Research and Parameter Setting Recommendations for the UCB

Algorithm Based on Advertisement Deployment on the Amazon

Website

Yuankun Zhou

a

SWJTU-Leeds Joint School, Southwest Jiaotong University, Xian Road, Pidu, Chengdu, China

Keywords: Multi-Armed Bandits, Upper Confidence Bound (UCB) Algorithms, Exploration and Exploitation Trade-Off,

Machine Learning Applications.

Abstract: The multi-armed bandit problem, a cornerstone of decision-making theory, primarily addresses the critical

balance between exploration and exploitation to optimize choices. This problem is intrinsically linked with

numerous real-world applications, spanning diverse sectors from business to healthcare. It has inspired a

variety of algorithms, among which the Upper Confidence Bound (UCB) algorithm stands out. The UCB

algorithm, noted for its approach of setting an upper confidence interval for each option as a decision criterion,

has captured the attention of many scholars. This paper contextualizes its discussion within the framework of

advertisement deployment for products on Amazon, employing various algorithms to simulate ad campaigns

and analyze their effectiveness. It summarizes the unique characteristics and appropriate contexts for each

algorithm and explores enhancements through structural and parameter adjustments. Based on extensive

experimental data, the study offers recommendations for algorithm parameter settings in various scenarios,

aimed at maximizing the practical application and effectiveness of these algorithms in real-world settings.

This research not only enhances understanding of algorithmic adaptations but also provides valuable insights

for their application across different operational environments.

1 INTRODUCTION

The multi-bandit algorithm is a classical algorithm.

The concept of bandit problem was first proposed by

William R. Thompson in 1933 (Lattimore and

Szepesv ́ari, 2020), and its original purpose is to find

the better solution between two problems. At the

beginning, the number of arms considered in the

bandit problem was only two, that is, each decision

was a simple choice between two arms. The whole

problem was mostly theoretical reasoning within the

scope of mathematics, and no computer algorithm

had been introduced to deal with it h it(THOMPSON,

1933).

The bandit problem has attracted the attention of

many scholars. As the problem continues to develop,

computer algorithms have been introduced into the

problem. Computers have used relevant algorithms to

greatly improve people's ability to deal with the

bandit problem. There are also more and more

a

https://orcid.org/0009-0001-3850-3426

variables brought by environmental factors. With the

introduction of deep learning, the mulit-bandit

algorithm has become more complex and powerful.

As the multi-armed bandit problem evolved, the

sophistication of the algorithms used to address it also

increased significantly. The core objective remained:

to optimize the selection of arms to maximize

rewards. However, the inclusion of multiple arms

introduced greater complexity, requiring algorithms

to efficiently learn and adapt based on the outcomes

of previous selections.

This issue has given rise to numerous algorithms,

along with their variations and extensions, such as the

epsilon-decreasing strategy or contextual bandits,

where additional information about each arm's

context is used to make decisions, represent the

continuous advancement in the field of bandit

algorithms. These methods have proved vital in

numerous applications, from online advertising and

web page optimization to clinical trial design and

financial portfolio selection, showcasing the

Zhou, Y.

Research and Parameter Setting Recommendations for the UCB Algorithm Based on Advertisement Deployment on the Amazon Website.

DOI: 10.5220/0012968400004508

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st International Conference on Engineering Management, Information Technology and Intelligence (EMITI 2024), pages 685-691

ISBN: 978-989-758-713-9

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

685

versatility and power of multi-bandit algorithms in

dealing with complex, uncertain environments.

The applications of multi-armed bandit

algorithms are extensive and impactful across various

domains. In advertising, these algorithms optimize ad

placements by continuously adjusting to user

responses, thereby maximizing click-through rates

and overall campaign effectiveness. This dynamic

approach reduces wastage of ad spend and improves

the relevance of ads shown to users.

Today, advertising permeates every aspect of

people's lives, and for any product, the best way to

gain visibility is through advertising. Advertising

significantly boosts production and consumption by

ensuring that the right products reach the right people.

It generates billions in revenue; according to Statista,

global advertising expenditure is projected to reach

$1.089 trillion in 2024(https://www.statista.com,

2024). This represents a vast market, and enhancing

the quality and precision of advertising campaigns

can yield substantial benefits. Employing superior

algorithms for advertising promotions is undoubtedly

a strategy that can lead to significant economic

advantages.

