2008).

MAB problem is presented with a limited dataset,

and even little prior knowledge of the data. The MAB

algorithm balances the exploration and exploitation

phase of the experiment to achieve two goals:

minimize the loss, maximize the gain (Lattimore &

Szepesv´ari, 2020).

MAB problem was applied in many different

commercial fields with great usability. For example,

website optimization is a great example of MAB

a

https://orcid.org/0009-0006-9076-8508

application. Website elements, such as picture, font,

layout, could be sequentially decided for the best

reward. The clickthrough or the number of deals and

revenues generated from the website serves as a great

benchmark to analyse the resulting reward from the

reward distribution.

Similarly, MAB problem is also practical in the

advertisement placement. Different advertising

suggestions to the customer exhibits different

performance in customer interactions indicator, such

as click rate, preference score, or purchase rate. There

has been previous work on gaining using A/B testing

in the study of customer behaviour and successfully

gain data from one of the largest e-commerce

companies in Japan (Yuta, Shunsuke, Megumi, &

Yusuke, 2021).

In the MAB problem, the learner was unaware of

the environment of the dataset. So, the true

distribution lies in the environment class. The

measurement of MAB problem performance is regret.

Regret is a measurement of the numerical difference

between the reward at round n, the sub-optimal arm,

and the overall maximum reward or the most optimal

reward over n rounds of playing (Lai & Robbins,

Yang, H.

A Study on Multi-Arm Bandit Problem with UCB and Thompson Sampling Algorithm.

DOI: 10.5220/0012938400004508

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st International Conference on Engineering Management, Information Technology and Intelligence (EMITI 2024), pages 375-379

ISBN: 978-989-758-713-9

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

375

1985). In the stochastic bandit, the 𝑋

is the reward

for round 𝑛. 𝑎 is in the set of the environment class

𝐴. 𝜇

is denoted as the reward for action 𝑎. So, the

regret formula is expressed as follows: (Lattimore &

Szepesv´ari, 2020)

𝑅

= 𝑛 max

∈

𝜇

− 𝐸𝑋

1

The first term expresses the maximum reward

under the certain environment class. The second term

expresses the reward observed after the action, also

known as the suboptimal reward. So, if the action was

the optimal reward, the regret should be zero.

Therefore, as discussed earlier that MAB balances

exploration and exploitation, the goal is always to

develop the algorithm to reduce the regret across the

exploration and exploitation phase to best utilize the

dataset available to us.

Another important factor to be noted in this paper

is that this work only discusses the setting of

stochastic bandits (also known as stationary bandits)

where the action is independent from each and will

not be affected by the previous action taken

throughout the process. So, the dataset remains

untouched during the operation.

2 UPPER CONFIDENCE BOUND

ALGORITHM

The upper confidence bound algorithm (UCB) was

first proposed in 1985 (Lai & Robbins, 1985). The

UCB algorithm chooses an upper confidence bound

of each arm and its reward distribution. Over a

sequential decision-making process, each arm was

played and generated a confidence interval. The

algorithm always picks the arm with the largest upper

confidence bound value across all the armed had been

played. However, there is a possibility for

overestimate the optimal arm, and therefore causes

inaccuracy. However, as more data was added to an

arm, there could be a scenario where the arm will

never be chosen since the confidence interval shrinks

and upper confidence bound falls under the assumed

optimal confidence upper bound (Lattimore &

Szepesv´ari, 2020).

The UCB1 is initialized by playing each arm one

to obtain the initial reward distribution. Then, at every

time step 𝑡, each arm 𝑖 was selected to gain the

maximum result:

𝜇̂+

2log

1

𝛿

𝑛

2

, where 𝜇̂ is the mean reward of the all the arms

played. 𝑢 are the rounds played so far. (Auer, Cesa-

Bianchi, & Fischer, 2002) The regret formulation was

analysed to be logarithmic order as

𝑂(log 𝑛) (Agrawal, 1995).