In the field of applications, numerous scholars

have engaged in practical implementations in this

direction. X. Zhang and colleagues have employed

multi-armed bandit algorithms in a broader context of

generalized item recommendations, striving to make

optimal decisions(). Meanwhile, W. Chen and

associates have utilized the combinatorial Multi-

Armed Bandit (CMAB) framework specifically for

targeted advertising recommendations, addressing

real-world challenges. This paper specially targets the

advertisement deployment on the Amazon shopping

website, utilizing Amazon product data to enable

algorithms to simulate advertising campaigns. By

analyzing the performance of each algorithm based

on data-driven simulations, the study identifies

distinctive features and optimizes parameter settings

for each method. It also provides empirical

recommendations for parameter adjustments tailored

to different scenarios, aiming to maximize

algorithmic performance. This approach not only

enhances the efficiency of advertisement placements

but also contributes to a deeper understanding of how

adaptive algorithms can be fine-tuned for specific

marketing challenges.

2 ALGORITHM MODEL

The Upper Confidence Bound (UCB) algorithm

embodies the optimism principle in uncertain

situations. It assumes that the best possible outcome

is likely and exploits current knowledge to minimize

long-term regret. By optimistically estimating

potential rewards from actions, the UCB algorithm

balances exploring new options and exploiting known

ones, effectively guiding decision-making processes

toward the most rewarding outcomes. This strategy is

crucial for problems like online ad placement and

clinical trials, where decisions must adapt to evolving

data.

In the UCB algorithm, after each decision-making

iteration, the algorithm assigns an Upper Confidence

Bound (UCB) to each arm based on the results

obtained. In the subsequent round, the arm with the

highest UCB is selected, which is anticipated to yield

the greatest return. This cycle is continuously

repeated to ensure that each decision represents the

theoretically optimal choice. While specific

procedures and the calculation method of the UCB

may vary among different UCB algorithms, the

underlying philosophy remains consistent.

For each round 𝑡=1,2,3,…,𝑛, the algorithm

must select an arm 𝐴

from the set

1,2,3,...,𝑖

Upon

making a decision, a random reward 𝑋

is received.

The reward probabilities for each arm are

independent. The cumulative reward for an arm is

defined as 𝐸𝑖 = ∑

𝑋

.The average expected return

for each arm is given by µ𝑖=

∑

, where𝑇

is the

number of times arm 𝑖 has been selected up to round

𝑡. The regret is defined as smaxi(µi) · T −∑T t =

1X , which quantifies the difference between the

cumulative reward of always choosing the optimal

arm and the cumulative reward actually accrued.

2.1 Algorithms Used in the Study

Lattimore presents a classical UCB algorithm and its

derived improved algorithm Asymptotic Optimality

UCB in his paper. For the classical UCB algorithm,

the UCB of each arm can be derived from P:

𝑃μ≥μ+

(

/

)

≤δ for all δ∈

(

0,1

)

(1)

Here, the reward probability of Lattimore's

default arm is consistent with 1-subgaussian random

variables.

The Asymptotic Optimality UCB. Distinct from

the classical UCB, its principal feature is the

elimination of the need to specify the horizon n,

which is the total number of algorithmic explorations.

This is greatly beneficial in practical applications

where the optimal number of explorations is often

unknown. The Asymptotic Optimality UCB

EMITI 2024 - International Conference on Engineering Management, Information Technology and Intelligence

686

effectively addresses this issue by adjusting the UCB

of each arm based on the number of explorations

already conducted, thus making the algorithm

independent of the total number of rounds. The UCB

for each arm is calculated using the following

formular:

𝐴

=maxμ

(

𝑡−1

)

+

(

)

(

)

(2)

Where 𝑓(𝑡) = 1 + 𝑡 \𝑙𝑜𝑔^2(𝑡) (3)

Jamieson et al. present an alternative Upper

Confidence Bound (UCB) algorithm in their paper,

which adheres to the logic of the classical UCB

framework but incorporates additional parameters.

This augmentation allows for a more flexible

adjustment of the algorithm, enabling it to adapt to a

wider and more complex array of environments

(Jamieson et al., 2014). The computation of the UCB

is as follows

𝑃= μ

+

(

1+β

)

1+

√

ε

(

)

(

)

(

)

(

)

(4)

Where , , and are employed to adjust the algorithm

to suit various environments. The term represents the

standard deviation of the Gaussian distribution, with

the variance being specified as , where and denote

the distribution's range limits.

Garivier and Cappé introduced a novel

computation method for the Upper Confidence

Bound in their paper, incorporating the concept of

Bernoulli Kullback-Leibler (KL) divergence:

𝐷

KL

(

𝑃∥𝑄

)

= 𝑝log

+

(

1 −𝑝

)

log

(5)

KL divergence is typically employed to quantify

the difference between two probability distributions,

p and q. Garivier and Cappé utilized this measure to

supplant the standard calculation in UCB algorithms.

They determine the greatest divergence P that

satisfies the inequality when each arm's value is

below a certain threshold, thus designating P as the

UCB for each arm(Garivier and Capp´e, 2011).

For each arm, the UCB is given by:

𝑃

= 𝑀𝑎𝑥𝑇

(

𝑡

)

∗𝐷

KL

μ

, 𝑇

(

𝑡

)

≤log

(

𝑡

)

+ 𝑐log

(

log

(

𝑡

))

(6)

It should be noted that, in contrast to other UCB

algorithms, the KL-UCB algorithm stipulates that the

reward for each arm must lie within the range [0,1].

This necessitates the transformation of rewards

greater than 1 into winning probabilities prior to

computation.

In the aforementioned algorithm, it is evident that

the computation of the UCB for each arm is relatively

complex, signifying that the algorithm demands

greater computational resources and time. This aspect

becomes apparent during the implementation phase,

where the KL-UCB algorithm requires more time to

process an equivalent number of calculations.

3 AMAZON SHOPPING

RECOMMENDATIONS

3.1 Experimental Background

The experiment constructs a scenario that simulates

the advertisement deployment for products on the

Amazon shopping website. In practical applications,

decisions regarding what to promote and to whom are

crucial, and the data sources are diverse,

encompassing aspects such as product sales, user

reviews, view counts, and prices. From the user's

perspective, demographic factors like gender and age

are considered. Moreover, complex composite data,

such as the purchasing rates of different genders for

various products or the acceptance of differing price

ranges by various age groups, are also integral. These

considerations are critical for designers of advertising

push algorithms.

This paper simplifies the environment by focusing

solely on the impact of product reviews on

advertisement efficacy, treating successful product

sales as a successful advertisement push. It explores

the performance of different algorithms and considers

how adjustments in parameters and structures can

optimize these algorithms. Importantly, while the

simulated environment is singular and defined, real-

world applications are complex and multifaceted.

Based on the experimental results, this study provides

recommendations for algorithmic parameter settings

in other environments to enhance performance under

unknown conditions, thereby ensuring the practical

applicability of the algorithms.

3.2 Experimental Setting

The study employed a dataset from the Amazon

shopping platform that encompasses an array of

products, user ratings on a scale from 0.5 to 5, and

sales figures. The intent was to discern the product

ratings that correlate with the highest purchase

likelihood and to tailor product recommendations

accordingly. The task assigned to the algorithm was

to emulate advertising campaigns based on varying

Research and Parameter Setting Recommendations for the UCB Algorithm Based on Advertisement Deployment on the Amazon Website

687

ratings. The success of an advertisement push was

quantified by actual product purchases recorded in the

database, which, in turn, provided a reward signal to

the algorithm. The overarching aim of the algorithm

was to optimize its selection strategy to favor

products with the highest purchase rates at specific

rating levels, thus mitigating the accumulation of

regret—a measure of the opportunity loss when not

choosing the optimal action.

This simulation reflects the quintessential

dilemmas in real-world advertising optimization

faced by digital platforms: which products to promote

and how to effectively allocate promotional efforts.

Through this research, the authors sought not only to

benchmark the performance of diverse algorithms but

also to enhance their algorithms to maximize the

return on advertising investment. This enhancement

is critical, as it could lead to improved customer

engagement, targeted marketing efficiency, and,

ultimately, increased sales revenue.