To average the overestimation, the previous work

therefore defines the upper confidence bound as the

following:

is define as the confidence interval of

the sample. (Lai & Robbins, 1985) 𝛿 is defined as the

error probability. Considering in the bandit problem

scenario, the term 𝑇

(

𝑡−1

)

is defined as the samples,

and the reward as 𝑈𝐶𝐵

(

𝑡−1, 𝛿

)

. 𝛿 is denote as the

error probability. Therefore, the UCB algorithm is

defined as follows:

Table 1: Upper Confidence Bound Algorithm.

input k and 𝛿

for t = 1 to n

choose action

𝐴

=argmax𝑈𝐶𝐵

(𝑡−1, 𝛿)

observe reward 𝑋

and update the upper

confidence bounds.

end for

where the UCB index is defined as

𝑈𝐶𝐵

(

𝑡−1, 𝛿

)

= 𝜇

̂

(

𝑡−1

)

+

2log

1

𝛿

𝑇

(

𝑡−1

)

(

3

)

3 THOMPSON SAMPLING

Thompson proposed one of the first method for bandit

problem in 1933. His method was later called

Thompson Sampling (TS). (Thompson, 1933) In a

general setting of Thompson Sampling, for a series of

action (𝑥

, 𝑥

, 𝑥

,….𝑥

) ∈𝑋 in an environment

class, one action is selected as 𝑥

for 𝑖

round action.

After each action, and reward 𝑦 is observed. With the

observation of reward, there generation a random

distribution based on the prior distribution of the set

𝑋 (Russo, Van Roy, Kazerouni, Osband, & Wen,

2018).

In a Bayesian scenario, for each round 𝑖, this work

chooses an arm 𝑎 in a set of all action and obtain a

reward 𝑟

. Each arm is related to the probability

density 𝑃(𝑟|𝑎) with an expected average reward

EMITI 2024 - International Conference on Engineering Management, Information Technology and Intelligence

376

𝜇

= 𝐸

(

𝑟

|

𝑎

)

𝑟|𝑎. In a Bayesian setting, the reality

distribution, denoted as 𝑃

(

𝑟

|

𝑎

)

is unknown.

Therefore, this work introduces a separate parameter

𝜃 to represent the present 𝑃(𝑟|𝑎) as per observed.

The reward distribution was updated after each action

and reward being observed. Therefore, the updated

distribution became the prior distribution for the next

action. And the real distribution was obtained after a

sequence of action and observation. So, the term

𝑃

(

𝜃

|

𝑎

𝑡

, 𝑟

)

is redefined as 𝑃

(𝜃) (Viappiani,

2013).

Here, this work presents a quick example to show

the process of Bayesian distribution being update

after an action was taken from the unknown

distribution of an environment class. Here is an

untransparent bag with two white balls (WW) and a

white ball and black ball (WB). Before any

observation was made, it is assumed that:

𝑃

(

𝑊𝑊

)

= 𝑃

(

𝑊𝐵

)

=

1

2

Such conclusions can only be made before any

observation. To update the prior distribution based on

the observations after one action so that the

distribution is closer to the real distribution of the

balls in the bag, when one black ball is picked

(𝑏𝑙𝑎𝑐𝑘) , the action obtains the following:

𝑃

(

𝑊𝑊

|

𝑏𝑙𝑎𝑐𝑘)=0 & 𝑃

(

𝑊𝐵

|

𝑏𝑙𝑎𝑐𝑘)=1

Therefore, the posterior distribution of the balls in the

bag is 0 1.

If one white ball was picked

(

𝑤ℎ𝑖𝑡𝑒

)

, the action

obtains the following:

𝑃

(

𝑊𝑊

|

𝑤ℎ𝑖𝑡𝑒)

= 𝑃

(

𝑤ℎ𝑖𝑡𝑒

|

𝑊𝑊)

∗

𝑃

(

𝑊𝑊

)

𝑃

(

𝑤ℎ𝑖𝑡𝑒

|

𝑊𝑊∗𝑃

(

𝑊𝑊

)

+ 𝑃

(

𝑤ℎ𝑖𝑡𝑒

|

𝑊𝐵) ∗𝑃(𝑊𝐵)

)

=

2

3

Therefore, the updated posterior distribution of

the balls in the bag is

.

In the context of Thompson Sampling, to perform

a Bayesian distribution calculation, it is introduced a

randomized generated number that represents each

arm. Therefore, setting an individual set of numbers

as a flag for each arm, the system is able to update the

posterior distribution based on the observation

(Lattimore & Szepesv´ari, 2020) (Scott, 2010) (Li,

& Olivier, 2011).

The Thompson Sampling Algorithm in the

Bayesian setting are defined as follows:

Table 2: Thompson Sampling Algorithm.