3.3 Simulated Result

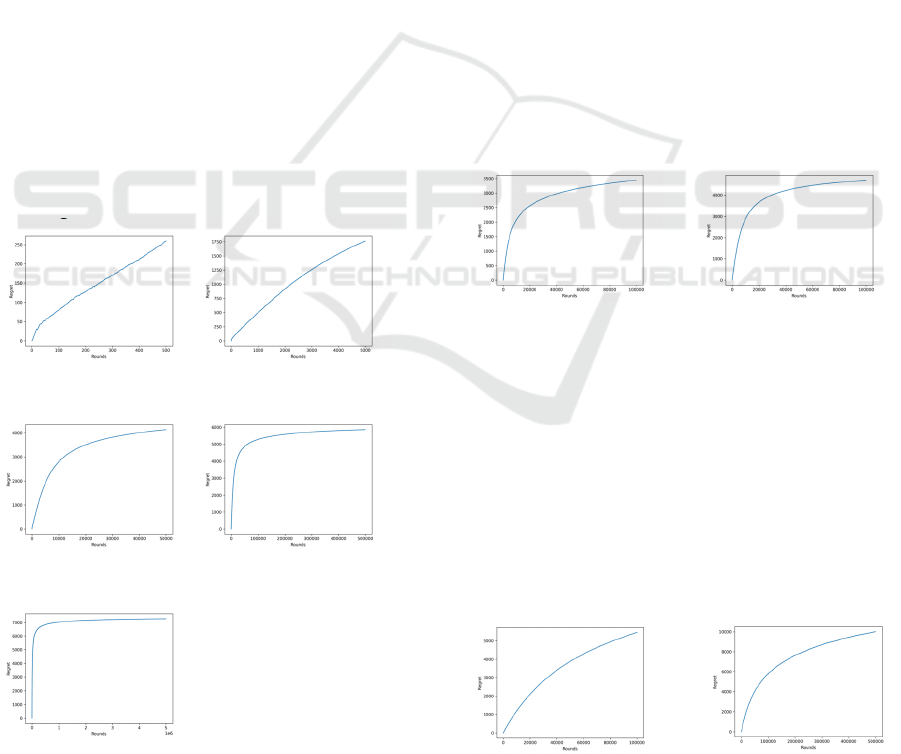

For the classical UCB algorithm, simulations were

conducted with the horizon n set at 500, 5,000,

50,000, 500,000, and 5,000,000, respectively. The

outcomes of these simulations are depicted in Figures

1 through 5.

Figure 1: n=500. Figure 2: n=5,000.

Figure 3 n=50,000. Figure 4: n=500,000.

Figure 5: n=5,000,000.

From Figures 1 to 5, it is evident that as the number

of explorations increases, the accumulation of

algorithmic regret also increases, though not in a

strictly linear manner. From Figure 1 with n=500 to

Figure 5 with n=5,000,000, the number of

explorations has increased by a factor of 10,000, yet

the accumulation of regret has only increased by

approximately 50 times. This observation suggests

that while regret does escalate with more

explorations, its rate of increase diminishes as the

number of explorations grows, indicating a sub-linear

relationship between exploration quantity and regret

accumulation. With the increase in the number of

explorations, the variation in the Regret of the UCB

algorithm exhibits a logarithmic form, which is

consistent with its theoretical Regret behavior.

For the Asymptotic Optimality UCB algorithm,

the number of explorations, n, is set to 100,000 and

contrasted its results with the classical UCB

algorithm addressed in the previous query. It is

important to clarify that this specification of n as

100,000 does not represent a parameter passed to the

Asymptotic Optimality UCB algorithm but merely

sets a stopping point for the exploratory process

within the program. If desired, the Asymptotic

Optimality UCB algorithm is fully capable of

continuing its exploration beyond this limit.

Figure 6: Asymptotic Figure 7: Classical UCB.

Optimality UCB.

The results reveal that the Asymptotic Optimality

UCB algorithm accumulates less Regret and does not

require pre-specification of the number of

explorations. This characteristic bears significant

implications for practical applications.

For the Lil'UCB algorithm, the number of

experimental runs was set to 100,000 and 500,000,

respectively. Following the recommendations of

Jamieson et al., is set to 0.01, was set to 1,and

within the open interval (0, 1).

Figure 8: n=100,000. Figure 9: n=500,000.

EMITI 2024 - International Conference on Engineering Management, Information Technology and Intelligence

688

The experimental outcomes indicate that the

performance of the algorithm was suboptimal. This

subpar performance is attributed not to inherent

deficiencies in the algorithm itself but to a parameter

configuration ill-suited to the experimental context.

Subsequent sections will discuss enhancements to the

algorithm, including modifications to the coefficient

settings and recommendations for other operational

environments.

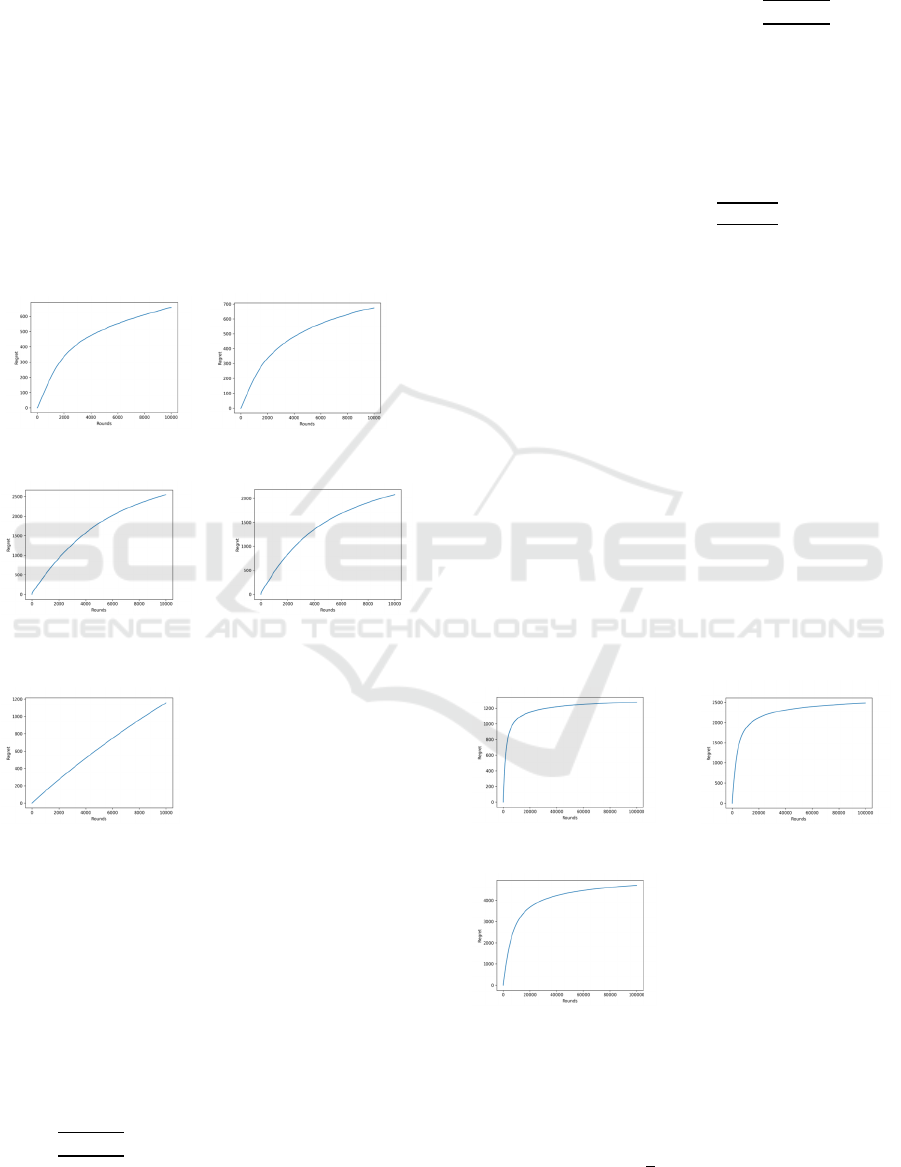

In the case of KL-UCB, two distinct methods

were employed for calculating the UCB of each arm:

linear root-finding and bisection root-finding. The

number of explorations, n, was set at 10,000, and the

results were compared with three other algorithms,

yielding the following outcomes:

Figure 10: KL-UCB:Linear. Figure 11: KL-UCB:bisection.