Input: Cumulative Density Function of the

mean rewards of arms

For 𝑡=1 to 𝑛

Random assign distribution 𝜃: 𝜃

(

𝑡

)

~𝐹

(𝑡) for

each arm 𝑖

Choose 𝐴

=argmax𝜃

(𝑡)

Observe 𝑋

and update:

𝐹

(

𝑡+1

)

= 𝑈𝑃𝐷𝐴𝑇𝐸 𝐹

(

𝑡

)(

4

)

End fo

r

4 PERFORMANCES OF

ALGORITHM

As described in the previous section, when choosing

a sub-optimal arm, a difference called regret was

generated. The MAB problem is balancing the

exploration and exploitation phase. The primary

objective of the MAB algorithm is to finalize the best

policy from exploration phase and apply the policy in

the exploitation phase. Therefore, cumulative regret

is the benchmark of the performance of the algorithm.

To accurately compare the UCB Algorithm and

Thompson Sampling, the following test was set up to

simulate the performance of two algorithms under the

same environment class.

There are four different settings of environment

class. This work is presenting the setting of 10 arms,

𝑘=10, and 100 arms, 𝑘= 100 to test the algorithm.

The best reward probability was set as 0.4 and reward

probability difference as 𝛿. For all arms except the

best arm, the reward probability is 0.4 −𝛿. The sub-

optimal arm is set 𝛿 as 0.1 and 0.01. The experiment

was set to be performed 100000 time.

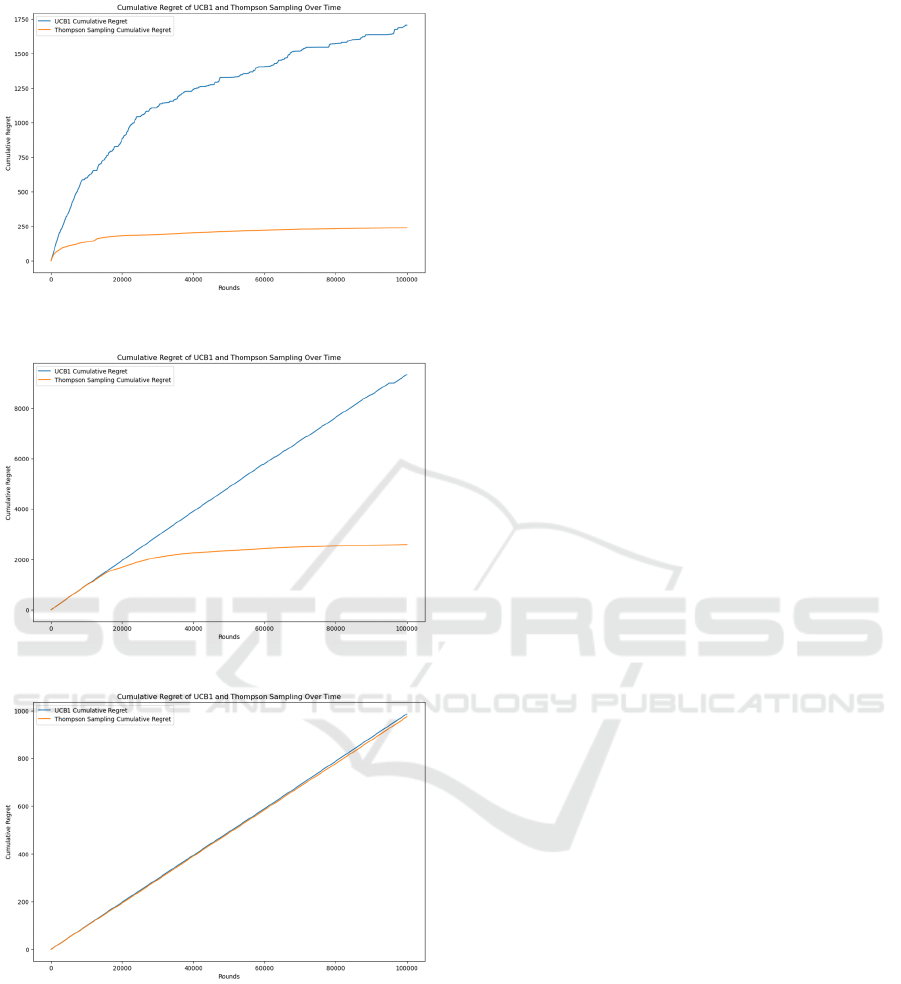

Figure 1: Test

Result

of 𝑘=10,𝛿=0.01.