Figure 12: Classical UCB. Figure 13: Asymptotic

Optimality UCB.

Figure: 14: Lil'UCB.

The results indicate that KL-UCB outperforms the

others, attributable to its parameter configuration and

algorithmic framework being more conducive to

environments with fewer exploration instances,

specifically at lower values of n. This will be

elaborated upon in the subsequent sections.

3.4 Improvement

In the preceding experiments, the UCB algorithm's

computation of the UCB for each arm was denoted as

μ

+

(

/

)

, under the condition that δ must be

significantly smaller than 1/𝑛, concretely set as δ=

1/𝑛

during experimentation. It is manifest from the

formula that the exploration extent of different arms

by the algorithm is determined by

(

/

)

, which

constitutes the crux of the entire algorithm.

Consequently, one can modulate the overall

exploratory behaviour of the algorithm to adapt to

varying environments by introducing a coefficient

within the radical .The revised computation for UCB

is as follows:

𝑃

= 𝜇

+

(

/

)

(7)

Subsequent empirical observations revealed a

direct proportionality between the exploration of

suboptimal choices by the algorithm and the

coefficient 𝑐; Larger 𝑐 values resulted in more

extensive exploration of suboptimal options. This

strategy enables the algorithm to more effectively

mitigate the selection of erroneous options due to

low-probability events. However, this may also

precipitate a wasteful expenditure of resources, as the

algorithm could allocate an excessive number of

explorations to suboptimal options, culminating in an

augmented accumulation of loss or, in algorithmic

vernacular, a heightened aggregation of Regret.

Therefore, striking an optimal balance in exploration

levels is paramount to enhancing algorithmic

efficacy. The algorithm's performance for c =1, 2, and

4, set against the backdrop of the antecedent Amazon

product dataset, is delineated below.

Figure 15: c = 1. Figure 16: c = 2.

Figure 17: c = 4.

The outcomes indicate that a larger coefficient c

correlates with an increased accrual of regret from

1200 (Fig.15) to more than 4000 (Fig.17). Drawing

upon additional experimental data, it is advised to set

the coefficient c to

(

max

(

μ

)

−min

(

μ

))

. Here,

Research and Parameter Setting Recommendations for the UCB Algorithm Based on Advertisement Deployment on the Amazon Website

689

max

(

μ

)

symbolizes the winning probability of the

optimal choice, and min

(

μ

)

that of the least

favorable choice. The rationale is that the degree of

exploration by the algorithm should be contingent on

the interval between the best and worst options; the

narrower the interval, the more indistinguishable the

options, and thus, the more challenging it is to discern

the optimal choice, necessitating a more extensive

exploration. Notably, both max

(

𝜇

)

and min

(

𝜇

)

are

based on pre-experimental empirical estimations,

rendering the algorithm's performance highly

dependent on these preliminary assessments. The

recommendations presented here serve as a heuristic,

and parameter tuning may require further specificity

to adapt to alternative scenarios.