A Study on Multi-Arm Bandit Problem with UCB and Thompson Sampling Algorithm

377

Figure 2: Test Result of 𝑘= 10, 𝛿=0.1.

Figure 3: Test Result of 𝑘= 100, 𝛿=0.1.

Figure 4: Test Result of 𝑘= 100, 𝛿=0.01.

Based on the testing result, under the following

setting: 𝑘= 100 𝛿=0.1, 𝑘=10 𝛿=0.01, and

𝑘=10 𝛿=0.01 , the Thompson Sampling is

showing an exceptionally better performance

compared to UCB algorithm. Under the UCB

Algorithm, Agrawal proved that regret displays

logarithmic scale. (Agrawal, 1995) Figure 2 shows

that regret is trending on a logarithmic scale. Also, it

is worth noting that, under 𝑘= 100, 𝛿=0.01

environment class setting, the Thompson Sampling is

demonstrating similar performance compared to

Upper Confidence Bound algorithm.

5 CONCLUSIONS

The Thompson Sampling is demonstrating an

exceptional performance compared to UCB

algorithm under all the setting except for 𝑘=

100, 𝛿=0.01. In the Thompson sampling, part of the

reason for a small regret deduction is due to the

posterior update. After each action, the posterior

distribution ensures that the distribution is closer to

the real distribution so that each action is induced

with less regret.

It is worth noting that although Thompson

Sampling generally displaying an exceptional, there

is an exception under the 𝑘= 100, 𝛿=0.01, where

both algorithms are demonstrating a very similar

performance in terms of cumulative regret. In fact,

Thompson Sampling demonstrated slightly worse

performance compared to UCB algorithm. It is worth

discussing in the future that under high number of

arms, and small reward probabilities difference, the

potential reason that led to the similar performance of

both algorithms.

REFERENCES

Agrawal, R. (1995). Sample mean based index policies by

o (log n) regret for the multi-armed bandit problem.

Advances in applied probability, 27(4), 1054-1078.

Auer, P., Cesa-Bianchi, N., & Fischer, P. (2002). Finite-

time analysis of the multiarmed bandit problem.

Machine learning, 47, 235-256.

Bubeck, S., & Cesa-Bianchi, N. (2012). Regret Analysis of

Stochastic and Nonstochastic Multi-armed Bandit

Problems. Foundations and Trends in Machine

Learning, 1-122.

Bubeck, S., & Cesa-Bianchi, N. (2012). Regret analysis of

stochastic and nonstochastic multi-armed bandit

problems. Foundations and Trends® in Machine

Learning, 5(1), 1-122.

Lattimore, T., & Szepesvári, C. (2020). Bandit algorithms.

Cambridge University Press.

Chapelle, O., & Li, L. (2011). An empirical evaluation of

thompson sampling. Advances in neural information

processing systems, 24.

Mahajan, A., & Teneketzis, D. (2008). Multi-armed bandit

problems. In Foundations and applications of sensor

management (pp. 121-151). Boston, MA: Springer US.

Russo, D. J., Van Roy, B., Kazerouni, A., Osband, I., &

Wen, Z. (2018). A tutorial on thompson sampling.

EMITI 2024 - International Conference on Engineering Management, Information Technology and Intelligence

378

Foundations and Trends® in Machine Learning, 11(1),

1-96.

Scott, S. L. (2010). A modern Bayesian look at the multi‐

armed bandit. Applied Stochastic Models in Business

and Industry, 26(6), 639-658.

Slivkins, A. (2019). Introduction to multi-armed bandits.

Foundations and Trends® in Machine Learning, 12(1-

2), 1-286.

Thompson, W. R. (1933). On the likelihood that one

unknown probability exceeds another in view of the

evidence of two samples. Biometrika, 25(3-4), 285-294.

Viappiani, P. (2013). Thompson sampling for Bayesian

bandits with resets. In Algorithmic Decision Theory:

Third International Conference, ADT 2013, Bruxelles,

Belgium, November 12-14, 2013, Proceedings 3 (pp.

399-410). Springer Berlin Heidelberg.

A Study on Multi-Arm Bandit Problem with UCB and Thompson Sampling Algorithm

379