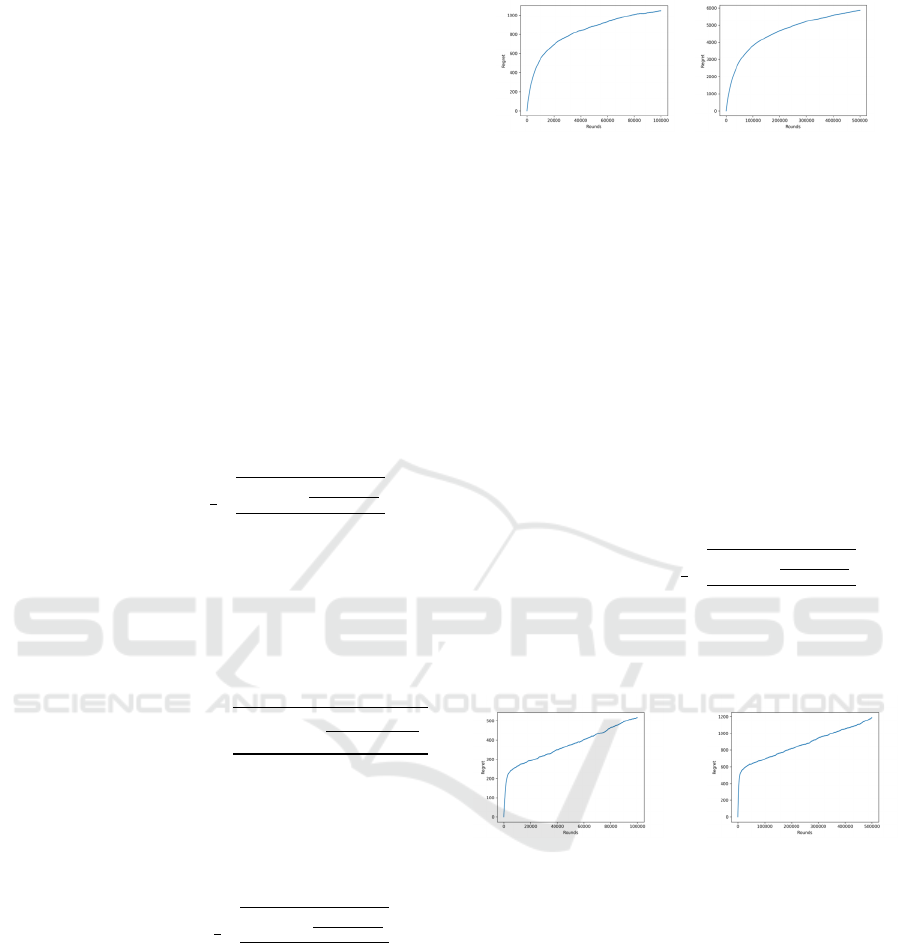

The empirical data from previous Lil'UCB

experiments reveal that, for different values of n, the

algorithm's accumulation of regret follows a trend

resembling a linear increase. This suggests that the

algorithm's control mechanism, represented by

𝑃= μ

+

(

1+β

)

1+

√

ε

(

)

(

)

(

)

(

)

(8)

It does not effectively facilitate an increased

frequency in selecting the optimal option over time.

This issue is primarily due to the parameter settings.

In terms of the algorithm's objectives, as the selection

count for an option increases, its average winning rate

should become more certain and its UCB should

decrease accordingly. Therefore, an enhancement can

be introduced into the

(

)

(

)

(

)

(

)

component by incorporating a variable c, which

impacts 𝑇_𝑖 to 'amplify' the effect of 𝑇_𝑖 , leading to

a decrease in the overall UCB value as the selection

count for an option increases. The revised formula for

UCB is now denoted as:

𝑃= μ

+

(

1+β

)

1+

√

ε

(

)

(

)

(

)

∗

(

)

(9)

Furthermore, the selection of 𝑐 must also consider

the total number of explorations 𝑛 . Based on

extensive experimentation, it is advised to set to a

relatively universal value of 𝑐, aiming for enhanced

performance. The experimental results are as follows,

for n =100,000 and n = 500,000:

Figure 18: n=100,000. Figure 19: n=500,000.

As can be observed, the algorithm, after the

enhancements, has reduced the regret to one-tenth of

its initial magnitude, significantly boosting

performance and decreasing inefficiencies. The

relatively universal parameter 10

/𝑛 has already

shown commendable performance; however, the

parameters can still be specifically tailored to better

suit the environment of Amazon product

advertisement campaigns. By evolving the simple

addition of the parameter 𝑐 to 𝑐𝑇

and specifically

set value, significant improvements in algorithmic

performance are achieved. This modification allows

the algorithm to identify the optimal option more

rapidly, thus minimizing wastage. Below is the

description of the revised algorithm:

𝑃= μ

+

(

1+β

)

1+

√

ε

(

)

(

)

(

)

∗

(

)

(10)

Where c = 10

/𝑛 . The performance of the

algorithm after the specificity-enhanced

improvements is as follows:

Figure 20: n=100,000. Figure 21: n=500,000.

It is evident that the performance of the algorithm

has significantly improved, achieving the optimal

choice with a minimal number of explorations. The

data corroborate this, showing that the accumulation

of regret is exceptionally low. It is important to note

that this performance is due to parameters specifically

tailored to a particular environment, and such

performance may not be replicable in different

settings. Particularly in scenarios where there is

minimal variance among options, this parameter

setting does not sufficiently explore suboptimal

choices, which could lead to erroneous decisions by

the algorithm. For other scenarios, a more general

parameter setting of is deemed safer.

EMITI 2024 - International Conference on Engineering Management, Information Technology and Intelligence

690

The form should be completed and signed by one

author on behalf of all the other authors.

4 CONCLUSIONS

The experimental results illustrate that different

algorithms excel in specific environments. The

Asymptotic Optimality UCB, with its advantage of

not requiring a preset number of explorations, is

particularly suitable for exploring unknown

environments in practical applications. The Lil'UCB,

with its array of adjustable parameters, allows for

tailored settings to enhance adaptability across

diverse environments. The KL-UCB, despite its

computational complexity, demonstrates superior

performance with a limited number of explorations

and exhibits robustness against environmental

variations, suggesting that it can perform well across

a range of scenarios without the need for specific

adjustments.

In addition to the UCB variants discussed in detail

above, numerous other derivatives have been

proposed, such as the UCB-g (greediness) algorithm

by Z. Wang et al(Wang et al., 2018)., the k-Nearest

Neighbour UCB algorithm by H. Reeve et al(Reeve

et al., 2018)., and the Restless-UCB by S. Wang

et al(Wang et al., 2020). Each algorithm brings

unique advantages, but a pivotal issue in practical

applications is how to select the appropriate algorithm

and set parameters effectively, often proving more

crucial than the study of the algorithm itself.

The experimental outcomes discussed underscore

that the efficacy of an application is not solely

dependent on the algorithm itself, but significantly on

the selection and calibration of the algorithm. This

paper provides recommendations for choosing

algorithms and setting parameters tailored to specific

scenarios, offering guidance for practical

implementations

REFERENCES

Chen, W., Wang, Y., and Yuan, Y. (2013). Combinatorial

multi-armed bandit: General framework and applica-

tions. In International conference on machine learning,

pages 151–159. PMLR.

Garivier, A. and Capp´e, O. (2011). The kl-ucb algorithm

for bounded stochastic bandits and beyond. In

Proceedings of the 24th annual conference on learning

theory, pages 359–376. JMLR Workshop and

Conference Proceedings.

Jamieson, K., Malloy, M., Nowak, R., and Bubeck, S.

(2014). lil’ucb: An optimal exploration algorithm for

multi-armed bandits. In Conference on Learning

Theory, pages 423–439. PMLR.

Lattimore, T. and Szepesv´ari, C. (2020). Bandit

algorithms.Cambridge University Press.

Reeve, H., Mellor, J., and Brown, G. (2018). The k-nearest

neighbour ucb algorithm for multi-armed bandits with

covariates. In Algorithmic Learning Theory, pages

725–752. PMLR.

Thompson, W. R. (1933). On The Likelhood That One

Unknown Probability Exceeds Another In view of the

Evidence of Two Samples. Biometrika, 25(3-4):285–

294.

Wang, S., Huang, L., and Lui, J. (2020). Restless-ucb,

anefficient and low-complexity algorithm for online

restless bandits. Advances in Neural Information

Processing Systems, 33:11878–11889.

Wang, Z., Zhou, R., and Shen, C. (2018). Regional multi-

armed bandits. In International Conference on Artificial

Intelligence and Statistics, pages 510–518.PMLR.

Zhang, X., Xie, H., Li, H., and CS Lui, J. (2020). Con-

versational contextual bandit: Algorithm and

application. In Proceedings of the web conf. 2020,

pages 662–672.

Statista. 2024. Advertising – Worldwide. [Online].

[Accessed 17 April 2024]. Available from: https://

www.statista.com/outlook/amo/advertising/worldwide

#ad-spending

Research and Parameter Setting Recommendations for the UCB Algorithm Based on Advertisement Deployment on the Amazon Website

691